Eurovision 2021 - Trustnet CMS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

This is not substantive investment research or a research recommendation, as it does

not constitute substantive research or analysis. This material should be considered as

general market commentary.

Eurovision 2021

We highlight potential opportunities within the European investment trust space…

Update

03 February 2021

Europe, despite its intention to put past crises to rest, may end Analysts:

up being a major economic flashpoint in 2021. With sudden

David Johnson

developments in Italian politics, battles over vaccinations and

bonds that guarantee a loss, investors may be forgiven for

expecting the once benign region to be the next big source

of volatility. Yet there is an equal argument for a European Kepler Partners is not authorised to make recommendations

renaissance with pan-European stimulus, attractively valued to Retail Clients. This report is based on factual information

equities and increasing demand for sustainable investing; the only.

argument is not quite as simple as it seems. In this note we aim to The material contained on this site is factual and provided

highlight key data-points and issues which are likely to determine for general informational purposes only. It is not an

near- and long-term returns from European equities. We hope to invitation or inducement to buy, sell or subscribe to

highlight the possibility that European stock markets may be full any product described, nor is it a statement as to the

of opportunities, even if the macro outlook is cloudy. suitability or otherwise of any investments for any person.

The material on this site does not constitute a financial

promotion within the meaning of the FCA rules or the

Political infighting financial promotions order. Persons wishing to invest in

any of the securities discussed in the website should take

their own independent advice with regard to the suitability

of such investments and the tax consequences of such

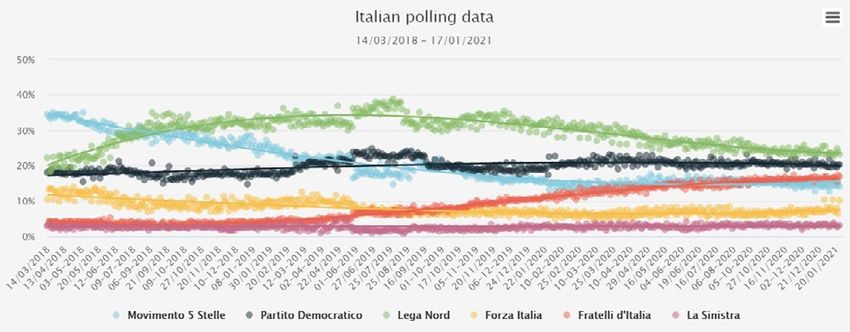

Fig.1: Aggregate Italian Polling Data investment.

Opportunities Trust (JEO), which has a 0% weighting

to Italy. JEO trades at a 10.6% discount and has a

strong track record, although it has suffered from

the fallout from Wirecard’s collapse. JEO’s manager

(Alexander Darwall) prefers to invest in European

countries with global exposure rather than those

sensitive to domestic factors, further insulating JEO

to domestic Europe’s political and broader domestic

Source: Europe Elects, as at 22/01/2021 risks. Political risk won’t stop with Italy though, as

Germany has its next federal election in September

Italy is starting 2021 off with a bang, thanks to the resignation this year, the first election without Angela Merkel

of its prime minister Giuseppe Conte. Having survived two leading the CDU for 16 years.

confidence votes but losing his governing majority after the Italia

Viva party withdrew their small support (they took issue with

Italy’s handling of the crisis), Conte’s resignation is a calculated

Europe may be behind us

gambit in order to build a new majority coalition. Yet it is on vaccines…

nonetheless a gamble, and as recent British politics have shown,

such gambles have the potential to backfire. If 2020 made one thing very clear, it is that Europe

has failed to get a handle on COVID-19. Despite

While Conte remains Italy’s most popular politician, the polls are lockdowns, campaigns and a plethora of fiscal

showing a tightening of support across the major parties, with stimulus to incentivise people to remain indoors,

the right-wing populist party Fratelli d’Italia gaining ground at Europe is still facing the worst wave of COVID-19

the cost of M5S and the Lega Nord, the two incumbent parties. infections yet. The only practical solution to the

Rarely is there any winner during times of political volatility, and pandemic is mass vaccinations, something Europe

so it may be prudent to seek opportunities in strategies with is well behind the curve on when compared to the

a fundamental underweight to the country, such as European UK and the US. If recent headlines are anything to go

Kepler Trust Intelligence is written and published by the investment companies team at Kepler Partners.

Visit www.trustintelligence.co.uk for new investment ideas and detailed thematic research every week. 1

This is not substantive investment research or a research recommendation, as it does not constitute substantive research or analysis. This material should

be considered as general market commentary.

by, expect the region to remain behind the curve as Europe managers, especially in some recovery stories. Of course,

continues to joust with the pharmaceutical giants over its this depends on the course of the vaccination programme,

access to the valuable vaccine. While Europe ‘demands’ which could confound the IMF’s expectations.

AstraZeneca divert vaccines from the UK to the Continent,

we doubt it will be as easy as that. If Europe’s demand for While any European strategy stands to benefit from

vaccines becomes a genuine threat to the UK’s vaccination an economic rebound, those with greater exposure to

programme, the UK may respond with the same export the domestic economy and to European consumers are

restrictions Europe has already enacted, adding further the most likely to outperform during a rebound. This

uncertainty to Europe’s COVID-19 exit plan. includes European small- and mid-cap strategies, such

as European Assets Trust (EAT), as well as those exposed

Fig.2: Vaccines Administered Per 100 People, to economically sensitive sectors, like BlackRock Greater

Per Country Europe Investment Trust (BRGE). BRGE’s investment

universe includes developing Europe, and it is heavily

Vaccines administered per 100 people, per country

01/12/2020 - 28/01/2021

exposed to the region’s high-quality manufacturers,

15

allowing it to capitalise on both the sectoral and regional

recoveries. Despite its wide reach it is a quintessential

Vaccines administered per 100

stock-picker strategy, preferring to focus on corporate

10

fundamentals rather than macro factors, thus allowing

investors to benefit from the broader European recovery

5 without being exposed to unnecessary risks. Conversely,

EAT offers investors a portfolio of high-quality European

small and mid-caps. Despite its high exposure to Germany

0

14. Dec 28. Dec 11. Jan 25. Jan and Sweden (amongst the nations least impacted by

Austria China Denmark France

COVID-19), it still trades at a 9.5% discount, a potentially

Germany Spain Netherlands Ireland attractive entry point for a COVID-19 recovery trade.

United Kingdom United States

everviz.com

Outside of the economic upside, EAT offers investors an

Source: Our World in Data, as at 29/01/2021 attractive yield, with 6% of the NAV paid out as income

annually. We believe that this gives income investors the

…But it retains the edge on ability to take advantage of a potential small-cap rally

without sacrificing yield.

growth

Lower for longer

Fig.3: Developed Europe GDP Growth

And Predictions

Fig.4: Aggregate Nominal Yields Of AAA-Rated

Developed Europe GDP growth European Government Bonds

Spain

Italy

Average nominal yield of 10-year AAA European Government

Portugal issued bonds

France

United Kingdom 06/09/2004 - 22/01/2021

Belgium 6

European Union

Austria

Germany

Netherlands 4

Sweden

Denmark

World

2

%

Finland

Ireland

-14 -12 -10 -8 -6 -4 -2 0 2 4 6 8 10

0

%

2020 2021

-2

everviz.com 2006 2008 2010 2012 2014 2016 2018 2020

Source: IMF, as at 30/11/2020 Yield

While Britain may have the edge on the vaccine roll-out, Source: European Central Bank, as at 22/01/2021

the aggregate impact of COVID-19 on economic output

has been worse for the UK than for the eurozone, as can European yields have long been on a downward path, with

be seen by the above data from the IMF. The forecast the European Central Bank (ECB) having needed to contend

economic rebound is also higher in many European with anaemic growth and low inflation for nearly a decade

countries, which may provide opportunities for fund now. The great inflection point for European interest rates

Kepler Trust Intelligence is written and published by the investment companies team at Kepler Partners.

Visit www.trustintelligence.co.uk for new investment ideas and detailed thematic research every week. 2This is not substantive investment research or a research recommendation, as it does not constitute substantive research or analysis. This material should

be considered as general market commentary.

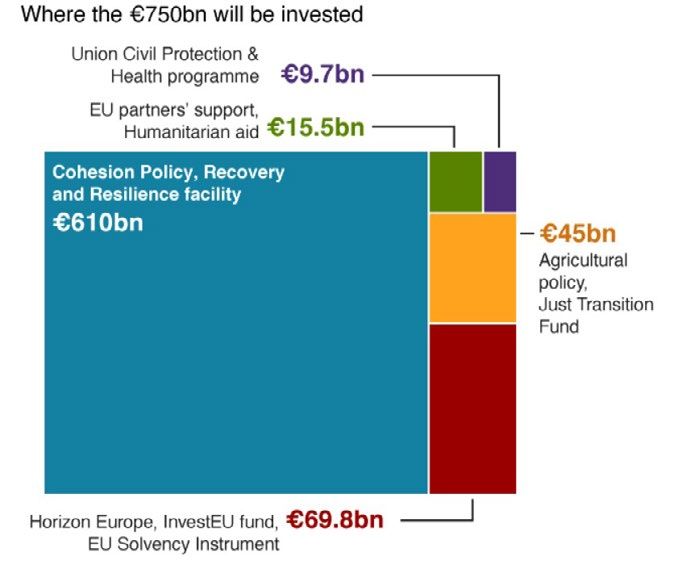

was undoubtably in July 2012, when the then president of The Next Generation EU recovery fund, a €750bn stimulus

the ECB Mario Draghi famously said he would do “whatever package, is a monumental moment for the bloc. While it

it takes” to save the euro. Since then, “whatever it takes” brings a much-needed jab in the arm to the EU economy

has become the catchphrase synonymous with European (although it pales in comparison to the fiscal stimulus

central bank policy, which has been one of near endless being rolled out by the US), what matters more is where

monetary stimulus. While ten-year AAA-rated bonds issued it is invested and how it is funded. The stimulus is funded

by European governments have flirted with negative by the first ever issuance of a common Eurobond, the joint

nominal yields for many years, 2020 finally pushed them debt issuance by the EU member states. This has been the

over the edge. The sudden surge in stimulus, combined white whale of Europe for many years, as the wealthier

with pandemic-induced fear, sent ten-year nominal AAA nations have previously been hesitant to guarantee the

yields firmly into the negative. debt of the poorer nations, but this could ultimately prove

the linchpin in a more united European economy. While the

As more and more European bonds now guarantee short-term impacts are relatively small, such unity could be

investors a loss (even without considering the effects of the first step in a stronger European economy, which may

inflation), equities become an increasingly promising support long-term growth.

investment, given the declining opportunity cost. This

is more the case for growth-orientated investments: as The second potential tailwind from the recovery fund is

bond returns (as well as many equity returns thanks to more specific and relates to how it is targeted, with the

COVID-19) become ever more scarce, companies with lion’s share of the fund being allocated to digital and

strong growth potential become even more attractive. sustainable trends, with at least €250bn and €135bn of

Negative interest rates also make the carry trade (whereby the Cohesion Policy, Recovery and Resilience facility being

investors take out debt at rock-bottom rates and invest it in allocated to each respectively. This opens up a host of

high-yielding equities) increasingly more appealing – and new opportunities within Europe and will make inroads

profitable. There are several growth-focussed investment into securing the region’s sustainability. We expect the

strategies with a high exposure to Europe, such as Martin dedicated environmental strategies, like Jupiter Green

Currie Global Portfolio Investment Trust (MNP), which Investment Trust (JGC) and Impax Environmental Markets

could benefit from the low-rate environment. MNP offers Trust (IEM), to be the most obvious beneficiaries. IEM

a high-conviction portfolio of global equities, with the has been a mainstay of the environmental investing

manager increasingly bullish on Europe’s high-quality (and space, having been launched in 2002, and has been

expensive) consumer goods producers, like Ferrari and consistent in its objective of profiting from the transition

Massimo Dutti. MNP’s long-term outperformance has only to a sustainable future. With a 30% exposure to European

been improved upon by its manager Zehrid Osmani, who equities, it retains a substantial exposure to the tailwinds

joined in 2018, thanks to his forward-looking approach resulting from the recovery fund. With its exposure to

and sophisticated investment process. The quality growth sustainable small and mid caps, IEM offers a unique

bias has been a long-term trend for MNP, which we see exposure to companies which are unlikely to be on

as making it a major beneficiary of the declining-rate the radar of its global peers, or even that of dedicated

environment. European managers. In a similar vein, JGC offers investors

a portfolio of companies offering solutions to the world’s

environmental challenges. JGC also offers investors a

All for one, one for all high exposure to sustainable European companies, with a

43% exposure to the region. JGC has recently undergone

Fig.5: Breakdown Of The Next Generation EU a change in manager, with Jon Wallace taking the helm,

Recovery Fund which we outline in detail in our recent flash update. Jon

is increasingly positioning JGC towards what he believes

are the ‘accelerator’ and ‘innovator’ companies in the

environmental space: those with some of the highest

growth trajectories. We expect such companies to be

squarely in the sights of the recovery fund as Europe looks

to further expand its sustainability industry.

Unlucky in love

European investors can be an odd bunch, despite their

regional pride they seem to have far more love for America

and Asia, at least when it comes to equity funds. As

the above chart shows, European investors have been

Source: BBC

Kepler Trust Intelligence is written and published by the investment companies team at Kepler Partners.

Visit www.trustintelligence.co.uk for new investment ideas and detailed thematic research every week. 3This is not substantive investment research or a research recommendation, as it does not constitute substantive research or analysis. This material should

be considered as general market commentary.

increasing their exposure to the US and Asia more than may be forgiven for their aversion to their domestic

other major regions, including their own. The siren call markets. But as can be seen from the above chart, this

of faster-growing US companies and more dynamic divergence in long-term performance is the widest it has

Asian equities is attractive, and reflects the global been for some readers’ lifetimes. While this divergence is

rotation from value into growth (given the difference in partially reflective of the two regions differing economic

valuations between Europe and the US) as well as Asia’s fundamentals, with past debt crises and lack of growth

better handling of the pandemic. Does Europe’s trend in having dragged on Europe over the last decade, it is also

investment reflect the superior long-term prospects of the reflective of the underlying companies. Europe has lagged

US and Asia, or is it instead an indicator of the recent fear? the US in the emergence of global tech players, and though

If it is indeed driven by short-term returns and fear, there the region does have a few market leaders like ASML and

could in fact be pent-up demand for European equities, Spotify, it is fair to say that European companies fail to

with investors coming home to roost at the first sign of hold a candle to the market dominance and growth of

improving conditions. the US tech giants over the last decade. The question

investors need to ask themselves today is whether there is

Fig.6: Net Asset Growth Of European-Domiciled the potential for this trend to continue: can US companies

Funds, By Sector justify their higher price multiples and continue to push

their markets to new highs, or will Europe close the gap in

Growth in Net Assets of European domiciled funds

a post-COVID-19 rotation into value and cyclicals?

01/2019 - 11/2020

30%

Fig.7: Rolling Ten-Year Relative Returns: US

Versus European Equity Markets

20%

10%

Positive values indicate US outperforms, negative values

0%

%

indicate Europe outperforms.

-10%

Rolling 10 year relative returns: US vs Europe

-20%

1980 - 2020

300

-30%

Jan '19 May '19 Sep '19 Jan '20 May '20 Sep '20

200

Japan Equity UK Equity US Equity

European Equity Asia Equity (inc. China)

100

Source: Morningstar, as at 30/11/2020 0

%

The possibility for a rotation into European equities, or -100

even simply a growth-to-value rotation, translates into an -200

appealing case for European trusts at the widest discounts

(which have the possibility to further enhance returns -300

1990 2000 2010 2020

through a narrowing discount). Such a trust is JPMorgan

Difference

European Smaller Companies Trust (JESC), which trades

at an 11.7% discount, the largest of any European trust Source: Morningstar, as at 31/12/2020

(Source: JPMorgan Cazenove, as at 28/01/2021). This The US equity market reflects the S&P 500, while Europe reflects

discount is arguably unwarranted, given the long-term the MSCI Europe; both are reported in USD.

outperformance of the strategy as well as its disciplined

yet adaptive approach to investing. The managers Riding the green wave

(Francesco Conte and Edward Greaves) have recently

been taking advantage of this flexibility to rotate out of The increased demand for European companies may

defensive companies and into the more cyclical names, not solely be the result of improving economic fortunes,

consciously positioning the trust for a post-COVID-19 but also due to a change in investor preferences. The

recovery. We therefore foresee a potential duo of tailwinds increasing demand for ESG and sustainable investing is

supporting a narrowing of this discount. well documented, as we discussed in a recent strategy

note, with there being an increasing number of dedicated

sustainable strategies or ESG-compliant investment

Mean reversion, or return processes. While these funds aim to cover multiple regions

aversion? and asset classes so as to appeal to a range of risk/return

profiles, the actual variety of sustainable companies is

Given the recent divergence of performance between much smaller. As can be seen in the above pie chart, the

European and American bourses, European investors most sustainable equity strategies (in absolute terms,

not relative) are either located in the Global sector or

Kepler Trust Intelligence is written and published by the investment companies team at Kepler Partners.

Visit www.trustintelligence.co.uk for new investment ideas and detailed thematic research every week. 4This is not substantive investment research or a research recommendation, as it does not constitute substantive research or analysis. This material should

be considered as general market commentary.

in Europe. It is hard to foresee an environment where

corporate cultures and business practices are able to

evolve fast enough to keep up with investors’ demand

for sustainability. We believe that this inflexibility will

ultimately be a tailwind for European equities, as ESG-

conscious investors are increasingly funnelled into

European equities, if for no other reason but for lack of

choice.

Fig.8: Sector Breakdown Of The Most

Sustainable Funds

The most sustainable trusts by sector

Europe

Europe Equity Mid/Small Cap

US

U S Equity Large Cap Blend

Financials

F inancials Sector Equity

Global

G lobal Equity Large Cap

Global Equity Mid/Small Cap

Global

Equity Miscellaneous

Equity

Latin America Equity

Latin

Europe

Europe Equity Large Cap Technology

T echnology Sector Equity

C onsumer Goods &

Consumer

Services Sector Equity

Source: Morningstar, as at 27/01/2021

This data reflects the total number of open-ended equity strategies (excluding REITs) with

a Morningstar sustainability score lower than 20.

As demand for sustainability outstrips supply, we expect

this trend to benefit strategies like Henderson EuroTrust

(HNE), which is amongst the most sustainable trusts in

the AIC Europe sector. What is interesting about HNE is

that its investment process does not require dedicated

ESG integration, for the manager (Jamie Ross) makes a

conscious effort to generate alpha through the positive

impact good governance and sustainability have on his

investments’ revenues. Therefore we view HNE as a perfect

example of the inherent sustainability of the broader

European equity sector. A good sustainability rating does

not come at the cost of returns for HNE, as it has a strong

track record of outperformance versus its benchmark.

Kepler Trust Intelligence is written and published by the investment companies team at Kepler Partners.

Visit www.trustintelligence.co.uk for new investment ideas and detailed thematic research every week. 5This is not substantive investment research or a research recommendation, as it does not constitute substantive research or analysis. This material should

be considered as general market commentary.

Disclaimer

Past performance is not a reliable indicator of future results. The value of investments can fall as well as rise and you may get back

less than you invested when you decide to sell your investments. It is strongly recommended that Independent financial advice

should be taken before entering into any financial transaction.

The information provided on this website is not intended for distribution to, or use by, any person or entity in any jurisdiction or

country where such distribution or use would be contrary to law or regulation or which would subject Kepler Partners LLP to any

registration requirement within such jurisdiction or country. In particular, this website is exclusively for non-US Persons. Persons

who access this information are required to inform themselves and to comply with any such restrictions.

The information contained in this website is not intended to constitute, and should not be construed as, investment advice. No

representation or warranty, express or implied, is given by any person as to the accuracy or completeness of the information

and no responsibility or liability is accepted for the accuracy or sufficiency of any of the information, for any errors, omissions or

misstatements, negligent or otherwise. Any views and opinions, whilst given in good faith, are subject to change without notice.

This is not an official confirmation of terms and is not a recommendation, offer or solicitation to buy or sell or take any action in

relation to any investment mentioned herein. Any prices or quotations contained herein are indicative only.

Kepler Partners LLP (including its partners, employees and representatives) or a connected person may have positions in or

options on the securities detailed in this report, and may buy, sell or offer to purchase or sell such securities from time to time,

but will at all times be subject to restrictions imposed by the firm’s internal rules. A copy of the firm’s Conflict of Interest policy is

available on request.

PLEASE SEE ALSO OUR TERMS AND CONDITIONS

Kepler Partners LLP is authorised and regulated by the Financial Conduct Authority (FRN 480590), registered in England and Wales

at 9/10 Savile Row, London W1S 3PF with registered number OC334771.

Kepler Trust Intelligence is written and published by the investment companies team at Kepler Partners.

Visit www.trustintelligence.co.uk for new investment ideas and detailed thematic research every week.

6You can also read