GLOBAL SUMMARY MINING - Week Commencing 15th March MAR 2021 - Fitch Solutions

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MAR 2021 GLOBAL SUMMARY MINING Week Commencing 15th March

Global Summary Mining | 20210315

Contents

Global ................................................................................................................................................................................................. 4

Quantifying The Impact Of EV Adoption On Nickel: Stronger-Than-Expected Demand Ahead .................................................................. 4

Mining - Weekly Projects Round-Up & Developments .................................................................................................................................................. 7

Mining - Weekly Projects Round-Up & Developments ................................................................................................................................................13

Africa................................................................................................................................................................................................19

Africa Lithium Outlook: SSA To Offer Diversification Amid The Race To Secure Critical Materials............................................................19

Asia...................................................................................................................................................................................................26

Asia Fertiliser Outlook: South East Asia To Drive Demand As Indian Rebound Fades.....................................................................................26

© 20

2021

21 Fit

Fitch

ch Solutions Gr

Group

oup Limit

Limited.

ed. All rights rreserv

eserved.

ed.

All information, analysis, forecasts and data provided by Fitch Solutions Group Limited is for the exclusive use of subscribing persons or organisations (including those

using the service on a trial basis). All such content is copyrighted in the name of Fitch Solutions Group Limited and as such no part of this content may be reproduced,

repackaged, copied or redistributed without the express consent of Fitch Solutions Group Limited.

All content, including forecasts, analysis and opinion, has been based on information and sources believed to be accurate and reliable at the time of publishing. Fitch

Solutions Group Limited makes no representation of warranty of any kind as to the accuracy or completeness of any information provided, and accepts no liability

whatsoever for any loss or damage resulting from opinion, errors, inaccuracies or omissions affecting any part of the content.

This report from Fitch Solutions Country Risk & Industry Research is a product of Fitch Solutions Group Ltd, UK Company registration number 08789939 (‘FSG’). FSG is an

affiliate of Fitch Ratings Inc. (‘Fitch Ratings’). FSG is solely responsible for the content of this report, without any input from Fitch Ratings. Copyright © 2021 Fitch Solutions

Group Limited.

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 3

Global Summary Mining | 20210315

Global

Quantifying The Impact Of EV Adoption On Nickel: Stronger-Than-

Expected Demand Ahead

Key View

• As a key component of battery cathode chemistry in many existing and upcoming electric vehicles (EVs), nickel will remain an

important metal to watch in the coming decade.

• We are updating in this article our estimate of the impact of electric vehicle (EV) battery manufacturing on nickel consumption.

• We expect nickel demand for EV battery manufacturing to experience an annual average growth rate of 29% over 2021-2030,

outpacing both lithium and cobalt demand. Interestingly, this estimate has significantly increased from the forecast we laid out in

our 2018 battery report, due to upwards revisions in our Autos team's EV sales forecasts.

• Nickel demand will be supported by the metals persisting popularity in battery cathode chemistry, with downside risks caused by

concerns over future supply availability.

As battery metals continue to rise to the forefront of attention in 2021, much of the attention has centered around lithium and

cobalt. In turn, governments have enacted policies to encourage investment into the critical raw materials they deem essential to

the green energy transition. At the same time, supply chain concerns surrounding nickel have begun to garner increasing focus. As

a key component of battery cathode chemistry in many existing and upcoming electric vehicles (EVs), nickel will

remain an important metal to watch in the coming decade.

We have long identified nickel as one of they key metals that will strongly benefit from the battery revolution concerning an

accelerated EV uptake. In line with our views outlined back in 2018, nickel-based batteries have gained in popularity since.

Steep EV Sales Growth To Drive Demand For High-Grade Nickel

Electric Vehicles Sales & Total Fleet

f = Fitch Solutions Autos Service forecast. Source: Fitch Solutions

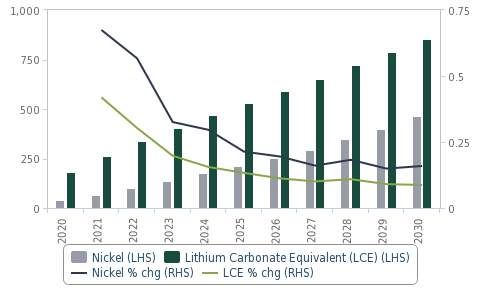

We are updating in this article our estimate of the impact of electric vehicle (EV) battery manufacturing on nickel consumption. We

expect nickel demand for EV battery manufacturing to experience an annual average growth rate of 29.2% over

2021-2030, outpacing both lithium and cobalt demand. Our EV nickel demand forecast has significantly increased from

the forecast in our 2018 battery report, due to upwards revisions in our auto teams forecasts for EV sales.

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 4

Global Summary Mining | 20210315

We are estimating the added demand for nickel in the coming years building on our Autos' team views, using current and

expected battery chemistry market share, estimated metal content in batteries and our EV sales forecasts. We note that our Autos

team will revisit its forecasts for cathode chemistry demand in the coming months as battery manufacturing is a fast moving sector,

which has undergone significant transformation particularly during the past year. We will therefore keep updating

our estimates for nickel demand as the sector evolves.

Nickel To Outpace Lithium Battery Demand Growth

EV Battery Demand - Lithium And Nickel (kt)

Source: Fitch Solutions

Our estimates of the impact of EV battery manufacturing on nickel demand that we present in this article rely on our 2018 forecasts

for demand by cathode type, isolating demand for the lithium-nickel-manganese-cobalt oxide (NMC) chemistry, which we expect to

be the preferred cathode of choice moving forward. We also maintain the underlying assumption that NMC 811 cathodes will rise to

80.0% of NMC market share by 2027, which will effectively raise the average nickel content from 34.6kg to 44.5kg for each NMC

cathode produced. Automakers such as BMW, Hyundai and Renault use the NMC chemistry in their vehicles, and Tesla currently

employs a lithium-nickel-cobalt-aluminum oxide (NCA) chemistry in its models. Going forward, Tesla will exchange its NCA chemistry

for three different offerings based on vehicle cost and performance: lithium-iron-phosphate (LFP), NMC and a high-nickel, cobalt-

free option.

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 5

Global Summary Mining | 20210315

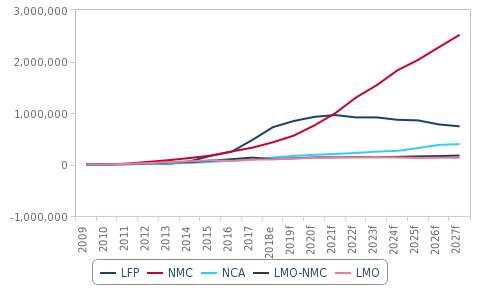

NMC Demand To Surpass LFP, Bolstered By Chinese Subsidies

EV Sales By Cathode Type (Volume)

Source: Fitch Solutions

Nickel demand will be supported by the metals persisting popularity in battery cathode chemistry, with downside

risks caused by concerns over future supply availability. We expect nickel-dominant cathodes to be favoured for

automakers' heavy duty and long-range vehicles, however a shortage of Class 1, battery-grade nickel may encourage automakers to

explore lithium-iron-phosphate (LFP) batteries for mass market vehicles. For example, Tesla CEO Elon Musk iterated in February

2021, that Nickel remains the firm’s biggest obstacle to successfully scaling lithium-ion cell production and has prompted Tesla to

shift its standard range vehicles to contain LFP cathodes. Furthermore, the firm reached an agreement in March 2021 to source raw

materials from the Goro nickel mine in New Caledonia for its batteries by serving as a technical and industrial partner. This signifies

the continuing preference for nickel-heavy batteries due to higher energy density properties. Earlier in January 2021, Musk stated in

an investor call that the company did not have enough battery cells to scale production for new vehicles such as its Semi truck.

Tesla intends to use the high-nickel, cobalt-free cathode for its Cybertruck and Semi truck. We would expect nickel demand to

be adversely impacted should other automakers follow Tesla's suit, by switching to LFP batteries in lower-range

models due to concerns over raw materials security.

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 6

Global Summary Mining | 20210315

Mining - Weekly Projects Round-Up & Developments

In this week's round-up we examine upwards revisions on our nickel and zinc price forecasts amid high bases at the start of the year,

and review the latest updates from Impala Platinum's company strategy.

Zinc Prices: Upwards Revisions Though Price Rally To Ease

We have revised up our 2021 zinc price forecast to USD2,600/tonne, up from USD2,450/tonne previously, to account for the

persisting price elevation throughout the first two months of the year. Declining Chinese consumption, particularly during H221, will

weigh on the global refined zinc demand. At the same time, accelerated production growth in other markets coupled with large

refined stocks housed in private warehouses, will offset a slowdown in Chinese production. Beyond 2021, we expect more

significant increases in the refined zinc production surplus to cause prices to trend lower. We expect price volatility due to the

Covid-19 pandemic to remain a key risk throughout the remainder of 2021, as news surrounding new variants of the virus, vaccine

efficacy and vaccine nationalism continue to emerge.

Early 2021 Price Rally To Lose Steam

LME Zinc Three-Month Rolling Forward (USD/tonne)

Source: Bloomberg, Fitch Solutions

Nickel Prices: Correction Likely To Stay Over 2021

We are revising up our 2021 average price forecast for nickel from USD15,250/tonne to USD15,750/tonne as prices started the

year from a high base. We expect LME nickel prices will hover around current levels in the coming months as investors price in the

recent Tsingshan announcement while economic stimulus in China and a weakening US dollar continues providing support. Prices

will be supported in the near term by Chinese demand following the lunar new year holiday and a weakening US dollar. We are

maintaining our bearish outlook on prices in 2021 compared with the year-to-date average of USD18,140/tonne as increasing

supply over the year reduces the market deficit, maintaining lower prices. Over the long term, we believe a sustained market deficit

will support higher prices over our forecast period.

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 7

Global Summary Mining | 20210315

Correction Likely To Stay As New Supply Ramps Up

Three-Month LME Nickel, USD/tonne (daily)

Note: Horizontal red lines are Fitch Solutions forecasts. Source: Bloomberg, Fitch Solutions

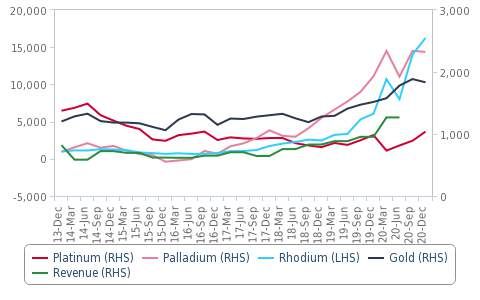

Impala Platinum: Impala Canada Boosts Interim Operational Performance

Impala Platinum will continue to focus on cost containment and efficiency improvements, particularly through the

replacement of older shafts with more efficient ones. The company will also focus on its Zimbabwe operations as the

government opens up to investment, presenting new growth opportunities. In its 2021 interim results, Impala Platinum reported a

strong operational performance during the first half of FY2021 (ending December 30 2020). Refined platinum and palladium

production increased by 20.0% and 47.0% y-o-y respectively. Total refined rhodium production grew by 20.0% y-o-y; however,

nickel production experienced a 2.0% y-o-y contraction.

The firm has also increased its production guidance for FY2021 to 3.2-3.5koz from 2.8-3.4koz previously, while revising down its

capital expenditure guidance to ZAR5.8-6.2bn, from ZAR6.0-6.8bn previously.

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 8Global Summary Mining | 20210315

Revenue Improving Upon Price Rally Despite Covid-19 Operational Impact

Impala Platinum - Revenue (USDmn) and Select Commodities Prices (USD)

Note: Quarterly revenue figures are an even split of the semi-annual reported revenue. Source: Bloomberg, Fitch Solutions

PROJECT DEVELOPMENT - MINING PROJECT UPDATES: MARCH 3-9 2021

Country Company Mine Commodity Update

Has reported new high-grade drilling results at the

Australia Horizon Minerals Limited Windanya Gold

project

BOWEN COKING COAL

Coal - BOWEN COKING COAL LIMITED has commenced new

Australia LIMITED, Sumitomo Hillalong

Coking exploration program at the project

Corporation

ANTIPA MINERALS LTD. has reported broad spaced,

ANTIPA MINERALS LTD., IGO Copper, vertical, shallow air core drilling intersects highly

Australia Paterson

Limited Gold anomalous zones of gold‐copper mineralisation and

multiple other pathfinder elements at the project

Copper, Has reported assay results at Constellation deposit of

Australia Aeris Resources Limited Tritton

Gold the project

Red 5 Limited has signed a letter of intent with

MACMAHON HOLDINGS

Australia King of the Hills Gold MACMAHON HOLDINGS LIMITED for the award of

LIMITED, Red 5 Limited

mining contract for the project

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 9Global Summary Mining | 20210315

Country Company Mine Commodity Update

Copper,

Australia Elementos Limited Cleveland Lead, Tin, Has identified a new drill target at the project

Zinc

St Barbara Limited has selected MACMAHON

MACMAHON HOLDINGS

Australia Gwalia Gold HOLDINGS LIMITED as the underground mining

LIMITED, St Barbara Limited

contractor for the project

The federal government has awarded major project

Australia TNG Limited Mount Peake Iron Ore

status to the project

Osisko Mining Inc. has placed an order for grinding

FLSmidth & Co. A/S, Osisko

Canada Windfall Gold equipment and ancillaries from FLSmidth & Co. A/S for

Mining Inc.

the project

Has commenced a new 3500m diamond drill program

Canada Anaconda Mining Inc. Goldboro Gold

at the project

Wallbridge Mining Company Has reported new results from the definition drill

Canada Fenelon Gold

Limited program at the project

IAMGOLD Corporation has reported assay results from

IAMGOLD Corporation,

Canada Rouyn Gold the 2020 exploration diamond drilling program,

Yorbeau Resources Inc.

completed on Astoria target area at the project

IAMGOLD Corporation, IAMGOLD Corporation has reported additional assay

Canada Sumitomo Metal Mining Co., Cote Gold results from the delineation diamond drilling program

Ltd. at the project

Copper,

Thunder Bay Gold, Nickel, Has commenced a 40000m diamond drill program at

Canada Clean Air Metals Inc.

North Palladium, the project

Platinum

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 10Global Summary Mining | 20210315

Country Company Mine Commodity Update

Copper, Has reported an initial mineral resource of 1127.4mnt

Canada Tudor Gold Corp. Treaty Creek

Gold at the project

Canada Renforth Resources Inc. Parbec Gold Has reported drill results at the project

Has reported additional results from the 2020 drill

Canada Probe Metals Inc. Val-d'Or East Gold

program at the project

Has reported further strong results from site operations

Congo (DRC) AVZ Minerals Limited Manono Tin

at the project

Has reported assay results from down-plunge extension

Cote d`Ivoire Roxgold Inc. Seguela Gold drilling below the high grade Koula deposit of the

project

Has identified new, near surface, high grade

Dominican Copper,

Unigold Inc. Neita mineralization at Candelones Extension deposit of the

Republic Gold

project

Has delivered and mobilized two new drilling rigs and

continued high grade gold results from surface drilling

Fiji Lion One Metals Limited Tuvatu Gold

and underground channel sampling programs at the

project

Mali Cora Gold Limited Sanankoro Gold Has awarded new exploration permit for the project

Auris Minerals Limited,

Auris Minerals Limited has received high grade gold

New Zealand OceanaGold Corporation, Sams Creek Gold

results from diamond drilling at the project

Sandfire Resources Ltd

Ascendant Resources Inc., Copper,

Ascendant Resources Inc. has reported an updated

Portugal Empresa de Desenvolvimento Lagoa Salgada Gold, Lead,

mineral resource of 12.1mnt at the project

Mineiro SA Tin, Zinc

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 11Global Summary Mining | 20210315

Country Company Mine Commodity Update

Copper,

United States KGHM Polska Miedz S.A. Robinson Is planning to divest the mine

Gold

United States KGHM Polska Miedz S.A. Carlota Copper Is planning to divest the mine

Source: Company announcements, Fitch Solutions

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 12Global Summary Mining | 20210315

Mining - Weekly Projects Round-Up & Developments

In this week's round-up we outline our view on the commodities complex within our Monthly Commodities Strategy, quantify the

impact of electric vehicle adoption on the nickel market and analyse the impact of Tsingshan's announcement on class-1 nickel

supply.

Monthly Commodities Strategy: Key Metals, Agricultural Commodities Close To Peaking

The outlook for commodities has become increasingly positive in 2021, and we at Fitch Solutions have made a

number of upward revisions to our forecasts in recent weeks, most notably to nickel, cotton, natural gas (henry hub), zinc, rice,

and steel. The positive macroeconomic backdrop for commodities will help prices across all sub-sectors average higher in 2021,

and we see copper and nickel, corn and soybean averaging at a seven-year high in 2021, iron ore at an eight-year high, palm oil at a

10-year high. While the oil market is also on a recovery trend, the uptick will be less impressive relative to previous years, and we

currently see Brent averaging below 2019 levels. Strong momentum for metals will most likely keep prices in an uptrend,

but we are bearish on base metals and iron ore on a six-month horizon, as we believe a more nuanced fundamental picture

will emerge later in the year. Accelerating inflation, leading to DM central bank tightening and weakening EM FX, could put additional

downside pressure on industrial commodities.

Looking beyond 2021, we see some bright spots among commodities, but we not believe that we are currently in the middle of a

commodities super cycle, which is a view held elsewhere. The prices of metals key to the green and tech economy, such as copper

and nickel, will shine and average higher in the coming years, but we maintain a rather modest outlook on other commodities.

Good Performance Across Commodities In 2021, Risks Of A Relapse In 2022

Fitch Solutions Commodity Prices Indices, % chg y-o-y

Note: Composite equally weighted price indexes based on Fitch Solutions annual average price forecasts. Source: Fitch Solutions

Quantifying The Impact Of EV Adoption On Nickel: Stronger-Than-Expected Demand Ahead

As a key component of battery cathode chemistry in many existing and upcoming electric vehicles (EVs), nickel will

remain an important metal to watch in the coming decade. We are updating in this article our estimate of the impact

of electric vehicle (EV) battery manufacturing on nickel consumption. We expect nickel demand for EV battery manufacturing to

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 13Global Summary Mining | 20210315

experience an annual average growth rate of 29% over 2021-2030, outpacing both lithium and cobalt demand. Interestingly, this

estimate has significantly increased from the forecast we laid our in our 2018 battery report, due to upwards revisions in our Autos

team's EV sales forecasts. Nickel demand will be supported by the metals persisting popularity in battery cathode chemistry, with

downside risks caused by concerns over future supply availability.

Steep EV Sales Growth To Drive Demand For High-Grade Nickel

Electric Vehicles Sales & Total Fleet

f = Fitch Solutions Autos Service forecast. Source: Fitch Solutions

Indonesian Nickel Matte Supply Deal Adds Upside Risk To Near-Term EV Battery Supply

A recent nickel matte supply deal between Tsingshan Holding Group, Huayou Cobalt and CNGR Advanced Material

will likely alleviate near-term supply concerns, with the scope of Class 1 nickel supply risk depending on the technology

behind the company's nickel matte processing. Within the context of the Tsingshan supply deal, we maintain our positive outlook

for Indonesia’s expanding role in the electric vehicle battery supply chain. We expect to see continuing high-pressure acid leach

nickel smelting projects in Indonesia, though we note permitting delays for waste disposal may hinder the development timeline.

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 14Global Summary Mining | 20210315

Indonesia Positioned To Reap Nickel Price Benefits

Selected Countries - Nickel Production,' 000 tonnes (2015-2030)

e/f = Fitch Solutions estimate/forecast. Source: National sources, Fitch Solutions

PROJECT DEVELOPMENT - MINING PROJECT UPDATES: MARCH 10 - 16 2021

Country Company Mine Commodity Update

Has completed front-end loading 3 report for the

Australia TNG Limited Mount Peake Iron Ore

beneficiation plant at the project

Is on track to deliver first gold production from the

Australia Red 5 Limited King of the Hills Gold

mine in mid-2022

ANTIPA MINERALS LTD. has reported that reverse

Copper,

ANTIPA MINERALS LTD., circulation drill testing of initial greenfield targets

Australia Wilki Gold, Lead,

Newcrest Mining Limited intersects minor zones of anomalous gold, copper

Zinc

mineralisation at the project

Auris Minerals Limited has completed the first hole of

Auris Minerals Limited,

Australia Forrest Copper the six diamond drill holes for 2540m planned at the

Westgold Resources Limited

project

Australia Artemis Resources Limited Carlow Castle Copper, Gold Has reported drill results at the project

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 15Global Summary Mining | 20210315

Country Company Mine Commodity Update

Castelo de Has reported an updated mineral resource of 2.2Moz at

Brazil TriStar Gold Inc. Gold

Sonhos the project

Velocity Minerals Ltd. has received an initial inferred

GORUBSO-KARDZHALI AD,

Bulgaria Obichnik Gold mineral resource of 0.2Moz for Durusu zone of the

Velocity Minerals Ltd.

project

Has commenced a 4000m diamond drill program at the

Canada Anaconda Mining Inc. Point Rousse Gold

project

Has reported new analytical results from the ongoing

Canada Osisko Mining Inc. Windfall Gold

drill program at the project

Has reported an updated mineral resource of 0.7Moz at

Canada Granada Gold Mine Inc. Granada Gold

the project

Has reported new wide, high-grade intersections in

Canada Kirkland Lake Gold Ltd. Detour Lake Gold

Saddle zone at the project

Has reported the results from the first drill holes

Canada Marathon Gold Corporation Valentine Gold completed under the 2021 exploration program at the

project

Has reported complete and partial drill assay results

Canada Talisker Resources Ltd. Bralorne Gold from ongoing stage one 50000m drill program at the

project

Has reported an updated inferred resource of 1.2Moz at

Canada Gold Terra Resource Corp. Yellowknife City Gold

the project

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 16Global Summary Mining | 20210315

Country Company Mine Commodity Update

Has reported additional assay results from southwest

Canada Troilus Gold Corp. Troilus Copper, Gold

zone at the project

Imperial Metals Corporation, Imperial Metals Corporation has discovered new zones

Canada Red Chris Copper, Gold

Newcrest Mining Limited of higher grade mineralization at the project

African Gold Group, Inc. has reported positive test

African Gold Group, Inc.,

Mali Kobada Gold results from metallurgical testing on sulphide material

Government of Mali

at the project

Firefinch Limited, Government Firefinch Limited has intended to commence mining of

Mali Morila Gold

of Mali satellite pits at the project in mid-2021

Has reported the results from 14 diamond drill holes

Gold, Lead,

Mexico Discovery Metals Corp. Cordero targeting the Josefina and Todos Santos high-grade vein

Zinc

trends at the project

A pre-feasibility study has reported that the mine will

Nicaragua Calibre Mining Corp. Pavon Gold

produce 47koz/yr of gold over a mine life of 4 years

Has reported positive drill results from expansion

Nicaragua Mako Mining Corp. San Albino Gold

drilling at the project

Has confirmed significant zones of mineralisation in the

Spain Elementos Limited Oropesa Tin current campaign to convert existing inferred resources

into indicated resources at the project

Has reported initial underground drilling results at the

United States Arizona Gold Corp. Copperstone Gold

project

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 17Global Summary Mining | 20210315

Country Company Mine Commodity Update

Has reported assay results for five-large diameter core

United States Viva Gold Corp. Tonopah Gold holes from previously announced reverse circulation

and core drilling program at the project

Has reported that initial surface and underground

United States Gold Bull Resources Corp. Sandman Gold sampling has produced favourable assay results at the

project

Source: Company announcements, Fitch Solutions

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 18Global Summary Mining | 20210315 Africa Africa Lithium Outlook: SSA To Offer Diversification Amid The Race To Secure Critical Materials Key View • We at Fitch Solutions expect to see an increase in lithium development projects in Africa, amid our bullish outlook for a sustained recovery in prices. • We estimate there are eight lithium mining projects currently in development in Africa - in Zimbabwe, Namibia, Mali, Ghana and the DRC - which is still small relative to the number of projects being developed in the Americas, Australia and Europe for example. • Zimbabwe will remain the largest lithium producer in Africa in the near-term, with production growth underpinned by the Arcadia lithium project and government support. • The advancement of the Karibib project in Namibia could benefit ESG focused European battery manufacturers. Meanwhile, political instability in Mali will pose risks to project development. • Continued success at AVZ Mineral's USD454mn Manono project in the DRC, will add upside to the development of the domestic lithium sector within 2021. Still, projects in countries with lower levels of country risk, such as Ghana, will be more likely to attract financing from the risk-averse investor. We at Fitch Solutions expect to see an increase in lithium development projects in Africa, amid our bullish outlook for a sustained recovery in prices. Lithium is a critical raw material (CRM) necessary for the transition to a green economy, with applicable uses in lithium ion batteries which are commonly utilised in EV manufacturing as well as in electric devices or alongside solar panels to store excess solar energy. Efforts to diversify lithium sources will attract foreign investment into Africa in the coming years as major economies look to secure lithium for their battery supply chains. We expect mining firms to broaden exploration activities to Africa in countries such as Zimbabwe, Namibia, Mali, Ghana and the Democratic Republic of Congo (DRC). This includes all African countries with known reserves, those which are current lithium producers, such as Zimbabwe and Namibia as well as those with ongoing lithium developments. THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research. fitchsolutions.com 19

Global Summary Mining | 20210315

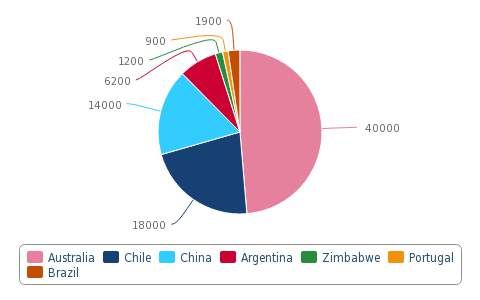

Miners To Look To Africa To Diversify Supply

Global - Lithium Mine Production, 2020 (Metric Tonnes)

Source: USGS, Fitch Solutions

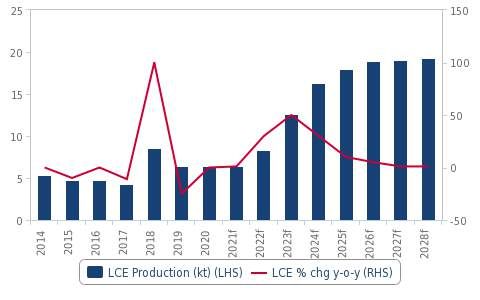

Zimbabwe: Set To Remain Largest African Producer In The Short-Term

Zimbabwe will pave the way for lithium mine advancement in Africa, underpinned by the Arcadia Lithium

Development. In 2020, Zimbabwe was the sixth largest lithium producer in the world, and its position stands to benefit from key

developments such as the USD162mn Arcadia large-scale lithium project, near the city of Harare. The project is currently owned by

Prospect Resources, and is one of the most advanced lithium projects globally, with the firm having secured off-take

agreements across both Europe and Asia and having received full-permitting to commence production. In March 2021, Prospect

announced that it has begun to develop a smaller commercial scale pilot plant for the production of technical-grade petalite in an

effort to de-risk an accelerated production timeline. The firm will then ramp up production in two phases from 1.2mtpa to 2.4mtpa,

with a targeted commencement in 2022.

Previously, on August 17, Prospect announced a seven-year offtake agreement with Belgian firm, Sibelco, positioning the mine to

become the largest global supplier of ultra-low iron petalite. Under the agreement, Prospect will supply Sibelco with up to

approximately 10kt of lithium carbonate equivalent (LCE) per year. Past assays have demonstrated that Arcadia could be the only

lithium mine capable of supplying the premium glass and ceramics market both spodumene and petalite, giving Zimbabwe a

differentiation strategy advantage. Other prominent lithium developments within Zimbabwe, include Premier African Minerals

Zulu lithium project which was granted an exclusive prospect order (EPO) in March 2021. The company aims to initiate a definitive

feasibility study (DFS) to be completed within 14 months.

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 20Global Summary Mining | 20210315

Arcadia To Fuel Large Production Gains

Zimbabwe- Lithium Production, Lithium Carbonate Equivalent (LCE)

f = Fitch Solutions forecast. Source: USGS, Fitch Solutions

The government will help bolster mining investment in the lithium sector through a series of support initiatives. In

January 2020, the government of Zimbabwe confirmed that it is on track to achieve its targeted USD12bn mineral export goal by

2023, marking a 344% increase over USD2.7bn in mineral exports registered in 2017. Although the government's projected export

target is quite ambitious given the narrow timespan, it affirms the country's bright outlook for the sector. Furthermore, the

government expects commodities to drive its broader effort to significantly boost the country’s national income by 2030. The

Arcadia lithium project is expected to be a strong contributor to Zimbabwe’s 2023 extractive export target. The government also

holds long-term plans to build a lithium ore processing plant in Bulawayo, which if realised, would encourage investment

by increasing value-added domestic offerings.

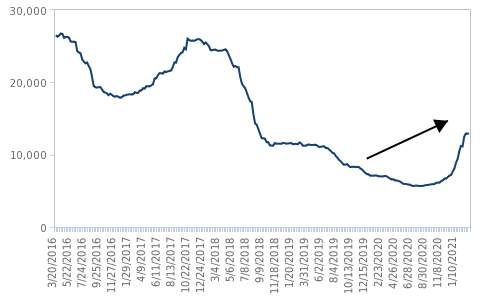

Sustained Price Recovery To Benefit Project Renewal In Namibia

China Lithium Carbonate 99.5% (USD/tonne)

Fitch/Solutions

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 21Global Summary Mining | 20210315

Namibia: Sustainable Production At Karibib Positioned To Appeal To ESG-Focused Manufacturers

Lithium production in Namibia has lagged behind Zimbabwe, as weak prices have slowed project investment. Lithium production

took off in Nambia in 2018, with Desert Lion Energy exporting lithium concentrate from the firm’s Rubicon and Helikon mines.

However, the country did not produce any lithium in 2019, and many key projects have stalled amid the slump in global lithium

prices beginning in August 2018. For example, Desert Lion halted all of its Namibian lithium operations in September 2018 before

merging with global lithium exploration and development company, Lepidico Limited in July 2019. We expect Lepidico’s large-

scale lithium project will offer upside potential to future domestic production in the medium term, as electric vehicle

demand narrows the present lithium surplus. In March 2021, the firm increased mineral resources for its USD139mn Karibib

project, now reaching 11.9mnt at 0.45% lithium dioxide across all categories. Previously, in May 2020, Lepidico revealed the

definitive feasibility study (DFS) for phase one of the project. The project also includes both of the firm's idled Rubicon and Helikon

deposits.

With an estimated annual production of 7kt of lithium carbonate equivalent (LCE), the advancement of the Karibib project

could benefit ESG focused European battery manufacturers. This is due to the utilisation of Lepidico’s patented L-Max and

LOH-Max technologies, which enables the firm to achieve low-cost production of lithium hydroxide in a more sustainable manner.

Steam is the only material emission involved in the L-Max process, while LOH-Max avoids the creation of the problematic byproduct

sodium sulphate. Fully permitted, Lepidico is scheduled to award the EPCM contract for a 60ktpa concentrator for Karibib by the

end of Q221, adding upside to our outlook for Namibian lithium production.

DRC AND MALI BOAST HIGHEST RESERVES WITHIN THE CONTINENT

Total Indentified Lithium Reserves

Share of Global Reserves Share of African Reserves

(mnt)

DRC 3 3.5% 69.1%

Mali 0.7 0.8% 16.1%

Zimbabwe 0.5 0.6% 11.5%

Ghana 0.09 0.1% 2.1%

Namibia 0.05 0.1% 1.2%

Source: USGS, Fitch Solutions

Mali And The DRC: Highest Reserves, Yet Higher Risks

In contrast, political instability in Mali will pose risks to the development timelines of lithium projects. In August 2020,

Firefinch (formerly Mali Lithium) reported that its operations had been unaffected by the previous military coup on August 18,

during which President Ibrahim Boubacar Keïta resigned and dissolved Parliament. However, Firefinch announced in its February

2021 investor presentation that it aims to de-merge its Goulamina lithium project to continue to focus on its gold assets such as the

Massigui and Dankassa gold projects.

The Goulamina project possesses high-grade spodumene concentrate and is fully permitted, but is likely to face difficulties

attracting interest in the near-term due to the country's high country risk. Firms will seek to avoid conflict-ridden Mali in the

coming quarters, evidenced by existing firms offloading assets. In August 2020, Anglogold Ashanti and Barrick Gold

announced that they would be selling their 80.0% interest in the Morila gold mine to Mali Lithium. The reach of the coup will extend

to administrative procedures, likely resulting in additional delays and red tape for mining firms.

On the other hand, Kodal Minerals Bougouni lithium project may add upside to Mali's lithium development. In September

2020, Kodal Minerals announced that it signed a memorandum of understanding (MOU) with Chinese firm Sinohydro to develop

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 22Global Summary Mining | 20210315

its USD117mn Bougouni lithium project. Sinohydro's previous experience in Mali developing large public infrastructure projects will

increase the likelihood of the project's advancement amid the backdrop of high political risk. We highlight political instability posing

a larger obstacle to the project's timeline. As of March 2021, Kodal is awaiting mining licence approval from the transition

government.

Mali and The DRC Present Largest Security Risks

SSA - Short- Term Political Risk Index, Security & External Threats

Note: Scores out of 100; higher score = more attractive market. Source: Fitch Solutions Short-Term Political Risk Index

Continued success at AVZ Mineral's USD454mn Manono project in the DRC, will add upside to the development of

the domestic lithium sector within 2021. In March 2021, AVZ reported wide intercepts of high-grade lithium mineralisation as a

result of recent drilling targeting ground-water monitoring. With a 20-year mine life, and likely expansion of the project's resource

base, which already includes a 400mnt high-grade open pit resource, Manono is well-positioned to be a leading lithium producer in

SSA. In the April 2020 feasibility study, Manono was estimated to produce up to 700,000 tonnes per annum of lithium spodumene.

AVZ holds a 65.0% stake in the project with the rest of the ownership held by a joint venture between AVZ and the Congolese

government through Dathcom Mining. The firm expects the reach a final investment decision within the second quarter of 2021,

with construction expected to begin in August.

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 23Global Summary Mining | 20210315

Ghana and the DRC's Established Mining Sectors To Benefit Lithium Investment

Select Countries - Mining Industry Risk Reward Index Scores and Mining Industry Value (MIV)

Note: Scores out of 100; higher score = more attractive market. Source: National Sources, Fitch Solutions Mining Risk/Reward Index

Although investors focused on battery metals have begun to shift away from the DRC's cobalt resources, due to humanitarian

concerns over child labour, formal lithium mining is likely to mitigate this risk. Still, projects in countries with lower levels of

country risk, such as Ghana, will be more likely to attract financing from the risk-averse investor. In January 2021,

reports stated that IronRidge has completed a successful scoping study on its Ewoyaa, hard-rock lithium project in Ghana, which

details a 2.0mntpa operational capacity. Furthermore, Ewoyaa's close proximity to existing infrastructure will boost project feasibility.

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 24Global Summary Mining | 20210315

LITHIUM DEVELOPMENTS IN AFRICA

Capex

Country Company Mine Phase Notes

(USDmn)

January 2021 - A scoping study has reported

that the mine will produce 295kt/yr of Li2O

New spodumene concentrate over a mine life of 8

Ghana IronRidge Resources Ewoyaa 68.1

Project years; Indicated Resources: 4.5mnt;The

project includes Ewoyaa, Abonko and

Kaampakrom deposits

February 2021 - Firefinch Limited is planning

New to spin off the project; Expected Production:

Mali Firefinch Limited (100%) Goulamina 194

Project 436kt/yr; Mine Life: 23years; Proved

Reserves: 8.1mnt

May 2019 - Premier African Minerals Limited

New has appointed KME Plant Hire Proprietary

Zimbabwe Premier African Minerals (100%) Zulu

Project Limited to carry out drilling works at the

project; Inferred Resources: 20.1mnt

December 2019 - Prospect Resources has

announced the results of definitive feasibility

New

Zimbabwe Prospect Resources (87%) Arcadia 197.4 study at the project; Proved Reserves:

Project

11.3mnt; Mine Life: 15.5years; Expected

Production: 173kt/yr

September 2020 - Kodal Minerals has signed

New a memorandum of understanding with

Mali Kodal Minerals Bougouni

Project Sinohydro Corporation Limited to develop the

project; Indicated Resources: 11.6mnt

Canadian strategic metals New

Zimbabwe Kamativi Indicated Resources: 26.3mnt

company Chimata Gold Corp Project

January 2021 - An independent study has

found lowest carbon footprints of lithium at

the project; January 2021 - AVZ Minerals

Limited has signed strategic offtake

agreement with Ganfeng Lithium Co Ltd for

New

Congo (DRC) AVZ Minerals (60%) Manono 545.5 the project; September 2020 - AVZ Minerals

Project

Limited has executed a share sale purchase

agreement with Dathomir Mining Resources

SARL to acquire an additional 10% stake in

the project; Proved Reserves: 44.6mnt; Mine

Life: 20years; Expected Production: 700kt/yr

May 2020 - Lepidico has delivered compelling

Namibia Lepidico (80%) Karibib definitive feasibility study for the project;

Proved Reserves: 1.9mnt; Mine Life: 14years

One of the largest lithium mines in Africa,

Zimbabwe Bikita Minerals Bikita Operational

operating since the 1950s.

Source: Fitch Solutions Global Mines Database

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 25Global Summary Mining | 20210315

Asia

Asia Fertiliser Outlook: South East Asia To Drive Demand As Indian

Rebound Fades

Key View

• Although Asia, led by China and India, will remain the largest consumer of fertilisers globally, the outlook for usage in China and

India is lacklustre as both countries aim to tackle the severely excessive application of fertilisers.

• Chinese potash inventories remained elevated for much of 2020 and allowed the Chinese consortium of buyers to agree on a

new potash contract on April 30 2020 at just USD220/tonne, below the last contracted signed in 2018/19 at USD290/tonne.

• China’s Canpotex contract expired in October 2020, and lower inland inventories in China could lead to a higher price during the

next contract renegotiation, although this could be challenged by a recent potash deal between China and the BPC.

• The Indian government will maintain fertiliser subsidies in 2020/21 but continues to promote balanced usage in a bid to reduce

chemical fertiliser consumption. It is estimated that the share of urea consumption as part of nitrogen-based fertilisers is at 80%

in India.

• South East Asia remains the bright spot for fertiliser consumption in Asia, while Indonesia is expected to be an outperformer and

Vietnam an underperformer. Emerging markets in Asia such as Myanmar and Cambodia will also see growth as demand starts

from a low base.

• India is undergoing a revival of its nitrogen fertiliser industry, which will lead to lower imports in the coming years. That said,

fertiliser sales in India have been trending upwards in 2019/20 owing to healthy monsoons, strong growth in the domestic

agricultural sector and buying surge due to Covid-19-related lockdowns.

China's Consumption On The Decline, Brazil's Rising

Global - Consumption Of Fertilisers, % nutrients

Source: FAO, Fitch Solutions

Asia Regional Consumption: Weak Outlook

Asian fertiliser consumption will prove better than we previously expected in 2020 despite efforts to reduce excessive usage, mainly

because of improved consumption in India where the 2020 monsoon brought abundant rainfall. We expect demand to grow only

modestly from 2021 to 2024, with potential for a mild increase in 2021 calendar year owing to high domestic grain prices

encouraging more plantings. While fertiliser consumption will be strong in South Asia with the rise in crop production over the short

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 26Global Summary Mining | 20210315

term, growth in Indian demand will most likely begin to taper off over the coming years (especially nitrogen fertiliser consumption)

as the country has embarked on a long-term trend towards increasing the efficiency of fertiliser application. China's demand will be

on the decline owing to environmentally friendly policies.

Regional Outlook To Soften Driven By China And India Overuse

Select Countries - Fertiliser Consumption By Type (LHS) & Application (RHS)

Sources: World Bank, FAO, Fitch Solutions

South East Asia: Agricultural Yields To Support Uptick

We estimate crop production in the region to remain broadly healthy in 2020/21 as was the case in 2019/20 with rice and palm oil

output on a steady uptrend. In the coming years, underlying trends for the agribusiness sector will be positive for fertiliser demand.

• We are particularly positive regarding demand growth in Thailand, Indonesia and emerging agribusiness countries such as

Cambodia and Myanmar, which are recording robust growth in crop output. For example, fertiliser imports in Myanmar have been

growing at a fast pace in recent years.

• Vietnam's demand will be weak owing to an excessive application of fertilisers and the slowdown in crop production growth as a

result of area cultivated and yield expansion constraints.

• The positive trends in South East Asia will be particularly positive for nitrogen demand (rice, fruit and vegetables) and potash

consumption growth (palm oil and sugar crops, for example, need more potash-based nutrients than grains).

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 27Global Summary Mining | 20210315

Fertiliser Trade Opportunities Across Asia

Select Countries - Fertiliser Trade Balance, USD '000 (2014-2019)

Note: Positive value denotes trade surplus in product category. Source: Trade Map, Fitch Solutions

China Production And Consumption: Slowdown Evident

The operating environment for China's fertiliser and pesticide sector is becoming increasingly challenging amid the rise in

environmentally friendly policies and we expect only minimal growth in Chinese ammonia and urea production in 2021. Production

has been on a declining trend as fertiliser and pesticide output trend lower. Apart from stricter policies and enforcement of rules,

elevated coal prices over recent years have pushed up the cost of urea production. As a result, the production capacity of ammonia

and urea has been contracting over recent years and, therefore, China's fertiliser exports will most likely remain on a downtrend in

the coming years. Crop production will also either decline year-on-year in 2020/21 (rice, wheat, cotton), or if it grows,

absolute output will remain below record levels seen in recent years (corn). Furthermore, the Covid-19 outbreak in the country will

lead to logistical concerns over the short term while greater efforts to ensure environment security may take centre stage. This,

coupled with an active policy to reduce the overuse of fertiliser, will lead to stagnant or decreasing usage in 2020/21 despite high

prices encouraging plantings.

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 28Global Summary Mining | 20210315

Crop Production Mostly On The Rise In 2020/21

Select Countries & Crops - Production Growth, % change y-o-y

f = Fitch Solutions forecast. Source: Local statistics, USDA, Fitch Solutions

China is a major importer of potash acquired by means of annual contracts in the second half of the calendar year. As of Q120,

China had not initiated a potash contract owing to high existing inventories in stock and this gave Chinese buyers significant room

for price manoeuvres. The contract was eventually signed on April 30 2020 at just USD220/tonne, down from USD290/tonne

signed in 2018/19. This trend encouraged major global suppliers to reduce their annual production capacity as global prices

weakened. One of China’s contracts, with Canpotex, expired in October 2020, and thus Canpotex members are no longer placing

product in Chinese warehouses. According to Nutrien management, local Chinese potash prices are higher than the April 2020

contract and inventories are relatively low, suggesting a higher-priced contract in 2021 year-on-year. However, contract

negotiations are likely to be challenging for the Canpotex members as the Consortium of Chinese buyers (Sinochem, CNAMPGC,

CNOOC) agreed to a contract price of USD247/tone CFR with the Belarussian Potash Company. Canpotex has stated that this

price is considerably below current potash price levels (which are over USD300/tonne in some cases)

Over the medium term, China's demand for fertiliser will contract, particularly in the case of nitrogen fertilisers. The authorities'

increasingly strict stance on environmental protection is impacting the use of fertiliser, as China's excessive application of inputs has

led to severe soil degradation. While we are positive on the outlook for other agricultural inputs, including machinery, seeds and

agtech adoption, the outlook for growth of fertiliser sales in China is bearish.

THIS COMMENTARY IS PUBLISHED BY FITCH SOLUTIONS COUNTRY RISK & INDUSTRY RESEARCH and is NOT a comment on Fitch Ratings' Credit Ratings. Any comments or data included in the report are solely

derived from Fitch Solutions Country Risk & Industry Research and independent sources. Fitch Ratings analysts do not share data or information with Fitch Solutions Country Risk & Industry Research.

fitchsolutions.com 29You can also read