NEW EU ORGANIC REGULATION NEW CONSTRAINTS AND OPPORTUNITIES - MICHEL REYNAUD VICE PRESIDENT ECOCERT BIOFRUIT CONGRESS MADRID OCTOBER , 23rd, 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

NEW EU ORGANIC REGULATION NEW CONSTRAINTS AND OPPORTUNITIES MICHEL REYNAUD VICE PRESIDENT ECOCERT BIOFRUIT CONGRESS MADRID OCTOBER , 23rd, 2019

2018:

Regulation

2012 Regulation

2018/848

203/2012 wine

2007 Regulation production

EU 834/2007

1999

Regulation EC

1804/99

Animal

1991 production

Regulation

EC 2092/92

plant

production

ORGANIC EU REGULATION

Implementation of the New Organic Regulation

From 01.01.2021

EU NEW

RULES ON Secondary Acts

Implementing/Delegated Acts

ORGANIC 06/2018 – mid 2020

PRODUCTION

Basic Act EU Reg 2018/848

2014 – 05/2018

EXTENSION OF THE SCOPE

LIMITATION OF DEROGATION

MAIN GROWER GROUP CERTIFICATION

CHANGES

MANAGEMENT OF CONTAMINATION –

RESIDUE OF PESTICIDES

IMPORT REGIME - COMPLIANCE vs

EQUIVALENCE

EXTENSION OF THE SCOPE.

• Extension to new products : Mate, Yeast, wineleaf, salt,

beewax….

LIMITATION OF DEROGATION:

• End of use of non organic reproductive material in 2035

MAIN GROWER GROUP CERTIFICATION:

CHANGES • Extension to the EU operators, official recognition,

detailed rules for EU and Third Country

CONTAMINATION IN ORGANIC PRODUCTS:

• clear steps to follow when suspicion at operator level

raise, investigation by the Control Bodies, no de-

certification threshold

2 SYSTEMS

• Trade Agreements with Third Countries

• Control Bodies/Authorities recognised

for the purpose of the compliance

IMPORT TRANSITIONAL PERIOD

REGIME • The recognition of equivalent Countries

under the current regime will expire 5

years after 1.01.2021

• The recognition of « equivalent »

control Bodies will expire up to a

maximum of 3 years after 1.01.2021

7

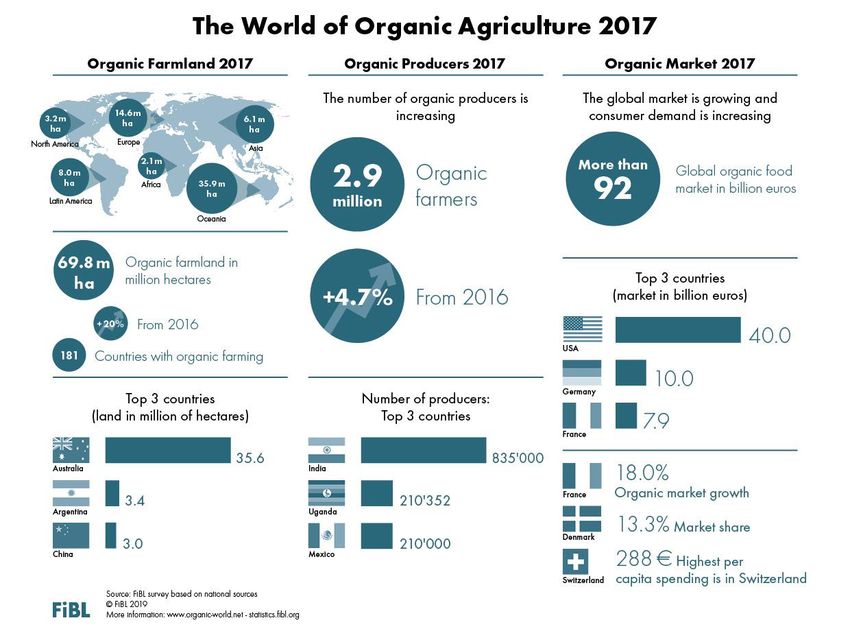

WORLD: ORGANIC RETAIL SALES 2017

288€ 13.3%

World North America

of the

approx. almost are spent per

food market

person in

92 billion € 43 billion € in Denmark is

Switzerland

organic

The largest single market is the The countries with the largest Switzerland has the highest per The highest shares the organic

USA followed by the EU (34.3 market for organic food are the capita consumption worldwide, market of the total market is in

billion €) and China. By region, United States (40 billion €), followed by Denmark and Denmark, followed by Sweden,

North America has the lead (43 followed by Germany (10 billion €), Sweden. Switzerland, Austria, and

billion €), followed by Europe France (7.9 billion €) and China (7.6 Luxembourg.

(37.3 billion €) and Asia. billion €).

Other US 5 Switzerland 5 Denmark 5

Sweden USA

Germany 4 Denmark 4 Sweden 4

Switze…

Canada France 3 Sweden 3 Switzerland 3

Italy

China 2 Luxembourg 2 Austria 2

China

France

Italy 1 Austria 1 Luxembourg 1

Germany

0 20.000 40.000 60.000 0 200 400 0 10 20

Retail sales in million Euros Euros Market share in %

Distribution of retail sales value The five countries with the largest The five countries with the highest The five countries with

by country 2017 markets for organic food 2017 per capita consumption 2017 the highest organic shares of

the total market 2017

Source: FiBL survey 2019 www.organic-world.net – statistics.fibl.orgIMPORT IN THE EU

Volume of organic agri food import EU 2018

900000 30

800000

25

700000

600000 20

500000

15

400000

300000 10

200000

5

100000

0 0

TONNES %

Source: EU Commission Import TRACESTOP 10 COUNTRIES

450000 14

TOP 10 IMPORTS INTO THE EU

400000

12

350000

10

300000

VOLUME IN TONNES

POURCENTAGE

250000 8

200000 6

150000

4

100000

2

50000

0 0

CHINA ECUADOR DOMINICAN UKRAINE TURKEY PERU US UAE INDIA BRAZIL

REPUBLIC

TONNES %

Source: EU Commission Import TRACESINTERNATIONAL REGULATIONS AND RECOGNITION

Trade Agreement between the consumption

market

Towards the compliance for export countriesEXPECTATIONS OF THE STRICT ORGANIC RULES

CONSUMMERS FOR FAIR PAY

ORGANIC AND CARBON SEQUESTRATION /

VALUE CHAIN CLIMATE CHANGE

FOOTPRINT but ALSO

WATER FOOTPRINT

BEYOND

ORGANIC ORGANIC AND WASTE

MANAGEMENT

PACKAGING

TRACEABILITY AND TRANSPARENCYTO SECURE THE SUPPLY – STRUCTURATION OF

THE SUPPLY CHAIN?

The way the market and supply chain are organiued does not allow to face the following challenges:

To avoid the viscissitudes of external factors: climate, fluctating prices and uncertainty of

the market;

To ensure an improved stability of supply and to give visibility for the future in order to

anticipate (producers and processors);

To master the value chain through a better knowledge of the production uptstream,

suppliers and through a balaced power relationship;

To answer to the expectation of transparency and traceability of stakeholders, and on the

social and environemental condition of the production, on the remuneration and impact

on the life of farmers

To valorise the commitment and practices, to develop sustainable, resilient supply chain.

Solution?The solution : building up resilient organic supply

chain - One tool: Fair for Life

1991 – Setting 2007- ECOCERT

up ECOCERT in launched its fair

France trade standard ESR

UNIVERSALITY

2014 – IMO

taken over

TRANSPARENC

by

ECOCERT Y

2017

New version PARTNERSHIP

1989 – 2006 - IMO launched

Setting up of its fair trade

IMO in standard– Fair for

Switzerland Life

14Within a Value-Chain partnership

To know each other, to meet , to interact and learn each other

To share a diagnostic of the challenges, exchange on a common vision

To identify the solution, building up a project for a long term.

To establish a beneficial partnership framework, to commit with sincerity

To Act with responsibility, respect and transparencyWhere transparency is at the heart of the approach

To ensure the practices are implemented

To bring /to share the story of the commitment to the consumers

to make the consumer an active player… where Everyone has a role to play

Operator at production Partner Brand Consummer

level Supports the producers ensures the Buys responsible and

To identify the pertinent action gives opportunity of market transparency to the supports the producer

to be developped consummerAccording to a continuous improvement

Operator at the Partner Brand Consummers

production level Supports the producers Ensures the Buys responsible and

To identify the pertinent action Gives opportunity of market transparency to the supports the consummer

to be developped consummers

Scheme owner and certification Body

1. Set up clear and understandable requirements

2. Ensure an efficient control

3. Make sure the infomation is availableTHANKS FOR YOUR ATTENTION

www.ecocert.com

www.fairforlife.orgYou can also read