CIBC Fixed Income Conference - April 10, 2019 - Keyera

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CIBC Fixed Income Conference April 10, 2019

Disclaimer

In the interests of providing Keyera Corp. (“Keyera” or the “Company”) shareholders and potential investors with information regarding Keyera,

including Management’s assessment of future plans and operations relating to the Company, this document contains certain statements and

information that are forward-looking statements or information within the meaning of applicable securities legislation, and which are collectively

referred to herein as “forward-looking statements". Forward-looking statements in this document include, but are not limited to statements and

tables with respect to: capital projects and expenditures; strategic initiatives; anticipated producer activity and industry trends; and anticipated

performance. Readers are cautioned not to place undue reliance on forward-looking statements, as there can be no assurance that the plans,

intentions or expectations upon which they are based will occur. By their nature, forward looking statements involve numerous assumptions, as

well as known and unknown risks and uncertainties, both general and specific, that contribute to the possibility that the predictions, forecasts,

projections and other forward-looking statements will not occur and which may cause Keyera’s actual performance and financial results in

future periods to differ materially from any estimates or projections of future performance or results expressed or implied by the forward-looking

statements. These assumptions, risks and uncertainties include, among other things: Keyera’s ability to successfully implement strategic

initiatives and whether such initiatives yield the expected benefits; future operating results; fluctuations in the supply and demand for natural

gas, NGLs, crude oil and iso-octane; assumptions regarding commodity prices; activities of producers, competitors and others; the weather;

assumptions around construction schedules and costs, including the availability and cost of materials and service providers; fluctuations in

currency and interest rates; credit risks; marketing margins; potential disruption or unexpected technical difficulties in developing new facilities

or projects; unexpected cost increases or technical difficulties in constructing or modifying processing facilities; Keyera’s ability to generate

sufficient cash flow from operations to meet its current and future obligations; its ability to access external sources of debt and equity capital;

changes in laws or regulations or the interpretations of such laws or regulations; political and economic conditions; and other risks and

uncertainties described from time to time in the reports and filings made with securities regulatory authorities by Keyera. Readers are

cautioned that the foregoing list of important factors is not exhaustive. The forward-looking statements contained in this document are made as

of the date of this document or the dates specifically referenced herein. For additional information please refer to Keyera’s public filings

available on SEDAR at www.sedar.com. All forward-looking statements contained in this document are expressly qualified by this cautionary

statement.

2

Keyera Representatives

Steven Kroeker

• Senior Vice President & Chief Financial Officer

Eileen Marikar

• Vice President, Finance

Avery Reiter

• Director, Treasury

KFS Frac and Storage

3

Keyera at a Glance1

Key Metrics

Market Capitalization2 ~$6.6 billion

Enterprise Value2 ~$8.8 billion

2018 Adjusted EBITDA $807 million

2018 Payout Ratio 56%

Dividend $1.80/share p.a. ($0.15/share per month)

Dividend Yield2 ~5.71%

Corporate Credit Ratings3 BBB/Stable

Net Debt/EBITDA 2.6x

2019 Growth Capital Program $800-$900 million

1. All information as at December 31, 2018, unless otherwise stated.

2. As at March 31, 2019.

3. DBRS and S&P.

One of Canada’s largest midstream companies 4

2018 Record Year even in a Challenging Environment

Record Financial Performance Operational Milestones

Adjusted EBITDA1,2 Distributable Cash Flow2 Net Earnings Record volumes

($ Millions) ($ per share) ($ Millions) • Simonette Gas Plant

• Ft Saskatchewan Fractionator

$807 • Condensate system

$3.08 $394

$2.70

• Marketing services

$617

$290

Invested ~$1.3B in 2018

2017 2018 2017 2018 2017 2018

1. Adjusted EBITDA is defined as earnings before interest, taxes, depreciation, amortization, accretion, impairment expenses, unrealized gains/losses and any other non-cash items such as

gains/losses on the disposal of property, plant and equipment.

2. See section of the MD&A in Keyera’s 2018 Year End Report titled “EBITDA” for a reconciliation of Adjusted EBITDA and “Divdends: Distributable Cash Flow” for a reconciliation of distributable cash 5

flow respectively, for their most closely related GAAP measures.

Integrated Value Chain

1. Percentage of total realized margin for the year ended December 31st 2018 (2017 - 80%). Realized margin is defined as operating margin excluding unrealized gains and losses from risk management

contracts from the Marketing segment. Realized margin is not a standard measure under GAAP.

6

Realized Margin by Segment

Realized Margin ($ millions)

• Keyera’s Gathering and Processing and 2016 2017 2018

Liquids Infrastructure businesses are Fee-for-Service Segments1 $536 $556 $598

predominately fee-for-service Marketing $137 $128 $296

Other2 $11 $14 $13

• Marketing segment had an excellent Total $684 $698 $907

2018, resulting in a lower fee-for-

Segment Realized Margin as a % of Total Realized Margin

service proportion of realized margin

2016 2017 2018

• Keyera’s Marketing business is backed Fee-for-Service Segments1 78% 80% 66%

by ownership in assets Marketing 20% 18% 33%

Other2 2% 2% 1%

Total 100% 100% 100%

* All figures represent last twelve month results as of December 31.

1. Includes intersegment transactions.

2. “Other” includes production segment.

7

Solid Contractual Foundation

• Keyera’s current cash flows are well supported by fee-for-service contracts, including take-or-pay

contracts

• Adjusted EBITDA from Keyera’s current ~$2.1 billion capital program will be supported by a

combination of fee-for-service, take-or-pay and area dedication agreements

2018 Realized Margin Take-or-Pay Revenue as a % of

2018 Adjusted EBITDA

1%

Fee-for-Service

Take-or-Pay

33%

Marketing 43%

57%

66% Non Take-or-Pay

Other

8

Low Counterparty Credit Risk

Consolidated1,2,3 Gathering and Processing

• Keyera provides essential

infrastructure and marketing services

to industry 18% Investment Investment

Grade/Secured Grade/Secured

30%

• ~82% of Keyera’s total revenue in 13% Split Split

2018 came from investment 69%

59%

11%

Non-IG Non-IG

grade/secured or split rated

counterparties

• Credit risk management strategies Liquids Infrastructure Marketing

include: letters of credit, netting

agreements, pre-payments 1%

7% Investment

Investment 14%

Grade/Secured Grade/Secured

• Broad domestic and international

14% Split

customer base Split

72% Non-IG

Non-IG

93%

1. Based on 2018 revenues.

2. Counterparty ratings are representative of the counterparties’ rating as of March 15 th, 2019. Where parental guarantees are in place, the credit rating of the parent is used. The secured category

includes counterparties who are on prepay terms or have posted a letter of credit. 9

3. Split denotes counterparties with an investment grade rating by one rating agency and non-investment grade rating by another agency.

Investment Opportunities Continue

Millions ANNUAL CAPITAL EXPENDITURES

$1,400

$1,200

$1,000

$800

$600

$400

$200

$- 2

1

12/31/13 12/31/14 12/31/15 12/31/16 12/31/17 12/31/18 12/31/19e

Growth Capital Upper End of Growth Capital Range Acquisitions Maintenance Capital

1. Acquisition capital in 2017 reflects the $55 million purchase price for undeveloped land in the Industrial Heartland of Alberta completed in 1Q17, among other actual YTD costs.

2. Keyera’s 50% acquisition of the South Grand Rapids pipeline is included in 2018 Acquisitions.

$800 – $900 Million of Growth Capital Investment in 2019 10Growth Projects Currently Under Development

Approved Projects Capital Cost 2018 2019 2020

(Net, in $ Millions)1

Wapiti Area Gathering & Processing Complex (Phase I) 575

Wapiti Gas Plant (Phase II) & North Wapiti Pipeline System 325

Wapiti Water Disposal System 100

Simonette Inlet & Acid Gas Injection Enhancements 100

Simonette Plant Expansion 85

Pipestone Plant (Phase I) 2 600

Wildhorse Terminal US185

Storage Cavern Development Program at Keyera Fort Saskatchewan 110

TOTAL ~$2.1 Billion

1. Keyera’s share of estimated capital cost. See Keyera’s 2018 Year End MD&A for capital investment risks and assumptions. 2. Pipestone plant expected to start up in 2021. 3. Return on Capital is defined

as operating margin divided by the estimated capital cost of the projects noted on this slide. Keyera expects to achieve this return, in 2022 once all projects achieve their annual run rate. See “non-GAAP

Financial Measure” and “Forward-Looking Statements” in Keyera’s 2018 Year End MD&A for further details.

$2.1B Program expected to achieve 10-15% return on capital3 11Gathering and Processing Business Unit

Wapiti

Plant

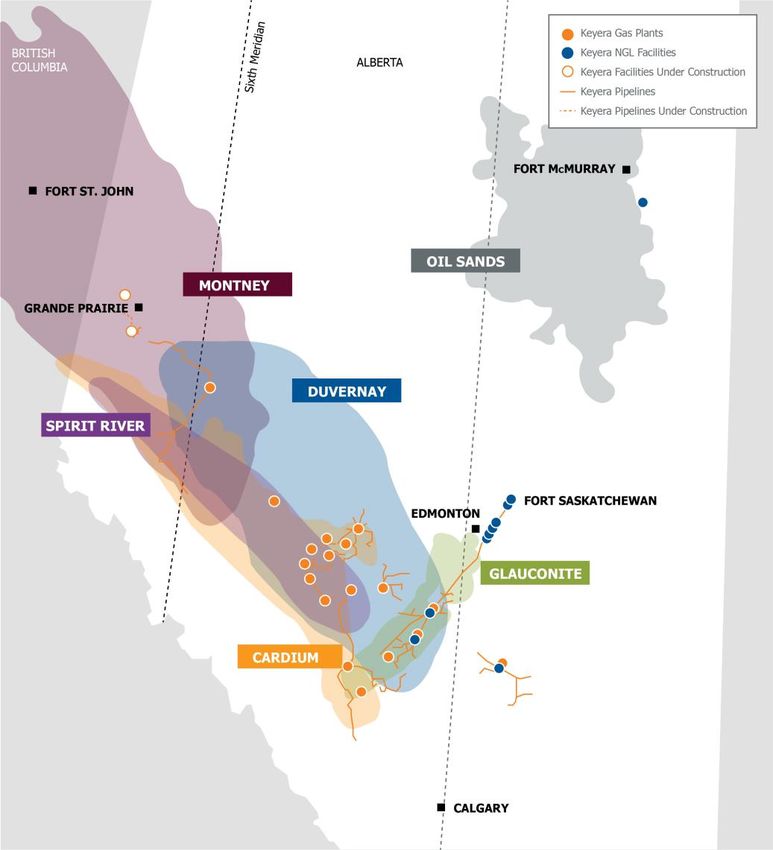

12Growing Presence in Liquids-Rich Area of NW Alberta

Gross Sour Gas Processing Capacity (Year End) Condensate Handling Capacity (Year End)

1000 100,000

900 90,000

200

800 80,000

700 70,000 38,000

bbls/d

mmcf/d

600 300 300 60,000 14,000 14,000

500 150 950 50,000 90,000

400

mmcf/d 40,000 25,000 25,000 25,000 b/d

14,000

300 30,000

200 450 450 450 20,000

300 300 27,000 27,000 27,000 27,000

100 10,000

10,000

0 -

2017 2018 2019 2020 2021 2017 2018 2019 2020 2021

Simonette Wapiti Pipestone Simonette Wapiti Pipestone

Supporting Producer Growth Plans in Liquids-Rich Developments 13Relatively Stable Throughput

H I S T O R I C A L T H R O U G H P U T & T H E P E R C E N T AG E C H A N G E I N AE C O & W T I T O D e c e m b e r 3 1 , 2 0 1 8

14Liquids Business Unit Unmatched Infrastructure for NGL and Oil Sands Customers 15

Fractionation at Multiple Locations

Gilby Gas Plant Nevis Gas Plant

3,650 bbls/d gross (2,930 bbls/d net) 3,740 bbls/d of C3+ fractionation capacity

of C3+ fractionation capacity

Rimbey Gas Plant Dow Fort Saskatchewan

28,000 bbls/d gross (27,640 bbls/d net) Keyera Fort Saskatchewan 30,000 bbls/d gross (5,420 bbls/d net)

of C3+ fractionation capacity of C3+ fractionation capacity

20,000 bbls/d gross (19,740 bbls/d net) 65,200 bbls/d gross (50,000 bbls/d net) of 30,000 bbls/d gross (23,010 bbls/d net) of 69,200 bbls/d gross (6,920 bbls/d net)

of de-ethanization capacity C3+ fractionation capacity de-ethanization capacity of de-ethanization capacity

Adding Value by Processing NGLs from the Gas Stream 16Oil Sands Production Continues to Grow

Bitumen Production Growing Diluent Demand > Condensate Supply

3,000 1,000

900

2,500

800

700

2,000

MBbl/d

600

MBbl/d

1,500 500

400

1,000

300

200

500

100

0 0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2018A 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Actual CIBC World Markets Forecast WCSB Supply Forecast Demand

Source: Estimates as per CIBC World Markets.

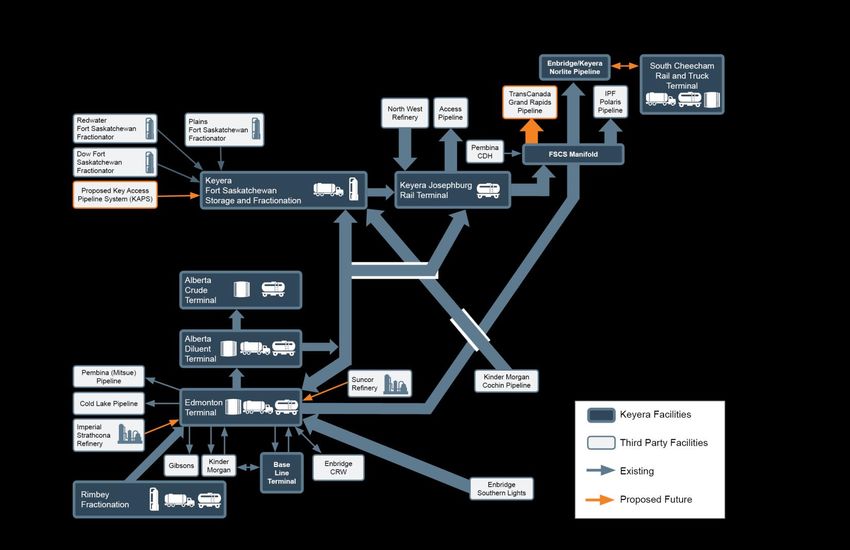

Bitumen Production Growth Driving Condensate Demand 17Extensive, Flexible Condensate Infrastructure

• Most connected condensate hub in Western Canada

• Major oil sands delivery options:

– Polaris – Access – Grand Rapids

– Norlite – FSPL – South Cheecham

• Supply through multiple receipt points:

• Local fractionators and refineries

• Kinder Morgan Cochin pipeline

• Enbridge Southern Lights pipeline and CRW pool

• Western Canada feeder pipelines

• Canadian Diluent Hub

• Rail imports at the Alberta Diluent Terminal

• Storage at Keyera Fort Saskatchewan – Imperial Oil (Kearl) – Cenovus (Christina Lake)

– Husky/BP (Sunrise) – CNRL (Kirby, Primrose)

• Long-term take-or-pay and fee-for-service agreements: – Suncor/Teck/Total (Fort Hills) – JACOS/Nexen (Hangingstone)

– North West Upgrading – Devon (Jackfish)

Industry-Leading Diluent Handling Services 18Crude Oil Storage

Baseline

Tank

Terminal

Wildhorse

Terminal

Expanding and Diversifying Keyera’s Service Offering 19Marketing Services

• Facilities based marketing

Condensate

C5+

• Prudent risk-management hedging • Keyera’s C5+ hub creates industry liquidity

• Consumed in Alberta as diluent for bitumen

strategy • Significant imports required today to meet

demand

Butane

C4

• Sourced and consumed in Alberta Ethane

• Feedstock for iso-octane production at

C2

• Sold under long-term agreements to

Alberta EnviroFuels

petrochemical producers in Alberta

• Seasonal imports from the U.S.

• Limited spot market in western Canada

• Produced at three Keyera facilities

Propane

Iso-octane

C3

•

iC8

Supply exceeds demand in North America

• Majority of sales in the U.S. • Majority sold into U.S. markets

• High quality gasoline additive • Demand and pricing vary seasonally

• Produced from butane at Keyera’s • Keyera uses its storage and logistics to

Alberta EnviroFuels facility access markets

Diversified Portfolio of Logistics Services 20Alberta EnviroFuels (AEF)

• Iso-octane (iC8) is a high octane, low vapour pressure

gasoline additive

• Butane is the NGL feedstock

• Only merchant iC8 facility in North America

• Licensed capacity of 13,600 bbls/d

• Supply networks and distribution infrastructure used to

source feedstock while rail logistics broaden sales markets

• Financial forward markets enable hedging of feedstock costs

and large portion of iC8 margin

• iC8 demand driven by premium gasoline demand

• Seasonality is complementary to propane and butane

iC8 is a Premium Value-Added Product Produced in Alberta 21Conservative Capital Structure

LONG-TERM DEBT MATURITIES2 (excludes drawings under revolver)

Issuer Credit Ratings:

• DBRS Limited: BBB with a Stable trend

2.6x • S&P Global: BBB/Stable

Net Debt1 to

EBITDA

1. Calculated as of December 31, 2018 in accordance with Keyera’s debt covenants. For further information regarding covenant calculations, please see

Keyera’s 2018 Year End Report MD&A or copies of the note purchase agreements, all of which are filed on SEDAR.

2. All US dollar denominated debt is translated into Canadian dollars at its swap rate. 2019 maturities as of February 1, 2019.

Well Positioned to Fund Keyera’s $2.1 Billion Capital Program 22You can also read