MONTHLY INVESTMENT INSIGHTS - JUNE 2018 - PSG

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MONTHLY INVESTMENT INSIGHTS JUNE 2018

Contents 1. The monthly interview – Economist, Tim Harford 3 2. Tactical asset allocation preferences 7 3. Market commentary 8 4. Local unit trust solutions 9 5. Offshore unit trust solutions 15 6. PSG Wealth equity portfolios 22 7. Other publications 27 2 | PAGE PSG Wealth | Monthly Insights - June 2018

The monthly interview

This month we bring you some more insights from the economist, Tim Harford. At the PSG annual conference,

Harford highlighted the common pitfalls of forecasting and shared what sets super forecasters apart: self-

measurement, flexible thinking and the willingness to change your mind/opinion. We interviewed him after

the conference.

What, in your opinion, is the Irving Fisher was basically making heavily leveraged bets

mind shift that advisers would which, always makes you very vulnerable to a downturn. So,

need to make to get to become the first thing to ask yourself is does the forecast have to be

better forecasters? right, because if the forecast has to be right, then we are

probably already in a difficult situation. The second thing is

I remember working for a big oil how to make a better forecast. I referred in my presentation to

company many years ago and research by Philip Tetlock, who has studied tens of thousands

being asked to make some GDP of forecasters over many decades, measuring everything

forecast. And I remember saying about the people who forecast well and the people who

Economist, Tim Harford

“Well I don’t really know, here is don’t.

what the international consensus

says,” and the guy said “Well, what do you mean you How can advisers improve their forecasting skills?

don’t know? I need to know the forecasts!” He said it

It is important to note that you can get better at forecasting,

is like he was about to fire a missile and was asking me

you can improve yourself. An easy way to improve is to keep

to give him the coordinates, and he couldn’t make his

track of what you were forecasting before, be specific, keep

business plan work until I gave him the coordinates.

track and to go back and check. Most people don’t do this

and if they do it informally, they systematically mis-remember

I remember thinking to myself: OK, if I tell you I cannot

what they had forecast.

give you the coordinates you probably should not fire the

missile, or maybe you should be launching your business

For example, all these people who now think they forecast

plan in a different way that does not require the perfect

2008’s financial crisis and recession. There are a lot of people

coordinates to start with. So, I guess the first question to

who think they did. However, most of them didn’t, and

ask is, what is our strategy in whatever we are doing, and

most of them will struggle to point to something in writing

is our strategy dependent on the forecast being correct.

beforehand.

Because, if the strategy is dependent on the forecast being

So, keep score because you can get better at forecasting - that

correct then, it is probably not a very good strategy. There

is the first thing. The second thing is, think in a probabilistic

are certain things in this world that we can forecast very

way (involving chance variation) when you are trying to make

well, but the big picture economic geopolitical stuff is not

a forecast. Ask yourself a question, for example what is the

among them.

chance that the economy will go into recession, this year?

The first thing you can do is say well, how often does this

So, the first thing to say is “OK, I need to have an investment

economy go into recession? How often is that true generally.

portfolio, an investment strategy that is robust, if the

forecast is not very good.” I talked about the investment

I don’t know the statistics for South Africa, but in my own

strategy of John Maynard Keynes and Irving Fisher in my

country, the UK goes into recession roughly about every

presentation, and neither of their strategies were robust to

nine years. So, if you do nothing else, you could say well

forecast failure.

the chance of the UK going into recession this year is about

one in nine. And that is not an amazing forecast, but already

that’s better than many forecasts will be.

Tell us a bit more about the strategies of Keynes

and Fisher?

The same thing applies to political transitions. How often

John Maynard Keynes’s entire strategy was based on “I’m do presidents’ get replaced? How often do incumbents

going to move between sectors, pro-cyclical or counter- lose elections? How often are there coups? How often do

cyclical, depending on whether I can forecast the recessions presidents’ die in office, and so on. You could look at all this

or the booms.” If you can’t forecast recessions or booms (and sort of stuff, you can get data on all of this, if you want to

as it turns out he could not forecast recessions or booms) and that really helps.

then, that strategy is completely useless.

The opinions expressed in this interview are the opinions of the interviewee and not necessarily those of PSG and do not constitute advice. Although the utmost care has

been taken in the research and preparation of this document, no responsibility can be taken for actions taken on information in this interview.

3 | PAGE PSG Wealth | Monthly Insights - June 2018

The monthly interview

What is the most important thing to remember Because you are gaining something when the numbers and

when forecasting? your instincts tell you something different, (you should know)

The most important thing, is open-mindedness. So, Tetlock is there is something there to explore. And I don’t think there’s

a psychologist and he measures what he calls, actively open- a hard and fast rule that says, ‘and you should always go with

minded thinking - a constant questioning of your previous the number’ or ‘you should always go with your gut.’

beliefs’ meaning. You are constantly asking yourself, what

am I missing? And you are happy to change your own mind. Jeff Bezos made a very interesting comment, that I do not

You see it as a sign of progress, ‘I’m getting smarter,’ rather completely agree with, but I thought it was interesting. He

than a sign of failure or weakness. said when the numbers and the anecdotes are telling you

something different, the anecdotes are usually right, and it

Actively open-minded thinkers like to get into arguments and is usually because the numbers aren’t measuring the right

disagreements with other people, because they think that’s a thing, that’s interesting.

source of insight. If I disagree with someone, then maybe he

is wrong, maybe I’m wrong. So, let’s have the argument and I So, I think that when (these views) clash you learn something

might get smarter. Most of us don’t think like that. (Fostering - you have to start asking yourself why do they clash? Is it

this quality makes) you a better forecaster, but it also makes because I, personally am getting a very (biased) view of the

you more robust to forecast failure. So, if you did get it wrong, situation, my instincts are leading me astray or I’m talking

a willingness to recognize that quickly, can overcome some of to the wrong people, or is it that the numbers are omitting

the facts that you got wrong. something really important? Are they fraudulent or do they

just not measure what matters? There is no straight forward

In your talk, you mentioned how there is this bias answer, but the existence of tension, I think is informative.

towards numbers, like in the case of Fisher. Whereas

Keynes had the perspective on animal spirits and If you have to give one piece of advice to our

the role of emotions in investing. How (do) we advisers on how they guide clients into better

incorporate that into our thinking? decision making, what would you say?

Some people love emotions. They love gut feeling and they I think (when) talking to the client, you always have to have

hate numbers. So, I have been thinking about this recently. a conversation about the alternative scenarios. Where we

I sometimes call it statistics fast and slow, after Daniel are making decisions together, we all have to ask ourselves,

Kahneman’s book, Thinking fast and slow. Here thinking ‘what if I am wrong? When you are (wrong), having

slow is rational, cognitively taxing, really thinking through that conversation with a client. I would have the honest

the statistical or the logical structure of a situation. Whereas conversation.

thinking fast is just, certain things are automatic, certain

processes are intuitive, not necessarily right, but intuitive and I think that is hard to do, because it suggests a certain

easy. pliability - that actually my own dealings with professionals,

the ones that explore different possibilities and raise the

I think statistics fast and statistics slow, (is) clashed between prospects, they might be wrong. I find that, to actually have a

this kind of logical, numerical view of the world and your conversation about that, personally, is very appealing. “What

anecdotal impressions or your gut feel. That is a healthy if I’m wrong?” So ensure you explore various scenarios that

thing and that is a source of further reflection and open- might impact your client’s wealth and share it with them.

mindedness.

The opinions expressed in this interview are the opinions of the interviewee and not necessarily those of PSG and do not constitute advice. Although the utmost care has

been taken in the research and preparation of this document, no responsibility can be taken for actions taken on information in this interview.

4 | PAGE PSG Wealth | Monthly Insights - June 2018

Tactical asset allocation preferences

EMERGING EQUITY DEVELOPED

South Africa ITY Global

U PRO

EQ PER

Cyclical Defensive TY

sive Retail

Defen

Challenging economic conditions persists,

al

but valuations do not seem to price in all clic

Cy

the risks. Liquidity in the event of a market l Re Global growth sets a healthy backdrop,

tia sid

shock remains a concern. n en but valuations seem to be pricing in a lot

TY

s ide tia

Re of good news.

ER

l

OP

Go

BO

PR

ve

rn

ND

Disruptive technologies are causing

m

en

S

headwinds in the retail property space.

t

Particularly in the US, stronger growth

Here we are very selective in our approach favours credit over government bonds,

Cre

l

tai

and cautious with our allocations.

dit

Re

although there exists a caveat for high

quality, investment grade exposure, and

very selective buying.

it

USD

Our current view on government bonds is Cred

BONDS

neutral, while we assess pockets of risk and

CURRENCY

opportunity. If the rand strengthens beyond

t

Governmen

our base view we expect bonds are likely to

GBP

rally and yields could decline. To us it seems The USD seems too strong, while

as if the bond market is already pricing in the GBP and EUR seems too weak in

MPC rate cuts expected on the horizon. relation to the USD.

CASH

ZAR

EUR

Strategic asset allocation

Tactical asset allocation

The market is expecting that the MPC will Changes this month

cut rates, but we feel the MPC will lean

towards a cautious approach.

Overweight: Neutral: Underweight:

Tactical recommendation to Tactical recommendation to Tactical recommendation to

hold more of the asset class hold the asset class in line hold less of the asset class

than specified in the with its weight in the than specified in the

strategic asset allocation strategic asset allocation strategic asset allocation

Bottom line

• Our assessment shows that domestic equity is now • Domestic listed property is undervalued by 2.50% • Similarly, domestic bonds are, in general, also overvalued • Global equity is slightly overvalued by 17.50% on a

roughly 22.70% overvalued relative to its historic relative to its historic earnings yield. In addition, we by more than 23.60% and will struggle if domestic historic earnings basis, although the shift towards

yield. Some pockets of the market are expensive and remain of the opinion that the interest rate cycle will interest rates normalize. There are always exceptions, fiscal stimulus could support the asset class. In the US,

investors should expect continued volatility at current impact the strength and sentiment of the domestic but generally speaking bond yields seem stretched. further aims at deregulation will support corporate

levels. Skilled stock pickers should be able to find value economy, and the affordability of the property sector earnings, although the timing of fiscal support policies

in selected shares specifically. This will present headwinds for capital • Domestic cash is most likely generating a negative real and potential deregulation is uncertain at this stage.

growth in the property sector. We expect property return for investors, after fees and taxes. We remain of

yields, which are calculated as a percentage of capital, the view that although cash can play a strategic role in

to normalize on the back of downward pressure on a portfolio, there is a material trade-off over the long

capital values. term.

5 | PAGE PSG Wealth | Monthly Insights - June 2018

Market commentary

In their monthly market review, Schroders notes that global equities gained overall in May, although regional

performance was mixed. Economic data remained broadly supportive, but politics in Europe and trade worries

weighed on some riskier assets. US equities advanced with economic data resilient enough to allow investors

to shrug off trade sanction uncertainties. Eurozone equities saw negative returns as political uncertainty in Italy

dominated market moves. Financials, especially banks, saw sharp declines. Emerging markets equities lost value,

with US dollar strength a headwind. Government bond yields fell (i.e. prices rose), reflecting increased risk aversion

over the month.

JSE All Share Index - February 2018

59 500

59 000

-3.57%

58 500

58 000

57 500

57 000

56 500

Daily JSE All share index closing value

56 000

55 500

55 000

54 500

54 000

2.01% 1.26% 1.86% 1.00%

53 500

53 000 The JSE slipped in broad- The JSE closed firmer on a The JSE slipped in broad-based The JSE closed firmer in its

based losses, with rand- sterling performance from losses, as a series of events prompted best one-day performance

52 500 sensitive stocks faring Naspers, while platinum investors to shy away from risk in two weeks, with all the

52 000 worst, as a 4.45% drop and gold stocks dropped on assets. The rand was weaker despite major indices recording

by Naspers put the most weaker metal prices and a the release of upbeat inflation data gains.

51 500

pressure on the local stronger rand. earlier, putting pressure on banks,

51 000 bourse. financials and retail stocks. The

resurfacing of fears over global trade

50 500

also put pressure on commodity

50 000 prices, ensuring local miners were

49 500 lower on the day.

49 000

April 30 May 04 May 08 May 12 May 16 May 20 May 24 May 28

Source: Bloomberg

Domestic key moves

The benchmark repo rate was left unchanged at The US unemployment rate fell to 3.80% in May

6.50% 3.80% 2018 from 3.90% in the previous month, and

6.50% by the South African Reserve Bank

(SARB) on 24 May 2018 after trimming it by 25 bps in the below market expectations of 3.90%. It was the lowest

previous meeting and matching market expectations. rate since April 2000, as the number of unemployed

decreased by 281 000 to 6.07 million and employment

South Africa’s jobless rate stayed steady at rose by 293 000 to 155.47 million.

26.70%

26.70% in the first quarter of the year. The

number of unemployed remained unchanged from the Unemployment rate in the US

previous period. The number of unemployed increased 4.6

by 100 000 to 5.98 million and the number of employed

rose by 207 0000 to 16.38 million. 4.4

4.4

4.3 4.3

4.2

Global key moves

4.2

4.1 4.1 4.1 4.1 4.1 4.1

4

US

3.9

3.8

3.8

0.60%

Personal spending in the US increased 0.60% in

April 2018 after an upwardly revised 0.50% gain Jul 2017 Oct 2017 Jan 2018 Apr 2018

3.6

in March and beating market expectations of a smaller

0.40% gain. It is the biggest increase in personal spending Source: Trading Economics

in five months, mainly boosted by a rebound in

consumption of nondurable goods.

6 | PAGE PSG Wealth | Monthly Insights - June 2018

Market commentary

EU Japan

1.90%

The annual inflation rate in the Eurozone is Japan’s trade surplus widened 30.90% to JPY

expected to rise to 1.90% in May 2018 from 30.90%

626 billion in April 2018 from JPY 478 billion

1.20%. It is the highest rate since April 2017, mainly in the same month a year earlier and beating market

boosted by rising oil prices. expectations of a JPY 405.6 billion surplus.

The unemployment rate in the Eurozone The unemployment rate stood at 2.50% in April

3.80% decreased slightly to 8.50% in April 2018, 2.50%

2018, the same as in the prrvious two months

following an upwardly revised 8.60% in March. Markets and matching market estimates. The jobs-to-applicants

expected a number of 8.40%. It remains the lowest ratio was also unchanged from the previous month at

jobless rate since December 2008, well below 9.20% a 1.59%, while markets expected 1.60%.

year earlier.

The unemployment rate in Japan

China 3.2

3.1

12.90%

Chinese exports grew by 12.90% to $200.49 3

billion, recovering from a 2.70% decline in the 2.8 2.8 2.8 2.8 2.8

preceding month, but above forecasts of a 6.30% gain. 2.7 2.7

2.8

Outbound shipments of unwrought aluminium and

2.6

aluminium products, including alloy and semi-finished 2.5 2.5 2.5

aluminium products, came in at 451 000 tonnes in April. 2.4

2.4

Interest rates in China fell to 1.80% in April 2.2

1.80% 2018, from 2.01% in the previous month, Jul 2017 Oct 2017 Jan 2018 Apr 2018

missing market consensus of 1.90%. It was the lowest Source: Trading Economics

rate since January, mainly due to a sharp slowdown in

food inflation.

7 | PAGE PSG Wealth | Monthly Insights - June 2018

PSG Wealth Fund of Funds Solutions

Local funds

Performance table

Fund 6 Month 1 Year 2 Year 3 Year 4 Year 5 Year

PSG Wealth Enhanced Interest D 3.91% 8.02% 8.13% 7.87% 7.44% 7.11%

PSG Wealth Income FoF D 4.18% 7.88% 8.36% 8.28% 8.17% 7.70%

PSG Wealth Preserver FoF D 0.68% 5.54% 4.84% 6.29% 7.41% 7.76%

PSG Wealth Moderate FoF D -1.96% 4.76% 3.73% 5.22% 6.94% 8.57%

PSG Wealth Creator FoF D -4.82% 4.99% 4.43% 3.27% 5.13% 8.71%

Source: PSG Wealth research team

Local fund performance

10.00%

8.00%

6.00%

4.00%

2.00%

0.00%

-2.00%

6 Month 1 Year 2 Year 3 Year 5 Year

-4.00%

-6.00%

-8.00%

PSG Wealth Enhanced Interest D PSG Wealth Income FoF D PSG Wealth Preserver FoF D PSG Wealth Moderate FoF D PSG Wealth Creator FoF D

Source: PSG Wealth research team data as at 31 May 2018 *Dots represent the relevant benchmark

Disclaimer: All performance is reported in ZAR unless specified otherwise

8 | PAGE PSG Wealth | Monthly Insights - June 2018

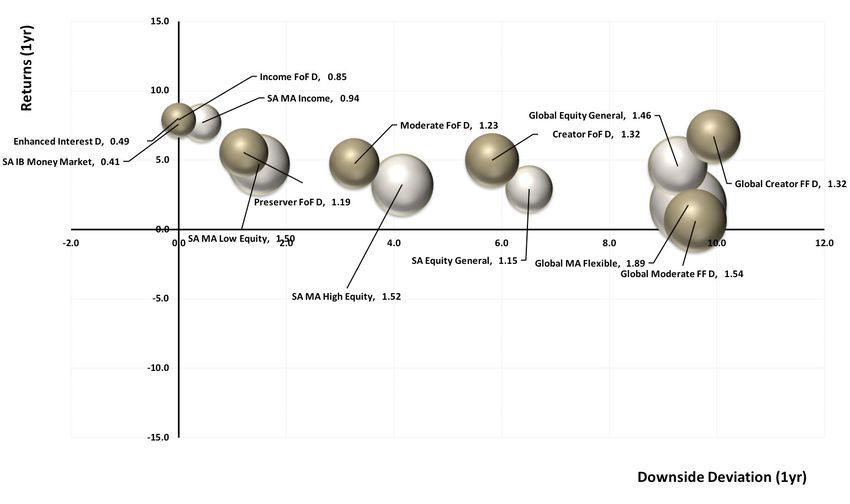

PSG Wealth Domestic Solutions

PSG Wealth Local Fund of Funds bubble chart

Source: PSG Wealth research team

HOW TO READ THE BUBBLE CHARTS

shows TER which is an indication of cost. The

Vertical axis shows the return of each fund Size of the bubble TERs for the fund benchmarks are assumed to

be 1.14% including VAT.

Horizontal axis shows the downside deviation which is a measure of Grey bubbles indicate relevant fund benchmarks

downside risk that focuses on returns that fall below a

minimum threshold or minimum acceptable return (MAR) Gold bubbles represent PSG Wealth EB solutions

Disclaimer: All performance is reported in ZAR unless specified otherwise

9 | PAGE PSG Wealth | Monthly Insights - June 2018

PSG Wealth Domestic Solutions

PSG Wealth Enhanced Interest Fund PSG Wealth Income FoF

• The PSG Wealth Enhanced Interest Fund delivered • This fund delivered a return of 0.29% for May 2018,

a return of 0.69% for May 2018, compared to the compared to the 0.64% of its benchmark, the Stefi

0.60% of its benchmark, the South Africa IB Money 12 Months NCD.

Market Sector Average. • The PSG Wealth Income FoF has an investment

• This fund has an investment horizon of one year, horizon of two years, and it has outperformed its

and the fund has outperformed its benchmark benchmark comfortably with 8.36% against 8.20%

comfortably with 8.02% against 7.56% over the over the two-year period, and is ranked 25th out of

one-year period. 65 funds over this period.

• The fund has also outperformed its benchmark over • This fund also delivered first or second quartile

all measurement periods of one month and longer. performances for all measurement periods over six

months.

Asset allocation

Asset allocation

Domestic bonds, 43.07

Domestic cash and money market, 41.6

Domestic property, 4.67

Domestic cash and money market, 100 Foreign other, 2.54

Foreign bonds, 1.99

Domestic equity, 1.78

Domestic other, 1.34

Foreign property, 1.11

Foreign equity, 1.05

Foreign cash and money market, 0.84

Source: PSG Wealth research team

Source: PSG Wealth research team

Risk and expectations: We are confident the fund

will continue to deliver returns in access of money

market rates to reduce the negative effects of high

inflation on cash. Risk and expectations: We expected that higher

Radar: No funds on the radar screen. inflation and rising interest rates could be a drag

Changes: There are no changes to the underlying on performance over the short-term, but current

funds. indications are that the underlying portfolio managers

are able to take advantage of the higher yields on

short-term instruments to deliver attractive returns

close to the top of the inflation cycle. We are confident

that the underlying portfolio managers will continue

to deliver attractive above average returns until well

after the interest rate cycle has peaked.

Radar: No funds on the radar screen.

Changes: No changes to underlying funds.

10 | PAGE PSG Wealth | Monthly Insights - June 2018PSG Wealth Domestic Solutions

PSG Wealth Preserver FoF PSG Wealth Moderate FoF

• The PSG Wealth Preserver FoF delivered a negative • The PSG Wealth Moderate FoF delivered a negative

return of 0.68% for May 2018, compared to the return of 1.75% for May 2018, compared to the

1.00% of its performance target of CPI plus three negative return of 1.97% of its benchmark, the

percent. South African MA High Equity Sector Average.

• This FoF has an investment horizon of three years, • This FoF has an investment horizon of five years, and

and it has underperformed CPI plus three percent has outperformed its benchmark comfortably with

with 6.29% against 8.53% over this period. 8.57% against 6.82% over the five-year period. It

• The fund also outperformed the 5.09% of the South is also ranked 12th out of 87 funds over this period.

African MA Low Equity Sector Average comfortably • It also delivered a second quartile performance for

over the three-year period, and is ranked 16th out of 1-month and 3-month periods and first quartile

107 funds over this period. performance over all other measurement periods.

• This fund also delivered first or second quartile

performances over all measurement periods over Asset allocation

one month.

Domestic equity, 40.65

Asset allocation Foreign equity, 22.5

Domestic bonds, 16.97

Domestic bonds, 32.91 Domestic cash and money market, 10.91

Domestic cash and money market, 20.69 Domestic property, 6.35

Domestic equity, 19.27 Foreign property, 1.72

Foreign equity, 17.29 Foreign cash and money market, 0.84

Domestic property, 5.25 Foreign bonds, 0.05

Foreign property, 2.18 Domestic other, 0.01

Foreign cash and money market, 1.8

Foreign bonds, 0.44

Domestic other, 0.19

Source: PSG Wealth research team

Foreign other, -0.02

Source: PSG Wealth research team Risk and expectations: The PSG Wealth Moderate

Risk and expectations: The PSG Wealth Preserver FoF may hold up to a total of 75% in domestic

FoF can hold up to a total of 40% in domestic equities equities and offshore equities, and could deliver

and offshore equities, and may deliver negative negative short-term performances in sharp equity

short-term performances in sharp equity corrections corrections or equity bear markets. We are, however,

or equity bear markets. We are, however, confident confident that the fund will always deliver positive

that the fund will always deliver positive returns returns over the preferred investment period of

over the preferred investment period of three years five years and longer, and that it will continue to

and longer, and that it will protect the capital of deliver above average long-term returns with below

clients during severe negative market corrections. average risk overall market cycles.

Radar: The Sim Inflation Plus Fund, The Investec Radar: The Sim Balanced Fund has been added to

Cautious Managed Fund, The Coronation Balanced the radar screen.

Defensive Fund and The Prudential Inflation Plus Changes: No changes to underlying funds.

Funds have been added to the radar screen.

Changes: No changes to underlying funds.

11 | PAGE PSG Wealth | Monthly Insights - June 2018PSG Wealth Domestic Solutions

PSG Wealth Creator FoF

• The PSG Wealth Creator FoF delivered a negative

return of 2.70% for May 2018, compared to the Risk and expectations: Although the outlook for

negative return of 3.72% of its benchmark, the equities are still uncertain, we are confident that the

South African EQ General Sector Average + relative performance of the underlying managers in

• The FoF has an investment horizon of five years and the fund will continue to improve in the near future.

longer, and has outperformed its benchmark with The managers are all active managers that have

8.71% against the 6.65% over the five-year period. demonstrated the ability to add alpha through careful

It is also ranked 22nd out of 98 funds over this stock selection, particularly during turbulent equity

period. markets. This fund will always maintain an equity

• It also delivered first or second quartile performances exposure of close to 100% in domestic and offshore

for all measurement periods. equities. It will deliver negative performances in

sharp equity corrections or equity bear markets. We

are, however, confident that the fund will always

Asset allocation deliver positive returns over the preferred investment

period of five years and longer. It will continue to

deliver above average long-term returns with below

Domestic equity, 79.35

average risk overall market cycles.

Foreign equity, 15.78

Radar: No funds on the radar screen.

Domestic property, 2.48 Changes: No changes to underlying funds.

Domestic cash and money market, 1.91

Foreign property, 0.27

Foreign cash and money market, 0.21

Source: PSG Wealth research team

12 | PAGE PSG Wealth | Monthly Insights - June 2018PSG Wealth Offshore Solutions

Offshore funds

Performance table

Reported in USD

Fund 6 Month 1 Year 2 Year 3 Year 4 Year 5 Year

PSG Wealth Global Preserver FoF D USD -0.22% 1.61% 5.05% 3.30% 3.02% 3.48%

PSG Wealth Global Moderate FoF D USD -0.22% 5.01% 6.61% 1.89% 1.90% 3.64%

PSG Wealth Global Flexible FoF D USD 1.49% 7.96% 12.03% 7.36% 6.12% 7.49%

PSG Wealth Global Creator FoF D 3.05% 11.47% 13.71% 7.61% 7.19% 8.69%

Reported in GBP

Fund 6 Month 1 Year 2 Year 3 Year 4 Year 5 Year

PSG Wealth Global Preserver FoF D GBP 1.19% -0.16% 8.48% 6.74% 6.91% 6.11%

PSG Wealth Global Flexible FoF D GBP 1.84% 3.26% 15.42% 10.47% 11.36% 9.67%

Source: PSG Wealth research team

Offshore funds performance

16.00%

14.00%

12.00%

10.00%

8.00%

6.00%

4.00%

2.00%

0.00%

-2.00%

-4.00%

3 Month 6 Month 1 Year 2 Year 3 Year 5 Year

PSG Wealth Global Preserver FoF D USD PSG Wealth Global Moderate FoF D USD PSG Wealth Global Flexible FoF D USD PSG Wealth Global Creator FoF D USD

Source: PSG Wealth research team data as at 31 May 2018 *Dots represent the relevant benchmark

All performance is reported in USD unless specified otherwise.

13 | PAGE PSG Wealth | Monthly Insights - June 2018PSG Wealth Offshore Solutions

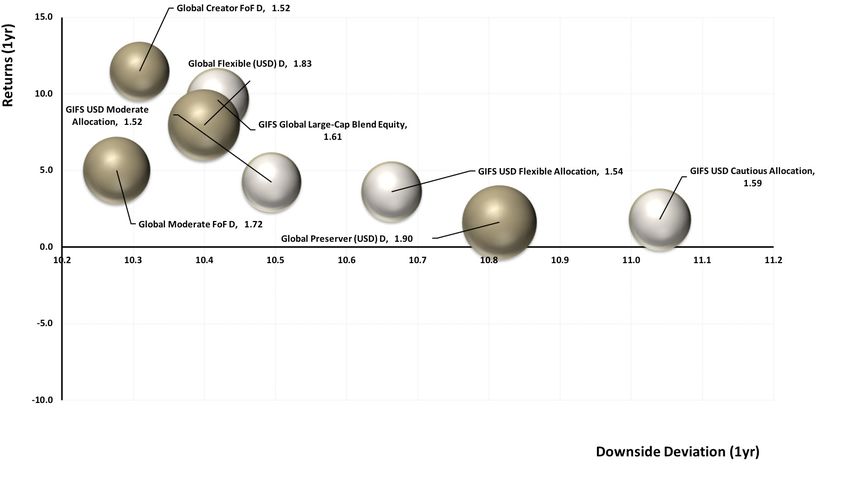

PSG Wealth Offshore Fund of Funds (USD)

Source: PSG Wealth research team

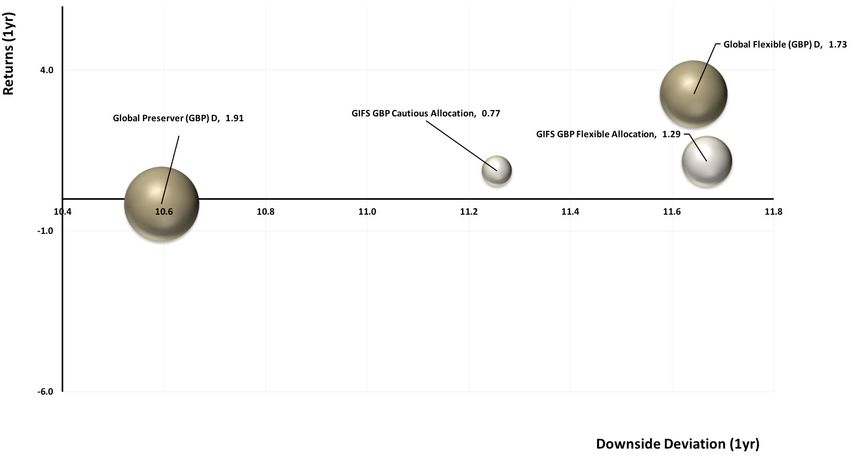

PSG Wealth Offshore Fund of Funds (GBP)

Source: PSG Wealth research team

HOW TO READ THE BUBBLE CHARTS

Vertical axis shows the return of each fund Size of the bubble shows TER which is an indication of cost

Horizontal axis shows the downside deviation which is a measure of Grey bubbles indicate fund peers

downside risk that focuses on returns that fall below a

minimum threshold or minimum acceptable return (MAR) Gold bubbles represent PSG Wealth solutions

14 | PAGE PSG Wealth | Monthly Insights - June 2018PSG Wealth Offshore Solutions

PSG Wealth Global Preserver Fund of

Funds (USD)

• The PSG Wealth Global Preserver FoF USD made a

negative return of 0.07% for May, outperforming The basis for this decision was the potential

the benchmark GIFS USD Cautious allocation sector drawdown risk the fund brings into the FoF. Given

average, which delivered a negative 0.25%. its focus on real returns achieved through a high

• The PSG Wealth Global Preserver FoF USD ranked in allocation to a concentrated portfolio of equities,

the top quartile of its global sector over all periods our view is that the fund’s potential drawdowns

longer than 12 months and is ranked fourth out of could be too high for the conservative role the PSG

58 funds over the last five years. The FoF has delivered Wealth Global Preserver FoF plays in our global fund

1.82% per annum above the benchmark sector range. Ensuring the underlying fund’s mandate fits

average over 5 years. our FoF mandate is a key part of our investment

philosophy, and given that the Veritas fund is not a

Asset allocation good match for the Global Preserver FoFs mandate

we decided to disinvest from the fund.

Foreign bonds, 48.59

Foreign equity, 25.17

Foreign cash and money market, 19.97

Foreign other, 3.73

Foreign property, 2.6

Domestic bonds, 0.81

Domestic cash and money market, -0.8

Source: PSG Wealth research team

Risk and expectation: The portfolio has a high

equity allocation relative to peers and could

underperform during periods of strong equity

market declines, conversely the portfolio will

perform well when equity markets outperform

other asset classes. Rising global interest rates could

also result in capital losses on the fixed interest and

property portions of the portfolio, however this

impact is limited due to the FoF’s low bond duration,

1.25. Additionally, sufficient diversification through

its overweight allocation to equities to provide

some protection to the portfolio in the event of any

unexpected interest rate increases.

Radar: No funds are on the radar screens.

Changes: : The Veritas Global Real Return fund was

removed from the PSG Wealth Global Preserver FoF

during May, the proceeds were allocated equally to

the remaining five managers in the portfolio with

5% remaining in cash.

All performance is reported in USD unless specified otherwise.

15 | PAGE PSG Wealth | Monthly Insights - June 2018PSG Wealth Offshore Solutions

PSG Wealth Global Preserver Fund of PSG Wealth Global Moderate Fund of

Funds (GBP) Funds (USD)

• The PSG Wealth Global Preserver FoF GBP returned • The PSG Wealth Global Moderate FoF made a

2.38% for May in GBP, outperforming the benchmark negative return 0.58% for May, underperforming

GIFS GBP Cautious allocation sector average, which the GIFS USD Moderate Allocation sector average,

delivered 0.74%. which delivered negative 0.22%, but on par with the

• The PSG Wealth Global Preserver FoF GBP ranked the ASISA Global MA Flexible sector which returned

in the top quartile of its global sector over all a negative 0.06%.

measurement periods excluding the one-year period • The PSG Wealth Global Moderate FoF D has

and is ranked second from 28 funds over the last consistently outperformed the ASISA Global MA

five years. The FoF has delivered 3.15% per annum sector average for 3-month and 6-month periods,

above the benchmark sector average over five years. delivering 1.25% in excess returns per annum.

The FoF is ranked in the second quartile of Global

Asset allocation Moderate Allocation funds.

Asset allocation

Foreign bonds, 46.06

Foreign equity, 23.86 Domestic equity, 40.65

Foreign cash and money market, 24.29 Foreign equity, 22.5

Foreign other, 3.41

Domestic bonds, 16.97

Foreign property, 2.43

Domestic cash and money market, 10.91

Domestic bonds, 0.8

Domestic property, 6.35

Domestic cash and money market, -0.78

Foreign property, 1.72

Foreign cash and money market, 0.84

Foreign bonds, 0.05

Foreign other, 0.01

Source: PSG Wealth research team

Source: PSG Wealth research team

Risk and expectation: The portfolio has a high Risk: The portfolio is defensively positioned with a

equity allocation relative to peers and could developed market overweight and performance will

underperform during periods of strong equity likely be muted during periods of positive market

market declines, conversely the portfolio will sentiment when risky assets such as emerging markets

perform well when equity markets outperform outperform. The portfolio currently has 27.09% in

other asset classes. Rising global interest rates could bonds which could be negatively impacted by any

also result in capital losses on the fixed interest and unexpected interest rate increases. However, this risk

property portions of the portfolio, however this is mitigated to an extent by relatively large equity

impact is limited due to the FoF’s low bond duration, allocation, 60.02%

1.25. Additionally, sufficient diversification through Expectation: We expect volatility to remain high in

its overweight allocation to equities to provide the short term with fluctuating market sentiment in

some protection to the portfolio in the event of any global equity markets, the cash position provides a

unexpected interest rate increases. buffer against market downturns. Our underlying

Radar: The Schroder ISF Glbl MA Inc Acc GBP H has managers are also able to deploy this cash when

been added to the radar screen. they find more attractive opportunities in the

Changes: The Veritas Global Real Return fund was market. Interest rate risk is actively managed by our

removed from the PSG Wealth Global Preserver FoF underlying managers, with most positioned on the

during May, the proceeds were allocated equally to shorter end of the yield curve.

the remaining five managers in the portfolio with Radar: The MFS Meridian Global Total Ret l1 USD

5% remaining in cash. and the BGF Global Allocation A2 has been added to

the radar screen.

Changes: No changes made to underlying funds.

All performance is reported in USD unless specified otherwise.

16 | PAGE PSG Wealth | Monthly Insights - June 2018PSG Wealth Offshore Solutions

PSG Wealth Global Moderate Feeder Fund PSG Wealth Global Flexible Fund of

(ZAR) Funds (USD)

• The PSG Wealth Global Moderate FF D delivered a • The PSG Wealth Global Flexible FoF USD delivered

negative return of 0.47% in rand terms for May, 0.62% for May, outperforming the GIFS USD Flexible

underperforming the GIFS USD Moderate allocation allocation sector which returned a negative 0.11%.

sector average which delivered a negative 1.21%. • The PSG Wealth Global Flexible FoF USD ranked in

• The rand weakened by approximately 1.88% against the top quartile of its global sector over all periods

the US dollar over May, thus slightly increasing global from 3-months to since inception, and is ranked

portfolio returns reported in ZAR. eighth out of 66 funds over the last five years.

• The PSG Wealth Global Moderate FF D delivered • The FoF has delivered excess returns of 5.09% per

third quartile returns for all measurement periods annum above the sector average over the last five

below three years. years.

Asset allocation Asset allocation

Foreign bonds, 55.06

Foreign bonds, 28.11

Foreign equity, 82.69

Foreign cash and money market, 9.7

Foreign cash and money market, 11.92

Foreign other, 4.43

Foreign bonds, 3.96

Domestic cash and money market, 1.79

Foreign other, 0.78

Foreign property, 0.73

Foreign property, 0.66

Domestic equity, 0.1

Domestic bonds, 0.08

Source: PSG Wealth research team Source: PSG Wealth research team

Risk and expectation: We expect increased Risk and expectation: The portfolio currently has

volatility in the Rand over the short term, which an equity allocation of 81.08% which is above

could have a significant impact on ZAR returns for the average in the global flexible sector, thus the

our global funds. However, over longer periods portfolio will likely underperform should there be

(seven years +) we expect the currency effect will a significant correction in global equity markets.

be relatively flat and given the relative valuation of We expect volatility to remain high in the short

global assets, especially equities, we still believe the term with fluctuating market sentiment in global

fund offers good opportunities. equity markets, however we are confident that our

underlying managers will adjust the positioning of

their portfolios as they find opportunities that offer

good returns relative to the risk taken.

Radar: No funds on the quantitative or qualitative

radar.

Changes: Disinvested from the Sarasin Global

Real Estate Equity fund and invested the proceed

in the Veritas Global Real return fund. The basis

for this is due to qualitative concerns due to

significant changes in the management team

of the portfolio, combined with the focus on

implementing split funding in the portfolio. The

Sarasin Global Real Estate Equity fund’s portfolio

manager (Guy Mountain) and the deputy portfolio

manager (Geoffrey Armstrong) both resigned from

Sarasin. The real estate fund is not suited for the

unconstrained multi asset flexible nature of the PSG

Wealth Global Flexible FoF.

All performance is reported in USD unless specified otherwise.

17 | PAGE PSG Wealth | Monthly Insights - June 2018PSG Wealth Offshore Solutions

PSG Wealth Global Flexible Fund of Funds PSG Wealth Global Creator Feeder Fund

(GBP) (ZAR)

• The PSG Wealth Global Creator FF D delivered a return

• The PSG Wealth Global Flexible FoF GBP returned

of 1.79% for May in rand terms, outperforming the

3.62% in GBP for May, outperforming the benchmark

global sector average which returned 1.26%, as well

GIFS GBP Flexible allocation sector average which

as the ASISA Global Equity General sector, which

delivered 0.70%.

returned 0.96%.

• The PSG Wealth Global Flexible FoF GBP ranked in

• The rand weakened by approximately 1.88% against

the top quartile of its global sector overall periods

the US dollar over May, thus slightly increasing global

from 12 months to since inception, and is ranked

portfolio returns reported in ZAR.

fifth out of 60 funds over the last five years. The FoF

• The PSG Wealth Global Creator FF D delivered top

has delivered excess returns of 5.95% per annum

quartile returns since inception. Over the last four

above the sector average over this period.

years the FF outperformed the ASISA Global Equity

General sector average by 2.78% per annum.

Asset allocation

Asset allocation

Foreign equity, 83.06

Foreign cash and money market, 10.11

Foreign bonds, 3.69

Foreign property, 1.1 Foreign equity, 94.29

Domestic cash and money market, 1.01 Foreign cash and money market, 3.94

Foreign other, 0.73 Foreign property, 1.49

Domestic equity, 0.31 Domestic cash and money market, 0.28

Source: PSG Wealth research team

Source: PSG Wealth research team

Risk and expectation: The portfolio currently has

an equity allocation of 83.07% which is above

the average in the global flexible sector, thus the Risk and expectation: We expect increased

portfolio will likely underperform should there be volatility in the rand over the short term, which

a significant correction in global equity markets. could have a significant impact on ZAR returns for

We expect volatility to remain high in the short our global funds. However, over longer periods

term with fluctuating market sentiment in global (seven years +) we expect the currency effect will

equity markets, however we are confident that our be relatively flat and given the relative valuation of

underlying managers will adjust the positioning of global equities we still believe the fund offers good

their portfolios as they find opportunities that offer opportunities.

good returns relative to the risk taken.

Radar: The Schroder ISF Glbl MA Inc C Acc GBP H

has been added to the radar screen.

Changes: Disinvested from the Sarasin Global Real

Estate Equity fund and invested the proceed in the

Veritas Global Real return fund.

All performance is reported in USD unless specified otherwise.

18 | PAGE PSG Wealth | Monthly Insights - June 2018PSG Wealth Offshore Solutions

PSG Wealth Global Creator Fund of Funds

(USD)

• The PSG Wealth Global Creator FoF returned

1.01% for May, outperforming the benchmark Risk: Most of our underlying managers remain

GIFS Global Large-Cap Blend equity sector which relatively defensively positioned, with a preference

delivered a negative 0.02% and the MSCI World for high quality stocks with very strong balance

Index which returned 0.06%. sheets, strong moats and steady earnings outlooks.

• The PSG Wealth Global Creator FoF is ranked in Given the high allocation to quality large caps, mostly

the second quartile of global equity funds since in developed markets, we expect to underperform

inception in December 2012. global markets when sentiment is very positive and

relatively risky assets, such as emerging market

equities, perform strongly (risk-on trade).

Asset allocation

Expectation: We are confident that our underlying

managers will adjust the positioning of their

portfolios (including exposure to emerging markets)

as they find opportunities that offer good returns

relative to the risk taken. We expect volatility to

Foreign equity, 94.55 remain high in the short term with fluctuating

Foreign cash and money market, 3.95 market sentiment in global equity markets, thus

Foreign property, 1.5 we are comfortable with the overall defensive

positioning of our fund.

Radar: Nedgroup Global Equity funds were added

to the quantitative radar screen.

Source: PSG Wealth research team

All performance is reported in USD unless specified otherwise.

19 | PAGE PSG Wealth | Monthly Insights - June 2018PSG Wealth Equity Portfolios

Performance table

PSG Wealth Equity portfolios

Fund 1 Month 3 Months 6 Months 12 Months Since

inception

PSG Wealth SA Equity Portfolio -3.73% -3.46% 0.79% 8.19% 9.01%

PSG Wealth SA Property Portfolio -4.09% 2.26% -1.60% 0.49% -1.87%

PSG Wealth Offshore Equity Portfolio (USD) -1.56% -2.98% 0.43% 12.08% 13.11%

PSG Wealth SA Dividend Income Equity Portfolio -7.05% -6.24% 3.60% 13.80% 6.55%

PSG Wealth Managed Volatility Equity Portfolio -3.92% -4.02% 2.27% 3.56% 2.66%

Source: PSG Wealth research team

PSG Wealth SA Equity Portfolio

Appropriate for investors seeking real returns

in capital that exceed the local equity market

returns, but who are comfortable with the capital

fluctuations that characterizes an investment of this type.

PSG Wealth

SA Managed

Volatility Equity

PSG Wealth

Tailored for investors who

Offshore Equity

require a smoother path

Portfolio

to long-term returns by

Appropriate for

reducing downside risk while Overview investors seeking real returns

maintaining full exposure of equity in capital that exceed the

to the equity risk premium

in the long run. Benefits of portfolios international benchmark

returns.

this strategy should be more

pronounced during periods of

heightened volatility.

PSG Wealth SA Dividend PSG Wealth SA Property

Income Equity Portfolio Equity Portfolio

Suitable to the investor that For the more risk adverse investor

requires a regular and growing stream of who requires a regular income.

income derived from dividends with the

potential of a real growth in capital value.

20 | PAGE PSG Wealth | Monthly Insights - June 2018PSG Wealth Equity Portfolios

PSG Wealth SA Equity Portfolio

• The PSG Wealth SA Equity Portfolio made a negative

Expectations:

return of 3.73%, while the FTSE/JSE Capped All Share

• Equity market returns are slightly behind their long-

TR made returned negative 5.68% for May.

term averages.

• Thirteen (59%) of the 22 stocks in this portfolio ended

• With multiples ahead of their long-term averages,

above its benchmark last month.

we expect returns to materialise primarily through

growth in earnings and not through a material

Performance since inception change in valuation multiples.

• We expect value to outperform growth and have

10.00% tilted the portfolio’s exposure accordingly.

8.00% • Our largest underweight position is towards the

6.00%

consumer stable sector primarily due to concerns

regarding the valuation of food and drug retailers.

4.00%

• Our foreign exposure is through domestic

2.00% investments with international exposure rather than

0.00% through pure rand hedges which we feel offer less

value.

-2.00%

• Selected large rand-hedges, however, continue to

-4.00% hold value on a relative basis.

-6.00% • Exchange rate movements will remain a dominant

1 Month 3 Month 6 Month 12 Month Since Inception driver of short-term equity market returns.

• Sensible policy changes by a new administration

PSG Wealth SA Equity Portfolio could become a tailwind.

Source: PSG Wealth research team data as on 31 May 2018 • A weaker exchange rate is likely to be a headwind

*Inception date: 30 August 2015 to relative returns but given the diversification of

the portfolio and the quality of its investments, we

believe its performance should not be fundamentally

Asset allocation

dependent on exchange rate movements.

• Global investment markets are expected to remain

volatile given the difficulty to forecast macro

Materials variables.

Telecommunication services • Our focus will remain on the underlying fundamentals

Consumer discretionary of the individual companies rather than on broad

Consumer staples macro-issues.

Financials

Healthcare Risk:

Industrials • Changes in the perception of sovereign risk (positive

Cash and negative) and its flow through to exchange- and

interest rates, can have an impact on portfolio values.

• Accommodative monetary policy continues to

Source: PSG Wealth research team provide support to developed economies and creates

artificial demand for high yielding emerging market

securities. Should foreign capital inflows from these

markets end abruptly, it will have an adverse impact

on market valuations.

• The portfolio is likely to underperform should

international monetary easing prove sustainable. An

environment of sustained monetary easing should

support ‘bond-proxy stocks’ to which the portfolio is

under exposed to due to our valuation concerns. This

could lead to portfolio underperformance.

• Overestimating growth and operational

improvements in highly-rated and large benchmark

constituents.

21 | PAGE PSG Wealth | Monthly Insights - June 2018PSG Wealth Equity Portfolios

PSG Wealth SA Property Portfolio

• The PSG Wealth SA Property Equity Portfolio made a

negative return of 4.09% during May, outperforming Expectations:

the FTSE/JSE SA Listed Property Capped TR which • The sluggish economic environment will continue

returned a negative 5.30% to place pressure on the real estate sector.

• Thirteen (72%) of the 18 stocks in the portfolio • There is generally an oversupply of office space.

performed above its benchmark. New local developments could lead to a higher

supply while demand is weak.

Performance since inception • Demand for vacant space will remain muted,

placing further pressure on rentals. Weak

3.00% economic growth might result in higher vacancy

profiles and rental reversions.

2.00%

• Due to the highly competitive and weak market

1.00% dynamics, attracting and retaining tenants has

0.00% become costlier with retail companies increasing

-1.00% incentives for tenants.

• Improving tenant retention rates have come at

-2.00%

the expense of lower escalations.

-3.00% • Capital market changes generally dominate

-4.00% short-term returns.

-5.00%

•

1 Month 3 Month 6 Month 12 Month Since Inception Risk:

• Weaker-than-expected growth could erode

PSG Wealth SA Property Portfolio

dividends underpinning the current valuations.

Disclaimer: Annualised for periods greater than one year

• Cannibalization is a risk in the retail segment.

• Low global bond yields have aided valuations –

Source: PSG Wealth research team data as on 31 May 2018

a reversal of this trend and tighter US monetary

*Inception date: 1 December 2015

policy could impact valuations.

• Changes in sovereign risk (positive and negative)

Asset allocation and its flow through to capital markets can

have a significant impact on valuations.

• Value-destructive acquisitions, especially in

offshore territories where management has less

experience, could impact the portfolio.

Diversified REITs • Liquidity risk which could lead to the inability to

Real estate operating companies sell underperforming assets quickly.

Retail REITs

Cash

Source: PSG Wealth research team

22 | PAGE PSG Wealth | Monthly Insights - June 2018PSG Wealth Equity Portfolios

PSG Wealth Offshore Equity Portfolio Performance since inception

• The PSG Wealth Offshore Equity Portfolio made

14.00%

a negative return of 1.56% (USD) in May,

12.00%

underperforming the Dow Jones Global Titans 50 TR

that delivered a positive return of 1.49% 10.00%

• Four (27%) of the 15 stocks in this portfolio ended 8.00%

above its benchmark. 6.00%

4.00%

2.00%

Expectations:

0.00%

• Investment markets are expected to remain

volatile given the high amount of uncertainty in -2.00%

forecasting macro variables. -4.00%

1 Month 3 Month 6 Month 12 Month Since Inception

• Given the diversification of the portfolio and

the quality of its chosen investments, we believe PSG Wealth Offshore Equity Portfolio (USD)

that the impact of macro variables should be

Disclaimer: Annualised for periods greater than one year

reduced.

• Our focus will remain on the underlying Source: PSG Wealth research team data as at 31 May 2018

*Inception date: 30 August 2015

fundamentals of the individual companies rather

than on broad macro issues.

Asset allocation

Risk:

• Sustained international monetary easing

creates demand for quality, stable, high yielding Telecommunication services

equities. This provides a valuation underpin to Consumer discretionary

investments in the portfolio. The portfolio is Consumer staples

likely to underperform should this deteriorate. Financials

Healthcare

Information technology

Cash

Source: PSG Wealth research team

23 | PAGE PSG Wealth | Monthly Insights - June 2018PSG Wealth Equity Portfolios

PSG Wealth SA Dividend Income Equity Performance since inception

Portfolio

15.00%

• The PSG Wealth SA Dividend Income Equity Portfolio

made a negative return of 7.05% during the month.

10.00%

Underperforming the benchmark, the FTSE/JSE

Dividend Plus TR, which made a return of negative

5.00%

5.66% over the same period.

• Eight (40%) of the 20 stocks in this portfolio came in

0.00%

above the benchmark.

-5.00%

-10.00%

Expectations: 1 Month 3 Month 6 Month 12 Month Since Inception

• Investment markets are expected to remain

volatile given the difficultly to forecast macro PSG Wealth SA Dividend Income Equity Portfolio

variables. Disclaimer: Annualised for periods greater than one year (since inception)

• A shift from highly-valued, high-quality defensive Source: PSG Wealth research team data as at 31 May 2018

stocks towards more reasonable priced consumer *Inception date: 29 April 2016

cyclicals and financial stocks in the medium term.

Asset allocation

Risk:

• Changes in the perception of sovereign risk

(positive and negative) and its flow through to Materials

exchange rates and interest rates can have an Telecommunication services

impact on portfolio values. Consumer discretionary

• The portfolio is likely to underperform should Consumer staples

Energy

international monetary easing prove sustainable.

Financials

An environment of sustained monetary easing Healthcare

should support ‘bond-proxy stocks’ to which the Industrials

portfolio is under exposed to due to valuation Cash

concerns.

Source: PSG Wealth research team

24 | PAGE PSG Wealth | Monthly Insights - June 2018PSG Wealth Equity Portfolios

PSG Wealth SA Managed Volatility Equity Performance since inception

Portfolio

4.00%

• The PSG Wealth SA Managed Volatility Equity

3.00%

Portfolio made a negative return of 3.92% for May,

2.00%

outperforming the benchmark, the PSG Wealth

Custom Low Volatility Index TR, which ended the 1.00%

month at negative 6.07%. 0.00%

• Twelve (57%) of the 21 stocks in this portfolio came -1.00%

in above the benchmark. -2.00%

-3.00%

-4.00%

Expectations:

-5.00%

• The valuation of most benchmark constituents

1 Month 3 Month 6 Month 12 Month Since Inception

currently seems elevated.

• Relative outperformance against the benchmark PSG Wealth SA Managed Volatility Equity Portfolio

through not owning the most expensive pockets Disclaimer: Returns annualised since inception

of shares.

Source: PSG Wealth research team data as at 31 May 2018

• Lower portfolio drawdown, while still *Inception date: 28 July 2016

participating in equity market returns.

• Low volatility investing in a defensive way to

take risks. Asset allocation

• Portfolio outperformance relative to local equity

markets during periods of stress.

• Positive relative performance over the longer

Materials

term. Consumer discretionary

Consumer staples

Risk: Financials

• A negative performance relative to the local Healthcare

equity market during strong bull markets. Industrials

Cash

Source: PSG Wealth research team

25 | PAGE PSG Wealth | Monthly Insights - June 2018Other publications

Previous publications

Daily Weekly

27 June 20 Jun 08 Nov 10 May 09 Nov 15 Jun

13 Jun 18 Oct 03 May 02 Nov 08 Jun

06 Jun 11 Oct 19 April 26 Oct 01 Jun

23 May 04 Oct 12 April 12 Oct 25 May

16 May 20 Sept 05 April 05 Oct 18 May

09 May 13 Sept 22 Mar 28 Sept 11 May

18 Apr 06 Sept 15 Mar 14 Sept 04 May

11 Apr 23 Aug 08 Mar 07 Sept 26 Apr

04 Apr 16 Aug 01 Mar 31 Aug 20 Apr

22 Mar 03 Aug 15 Feb 17 Aug 12 Apr

14 Mar 19 July 06 Feb 10 Aug

07 Mar 12 July 18 Jan 02 Aug

07 Feb 21 Jun 11 Jan 27 Jul

17 Jan 14 Jun 14 Dec 13 Jul

06 Dec 07 Jun 07 Dec 06 Jul

22 Nov 31 May 30 Nov 29 Jun

15 Nov 17 May 16 Nov 22 Jun

Monthly Research and Strategy Report

May 2018 Jun 2017 Jul 2016 Autumn 2018 Summer 2017

Apr 2018 May 2017 Jun 2016 Summer 2018 Spring 2016

Mar 2018 Apr 2017 May 2016 Spring 2017 Winter 2016

Feb 2018 Mar 2017 Apr 2016 Winter 2017 Autumn 2016

Jan 2018 Feb 2017 Mar 2016 Autumn 2017 Summer 2016

Nov 2017 Jan 2017 Feb 2016

Oct 2017 Nov 2016 Dec 2015

Sep 2017 Oct 2016 Nov 2015

Aug 2017 Sep 2016 Oct 2015

July 2017 Aug 2016

Special report Wealth Perspective

New offshore brochure Mar 2018

Volatility is uncomfortable, but expected Dec 2017

Stocks that could outperform in stronger Sept 2017

economy Jun 2017

New ANC leader, too close to call Mar 2017

Our exposure to Steinhoff Dec 2016

Local currency downgraded to junk Sep 2016

Blockchains and Bitcoins Jul 2016

UK snap election Apr 2016

Berkshire 2017 AGM Jan 2016

Distributions explained Oct 2015

S&P junk status

Research provided

Fed hike inevitable?

S&P 2 Dec review

US election

Market PE’s

Local government elections

Brexit vote

26 | PAGE PSG Wealth | Monthly Insights - June 2018Disclaimer PSG Wealth is a brand underneath PSG Konsult Ltd, which consists of the following legal entities: PSG Multi-Management (Pty) Ltd, PSG Securities Ltd, PSG Fixed Income and Commodities (Pty) Ltd, PSG Scriptfin (Pty) Ltd, PSG Invest (Pty) Ltd, PSG Life Ltd, PSG Employee Benefits Ltd, PSG Trust (Pty) Ltd, and PSG Wealth Financial Planning (Pty) Ltd. Affiliates of the PSG Konsult Group are authorised financial services providers. The opinions expressed in this document are the opinions of the writer and not necessarily those of PSG Konsult Group. The information is provided as general information. It does not constitute financial, tax, legal or investment advice and the PSG Konsult Group of Companies does not guarantee its suitability or potential value. Although the utmost care has been taken in the research and preparation of this document, no responsibility can be taken for actions taken on information in this document. Should you require further information, and since individual needs and risk profiles differ, we suggest you consult a qualified financial adviser, if needed. Collective Investment Schemes in Securities (CIS) are generally medium- to long-term investments. The value of participatory interests (units) may go down as well as up and past performance is not a guide to future performance. CIS are traded at ruling prices and can engage in borrowing and scrip lending. A fund of funds is a portfolio that invests in portfolios of collective investment schemes, which levy their own charges, which could result in a higher fee structure for these portfolios. Fluctuations or movements in the exchange rates may cause the value of underlying international investments to go up or down. A schedule of fees and charges and maximum commissions is available on request from PSG Collective Investments Limited. Commission and incentives may be paid and if so, are included in the overall costs. Forward pricing is used. The portfolios may be capped at any time in order for them to be managed in accordance with their mandate. Different classes of participatory interest can apply to these portfolios and are subject to different fees and charges. Figures quoted are from I-Net, Stats SA, SARB, © 2015 Morningstar, Inc. All Rights Reserved for a lump sum using NAV-NAV prices net of fees, includes income and assumes reinvestment of income. PSG Collective Investments Limited is a member of the Association for Savings and Investment South Africa (ASISA) through its holdings company PSG Konsult Limited. Conflict of Interest Disclosure: The fund may from time to time invest in a portfolio managed by a related party. PSG Collective Investments Limited or the Fund Manager may negotiate a discount on the fees charged by the underlying portfolio. All discounts negotiated are reinvested in the fund for the benefit of the investor. Neither PSG Collective Investments Limited nor the Fund Manager retain any portion of such discount for their own accounts. PSG Multi-Management (Pty) Ltd (FSP No. 44306), PSG Asset Management (Pty) Ltd (FSP No. 29524) and PSG Collective Investments Limited are subsidiaries of PSG Group Limited. The Fund Manager may use the brokerage services of a related party, PSG Securities Ltd.

You can also read