Emkay Investment Managers Ltd

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Emkay Investment Managers Ltd Emkay’s 12 An equal weighted twelve stock large cap oriented PMS strategy as on 31st May 2021

Mitigating "Selection bias" and "Allocation bias"

● Mitigating Selection Bias :

» Sticking to the portfolio universe assiduously

» Focusing on compounding themes rather than flavour of the season

» Very high quality standards for companies to be eligible

● Mitigating Allocation bias :

» Concentrated portfolio of a fixed number of high – conviction stocks

» Back the high-quality portfolio with an Equi-Weighted construction

» Re-balancing once a year to avoid concentration risk

» Monitor regularly, prune when required

● Unique framework which seeks to maximize the potential out of a

concentrated portfolio while managing risk

2

Presenting Emkay’s 12 - pioneering the concept of “Smart Alpha” Where every performing stock gets equal attention 3

Mitigating “Selection bias” through a rigorous framework 4

Emkay’s 12 – Key Investment Themes

Value Migration

IT, Chemicals, Unorganised to Organised, Voice to Data etc.

Domestic

Consumption

Auto, Building Materials, FMCG, Consumer Durables, etc.

Domestic

Infra

Cement, Capital Goods, etc.

5

Key Investment Themes : Value Migration

The portfolio seeks to achieve long term capital appreciation by investing in these themes

Beneficiaries

● Value Migration is “the flow of economic and

shareholder value away from obsolete business Low cost

models to new, more effective designs that are producers

better able to satisfy customers’ most important

priorities”

● The framework tries to identify industries where Technology

Value Migration is underway and helps pick leaders

potential winners early in the cycle.

● Few examples: Onshore to Offshore IT services, Efficient

Private banks vs PSU banks, Chemicals, Voice products/

delivery

to Data, Organised vs Unorganised Retail, models

Unorganised lending to Organised lending etc.

6

Value Migration : Reliance Industries

Reliance Industries Nifty 50

Reliance Industries - FY 2020

600

Financial Performance

500 Financial

FY 2020

Performance

400

Revenue (Rs Cr) 5,96,743

300

PAT (Rs Cr) 42,851

200

ROC 10%

100 ROE 9%

0 Market Cap * (Rs Cr) 13,69,605

Jun-15

Jun-16

Jun-17

Jun-18

Jun-19

Jun-20

Mar-15

Mar-16

Mar-17

Mar-18

Mar-19

Mar-20

Mar-21

Dec-14

Sep-15

Dec-15

Sep-16

Dec-16

Sep-17

Dec-17

Sep-18

Dec-18

Sep-19

Dec-19

Sep-20

Dec-20

Price * (Rs) 2,161

7

*As on 31st May 2021

Reliance Industries ● RIL’s strength lies in its ability to build businesses of global scale and execute complex, time critical, and capital-intensive projects which will prove advantageous as it embarks on large investments in all core segments. ● Reliance has changed the dynamics of telecom industries by moving the value of revenues from voice to data through the launch of Reliance Jio.Jio Platforms has expanded its portfolio of services to become a multiplay service provider, equipment supplier, content producer and developer in new technologies (eg. Jio Glass). ● This has forced incumbents to aggressively roll out data networks and re-align their business design/networks from being traditionally tailored for voice to increasingly cater to explosive data demand as data climbs up the consumer priorities list for communication and as market value of telcos increasingly gets linked to data growth. ● Due to value migration, global investors such as Facebook, Google, Qualcomm and Intel have invested in Jio platform. It has raised approximately $20 billion from 13 global investors by selling 32.9% stake. ● With the acquisition of Future Group, the deal adds to Reliance Retail’s offline presence and they get access to wide network, logistics and warehousing business. With control over the value chain, Reliance can beat down prices to earn higher margins. 8

Key Investment Themes : Domestic Consumption

The portfolio seeks to achieve long term capital appreciation by investing in these themes

● India’s GDP is expected to grow from

$2.7tn in FY19 to $5.0 tn by 2024.

● Domestic private consumption as a %

of GDP in FY19E stands at 60% which

is $ 1.6tn.

● The strategy aims to benefit from the

growth in GDP and the attendant

impact on domestic consumption

driven sectors.

● Few examples: FMCG, Consumer

Discretionary, Housing finance,

Auto & Auto Ancillary

9

Source: Emkay Research

Domestic Consumption : Titan Company

Titan Nifty 50 Titan Company - FY 2020

450 Financial Performance

400 Financial

FY 2020

350 Performance

300 Revenue (Rs Cr) 21,051

250

PAT (Rs Cr) 1,501

200

150 ROC 24%

100

ROE 23%

50

0 Market Cap * (Rs Cr) 1,41,593

Jun-20

Jun-15

Jun-16

Jun-17

Jun-18

Jun-19

Mar-15

Mar-16

Mar-17

Mar-18

Mar-19

Mar-20

Mar-21

Dec-16

Dec-14

Dec-15

Dec-17

Dec-18

Dec-19

Dec-20

Sep-15

Sep-16

Sep-17

Sep-18

Sep-19

Sep-20

Price * (Rs) 1,595

10

*As on 31st May 2021Titan Company

● Eye on unorganised: Titan is a specialty retailer with strong presence in jewellery,

watches and eyewear, alongwith fashion accessories and fragrances among others.

Most of the segments are characterized by the presence of significant unorganized market

● Long run way for growth: Titan is a strong play on the consumption theme and rides on the

long term opportunity of rising per capita income, increased discretionary spending, gains from

penetration and premiumization trends. Given Titan has 10% market share in jewellery shows

that it has significant headroom for growth

● Strong Fundamentals: Titan has consistently delivered ROCE of 20%+ and has demonstrated

tremendous discipline in investing the incremental cash in the business that continues to deliver

top quartile ROCE.

11Key Investment Themes : Domestic Infra

The portfolio seeks to achieve long term capital appreciation by investing in these themes

● Infrastructure are the basic systems that

undergird the structure of the economy.

● These systems tend to be capital intensive and

high-cost investments, and they are vital to a

country's functioning, economic development,

and prosperity.

● The strategy aims to identify companies

that are poised to benefit from the rise

in demand for infrastructure in the country

– both retail and institutional spending.

● Few examples: Cement, Capital Goods, etc.

12

Source: Emkay ResearchDomestic Infra : Ultratech Cement

Ultratech Cement Nifty 50 Ultratech Cement FY 2020

300

Financial Performance

Financial

FY 2020

250 Performance

200 Revenue (Rs Cr) 42,125

150 PAT (Rs Cr) 5,747

100 ROC 12%

50 ROE 16%

0 Market Cap * (Rs Cr) 1,93,689

Jun-15

Jun-16

Jun-17

Jun-18

Jun-19

Jun-20

Mar-15

Mar-16

Mar-17

Mar-18

Mar-19

Mar-20

Mar-21

Dec-14

Sep-15

Dec-15

Sep-16

Dec-16

Sep-17

Dec-17

Sep-18

Dec-18

Sep-19

Dec-19

Sep-20

Dec-20

Price * (Rs) 6,710

13

*As on 31st May 2021Ultratech Cement

● Enough room for growth: Ultratech Cement has consolidated cement capacity

of 117mn tonne. With FY20 volumes of 82mn tonne or capacity utilisation of 70%,

Ultratech has enough room to grow volumes without adding new capacities.

● Working aggressively on cost cutting: Ultratech Cement is aggressively working on cutting

costs with recently commissioning 33MW WHRS plant and has already started working on

another 11MW WHRS and also 32MW solar power plant to cut power cost which is 23.6% of

total cost.

● One of the lowest cost manufacturer in India : Ultratech is one of the lowest cost producer

of cement in India. Low cost and premium pricing has helped Ultratech to consistently report

one of the highest EBIDTA/tonne of Rs1000+

● Strong Fundamentals: Ultratech’s RoCE is currently at 11%. However, as the capacity

utilisation rises, the RoCE is expected to improve to 16% by F23. RoIC will be better at 18%.

Despite high capex over last few years, net debt/equity is at just 0.2x and net debt/EBIDTA at

1x. The company is expected to be almost net debt free by FY23.

14Core Investment Framework

Leadership

● Market-share Leadership

● Profit-pool Leadership (Apple vs Rest of the manufacturers)

● Cost efficient Leadership (Export oriented sectors like IT, Textiles, Chemicals)

● Growth Leadership (Companies with best growth in the sector like Private banks vs PSU Banks)

● Product Leadership

● Moat / Niche in the Business

How different is the company?

» Edge, Entry-barrier, Competition, Pricing-power

» Bargaining power of the industry

Discipline

● Identifying Price-Value gap with focus on margin of safety

● Comparative valuations

● Market-cap vs Opportunity size

Excellence

Ambition

Strong Management Credentials

● Track record of past decisions Strong Earnings Visibility & Quality

● Management Comments v/s Delivery ● How big the sector can be (3x, 4x....)

● Futuristic vision ● Revenue/ PAT/ Cash-flow growth

● Avoid aggressive accounting policies ● RoE, RoCE analysis

● Management background ● High operating/ Free cash-flow generation

15Emkay’s 12 A Unique Strategy in the Indian Large cap investment space ! 16

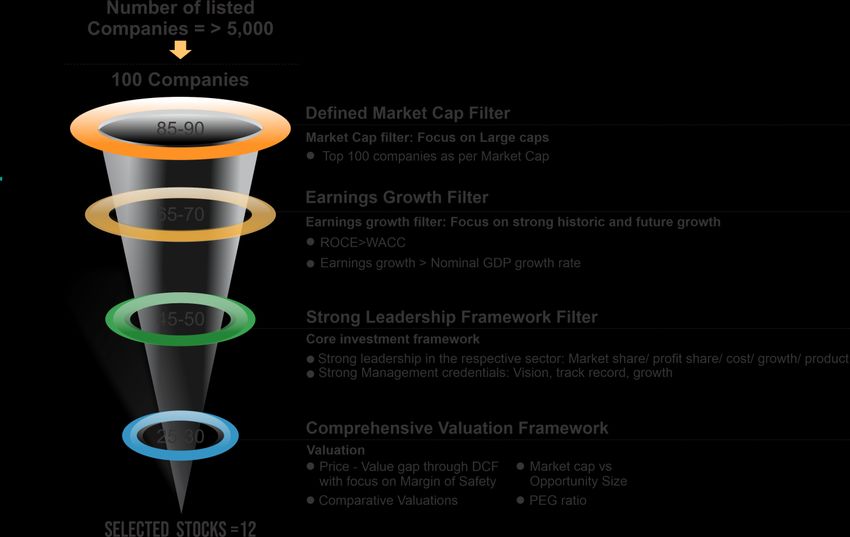

Focus on large and mid cap companies

● >50% exposure in companies with Market capitalization >$ 3 bn

● Investment only in top 100 companies by market capitalization

● Companies with minimum turnover of INR 500 cr

Risk Management

● Equi-weighted portfolio

● >15% price movement in a month triggers review of the stock

Strong risk ● Focus on Liquidity risk

management ● No use of leverage

strategy with ● Monthly portfolio review

focus on

Capital

Diversification across industries and companies

Preservation

● < 30%* exposure in one sector

● GDP growth

17

*At the time of initiationTypical issues faced by conventional large cap MF schemes

● Compressing alpha

» The average alpha generated by large cap schemes has been

3.1% over their respective benchmarks in the last 5 years.

» Large cap schemes have been waylaid by ETFs with shorter timeframes

● High expense ratio

» Regulator defined, rigid expense ratios

● Unwieldy “diversified” portfolio

» Average number of stocks in the top few schemes is 40-50

» Leads to “closet indexing” rather than alpha generation

● Rapid flows in and out of the scheme

» Fund managers have to manage sufficient liquidity most times

18Financial Snapshot – Emkay’s 12 v/s Nifty 50

FY22E

FY2020 Sales Growth (%) Ebitda Growth (%) PAT Growth (%) ROCE (%) ROE (%)

P/E* PEG*

Emkay’s 12 11.9 15.5 29.8 34.1 24.5 34.9 0.8

Nifty 50 0.0 5.7 2.5 10.9 11.4 19.9 0.7

450 Emkay’s 12 CAGR 12%

400

350

300

Nifty 50 CAGR 5%

250

200

150

100

50

0

Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18 Mar-19 Mar-20

Emkay 12 Nifty 50

19

Note: Emkay’s 12 portfolio went live on 1st August’19. The back tested performance data is for

illustration purpose only. All fund data have been rebased to 100 from FY-2010.Emkay’s 12 vis-à-vis leading Large Cap MF schemes

1 Year Monthly Rolling from 2009 (Rolling Return From 29-04-2009 to 31-03-2021)

Emkay 12

Scheme A1 (G) A2 (G) D (G) F (G) H (G) I (G) K (G) S (G) M (G) Nifty 50

(Rebased)

From Apr’09 Apr’09 Jan’10 Apr’09 Apr’09 Apr’09 Apr’09 Apr’09 Apr’09 Apr’09 Apr’09

To 1st April, 2021

Minimum -21.41 -29.73 -20.36 -27.88 -31.10 -34.05 -27.84 -24.56 -27.03 -26.83 -29.20

Maximum 68.41 78.17 56.02 71.12 85.42 74.95 77.66 79.19 82.50 94.54 80.13

Average 15.89 12.24 11.10 10.01 10.70 10.13 13.26 11.10 12.56 16.02 9.72

Std. Deviation 14.22 18.26 14.54 16.01 16.96 21.59 17.16 16.26 18.27 20.45 15.59

No of

Observations 86 85 78 85 85 85 85 85 81 85 86

More than 10% 66.28% 51.76% 55.13% 45.88% 48.24% 42.35% 52.94% 51.76% 55.56% 58.82% 51.16%

More than 15% 50.00% 40.00% 43.59% 34.12% 35.29% 38.82% 42.35% 36.47% 44.44% 42.35% 33.72%

Average of Peers is 11.9% Average of Peers > 10% is 51.4% Average of Peers > 15% is 39.7%

20

Source : Independent analysis done by MSJ MisterBond Pvt Ltd

20Emkay’s 12 vis-à-vis leading Large Cap MF schemes

3 Year Monthly Rolling from 2009 (Rolling Return From 29-04-2009 to 31-03-2021)

Emkay 12

Scheme A1 (G) A2 (G) D (G) F (G) H (G) I (G) K (G) S (G) M (G) Nifty 50

(Rebased)

From Apr’09 Apr’09 Jan’10 Apr’09 Apr’09 Apr’09 Apr’09 Apr’09 Apr’09 Apr’09 Apr’09

To 1st April, 2021

Minimum 4.05 -2.10 0.98 -1.96 -3.10 -8.96 0.75 -2.37 -1.11 0.99 -2.01

Maximum 31.07 28.32 26.44 20.55 22.70 24.57 24.89 24.54 29.50 29.38 20.32

Average 15.54 11.68 12.96 9.09 9.63 8.58 12.14 10.35 12.35 14.51 9.11

Std. Deviation 6.05 7.19 5.54 5.52 6.05 8.06 5.68 6.15 7.99 7.28 4.86

No of

Observations 71 71 64 71 71 71 71 71 67 71 71

More than 10% 85.92% 54.93% 70.31% 39.44% 49.30% 43.66% 71.83% 47.89% 56.72% 71.83% 45.07%

More than 15% 49.30% 28.17% 39.06% 14.08% 19.72% 19.72% 29.58% 25.35% 32.84% 49.30% 8.45%

Average of Peers is 11.25 % Average of Peers > 10% is 56.21% Average of Peers > 15% is 28.65%

21

Source : Independent analysis done by MSJ MisterBond Pvt Ltd

21Emkay’s 12 vis-à-vis leading Large Cap MF schemes

5 Year Monthly Rolling from 2009 (Rolling Return From 29-04-2009 to 31-03-2021)

Emkay 12

Scheme A1 (G) A2 (G) D (G) F (G) H (G) I (G) K (G) S (G) M (G) Nifty 50

(Rebased)

From Apr’09 Apr’09 Jan’10 Apr’09 Apr’09 Apr’09 Apr’09 Apr’09 Apr’09 Apr’09 Apr’09

To 1st April, 2021

Minimum 2.23 -0.69 4.95 -1.72 -1.92 -4.65 0.54 0.20 -0.01 2.69 -0.79

Maximum 26.62 21.02 18.38 15.43 17.18 19.15 20.13 18.12 22.03 23.97 15.36

Average 15.88 13.50 13.18 10.41 11.26 10.59 13.64 11.96 14.07 16.48 9.88

Std. Deviation 5.08 4.52 3.00 3.56 4.00 5.64 4.07 3.46 4.60 4.50 3.27

No of

Observations 55 55 48 55 55 55 55 55 51 55 55

More than 10% 90.91% 80.00% 85.42% 60.00% 65.45% 56.36% 81.82% 72.73% 90.20% 94.55% 56.36%

More than 15% 69.09% 43.64% 31.25% 7.27% 12.73% 27.27% 49.09% 18.18% 52.94% 61.82% 1.82%

More than 20% 21.82% 3.64% 0.00% 0.00% 0.00% 0.00% 1.82% 0.00% 3.92% 23.64% 0.00%

Average of Peers Average of Peers Average of Peers Average of Peers

is 12.79% > 10% is 76.28% > 15% is 33.8% > 20% is 3.67%

22

Source : Independent analysis done by MSJ MisterBond Pvt Ltd

22Significant outperformance over well known Large Cap Mutual Funds

450

10-years performance for the portfolio has been

significantly above well-known Large Cap Mutual Funds Emkay’s 12 CAGR 12%

400

350

300 MF Avg CAGR 7%

250

200

Nifty CAGR 5%

150

100

50

-

Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18 Mar-19 Mar-20

Emkay's 12 Mutual Funds* Nifty 50

23

*Source : Independent analysis done by MSJ MisterBond Pvt Ltd

Note: Emkay’s 12 portfolio went live on 1st August’19. The back tested performance data is for

illustration purpose only. All fund data have been rebased to 100 from FY-2010.Emkay’s 12 - Portfolio Snapshot

Top Sectors

7.2% Financial Services

7.1%

Cement

31.3%

8.7% Oil & Gas

Pharmaceuticals

IT

8.3%

Gems & Jewellery

8.1% 9.6% Specialty Chemicals

9.7% 8.5% Auto & Auto Ancillary

Top 5 Holdings Market Cap

Divi's Laboratories Ltd. 9.7% 1.4%

Ultratech Cement Ltd. 9.6%

Large Cap

ICICI Bank Ltd. 9.3%

Cash

Pidilite Industries Ltd. 8.7%

Reliance Industries Ltd. 8.5% 98.7%

24

*Data as on 31st May 2021Emkay’s 12 Strategy - Performance Update

Emkay'12 (Model Portfolio) Emkay'12 (TWRR)

Nifty Nifty

Outperformance (Model v/s Nifty) Outperformance (TWRR v/s Nifty)

70.0 70.0

60.0 60.0

50.0 50.0

40.0 40.0

30.0 30.0

20.0 20.0

10.0 10.0

0.0

0.0

-10.0

-10.0

-20.0

3M 6M 12M Since

Inception 3M 6M 12M Since

Inception

3M 6M 12M Since Inception

Emkay'12 (Model Portfolio) 9.4 17.0 56.6 22.1

Emkay'12 (TWRR) 9.1 16.4 53.2 19.9

Nifty 7.3 20.2 62.7 21.1

Outperformance (Model v/s Nifty) 2.2 -3.2 -6.1 1.1

Outperformance (TWRR v/s Nifty) 1.9 -3.7 -9.4 -1.2

Inception Date : 1st August 2019 Data as on 30.05.2021

25Emkay’s 12 Strategy : a “Smart Alpha” large cap portfolio

Key features

Portfolio of 12

Focus on risk structural growth

adjusted returns companies

Steady performance

over medium term Possible alternative to

framework Large cap MFs

EMKAY’s

12

Lower portfolio volatility

Low portfolio turnover and high liquidity

• Emkay’s 12 is an equal weighted twelve stock large cap oriented strategy.

• A buy and hold strategy focusing on companies with wider economic moat and dominant position in the sector.

• Combination of value and growth to deliver medium to long term wealth creation.

26Fund Managers – Emkay L.E.A.D.

Kashyap Javeri Fund Manager

Kashyap Javeri is a fund manager with more than a decade of experience in company and sector research.

He brings exceptional insights into stocks and economy. Prior to joining Emkay Investment Managers,

he was a rated BFSI analyst in Emkay Institutional Equities for eight years and also worked with Sharekhan

Ltd as midcap analyst. Kashyap brings with him immense in-depth knowledge on not only variety of

manufacturing and services sectors but also on banking and economics.

Sachin Shah Co-fund Manager

Sachin is a seasoned fund manager with over two decades of experience in the Indian equity markets.

By virtue of his extensive research, Sachin realised early-on the need for a framework in which companies

with evasively tricky standing needed to be filtered out very objectively, leading to the development of E-Qual

Risk, EIML’s proprietary module which helps us to evaluate and compare listed companies on various

aspects of governance. Sachin shares his knowledge and insights through various media interactions across

print and digital platforms.

27Our Team

EGFSL: Emkay Global Financial Services Ltd | EIML: Emkay Investment Managers Limited

28Our reach & research across

~600 Non-institutional Clients ~ 60 Institutional Clients

~260 Stocks Research Coverage ~26 Industries Research Coverage

5 member investment team with collective experience of ~ 60 years

As on 31st May 2021

29About Emkay Global Financial Services Limited 30

Promoters

Krishna Kumar Karwa, Managing Director

A rank holder from the Institute of Chartered Accountants of India (ICAI), Krishna

is the promoter and Managing Director of the Company. He has rich and varied

experience of more than three decades in all aspects of the Equity Capital Markets

and overlooks the Research, Equity Asset Management and Corporate Advisory

divisions at Emkay.

Prakash Kacholia, Managing Director

A qualified Chartered Accountant of the 1987 batch, Prakash is the Promoter and

Managing Director of the Company. He has a rich experience of more than three

decades in the Capital Market and overlooks the Derivatives business and Retail

division at Emkay. He has been on the board of the SEBI Committee on

Derivatives. He has also served as a Director on the boards of Bombay Stock

Exchange Limited, BOI Shareholding Limited and Central Depository Services

(India) Limited.

31The figures speak for themselves

1,44,388 Non-institutional Clients 301 Institutional Clients

305 Stock Research Coverage

16 Sectors (Asset Mgmt, Retail, Insurance

are among the other sectors under coverage)

(Active + Soft coverage)

21 Branches 153 Franchisees

485 Employees Pan India Data as on 30 April 2021

32Collaboration with DBS Vickers Securities

Emkay Global Financial Services Ltd. signed an

exclusive agreement with DBS Vickers Securities

(Singapore) Pte. Ltd., a wholly owned subsidiary of

DBS Bank, the largest bank of South-east Asia, for

sharing of knowledge, co-branding of research and

it’s distribution to the global clients of DBS Vickers.

33Contact Us

Emkay Investment Managers Ltd

7th Floor, The Ruby, Senapati Bapat Marg, Dadar - West, Mumbai 400028. India

CIN: U67190MH2010PLC203819 | PMS: INP000004458

Website: www.emkayim.com

For Sales

Ashu Tomar +91 98673 03861

Samir Merchant +91 99876 06786 | Kyra Ahuja +91 98219 14842

For Support

Namrata Momaya +91 22 6617 5453 | Email: pmsoperations@emkayim.com

Janhavi Surve +91 22 6612 1279 | Email: Janhavi.surve@emkayim.com

Disclaimer: This document has been prepared by Emkay Investment Managers Ltd (EIML) for information purposes only. This document and the

information contained herein shall not be disclosed or reproduced in whole or in part for any other purpose or furnished to any third party without the

express prior written permission of EIML.

EIML does not represent or warrant (express or implied) of any nature nor takes any responsibility or liability of any kind for any error or inaccuracy or any

losses suffered on account of information contained in this document. Information and/or data contained in this document is obtained from sources believed

to be reliable but cannot be guaranteed as to the completeness, timeliness, adequacy or accuracy of the information, hence EIML advises each recipient of

this document to verify the veracity / appropriateness of the information before taking any investment decisions. Past Performance if mentioned herein, is

not an indicator of future performance. Performance related information enclosed in this document is not verified by SEBI.

EIML and its group companies, its directors and employees shall have no liability for any misstatement or omission (by reason of negligence), opinions,

derivations, information or matters (express or implied) contained in the document. Each recipient of this document are advised to consult and/or make its

own independent evaluation and/or investigation before taking any investment decision.

PMS Investment products are subject to market risks, investors are advised to read all the PMS scheme related documents carefully before investment. For

further details, please visit: www.emkayim.com

34You can also read