CAPITAL MARKETS DAY 25/06/2019 - Investor Relations ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CAPITAL MARKETS DAY 25/06/2019

LEGAL DISCLAIMER & CONTACTS

The document has been prepared by Europcar Mobility Group (the “Company”). Recipients should conduct and will be solely responsible for their own investigations and analysis

of the Company. This presentation does not contain or constitute an offer of securities for sale or an invitation to invest in securities in France, the United States or any other

jurisdiction.

None of the Company nor its respective employees or officers, makes any representation or warranty, express or implied, as to the accuracy, relevance and/or completeness of

the document or any information, forward-looking statements contained herein and the Company shall not incur any liability for the information contained in, or any omissions

from, the document.

Forward-looking statements are statements that are not historical facts. These statements may include projections and estimates and their underlying assumptions, statements

regarding plans, objectives, intentions and expectations with respect to future financial results, events, operations, services, product development and potential, and statements

regarding future performance or events. Forward looking statements are generally identified by the words "expects", "anticipates", "believes", "intends", "estimates", "plans",

“projects”, “may”, “would” “should” and similar expressions. Forward-looking statements are based on the Company management's current expectations or beliefs on or about the

date of the document but are not guarantees of future performance and are subject to inherent risks, uncertainties (including without limitation, risks identified in the "Risk factors"

section of the Annual Registration Document filed with the Autorité des marchés financiers and also available on the Company's website: www.europcar-group.com) and

assumptions about Europcar Mobility Group and its subsidiaries and investments, trends in their business, future capital expenditures and acquisitions, developments in respect

of contingent liabilities, changes in economic conditions globally or in Europcar Mobility Group’s principal markets, competitive conditions in the market and regulatory factors.

Those events are uncertain; their outcome may differ from current expectations which may in turn materially affect expected results. Actual results may differ materially from those

projected or implied in these forward-looking statements. Other than as required by applicable law, the Company does not undertake to revise or update any forward-looking

statements in light of new information or future events.

INVESTOR RELATIONS

Olivier Gernandt +33.1.80.20.91.81 olivier.gernandt@europcar.com

Investor Relations +33.1.80.20.92.65 investor.relations@europcar.com

For all financial or business information, please refer to our IR website at: https://investors.europcar-group.com/

MEDIA RELATIONS

Valérie Sauteret valerie.sauteret@europcar.com

2

WITH YOU TODAY

Caroline Parot Fabrizio Ruggiero Olivier Baldassari Albéric Chopelin Luc Péligry

CEO Deputy CEO Group Chief Countries Group Chief Commercial Group Chief

Head of Business Units and Operations Officer and Customer Officer Finance Officer

Management board

3

WITH YOU TODAY: “MOBILITY TALKS” SPEAKERS

Xavier Corouge Alexandre Crosby Luc Péligry Darragh Genockey

Managing Director, Group Chief Group Chief Business Leader

Urban Mobility BU Product Officer Finance Officer Vehicle Sharing

(former Group Urban Mobility BU

Digital & Marketing officer)

4

CAPITAL MARKETS DAY 25/06/2019

MOBILITY IS

- AND HAS

ALWAYS BEEN -

A FUNDAMENTAL

NEED FOR PEOPLE

AND SOCIETIES

6

MOBILITY IS AT A

PIVOTAL POINT TODAY:

MORE PEOPLE,

MORE VEHICLES,

MORE CONGESTION,

MORE CO2 EMISSIONS.

As congestion in cities rises, existing transportation — from cars to buses to trains — can no longer keep up with the growing population.

Americans have lost an average of 97 hours a year due to congestion, according to the 2018 INRIX National Traffic Scorecard.

In 2018, it cost Americans roughly $87bn, or an average of $1,348 per driver.

7

WE ARE AT THE BEGINNING

OF A SOCIETAL REVOLUTION

MOBILITY SOLUTIONS

WILL PLAY AN ESSENTIAL PART IN IT

IT IS NOW CRITICAL TO RECONCILE

THE FUNDAMENTAL NEED THAT MOVING IS,

WITH WHAT IS AT STAKE

8

WE BELIEVE

MOBILITY

IS ALL ABOUT

ATTRACTIVE,

ALTERNATIVE

SOLUTIONS

TO CAR OWNERSHIP,

IN A RESPONSIBLE

AND SUSTAINABLE WAY

9

GOOD NEWS #1

SHARED MOBILITY IS AT THE CORE OF OUR DNA

(AND HAS BEEN SINCE 1949)

1949

10MISSION

Be the preferred

“mobility service company”

VISION by offering alternative

PURPOSE

The future needs global attractive solutions

is to deliver an experience of

mobility providers, to vehicle ownership. open mobility for all, lifting all

making people’s life easier. barriers, giving individuals as well

as groups of people easy access

to this great new world of mobility

We will play a leading solutions, whenever and wherever

they want, whatever the ride.

role in the mobility Accessibility is key: mobility

new ecosystem. should be inclusive,

not excluding.

11GOOD NEWS #2

MEGATRENDS ARE VERY PROMISING:

OUR GROUP IS IN A GROWTH STORY

12WITH WORLDWIDE LEISURE FLOWS

GLOBALIZATION,

MORE AND MORE

PEOPLE ARE

EUROPE

MOVING MORE

FREQUENTLY

FROM A TO B, +

FOR BUSINESS

OR LEISURE

PURPOSES

13MEGACITIES POPULATION DENSITY WILL AVERAGE 2.000/KM2 IN 2030,

AND THE DISTANCES TRAVELLED FROM A TO B WILL SKYROCKET.

THERE WILL BE A MASSIVE NEED OF MULTIMODAL URBAN MOBILITY SOLUTIONS.

14WE HAVE ENTERED THE SHARING ECONOMY ERA

100M

subscribers

150M

users 400 000 members 150M

400 locations subscribers

90 cities

1516

MOBILITY IS MOBILITY

NEITHER IS AN UNRELENTING

A MARKET, SOCIETAL

NOR A CATEGORY REVOLUTION

MOBILITY AS SUCH,

IS BECOMING MOBILITY IS

AN ESSENTIAL A BLESSED

SERVICE BUSINESS!

17THE ‘‘MOBILITY BUSINESS’’

2030

TODAY

16% 19%

World World

GDP, GDP,

#2 #1

18

Source: International Data (IDC), Siemens “Megacity Challenges”, World Bank, Oliver Wyman analysisMOBILITY IS A BIG CAKE AND EVERYONE WANTS A SLICE OF IT

SEAMLESS

INTEGRATED START UP

ACCESSIBILITY

MAAS

FREEDOM

PLATFORM

CONNECTED

MULTIMODALITY

PROVIDER

LOCAL AUTHORITIES

ONE APP

FLEET

MOBILE

URBAN

INTEGRATION

QUALITY

TECH OF LIFE

ECOLOGIC GLOBAL

TAILORMADE

MULTIMODALITY CO-CONSTRUCTION

19 COOPETITIONWHERE DOES

EUROPCAR MOBILITY

GROUP STAND?

20EVOLUTION OF WORLDWIDE ADDRESSABLE WHEELED MARKET

2017 +8.3% 2030

CAGR

415 1000

+4%

CAGR

€865bn €1700bn

+12.5%

450 CAGR 700

Rental / Leasing Urban Mobility

21

SOURCES: Oliver WymanOVER THE LAST 3 YEARS,

WE HAVE HEAVILY INVESTED*

TO CAPTURE GROWTH

22

*CAPEX & OPEXSTRONG REFOUNDATION OF OUR “OPERATING SYSTEMS”

(MIDDLEWARE) TO SUPPORT OUR TRANSFORMATION

Click&Go program

> digital customer

journey

NPS 110 program

New CRM

> customer satisfaction

> digital performance

ONE GROUP

CALL CENTERS Connected Vehicles

> customer care program > digital

(3C program) operations

23 STRONG GROWTH MOMENTUM SINCE 2015

2.142

2.929 251 350

+37% +39%

FY REVENUE (€M)

FY ADJUSTED CORPORATE EBITDA*

44 56.4 CAPEX DIGITAL €170M

€200M

OPEX URBAN MOBILITY €30M

+12pts

FY EUROPCAR NPS

24

NOTES: REVENUE AND ADJUSTED CORPORATE EBITDA ARE REPORTED FIGURES

EXCL. NEW MOBILITY (€M)WE ARE READY TO ADDRESS A BROADER RANGE

OF WHEELED MOBILITY USAGES…

DAY(S) HOUR HOURS

TO OR TO

WEEK(S) LESS DAY(S)

& more

RENTAL URBAN MOBILITY

25WITH VERY STRONG ASSETS

TO MOVE FORWARD

AND SEIZE THE OPPORTUNITIES

WHICH ARE AHEAD OF US…

26WE HAVE A UNIQUE, CENTRAL POSITION

Mapping of relevant players on the mobility value chain

Platform &

Vehicle Maintenance & Fleet mgt. Customer

Services

Manufacturing Repair Incl. financing Operations

MaaS

OEMs B2C Platforms

Micro-mobility

Ride-hailing/Taxi

Car sharing

Car & Van rental

Leasing

27WE SERVE OUR CUSTOMERS IN MORE THAN 130 COUNTRIES

45

2 TERRITORIES 15

TERRITORIES TERRITORIES

PARTNERS

13

TERRITORIES NORTH AMERICA

Canada

USA

ASIA

30 India

TERRITORIES China

29

Japan

TERRITORIES 7

TERRITORIES

30

TERRITO

28 RIES7.7M ACTIVE CUSTOMERS IN 2018

27%

market

share

x 2.75

29WITH 27% MARKET SHARES, WE ARE THE UNDISPUTED

CAR RENTAL LEADER IN EUROPE

Avg. Market share

27% 18% 18% 14% 13% 10%

Others

30

1. Euromonitor data, including total revenue from franchisees and vans rental market below 1Ton

Source: Euromonitor 2018, Oliver Wyman analysisWITH 60% LEISURE & 40% BUSINESS,

WE BENEFIT FROM A BALANCED POSITIONING

Rental revenue breakdown by customer group Corporate car rental market growth

2018, Worldwide, in % 2017-2030, Worldwide, in M€

+4%

CAGR 37,342

23,570

Corporates 40% 2017 2030

60% Leisure Leisure car rental market growth

2018-2030, Worldwide, in M€

71370

+8.2%

CAGR

27764

2018 2030

31 1. Includes accident replacement 2. In corporate countries

Source: Companies Annual reports, Companies investor presentation, EMobG presentations, Euromonitor, Oliver Wyman analysisWE ARE A LARGE SCALE, ASSET LIGHT FLEET MANAGER

2018

Fleet average size 315k 90% Fleet in buy back

Sales points served 1900 246€ Controlled and derisked FCPU

Number of rental days 90M

€5bn €5bn

Fleet Back

asset financing

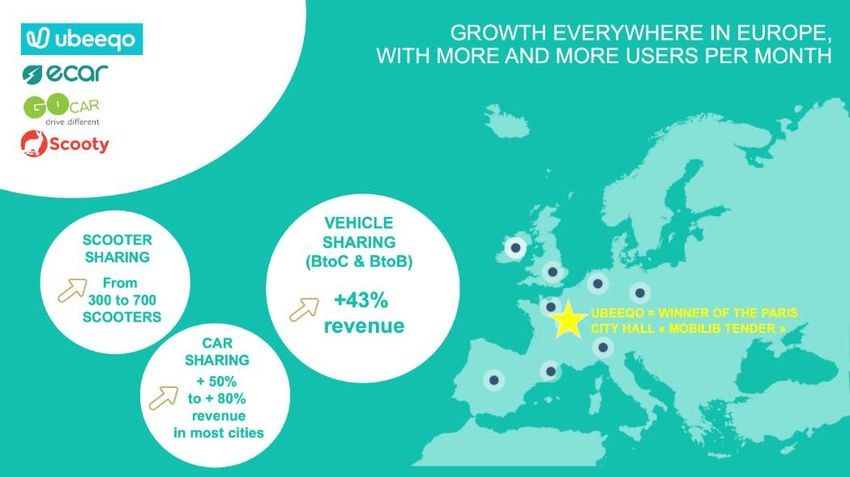

32WE ARE SCALING UP OUR URBAN MOBILITY ASSETS,

WITH VERY PROMISING PERSPECTIVES AHEAD OF US

Evolution of car sharing market worldwide Europcar Mobility Group vehicle sharing facts & figures,

2018-2025, in $USbn Q1 2019

UBEEQO’S

GROWTH RATE

+11%

IS 4 TO 5 TIMES 2018

CAGR SUPERIOR +52%

revenue

TO THE

MARKET’S ONE

10.9

5.6

2018 2025

• Ubeeqo to be break even during our journey to 2023.

But priority is first manage to seize market opportunities and take position,

then scale up to profitability. Ireland cities are already porfitable since 2018.

33

Sources: PS Market research / gminsights.comLEVERAGING THESE STRONG ASSETS,

WE ARE INVESTING TO BUILD

ONE FULLY INTEGRATED

TARGET OPERATING MODEL

& BEST CAPTURE

GROWTH OPPORTUNITIES

342023: ONE GROUP TARGET OPERATING MODEL

ONE INTEGRATED, AUGMENTED INFRASTRUCTURE

4 CORE BRANDS

ONE GLOBAL NETWORK

ONE CUSTOMER

ONE TECH BACKBONE JOURNEY

ONE ONE ENLARGED

CONNECTED CUSTOMER BASE

FLEET ONE AGILE ORGANIZATION

ONE TALENT POOL

352023

> €4.0bn

Urban

2018

+33% Mobility

X10*

2.9bn

36

*circaCAPITAL MARKETS DAY 25/06/2019

AS OF TODAY, OUR ORGANIZATION BY BUs’ IS THE ‘‘ENGINE’’

OF THE GROUP

CUSTOMERS

CARS LOW COST VANS & TRUCKS URBAN MOBILITY

DIGITAL DISTRIBUTION PLATFORMS OPERATING

MODEL

PHYSICAL PLATFORMS TODAY

38WE HAVE BUILT A POWERFUL BATTLESHIP

CUSTOMERS

CARS LOW COST VANS & TRUCKS URBAN MOBILITY

• Direct2Brand eCom • Full integration in • Started expansion, • Open car sharing focus

growth: +9 % in 2018 9 months in the flexi market, where we can get scale:

vs previous year • Double-digit covering longer Paris!

• Strongly multi-segment: growing market duration • Clear opportunity in the

B2C, B2B and B2B2C • Platform for global • Network reinforced Corporate Car Sharing

• Geographical expansion with super-sites market

expansion (India, • 1 500 cars already

Israel…) dedicated to PHV

(Uber-like) drivers

• Asset utilization centric organization at 76%

39

• Highest buyback share in the market

• Constant fleet cost optimization… AND THIS BATTLESHIP HAS BEEN ABLE TO SUPPORT OUR GROWTH

+10% +199% +29% +45%

€2.122M €388M €344M €35M

CARS LOW COST VANS & TRUCKS URBAN MOBILITY

40

2018 FY results, reported revenueWITH THESE 4 ‘‘VERTICALS’’, WE ARE WELL POSITIONED

TO FURTHER CAPTURE GROWTH

2017 +8.3% 2030

CAGR

415 1000

+4%

CAGR

€865bn €1700bn

+12.5%

450 CAGR 700

Rental / Leasing Urban Mobility

41

SOURCES: Oliver Wymanshift OUR

2023

ROADMAP

TO FURTHER

CAPTURE GROWTH

42WE HAVE SET OURSELVES AMBITIOUS GOALS

> 4bn

REVENUE

(CIRCA 10% 15M

coming ACTIVE

from Urban

Mobility) CUSTOMERS GROUP

NPS*

AT 50

43

PROFITABLE GROWTH

*Including all brands scores5 PRINCIPLES, ON WHICH WE ALL COMMIT TO ACHIEVE THESE GOALS

S peed up

High value creation

I nvest in the future

shift 2023

Focus on customers

Tech & talents-powered

44WE WILL WIN 2 BATTLES WITH 5 ACTIVATION LEVERS

1 One Brand Portfolio

AUGMENT AMPLIFY

CORE BUSINESS BUSINESS SERVICES

One Phygital Customer

Enhanced car rental 2 Journey

Develop customer experience on

the car rental market

One B2B Commercial

Enhanced van rental

Services to Corporates 3 Platform

Become the first European one-stop- Offer corporate customers a

shop for van rental offering a flexible, comprehensive platform of mobility

digital and hassle-free rental experience services, leveraging public subsidies

for all customers, specially for SME and enabling companies to improve One Connected Fleet

employees’ quality of life 4 and One Network

Scaled-up Urban Mobility

Scale-up to conquer European major

One Customer

cities with an hybrid model 5 Data Base

45THE WORLD IS OUR BATTLEGROUND 46

ENHANCE CAR RENTAL

> € 3.1 bn

€ 2.5 bn > 25%

REVENUE

• Digitisation of the customer journey

WHAT • Individualisation / Personalisation of the offer

IS FEEDING • Customer repetition

THE GROWTH? • Flexibility as a “core” element of the offer

• Global expansion

47ENHANCE VAN RENTAL

€ 0.5 bn

€ 0.35 bn > 50% REVENUE

• Digitisation of the customer journey, dedicated to the B2B world

WHAT • Flexibility as a “core” element of the offer, covering longer durations

IS FEEDING

THE GROWTH? • Proximity with higher specialization

• Selective M&A

48SCALE-UP URBAN MOBILITY

€ 0.4 / 0.5 bn

€ 0.04 bn circa X 10

revenue

• Focus and scale in big cities, where we can assure proximity (a car

WHAT within 400M in Paris) and leverage our core infrastructure

IS FEEDING • Car rental B2B focus to feed Corporate Car Sharing and ride hailing

THE GROWTH? solutions

• PHV (Uber drivers) market growth

49SERVICES TO CORPORATE

40% 45%

B2B + 5pts B2B

revenue revenue

• From business travel and car replacement to new uses cases: flexi

WHAT lease, corporate car sharing, …

IS FEEDING • Total access to the full digital customer journey

THE GROWTH? • New platforms and new loyalty program

• Entry point for the BLEISURE (business-leisure) growth

50ACHIEVE NURTURE

OPERATIONAL & ENLARGE

EXCELLENCE OUR

AS ONE CUSTOMER

GROUP BASE

Olivier Baldassari Albéric Chopelin

Group Chief Countries Group Chief Commercial

and Operations Officer And Customer Officer

51WE OPERATE

A VERY CONCRETE BUSINESS

AT A LARGE SCALE:

GRANULAR,

DAILY,

LOCALIZED,

EXPERT,

PROFITABLE

52OUR OPERATIONS AT A GLANCE

12 000 € 2.929 bn

employees revenues

7.7M

~ 70% employees clients ~ 24% of revenue

in stations 315 000 vehicles in station costs

~ 30% employees 90M rental days ~ 12% of revenue

in support functions 14M Rentals in support

~ 76% utilization rate function costs

1 900

stations directly

operated 646 000 m3

~ 35 000 = yearly water

300 stations in airports

connected cars consumption

60 stations in railway

~ 4 200 cars to wash cars

32 Supersites

8 cities with car with direct access

sharing activated ~ 4 600 Low

emission vehicles

533 KEY INITIATIVES TO SUPPORT GROWTH AND ACHIEVE OPERATIONAL

EXCELLENCE SHIFT 2023

ONE ONE ONE

OPERATIONAL CONNECTED DIGITALIZED

FRAMEWORK FLEET NETWORK

€30M support 2% margin

functions run 80% connected improvement

rate reduction vehicles by 2023 in 2023

by end 2020

54ONE OPERATIONAL FRAMEWORK

SHIFT 2023

We are standardizing our target

Countries, business units and operating model through our HQ 2020

Functions are organization pillars program

• Target Operating Models have been

defined for all main functions

BUSINESS

UNITS GLOBAL • Group Functions leadership has •€10M savings in 2019

FUNCTIONS

authority for the organization and

•€30M support functions

the processes within their function

run rate reduction by

• Business Units are integrated in end 2020

each country organization and

COUNTRIES

resources are shared

• Country Management team focus

on execution

• Discipline is a new motto

55ONE CONNECTED FLEET

SHIFT 2023

Automated fleet inventory

Geofencing based alerts

ASSETS Vehicle anomalies detection

Theft alerts

Mileage based alerts

Direct Access

Direct return CUSTOMER At least 80% connected

Enhanced safety EXPERIENCE vehicles by 2023

Enhanced Driving experience

Deskless station

STATION Turnaround process monitoring

Telemetry

OPERATION

Damage management

Performance Management

56ONE DIGITALIZED NETWORK

SHIFT 2023

Tactical Optimisation Design Optimization One digitalized Network

• Network • Airports & railways •2000 points of sales within • 1pt margin

improvement

resizing in (389) one integrated physical

by 2020

UK (199->129), • Supersites (32) network

France (315 ->246), • Retail stations (1500) •One Integrated digital • 2pts margin

• Germany and Spain • Maintenance & Infleet platform improvement

in progress •Pilot in Mallorca (5000 in 2023

/ Defleet centers (20)

• Logistic network vehicles)

optimization •Ubeeqo (3500 vehicles)

•Europcar Ireland (10200

vehicles)

•GoCar (700 vehicles)

57

•One Fleet across all brands2019 – 2023 OPERATIONAL EXCELLENCE ROADMAP

SHIFT 2023

2019 2020 2021 2022 2023

One

Arming

operational phase Execution

framework €30M run rate reduction

One

Connected Planning

Fleet 80% connected

One digitalized Planning

Network

1pt margin improvement 2pts margin improvement

58WE OPERATE

A VERY CONCRETE BUSINESS

WITH A GREAT DIVERSITY OF CUSTOMERS:

DIFFERENT CULTURES,

DIFFERENT NEEDS,

DIFFERENT USAGES AND DURATION,

DIFFERENT SATISFACTION TRIGGERS,

VALUABLE

59COMMERCIAL & CUSTOMERS KEY FACTS & FIGURES

SHIFT 2023

7.7M Active Customers 15M Active Customers

Group Customer Database Omnichannel Approach

4

Group Customer ID Core Commercial Platforms

Brands

Group CRM Platform Group Loyalty Program

3 Bn€ Revenue > 4 Bn€ Revenue

603 PRIORITIES

Mission: Lead worldwide Sales & Marketing Expertise of Europcar Mobility Group

into Excellence & Customer Centricity,

in order to nurture a profitable & sustainable growth

1 2 3

BRAND

OFFER CUSTOMER

PORTFOLIO

DESIGN ENGAGEMENT

MANAGEMENT

61AMBITION: 15M ACTIVE CUSTOMERS

x2

QUANTITATVIVE

+2 15M

+2

+2 Services to corporate

& Urban Mobility

+1 Services to

corporate

7.7 M

Enhanced

van rental

Enhanced

car rental

QUALITATIVE

2018 Incremental SMEs Business Business & Urban 2023

leisure travelers mobility

Frequency

Sessions per month per user 10 >15

Customer average spend +/- + ++ +++

62

1. In peak season, ~2 outside peak season1

BRAND

PORTFOLIO

MANAGEMENT

634 CORE BRANDS

SUSTA

SMART CONNECTED PIONEER INABL

SUSTAINABLE

E

RELIABL

FAIR FAST RELIABLE SPONTANEOUS

E

FEEL GOOD SIMPLE GREEN CITY-ZEN

64VALUE CREATION

Revenue Margin Customer

Satisfaction

Brand Differentiation Operational Excellence

Brand Stretch Centralized marketing

Enhanced Car / Van Rental Engagement System

ROI Based Decisions

Urban Mobility Focus on Profit Pools

Offer Design & innovation Pricing Power

652

OFFER

DESIGN

66OFFER DESIGN

METHOLOGY EXAMPLE: SERVICES TO CORPORATES

1. Customer Selection & 2. Value capture /

Value Proposition Profit model

5. Operating Model

3. Scope of activities

4. Strategic control

& Assets

67OFFER DESIGN | SERVICES TO CORPORATES

For Travel Managers: integrated services can simplify For employees: more mobility options are available

processes, improve visibility, reduce travel costs, etc. and the travel experience is enhanced

Invoice Policy enforcement Ride-hailing Ride and car sharing

Digitization • Premium cars & drivers • In Parking

• Longer waiting times • Publicly available

Billing Benchmarking of Car rental Micro-mobility

customers • Corporate account • Bike sharing on-site

• Negotiated prices • Public Bike sharing info.

• Special rewards

ERP Integration Instant

payment

Incentive Scheme

Rewards for generated

savings for the company

Cost Reporting

Virtual Credit Card

Loyalty program

Rewards for frequent travellers

VAT claim Insurance applicable on leisure account

683

CUSTOMER

ENGAGEMENT

69CUSTOMER ENGAGEMENT

1 2 3 4 5 6

DESIGN ENLARGE CREATE CONSOLIDATE LAUNCH MONITOR

PHYGITAL CUSTOMER STICKYNESS A UNIQUE COMMERCIAL CUSTOMER

CUSTOMER BASE CUSTOMER ID OFFENSIVES SATISFACTION

JOURNEY

Group prototype Business CRM Cross-selling Specific platforms NPS 110 Program

travelers, SMEs, Personalization Packaged offers for Corporates, Reputation

Omnichannel

Business & urban & loyalty program Multibrand forces B2G & SMEs

Group CX Gate mobility Integration Boost cross seliing

70CUSTOMER ENGAGEMENT

ENHANCE PERSONALIZATION DIGITALIZE THE CUSTOMER JOURNEY

The right target at the right moment Phygital seamless experience defined at

brand level and optimized at Group level

+ 20% revenues through personalized • User Friendly app

web experience • Digital car check & return

• Click & Go, …

+15% revenues through personalized

upsells travel

Create

INCREASE FREQUENCY Stickyness DESIGN A BEST IN CLASS

2018 sessions per month per user LOYALTY PROGRAM in 2020

#, in US

• Bridge B2B & B2C

21

• Increase cross-selling

18

• No one size fits all program

10 9 • Smart Group contact plan

5

>1

Mobility Food Public Ride- Car Traditional

mapping Takeaway Transport hailing sharing car rental

71

Note: Index built using estimates that at least 21% of users take ride-hailing or taxi services at least once a month per HSBC broker report and that average number of sessions per month for Lyft or Uber is 9 per Verto. 42% of users take food takeaway at least monthly, ratio for ride-hailing is

applied to food takeaway to compute food takeaway number of sessions; Similarly, average frequency of use of public transport of 2,7 times per month vs. 2,3 for Uber or Lyft, this ratio is used to assess the number of sessions for public transport apps; and metrics for “other” categories

exclude companies separately called out in the same industry; sample of 20 companies with 2016 and 2018 data, 9 companies with 2017 and 2018 data, and 10 companies with 2018 data only Source: Verto Indexes 2016, 2017 and 2018; Oliver Wyman analysisCONSOLIDATE A UNIQUE CUSTOMER ID WITH EXISTING ASSETS

… creating a key asset for the

From 5 independent customer bases … … to a single group customer ID …

group to leverage through digital

EMobG’s customer data bases One consolidated database

Improved customer

Corporate

EMobG

1 acquisition

countries1

consolidated

Phoenix customer database

Franchisees Enhanced retention

In-house

or

Rentway

…

Incremental revenue

Bubirent Sigger

with with with

1 customer = X profiles 1 customer = 1 profile 1 Group Contact Plan

72AS A CONCLUSION… 73

3 PRIORITIES INTO 15M ACTIVE CUSTOMERS

1 2 3

BRAND

OFFER CUSTOMER

PORTFOLIO

DESIGN ENGAGEMENT

MANAGEMENT

• Focus on 4 Core Brands • Innovation • Phygital Customer Journey

• Empowered Brands with unique • Cross selling • Unique Customer Database

& differentiated identity • Upselling • Global CRM Platform / Personalization

• Pricing power • Bundled offers • Group Customer ID

• Centralized marketing • Service to Corporates • Loyalty Program

• Systematic ROI decisions • E Commerce & Direct Sales • NPS 110 & Reputation

74FINANCE SECTION

GROUP KEY FINANCIALS OVER LAST FOUR YEARS

REVENUE (€M) ADJUSTED CORPORATE EBITDA excl. New Mobility (€M)

Growth +39%

Growth +37%

350

2,929

251

2,142

FY 2015 FY 2018 FY 2015 FY 2018

CORPORATE FREE CASH FLOW (€M)

Growth +57%

135

• c.€470m of Corporate FCF

86 generated over 2015-18

• Total shareholder returns over the

last four years of c.€200m

FY 2015 FY 2018

Strong growth in all three key financials indicators

76

NOTES: REVENUE, ADJUSTED CORPORATE EBITDA AND CORPORATE FREE CASH FLOW ARE REPORTED FIGURESSTRONG OPERATIONAL GROUP PERFORMANCE OVER LAST 4 YEARS

RENTAL DAY VOLUME (MILLION) FLEET COSTS PER UNIT PER MONTH (€)

Growth +54% Change (11)%

88 253

57

226

FY 2015 FY 2018 FY 2015 FY 2018

UTILIZATION RATE (%) AVERAGE FLEET (THOUSAND)

Growth +54%

76.1% 76.1%

316

205

FY 2015 FY 2018 FY 2015 FY 2018

High capability to manage superior growth with resilient and flexible operating model

77

NOTES: FIGURES AT CONSTANT EXCHANGE RATEFOCUS ON GOLDCAR AND BUCHBINDER ACQUISITION SYNERGIES

2018 2019 2020 %1 2018 2019 2020 %1

≥ Fleet

purchasing 66%

33%

c.€10m c.€2m

33% Fleet financing N/A N/A N/A

synergies synergies

already attained already attained

in 2018 for in 2018 for

Goldcar ≤ Buchbinder

Other 33%

33%

Total

100% synergies 100%

Well on track to reach over €30m synergies for Goldcar and over €10m synergies for Buchbinder by 2020

78

NOTE: 1 - PERCENTAGE OF TOTAL ESTIMATED SYNERGIESSELF-HELP MEASURES

TOTAL

HQ EXPECTED NETWORK

2020 SYNERGIES OPTIMIZATION

2%

OF GROUP REVENUE

BY 2020

3%

OF GROUP REVENUE

BY 2023

792020 CORPORATE EBITDA MARGIN PROSPECTS

Corporate EBITDA margin bridge between 2018 and 2020

Low end In line

with current market

Including (0.9)% of

consensus

UM impact

+0.9-1.0%

+0.7-1.0%

+0.7-1.0% 12.5% - 13.0%

11.2% (0.6-0.7)%

(0.4-0.6)%

-

2018 Network HQ efficiencies Synergies Marketing & Macro environment 2020

optimization Digitization

Accelerating self help measures confirmed on a 2021 run rate basis

80 Target of Corporate EBITDA margin range between 12.5% and 13.0% by 2020GROUP REVENUE MID-TERM AMBITION

Revenue bridge between 2018 and 2023

>€4bn

CAGR +50%

2018-23 +8%

+8%

+3%

€2.9bn

2018 Cars Vans & Trucks Low Cost Urban Mobility M&A 2023

New Group Revenue target of above €4bn by 2023 implying a CAGR of above 10%

81 Urban Mobility BU expected to grow Revenue by at least 50% per annum over the periodCASH ALLOCATION PROSPECTS

Growth acceleration

M&A Selective & strategic focus on bolt-on and international expansion

Maximum 2.5% of Group Revenue in 2020-2023

NON-FLEET CAPEX

Over 70% of which into Group digitization

Shareholder returns

DIVIDEND POLICY Maintain the current dividend policy

& TACTICAL SBB Funded by excess cash when appropriate

Balanced cash allocation between growth acceleration and shareholder returns

82FINANCIAL AMBITION FOR 2023

• Organic Growth

REVENUE • Urban Mobility

> €4bn Group Revenue

• M&A / Strategic partnerships

• Fleet Costs

PROFITABILITY • Network Rationalisation > €500m Corporate EBITDA *

• HQ Optimisation

• Strong FCF Generation

LEVERAGE • Ability to deleverage by around [2.0-2.5x] Corporate net leverage

0.5x EBITDA per annum

83

NOTE: * CORPORATE EBITDA EXCLUDES IMPACT OF IFRS 16 ; INCLUDING IFRS 16, THIS FIGURE WOULD BE CLOSER TO €600 MILLIONKEY

TAKE-AWAYS

84WE HAVE A UNIQUE, CENTRAL POSITION

Mapping of relevant players on the mobility value chain

Platform &

Vehicle Maintenance & Fleet mgt. Customer

Services

Manufacturing Repair Incl. financing Operations

MaaS

OEMs B2C Platforms

Micro-mobility

Ride-hailing/Taxi

Car sharing

Car & Van rental

Leasing

85Car rentals Car manufacturers New mobility

-1% 19-23

1% 10% 17% -4% 4% 17% 66% 143%

69%

2016 - 2018

Sales CAGR

median

5% 8% 12% 13% 4% 7% 8%

EBITDA

Margin 2018

(EBIT for car

manufacturers)

median

0% 0% 3% 0% 2% 5% -19% -16%

-14%

FCF/Sales

2018

median

1.5x 1.8x 2x 2.4x 0.2x 1x 1.4x 6.7x 6.8x

EV/Sales

2019e

median 865 PRINCIPLES, ON WHICH WE ALL COMMIT TO EXECUTE OUR 2023

ROADMAP

S peed up

High value creation

I nvest in the future

shift 2023

F ocus on customers

T ech & talents-powered

87WE HAVE SET OURSELVES AMBITIOUS GOALS

> 4bn

REVENUE

(CIRCA 10% 15M

coming ACTIVE

from Urban

Mobility) CUSTOMERS GROUP

NPS*

AT 50

88

PROFITABLE GROWTH

*Including all brands scores2023: ONE GROUP TARGET OPERATING MODEL

ONE INTEGRATED, AUGMENTED INFRASTRUCTURE

4 CORE BRANDS

ONE GLOBAL NETWORK

ONE CUSTOMER

ONE TECH BACKBONE JOURNEY

ONE ONE ENLARGED

CONNECTED CUSTOMER BASE

FLEET ONE AGILE ORGANIZATION

ONE TALENT POOL

892023

> €4.0bn

Urban

2018

+33% Mobility

X10*

ADJUSTED

CORPORATE

2.9bn EBITDA

> €500M

90

*circaQ&A 91

WITH YOU TODAY: “MOBILITY TALKS” SPEAKERS

Xavier Corouge Alexandre Crosby Luc Peligry Darragh Genockey

Managing Director, Group Chief Group Chief Business Leader

Urban Mobility BU Product Officer Finance Officer Vehicle Sharing

(former Group Urban Mobility BU

Digital & Marketing officer)

How to build a Discovering our Understanding our How to build a

compelling digital Product organization Group’s debt and profitable car sharing

customer journey and our Connected refinancing structure business (Ubeeco and

Cars product lines it affiliate GoCar)

92CAPITAL MARKETS DAY 25/06/2019

APPENDIX

You can also read