Dutch EV policy in an international perspective - March 2021 - Authors: FIER Automotive & Mobility - Rijksdienst voor Ondernemend Nederland

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Dutch EV policy in an international perspective

March 2021

Authors: FIER Automotive & Mobility

Harm Weken, Edwin Bestebreurtje,

Sascha van der Wilt, Rob Kroon

The aim of this report, which is part of the EU project proEME, is to put Dutch BEV policy in perspective with foreign policies. To do so, Dutch BEV policy is compared with policies in Norway, Germany, and France, but also with Belgium, Sweden, Austria, Denmark, the UK, China and the USA. This research was led by FIER Automotive & Mobility. FIER would like to thank the following people for their contribution to this report: - Robert Kok, Partner at Revnext, the Netherlands - Marco van Eenennaam, Adviseur Public Affairs at ANWB, the Netherlands - Tim Anderson, Group Head of Transport at Energy Saving Trust, United Kingdom - Sveinung André Kvalø, Senior adviser at Department of Analysis and Advisory Services Norwegian EV association, Norway - Ian Faye, Project Manager Powertrain Solutions at BOSCH GmbH, Germany - Gent Grinvalds, Programm Manager at Copenhagen Electric, Denmark - Máté Csukás, Consultant at DBH Group, Hungary - Philippe Vangeel, Secretary General at Avere, Belgium - Maarten van Biezen, Director at RouteZERO, the Netherlands - Rogier Kuin, Manager Public Affairs at BOVAG, the Netherlands - Thijs Duurkoop, Adviseur elektrisch vervoer at Rijksdienst voor Ondernemend Nederland, the Netherlands - Frank Burmeister, Elektrisch Vervoer + Monitoring & Evaluatie Klimaatakkoord Mobiliteit DGMO at Ministerie van Infrastructuur en Milieu, the Netherlands - Hielke Schurer, Adviseur Duurzame Mobiliteit at Rijksdienst voor Ondernemend Nederland, the Netherlands http://www.fier.net © 2021 FIER Automotive & Mobility

Contents

• Management summary

• Success of BEV sales + Effect of BEV policy abroad

The Netherlands, Norway, France, Germany, Belgium, Sweden, Austria, Denmark

• Deep dive in effect of BEV policy abroad

The Netherlands, Norway, France, Germany

• Benchmarking the Netherlands

• Survey on the perspective on BEV

• Analyses of China, USA and UK

• Observations & findings

• Definitions, methods and source references

Management Summery

Management summary:

Observations and findings

General factors in purchasing behaviour Financial / economic

Vehicle availability BEVs have a higher list price than gasoline cars in all

The number of BEV models available is vehicle segments, the difference is relatively highest in

rapidly growing in the last few years, from 17 the smaller segments. The predicted price reductions,

models in 2018, 25 models in 2019, up to seems to go slower than earlier expected. For smaller

41 in 2020. It is noticeable that in all popular Financial / vehicle, car manufacturers sacrifice battery size and

vehicle type segments there is a choice of Available BEV’s hence range to limit somewhat the price differential.

economic

vehicle models. In the past, the decision not

The financial and economic factors are the largest

to buy a BEV because the ‘right model’ was

roadblock for a further increase of the BEV uptake. This is

not available was a valid reason, but this now

discussed in depth on the next pages.

seems to be a lot less applicable. Considering

this, the growing model availability has a

positive impact the BEV sales.

In the Netherlands specifically, the relative Usability of the

growth of BEV models is higher than the Mindset

vehicle Mindset

growth in sales, resulting in a lower average

number of BEV sold per model. In the Netherlands, public opinion on BEVs is shifting

rapidly in favour of BEVs. For instance, the survey

presented in this research showed that only 20% of the

public in the Netherlands opposes incentivizing BEVs

Usability over gasoline powered cars.

Over the last couple of years, the usability of BEVs has massively improved. This is seen in There are, however, still problematic misunderstandings

increased ranges, lowered charging times, and better battery quality. There are also still hurdles that negatively influence the public opinion. The

for BEVs, one of those is the standardization across borders. This is not on the level it should be “Elektrisch rijden monitor” by the ANWB shows that not

yet. Ultimately, usability of BEVs has increase severely, but is not yet on the level of the gasoline enough people know about, and understand the

car. This research showed that with the increase of BEV sales, the number of public recharging incentives in place for BEVs in the Netherlands.

points per BEV is decreasing. Investment in public available recharging points, therefore, remains

necessary.

Management summary:

Overview of incentives for BEVs

Norway France Germany

- BEVs are excluded from CO2 -, NOx -, and - Purchase grant of a max. of €7.000. - VAT was reduced with 3% till the end of ‘20.

weight tax. BEVs are, also in the private - Conversion bonus of €2.500 for scrapping an - Purchase grant increased to a max. of

market, exempted from VAT. old gasoline (

Management summary:

Comparison average purchase price of the Netherlands, Germany, Norway, and France

Observations Purchase price

Extremes in single segments, for instance, the B segment in the Netherlands and France, are € 45.000

caused by the high nett price of BEVs. Also, the batteries are, relative to the nett price of the

car, more expensive in the smaller segments. That causes a bigger difference in the purchase

€ 40.000

price of BEVs and gasoline cars.

Norway exempts BEVs from VAT. This advantage, compared to gasoline cars, gets bigger as the

€ 35.000

nett price increases. Therefore, Norway is the only country in which, on average, BEVs purchase

price for private owners, are cheaper than gasoline cars. Norway is also the only country with

more private- than business BEV sales, although this is slowly shifting. In 2020, the BEV sales € 30.000

in the private market were only twice as high as in the business market, where it used to be

above 95%. € 25.000

The purchase subsidy limit in France shows the effect in the difference between the C and the

D segment, the D segment is not eligible for the purchase subsidy. € 20.000

Most tax systems have a bonus/malus scheme, or a variation on this. The complexity of tax

systems, however, makes it hard to recognise regulations as such. It is important to note, that € 15.000

the “polluter pay’” principle is the basis of the bonus/malus scheme in most countries.

€ 10.000

Business Privat e

Purchase price* € 5.000

B segment C segment D segment B segment C segment D segment

€0

Netherlands incl. subidy

- - - -€ 12.924 -€ 4.668 - ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV

(currently unavailable)

Business Private Business Private Business Private Business Private

Netherlands -€ 12.303 -€ 5.577 -€ 3.661 -€ 16.924 -€ 8.668 -€ 7.724

Netherlands Germany Norway France

Germany -€ 3.901 € 3.809 € 3.001 -€ 5.959 € 3.000 € 2.041 *Note: The deltas of the B segment are disproportionally negative for BEVs. For

selecting the vehicles per segment, the method of the RAI was followed. This

Norway -€ 10.336 -€ 5.457 € 6.881 -€ 5.717 € 113 € 14.814 method was chosen to equalize the method over all countries. However, in the B

segment this method includes luxurious and expensive BEVs, compared to gasoline

France -€ 10.416 -€ 1.559 -€ 6.029 -€ 11.539 -€ 1.030 -€ 8.001 powered cars, such as the BMW i3 and the Hyundai Kona-electric.

Management summary:

Comparison average TCO of the Netherlands, Germany, Norway, and France

Observations Average TCO BEV vs. gasoline cars

The only markets in which the average TCO of BEVs is higher than the average of gasoline cars, € 40.000

are the private markets in the Netherlands and France

The depreciation of BEVs, especially in the private market, is higher than that of gasoline cars in € 35.000

France, Germany, and the Netherlands. In France and Germany, this is partially compensated by

the purchase grants. In the Netherlands, the size of the difference in depreciation between BEVs

€ 30.000

and gasoline cars is really shown. Norway is the only country in which the depreciation of BEVs

is lower than that of gasoline cars. This is caused by the VAT exemption in the private market,

which also stimulates second hand BEVs, keeps the residual value high, and thus the € 25.000

depreciation low. In the business market in Norway, gasoline cars also are not due VAT,

nevertheless, the depreciation of BEVs is still lower than that of gasoline cars. € 20.000

The D segment in the Netherlands and Norway shows the effect of a progressive tax system on

pollution. In these segments, the gasoline cars emit more CO2 than in the B- and C segment, € 15.000

therefore, the benefit of BEVs not having to pay this tax is larger in the D segment. In France

and Germany, the C segment is most beneficial compared to gasoline cars. This is because

these countries do not have a “polluter pays” tax system. € 10.000

€ 5.000

Business Privat e

TCO*

€0

B segment C segment D segment B segment C segment D segment

ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV

Netherlands incl. subidy Business Private Business Private Business Private Business Private

- - - -€ 3.775 € 830 -

(currently unavailable) the Netherlands Germany Norway France

Netherlands -€ 969 € 3.488 € 7.121 -€ 7.775 -€ 3.170 -€ 1.430 Depreciation Energy costs Road tax Insurance Maintenance

Germany € 2.600 € 6.305 € 5.438 -€ 959 € 3.784 € 2.582 *Note: The deltas of the B segment are disproportionally negative for BEVs. For

selecting the vehicles per segment, the method of the RAI was followed. This

Norway € 3.780 € 5.974 € 17.070 € 5.771 € 8.014 € 17.637 method was chosen to equalize the method over all countries. However, in the B

segment this method includes luxurious and expensive BEVs, compared to gasoline

France -€ 26 € 5.075 € 2.086 -€ 3.422 € 2.183 -€ 4.417 powered cars, such as the BMW i3 and the Hyundai Kona-electric.

Management summary:

Taxation on Benefit-in-kind

BiK delta (average between gasoline and BEV)

€ 2.500

€ 2.000

Observations

- Until, and including, 2019, there only was a substantial advantage of

BEVs opposed to gasoline cars in the BiK taxation in the Netherlands and € 1.500

Norway. Germany has only recently adjusted the BiK taxation and

increased the benefit of BEVs over gasoline cars.

- Only the Dutch government is shrinking the advantage of BEVs in the BiK € 1.000

taxation over the last few years, completely opposite to what the other

countries are doing.

Delta in BiK

- The past has proven that in the Netherlands, the impact of the BiK on the € 500

choice of vehicle between a BEV or a gasoline car is significant: A clearly

communicated increase of the BiK percentage on the one hand, leads to

end of year sales impulses, as seen near the end of 2019, and on the

other hand, in case of a strong increase, to a significant and lasting decline €-

of sales in the following years. The logical conclusion, seeing the increase 2015 2016 2017 2018 2019 2020 2021 2022 2023

of BiK taxation on BEVs in 2021, would be that there will be an increase

of BEV sales in the end of 2020, and a decrease in 2021. -€ 500

- It is not the BiK tax percentage that is decisive, but the difference in BiK

tax relative to gasoline cars. As soon as the cost advantage declines too

much, it will be a realistic scenario that the corporate demand will decline, -€ 1.000

and corporate users will opt for gasoline cars.

-€ 1.500

Year

Germany Norway France Netherlands

Management summary:

Observations and findings: Trends in governmental incentives

Trends in governmental incentives

All European governmental organizations discussed in this report encourage the purchase of BEVs. The form of these incentives is

partially forced by the tax systems in place. The incentives can influence either the purchase costs and on the operational costs and can

have an affect on the costs of either the owner or the driver.

BiK taxation on BEVs is disproportionally increased in the Netherlands, compared to the other countries

in this research.

Tax systems with a lower tax burden demand larger subsidy programs to positively impact BEV sales.

Operational

Driver

costs

The Netherlands is decreasing some of the key incentives for BEVs, while other countries are

increasing some key incentives.

Purchase

Owner

costs

Norway mainly incentivizes the private market, the Netherlands mainly the business market. France

and Germany do not make a big distinction between the private- and business market.

There is a limited focus on the occasion market.Management summary:

Observations and findings: Effects of governmental incentives

Effects of governmental incentives (on the purchase price and TCO)

The effects of incentives depend on the incentive, the tax system in place, and contextual factors.

The purchase price is an important determining factor more so in the private market. This is a combination of a limited understanding of the operational costs and

Purchase Price a potential limited upfront investment power.

Emission-based taxes result in higher purchase prices of gasoline cars.

Purchase prices of BEVs are higher across all markets, expect for the private market in Norway.

Purchase grants support BEVs in the least emitting segments.

The TCO is an important determining factor in the private market, but more so in the business market. In the business market the initial investment is less of a

TCO roadblock than in the private market.

Depreciation is the largest cost in the TCO, only Norway has lower depreciation for BEVs compared to gasoline cars.

BEVs in the Netherlands and France have a higher TCO than gasoline cars.

Road tax on emission; higher incentives in high CO2 emitting segments.

The operational costs of a BEV are lower than a gasoline car when used frequently, gasoline cars can have lower operational costs when used infrequent.Success of BEV sales + Effect of BEV policy abroad The Netherlands, Norway, France, Germany, Belgium, Sweden, Austria, Denmark

Success of BEV sales – which factors play a role?

Financial Policy

General factors in purchasing behaviour

The success of BEV sales is determined by VAT reduction or exemption

various factors influencing buying behaviour. For

governmental organisations it is possible to steer

purchase behaviour, mainly by financial policy.

Purchase Purchase tax (NL: BPM)

Financial / costs reduction or exemption

Available BEV’s

economic

BEV fleet worldwide

Purchase and/or leasing

subsidy or other tax advantages Owner

6

Million

5 4,79

Usability of the

4 Mindset Road tax reduction or

3,27

vehicle exemption

3

1,93

2 Operational Excise duty on energy (petrol,

1,18 costs diesel, electricity)

1 0,72 There are different (eco)systems in

0,11 0,22

0,40 the countries discussed in this report,

0 and therefore these factors play a Tax on benefit in kind

2012 2013 2014 2015 2016 2017 2018 2019 different role when countries are (hereafter called BIK) reduction Driver

Source: IEA (2020)

compared. or exemptionEffect of BEV policy abroad

Primary focus

The report starts with a general overview of the different countries Secondary focus

(primary and secondary focus). This general overview includes the

current applicable incentives, the EV uptake over several years, the

growth of public available chargers as well as the top 5 BEVs sold.

This is followed by an in-depth analysis of the Netherlands, Norway,

France, and Germany (primary focus). Here we discuss the

chronology, purchase costs, the “Total Cost of Ownership” (TCO),

and the recharging infrastructure in depth. Within the chronology the

BEV sales per month are plotted against the change of financial

incentives or other relevant events. The identified financial incentives

are put in to perspective by calculating the purchase costs and TCO

of BEVs and gasoline cars.

The purchase price and TCO calculation methods are described in

the section “Methods and source references”.

In the tertiary focus, the UK, the USA, and China are analysed. This

analysis is more general than the primary- and secondary focus.The Netherlands

Overview

Purchase grant Road tax BEV registrations

From July 2020, BEVs in BEVs are exempted from road 70.000 18% Ambitions

the Netherlands were taxes, a plugin hybrid has its 16%

beckoned by a subsidy of road tax reduced by 50%.

60.000 15,3% - By 2030, only zero-emission cars will be sold in

14% the Netherlands.

€4,000 for the purchase of 50.000

12%

a new BEV with a list price 11,6%

Recharging infra 40.000 10%

between €12,000 and

€45,000 and a minimum 30.000 8%

There is no incentive for

range of 120 6% Top 5 BEVs sold '19

individuals, but there are 20.000 5,4%

kilometers. There was a

incentives for companies. 4%

limited budget for this 10.000 Other

Via the MIA, companies can 1,9% 2% Tesla Model 3

subsidy. The subsidy 24%

get an investment deduction of 0,7% 0,7% 1,1%

budget for ‘20 and ‘21 0 0,2% 0,6% 0% 48%

36%. 2012 2013 2014 2015 2016 2017 2018 2019 2020

was exhausted on January

until Kia Niro EV

4th, 2021. BEV

yellow marked bar registration

indicates % BEV in registrations

a significant change

Sept. 6%

Profit tax

yellow marking indicates a significant change

The Netherlands have the MIA Nissan Leaf

Recharging infrastructure (AC & DC) 6%

regulation in which

investments in cleaner Audi e-Tron

70.000 2,5

BiK taxation technology (BEVs) are being 7%

60.000 Hyundai Kona Electric

encouraged by making them 2 9%

Individuals with a BEV have deductible in profit tax. 50.000

a lower percentage of the 40.000 1,5

list price added to their Observations

income when using their 30.000

Registration tax 1

company car also privately. 20.000 - The low taxation on BiK for BEVs has had a

For gasoline cars this is Zero emission cars are exempt 0,5 significant influence on the BEV sales. This is

10.000

22%. For BEVs it was 4%, from paying registration tax. further explained in “Benchmarking the

0 0 Netherlands”.

has risen to 8% in 2020, For other cars, the system is 2012 2013 2014 2015 2016 2017 2018 2019 2020

12% in 2021, and will be progressive, with different until - The ‘stop-and-go’ nature of the incentives

on the same level as levels of CO2 emissions that Sept. regarding BEVs have caused heavy fluctuations in

Number of public recharging points

gasoline cars (22%) in pay different amounts of sales month on month.

2026. registration tax. Number of public rechargepoints per BEVNorway

Overview

BEV registrations Ambitions

70.000 60%

Purchase incentives Road tax - All new passenger cars and light vans sold should

60.000 be zero-emission by 2025

50% 50%

The current Government Norway bases their road tax 46%

has decided to keep the on the type of vehicle. € 41,- 50.000

40%

incentives for zero-emission is the annual road tax for

40.000 Top 5 BEVs sold 2019

cars until the end of 2021. both fully-electric vehicles 31% 30%

This means : and plug-in hybrids, 30.000

• No CO2 tax, 21% Tesla Model 3;

20%

• No NOx tax, 20.000 17% 16% 26%

Other; 32%

• No weight tax, 13%

Recharging infra 10.000 10%

• No VAT. 6%

3%

No federal incentives, only 0 0%

2012 2013 2014 2015 2016 2017 2018 2019 2020

local. Local incentives are all until

around €450,-. BEV registrations % BEV in registrations

Sept. VW e-Golf;

BMW i3; 15%

Registration tax 8%

Recharging infrastructure (AC & DC) Audi e-Tron;

Ownership / circulation tax Nisan Leaf;

BEVs have been exempted 20.000 1 9% 10%

from registration tax since benefits

1990.

Norway bases circulation 15.000

taxes on the type of fuel.

BEVs and PHEVs are 10.000 0,5 Observations

granted a reduction and only

Bik taxation pay a scrapping fee, 249 - BEVs in the private market, for new and used

5.000 cars, competitive with gasoline cars due to the

Euro. The ownership tax will

Taxation of benefit in kind increase to 70% of that of VAT exemption.

is for BEVs reduced to 40% gasoline cars. 0 0

2012 2013 2014 2015 2016 2017 2018 2019 2020

- The low amount of public recharging points is not

until problematic due to the high amount of private

Number of public recharging points Sept. recharging points.

Number of public recharging points per BEVFrance

Overview

Purchase grant Registration tax benefits BEV registrations

Ambitions

BEVs receive a bonus of BEVs are eligible for, either a 80.000 7%

max. €7,000 (up to 27% of 50% discount, or are fully - The French government’s Multiannual Energy

70.000 6,0%

the acquisition cost), when exempt from paying the license

6% Programme aims to increase the current size of

the list price of the car is plate registration (carte grise) 60.000

5% the national e-mobility market twelvefold. The goal

below €45.000. The grant is depending on the region. 50.000 is to have 1,3 million electric vehicles and plug-in

€3,000 when the list price is 4% hybrid electric vehicles on the road by 2023, and

40.000

between €45.000 and Recharging infra 3%

5,3 million by the end of 2028. This goes for

€60.000. 30.000 both private- and commercial vehicles.

2,1% 2%

€300 tax credit on the purchase 20.000

Conversion bonus and installation of a home- 1,4%

1,1% 1,2% 1%

10.000 0,9%

recharger, maxed at %. 0,5% 0,6%

There is a conversion bonus For recharging infrastructure in 0

0,3%

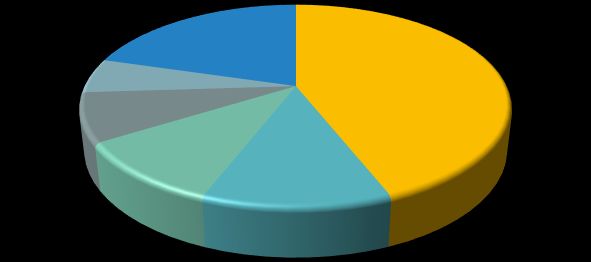

0% Top 5 BEV sold '19

of €2,500 when scrapping a collective living situations, 50% 2012 2013 2014 2015 2016 2017 2018 2019 2020

gasoline car from before is covered with a maximum of BEV registrations % BEV in registrations until Other

yellow marked bar indicates a significant change Sept. 21%

2006, or a diesel car from €1,660 (ex.)

before 2011. This bonus is Kia Niro EV Renault Zoe

€5,000 for low income BiK taxation 4% 44%

households. Recharging infrastructure (AC & DC)

The calculated benefit in kind is

50.000 0,3 BMW i3

reduced by 50% with a yearly 7%

maximum advantage is set at 0,25

40.000 Nissan Leaf

€1800.

0,2 9%

30.000

Tesla Model 3

0,15

15%

20.000

Company profit tax 0,1

Special COVID incentive 10.000 0,05

TVS Tax (Taxe sur les véhicules

Observations

France increased the purchase grant 0 0

from €6,000 to €7,000 due to the de société) is applicable to all 2012 2013 2014 2015 2016 2017 2018 2019 2020

- The share of BEV sales has been quite stable

COVID-19 crisis. Also, the income corporate passenger cars, until until 2020 where new incentives were introduced.

limits for the conversion bonus were except for BEVs. This saves Number of public recharging points Sept.

- The Renault Zoe accounted for almost half the

loosened, however, this was turned companies a couple of hundred

back in August 2020. Number of public recharging points per BEV BEV sales in 2019.

euros.Germany

Overview

Purchase grant Road tax

BEV registrations

For BEVs and fuel-cell vehicles BEVs are exempted from road 120.000 5% Ambitions

the total bonus (federal share + tax during the first five years 4,7%

5% - The German government aims to have up to 10

manufacturer share) is €9.000. after the first registration date. 100.000 million EVs and 1 million recharging stations on

4%

For BEVs with a net list price 4% German roads by 2030.

between €40.000 and 80.000

BiK taxation 3%

€65.000, the total bonus is

60.000 3%

€7,500 and for plug-in hybrid BEVs with a maximum list

1,9% 2%

and range-extended electric

vehicles it's € 5.625.

price of €60,000 (increased 40.000

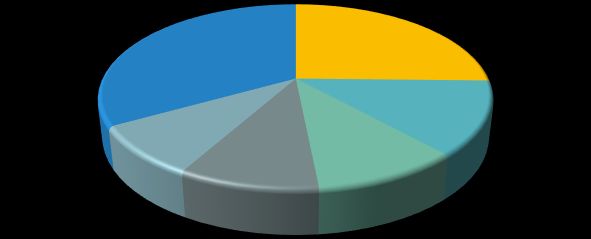

2% Top 5 BEV sold '19

from € 40.000 in June 2020) 1,0% 1%

20.000 Renault Zoe

will receive greater support. 0,7%

1% 15%

Only a quarter of the BiK is 0,3% 0,4% 0,3%

0 0,1% 0,2% 0% Other

taxed (0.25%). 35%

2012 2013 2014 2015 2016 2017 2018 2019 2020 BMW i3

until 15%

BEV registrations % BEV in registrations

Sept.

Ownership / circulation

Tax benefits

Recharging infra

For initial registrations Recharging infrastructure (AC & DC) Tesla Model

from 1 January 2016 Differs per state, as an Smart

50.000 0,5 Volkwagen 3

until 31 December example, Nordrhein- ForTwo ED

e-Golf 15%

2025, there is a tax Westfalen. Individuals get 9%

40.000 0,4 11%

exemption of 10 50% reimbursed for a

years for BEVs charging point, up to max.

€1,000 or €2,500 when

30.000 0,3 Observations

the charging point is 20.000 0,2 - Due to low taxes on car purchases, Germany

“controlled”. The max for cannot give BEVs a lot of tax breaks and must

Special COVID incentive companies, also at 50%, is 10.000 0,1 use a purchase grant as an incentive.

Germany temporarily reduced the VAT set at €1,000 and €3,000

for wall boxes and

- The German automotive sector lobbied for a

rates from 19% to 16% (regular VAT 0 0

charging stations 2012 2013 2014 2015 2016 2017 2018 2019 2020 purchase grant for ICE cars as well but the grant

rate) and from 7% to 5% (reduced remained solely for electric powered vehicles.

respectively. This will be until

VAT rate) for the period from 1 July

Number of public recharging points Sept.

2020 to 31 December 2020. This increased to €2,500 and - There was no dominant model in the BEV sales of

has not been extended. €4,500. Number of public recharging points per BEV 2019.International comparison - Belgium

BEV registrations

10.000 3,0%

2,8% Ambitions

Purchase grant Road tax

2,5% - Only allowing the sale of zero emission vehicles.

(corporate) 8.000

BEV ownership tax €0 or For this there is no specified date.

2,0%

Corporate BEVs and €77,35 (Wallonia, Brussels), 6.000 1,7% - All new bought company cars must be zero

PHEVs are eligible for a compared to diesel € 1.900. 1,5% emission vehicles from 2026 onwards.

purchase grant. If the 4.000

price is under €31,000 Registration tax 1,0%

the grant is €4.000. If 2.000 0,7%

the list price is between BEV is exempted from 0,5% 0,5%

0,4%

0,2% 0,3%

€31,000 and €41,000 registration tax (Flanders) or a

0

0,1% 0,1%

0,0% Top 5 BEVs sold ‘19

the grant is €3,500. If reduced amount applies € 2012 2013 2014 2015 2016 2017 2018 2019 2020

the list price is between 61,50 (Wallonia and Brussels) until Tesla model 3

Total BEV sales % BEV in registrations Overig

€41,000 and €61,000, Sept. 30%

the grant is €2,500. If 36%

Profit tax

the list price is above

€61,000 the grant is BEVs are deductible in profit

€2,000. This grant tax for 120% until 2019 and

Recharging infrastructure (AC & DC) Audi e-Tron

Hyundai 11%

ends in 2020. for 100% from 2020 onwards. 10.000 0,5 Kona BEV Nissan Leaf

7% Renault Zoe

9%

8.000 0,4 7%

6.000 0,3

Observations

4.000 0,2 - The ambitions with regards to company cars are

ambitious. Also, this ambition is for the whole

2.000 0,1 country whereas incentives can differentiate

between Flanders and Wallonia.

0 0

2012 2013 2014 2015 2016 2017 2018 2019 2020 - Belgium has more governmental layers than other

until European countries, this can lead to different

Number of public recharging points Sept. incentive programs in different parts of Belgium.

Number of public recharging points per BEVInternational comparison - Sweden

BEV registrations

18.000 9%

Purchase grant Ambitions

16.000 8,0% 8%

- The Swedish government is banning the sale of

The so-called “super green car 14.000 7%

combustion engines by 2030.

rebate” was replaced in 2018 by a 12.000 6%

bonus-malus arrangement. BEVs get - The Swedish government presented the goal of

10.000 5,1% 5%

a bonus of €5,800 (60,000 SEK) net zero emissions by 2045.

and cars emitting low amounts of 8.000 4%

CO2 get a bonus of €960 (10,000 6.000 3%

SEK). The malus for high CO2 4.000 2,0% 2%

emitting cars is not presented in a

1,1%

higher purchase price but a higher 2.000

0,4%

0,9% 0,8% 1% Top 5 BEVs sold ‘19

annual circulation tax. 0 0,1% 0,2% 0%

2012 2013 2014 2015 2016 2017 2018 2019 2020 Tesla Model 3

until Overig 27%

BEV registrations % BEV in registrations Sept. 33%

BiK taxation

The taxable value of BEVs is Recharging infrastructure (AC & DC)

reduced in two steps. First, the 14000 1,2 Kia Niro EV

Renault Zoe

benefit value is reduced to that of a Nissan Leaf 13%

8% Tesla Model S

12000 1 10%

comparable gasoline car. Until 2020 9%

the calculated benefit value was 10000

0,8

reduced by 40%, but this incentive 8000

is cancelled since 2021. 0,6

6000

0,4 Observations

4000

2000 0,2 - Both the registration of BEVs and the charging

Recharging infra infrastructure have increased year on year.

0 0

Home rechargers are subsidized for 2012 2013 2014 2015 2016 2017 2018 2019 2020 - The benefit for BEVs in the taxation on BiK is

50%, up to a maximum of €960. until reduced as of 2021.

Number of public recharging points Sept.

Number of public recharging points per BEVInternational comparison – Austria

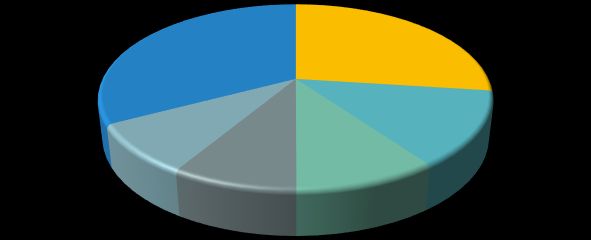

BEV registrations

Recharging infra Other benefits

10.000 6%

Privat individuals can Several other benefits 9.000 Ambitions

5,0% 5%

get €600 for a wallbox, are put in place. EVs will 8.000

- The Austrian government aims to be carbon

this can go up to in the future have higher 7.000

4% neutral by 2040. The ambitious plan includes

€1800 for multi-party speed limits (130 km/h 6.000 heavy decarbonization of the mobility sector.

buildings. instead of 100 km/h) 5.000 3,0% 3%

on designated highways,

4.000

DC charging stations for EVs will be allowed to 2,0% 2%

commercial vehicles, drive on the bus lanes, 3.000

1,5%

with more than 150 KW and will have reduced 2.000 1,2% 1%

output, are eligible for parking fees. 1.000

0,4% 0,5% Top 5 BEVs sold ‘19

up to €30,000 in 0,1% 0,2%

0 0%

subsidy. 2012 2013 2014 2015 2016 2017 2018 2019 2020 Tesla Model 3

until Overig 25%

VAT Total BEV sales % BEV in registrations 33%

Companies with a Sept.

publicly available Company BEVs are

BMW i3

charging infrastructure exempted from VAT Recharging infrastructure (AC & DC) 13%

can receive between (eligible for pre-tax

€300 and €15,000. 10.000 1 Volkswagen

deduction). Hyundai

e-Golf Renault Zoe

9% Kona BEV

8.000 0,8 10%

10%

6.000 0,6

Observations

4.000 0,4 - The VAT exemption for company BEVs is a unique

incentive.

2.000 0,2

- The charging infrastructure almost doubled in the

0 0 first half of 2020.

2012 2013 2014 2015 2016 2017 2018 2019 2020 - An interesting non-monetary incentive is that the

until

Number of public recharging points Sept.

country has introduced higher speed limits for

Number of publicchange

recharging points per BEV

BEVs on certain highways.

yellow

yellowmarked

marked bar

bar indicates aa significant

significant change

yellow marking indicates a significant changeInternational comparison - Denmark

BEV registrations

8.000 6%

Ambitions

7.000 5,3% - The Danish government is aiming to put at least 1

5% million BEVs on the road by 2030. Currently the

6.000

fleet of BEVs consists of around 20.000.

4%

5.000

Registration tax Road tax

4.000 3%

2,6%

Plug-in hybrids In Denmark, the road tax 3.000 2,2%

(PHEV) and battery is based on fuel

2.000

2% Top 5 BEVs sold ‘19

electric vehicles (BEV) consumption and weight

1% Overig

are granted a (further) of the vehicle. BEVs pay 1.000 0,8% 0,7%

0,5% 20%

reduction in the the minimum amount 0,3% 0,3% 0,3%

0 0% Tesla Model 3

calculated registration and PHEVs pay less than 2012 2013 2014 2015 2016 2017 2018 2019 2020 Nissan Leaf

6% 44%

tax of up to DKK an equivalent gasoline Total BEV sales % BEV in registrations until

40,000 in 2020. car. Sept.

BMW i3

PHEVs and BEVs are yellow marking indicates a significant change

8%

granted a reduction in Recharging infra

the taxable value of Renault Zoe Hyundai

Recharging infrastructure (AC & DC) Kona BEV

the car for battery There is an incentive for 10%

12%

capacity of DKK 1.700 commercial charging 3.500 0,6

pr. kWh until the end that is exempted from 3.000 0,5

of 2022. In 2019 and taxes.

2.500 Observations

2020 electric, plug-in 0,4

hybrids and hydrogen Purchase grant 2.000 - Incentives were phased out from 2016 on,

vehicles up to 0,3 collapsing the percentage of BEV sales from

1.500

400,000 DKK paid in Per July 2020 there is no 2,2% to 0,5%.

0,2

practice 0 registration known purchase subsidy 1.000

- Following the growth of BEV sales in 2015, the

tax. available. 0,1

500 number of public recharging points increased in

0 0 2016. In 2019, the BEV sales started to grow

2012 2013 2014 2015 2016 2017 2018 2019 2020 again, but the number of public recharging points

until has not grown. Therefore, the number of public

Number of public recharging points Sept. recharging points per BEV is declining

Number

yellow marked bar indicates of publicchange

a significant recharging points per BEVBudget comparison the Netherlands, Germany, and France

Disclaimer Budget for BEV subsidies

The calculations are done with publicly available data about the budgets.

€25 € 2,000

The budgets for different countries are allocated for different timeframes

Billions

and are often changed along the way. The budgets are calculated back to

one year since the timeframes over which the budgets are allocated differ € 1,800

per country. Displaying one year can lead to a diffused image. The

Netherlands, for instance, used part of its budget of 2021, to subsidize €20 € 1,600

cars in 2020. France and Germany also heightened their budgets for

2020, this was as a response to the Covid-19 crisis.

€ 1,400

This graph only includes the purchase subsidies, it does not include

budgets of other incentives for BEVs, such as the exemption of purchase

taxes. A tax exemption can be a significant incentive for BEVs, especially in €15 € 1,200

Budget per capita

countries where purchase taxes are higher for the more polluting cars.

Total budget

This is, for instance, the case in the Netherlands. € 1,000

€10 € 0,800

Observations € 0,600

- The purchase grants are different over the different

countries. Taking these differences into account, the €5 € 0,400

numbers of cars that can be subsidized are as follows;

€ 0,200

- The Netherlands: 5.823

- Germany: 335.455

€- €-

- France: 177.778 the Germany France United States

Netherlands

Budget per capita Total budgetOverview of incentives for BEVs

Norway France Germany

- BEVs are excluded from CO2 -, NOx -, and - Purchase grant of a max. of €7.000. - VAT was reduced with 3% till the end of ‘20.

weight tax. BEVs are, also in the private - Conversion bonus of €2.500 for scrapping an - Purchase grant increased to a max. of

market, exempted from VAT. old gasoline (Deep dive in effect of BEV policies abroad The Netherlands, Norway, France, Germany Number of BEV sales (chronological) Effect on purchase price and TCO Recharging infrastructure

Method and assumptions of purchase and TCO calculations

The methodology and assumptions for the purchase price and TCO calculation used for the calculations are explained below:

TCO calculation

- A usage period of four years was used in the TCO calculation with the assumption of 28.000 km per year for the business-segments and 15.000 km per year for the private-segments.

- The depreciation is an important part of the TCO and was calculated using the valuation tool INDICATA. The explanation of the calculation on residual value, and thus the depreciation, is

shown on the next slide.

- To eliminate the outliers that cause fluctuation on depreciation, the average depreciation percentages per drivetrain type (BEV and gasoline) over the different segments was used. This

also applies to the depreciation percentages between countries. The differences between the Netherlands, Germany and France were relatively small (BEV occasion market relative to total market

Method

Observations

In this study, we analysed the occasion market for BEVs in 8 different EU markets, with the

Dutch market as a basis. In order to analyse these markets, we used the occasion prices of - The graph depicts the residual value of BEVs, calculated over the BMW i3,

the different BEV-models from the INDICATA valuation tool. The 8 countries in this Volkswagen e-Golf, and Nissan Leaf. The graph shows the average residual value

comparison are Germany, France, Norway, Austria, Belgium, Denmark, Sweden and the curve as an average of the Netherlands, Germany, France, Norway, Belgium,

Netherlands. For the comparison of the prices we analysed the 100% market prices of

November 2020. We analysed BEV-models from 2 different segments: B- and C-segment.

Austria, Denmark, and Sweden.

The specific analysed models are: the BMW i3, the Volkswagen e-Golf, and the Nissan Leaf. - The data behind the residual value slide shows higher residual values, and thus

For the 100% market prices we calculated age (year to market) and mileage (28.000 lower depreciation and a lower TCO, in the more mature BEV-market in Norway.

km/year) similar to all models

Country Occasion portal # BEV # vehicles % BEV / Compared to Note:

presented presented Total BEV% in fleet

Residual value

The depreciation, and with it the

100% residual value, is an essential part

Netherlands Autoscout24.nl 3.800 220.000 1.7% 1,26% of the TCO. It is also the most

90%

difficult part to calculate, especially

80% for BEVs. The BEV market is still

maturing, in size and model

70%

Germany Mobile.de 19.000 1.500.000 1.2% 0,28%

offering. Model A can depreciate

60% more heavily in a certain year than

model B, this is not specific to the

50% BEV market. What is specific to the

40% BEV market, is that this volatility is

France Leboncoin.fr 10.000 905.000 1.1% 0,52% not averaged out by many available

30% models, since only a few second

hand BEVs are four years old.

20%

The residual value calculation

10% creates a unique insight into the

Norway Finn.no 6.600 54.000 12,2% 8,62% BEV depreciation. Although the

0%

0 1 2 3 4 calculation is reliable, the

Vehicle age robustness of the calculation will

increase as the market matures.The Netherlands

Chronology

Observations

Dec 2019: BiK for Purchase

BEV increased from incentive for - There are some large deviations

4% to 8% on 1 consumers: between months in BEV sales with

January 2020 from July 2020 two noticeable peaks;

Dec 2018: Change of BEVs in the

Benefit in Kind Taxation Netherlands - These peaks are both observed in

per 1 January 2019: will be eligible the month before a change in the

• 4% BIK for BEV list for a purchase BiK taxation;

price ≤ €50.000 and subsidy of

22% for > €50.000 €4.000 - It is noticeable that there is a higher

• Before it was 4% of number of sales at the last month of

the total list price the quarter. This is caused by an

increased number of registrations

when the boats with new BEVs

arrive;

- The effect of the purchase subsidies

for consumers is not visible in this

graph yet.The Netherlands excl. €4,000 subsidy

Average Purchase price and TCO from B-, C-, and D segment

Purchase costs TCO costs

€ 45.000

€ 40.000

€ 35.000

€ 35.000

€ 30.000

€ 25.000

€ 25.000

€ 20.000

€ 15.000 € 15.000

€ 10.000

€ 5.000

€ 5.000

€0

Purchase Total tax Purchase Total tax Purchase Total tax Purchase Total tax

-€ 5.000 price and price and price and price and TCO Total tax TCO Total tax TCO Total tax TCO Total tax

incentives incentives incentives incentives -€ 5.000 and and and and

incentives incentives incentives incentives

Gasoline BEV Delta Gasoline BEV Delta

Gasoline BEV Delta Gasoline BEV Delta

Business Private

Business Private

Nett (excl VAT en excl purchase tax) VAT (BTW) Purchase tax (BPM)

Depreciation Energy costs Road tax Insurance Maintenance Total tax and incentives Delta

Total purchase

MIA tax subsidy

advantage Delta Total tax and incentives

Observations

Observations

- BEVs are exempted from BPM, and BEVs in the business market are eligible for an

investment-incentive, the MIA. In both the private- and the business market, this does - There is no road tax for BEVs and BEVs have significant lower energy costs. In the

not compensate the higher nett price of the BEVs compared to gasoline cars. business market, therefore, the TCO of BEVs is +/- €3.000 lower than that of a

gasoline car.

- The difference between gasoline cars and BEVs in bigger in the private market due to

the VAT. BEVs are due more VAT because of the higher nett price. - In the private market, the savings on energy costs are lower than in the business

market because the utilization rate of the vehicles is lower. Ultimately, on average, BEVs

- There was a purchase subsidy of €4.000 available for a short period, but this was not have a higher TCO than gasoline cars in the private market.

used in this calculation due to the low availability and uncertainty.The Netherlands incl./excl. €4,000 subsidy

Average Purchase price and TCO from C segment

Purchase costs private TCO costs private

45.000 35.000

40.000

30.000

35.000

30.000 25.000

25.000

20.000

20.000

15.000 15.000

10.000

€ 8.668

€ 4.668

10.000

5.000

- 5.000 € 3.170

Total tax Total tax Total tax -€ 830

-5.000

and and and -

-10.000 incentives incentives incentives TCO Total tax and TCO Total tax and TCO Total tax and

-5.000 incentives incentives incentives

Gasoline BEV excl. subsidy Delta BEV incl. Subsidy Delta

Gasoline BEV excl. subsidy Delta BEV incl. Subsidy Delta

Private

Private

Nett (excl VAT en excl purchase tax) VAT (BTW) Depreciation Energy costs Road tax Insurance Maintenance Total tax and incentives Delta

Purchase tax (BPM) Total purchase subsidy

Observations

Observations

- Business purchases are not influenced by the purchase subsidy since only private

purchases are eligible for the €4,000 subsidy. - Unlike the initial purchase prices, the TCO for C-segment BEVs is relatively close to that

of gasoline cars. Without the subsidy, the difference is €3.170 over a four year period.

- The purchase costs go down with €4,000 when the subsidy is included in the C With the subsidy included, the TCO over four years is slightly lower for BEVs, namely

segment for private car purchases. BEVs are still €4,668 more expensive than gasoline €830.

cars.Norway

Chronology

May 2015: Jan 2018:

• Governmental announcement to • Local governments

keep existing incentives through Jan 2017: can charge a March 2020: Delivery

2017. Announcement VAT maximum of 50% of new Tesla Model 3

• In 2018, start reducing/phasing exemption extended toll to EV owners.

out incentives to 2020. 50% rule of This to prevent

Observations

• 2018: Local governments entitled maximum tax rate higher rates. - The real growth of BEV sales started

to decide about use bus • Company tax in 2014. From 2014 till 2017 there

lanes/free parking reduction

decreased to 40%

was a steady sales number of 2,000

(was 50%) BEVs per month;

- The number of BEV sales grew since

2017. The average sales in 2019

and 2020 was above 4,000 BEV’s

per month.

2012: Governmental decided to maintain the

existing EV incentives until 2018 or when the

target of 50,000 EVs is reached. In 2018,

start of slowly reducing/phasing out incentivesNorway

Average Purchase price and TCO from B-, C-, and D segment

Purchase costs TCO costs

€ 40.000

€ 35.000

€ 30.000

€ 25.000

€ 20.000

€ 15.000

€ 10.000

€ 5.000

Total tax Total tax Total tax Total tax €0

-€ 5.000 and and and and TCO Total tax TCO Total tax TCO Total tax TCO Total tax

incentives incentives incentives incentives and and and and

incentives incentives incentives incentives

Gasoline BEV Delta Gasoline BEV Delta

-€ 10.000

Gasoline BEV Delta Gasoline BEV Delta

Business Private

Business Private

Nett (excl VAT en excl purchase tax) VAT Scrap deposit tax

Tare weight tax CO2 tax Nox tax Depreciation Energy costs Road tax Insurance Maintenance Total tax and incentives Delta

Observations Observations

- The depreciation of BEVs is in Norway lower compared to other countries. This is partly

- In Norway, BEVs only pay the scrap deposit tax, whereas gasoline cars are also due

due to the maturity of the second hand market. The interest in purchasing second hand

CO2 tax, NOx tax, and the tare weight tax. These tax breaks significantly reduce the

BEVs keeps the depreciation low.

purchase price of BEVs.

- The private market sees a similar pattern as the business market, the difference is the

- Despites the tax breaks, BEVs are more expensive than gasoline cars in the business

lower depreciation of BEVs. This is caused by the VAT exemption for BEVs, gasoline

market. In the private market, BEVs are cheaper than gasoline cars. This is because

cars do pay VAT over the nett price, therefore, the depreciation for gasoline cars is

gasoline cars in the private market have to pay VAT, BEVs are exempted from VAT.

higher. BEVs are ultimately around €10.500 cheaper than gasoline cars.France

Chronology May 2020: Purchase

incentive announcement;

from June 2020 BEVs in

France will be beckoned by a

subsidy of €7,000 (private)

and €5,000 (business)

Aug 2019: Purchase

Jan 2018: Purchase incentive for BEVs

incentive for BEVs still increased up to € 5,000

at €6,000,- Conversion

January 2016:

Conversion program is

bonus for new BEVs to Observations

€2,500

introduced. Jan 2019: Conversion - For a long period (until 2019) there

bonus raised from were stable BEV sales, with a slight

June 2017:

€2.000 to € 2.500 growing trend;

when buying a new-

Conversion bonus - In January and February 2020 there

or second-hand

when buying an EV was a significant growth of BEV

electric- or hybrid car

increased up to

€3,700,-

sales in the first two months;

- After a short fallback, especially June

was a high peak of BEV sales, mainly

caused by new purchase subsidies.

France started in 2008, as one

of the first in the world, with an

incentive program. In 2016, this

bonus was set at €6,300,-.France

Average Purchase price and TCO from B-, C-, and D segment

Purchase costs TCO costs

€ 35.000

€ 40.000

€ 25.000

€ 30.000

€ 20.000

€ 15.000

€ 10.000

€ 5.000

€0

Purchase Total tax Purchase Total tax Purchase Total tax Purchase Total tax

price and price and price and price and

TCO Total tax TCO Total tax TCO Total tax TCO Total tax

-€ 10.000 incentives incentives incentives incentives

-€ 5.000 and and and and

Gasoline BEV Delta Gasoline BEV Delta incentives incentives incentives incentives

Business Private Gasoline BEV Delta Gasoline BEV Delta

Nett (excl VAT en excl purchase tax) VAT Registration Fee Business Private

Total purchase subsidies Delta Total tax and incentives Depreciation Energy costs Road tax Insurance Maintenance Total tax and incentives Delta

Observations Observations

- In the private market, BEVs are roughly €7.000 more expensive than gasoline cars.

- In the business market, the depreciation is higher for BEVs but this is compensated by

Due to the purchase grant, the higher prices of BEVs are compensated to a certain

the lower cost of energy and lower maintenance costs. In the end, BEVs are around

extend but not completely.

€2.500 cheaper in the TCO than gasoline cars.

- The difference in purchase price is not favourable for BEVs because new gasoline cars

- The same goes for privately run cars. The difference is that the utilization rate is not

are taxed rather lightly. France does have a progressive CO2 tax system, meaning that

high enough to offset the higher depreciation of BEVs.

a more polluting car is due higher purchase taxes.Germany

Chronology

June 2020– purchase

subsidy of 9,000 EUR for a

BEV with a basic net list

price of 40,000.

(6,000 EUR Federal share,

3,000 EUR Manufacturer

share)

Jan 2019 – Company car

BiK tax reduction. BEVs Observations

with a gross list price of a - Germany seems to have a relatively

July 2016–

maximum of 60,000

purchase steady growth in the BEV sales

Euros receive greater

subsidy of

support, with only a figures;

4.000 EUR for

BEV and FCEV

quarter of the monetary - The first purchase subsidy of 4.000

advantage being taxed in July 2016 had only a limited

(0,25%).

impact on the BEV sales;

- In the beginning of 2019, there was

an increase in BEV sales, which was

followed with a new increase in the

beginning of 2020.

Nov 2020– purchase subsidy of 6,000

EUR for a BEV with a basic net list

price of 40,000. For PHEV 4,500 EURGermany

Average Purchase price and TCO from B-, C-, and D segment

Purchase costs TCO costs

€ 40.000 € 30.000

€ 30.000

€ 20.000

€ 20.000

€ 10.000

€ 10.000

€0

Purchase Total tax Purchase Total tax Purchase Total tax Purchase Total tax €0

price and price and price and price and TCO Total tax TCO Total tax TCO Total tax TCO Total tax

incentives incentives incentives incentives and and and and

-€ 10.000 incentives incentives incentives incentives

Gasoline BEV Delta Gasoline BEV Delta

Gasoline BEV Delta Gasoline BEV Delta

Business Private -€ 10.000

Business Private

Nett (excl VAT en excl purchase tax) VAT Registration Fee

Depreciation Energy costs Road tax Insurance Maintenance Total tax and incentives Delta

Total purchase subsidies Delta Total tax and incentives

Observations Observations

- Similar to France, Germany has very few taxes on cars. VAT is the only significant - In the private market, BEVs are around €2.000 cheaper than gasoline cars. The

taxation on cars. Therefore, Germany cannot give BEVs tax breaks and had to resort to difference is smaller than in the business market because of the lower utilization rate

a purchase grant of €9.000. and the high depreciation.

- The D segment, BEVs in our calculation are, unlike in other countries with purchase - Noteworthy is the cost of energy in Germany. The difference between BEVs and

grants, eligible for the full grant. That is the reason why the average purchase prices of gasoline cars is significantly smaller than in other countries. The saving of BEVs on

BEVs and gasoline cars are closer to each other than in other countries. energy is, therefore, also considerably lower.Benchmarking the Netherlands Number of BEV sales Effect on purchase price and TCO

Comparison of the BEV yearly sales- and fleet development in the Netherlands,

Norway, France, and Germany

Total BEV sales Total fleet BEVs

100.000 300.000

80.000

200.000

60.000

40.000

100.000

20.000

0 0

2012 2013 2014 2015 2016 2017 2018 2019 2020 until 2012 2013 2014 2015 2016 2017 2018 2019 2020 until

Sept. Sept.

the Netherlands Norway France Germany the Netherlands Norway France Germany

Percentage BEV sales per year In France and Germany, special incentives schemes were launched this year. These

‘Covid-19’ incentives have had a significant positive effect on the purchase price of

BEVs and seem to be effective in sales numbers.

50%

40%

The number of BEV models available is rapidly growing over the last few years. In

the past, an important reason for not buying a BEV, was that the ‘right model’ was

30% not available. This reason seems to be a lot less applicable nowadays, there is an

20% abundancy of BEV models. The number of available models has increased more

10% relative to the increase in BEV sales. Due to the increase in BEV models, there were

fewer BEVs sold per model.

0%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

until Note:

Sept.

the Netherlands Norway France Germany

The information on 2020 is limited since not all data is available. An update in the

next report can, therefore, contain more detailed information. The observations

written on this slide could need adjustments when the data becomes available.

17 BEV models 17 BEV models 25 BEV models 41 BEV models

2017 2018 2019 2020Comparison average purchase price of the Netherlands, Germany, Norway, and

France (1/2)

Observations Purchase price

Extremes in single segments, for instance, the B segment in the Netherlands and France, are € 45.000

caused by the high nett price of BEVs. Also, the batteries are, relative to the nett price of the

car, more expensive in the smaller segments. That causes a bigger difference in the purchase

€ 40.000

price of BEVs and gasoline cars.

Norway exempts BEVs from VAT. This advantage, compared to gasoline cars, gets bigger as the

€ 35.000

nett price increases. Therefore, Norway is the only country in which, on average, BEVs purchase

price for private owners, are cheaper than gasoline cars. Norway is also the only country with

more private- than business BEV sales, although this is slowly shifting. In 2020, the BEV sales € 30.000

in the private market were only twice as high as in the business market, where it used to be

above 95%. € 25.000

The purchase subsidy limit in France shows the effect in the difference between the C and the

D segment, the D segment is not eligible for the purchase subsidy. € 20.000

Most tax systems have a bonus/malus scheme, or a variation on this. The complexity of tax

systems, however, makes it hard to recognise regulations as such. It is important to note, that € 15.000

the “polluter pay’” principle is the basis of the bonus/malus scheme in most countries.

€ 10.000

Business Privat e

Purchase price* € 5.000

B segment C segment D segment B segment C segment D segment

€0

Netherlands incl. subidy

- - - -€ 12.924 -€ 4.668 - ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV

(currently unavailable)

Business Private Business Private Business Private Business Private

Netherlands -€ 12.303 -€ 5.577 -€ 3.661 -€ 16.924 -€ 8.668 -€ 7.724

Netherlands Germany Norway France

Germany -€ 3.901 € 3.809 € 3.001 -€ 5.959 € 3.000 € 2.041 *Note: The deltas of the B segment are disproportionally negative for BEVs. For

selecting the vehicles per segment, the method of the RAI was followed. This

Norway -€ 10.336 -€ 5.457 € 6.881 -€ 5.717 € 113 € 14.814 method was chosen to equalize the method over all countries. However, in the B

segment this method includes luxurious and expensive BEVs, compared to gasoline

France -€ 10.416 -€ 1.559 -€ 6.029 -€ 11.539 -€ 1.030 -€ 8.001 powered cars, such as the BMW i3 and the Hyundai Kona-electric.Comparison average purchase price of the Netherlands, Germany, Norway, and

France (2/2)

Observations Horizontal yellow marking indicates the purchase price incl. subsidy

Extremes in single segments, for instance, the B segment in the Netherlands and France, are

caused by the high nett price of BEVs. Also, the batteries are, relative to the nett price of the Average purchase price BEV vs. gasoline cars

car, more expensive in the smaller segments. That causes a bigger difference in the purchase

price of BEVs and gasoline cars.

€ 40.000

Norway exempts BEVs from VAT. This advantage, compared to gasoline cars, gets bigger as the

nett price increases. Therefore, Norway is the only country in which, on average, BEVs purchase

price for private owners, are cheaper than gasoline cars. Norway is also the only country with

€ 30.000

more private- than business BEV sales, although this is slowly shifting. In 2020, the BEV sales

in the private market were only twice as high as in the business market, where it used to be

above 95%.

€ 20.000

The purchase subsidy limit in France shows the effect in the difference between the C and the

D segment, the D segment is not eligible for the purchase subsidy.

Most tax systems have a bonus/malus scheme, or a variation on this. The complexity of tax

€ 10.000

systems, however, makes it hard to recognise regulations as such. It is important to note, that

the “polluter pay’” principle is the basis of the bonus/malus scheme in most countries.

€0

Business Privat e

Purchase price* ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV

Business Private Business Private Business Private Business Private

B segment C segment D segment B segment C segment D segment

-€ 10.000 the Netherlands Germany Norway France

Netherlands incl. subidy

- - - -€ 12.924 -€ 4.668 -

(currently unavailable)

Nett car price VAT Registration tax

Netherlands -€ 12.303 -€ 5.577 -€ 3.661 -€ 16.924 -€ 8.668 -€ 7.724 Scrap deposit taks (NO) Tare weight taks (NO) CO2 taks (NO)

Nox taks (NO) Total purchase subsidy Purchase price - subsidy

Germany -€ 3.901 € 3.809 € 3.001 -€ 5.959 € 3.000 € 2.041 *Note: The deltas of the B segment are disproportionally negative for BEVs. For

selecting the vehicles per segment, the method of the RAI was followed. This

Norway -€ 10.336 -€ 5.457 € 6.881 -€ 5.717 € 113 € 14.814 method was chosen to equalize the method over all countries. However, in the B

segment this method includes luxurious and expensive BEVs, compared to gasoline

France -€ 10.416 -€ 1.559 -€ 6.029 -€ 11.539 -€ 1.030 -€ 8.001 powered cars, such as the BMW i3 and the Hyundai Kona-electric.Comparison average TCO of the Netherlands, Germany, Norway, and France

Observations Average TCO BEV vs. gasoline cars

The only markets in which the average TCO of BEVs is higher than the average of gasoline cars, € 40.000

are the private markets in the Netherlands and France

The depreciation of BEVs, especially in the private market, is higher than that of gasoline cars in € 35.000

France, Germany, and the Netherlands. In France and Germany, this is partially compensated by

the purchase grants. In the Netherlands, the size of the difference in depreciation between BEVs

€ 30.000

and gasoline cars is really shown. Norway is the only country in which the depreciation of BEVs

is lower than that of gasoline cars. This is caused by the VAT exemption in the private market,

which also stimulates second hand BEVs, keeps the residual value high, and thus the € 25.000

depreciation low. In the business market in Norway, gasoline cars also are not due VAT,

nevertheless, the depreciation of BEVs is still lower than that of gasoline cars. € 20.000

The D segment in the Netherlands and Norway shows the effect of a progressive tax system on

pollution. In these segments, the gasoline cars emit more CO2 than in the B- and C segment, € 15.000

therefore, the benefit of BEVs not having to pay this tax is larger in the D segment. In France

and Germany, the C segment is most beneficial compared to gasoline cars. This is because

these countries do not have a “polluter pays” tax system. € 10.000

€ 5.000

Business Privat e

TCO*

€0

B segment C segment D segment B segment C segment D segment

ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV ICE BEV

Netherlands incl. subidy Business Private Business Private Business Private Business Private

- - - -€ 3.775 € 830 -

(currently unavailable) the Netherlands Germany Norway France

Netherlands -€ 969 € 3.488 € 7.121 -€ 7.775 -€ 3.170 -€ 1.430 Depreciation Energy costs Road tax Insurance Maintenance

Germany € 2.600 € 6.305 € 5.438 -€ 959 € 3.784 € 2.582 *Note: The deltas of the B segment are disproportionally negative for BEVs. For

selecting the vehicles per segment, the method of the RAI was followed. This

Norway € 3.780 € 5.974 € 17.070 € 5.771 € 8.014 € 17.637 method was chosen to equalize the method over all countries. However, in the B

segment this method includes luxurious and expensive BEVs, compared to gasoline

France -€ 26 € 5.075 € 2.086 -€ 3.422 € 2.183 -€ 4.417 powered cars, such as the BMW i3 and the Hyundai Kona-electric.You can also read