Studies in Applied Finance - INVESTMENT THESIS FOR INTEL CORPORATION (NYSE: INTC) - Johns Hopkins ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SAF/No.4/June 2016

Studies in Applied Finance

INVESTMENT THESIS FOR

INTEL CORPORATION

(NYSE: INTC)

Vinitha Kumar

Johns Hopkins Institute for Applied Economics,

Global Health, and Study of Business Enterprise

Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

Investment Thesis for Intel Corporation (NYSE: INTC)

By Vinitha Kumar

Disclaimer: These research reports are primarily student reports for academic purposes and are not

specific recommendations to buy or sell a stock. Potential investors should consult a qualified

investment advisor before making any investment. This study was completed in May 2016.

About the Series

The Studies in Applied Finance series is under the general direction of Prof. Steve H. Hanke, Co-Director

of the Johns Hopkins Institute for Applied Economics, Global Health, and Study of Business Enterprise

(hanke@jhu.edu) and Dr. Hesam Motlagh (hnekoor1@jhu.edu), a Fellow at the Johns Hopkins Institute

for Applied Economics, Global Health, and Study of Business Enterprise. This working paper is one in a

series on applied financial economics, which focuses on company valuations. The authors are mainly

students at the Johns Hopkins University in Baltimore who have conducted their work at the Institute as

undergraduate researchers.

About the Author

Vinitha Kumar is a rising senior at Johns Hopkins University double majoring in Economics and Public

Health Studies. She wrote this paper during her time as an undergraduate researcher for the Institute of

Applied Economics, Global Health, and Study of Business Enterprise in the Spring of 2016. Vinitha will

graduate in May 2017.

Abstract

This working paper is an in-depth analysis of Intel Corporation. Our analysis examines on the factors that

impact Intel’s underlying business. This economic analysis is then combined with our proprietary, Hanke-

Guttridge Discounted Cash Flow (HG-DCF) model to determine Intel’s financial position. The HG-DCF

model will be presented along-side Monte-Carlo simulations to reveal the distribution of probable free

cash flows and the likelihood of future earnings. In addition to these quantitative factors, we also examine

the compensation plans of Intel’s executives to assess alignment with shareholders. At the conclusion of

this analysis, it is our intention for readers to understand Intel’s business plan and the company’s financial

standing to arrive at a sound investment decision.

Acknowledgments

I thank Professor Steve Hanke, Dr. Hesam Motlagh, Ryan Guttridge, James Shin, whose original model was

adapted for this thesis, and Abigail Biesman for guidance and draft comments.

Keywords: Financial Modelling, Intel Corporation, Discounted Cash Flow, Free Cash Flow, Monte-Carlo

Simulation, Investment Thesis, Management Compensation

JEL codes: C63, G11

1

Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

Rating – Buy – Projected Free Cash Flow per Share: $37.07

Company Name: Intel Corporation

Date: 5/11/2016

Current Price: $30.06

Fiscal Year End (Current Quarter): Dec. 26 (Q2)

Diluted shares outstanding: 4.875B1

Market Cap: 143.56B

Dividend Yield: 4.1458%

Enterprise Value 145,844.3M

Beta: 0.962

52-week range: 24.87-35.59

2012 EPS 2.13

2013 EPS 1.89

2014 EPS 2.31

2015 EPS (ttm): 2.33

2015 P/E (ttm): 12.79

2016 EPS (P/E) 2.4 (12.53x)3

2017 EPS (P/E) 2.58 (11.66x)

2018 EPS (P/E) 2.68 (11.23x)

Price to Book 2.28

Price to Sales 2.50

1

"Intel Corporation 10-K." SEC. SEC, 2 Feb. 2016. Web. 15 May 2016.

2

"Intel Corporation": NASDAQ:INTC Quotes & News. Google Finance, n.d. Web. 15 May 2016.

.

3

Bloomberg Terminal, search for INTC US Equity, 5/11/2016

2

Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

Contents

Executive Summary: ................................................................................................................................... 4

Risks and Firm Specific Issues: ................................................................................................................. 4

Company Overview: ................................................................................................................................... 5

2016 Overview: ......................................................................................................................................... 6

2015 Overview: ......................................................................................................................................... 6

2014 Overview: ......................................................................................................................................... 6

Goodwill: .................................................................................................................................................. 6

Long-term Asset Turnover and Useful Life: ........................................................................................... 7

Facilities: .................................................................................................................................................. 8

Credit: ....................................................................................................................................................... 8

Model of Company: .................................................................................................................................... 9

Results and Discussion of Model: ............................................................................................................ 10

Execution Risk: ...................................................................................................................................... 12

Analysts’ Recommendations:................................................................................................................. 12

Proxy Report: ............................................................................................................................................ 13

Management Compensation: ................................................................................................................. 13

Base Salary and Cash Bonuses:.......................................................................................................... 13

Long-term Incentive Compensation: ................................................................................................... 14

Total Compensation: ........................................................................................................................... 14

Current Executive Committee: .............................................................................................................. 16

Current Board of Directors and Relative Compensation: .................................................................... 16

Compensation Committee: ..................................................................................................................... 16

Companies in Technology Peer Group: ................................................................................................ 16

Companies in S&P 100 Peer Group:..................................................................................................... 17

Dividend and Share History: ................................................................................................................. 17

Multiples:................................................................................................................................................ 19

Insider Transaction Information: ......................................................................................................... 19

Conclusion: ................................................................................................................................................ 20

*Information in thesis is in tandem with accompanying spreadsheet and data

3Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

Executive Summary:

Intel Corporation (NYSE: INTC) specializes in designing and manufacturing advanced integrated

digital technology platforms. These platforms consist of a microprocessor and a chipset, as well

as optional additional technology and services that could enhance the platform. INTC sells

platforms to various manufacturers and industries, including original equipment manufacturers,

original design manufacturers, and communications industries. INTC’s platforms are used in

notebooks, 2 in 1 systems, desktops, phones, servers, tablets, and retail devices4. The market

currently prices INTC at $30.06, which lies in the middle of its 52-week range ($24.87-$35.59).

This price is lower than the probable free cash flow per share ($37.07) determined through the

Hanke-Guttridge Discounted Cash Flow (HG-DCF) model. Analyst’s 12-month target price is

$35.52, which is also higher than the current market price.5 My recommendation for INTC is to

buy.

During 2015, INTC saw decreased earnings and compressed margins. The Company is now

restructuring to closer match the needs of customers by shifting its concentration on personal

computers (PC) to connected computing devices6. As such, we anticipate that INTC will see a

mean reversion in their margins, asset turnover ratios, and revenues, which will free up cash flow

to shareholders. As INTC restructures, the Company still believes the PC supply chain is healthy.

When completing the HG-DCF, it is important to think of how the financial statements are

connected. The HG-DCF incorporates both the balance sheet and income statement of a company,

and our investment thesis centers on the expanding the balance sheet translating into growth that

the market has not discounted. Their restructuring will be fueled by their recent acquisition of

Altera, a semiconductor company, in Q1 of 2016. This acquisition is expected to help INTC drive

Moore’s Law and the growth in data centers and internet of things (IOT), which will also allow

INTC to provide new classes of products to these market segments.

Risks and Firm Specific Issues:

Change in demand and macroeconomic environment

High competition environment

Defective products, errors in manufacturing

IP risks

Legal, regulatory, and litigation issues

Cybersecurity issues7

4

"Intel Corporation 10-K." SEC. SEC, 2 Feb. 2016. Web. 15 May 2016.

5

Bloomberg Terminal search for INTC US Equity, 5/15/2016

6

Press release on Q1 2016 restructuring, http://www.intc.com/investornews.cfm.

7

"Intel Corporation 10-K." SEC. SEC, 2 Feb. 2016. Web. 15 May 2016.

4Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

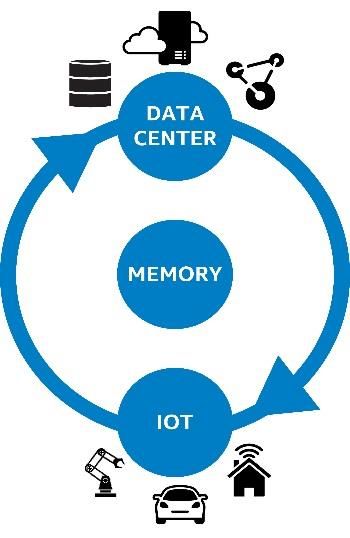

Company Overview:

INTC was founded in 1968 in Santa Clara, California and went public in 1971.8 INTC strives to

offer complete and connected platforms, and to drive “Moore’s Law.” Moore’s Law is the idea

that processor speeds and power will double every two years9. INTC is focused on the,

“personalization of compute,” which refers to the phenomenon that computing is increasingly

becoming personal and incorporated into most aspects of life. In order to develop the

personalization of compute, INTC adheres to three assumptions: sensification of compute, smart

and connected, and extension of you. INTC’s growth strategy is summarized by the virtuous cycle

of growth, which is comprised of data centers, IOT, and memory. IOT and data centers go hand

in hand: as the world grows more connected and “smart,” there will be increased demand for data

and connectivity to devices. Memory will complement data centers and IOT, enabling systems to

be faster and more efficient. Below is a visual representation of INTC’s growth strategy10 (Figure

1). Furthermore, as mentioned previously, INTC recently announced plans to restructure their

initiative to move away from a PC company to a company that focuses on clouds and smart,

connected computing devices. 11

Virtuous Cycle of Growth

Figure 1: Virtuous Cycle of Growth for INTC

Source: "Intel Corporation 10-K." SEC. SEC, 2 Feb. 2016. Web. 15 May 2016.

INTC splits its revenues into operating segments and geography. The operating segments consist

of Client Computing Group (CCG), formerly PC Client Group and Mobile & Communications

Group, Data Center Group (DCG), Internet of Things Group (IOTG), Software and Services, and

other. CCG includes platforms for notebooks, 2 in 1 systems, desktops, tablets, phones, wireless

8

"Intel Timeline: A History of Innovation." Intel. N.p., n.d. Web. 15 May 2016.

.

9

"Moore's Law." Moore’s Law. N.p., n.d. Web. 15 May 2016. .

10

"Intel Corporation 10-K." SEC. SEC, 2 Feb. 2016. Web. 15 May 2016.

11

Press release on Q1 2016 restructuring, http://www.intc.com/investornews.cfm.

5Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

and wired connectively products, and mobile communication components. DCG includes

platforms for enterprise, cloud, communications infrastructure, and technical computing segments.

IOTG includes platforms for the IOT, such as retail, transportation, and home use. Software and

Services includes products that supply solutions, such as security. The other category for both

revenues and expenses include the following: Non-Volatile Memory Solutions Groups (NSG),

New Devices Group, restructuring and asset impairment charges, employee compensation,

divested businesses, and acquisition-related costs12. The geographical segments consist of China

(including Hong Kong), Singapore, United States, Taiwan, and other countries.

Given INTC’s acquisitive behavior, we have outlined recent major transactions below to highlight

their investments into future earnings.

2016 Overview:

In Q1 of 2016, INTC completed the acquisition of Altera. As mentioned, Altera is a semiconductor

company specializing in programmable semiconductors and logic devices, such as field-

programmable gate arrays (FPGAs), as well as System-on-Chip (SoC) devices. In 2016, from Q1

results, net income for the year is annualized to be around $55 billion. Q1 earnings were $13,702

million, which is higher than 2015 Q1 earnings of $12,781 million. The business appears to be

cyclical, as earnings for 2015 were more than four times Q1 earnings. For consistency with the

model, 2016 Q1 numbers were annualized by multiplying the amount by four. Using this metric,

however, may not accurately represent INTC’s future sales, and therefore the model’s estimate for

2016 annualized revenue could be an underestimate.

2015 Overview:

During 2015, INTC completed eight acquisitions, which aggregated to a cost of $1.0 billion. Most

of these acquisitions were financed with cash and accounted for in goodwill or other intangible

assets. A significant acquisition in 2015 was the acquisition of Lantiq Semiconductor, which will

complement INTC’s cable home gateways into digital subscriber line (DSL) and fiber markets.

The revenue generated from these business services fall under their client computing group. INTC

also completed three divestitures transactions in 2015, generating $153 million.

2014 Overview:

During 2014, INTC completed eight acquisitions, for a total cost of $963 million. The

acquisition of Axxia Networking Business of Avago Technologies Limited, will complement

INTC’s mobile wireless base station business. The revenue generated from these business

services fall under their data center group. INTC divested the assets of Intel Media to Verizon

Communications Inc. in 2014 as well13.

Goodwill:

As a result of years of acquisitions, INTC has steadily grown its Goodwill. Below is a chart of

their Goodwill since 2011 (Figure 2). Goodwill represents the excess in fair value of a business’s

assets that accounts for its intangible value and brand name value. It is important to monitor a

company’s impairment of Goodwill to assess whether or not it is pricing its acquisitions correctly.

12

"Intel Corporation 10-K." SEC. SEC, 2 Feb. 2016. Web. 15 May 2016.

13

"Intel Corporation 10-K." SEC. SEC, 2 Feb. 2016. Web. 15 May 2016.

6Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

INTC combines its asset impairment with its restructuring charges. This amount has increased

from 2013 to 2015, but this could be a result from their 2013 and 2015 restructuring programs.

Figure 2: INTC’s Goodwill

Source: "Intel Corporation 10-K." SEC. SEC, 2 Feb. 2016. Web. 15 May 2016.

Graph made by Vinitha Kumar

Long-term Asset Turnover and Useful Life:

As previously explained, INTC’s long-term asset turnover (LTAT) makes them a unique case to

assess. LTAT shows how efficiently a company is utilizing their asset base to generate revenues.

The following chart shows both their LTAT and useful life historically, and projected through the

HG-DCF. Recently, INCT’s LTAT has been decreasing. This is a result of their acquisitions and

higher amounts of assets, while having similar revenues each year. However, the HG-DCF

demonstrates that if there is a mean reversion of LTAT to historic levels (i.e. INTC is effective in

integrating these assets), these acquisitions will increase future revenues over time (see past red

line on figure below).

7Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

INTC LTAT and Useful Life

10.00

9.00

8.00

7.00

6.00

Value

5.00

4.00

3.00

2.00

1.00

0.00

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Years

LAT Useful Life

Figure 3: INTC’s LTAT and Useful Life

Source: "Intel Corporation 10-K." SEC. SEC, 2 Feb. 2016. Web. 15 May 2016.

Graph made by Vinitha Kumar, projections after 2016 determined through HG-DCF

Facilities:

While INTC leases a few of their facilities, it owns the majority of them, giving the Company

significant intrinsic value. Table 1 highlights the facilities INTC owns versus what it leases and

where.

(Square Ft in Millions) United States Other Total

Countries

Owned facilities 30.7 17.2 47.9

Lease facilities 2.1 6 8.1

Total facilities 32.8 23.2 56

Table 1: INTC’s Facilities

Source: "Intel Corporation 10-K." SEC. SEC, 2 Feb. 2016. Web. 15 May 2016.

Credit:

Table 2 below shows various companies’ credit rating for INTC, demonstrating that INTC’s debt

is not distressed.

Company Credit Rating

Morningstar AA-

Moody’s Stable, A1 (for long term and

senior unsecured debt)

8Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

Standard & Poor’s Stable, A+ (for long term

debt)

Fitch Stable, A+

Egan-Jones Rating Company A+

Table 2: INTC’s Credit

Sources:

"Intel Corp." INTC Debt, Bond, Rates, Credit. Morningstar, n.d. Web. 15 May 2016.

.

Bloomberg Terminal, search for INTC US Equity, 5/15/2016

Model of Company:

The primary difficulty in modeling INTC was estimating its future growth revenue, as INTC’s

separate business segment revenues fluctuate significanty year to year and change often. Thus, it

is difficult to estimate what the segment will generate in the future given the growth in certain

segments and the secular headwinds faced in the PC markets. Historical averages and compounded

annual growth rates were used to project future revenues. The final growth estimate used for the

HG-DCF was the 10-year compounded annual growth rate from projecting segment data. Below

is the table of historical averages and numbers used to project revenue by segment.

The final growth rate used for the HG-DCF was 4.95%. This growth rate relies on the assumption

that there will be a mean reversion in revenues from all of INTC’s recent acquisitions which we

believe is realistic. For example, the acquisiton of Altera is expected to drive growth in the Data

Center Group and the IOT Group. As seen below, the growth rates used to project revenue in these

segments are much higher than other segments.

Note: this growth rate may overestimate the revenue growth rate in the near future, and thus the

future projected free cash flow per share. The model is very sensitive to assumed growth rates

which we address with our Monte Carlo simulation in subsequent sections.

2016

2011 2012 2013 2014 2015

Segments Q1A Average Assumed CAGR St Dev.

Client Computing Group

32,219 30,196

(CCG)

% growth (6.28%) -6.28% -3.19% -3.19% 0.00%

PC Client Group 35,624 34,688 33,270 34,669

% growth (2.63%) (4.09%) 4.20% -0.84% 0.00% -0.68% 3.61%

Data Center Group 9,911 11,219 12,161 14,387 15,977 15,996

% growth 13.20% 8.40% 18.30% 11.05% 0.12% 10.21% 10.21% 8.31% 6.00%

Internet of Things Group - 1,600 1,801 2,142 2,298 2,604

% growth 12.56% 18.93% 7.28% 13.32% 13.02% 13.02% 10.23% 4.13%

Mobile &

Communications - 1,791 1,375 202

Group

-

(23.23%) (85.31%)

% growth -54.27% 0.00% 51.68% 31.04%

Software and services 1,870 2,072 2,190 2,216 2,167 5,812

% growth 10.80% 5.69% 1.19% (2.21%) 168.20% 3.87% 12.34% 20.80% 65.88%

All other 6,594 1,971 1,911 2,254 2,694 200

9Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

-

(70.11%) (3.04%) 17.95% 19.52% (92.58%)

% growth -25.65% -25.65% 44.16% 46.71%

Total net revenue 53,999 53,341 52,708 55,870 55,355 54,808

% growth (1.22%) (1.19%) 6.00% (.92%) (.99%) 0.34% 0.34% 0.25% 2.83%

Table 3: INTC Revenue Growth

Original calculated by James Shin, adapted and updated by Vinitha Kumar

Further, capital expenditures (CAPEX) was set to depreciation and amoritization (D&A) levels.

This assumes that INTC will replace its capital at the rate of its D&A levels. Although historically

INTC has made strategic acquisitions, this assumption relies on INTC focusing on translating

previous acquisitions into revenues, and reducing the rate at which it acquires companies. In 2015,

INTC saw high levels of CAPEX (42.73%). However, keeping up this rate with acquisitions is

unrealistic. The assumed rate used in the HG-DCF was 14.39%. This assumption is validated from

its restructuring efforts to transform its company and its focus on the recent acquisiton of Altera

to help its movement.

Results and Discussion of Model:

The probable free cash flow per share determined through the HG-DCF was $37.07, compared to

a market price of $30.06. In order to estimate this price, margins and revenue were projected using

historical data. These projections and assumptions can be found in both the revenue growth tab

and the Hanke-Guttridge Free Cash Flow (HG-FCF) page. Below is a summary of the HG-FCF,

which shows the Company’s various value drivers (Table 4).

The HG-FCF shows that INTC has stable margins, as all the standard deviations are low, with the

exception of CAPEX. Stable margins indicate good management and consistency in management

decisions.

Although historical LTAT has been decreasing, it is expected, through the HG-DCF, to begin

increasing as more revenue is generated with the asset base reflecting management’s ability to

integrate these assets into the business. Although useful life is historically increasing, it is expected

to decrease through the HG-DCF beacuse the model assumes that D&A and CAPEX grow at the

same rate so the asset base will stay the same.

A Monte-Carlo Simulation was performed to assess the projected free cash flow per share and its

probable distribution. The current price falls between the 20th and 30th percentile of the simulation

(see Figure 4 below). This indicates that we anticipate INTC’s shares to be underpriced. With the

probable free cash flow being $37.07, 23.33% higher than its current price, and the current price

falling to the left of the distribution, there appears to be an upside: this distribution supports the

hypothesis that the market is not pricing INTC correctly to account for its future mean reversion

and increased value.

10

Table 4: INTC HG FCF and Value DriversInvestment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

Std.

Year 2011 2012 2013 2014 2015 2016

Average Dev.

Net revenue 53,999 53,341 52,708 55,870 55,355 54,808

54,347 1,214

% growth (1.22%) (1.19%) 6.00% (.92%) (.99%) 0.34% 2.83%

Cost Structure (as % of net revenue)

Cost of goods sold, net D&A 26.26% 23.75% 24.96% 20.96% 21.62% 25.96% 23.92% 2.03%

R&D 15.46% 19.02% 20.13% 20.65% 21.91% 23.69% 20.14% 2.55%

Marketing, general & administrative 14.20% 15.10% 15.34% 14.56% 14.33% 16.25% 14.96% 0.70%

Restructuring & asset impairment

0.00% 0.00% 0.46% 0.53% 0.64% 0.00%

charges 0.27% 0.28%

EBITDA (as % of net revenue) 44.08% 42.12% 39.11% 43.30% 41.51% 34.10% 40.70% 3.34%

Gains (losses) on equity investments,

net 0.21% 0.26% 0.89% 0.74% 0.57% 0.16%

(as % of net revenue) 0.47% 0.28%

Interest and other, net (as % of net

0.36% 0.18% (0.29%) 0.08% (0.19%) (0.60%)

revenue) -0.08% 0.32%

Income tax provision (as % of

20.33% 17.22% 14.51% 16.94% 12.15% 9.89%

EBITDA) 15.17% 3.45%

Cash flow drivers (as % of net

revenue)

Change in working capital 2.26% 5.43% (6.59%) 0.40% (4.69%) -0.64% 4.43%

Capital expenditures 28.62% 29.05% 22.27% 13.10% 42.73% 27.16% 9.69%

D&A (as % of net revenue) 11.23% 14.10% 15.24% 15.30% 15.74% 14.71% 14.39% 1.50%

11Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

Execution Risk:

The Monte-Carlo distribution helps to assess the execution risk of investing in INTC. From the

figure, there appears to be more upside than downside. There is, however, the risk that the

assumptions in the HG-DCF are wrong. For example, INTC could acquire companies, as it did in

2015, and cash flow would not be freed for shareholders. Alternatively, the macroeconomic

environment could worsen and revenue growth could either decline or plateau in addition to

management failing to properly integrate these assets to generate meaningful revenue.

Analysts’ Recommendations:

As stated before, Bloomberg reports that analysts have a target price of $35.53 for INTC, giving a

return potential of 18.8%. The following graphic reviews various analysts’ recommendations on

INTC (Figure 5). 56.8% of firms recommend a buy, 36.4% recommend a hold, and 6.8%

recommend a sell. Therefore, there is not a general consensus on INTC being a buy, but most

analysts predict INTC will either keep up with the market or outperform it.

Figure 5: Analysts’ Recommendations

Source: Bloomberg Terminal. Search for INTC US Equity, 5/15/2016

Given that our investment thesis is predicated on the mean-reversion of future asset turns, we

opted to investigate management compensation and determine if executive incentives are aligned

with our projections.

12Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

Proxy Report:

Management Compensation:

Base Salary and Cash Bonuses:

The total base salary of all 5 executives in 2015 was $4,165,000. The main portion of cash

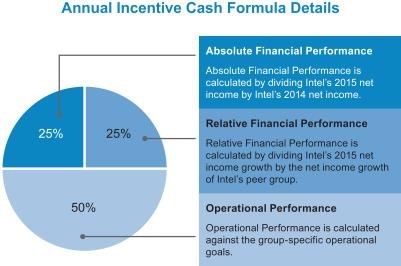

payments are annual incentive payouts based on various measures of company performance. Due

to lower financial earnings in 2015, incentive cash payouts were lower in 2015 than in 2014.

Whereas in 2014 the payout was 122% of the target, the payout in 2015 was 94.3% of the target.

Figure 6, below, details how annual cash incentive payments are calculated. The calculation

includes inspecting changes in net income, net income growth, and group-specific goals. Also

below are the amounts paid out in cash and the change from 2014 (Table 5). Most amounts

declined from 2014 to 2015, which reflects that management was not paid when the Company

underperformed.

Figure 6: Annual Incentive Cash Formula Details

Source: "Intel Corporation Schedule 14A." SEC. SEC, 4 Apr. 2016. Web.

15 May 2016.

.

Name 2015 Annual Cash 2014 Annual Cash % Change 2015 vs.

Incentive ($) Incentive ($) 2014

Brian M. Krzanich 3,301,700 3,221,400 2%

Andy D. Bryant 1,369,700 1,776,300 (23)%

Stacy J. Smith 1,698,000 1,581,800 7%

William M. Holt 1,013,000 1,179,500 (14)%

Renee J. James 1,918,100 2,487,200 (23)%

Table 5: Annual Cash Incentives 2014 and 2015

Source: "Intel Corporation Schedule 14A." SEC. SEC, 4 Apr. 2016. Web. 15 May 2016.

.

13Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

Long-term Incentive Compensation:

Equity awards consisting of restricuted stock units and outperformance restricted stock units are

given based on company performance, notably absolute and relative total shareholder return

(TSR). In 2015, TSR was 9.3%, which was above INTC’s peer group. Total payout in equity

awards was 158% of target. TSR is used as the financial criteria so that the executive committee

can align their interests with that of shareholders. Further, every executive must hold stock in

INTC. The table below details the specific equity ownership requirements.

Title Minimum Number of Shares

CEO 250,000

Executive Chairman & President 150,000

CFO 125,000

Executive Vice President 100,000

Senior Vice President 65,000

Corporate Vice President 35,000

Other VPs, Intel Fellows, and Senior Leaders 5,000 to 10,000

Table 6: Minimum Equity

Source: "Intel Corporation Schedule 14A." SEC. SEC, 4 Apr. 2016. Web. 15 May 2016.

Total Compensation:

.

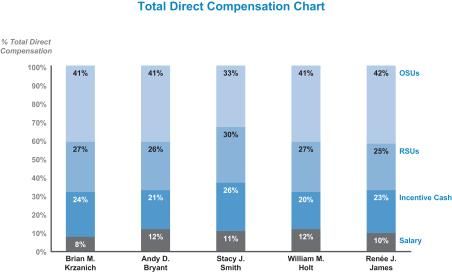

Figure 7, below, demonstates how annual compensation was allocated for 2015, and a summary

comepsnation table floows.

Figure 7: Compensation Chart

Source: "Intel Corporation Schedule 14A." SEC. SEC, 4 Apr. 2016. Web. 15 May 2016.

.

14Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

Table 7: Compensation Summary

Source: "Intel Corporation Schedule 14A." SEC. SEC, 4 Apr. 2016. Web. 15 May 2016.

.

15Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

Current Executive Committee:

Name Age Position

Brian M. Krzanich 56 Chief Executive Officer

Andy D. Bryant 64 Chairman of the Board

Stacy J. Smith 52 Executive Vice President and Chief Financial

Officer

William M. Holt 62 Executive Vice President, General, Manager,

Technology, &Manufacturing Group

Renee J. James 51 Former President

Table 8: Current Executive Committee

Source: "Intel Corporation Schedule 14A." SEC. SEC, 4 Apr. 2016. Web. 15 May 2016.

.

Current Board of Directors and Relative Compensation:

Charlene Barshefsky $313,700

Aneel Bhursi $213,700

Susan L. Decker $378,700

John J. Donahue $261,000

Reed E. Hundt $316,200

James D. Plummer $326,200

David S. Pottruck $333,700

Frank D. Yeary $331,200

David B. Yoffie $343,400

Table 9: Current Board of Directors and Compensation

Source: "Intel Corporation Schedule 14A." SEC. SEC, 4 Apr. 2016. Web.

15 May 2016.

Compensation Committee:

.

John J. Donahue

David S. Pottruck (Chair)

David B. Yoffie

Table 10: Compensation Committee

Source: "Intel Corporation Schedule 14A." SEC. SEC, 4 Apr. 2016. Web.

15 May 2016.

.

*Note: there is no overlap between the compensation committee and the executive committee.

Companies in Technology Peer Group14: Applied Materials, Inc.

Amazon.com Cisco Systems, Inc.

Apple Inc. eBay Inc.

EMC Corporation

14

“Intel Corporation Schedule 14A." SEC. SEC, 4 Apr. 2016. Web. 15 May 2016.

.

16Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

Google Inc. General Electric Company

HP Inc. Johnson & Johnson

International Business Machines Merck & Co., Inc.

Corporation Pfizer Inc.

Microsoft Corporation Schlumberger Limited

Oracle Corporation United Parcel Service, Inc.

Qualcomm Inc. United Technologies Corporation

Texas Instruments Inc Verizon Communications Inc.

TSMC Ltd

Western Digital Corporation

Companies in S&P 100 Peer Group:

AT&T Inc.

The Dow Chemical Company

INTC lies within the 53rd percentile with revenues, 73rd percentiled with net income, and the 57th

percentile with market capitalization.

Dividend and Share History:

INTC currently has 4,875 million diluted shares outstanding. This amount has steadily decreased

since 2011, as the Company has an ongoing share repurchase plan in place. In 2005, the Board of

Directors authorized repurchase of shares up to $65 billion. At the end of 2015, $9.4 billion

remained in the program for repurchase of shares15. The total number of shares repurchased during

2015 was $95.7 million, which was a total of 16 million shares. Below is a chart depicting the

decrease in number of shares outstanding over the past five years. The share repurchase explains

why EPS increased, as net income decreased, from 2014 to 2015.

15

"Intel Corporation 10-K." SEC. SEC, 2 Feb. 2016.

Web. 15 May 2016.

17

Figure 8: INTC Current Shares Outstanding

Source: Bloomberg Terminal, search , define Current Shares Outstanding as field, for INTC US Equity, 5/15/2016Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

INTC has historically paid dividends, and the dividends have been increasing in value. The

following shows the dividend yield of INTC over the past five years. The dividend yield is

currently 4.1458%. The amount paid in cash has also increased over time. In 2016, INTC

declared that it would pay a quarterly dividend of $0.26.

18Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

Cash Dividends per Share

1.10 1.04

1.00 0.96

0.90 0.90

0.90 0.87

0.78

0.80

0.70

0.60

0.50

2011 2012 2013 2014 2015 2016 Q1A

Figure 10: INTC Cash Dividends per Share

Created by Vinitha Kumar

Multiples:

INTC’s current P/E is 12.79. Multilpying this by its EPS of 2.33 yields a stock price of $29.8,

which is near the current stock price. This P/E implies that an investor would be willing to pay

$12.79 per $1 of earnings from INTC. INTC’s current price to book ratio is 2.2726, which is on

the lower end of its historical values.

Insider Transaction Information:

The top two holders of INTC are Vanguard Group and BlackRock. The top ten holders of INTC

hold 30.64% of shares oustanding. Investment advisors hold 88.76% of shares, pension funds hold

3.17%, and banks hold 2.18%. Insiders only hold .04% of shares. The screenshot below from

Bloomberg reviews these statistics.

19Investment Thesis for Intel Corporation (NYSE: INTC) by Vinitha Kumar

Figure 10: INTC Ownership

Source: Bloomberg Terminal, search , for INTC US Equity, 5/15/2016

Conclusion:

Although 2015’s results were not as strong as 2014’s, INTC continues to make sound management

decisions and adapt to customers’ needs. The market currently prices INTC at $30.06, which is

lower than the probable free cash flow per share of $37.07 determined through our HG-DCF. The

HG-DCF relies on the assumption that there will be a mean reversion in revenues, asset turnover

ratios, and margins. This assumption makes sense as INTC has historically made strategic

acquisitions, but is now focusing on restricting their company and utilizing their recent acquisitions

to complement their various business segments. In order for this to happen, CAPEX must be

sustained at lower levels, and revenue growth rates must increase as the acquired assets begin to

generate revenue. The Monte-Carlo simulation shows that the current stock price is between the

20th and 30th percentile, indicating that there is more upside than downside with investing in INTC

based on our model. There are certain risks with relying on the HG-DCF for investment decisions,

notably the assumptions used to predict the future free cash flow to shareholders. After analyzing

INTC’s management compensation, it is evident that executives are aligned with shareholders

interest as they are required to hold equity and are compensated based on total shareholder return.

There were no clear red flags when reading through INTC’s management compensation and

nothing stood out as inconsistent with our investment thesis. Assuming the revenue growth rates

and CAPEX rates hold and management decisions stay sound, I recommend INTC as a buy.

20You can also read