MONTHLY INVESTMENT INSIGHTS - MAY 2019 - PSG

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MONTHLY INVESTMENT INSIGHTS MAY 2019

Contents 1. The monthly interview – Chair of the ANC sub-committee on economic transformation, Enoch Godongwana 3 2. Tactical asset allocation preferences 5 3. Market commentary 6 4. Local unit trust solutions 8 5. Offshore unit trust solutions 13 6. PSG Wealth equity portfolios 20 7. Other publications 26 2 | PAGE PSG Wealth | Monthly Insights - May 2019

The monthly interview

At the PSG Annual Conference held earlier this month, Bruce Whitfield, financial journalist, interviewed Enoch

Godongwana, chair of the ANC sub-committee on economic transformation. His responses highlight the

importance of correcting the ruling party’s mistakes and rebuilding the ANC’s stature after the 2019 general

elections.

What’s your take on the election Tell us a bit more about land redistribution, how

outcome, are you concerned will it not endanger the economy as the president

about the latest results? indicated?

The voter turnout wasn’t as good as I Part of the problem in the ANC is that we need to address

would have liked, but I am not worried people not doing what they are meant to, instead of the

Enoch Godongwana. Chair of

about the results. I’m already preparing policies. On the ANC’s priority list, land is number 30.

the ANC sub-committee on for the inauguration of President Cyril There’s also a conceptual difference between the ANC

economic transformation

Ramaphosa on 25 May and preparing and the EFF. The EFF wants the nationalisation of land – all

for his state of the nation address on 20 June. land. What the ANC wants to achieve is redistribution.

Are the EFF and ANC separate, or do we see a union In other words, you take land for public purposes; not just

of ideologies? because you want it in state hands. There is already too

The truth of the matter is that we fought for these much land in state hands that isn’t used productively. In

elections with our backs against the wall. I said to the EFF fact, our target is to start redistributing land that’s in the

that once they let us win these elections, there’s no going hands of the state.

back. Our preoccupation going forward must be to correct

our mistakes and rebuild our stature as an organisation. Decades later and we can’t even undo District 6,

a small part of the country where people were

The ANC has seen its support slide, and we’ve seen forcibly removed. What hope is there for fair and

low voter turnout. Have people lost faith in the equitable restitution, redistribution and correction

political process? of the past when we can’t fix one small example?

This is not a South African phenomenon, but a global The constitution talks about three pillars. The first one is

phenomenon – e.g. also in the UK. Once democracy restitution and we have made progress, but it is taking

matures, people lose interest in participating in the political longer than we think. Our focus is more on redistribution

process. than on restitution, and restitution will take another 109

years. Another pillar of this is tenure. In rural areas, we

The EFF has forced the ANC’s hand on policy positions have permission to occupy, we don’t have titles. That’s the

very effectively, e.g. the land issue, nationalisation kind of transformation we need.

of the South African Reserve Bank (SARB), would

you agree? What about the power of traditional leaders,

I would imagine that’s not correct. There’s too much having a say of who gets to stay where? Surely that

speculation around the role of the EFF. Its leaders still have is something in a 21st democracy that has to change.

close ties to people in the ANC. So, whatever happens in In the ANC, we’ve adopted a model of one size fits all.

the ANC, leaks [out to the EFF]. Julius Malema will then But the power of the traditional leaders in KZN is not the

rush out and announce what he hears. Then people think same as elsewhere. Yet, people extrapolate this power.

Malema is driving the agenda. On the nationalisation of What has failed is not economic policy; what has failed is

the SARB, I suspect that some of the shareholders of the implementation.

SARB want the bank to be nationalized, because they

want to extract some benefit. This debate was initiated After the Global Financial Crisis (GFC), we saw a temporary

in 2010. recovery, but this was short-lived. You are not going to

have social cohesion and stability until we ensure the

It is perceived that the ANC is seen to act according economy grows.

to the whim of the EFF, e.g. Julius Malema calls for

the nationalisation of the SARB and suddenly the The first issue: How do we build confidence in the mind

ANC has a vote on it and EFF members are seen to of South Africans, and investors?

lead it, what’s your take on this?

Malema was putting us on the spot. He simply moved a The second issue: What are the key structural constraints

motion that the ANC took to parliament after we passed we need to address? Do we need to amend any regulation

the resolution – it wasn’t the EFF’s resolution. so that the private sector can put money into the economy?

The opinions expressed in this interview are the opinions of the interviewee and not necessarily those of PSG and do not constitute advice. Although the utmost care has

been taken in the research and preparation of this document, no responsibility can be taken for actions taken on information in this interview.

3 | PAGE PSG Wealth | Monthly Insights - May 2019

The monthly interview

Third: How do we build a partnership between business Why should people have faith in the ANC’s

and government? policymaking structures if one guy on his way out

can make such a snap decision?

What about prescribed assets? On the economic front, since 1992, we’ve had consistent

I write these resolutions carefully when I do so. The leadership that’s been producing rational policies. We’ve

resolution on prescribed assets says ‘investigate’. There is had our challenges recently, that’s a different matter,

a perception that we want to take money, loot it and put but generally policy has been focused on growing the

it into Eksom. But the first thing you must understand: economy and doing the right thing. Our current leadership

we have not even started the process of investigating. Not and president are focused on doing the right thing.

every resolution gets implemented.

Why do many in the ANC not support the notion of

In what aspect would the notion of prescribed eliminating State-Owned Enterprises (SOEs)? One

assets be positive? Asset managers can currently gets the sense the broader ANC doesn’t actually

invest in these assets, but they don’t. have a clear single vision for this economy.

How it was applied in the past was destructive. This is not The ANC does have a clear single vision. The ANC’s position

a good template. This is why we need to investigate. We has not changed since 1992, contained in a document

need a better template if we decide to implement. called ‘Ready to govern’. That document says that we

will be guided by balance of evidence; facts. We are not

How then do we fund coal in SA? religious about nationalisation or privatisation. That is the

The outcome of the energy plan will be what is going to position as it stands. There is nothing in ANC policy which

be our energy mix going forward. We need to conclude is against privatisation.

this discussion. We have six billion tons of coal in this

country. There is currently research underway to generate Is there a chance that Moody’s might lower our

clean coal. We cannot say we will not be part of it. credit rating to so-called ‘junk status’? Can we

avoid this?

Why does policymaking take so long in SA? I am praying that we avoid this. Moody’s has been rational.

Policymaking in a democratic environment with the President Ramaphosa has to say a number of things and

constitution we have, takes this long. And anyone can take a number of actions to take South Africans with us.

contest a process in court.

Is around 57% (as currently indicated) of the vote

SA now has a free education liability we cannot a strong enough mandate for Ramaphosa to grow

afford. Yet Jacob Zuma can make an instant this country and to put the challenges of the last

guarantee that we can offer this, a decision that did decade behind us?

not follow the appropriate process. Yes, for me this is strong enough. People are fearful he

A committee chaired by Naledi Pandor has been working will be undermined internally. I can tell you now there’s

on this matter. They came to the conclusion that we no such (problem). Anyone who is going to try and make

needed to fund students in need. On the eve of the Nasrec Ramaphosa’s life difficult will also run for cover.

conference, Zuma made that announcement. Which was

unfortunate.

The opinions expressed in this interview are the opinions of the interviewee and not necessarily those of PSG and do not constitute advice. Although the utmost care has

been taken in the research and preparation of this document, no responsibility can be taken for actions taken on information in this interview.

4 | PAGE PSG Wealth | Monthly Insights - May 2019

Tactical asset allocation preferences

EMERGING EQUITY DEVELOPED

South Africa ITY Global

U PRO

EQ PER

Cyclical Defensive TY

sive Retail

Defen

Challenging economic conditions persist. l The inverted yield curve in the US

Liquidity in the event of a market shock clica continues to make news headlines every

Cy

remains a concern. l Re other day. This is simply because it acts

ntia sid

en as a strong leading indicator, but the lead

TY

s ide tia

Re

ER

l can also be relatively long.

OP

Go

BO

PR

ve

rn

ND

m

Oversupply and lagging demand are

en

S

t

causing headwinds in the retail property Particularly in the US, stronger growth

Cre

l

space. Here we are very cautious with our

tai

favours credit over government bonds,

dit

Re

allocations. although there exists a caveat for high

quality, investment grade exposure, and

it

very selective buying.

USD

Cred

BONDS

CURRENCY

Our current view on government bonds has

t

Governmen

changed to neutral due to a decline in the

GBP

The USD seems too strong, while

yield curve.

the GBP and EUR seems too weak in

relation to the USD.

CASH

ZAR

EUR

Strategic asset allocation

Tactical asset allocation

Cash is the least striking local asset class as Changes this month

valuations across all other asset classes are

generally very attractive.

Overweight: Neutral: Underweight:

Tactical recommendation to Tactical recommendation to Tactical recommendation to

hold more of the asset class hold the asset class in line hold less of the asset class

than specified in the with its weight in the than specified in the

strategic asset allocation strategic asset allocation strategic asset allocation

Bottom line

• Tactically, we remain bullish on equities on the domestic over preceding years, especially in cases where the included most of the bad news. Everything considered, investments like property.

front. We think the market offers value, but only when outlook for earnings growth is more uncertain. Equities we recognise the higher yields, but remain cautious • We are overweight on domestic government bonds

you adjust valuations to remove some of the more still offer the greatest opportunity set for longer-term about the asset class as funding pressure could well because their yields are attractive.

expensive counters. We think there is particular value investments. accelerate in an increasing interest rate environment. • Domestic cash remains unattractive from a long-

in selected small and mid-cap stocks if attended to • We are marginally negative on domestic property at Our view on global property remains negative despite term wealth creation perspective, although the

carefully. We caution against counters which have this stage. The fundamentals truly look dire, but many robust global growth, especially as the potential rate diversification and risk management benefits remain

been significant beneficiaries of severe rand weakness counters are also trading at levels that seem to have hikes could be a substantial deterrent to bond proxy attractive.

5 | PAGE PSG Wealth | Monthly Insights - May 2019

Market commentary

In their monthly review, Schroders notes that global equity markets advanced in April, boosted by a continued

dovish tone from key central banks, together with better-than-expected economic data. GDP growth in the US

over the first quarter supported US equity performance while emerging markets kept their nerve amid mounting

pressure from the threat of a slowing global economy. South Africa pushed the MSCI Emerging Markets Index

higher as equities surged in anticipation of the 6th general election. US 10-year treasury yields bounced back from

their lowest level in over a year in April, following the release of positive data as the US economy continued to

grow. Strong US and Chinese economic data enhanced government bond yields, increasing investor appetite for

riskier assets.

JSE All Share Index - April 2019

60 500

60 000 3.41%

59 500

59 000

58 500

58 000

57 500

57 000

56 500

56 000

55 500

55 000

54 500

54 000

53 500

53 000

52 500 1.34% 1.12% 0.74% 0.50%

52 000

51 500 The JSE closed up on South African markets The JSE closed in the red on South African markets closed

51 000 3 April after Moody’s closed in the green on 16 24 April, weighed down by in the red on 25 April, pulled

kept their current credit April, boosted by broad broad-based losses in the down by losses in mining

50 500

rating for South Africa based gains in gold mining retail and banking sectors. sector stocks.

50 000 unchanged. and retail sector stocks.

49 500

49 000

01 April 04 April 07 April 10 April 13 April 16 April 19 April 22 April 25 April 28 April

Source: Bloomberg

Domestic key moves Global key moves

South Africa’s unemployment rate went up to US

27.60% 27.60% in 1Q19, compared to 27.10% in the

previous quarter. The number of unemployed persons US manufacturing production went down by

increased by 62 thousand to 6.20 million, marking the 0.50% 0.50% in April compared to market predictions

highest jobless rate since the 3Q17. of a 0.10% increase. This decline can be attributed to

a sizable drop in factory output as the production of

Local retail sales took a 0.70% knock in March automobiles dropped over the last few months.

0.70%

compared to a 0.60% increase in the previous

month. Annually, retail sales rose by 0.20% in March US import prices edged 0.20% higher in April,

0.20%

following an upwardly revised 1.40% increase in following a 0.60% gain in March and missing

February. market forecasts of a 0.70% gain.

6 | PAGE PSG Wealth | Monthly Insights - May 2019

Market commentary

EU Japan

Eurozone’s inflation rate for April was in line Japan’s producer prices increased to 101.80

0.70% 101.80

with market predictions rising by 0.70%, index points in April from 101.50 in March. On

compared to a 1% increase in March. an annual basis, producer prices went up by 1.20% over

the same period, slightly missing market forecasts of

Following a downwardly revised 0.10% 1.10%.

0.10% decrease in February, industrial production in

the Eurozone declined by 0.30% in March, on par with Preliminary estimates showed that Japan’s

0.50%

market expectations. GDP expanded by 0.50% in the first quarter of

2019, well above market expectations of a 0.10%

China decline.

Decelerating from an 8.50% rise in March,

5.40%

China’s industrial production figure went up

by 5.40% y/y, missing market expectations of a 6.50%

gain.

Missing market projections of an 8.60%

7.20%

increase, Chinese retail sales surged 7.20% y/y

in April from a month earlier.

7 | PAGE PSG Wealth | Monthly Insights - May 2019

PSG Wealth Fund of Funds Solutions

Local funds

Performance table

Fund 6-Month 1-Year 2-Years 3-Years 4-Years 5-Years

PSG Wealth Enhanced Interest D 3.94% 8.02% 8.03% 8.09% 7.86% 7.52%

PSG Wealth Income FoF D 4.24% 7.45% 7.91% 8.31% 8.10% 8.14%

PSG Wealth Preserver FoF D 4.88% 5.79% 6.11% 6.23% 6.37% 7.41%

PSG Wealth Moderate FoF D 6.22% 4.79% 5.53% 5.65% 5.47% 7.09%

PSG Wealth Creator FoF D 8.17% 2.58% 4.58% 5.20% 3.46% 5.46%

Source: PSG Wealth research team

Local fund performance

12.00%

10.00%

8.00%

6.00%

4.00%

2.00%

0.00%

6-Month 1-Year 2-Years 3-Years 5-Years

PSG Wealth Enhanced Interest D PSG Wealth Income FoF D PSG Wealth Preserver FoF D PSG Wealth Moderate FoF D PSG Wealth Creator FoF D

Source: PSG Wealth research team data as at 30 April 2019 *Dots represent the relevant benchmark

Disclaimer: All performance is reported in ZAR unless specified otherwise

8 | PAGE PSG Wealth | Monthly Insights - May 2019

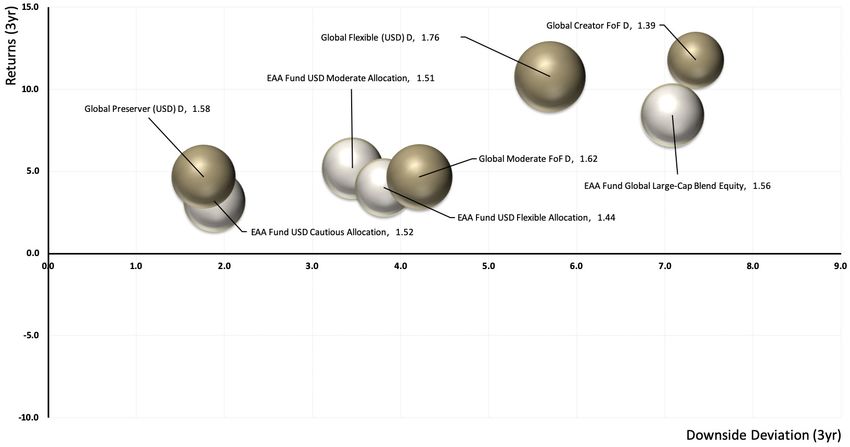

PSG Wealth Domestic Solutions

PSG Wealth Local Fund of Funds bubble chart

15.0

Returns (3yr)

Income FoF D, 0.84 Global Creator FF D, 1.20

SA MA Income, 0.94 Preserver FoF D, 1.14

Global Equity General, 1.46

10.0

Moderate FoF D, 1.20

Creator FoF D, 1.28

5.0

Enhanced Interest D, 0.49 SA MA Low Equity, 1.46

Global MA Flexible, 1.89

0.0

-2.0 0.0 2.0 4.0 6.0 8.0 10.0 12.0

SA IB Money Market, 0.40 Global Moderate FF D, 1.44

SA MA High Equity, 1.50 SA Equity General, 1.15

-5.0

-10.0

-15.0

Downside Deviation (3yr)

Source: PSG Wealth research team

HOW TO READ THE BUBBLE CHARTS

Shows TER which is an indication of cost. The

Vertical axis Shows the return of each fund Size of the bubble TERs for the fund benchmarks are assumed to

be 1.14% including VAT.

Horizontal axis Shows the downside deviation which is a measure of Grey bubbles Indicate relevant fund benchmarks

downside risk that focuses on returns that fall below a

minimum threshold or minimum acceptable return (MAR) Gold bubbles Represent PSG Wealth EB solutions

Disclaimer: All performance is reported in ZAR unless specified otherwise

9 | PAGE PSG Wealth | Monthly Insights - May 2019

PSG Wealth Domestic Solutions

PSG Wealth Enhanced Interest Fund PSG Wealth Income FoF

• The PSG Wealth Enhanced Interest Fund delivered • The PSG Wealth Income FoF delivered a return of

a return of 0.68% for April 2019, outperforming 0.94% for April 2019, compared to the 0.64% of its

the South Africa IB Money Market sector average benchmark, the Stefi 12 Months NCD.

benchmark that delivered a return of 0.55% over • The PSG Wealth Income FoF has an investment

the same period. horizon of two years, and it has underperformed

• This fund has an investment horizon of one year its benchmark with 7.91% against 8.05% over the

and has outperformed its benchmark with 8.02% two-year period and is ranked 48th out of 73 funds

against 7.41% over a one-year period. over this period.

• The fund has also outperformed its benchmark over • This fund also delivered first, second or third quartile

all measurement periods. performances for all measurement periods over two

years.

Asset allocation

Asset allocation

Domestic cash and money market, 45.25

Domestic bonds, 39.26

Foreign bonds, 4.36

Domestic property, 2.93

Domestic cash and money market, 100

Foreign cash and money market, 2.10

Domestic equity, 1.58

Domestic other, 1.30

Foreign equity, 1.21

Foreign other, 1.13

Foreign property, 0.87

Source: PSG Wealth research team

Source: PSG Wealth research team

Risk and expectations: We are confident the fund will

continue to deliver returns in access of money market rates Risk and expectations: We expected that higher inflation

to reduce the negative effects of high inflation on cash. and rising interest rates could be a drag on performance

Radar: No funds on the radar screen. over the short-term, but current indications are that the

Changes: There are no changes to the underlying funds. underlying portfolio managers are able to take advantage

of the higher yields on short-term instruments to deliver

attractive returns close to the top of the inflation cycle. We

are confident that the underlying portfolio managers will

continue to deliver attractive above average returns until

well after the interest rate cycle has peaked.

Radar: The Prudential Enhanced Income Fund and the

PSG Diversified Income Fund were removed from the

radar screen.

Changes: No changes to underlying funds.

10 | PAGE PSG Wealth | Monthly Insights - May 2019PSG Wealth Domestic Solutions

PSG Wealth Preserver FoF PSG Wealth Moderate FoF

• The PSG Wealth Preserver FoF delivered a return of • The PSG Wealth Moderate FoF delivered a return of

1.81% for April 2019, compared to the 1.06% of its 2.41% for April 2019, compared to the 2.58% of its

performance target of CPI plus three percent. benchmark, the South African MA High Equity sector

• This FoF has an investment horizon of three years, average.

and it has underperformed CPI plus three percent • This FoF has an investment horizon of five years and

with 6.23% against 7.98% over this period. has outperformed its benchmark with 7.09% against

• The fund outperformed the 5.61% of the South 5.75% over the five-year period. It is also ranked 19th

African MA Low Equity sector average over the out of 100 funds over this period.

three-year period and is ranked 40th out of 120 funds • It also delivered first or second quartile performances

over this period. for all measurement periods over six months.

Asset allocation Asset allocation

Domestic bonds, 31.04

Domestic equity, 41.26

Domestic cash and money market, 20.78

Foreign equity, 24.36

Domestic equity, 20.12

Domestic bonds, 18.67

Foreign equity, 16.06

Domestic cash and money market, 6.31

Domestic property, 5.32

Domestic property, 4.42

Foreign bonds, 2.79

Foreign property, 1.25

Foreign cash and money market, 1.97

Foreign bonds, 1.19

Foreign property, 1.29

Domestic other, 0.52

Foreign other, 0.55

Domestic other, 0.06 Foreign cash and money market, 0.02

Source: PSG Wealth research team Source: PSG Wealth research team

Risk and expectations: The PSG Wealth Preserver FoF

can hold up to a total of 40% in domestic equities and Risk and expectations: The PSG Wealth Moderate

offshore equities and may deliver negative short-term FoF may hold up to a total of 75% in domestic equities

performances in sharp equity corrections or equity bear and offshore equities and could deliver negative short-

markets. We are, however, confident that the fund term performances in sharp equity corrections or equity

will always deliver positive returns over the preferred bear markets. We are, however, confident that the fund

investment period of three years and longer, and that it will always deliver positive returns over the preferred

will protect the capital of clients during severe negative investment period of five years and longer, and that it will

market corrections. continue to deliver above-average long-term returns with

Radar: The PSG Stable Fund remains on the radar screen. below average risk overall market cycles.

Changes: No changes to underlying funds. Radar: The PSG Balanced Fund remains on the radar

screen.

Changes: No changes to underlying funds.

11 | PAGE PSG Wealth | Monthly Insights - May 2019PSG Wealth Domestic Solutions

PSG Wealth Creator FoF

• The PSG Wealth Creator FoF delivered a return of

Risk and expectations: Although the outlook for

3.10% for April 2019, compared to the 3.99% of

equities is still uncertain, we are confident that the relative

its benchmark, the South African EQ General sector performance of the underlying managers in the fund will

average. continue to improve in the near future. The managers are

• The FoF has an investment horizon of five years and all active managers that have demonstrated the ability

longer, and has underperformed its benchmark with to add alpha through careful share selection, particularly

5.46% against the 4.04% over the five-year period. during turbulent equity markets. This fund will always

It is also ranked 38th out of 98 funds over this period. maintain an equity exposure of close to 100% in domestic

• It also delivered second quartile performances for all and offshore equities. It will deliver negative performances

measurement periods longer than six months. in sharp equity corrections or equity bear markets. We

are, however, confident that the fund will always deliver

positive returns over the preferred investment period of

Asset allocation five years and longer. It will continue to deliver above-

average long-term returns with below-average risk overall

market cycles.

Radar: The PSG Equity Fund remains on the radar

Domestic equity, 80.53 screen.

Foreign equity, 14.29 Changes: No changes to underlying funds.

Domestic property, 2.31

Domestic cash and money market, 2.03

Foreign property, 0.51

Foreign cash and money market, 0.32

Source: PSG Wealth research team

12 | PAGE PSG Wealth | Monthly Insights - May 2019PSG Wealth Offshore Solutions

Offshore funds

Performance table

Reported in USD

Fund 6-Month 1-Year 2-Years 3-Years 4-Years 5-Years

PSG Wealth Global Preserver FoF D USD 4.70% 3.81% 3.30% 4.67% 3.40% 3.46%

PSG Wealth Global Moderate FoF D USD 5.92% 0.86% 3.98% 4.65% 1.72% 2.03%

PSG Wealth Global Flexible FoF D USD 10.63% 8.83% 9.30% 10.77% 7.63% 6.96%

PSG Wealth Global Creator FoF D 11.57% 8.67% 10.86% 11.78% 7.86% 7.72%

Reported in GBP

Fund 6-Month 1-Year 2-Years 3-Years 4-Years 5-Years

PSG Wealth Global Preserver FoF D GBP 2.51% 7.32% 3.00% 7.38% 6.36% 6.84%

PSG Wealth Global Flexible FoF D GBP 7.95% 13.85% 8.05% 13.68% 10.69% 11.66%

Source: PSG Wealth research team

Offshore funds performance

14.00%

12.00%

10.00%

8.00%

6.00%

4.00%

2.00%

0.00%

3-Month 6-Month 1-Year 2-Years 3-Years 5-Years

PSG Wealth Global Preserver FoF D USD PSG Wealth Global Moderate FoF D USD PSG Wealth Flexible FoF D USD PSG Wealth Global Creator FoF D

Source: PSG Wealth research team data as at 30 April 2019 *Dots represent the relevant benchmark

All performance is reported in USD unless specified otherwise.

13 | PAGE PSG Wealth | Monthly Insights - May 2019PSG Wealth Offshore Solutions

PSG Wealth Offshore Fund of Funds (USD)

Source: PSG Wealth research team

PSG Wealth Offshore Fund of Funds (GBP)

Source: PSG Wealth research team

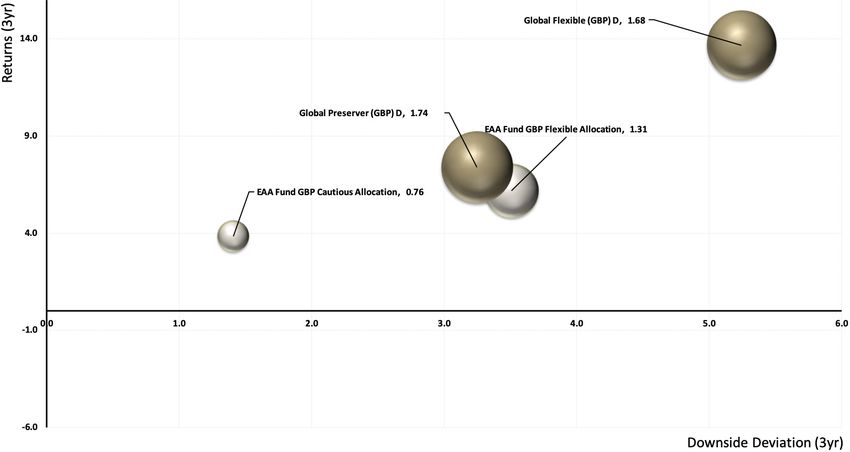

HOW TO READ THE BUBBLE CHARTS

Vertical axis Shows the return of each fund Size of the bubble Shows TER which is an indication of cost

Horizontal axis Shows the downside deviation which is a measure of Grey bubbles Indicate fund peers

downside risk that focuses on returns that fall below a

minimum threshold or minimum acceptable return (MAR) Gold bubbles Represent PSG Wealth solutions

14 | PAGE PSG Wealth | Monthly Insights - May 2019PSG Wealth Offshore Solutions

PSG Wealth Global Preserver FoF (USD)

• The PSG Wealth Global Preserver FoF USD returned 1%

for April in line with the benchmark, the Morningstar Risk and expectation: The portfolio has a high equity

EAA Funds USD Cautious Allocation sector average. allocation relative to peers and could underperform during

• The PSG Wealth Global Preserver FoF USD ranked periods of strong equity market declines, conversely

the portfolio will perform well when equity markets

in the second quartile of its global sector over the

outperform other asset classes. Rising global interest rates

previous month and is ranked 5th out of 70 funds over could also result in capital losses on the fixed interest and

the past five years. The FoF has delivered 1.70% per property portions of the portfolio. However, this impact is

annum above the benchmark sector average over five limited due to the FoF’s low bond duration. Additionally,

years. sufficient diversification through its overweight allocation

to equities to provide some protection to the portfolio in

Asset allocation the event of any unexpected interest rate increases.

Radar: There are no funds on the radar screen.

Changes: No changes were made to underlying

managers.

Foreign bonds, 71.12

Foreign equity, 36.16

Foreign other, 12.15

Foreign cash and money market, 10.21

Foreign property, 2.49

Domestic bonds, 0.67

Source: PSG Wealth research team

All performance is reported in USD unless specified otherwise.

15 | PAGE PSG Wealth | Monthly Insights - May 2019PSG Wealth Offshore Solutions

PSG Wealth Global Preserver FoF (GBP) PSG Wealth Global Moderate FoF (USD)

• The PSG Wealth Global Preserver FoF GBP returned • The PSG Wealth Global Moderate FoF returned

0.70% for April in GBP, in line with the Morningstar 1.80% for April, overperforming the Morningstar

EAA Funds GBP Cautious allocation sector average EAA Funds USD Moderate Allocation sector average,

benchmark, which also delivered a return of 0.70%. which delivered 1.60%.

• The PSG Wealth Global Preserver FoF GBP ranked • The PSG Wealth Global Moderate FoF is ranked in

in the first of its global sector over all measurement the second quartile of Global Moderate Allocation

periods over six months and is ranked 1st out of 29 Funds for all measurement periods over six months

funds over the past five years. The FoF delivered and is ranked 76th out of 201 funds over the past

1.98% per annum above-the-benchmark sector five years.

average over five years.

Asset allocation

Asset allocation

Foreign equity, 63.45

Foreign bonds, 22.86

Foreign bonds, 52.97 Foreign cash and money market, 9.11

Foreign equity, 26.47 Foreign other, 2.45

Foreign other, 10.92 Foreign property, 1.87

Foreign cash and money market, 6.78 Domestic bonds, 0.19

Foreign property, 2.18 Domestic equity, 0.09

Domestic bonds, 0.68 Domestic cash and money market, -0.02

Source: PSG Wealth research team

Source: PSG Wealth research team

Risk: The portfolio is defensively positioned with a

Risk and expectation: The portfolio has a high equity developed market overweight and performance will likely

allocation relative to peers and could underperform during be muted during periods of positive market sentiment

periods of strong equity market declines, conversely when risky assets such as emerging markets outperform.

the portfolio will perform well when equity markets The portfolio currently has 27% in bonds, which could be

outperform other asset classes. Rising global interest rates negatively impacted by unexpected interest rate increases.

could also result in capital losses on the fixed interest and However, this risk is mitigated to an extent by relatively

property portions of the portfolio. However, this impact is large equity allocation.

limited due to the FoF’s low bond duration. Additionally, Expectation: We expect volatility to remain high in the

sufficient diversification through its overweight allocation short term with fluctuating market sentiment in global

to equities to provide some protection to the portfolio in equity markets, the cash position provides a buffer

the event of any unexpected interest rate increases. against market downturns. Our underlying managers

Radar: No funds are currently on the radar screens. are also able to deploy this cash when they find more

Changes: No changes were made to underlying attractive opportunities in the market. Interest rate risk is

managers. actively managed by our underlying managers, with most

positioned on the shorter end of the yield curve.

Radar: The BlackRock Global Allocation fund was removed

from the quantitative risk radar.

Changes: No changes to underlying managers.

All performance is reported in USD unless specified otherwise.

16 | PAGE PSG Wealth | Monthly Insights - May 2019PSG Wealth Offshore Solutions

PSG Wealth Global Moderate FF (ZAR) PSG Wealth Global Flexible FoF (USD)

• The PSG Wealth Global Moderate FF D delivered • The PSG Wealth Global Flexible FoF USD delivered

a return of 0.68% in rand-terms for April, 3.10% for April, outperforming the Morningstar

underperforming the Morningstar EAA Funds USD EAA Funds USD Flexible allocation sector, which

Moderate allocation sector average, which delivered returned 1.50%.

1.03%. • The PSG Wealth Global Flexible FoF USD ranked in the

• The rand increased by approximately 1.42% against first quartile of its global sector over all measurement

the US Dollar over April, thus decreasing the global periods and is ranked 8th out of 70 funds over the

portfolio returns reported in rand. past five years.

• The PSG Wealth Global Moderate FF D is ranked in • The PSG Wealth Global Flexible FoF USD has delivered

the second quartile of the ASISA Global Multi Asset excess returns of 5.21% per annum above the sector

Flexible sector over all measurement periods over five average over the past five years.

years.

Asset allocation

Asset allocation

Foreign equity, 63.26

Foreign bonds, 22.79 Foreign equity, 64.95

Foreign cash and money market, 9.09 Foreign bonds, 22.26

Foreign other, 2.45 Foreign cash and money market, 9.14

Foreign property, 1.87 Foreign other, 3.59

Domestic cash and money market, 0.27 Foreign other, 0.07

Domestic bonds, 0.19

Domestic equity, 0.09

Source: PSG Wealth research team

Source: PSG Wealth research team

Risk and expectation: The portfolio currently has an

Risk and expectation: We expect increased volatility equity allocation of 64.95%, thus the portfolio will likely

in the rand over the short term, which could have a underperform should there be a significant correction in

significant impact on rand returns for our global funds. global equity markets. We expect volatility to remain high

However, over longer periods (seven years +) we expect in the short term with fluctuating market sentiment in

the currency effect will be relatively flat and given the global equity markets. However, we are confident that

relative valuation of global assets, especially equities, we our underlying managers will adjust the positioning of

still believe the fund offers good opportunities. their portfolios as they find opportunities that offer good

returns relative to the risk taken.

Radar: There are no funds on the radar screen.

Changes: During October 2018 the PSG Wealth fund

committee accepted a proposal to align the PSG Wealth

Global Flexible FoF (both USD and GBP classes) with its

intended role within the PSG Wealth Global Fund range

as a global multi-asset flexible fund. The main objective is

to align the fund with the PGS Multi Management’s split

funding investment philosophy and process. Over the

quarter, the following mandates were removed from the

PSG Wealth Global Flexible FoF (USD and GBP): Schroders

Global Multi-Asset Income, Fundsmith Equity and Veritas

Global Real Return. They were replaced with HSBC Global

Strategic Dynamic and Investec Global Multi-Asset Total

return funds. The new funds are a better mandate fit for

the FoF given their unconstrained multi asset approach.

All performance is reported in USD unless specified otherwise.

17 | PAGE PSG Wealth | Monthly Insights - May 2019PSG Wealth Offshore Solutions

PSG Wealth Global Flexible FoF (GBP) PSG Wealth Global Creator FF (ZAR)

• The PSG Wealth Global Creator FF D delivered a return

• The PSG Wealth Global Flexible FoF GBP returned

of 2.82% for April in rand terms, outperforming the

2.90% in GBP for April, outperforming the

global sector average, which returned 2.69% as well

benchmark Morningstar GBP Flexible Allocation

as the ASISA Global Equity General sector, which

sector average, which delivered 1.80%.

returned 2.75%.

• The PSG Wealth Global Flexible FoF GBP ranked in the

• The rand increased by approximately 1.42% against

first quartile of its global sector over all measurement

the US dollar over April, thus decreasing the global

periods and is ranked 1st out of 69 funds over the

portfolio returns reported in rand.

past five years. The PSG Wealth Global Flexible FoF

• Over the past five years, the PSG Wealth Global

GBP has delivered excess returns of 6.53% per

Creator FF D outperformed the ASISA Global Equity

annum above the sector average over this period.

General sector average by 3.48%, recording 14.58%

per annum.

Asset allocation

Asset allocation

Foreign equity, 65.35

Foreign bonds, 22.13

Foreign equity, 93.33

Foreign cash and money market, 8.89

Foreign cash and money market, 3.06

Domestic property, 3.57

Foreign property, 1.93

Foreign other, 0.07

Domestic cash and money market, 1.26

Foreign other, 0.41

Source: PSG Wealth research team

Source: PSG Wealth research team

Risk and expectation: The portfolio currently has an

equity allocation of 65.35%, thus the portfolio will likely

underperform should there be a significant correction in Risk and expectation: We expect increased volatility

global equity markets. We expect volatility to remain high in the rand over the short term, which could have a

in the short term with fluctuating market sentiment in significant impact on rand returns for our global funds.

global equity markets. However, we are confident that However, over longer periods (seven years +) we expect

our underlying managers will adjust the positioning of the currency effect will be relatively flat and given the

their portfolios as they find opportunities that offer good relative valuation of global equities we still believe the

returns relative to the risk taken. fund offers good opportunities.

Radar: No funds on the radar screen.

Changes: No changes were made to underlying

managers.

All performance is reported in USD unless specified otherwise.

18 | PAGE PSG Wealth | Monthly Insights - May 2019PSG Wealth Offshore Solutions

PSG Wealth Global Creator FoF (USD)

• The PSG Wealth Global Creator FoF returned 4.10%

for April, outperforming the benchmark Morningstar Risk: Most of our underlying managers remain relatively

EAA Funds Global Large-Cap Blend equity sector defensively positioned, with a preference for high-quality

stocks with very strong balance sheets, strong moats

which delivered 3.30%.

and steady earnings outlooks. Given the high allocation

• The PSG Wealth Global Creator FoF is ranked in the to quality large caps, mostly in developed markets, we

first or second quartile of its global sector over all expect to underperform global markets when sentiment

measurement periods. is very positive and relatively risky assets, such as emerging

• The PSG Wealth Global Flexible FoF USD has delivered market equities, perform strongly (risk-on trade).

excess returns of 1.71% per annum above the sector Expectation: We are confident that our underlying

average over the past five years. managers will adjust the positioning of their portfolios

• The ranking universe is not restricted to only funds (including exposure to emerging markets) as they find

registered for sale in South Africa and includes the opportunities that offer good returns relative to the

risk taken. We expect volatility to remain high in the

full range of global open-ended funds falling within

short term with fluctuating market sentiment in global

the Morningstar GIFS Global Large Cap Blend sector. equity markets, thus we are comfortable with the overall

defensive positioning of our fund.

Asset allocation Radar: No funds on the radar screen.

Changes: No changes to underlying managers.

Foreign equity, 93.72

Foreign cash and money market, 3.07

Foreign other, 1.94

Foreign property, 1.27

Source: PSG Wealth research team

All performance is reported in USD unless specified otherwise.

19 | PAGE PSG Wealth | Monthly Insights - May 2019PSG Wealth Equity Portfolios

Performance table

PSG Wealth equity portfolios

Fund 1-Month 3-Months 6-Months 12-Months 2-Years Since

inception

PSG Wealth SA Equity Portfolio 3.60% 3.88% 4.82% -3.71% 2.92% 6.64%

PSG Wealth SA Property Portfolio 1.12% -4.73% -3.24% -12.30% -4.65% -3.95%

PSG Wealth Offshore Equity Portfolio (USD) 4.33% 8.30% 9.11% 11.41% 14.71% 13.42%

PSG Wealth SA Dividend Income Equity Portfolio 5.53% 1.59% 3.96% -7.05% 4.91% 4.43%

PSG Wealth Managed Volatility Equity Portfolio 3.40% 0.50% -1.77% -11.71% -2.73% -1.34%

Source: PSG Wealth research team

PSG Wealth SA Equity Portfolio

Appropriate for investors seeking real returns

in capital that exceed the local equity market

returns, but who are comfortable with the capital

fluctuations that characterise an investment of this type.

PSG Wealth

SA Managed

Volatility Equity

PSG Wealth

Tailored for investors who

Offshore Equity

require a smoother path

Portfolio

to long-term returns by

Appropriate for

reducing downside risk while Overview investors seeking real returns

maintaining full exposure of equity in capital that exceed the

to the equity risk premium

in the long run. Benefits of portfolios international benchmark

returns.

this strategy should be more

pronounced during periods of

heightened volatility.

PSG Wealth SA Dividend PSG Wealth SA Property

Income Equity Portfolio Equity Portfolio

Suitable for investors that For the more risk-averse investor

require a regular and growing stream of who requires a regular income.

income derived from dividends with the

potential for real growth in capital value.

20 | PAGE PSG Wealth | Monthly Insights - May 2019PSG Wealth Equity Portfolios

PSG Wealth SA Equity Portfolio

• The PSG Wealth SA Equity Portfolio made a return

of 3.60%, while the FTSE/JSE Capped All Share TR Expectations:

returned 5% for April. • Equity market returns are slightly behind their long-

• Eight (40%) of the 20 stocks in this portfolio ended term averages.

above its benchmark last month. • With multiples ahead of their long-term averages,

we expect returns to materialise primarily through

growth in earnings and not through a material

Performance since inception

change in valuation multiples.

8.00%

• We expect value to outperform growth and have

tilted the portfolio’s exposure accordingly.

6.00%

• Our largest underweight position is towards the

4.00% stable consumer sector, primarily due to concerns

regarding the valuation of food and drug retailers.

2.00%

• Our foreign exposure is through domestic

0.00% investments with international exposure rather than

-2.00% through pure rand hedges which we feel offer less

value.

-4.00%

• Selected large rand hedges, however, continue to

-6.00% hold value on a relative basis.

1-Month 3-Month 6-Month 12-Month 2-Years Since inception • Exchange rate movements will remain a dominant

PSG Wealth SA Equity Portfolio

driver of short-term equity market returns.

• Sensible policy changes by a new administration

Disclaimer: Annualised for periods greater than one year

could become a tailwind.

• A weaker exchange rate is likely to be a headwind to

Source: PSG Wealth research team data as at 30 April 2019

relative returns, however, given the diversification of

*Inception date: 30 August 2015

the portfolio and the quality of its investments, we

believe its performance should not be fundamentally

Asset allocation dependent on exchange rate movements.

• Global investment markets are expected to remain

volatile given the difficulty to forecast macro

Materials variables.

Communication services • Our focus will remain on the underlying fundamentals

Consumer discretionary

of the individual companies rather than on broad

macro-issues.

Consumer staples

Financials

Risk:

Industrials • Changes in the perception of sovereign risk (positive

Cash and negative) and its flow through to exchange- and

interest rates can have an impact on portfolio values.

• Accommodative monetary policy continues to

provide support to developed economies and creates

artificial demand for high-yielding emerging market

Source: PSG Wealth research team

securities. Should foreign capital inflows from these

markets end abruptly, it will have an adverse impact

on market valuations.

• The portfolio is likely to underperform should

international monetary easing prove sustainable. An

environment of sustained monetary easing should

support ‘bond-proxy stocks’ to which the portfolio is

underexposed to due to our valuation concerns. This

could lead to portfolio underperformance.

• Overestimating growth and operational

improvements in highly-rated and large benchmark

constituents.

21 | PAGE PSG Wealth | Monthly Insights - May 2019PSG Wealth Equity Portfolios

PSG Wealth SA Property Portfolio

• The PSG Wealth SA Property Equity Portfolio made

a return of 1.12% during April, underperforming Expectations:

the FTSE/JSE SA Listed Property Capped TR which • The sluggish economic environment will continue

returned 1.72% to place pressure on the real estate sector.

• Ten (50%) of the 20 stocks in the portfolio performed • There is generally an oversupply of office space.

above its benchmark. New local developments could lead to a higher

supply while demand is weak.

Performance since inception • Demand for vacant space will remain muted,

2.00% placing further pressure on rentals. Weak

0.00%

economic growth might result in higher vacancy

profiles and rental reversions.

-2.00%

• Due to the highly competitive and weak market

-4.00%

dynamics, attracting and retaining tenants has

-6.00% become costlier with retail companies increasing

-8.00% incentives for tenants.

-10.00% • Improving tenant retention rates have come at

-12.00% the expense of lower escalations.

-14.00%

• Capital market changes generally dominate

1-Month 3-Month 6-Month 12-Month 2-year Since inception short-term returns.

PSG Wealth SA Property Portfolio

Risk:

Disclaimer: Annualised for periods greater than one year

• Weaker-than-expected growth could erode

dividends underpinning the current valuations.

Source: PSG Wealth research team data as at 30 April 2019

*Inception date: 1 December 2015

• Cannibalisation is a risk in the retail segment.

• Low global bond yields have aided valuations –

a reversal of this trend and tighter US monetary

Asset allocation policy could impact valuations.

• Changes in sovereign risk (positive and negative)

and its flow through to capital markets can

have a significant impact on valuations.

• Value-destructive acquisitions, especially in

Diversified REITs offshore territories where management has less

Real estate Operating Companies

experience, could impact the portfolio.

Retail REITs

• Liquidity risk which could lead to the inability to

Cash

sell underperforming assets quickly.

Source: PSG Wealth research team

22 | PAGE PSG Wealth | Monthly Insights - May 2019PSG Wealth Equity Portfolios

PSG Wealth Offshore Equity Portfolio Performance since inception

16.00%

• The PSG Wealth Offshore Equity Portfolio returned

14.00%

4.33% (USD) in April, overperforming the Dow Jones

Global Titans 50 TR that delivered 4.04%. 12.00%

• Ten (50%) of the 20 stocks in this portfolio ended 10.00%

above its benchmark.

8.00%

6.00%

Expectations: 4.00%

• Investment markets are expected to remain 2.00%

volatile given the high amount of uncertainty in

0.00%

forecasting macro variables.

1-Month 3-Month 6-Month 12-Month 2-Years Since inception

• Given the diversification of the portfolio and

the quality of its chosen investments, we believe PSG Wealth Offshore Equity Portfolio (USD)

Disclaimer: Annualised for periods greater than one year

that the impact of macro variables should be

reduced. Source: PSG Wealth research team data as at 30 April 2019

*Inception date: 30 August 2015

• Our focus will remain on the underlying

fundamentals of the individual companies rather

than on broad macro issues. Asset allocation

Risk:

Communication services

• Sustained international monetary easing

Consumer discretionary

creates demand for quality, stable, high yielding

Consumer staples

equities. This provides a valuation to underpin

Energy

investments in the portfolio. The portfolio is

Financials

likely to underperform should this deteriorate. Healthcare

Industrials

Information technology

Cash

Source: PSG Wealth research team

23 | PAGE PSG Wealth | Monthly Insights - May 2019PSG Wealth Equity Portfolios

PSG Wealth SA Dividend Income Equity Performance since inception

Portfolio

8.00%

• The PSG Wealth SA Dividend Income Equity Portfolio 6.00%

made a return of 5.53% during April, outperforming 4.00%

its benchmark, the FTSE/JSE Dividend Plus TR, which 2.00%

made a return of 5% over the same period. 0.00%

• Twelve (75%) of the 16 stocks in this portfolio came -2.00%

in above the benchmark.

-4.00%

-6.00%

Expectations: -8.00%

• Investment markets are expected to remain volatile 1-Month 3-Month 6-Month 12-Month 2-Years Since inception

given the difficulty to forecast macro variables.

PSG Wealth SA Dividend Income Equity Portfolio

• A shift from highly-valued, high-quality defensive

stocks toward more reasonable priced consumer Disclaimer: Annualised for periods greater than one year (since inception)

cyclical and financial stocks in the medium term. Source: PSG Wealth research team data as at 30 April 2019

*Inception date: 29 April 2016

Risk:

• Changes in the perception of sovereign risk Asset allocation

(positive and negative) and its flow through to

exchange rates and interest rates can have an

impact on portfolio values. Materials

• The portfolio is likely to underperform should Consumer discretionary

international monetary easing prove sustainable. Consumer staples

An environment of sustained monetary easing Energy

should support ‘bond-proxy stocks’ to which the Financials

portfolio is underexposed to due to valuation Healthcare

concerns. Industrials

Cash

Source: PSG Wealth research team

24 | PAGE PSG Wealth | Monthly Insights - May 2019PSG Wealth Equity Portfolios

PSG Wealth SA Managed Volatility Equity Performance since inception

Portfolio 6.00%

4.00%

• The PSG Wealth SA Managed Volatility Equity 2.00%

Portfolio recorded a return of 3.40% for April 0.00%

compared to its benchmark, the PSG Wealth Custom -2.00%

Low Volatility Index TR, which ended the month with -4.00%

a return of 3.66%. -6.00%

• Two (10%) of the 21 stocks in this portfolio came in -8.00%

above the benchmark. -10.00%

-12.00%

-14.00%

Expectations: 1-Month 3-Month 6-Month 12-Month 2-Years Since inception

• The valuation of most benchmark constituents

PSG Wealth SA Managed Volatility Equity Portfolio

currently seems elevated. Disclaimer: Returns annualised since inception

• Relative outperformance against the benchmark

Source: PSG Wealth research team data as at 30 April 2019

through not owning the most expensive pockets *Inception date: 28 July 2016

of shares.

• Lower portfolio drawdown, while still

participating in equity market returns.

Asset allocation

• Low volatility investing in a defensive way to

take risks.

• Portfolio outperformance relative to local equity Materials

markets during periods of stress. Consumer discretionary

• Positive relative performance over the longer Consumer staples

term. Financials

Healthcare

Risk: Industrials

Cash

• A negative performance relative to the local

equity market during strong bull markets.

Source: PSG Wealth research team

25 | PAGE PSG Wealth | Monthly Insights - May 2019Other publications

Previous publications

Daily Weekly

29 May 22 May 17 Oct 09 May 20 Sept 05 April

07 May 10 Oct 18 Apr 13 Sep 22 Mar

17 Apr 03 Oct 11 Apr 06 Sep 15 Mar

10 Apr 19 Sept 04 Apr 23 Aug 08 Mar

03 Apr 12 Sept 22 Mar 16 Aug 01 Mar

20 Mar 05 Sept 14 Mar 03 Aug 15 Feb

13 Mar 22 Aug 07 Mar 19 July 06 Feb

06 Mar 15 Aug 21 Feb 12 July 18 Jan

27 Feb 08 Aug 07 Feb 21 June 11 Jan

13 Feb 18 Jul 17 Jan 14 June 14 Dec

06 Feb 11 Jul 06 Dec 07 June 07 Dec

16 Jan 04 Jul 22 Nov 31 May 30 Nov

12 Dec 20 Jun 15 Nov 17 May 16 Nov

05 Dec 13 Jun 08 Nov 10 May 09 Nov

21 Nov 06 Jun 18 Oct 03 May 02 Nov

14 Nov 23 May 11 Oct 19 April 26 Oct

07 Nov 16 May 04 Oct 12 April 12 Oct

Monthly Research and Strategy Report

Apr 2019 May 2018 Jun 2017 Autumn 2019 Summer 2018

Mar 2019 Apr 2018 May 2017 Summer 2019 Spring 2017

Feb 2019 Mar 2018 Apr 2017 Spring 2018 Winter 2017

Jan 2019 Feb 2018 Mar 2017 Winter 2018 Autumn 2017

Nov 2018 Jan 2018 Feb 2017 Autumn 2018 Summer 2017

Oct 2018 Nov 2017 Jan 2017

Sep 2018 Oct 2017 Nov 2016

Aug 2018 Sep 2017 Oct 2016

Jul 2018 Aug 2017 Sep 2016

Jun 2018 July 2017 Aug 2016

Special report Wealth Perspective

Our view on Tito Mboweni as new Mar 2019

Minister of Finance Dec 2018

Value investing in the 21st century Sep 2018

Our bear risk indicator Jun 2018

Sequence risk and our bucket philosophy Mar 2018

Sequence risk video Dec 2017

New Offshore Brochure Sept 2017

Volatility is uncomfortable, but expected Jun 2017

Stocks that could outperform in stronger Mar 2017

economy Dec 2016

New ANC leader, too close to call Sep 2016

Our exposure to Steinhoff Jul 2016

Local currency downgraded to junk Apr 2016

Blockchains and Bitcoins

UK snap election

Berkshire 2017 AGM

Distributions explained

S&P junk status

Research provided

Fed hike inevitable?

26 | PAGE PSG Wealth | Monthly Insights - May 2019Disclaimer PSG Wealth is a brand underneath PSG Konsult Ltd, which consists of the following legal entities: PSG Multi-Management (Pty) Ltd, PSG Securities Ltd, PSG Fixed Income and Commodities (Pty) Ltd, PSG Scriptfin (Pty) Ltd, PSG Invest (Pty) Ltd, PSG Life Ltd, PSG Employee Benefits Ltd, PSG Trust (Pty) Ltd, and PSG Wealth Financial Planning (Pty) Ltd. Affiliates of the PSG Konsult Group are authorised financial services providers. The opinions expressed in this document are the opinions of the writer and not necessarily those of PSG Konsult Group. The information is provided as general information. It does not constitute financial, tax, legal or investment advice and the PSG Konsult Group of Companies does not guarantee its suitability or potential value. Although the utmost care has been taken in the research and preparation of this document, no responsibility can be taken for actions taken on information in this document. Should you require further information, and since individual needs and risk profiles differ, we suggest you consult a qualified financial adviser, if needed. Collective Investment Schemes in Securities (CIS) are generally medium- to long-term investments. The value of participatory interests (units) may go down as well as up and past performance is not a guide to future performance. CIS are traded at ruling prices and can engage in borrowing and scrip lending. A fund of funds is a portfolio that invests in portfolios of collective investment schemes, which levy their own charges, which could result in a higher fee structure for these portfolios. Fluctuations or movements in the exchange rates may cause the value of underlying international investments to go up or down. A schedule of fees and charges and maximum commissions is available on request from PSG Collective Investments Limited. Commission and incentives may be paid and if so, are included in the overall costs. Forward pricing is used. The portfolios may be capped at any time in order for them to be managed in accordance with their mandate. Different classes of participatory interest can apply to these portfolios and are subject to different fees and charges. Figures quoted are from I-Net, Stats SA, SARB, © 2015 Morningstar, Inc. All Rights Reserved for a lump sum using NAV-NAV prices net of fees, includes income and assumes reinvestment of income. PSG Collective Investments Limited is a member of the Association for Savings and Investment South Africa (ASISA) through its holdings company PSG Konsult Limited. Conflict of Interest Disclosure: The fund may from time to time invest in a portfolio managed by a related party. PSG Collective Investments Limited or the Fund Manager may negotiate a discount on the fees charged by the underlying portfolio. All discounts negotiated are reinvested in the fund for the benefit of the investor. Neither PSG Collective Investments Limited nor the Fund Manager retain any portion of such discount for their own accounts. PSG Multi-Management (Pty) Ltd (FSP No. 44306), PSG Asset Management (Pty) Ltd (FSP No. 29524) and PSG Collective Investments Limited are subsidiaries of PSG Group Limited. The Fund Manager may use the brokerage services of a related party, PSG Securities Ltd.

You can also read