A CASE STUDY OF THE PROSPECTS ON SOLAR INDUSTRY PLAYERS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Ming-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

A CASE STUDY OF THE PROSPECTS ON SOLAR INDUSTRY PLAYERS

Ming-Lang Wang1, *, Kang-Wei Wang2

marlon@g.chu.edu.tw1,*, w6211082000@yahoo.com.tw2

1

Department of Industrial Management, Chung Hua University, Associate Professor

30012, No.707, Sec.2, Wu-Fu Rd., Hsinchu City, Taiwan, R.O.C.

2

Medical Affairs Bureau Ministry of National Defense, Director, Comptroller Office

10462, No.409, Bei-An Rd., Taipei City 104, Republic of China (Taiwan)

*Corresponding author , marlon@g.chu.edu.tw

Abstract

Due to the rapid economic development, Taiwan’s demand for energy is increasing urgently. Nowadays, fossil fuels are still

the primary source of energy. However, carbon dioxide emissions cause the greenhouse effect and abnormal climate change.

To reduce carbon dioxide emissions, the Kyoto Protocol and the Copenhagen Accord have become the international norms.

"Renewable Energy" has become the focus of global energy development. The solar energy industry in Taiwan has been

developed for more than 20 years. The industry has developed from the past "amorphous silicon" research and manufacturing

to today's "crystalline silicon solar cells" mass production. This study expects that by discussing the development strategy of

the solar energy industry. In the current competitive environment, we will select an appropriate development strategy and

take the Taiwanese solar energy industry structure as the main elements of analysis. Based on the operating experience of key

solar companies in Taiwan and the formulation of government policies, the study finds that the driving factors affecting the

introduction of the solar industry are government promotion and intervention constructs, functional constructs, technical

constructs, efficiency constructs, and risk constructs. Besides, from the above findings, the following suggestions are made: 1.

The government must formulate accurate subsidies and incentives, 2. The government and industry strategic alliance, 3.

Improve the photoelectric conversion rate and establish technology Patents, 4. Develop the most appropriate development

strategy to avoid marginalization.

Keywords: Solar Industry; Development Strategy; Driving Factors; Industrial Potential

1.Background

In the face of the global energy crisis, the solar energy industry is becoming increasingly important.

In order for this industry to play the role of sustainable energy in Taiwan, the government and the

private sector promote relevant measures to raise the development of the solar energy industry. Taiwan

is located in the subtropical region, and the long sunshine time is very suitable for the development of

solar energy. Although the sunshine conditions are good, the land conditions in Taiwan where solar

energy equipment can be installed are insufficient. According to the statistics of the Department of

interior, Taiwan's per capita land area is 1532 square meters, Population density is second only to

Bangladesh, ranking second in the world (Xi-Min Lu, 2016). Under such conditions, the land area in

Taiwan where solar energy facilities can be installed is greatly restricted. Non-nuclear homes are the

primary energy policy of the Taiwanese government. It is expected that the renewable energy power

generation ratio will reach 20% by 2025. The development of solar energy has become a major

government policy. (Minutes of the "29th Committee Meeting of the National Council for Sustainable

Development of the Executive Yuan", 2016).

IJER – May - June 2020 89

available online @ www.ijeronline.com

Ming-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

The Executive Yuan announced the "Sustainable Energy Policy Convention" in 2008. At the clean

level, the country ’s carbon dioxide emissions will be reduced and will return to 2005 emissions in 2020.

The low-carbon energy in the power generation system will increase from 40% to more than 55%. (A

Study of Sustainable Energy Policy Convention, 2008). In 2000, Motech Industries Inc., Taiwan's first

solar industry manufacturer, was established. The company's solar cell conversion rate reached 13% in

the next year. In 2007, it was the first in Taiwan to pass the ISO14001 environmental management

systems and Occupational Health and Safety Assessment Series 18001 certification, becoming the

world's sixth largest solar electronics manufacturer and the leader of Taiwan's solar industry. Among

them are E-Ton Solar Tech.、Sino-American、Giga Solar、NSP Corp.、GINTECH and other related solar

listed and OTC companies.

Sino-American, Giga Solar, NSP Corp., and GINTECH have invested in stable and profitable

investments in power plants at home and abroad. In recent years, NSP Corp. has covered the United

States, Britain, and Japan, and has entered the European Union, Central Asia, Southeast Asia, Africa,

and Central and South America. After the power plant completes the merger and acquisition, part of the

power will be resold. To sell 70% to keep 30% of the business model. Although the long-term operating

investment rate of return of the power plant is less than 10%, it is very suitable for long-term stable

enterprise investment (Yong-Xiang Jian, 2016). Taiwan's solar output value reached a new high of NT$

2015 billion in 2010, but in 2011, due to the low price competition in China and the European debt crisis,

market demand has shrunk significantly, and the output value has dropped to NT$ 170.8 billion. In 2012,

it fell sharply to NT$ 93 billion. In 2014, the output value returned to NT$ 114.7 billion. Although it was

hit by the US anti-dumping and countervailing investigations in 2015, the output value still reached NT$

156.1 billion (Department of Statics, Economic of Affairs, 2015).

After years of development, Taiwan’s solar energy industry has become a core competitive

advantage of the industry with high efficiency, low cost, and flexibility. Integrate the cooperation of

upstream, midstream and downstream companies for R & D. Through international cooperation, develop

forward-looking key technologies and niche products to assist industrial technology upgrades. At the

same time, use overseas marketing strategies and operating methods to expand overseas markets.

Taiwan has unlimited potential to develop solar energy, and has excellent technology research and

development and manufacturing capabilities, but it lacks long-term planning, relevant regulatory

integration, and insufficient domestic demand market. It is necessary to create the highest benefits under

limited resources through industry-government-academic cooperation (Cheng-Cong Guo, 2015).

The core values of Taiwan's development of the solar energy industry are discussed from the

"economic energy perspective", "innovative technology perspective", and "environmental sustainability

perspective". The purpose of this study is: 1. To explore the driving factors driving the development of

the solar energy industry. 2. Analyze the development trend and industrial potential of Taiwan's solar

IJER – May - June 2020 90

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

energy industry. 3. Whether Taiwan is competitive in the development of the solar energy industry.

4. Provide reference for government to formulate relevant policies and counseling and subsidy

measures for enterprises.

2.Literature Review

2.1 Definition of Solar Energy

The types of solar energy can be divided into thermal energy and light energy. In the thermal

energy part, they can be divided into solar water heaters and solar thermal power generation. It can also

be called solar cell in the light energy part, and can be divided into silicon semiconductor and thin film.

Silicon semiconductors can be divided into a-Silicon wafer, Poly-Silicon silicon wafers, and a-Si thin

films; thin films can be divided into compound semiconductors and new technologies and new materials.

What are new technologies and new materials? For example, organic silicon dye-sensitized solar cell

(DSSC, DSC or DYSC), polymer, or nanotechnology, spherical silicon (Zhao-Wei Zheng, 2011).

2.2 Utilization, advantages and disadvantages of solar energy

There are three main methods for directly using solar radiation energy: the first method is

photothermic conversion; the second method is photoelectric conversion; the third method is

photochemical conversion. Photothermic conversion, which is a commonly used method at present, is

widely used in cooking, drying cereals, supplying hot water, heating indoors, air conditioning, solar

thermal power generation, and high temperature heat treatment. Solar energy can also be used in

seawater desalination, etc. Photoelectric conversion is the direct conversion of solar energy into

electrical energy. It uses the photoelectric effect of certain substances to directly convert solar radiation

energy into electrical energy. Its core is the solar cell. Since solar energy must have enough area to

receive sunlight, and it requires a large amount of silicon or compound semiconductors, the demand far

exceeds the use of integrated circuits (ICs). Therefore, the most important key to the solar industry lies

in the upstream raw materials and wafers. Whoever can master the upstream raw materials and wafer

production technology can master the entire industry. However, Taiwan does not have silicon ore

(silicon oxide) or silicon raw material manufacturing technology, so the raw materials used by Taiwan ’s

solar industry are actually controlled by foreign manufacturers.

Taiwan's main strength in the global solar energy industry chain is the silicon chips and battery

modules in the midstream. Silicon chip manufacturers include Green Energy, Danen Tech.,

Sino-American, Sino-American, Eversolcorp, and GIGASTORAGE. In terms of solar cells, major

manufacturers include Motech Industries Inc., NSP, GINTECH, Phoenix Silicon Inc., Tainergy Tech Co.

Ltd., E-Ton Solar Tech, TSEC Corp., etc. In 2015, with a total global solar cell production capacity of

55GW, Taiwan accounted for 8GW of production, and the world's second largest market share, after

China's 30GW. In terms of downstream modules, TYNSOLAR CORPORATION and Inventech are

represented. However, due to the small size and high cost of Taiwan's module factories, the global

IJER – May - June 2020 91

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

market competitiveness is weak (Jun-Hua Wu, 2017). In terms of materials, conductive paste is a key

component of solar cells. Silver aluminum paste can be applied to the serial wires of solar cell modules.

At present, Taiwanese manufacturer GigaSolar has become a leader in this field and can compete with

international manufacturers.

2.3. Taiwan solar energy development problems and solutions

According to the above, the problem can be categorized into two aspects: environmental aspect and

technical aspect. Cheng-Cong Guo (2015) pointed out that nothing more than land resource use and

ecological hazards. Although solar power plants can reduce air pollution, they require a lot of area.

Although solar power plants can reduce air pollution, they require a lot of area. In Taiwan, which is

densely populated, has a population density of 644 people per square kilometer, and ranks 10th in the

world, it requires considerable effort and coordination to build many solar power plants. Solution: (a)

Use the roof, walls, windows, etc. of the home school as much as possible to build solar power facilities;

(b) Use remote areas, mountain areas, open spaces on both sides of highways, and railways to build

large-scale solar power plants to compensate for the land insufficient. (c) Installing large-scale solar

power plants in lakes, reservoirs or idle fishing ports is also a solution. The case of neighboring Asian

countries that lack land (Japan, South Korea, etc.) are currently constructing or have completed the

MW-level floating solar power plant case, which can provide Taiwan reference.

The cost of solar power generation is still higher than the cost of petrochemical power generation.

According to the Sunshot project of the United States Department of Energy (DOE), it is expected that

the module cost will be reduced to $ 0.50 per watt in 2020. At present, various countries have different

subsidies for large-scale solar power generation systems, and some adopt the renewable energy power

generation ratio system (Renewable Portfolio Standard, RPS). Some adopt a renewable energy power

purchase system (Feed-in Tariff, FIT), which is regarded as the most effective economic incentive.

Guaranteeing the purchase price has the functions of stabilizing market prices, increasing investment

confidence and ensuring investment cost-effectiveness.

2.4. Overview of global solar energy

Some cities in Germany and Japan have developed into solar cities, and the country has paid

attention to the development of solar energy very early, and has detailed promotion plans and programs.

Regarding Germany, in 2015, the capacity of German solar installations increased by 1.3GW, and

1.3GW of new installations were added. Although it is less than the target set by the German

government ’s renewable energy plan in 2014 (2.5 GW), it also accounts for solar energy worldwide 2%

of the newly added device capacity. The German government expects to have about 200GW of solar

installation capacity by 2050, so an average of 4-5GW of solar installation capacity needs to be added

every year. The German official report pointed out that the total solar power output in 2015 was

estimated to be 38.5TWh, which is equivalent to 7.5% of German electricity usage, providing a total of

IJER – May - June 2020 92

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

38% of German electricity usage. According to statistics, at the end of 2015, the total solar energy

installation capacity in Germany was 40GW, and records show that during summer weekdays, solar

energy output can provide 35% of peaking power demand during weekends, and on weekends and

holidays, there are even records showing that solar energy output provides 50% peaking power demand.

Figure 1. Renewable energy generation ratio in Germany from 2005 to 2015

(Source: German Trade Office Taipei)

German solar power output began to increase significantly from 2010 to 2012, mainly due to

government policy guidance. The German government began to set solar power generation targets at the

time. This measure not only increased the proportion of solar power generation, but also helped the

energy transformation (German Trade Office Taipei, 2017).

In Japan, more than 80% of Japan ’s energy relies on imports. Since the Fukushima nuclear disaster,

the Japanese government has vigorously promoted renewable energy. In 2012, the “Special Measures for

Renewable Energy Act” was introduced, and electricity generated by solar power was purchased at a

high price. It also attracts Japanese companies to flock into the solar energy industry. However, as Japan

lowered its solar energy purchase price year by year, it caused Japan's "solar bubble" to collapse.

Japanese Tokyo Shoko Research (TSR) released a survey report on December 12, 2016, which pointed

out that the number of bankruptcies of Japanese solar-related companies reached 65 in 2016, a 20.4%

increase from 2015. The number of bankruptcies reached a record high since the investigation began in

2000. TSR also pointed out that "the elimination rate of the Japanese solar energy industry in 2017 will

probably be even greater than in 2016." In 2016, the purchase price of solar power in Japan was 24 yen

per KWh, which was 40% lower than the 40 yen in 2012. In 2017, the purchase price has been further

reduced to 21 yen. The Japanese government hopes to increase the proportion of renewable energy

generation to between 22% and 24% by 2030, but the current figure is still only 14%. Many renewable

energy supporters have begun to worry that the above goals may not have been achieved possibility

IJER – May - June 2020 93

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

(Cheng-Qi Tsai, 2017).

In China, in 2006, China began to implement the "Renewable Energy Law of the People's Republic

of China". The implementation of this law provides policy protection for the development of the solar

industry. The signing of the Kyoto Protocol, the announcement of environmental protection policies and

the commitment to the world have brought opportunities to China's solar energy-related industries. The

development of western China provides a huge domestic market for the solar energy industry. The rise

in oil prices and the adjustment of China's energy strategy have led the government to increase its

support for the development of renewable energy sources. All of these will bring great opportunities for

the development of China's solar energy industry. In addition, China is also actively using the funds and

technologies of international organizations such as the Global Environmental Fund, World Bank, the

United Nations Development Program, and the Asian Development Bank and related national

governments' fund and technology to accelerate the commercialization of China's solar cell industry and

solar power generation. Overall, the three major cities of Shenzhen, Beijing, and Shanghai took the

opportunity to garden park expositions, Olympics, and World Expos, and entered into a show of the use

and exhibition of green energy, such as solar energy and other renewable energy, and were planned to

enter the venue in the large-scale construction that highlights the image of the city, it demonstrates the

achievements China has made in developing solar power systems (Chia-Sheng Wang, 2011).

The largest solar plant in the United States, ISEGS, is located in the City of Needles, California.

There are three plants in total. The maximum power generation capacity is as high as 377,000 kw, which

is the largest in the world and can meet the peak-time electricity demand of 140,000 California

households. As the number of solar installations in the United States continues to grow, the price of

large solar power plants fell below the threshold of $ 1 per watt for the first time. The US market

continued the installed capacity of solar energy in 2016, and the installed capacity in the first quarter of

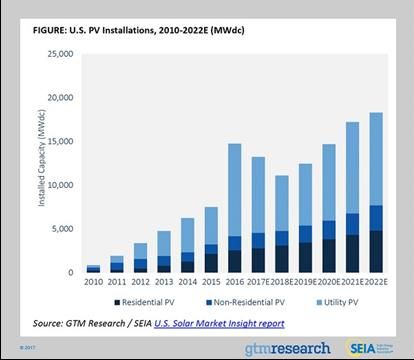

2017 increased by 2044MW. According to the US Solar Energy Industries Association (SEIA) and the

GTM research report "U.S. Solar Market Insight Report", the first quarter of 2017 was the sixth

consecutive quarter in the United States where the single-season installed capacity exceeded 2GW, and

the installed capacity of large-scale power plants also continued to exceed 1GW. The report points out

that the US non-residential solar market grew by 29% compared with the first quarter of 2016. However,

due to the peak installed capacity in the fourth quarter of 2016, the first quarter of 2017 fell by 39%

compared with the previous quarter. The report explained that after the United States announced the

extension of the Investment Tax Relief (ITC) program, the demand for rush-installation of large-scale

solar power plants decreased, and the demand continued from 2016 onwards. At present, the state with

the fastest solar energy development in the United States is Minnesota, and community-based solar

systems continue to contribute to the state's solar development. Idaho and Indiana saw significant growth

in solar capacity in the first quarter of 2017, with emerging markets in Utah, Texas and South Carolina,

IJER – May - June 2020 94

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

and California continuing to maintain the largest domestic solar market in the United States (Delilah Lin,

2017).

SEIA also estimated in the report that in the next five years, the total installed capacity of the

United States will increase three times than it is now; the installed capacity in 2017 will reach 12.9GW,

which will be 10% less than the installed capacity in 2016. Starting from 2022, the annual installed

capacity of solar energy will reach at least 18GW. Abigail Ross Hopper, SEIA ’s director and chief

executive, said, “The US solar industry continues to grow, contributing 17 times faster job opportunities

than the US economy. Moreover, solar energy has the advantage of low price and will become

increasingly important in the market. "

Figure 2 SEIA estimated solar system installation capacity from 2017 to 2022 (source:Austin Perea, 2017)

2.5. Comparison of advantages and disadvantages of the global solar industry

In order to enhance the future competitive advantages of Taiwan's solar photovoltaic industry, this unit

selects the four countries of the United States, Japan, Germany, and China to compare their solar energy

industry development trends and government related industrial policy key projects with Taiwan to provide

development directions and policy recommendations.

In the United States, the diversification of state markets is the strength of the United States, making

the United States less vulnerable to the non-prosperity or recession cycle encountered by many European

solar photovoltaic markets. Coupled with the vast land and sunny California and the southwestern

United States, the power plants are very densely set up, suitable for solar energy development. The US

plans to implement state-level and local policy measures including improved net metering electricity

prices and parallel system regulations. The regulations passed the third-party subsidy model and

IJER – May - June 2020 95

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

renewable energy power generation quota system (RPS). Unfortunately, the current tax incentives do not

take into account system performance, lifespan, and solar power generation time. Therefore, compared

to Europe, China, Japan, and other countries, the US market actually shows unhealthy growth (Jung-Hui

Chiu, 2012).

In China, solar energy resources are very rich. More than two-thirds of the country's land area has

more than 2200 hours of annual sunshine hours. Therefore, the prospects for using solar energy

resources in China are very broad. China's use of solar energy is still in its infancy, and there is still a

considerable gap compared with developed countries. Overall, the main components of the cost of solar

products include raw materials, equipment and manpower. The cost of raw materials accounts for the

highest proportion. Most of China's polysilicon is imported from abroad. With the current domestic

refining technology, the refined polysilicon has high cost and poor quality. Therefore, China has no

advantage in terms of raw material costs. But in terms of equipment and manpower, China's advantages

are quite obvious (Zhen-Hua Zhu, 2013).

In Germany, the common market is one of the most important goals of regional integration in

Europe. The purpose is to create a win-win situation for Germany through the free circulation of capital,

goods, services and personnel. Both technology and commodities have good circulation, further

expanding the market of German products, FIT created a solar miracle in Germany. The German version

of FIT allows power companies to distribute the additional costs equally to all users, allowing market

incentives other than government subsidies to become the main growth drivers of the industry. FIT

allows all power users to participate substantially, and it also promotes the willingness of private

financing to the solar industry. As long as the solar power generation system is connected to the national

distribution network, it will enjoy a 20-year fixed price purchase guarantee. In addition to facilitating the

calculation of the investment rate of return of the industry, group or individual, it also makes the relevant

manufacturers feel the need to save costs under market competition (Dan Martin, 2009).

In Japan, with the introduction of Japanese solar photovoltaics, the cost of the system also began to

decline. Through the company's technology development and government support policies and the

purchase of surplus power by power companies, the domestic market of Japanese solar photovoltaics has

been established. In addition, Japan's Ministry of Education, Science and Culture, Ministry of Land,

Infrastructure, Transport and Tourism has budgeted to invest in solar power generation-related measures.

Furthermore, 655 local governments and towns in Japan have their own subsidy programs for residential

solar systems. However, since the 311 strong earthquake that triggered the Fukushima nuclear disaster in

2011, Japan ’s “solar bubble” collapsed as Japan ’s solar energy purchase prices were lowered year by

year (Jung-Hui Chiu, 2012).

In Taiwan, the advantages of the development of the semiconductor and flat panel display

industries have made Taiwan have considerable potential for the development of the solar industry. It is

IJER – May - June 2020 96

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

also easier to enter the solar energy field because its manufacturing technology and semiconductor

manufacturing have many similarities. At present, Taiwanese manufacturers lack the manufacture of

silicon materials and must rely on foreign imports. The main production equipment must also rely on the

supply of foreign manufacturers. The cost of imports is high. Furthermore, Taiwan solar cell templates

and system verification systems and standards have not established international standards. Failure to

fully recognize each other internationally makes it extremely difficult to export products internationally.

Two-thirds of Taiwan ’s land is in high mountain areas, and only one-third of the land is suitable for

living, and most of it is concentrated on the southwestern coast, which limits the area of Taiwan ’s land

where solar facilities can be installed. Therefore, the use of unconventional installation area has become

an important strategy for the development of solar energy in Taiwan (Qi-Xiu Wang, Xiang-Ke Kong,

Zuo Yu-Ting, 2008).

3. Methodology

The purpose of the questionnaire is to explore Taiwan's solar industry players’ current

developments and related issues. The questionnaire used is the "Taiwan Solar Energy Industry

Development Questionnaire" compiled by researchers as a research tool. The Likert 5-points scale is

used, which are "very important", "important", "normal", "unimportant", and "very unimportant" for

respondents to evaluate the importance of relevant development profile questions. Among them, "very

important" is 5 points, and "very unimportant" is 1 point. Distribution period: From December 2019 to

February 2020, a total of 400 copies were distributed, and the number of collections was 184. The

effective recovery rate was 46%.

3.1 questionnaire design

The questions in this research questionnaire refer to relevant literature. In the design of the

questionnaire, the practitioners of the solar energy industry are also consulted to assess whether the

questionnaire questions conform to the actual environment faced by the relevant personnel of the solar

energy company. The questionnaire questions in this study have been streamlined to facilitate the

respondent's answers, and the factors and opinions considered by the relevant personnel of the solar

industry when facing the problem are detailed in the questionnaire to improve the data collection.

According to Ai-Ling Huang et al. (2013) research, promotion facet refers to persuasion activities on

products or organizations and how to market in 7W, hoping to change customers’ attitudes or induce

customers to adopt certain actions that the government expects, therefore, you need to decide the target

ethnic group and the content of the message before using the promotion strategy, and then consider the

transmission media, channels and methods.

Tsu-Lung Chou (1999) pointed out that technology strategy is a part of business strategy. When

technology becomes an important and critical element in business operation and competition, enterprise

strategy planning also becomes important in business strategy link. In the era of knowledge economy,

IJER – May - June 2020 97

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

technology has become the most important resource for enterprise competition. In high-tech industries,

technological resources and technical capabilities determine the main factors for the success or failure of

the industry's competition. Therefore, technology strategy is the key to business strategy. According to

domestic and foreign journals and literature, the facets that will affect the prospects of Taiwan's solar

industry are:

Prospects of the solar industry Development potential

Government promotion and intervention

Functional constructs

Technical constructs Solar industry

Efficiency constructs

Risk constructs

Figure 3-1. Research structure

3.2 Analysis method

Descriptive statistics provide a simple summary of the measured samples, and the results are

quantified. This result is part of the statistical data that forms a broader content. The data is organized

and summarized to describe the attributes of a certain group in order to have an overall understanding of

the general characteristics of the data.

Reliability analysis, questionnaire reliability refers to the reliability of the questions, that is the

measurement of error, and also the consistency or stability of the test results as the basis. Reliability

measures include test-retest reliability 、 split-half reliability 、 equivalent-forms reliability and

Cronbach’s α reliability, etc. (Wane S. Chou, 2002). Nunnally (1978) argues that in exploratory studies,

if the reliability is greater than 0.7, it is acceptable. The Cronbach's alpha value of this questionnaire is

0.709 in line with Nunnally's argument. If the reliability of the questionnaire is higher, it means that the

questionnaire is more stable.

Validity analysis, validity is whether the measurement tool can accurately check the consistency of

the items in the questionnaire. Generally used "Content Validity" and "Construct Validity". Content

validity refers to the appropriateness of the test questions to sample the relevant content or range of

IJER – May - June 2020 98

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

behavior. "Construct Validity" refers to the degree of correspondence between a certain structure shown

in the measurement results and the measured values, that is, the degree to which the questionnaire can

measure the theoretical concepts or characteristics. Factor analysis is commonly used to construct

validity. This method is to extract the common factors between variables and represent the more

complex data with fewer constructs; based on the common factors extracted from the questionnaire, you

can understand the effective measurement of the questionnaire. What are the characteristics? Generally

speaking, in validity analysis, the indicators used to measure whether the items of the questionnaire have

good validity mainly include factor loadings and KMO (Kaiser-Meyer-Olkin) sampling suitability test

(Yu Huang, 2012).

KMO (Kaiser-Meyer-Olkin) sampling suitability test to check the correlation between variables.

The KMO value is between 0 and 1. When the KMO value is larger, it means that the lower the partial

correlation coefficient between any two variables. The more common factors there are, the better the

effect of factor analysis and extraction of common factors, and the more suitable for factor analysis.

According to Kaiser (1974), the suitability of factor analysis can be judged from the size of the KMO

sampling suitability value. The KMO standard is calculated as

The standard can take a value between 0 and 1. The KMO value must be at least greater than 0.6, and a

value above 0.9 indicates excellent results. The Kaiser-Meyer-Olkin sampling suitability in this study is

0.697. In other words, the value of this study is closer to 1, and there are more common factors between

variables. The effect of extracting common factors by factor analysis is relatively good., Suitable for

factor analysis.

Bartlett Test of Sphericity

Bartlett Test of Sphericity, Bartlett proposed a spherical test for the correlation matrix between

variables, and this test method showed a χ2 distribution, the higher the correlation between the variables,

the higher the value of χ2, indicating that it is more suitable for factor analysis. The χ²-distribution is

quite sensitive to the sample size, so in actual analysis, it is rarely presented that the spherical test

accepts the null hypothesis, that is, when the spherical test method is used, the opportunity for presenting

the results of the resource analysis is suitable. If there are k samples and sample differences

then Bartlett's test statistics are (Bartlett, 1951):

IJER – May - June 2020 99

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

Factor analysis

The main purpose of factor analysis is to find out the structure of the data, use a few factors to

explain a group of variables that are related to each other, and retain the most information, and then

rename each factor. Factor analysis. The application of factor analysis is to find potential factors, filter

variables, summarize the data, select representative variables from the variables (select a variable to use

among the factors), construct validity, and simplify the data (variables with high correlation, only One

needs to be selected as a representative).

Factor Loadings

Factor loadings is the correlation between each variable and factor, so this value is like Pearson

correlations (Pearson correlations), the value is between -1 ~ 1. The square of the factor loadings

indicates how many variables this factor can explain. After executing the factor analysis, there is an

important decision, which variables can be attributed to a certain factor. According to Hair, J. F., Black,

B., Babin, B., Anderson, R. E., & Tatham, R. L. (1992) argument, factor loadings below 0.4 are too low

and 0.6 above is high. However, the data is just corroboration. Sometimes, due to various factors, the

results obtained are slightly lower than expected (Kim, J., & Mueller, C. W, 1978).

4. Results

4.1. Industry Sample Structure

This study uses secondary data analysis and literature review to establish a research structure, and

then through the literature to explore the relevant information and design questionnaire. It is hoped that

the results of the questionnaire survey will be used to understand the trend and vision of the solar

industry in Taiwan, and how the company will maintain a competitive edge and competitiveness in the

industry for future evaluation and research. Through the initial test, questionnaires are officially issued

and collected, and then use SPSS software to analyze. Beside, this study adopts Likert 5-Points Scale,

the instrument was validated in advance through several personal interviews with Solar Industry

managers on site, scoring the subjective cognition an "1" for very unimportant, and a "5" for very

important. The questionnaire was issued between December 2019 and February 2020. A total of 400

anonymous questionnaires were sent, and 216 valid questionnaires were found after deducting the

damaged and ones with incomplete answers. The effective recovery rate was 46.00%, and then use SPSS

18.0 software to analyze and understand the current and future trends and visions of Taiwan's food

biotechnology industry. The following are the results of our analysis such as the statistical variables of

the affiliated company, department, job title, work field, seniority of the relevant industry, company

capital composition, and company product items.

IJER – May - June 2020 100

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

4.1.1. The Companies

Table 1. Distribution of effective samples of companies

Frequency Percentage Effective percentage Cumulative percentage

Giga Solar 30 16.3 16.3 16.3

SEC Corporation 47 25.5 25.5 41.8

GIGASTORAGE

Corp.

28 15.2 15.2 57.1

DANEN TECH. 7 3.8 3.8 60.9

Sino-American

Silicon Products Inc. 15 8.2 8.2 69.0

Others 57 31.0 31.0 100.0

Total 184 100.0 100.0

From the distribution of the above companies, "Other (DelSolar, Alfa Energy)" accounts for the

majority of 31%, followed by "TSEC Corporation" at 25.5%, and at least "Danen Technology" 3.8%.

4.1.2. Departments

Table 2. Distribution of effective samples by department

Effective

Frequency Percentage Cumulative percentage

percentage

R&D Department 32 17.4 17.4 17.4

HR Dept. 1 .5 .5 17.9

Marketing Dept. 7 3.8 3.8 21.7

Quality Control

Department

48 26.1 26.1 47.8

Maintenance department 20 10.9 10.9 58.7

Materials

3 1.6 1.6 60.3

Department

Financial Accounting

Department

5 2.7 2.7 63.0

Manufacturing

department 50 27.2 27.2 90.2

Purchasing Department 4 2.2 2.2 92.4

1

other 14 7.6 7.6

100.0

sum 184 100.0 100.0

In terms of the distribution of the above-mentioned departments, the "manufacturing department"

accounts for 27.2% of the majority, followed by the "quality control department" of 26.1%, and the

smallest department is the "human resources department" of 0.5%.

IJER – May - June 2020 101

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

4.1.3. Job title

Table 3. Sample distribution of effective positions

Effective

Frequency Percentage Cumulative percentage

percentage

President 1 .5 .5 .5

General manager 1 .5 .5 1.1

Deputy General Manager 3 1.6 1.6 2.7

Director 3 1.6 1.6 4.3

Deputy Director 4 2.2 2.2 6.5

Associate Manager 2 1.1 1.1 7.6

Manager 6 3.3 3.3 10.9

Assistant manager 3 1.6 1.6 12.5

deputy manager 15 8.2 8.2 20.7

Section head 5 2.7 2.7 23.4

Senior Engineer 44 23.9 23.9 47.3

Engineer 93 50.5 50.5 97.8

Other 4 2.2 2.2 100.0

Sum 184 100.0 100.0

In terms of the distribution of the above titles, the majority of engineers are 50.5%, followed by

senior engineers are 23.9%, and at least the chairman and general manager are 0.5%.

4.1.4. Fields of work

Table 4. Distribution of samples in the field of work

Frequency Percentage Effective percentage Cumulative percentage

Technology R & D 37 20.1 20.1 20.1

Academic Research 3 1.6 1.6 21.7

Marketing 3 1.6 1.6 23.4

Industry analysis 3 1.6 1.6 25.0

Product planning 2 1.1 1.1 26.1

Policy implementation and

4 2.2 2.2 28.3

supervision

Production / Manufacturing 117 63.6 63.6 91.8

other 15 8.2 8.2 100.0

sum 184 100.0 100.0

In terms of the above-mentioned work areas, "production / manufacturing" accounts for 63.6% of

the majority, followed by "technology research and development" accounts for 20.1%, and at least

"product planning" accounts for 1.1%.

IJER – May - June 2020 102

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

5. Years of experience in related industries

Table 5. Distribution of effective sample of seniority

Frequency Percentage Effective percentage Cumulative percentage

0~3 years 72 39.1 39.1 39.1

4~6 years 45 24.5 24.5 63.6

7~10 years 31 16.8 16.8 80.4

11~15 years 23 12.5 12.5 92.9

More than 16 years 13 7.1 7.1 100.0

sum 184 100.0 100.0

In terms of the seniority of the above-mentioned related industries, the highest number of seniority

in "0 to 3 years" accounted for 39.1%, followed by "4 to 6 years" accounted for 24.5%, at least for "more

than 16 years" accounted for 7.1%.

6. The company's capital composition (%)

Table 6. Distribution of effective capital samples

Frequency Percentage Effective percentage Cumulative percentage

Foreign investment accounts

1 .5 .5 .5

for more than half

Foreign investment accounts

74 40.2 40.2 40.8

for less than half

All Taiwanese 109 59.2 59.2 100.0

sum 184 100.0 100.0

In terms of capital composition of the above-mentioned companies, "all Taiwan-funded" accounts

for a maximum of 59.2%, followed by "less than half of foreign investment" accounts for 40.2%, and at

least "more than half of foreign investment accounts for 0.5%".

7. Registered capital

Table 7. Distribution of valid sample of capital registration

Effective Cumulative

Frequency Percentage

percentage percentage

30 million to 80 million 3 1.6 1.6 1.6

80 million to 200 million 2 1.1 1.1 2.7

200 million to 1 billion 24 13.0 13.0 15.8

1 billion to 3 billion 56 30.4 30.4 46.2

3 billion to 6 billion 83 45.1 45.1 91.3

6 billion to 10 billion 16 8.7 8.7 100.0

sum 184 100.0 100.0

According to the capital registration of the above-mentioned companies, "3 billion to 6 billion"

IJER – May - June 2020 103

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

accounted for the most of 45.1%, followed by "1 billion to 3 billion" accounted for 30.4%, at least "80

million to 200 million" accounted for 1.1%.

8. The company's products

Table 8. Distribution of effective samples of product types

Response value

% Of observations

Number Percentage

Solar module 102 32.4% 55.4%

Solar conductive paste 29 9.2% 15.8%

Solar monocrystalline battery 101 32.1% 54.9%

Silicon chip 41 13.0% 22.3%

Solar Ingot / Block 19 6.0% 10.3%

Solar cell 8 2.5% 4.3%

other 15 4.8% 8.2%

total 315 100.0% 171.2%

It can be seen from the above results that the products produced by the solar energy company are

mainly "Solar Module" 32.4% and "Solar Monocrystalline Battery" 32.1%. Due to the relationship of

multiple choice questions, the sum of the percentage of observations is 171.2%, indicating that in a

multiple-choice question with a maximum of three answers, each person answered an average of 1.712

answers.

4.2. Reliability and validity verification

In order to discuss the interviewees' important issues on the solar industry and solar development,

this study designed a total of 20 items from expert interviews and secondary data. Through the initial test,

questionnaires are officially issued and collected, and then use SPSS software to analyze. Beside, this

study adopts Likert 5-Points Scale, the instrument was validated in advance through several personal

interviews with Solar Industry managers on site, scoring the subjective cognition an "1" for very

unimportant, and a "5" for very important. The questionnaire was issued between December 2019 and

February 2020, a total of 400 copies were distributed, and 184 valid questionnaires were found after

deducting the damaged and ones with incomplete answers. The effective recovery rate was 46%, and

then use SPSS 18.0 software to analyze and understand the prospects and visions of Taiwan's solar

industry. The following are the results of our analysis.

Table 9. KMO and Bartlett Test of Sphericity

Kaiser-Meyer-Olkin measure of sampling adequacy .697

Chi-Square Approximation Value 1139.275

Bartlett Test of Sphericity df 276

Significance .000

From the information obtained in Table 9 above, KMO=0.697、Bartlett Test of Sphericity is

1139.275,Significance=0.000,The results show that the data is suitable for factor analysis.

IJER – May - June 2020 104

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

After passing the test, the principal components analysis in the factor analysis is continued to

extract the common factors. According to the principle that the eigenvalues is greater than 1 as the

number of common factors, a total of 5 main factors are selected, which can explain 60.084% of the total

variation. Then through the VARIMAX, the selected factors are rotated to make the representative

meaning of each factor more obvious and easier to explain. The results are shown in Table 10. (The

yellow part is the absolute value of the factor loadings is greater than 0.45)

Table 10. Comparison of factor loadings

Elements

Variables

1 2 3 4 5

Government intervention .736 .062 .279 -.029 .045

Consensus to promote energy transformation .753 .122 .021 .038 .126

Government Promotion .717 .177 .036 -.038 -.059

Popularization of solar panels on the roof .695 -.061 -.199 -.157 .052

Increase the purchase price of solar power .503 .057 -.107 -.278 .446

Media propaganda .495 .001 .063 .026 -.045

Erecting solar panels on the coast, seaside, etc. .386 .081 .027 -.601 .110

Attractive forward-looking approach .214 .583 .064 .364 -.096

Power generation network .057 .692 .018 .036 -.023

Increase the guaranteed years of solar power acquisition -.022 .598 -.089 .191 .450

Move to high energy efficiency, renewable energy supply, and

store in smart grid

-.097 .351 -.009 .457 -.013

Solar conversion efficiency needs to be improved -.095 .178 .128 .651 .141

Encourage local government to actively participate .213 .226 -.318 .584 -.068

Waste recycling .395 -.202 .731 .103 .016

Uniform waste disposal standards -.261 .298 .635 .087 .040

Establish a waste disposal center -.053 -.116 .451 .385 -.031

Improve solar waste resource recycling technology .041 .038 .733 -.114 .043

Try to reduce risks and consider the status of nuclear power -.085 .155 .045 .009 .645

24 hours power supply .299 -.319 .223 .050 .649

Government Promotion .188 .676 .075 .003 -.074

IJER – May - June 2020 105

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

This study summarizes five factors and summarizes the detailed information as shown in the table

below:

Table 11. Results of principal component analysis

Total explained

Name of Factor Factor loading Eigenvalue

variance

1.Government promotion and intervention factors .753

Consensus to promote energy transformation .736

Government intervention .717

Government Promotion 3.926 16.359%

.695

Popularization of solar panels on the roof

Increase the purchase price of solar power .503

Media propaganda .495

2. Functional factors

Interwoven power generation network .692

Government Promotion .676 2.898 12.075%

Increase the guaranteed years of solar power

acquisition .598

Attractive forward-looking approach .583

3. Technical factors

Improve solar waste recycling .733

Improve solar waste recycling .731 2.152 8.965%

Uniform waste disposal standards .635

Establish a waste disposal center .451

4. Efficiency factors

The conversion efficiency of solar energy needs to be

improved .651

Encourage local government to actively participate .584 1.795 7.481%

Shift to high energy efficiency, renewable energy

supply .457

Erecting solar panels on the coast, seaside, etc. -.601

5. Risk factors

24 hours’ power supply .649

Try to reduce risks and consider the status of nuclear .645 1.135 4.728%

power

Increase the guaranteed years of solar power

acquisition .450

Factor 1 is mainly composed of six types of high-relevant variables, such as "government

intervention", "consensus to promote energy transformation", "government promotion", "Popularization

of solar panels on the roof ", "increasing the purchase price of solar power", and "media propaganda”,

the factor named as "Government Promotion and Intervention Factor". The factor loadings are between

0.495 and 0.753, the eigenvalue is 3.926, and the explained variance is 16.359%.

Factor 2 is mainly composed of four types of high-relevant variables, such as "Attractive

forward-looking approach", "Interweaving power generation network", "Increase the guaranteed years of

solar power acquisition", and "Government promotion”, named as "functional factor". The factor

loadings are between 0.583 and 0.692, the eigenvalue is 2.898, and the explained variance is 12.075%.

IJER – May - June 2020 106

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

Factor 3 is mainly composed of four types of highly relevant variables, such as "recycling auxiliary

materials for recycling waste", "uniform waste disposal standards", "establishing a waste disposal

center", and "improving solar waste recycling". Due to the higher loading of the first two factors, this

factor is named as "technical factor". The factor loading between 0.451 and 0.733, the eigenvalue is

2.152, and the explainable variation is 8.965%.

Factor 4 is mainly composed of four types of highly relevant variables, such as “Establish solar

panels along the coast and seaside", "Turn to high energy efficiency, renewable energy supply", "Solar

conversion efficiency needs to be improved”, and "Encourage local governments to actively participate".

Due to the higher loading of the first two factors, this factor is named as “Efficiency Factor”. The factor

loading between 0.451 and 0.657, the eigenvalue is 1.795, and the explainable variation is 7.481%.

Factor 5 is mainly composed of three highly relevant variables, such as "Increase the guaranteed

years of solar power acquisition ", "Try to reduce risks and consider the status of nuclear power ", and

"available power supply in 24 hours". Due to the higher loading of the first two factors, the factor is

named as "risk factor". The factor loading is between 0.450 and 0.649, the eigenvalue is 1.135, and the

explainable variation is 4.728%.

5. Conclusion and suggestion

5.1. Conclusion

Through the compilation of the literature, this study has learned that as environmental awareness is

raised, all countries are eager to find alternative energy sources, so the development of the solar energy

industry has potential. Taiwan ’s current lack of raw materials and production equipment in the solar

industry is also limited by land restrictions. Under the constraints of production equipment, Taiwan

should develop various patents to avoid relying on imports to cause excessive production costs; under

the constraints of small land area and dense population, for Taiwan to make solar energy a pivotal

alternative, it must have new thinking and think about both. The space reuse method effectively

increases the proportion of solar power generation. The case of neighboring Asian countries that lack of

land (Japan, South Korea, Singapore, etc.) are currently constructing or have completed the MW-level

floating solar power plant case, which can provide reference for Taiwan.

According to the analysis of the above data, this study divides the key factors that affect the

prospects of Taiwan's solar energy industry at this stage into five constructs, namely the government

promotion and intervention construct, function construct, technology construct, efficiency construct, and

risk construct, as follows describe the importance of each aspect to the company and the department:

In the government promotion and intervention aspect, the research results show that the two

companies " DelSolar Co Ltd." and "ALFA ENERGY CORPORATION" have a significant difference

in this aspect compared with other companies, and are more important than other companies, the quality

control department pays more attention to this aspect than other departments.

IJER – May - June 2020 107

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

In terms of functional aspects, the research results show that " GIGASTORAGE Corp." has a clear

difference in this aspect compared to other companies. In this aspect, the materials department pays

more attention than other departments.

In the technical aspect, the research results show that the company and the department have no

obvious significance in this aspect, of which "Giga Solar Materials Corp." is more important than other

companies, and the importance of the materials department is also higher than other departments.

In terms of efficiency, the results of the study show that "GIGASTORAGE Corp." is significantly

different from other companies in this aspect, and it is also more important than other companies. The

human resources department pays more attention than other departments.

In terms of risk, the research results show that "DANEN Technology Corp." is significantly

different from other companies and is more important than other companies. The material department

pays more attention than other departments.

5.2. Suggestion

5.2.1. The government needs to formulate perfect subsidies and incentives

Perfect subsidies and incentives are an important key to promote renewable energy, and also a policy

incentive for government and industry development. For the solar energy industry in Taiwan, government

policies, subsidy systems, regulations, etc. have a certain degree of influence on the industry. Therefore, it

is recommended to provide policies related to industrial development, and continue to cooperate with

industry players to expand end-user adoption and drive the expansion of the upstream and midstream.

5.2.2. Vertical integration and strategic alliance

Establish a complete industrial structure and value chain through domestic and foreign peers and

different industries. Because Taiwan ’s upstream raw materials must rely on imports in the solar industry

development structure, and the development of the solar industry must master the stable supply of

upstream raw materials in order to stabilize the solar industry development. Taiwan's main strength in

the global solar energy industry chain is the silicon chips and battery modules in the midstream. In terms

of downstream modules, although they can meet domestic needs, due to the small scale of module

factories, high costs, and weak global market competitiveness, mid- and downstream manufacturers

need to develop economies of scale among each other. At the same time, industry players need to

discuss strategies and methods to attract foreign industry investment to reduce the cost of raw materials

for the solar industry, and then make up for the deficiencies of the solar industry.

5.2.3. Improve photoelectric conversion efficiency and establish technology patents

Earth rotation and climate change factors make solar energy intermittent. Compared with traditional power

generation methods (power, water, wind, etc.), solar energy can only be used as auxiliary energy, Therefore, under

the environmental constraints, the development of solar photovoltaics must increase the conversion efficiency to

IJER – May - June 2020 108

available online @ www.ijeronline.comMing-Lang Wang, Kang-Wei Wang, Int. Jou Eco.& Res, 2020, V11 i3 (mj), 89 – 110 ISSN: 2229-6158

the maximum to supplement the peak power consumption; at the same time, establish solar storage technology to

ensure that the energy supply is not limited to environmental and climatic factors and affect stability. Taiwan has

great advantages in the development of the semiconductor and flat panel display industries, and Taiwan has

considerable potential for the development of the solar industry. Because the manufacturing involved in the solar

industry has many similarities with semiconductor manufacturing, it is easier to enter the solar field. However,

because Taiwan's solar cell template and system verification have not established international standards, they

cannot fully recognize each other internationally, which makes it extremely difficult to export products. Therefore,

to occupy a place in the international market, Taiwan technology patents must be established.

5.2.4. Formulate the most suitable development strategy to avoid market marginalization:

The external environment is changing rapidly. If you don’t keep up, you may be eliminated. However,

in addition to the government's efforts to strive for international space for industry, more medium- and

long-term development strategies and options are needed. In order to enhance competitiveness and expand

advantages, major manufacturers have gradually adopted vertical integration or strategic alliances in recent

years to respond to the fierce global competition. Therefore, this study suggests that on the existing basis,

the industry chooses suitable development strategies, integrates effective resources and solutions, and

strengthens cooperation between various supply chains to avoid being marginalized by the market in order

to enhance the competitiveness of Taiwan's solar industry.

REFERENCES

Ai-Ling Huang, Qing-Yan Yang, Wen-Xin Wang, Ji-Xian Huang, You-Da Lin, Her-Nian Xie, (2013),

“Discussion on Strengthening Policy Marketing Practices of Government Agencies - Take the

New Taipei City Government Tax Collection Office as an example to promote local tax online

reporting,” National Academy of Civil Service T&D Fashion, Vol.160, pp.1-15. [Accessed on

2020/03/29].

Austin Perea, (2017), Solar Market Insight Report 2017 Q4. Solar Energy Industries Association.

Bartlett, M. S., (1951). “An inverse matrix adjustment arising in discriminant analysis,” The Annals of

Mathematical Statistics, Vol. 22, pp.107-111.

Bureau of Energy, Ministry of Economic Affairs, (2015), “Taiwan's short, medium and long-term of

Solar Energy in Taiwan,” Energy Information Platform-Energy Analysis.

https://www.moea.gov.tw/MNS/dos/home/Home.aspx [Accessed on:2020/04/12]

Burns, John Edward, (2011), Comparative analysis of supporting solar policies in the USA: a study of

the potential effects of solar renewable energy certificates(SRECs) on residential photovoltaics,

National Chiao Tung University, Global MBA, unpublished master thesis, Hsinchu City.

Cheng-Cong Guo, (2015), “The Current Situation, Problems, Solutions or Suggestions for the

Development of Solar Energy in Taiwan,” Energy Information Platform” Chung-Hua Nuclear

Society.

Cheng-Qi Tsai, (2017), The Japanese solar bubble collapsed! Businesses have successively retreated,

and the number of bankruptcies has soared to a new high, MoneyDJ,

https://tw.money.yahoo.com/ [Accessed on 2020/03/25]

Chia-Sheng Wang, (2011), Project Evaluation: The Feasibility of Promoting Kaohsiung Become a Solar

City, National University of Kaohsiung IMEBA, unpublished master thesis, Kaohsiung City.

Dan Martin, (2009), “Feed-in Tariff, FIT”, Driving the Growth of the PV Industry.

http://www1.semi.org/zh/MarketInfo/ctr_031895 [Accessed on 2020/01/28]

IJER – May - June 2020 109

available online @ www.ijeronline.comYou can also read