Dispatchable renewables in the NEM - A markets and investor perspective

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Dispatchable renewables in the NEM A markets and investor perspective Australian Energy Storage Conference June 2019 Copyright © Baringa Partners LLP 2019. All rights reserved. This document is subject to contract and contains confidential and proprietary information.

Baringa Overview

We help clients in the energy industry run more effective businesses, launch new businesses and reach new markets,

understand and navigate industry change

60 Partners : 660 Employees

6 Offices Worldwide

London head office, with offices in

Ireland, USA, Germany, UAE and

Australia delivering projects globally

Unique Experience

Our clients tell us that they enjoy

the distinctive experience of

partnering with Baringa

Great Place To Work

Voted top 10 ‘Great Places to Work’

for 12 years running…this creates a

highly motivated, engaged and Baringa project location

passionate consulting team

Baringa office location

Upstream/ Trading / Distributed

T&D Retail / Supply Customer

Generation Sourcing Energy

Copyright © Baringa Partners LLP 2019. All rights reserved. This document is subject to contract and contains confidential and proprietary information.

2

Contents

Utility-scale storage: overview of use cases

FCAS bankability

Wholesale arbitrage and cap contract value

Hybrid economics across the NEM

Firming and bankability

Copyright © Baringa Partners LLP 2019. All rights reserved. This document is subject to contract and contains confidential and proprietary information.

Client Confidential 3

Storage applications, or ‘use cases’

As the NEM generation mix moves increasingly to a more intermittent and (in future) a potentially tighter supply side

attempting to meet a relatively inflexible demand side, flexibility will become critical to system stability

Service Market opportunity Applications Examples

50.2

Increasing need for faster- Assist AEMO in maintaining stable Grid frequency (where 50.1

50.0

system frequency by providing 50Hz = perfect supply/

Ancillary acting response due to lower

demand balance) 49.9

Ability to respond system inertia and retirement changes in generation or demand 49.8

quickly to external of existing response providers, Be available to generate when there is + kW

signals providing Regulation and a supply shortfall (e.g. plant trip), to Battery output in response

Contingency to mismatch in supply/

restore system frequency

demand balance - kW

Solar output

Price arbitrage in the NEM wholesale Solar output and

kW

energy market site consumption Consumption

Increasing peak/off-peak across the day

Arbitrage spread and renewable Provide cap contract cover to retailers

Shifting energy in 00:00 23:00

generation profiles create and large customers

response to a price or opportunities to profit from

+kW DISCHARGE

Match shape and profile of Battery charging/

time signal moving energy between periods renewables to customer demand to discharging pattern

CHARGE

provide firming services -kW

00:00 23:00

p/kWh

Provide system services to renewable

Network and Strategically locate storage in projects and/or NSP to reduce losses, Shape of electricity

charges across the day

system stabilty areas of high renewables to local curtailment and voltage

System stability provide system stability, instability 00:00 23:00

provision and enabling reduced curtailment and Generate at peak times to receive kW

deferral/avoidance of network Effect of battery

the deferral of network embedded benefits or avoid peak charging/ discharging

CHARGE Consumption

investment reinforcement retail tariffs for a customer DISCHARGE

on grid consumption

00:00 23:00

Copyright © Baringa Partners LLP 2019. All rights reserved. This document is subject to contract and contains confidential and proprietary information.

4

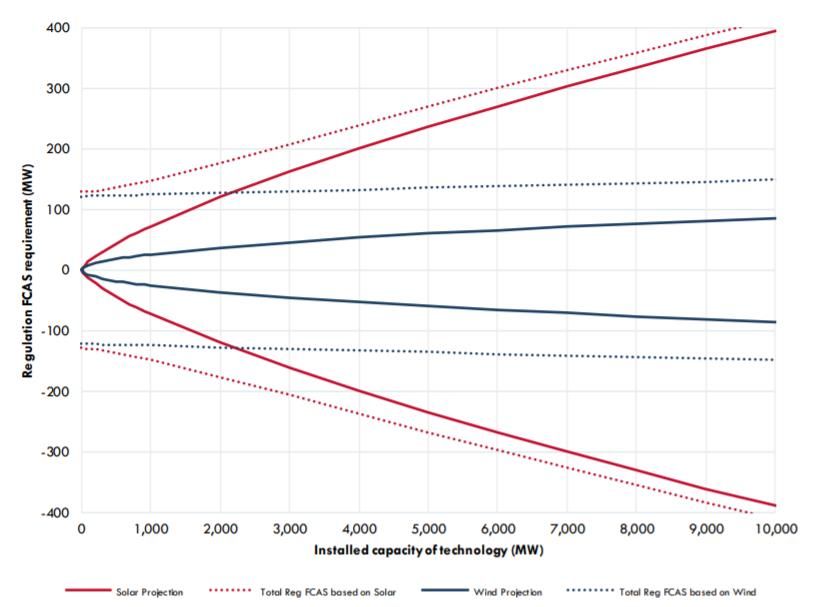

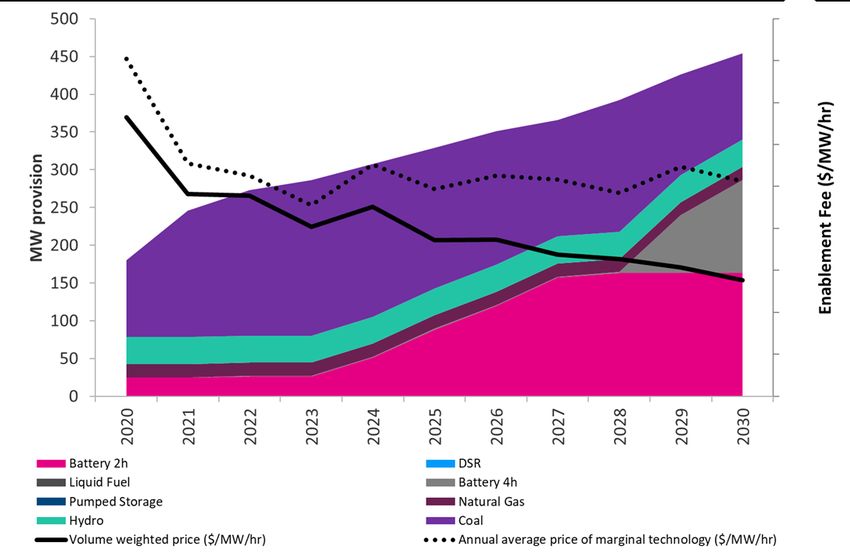

How big is the FCAS market?

While we project a doubling of secondary response requirements in line with increased intermittent renewable

penetration, the market size will remain modest at around 300-400 MW across the NEM

Regulation requirements are linked with variability Projected Regulation FCAS market size

As penetration of intermittent renewables on the system increases, it Reflecting this technical relationship, we can generate a projection of

is expected that the amount of regulation FCAS required to maintain Regulation FCAS over time under our Reference Case

frequency within the Normal Operating Frequency Bounds (NOFB)

We estimate a near-doubling of requirements to 2030

AEMO has mapped this relationship in its Integrated System Plan

Expect intense competition for this 300-400 MW

(ISP) from 2018

Large-scale solar deployment has a more material impact on

Regulation FCAS requirements compared to onshore wind

Source: AEMO, ISP 2018 Source: Baringa Analysis

Copyright © Baringa Partners LLP 2019. All rights reserved. This document is subject to contract and contains confidential and proprietary information. 5

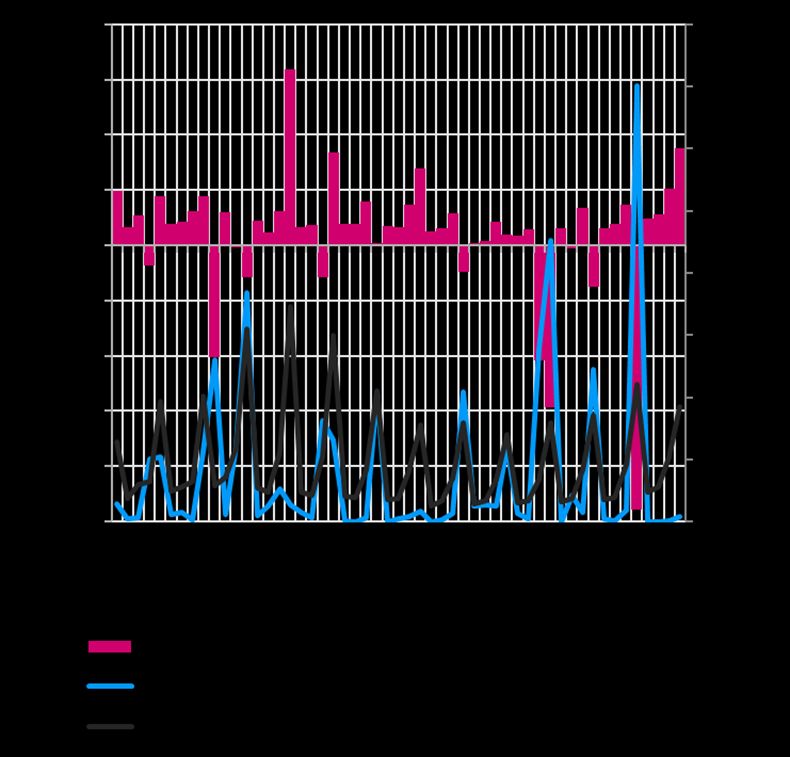

Is FCAS revenue bankable?

While potential revenues for Regulation Raise today are lucrative ($30-40/MW/hr), competition is likely to push prices

lower as thermal plant is displaced by storage competing on opportunity costs. Will the price collapse entirely?

Secondary Frequency response – Regulation Raise

Copyright © Baringa Partners LLP 2019. All rights reserved. This document is subject to contract and contains confidential and proprietary information. 6

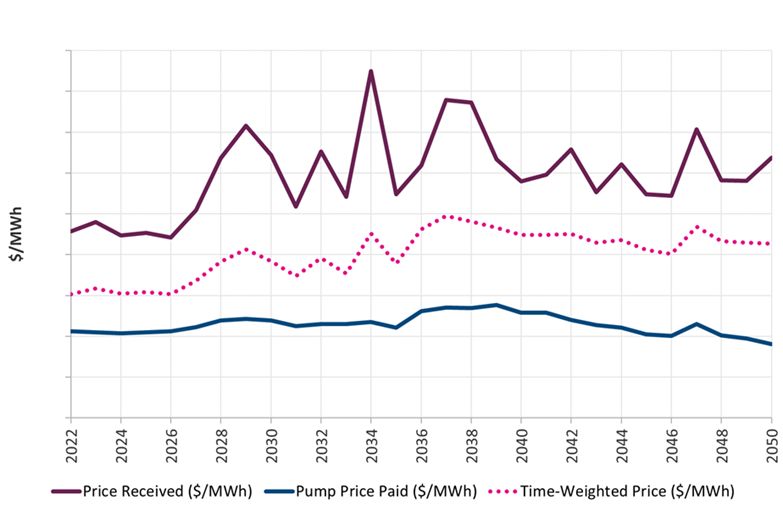

Wholesale arbitrage

Buy low, sell high (and lose some along the way)

Example: QLD pumped storage – characteristic day operations

Copyright © Baringa Partners LLP 2019. All rights reserved. This document is subject to contract and contains confidential and proprietary information.

Baringa Confidential

7

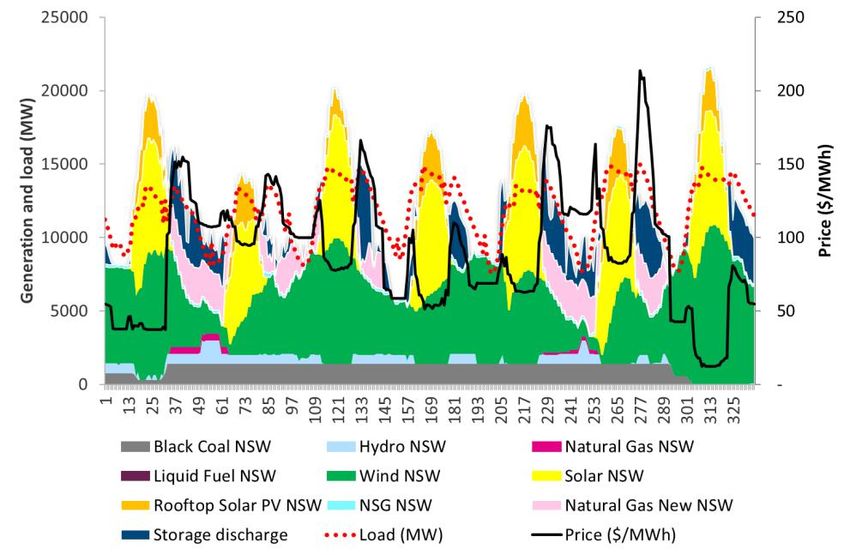

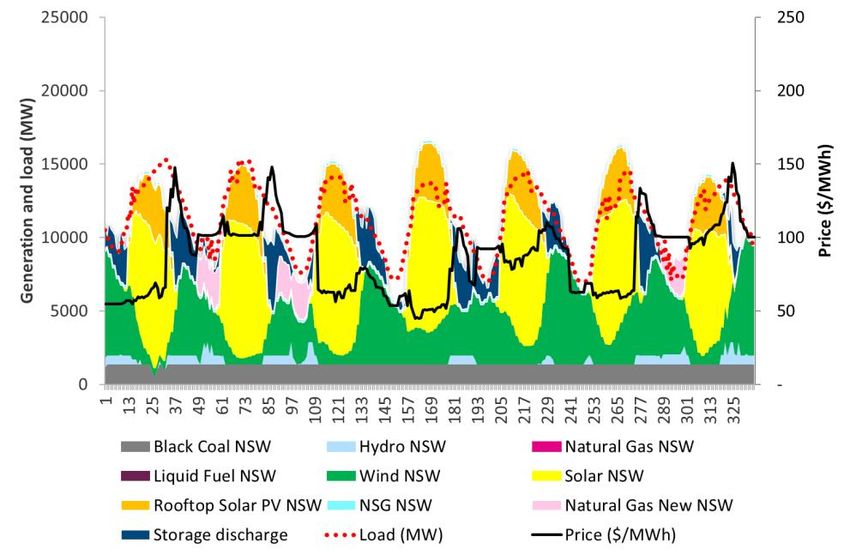

Storage as a key enabler of renewables

In a system with high renewables penetration, storage providing arbitrage is critical to system security and reliability –

shifting output from low-price to high-price periods right across the year

NSW, February 2040 NSW, August 2040

Copyright © Baringa Partners LLP 2019. All rights reserved. This document is subject to contract and contains confidential and proprietary information.

Baringa Confidential

8

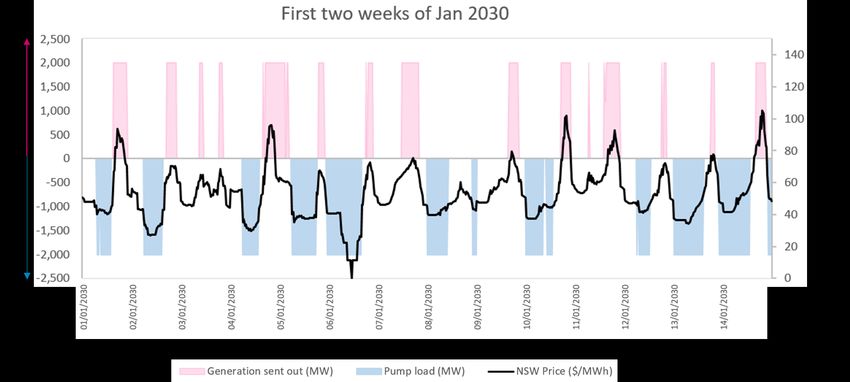

How important is duration?

Longer duration storage such as Snowy 2.0 with one week of reservoir capacity can provide multi-day and every multi-

week arbitrage in the long-term

Example: Snowy 2.0 – characteristic week of operations

Copyright © Baringa Partners LLP 2019. All rights reserved. This document is subject to contract and contains confidential and proprietary information.

Baringa Confidential

9

Banking on arbitrage value

Investors and lenders need to understand the fundamental drivers of price shape and spreads in the market, and how

these could change over time and under different market scenarios

Example: QLD pumped storage – price shape and spreads

Copyright © Baringa Partners LLP 2019. All rights reserved. This document is subject to contract and contains confidential and proprietary information. 10Cap contracts

With its rapid response time, storage can provide cap contract cover to retailers and large customers, and there is

evidence to suggest they are willing to pay for the insurance

QLD cap contract analysis

*The analysis is based on the available data for traded contracts, starting 1st Jun 2004 for the contract ‘QLD BASE QRT $300 Mar05’ (quarter ending Mar 2005)

Copyright © Baringa Partners LLP 2019. All rights reserved. This document is subject to contract and contains confidential and proprietary information. 11Hybrids and firming

Batteries can be physically or virtually co-located with renewables to provide ‘dispatchable’ or ‘firm’ capacity to the

system, and potentially improving the economics relative to a stand-alone renewable system

Example: QLD generation mix and price shape (indicative)

Can hybrid systems enable the creation of a ‘firm’ product from an otherwise intermittent generation source?

Hybrid systems can also enable the shaping of renewable output into fixed clip sizes to reduce trading costs and spot price exposure

This can create a ‘saleable’ product in the market, which may be valuable to a retailer with a fixed retail profile to meet

The economics depend on the value to the retailer within its portfolio, in particular the value of avoided imbalance or spot price exposure

Copyright © Baringa Partners LLP 2019. All rights reserved. This document is subject to contract and contains confidential and proprietary information. 12Is merchant risk investable?

The level of merchant risk to the project can be defined along a spectrum, with innovation required to move

investors and lenders from left to right

Merchant Risk

Debt Leverage

10yr Toll Fixed Price/Volume Cap Contracts Fully Merchant

200

200 200 200

150 150 150 150

$/kW

100 100 100 100

50 50 50 50

0 0 0 0

2021

2024

2027

2030

2033

2036

2030

2024

2021

2024

2027

2033

2036

2021

2024

2027

2030

2033

2036

2021

2027

2030

2033

2036

Volume Risk MLF / Curtailment

Gap in market for structures which share

merchant risk between generator and

offtaker – requires innovation

Baseload Price Risk Volatility

Copyright © Baringa Partners LLP 2019. All rights reserved. This document is subject to contract and contains confidential and proprietary information.

Client Confidential 13Our capabilities on storage

We are able to deploy our industry-leading market modelling approach for the NEM, alongside our deep expertise

and experience with storage asset developers and investors in Europe (both utility-scale and DER)

Dispatch modelling and gross margin projections Strategy, commercial advisory and delivery

Power market modelling and scenario development Storage business model development

– Outlook on the market (Baringa NEM Reference Case – Connection configuration and hybrid options

price projections and report) – Technical capability and assessment of revenue stream

– Development of bespoke market scenarios and eligibility (e.g. arbitrage, cap contracts, FCAS, NSCAS)

sensitivities – Developing revenue stacking models and contracting

– Market due diligence and lender reliance strategies

– MLF and curtailment studies – Behind-the-meter and DER platform strategy

Business case development Commercial advisory

– Asset modelling to produce wholesale arbitrage gross – Assessment and pricing of route to market options

margin projections – Analysis to underpin PPA negotiation and contract

– Long-term projections for other revenue streams structuring

– Revenue stream optimization to produce long-term gross Operating model development

margin projections

– Trading strategy

– Input to assessment of bankability of revenue streams

– Implementation of systems and processes in operation

Copyright © Baringa Partners LLP 2019. All rights reserved. This document is subject to contract and contains confidential and proprietary information.

Client Confidential 14About Baringa Partners Baringa Partners is an independent business and technology consultancy. We help businesses run more effectively, reach new markets and navigate industry shifts. We use our industry insights, pragmatism and original thought to help each client transform their business. Collaboration runs through everything we do. Collaboration is the essence of our strategy and culture. It means the brightest and the best enjoy working here. Baringa. Brighter Together. For more information please contact: Peter Sherry Peter.Sherry@baringa.com +61 457 676 940 Phil Grant Phil.Grant@baringa.com +44 7887 794 204 baringa.com Copyright © Baringa Partners LLP 2019. All rights reserved. This document is subject to contract and contains confidential and proprietary information. 15 Client Confidential

Copyright Copyright © Baringa Partners LLP 2019. All rights reserved. This document is subject to contract and contains confidential and proprietary information. Confidentiality, Limitation and Use Statement This Report has been prepared by Baringa Partners LLP (“Baringa”) specifically for its client named in the Report (“Client”) in order to provide further information to assist in consideration of the potential transaction named in the Report or made known by Client (“Transaction”). This Report is based on publicly available industry data and specific information provided by Client for investors potentially interested in the Transaction (“Investors”). This Report does not constitute a personal recommendation of Baringa or take into account the particular investment objectives, financial situations, or needs of the Investors in relation to the Transaction. Investors should consider whether the content of this Report is suitable for their particular circumstances and, if appropriate, seek their own professional advice and carry out any further necessary investigations before deciding whether or not to proceed with the Transaction. This Report should not, under any circumstances, be treated as a document containing complete and accurate information sufficient to make an investment decision. Baringa shall not be liable in any way for errors or omissions in information contained in this Report based upon publicly available industry data or specific information provided by Client. Baringa makes no representations or warranties (express or implied) concerning the accuracy or completeness of the information contained in this Report, nor whether such information fully reflects the actual situation described in this Report and all conditions and warranties whether express or implied by statute, law or otherwise are excluded. Any investment decisions by the Investors concerning the Transaction should be made on the basis of the Investors’ own conclusions and analyses concerning any assets or securities being acquired or sold and the terms of the Transaction. It is the responsibility of the Investors to conduct such due diligence as necessary of any risk factors not identified in the Report or which could affect the operation, financial standing and further development prospects of any assets being acquired or sold in the Transaction. Nothing in this Report constitutes an offer to sell, or the solicitation of an offer to buy, any assets or securities. Any offer or sale of assets or securities will only be made in accordance with applicable laws and pursuant to definitive agreements. Information and data contained in this Report is confidential and must not be disclosed to third parties without the written consent of Baringa. This Report may not be used in any processes involving the public offering in which shares of stock in a company are sold either privately or on a securities exchange. No part of this Report may be copied, photocopied or duplicated in any form by any means or redistributed (in whole or in part) without the prior written consent of Baringa. Where specific Baringa clients are mentioned by name in this Report please do not contact them without our prior written approval. Copyright © Baringa Partners LLP 2019. All rights reserved. This document is subject to contract and contains confidential and proprietary information. Client Confidential

You can also read