NIFHA Economic context, the housing sector and the outlook - Economist: Jordan Buchanan Ulster University Economic Policy Centre

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

NIFHA

Economic context, the

housing sector and the

outlook

Economist: Jordan Buchanan

Ulster University Economic Policy Centre

@UlsterUniEPC

Agenda

• Recent economic performance

• The housing sector

• The economic outlook

• Final thoughts

@UlsterUniEPC

Recent economic performance

Context in economic growth striking

Buoyant jobs market, weak output market

Explaining the post crash

recovery:

• Jobs rich recovery, both UK

and NI

• Much weaker output

recovery (GDP/GVA)

• Productivity growth has

stalled

• Creating jobs in lower

productivity sectors, losing

jobs in higher productivity

sectors

• Since 2009, full time

workers wages are down

5% in real terms!

@UlsterUniEPC

Boom & bust & return to normality?

@UlsterUniEPC

Source: LPS, UUEPC analysis

Housing sector

Value in the market?

Note: London house prices haven’t appreciated since

Brexit vote- but this is not a bad outcome!!

@UlsterUniEPC

Source: LPS, UUEPC analysis

Affordability a key selling point for NI

First Time Buyer:

Northern Ireland:

Average age of borrower: 30

Average price FTB home: £118k

Deposit: 15% (£18k) Loan size: £100,000

Loan income multiple: x3: i.e income: £33k

London:

Average age of borrower: 32

Average price FTB home: £313k

Deposit: 12% (£38k) Loan size: £275,000

Loan income multiple: x4: i.e income: £70k

Source: UK Finance Q2 2018

@UlsterUniEPC

Property type and tenure

13% rent from NIHE, 4% from Housing associations

Social renting demand: Key facts:

• Approx. 85k homes are rented from NIHE and

50k homes from other housing associations

• Last year there was 38,000 applicants on waiting

list- of which 24,000 in housing stress.

• 18,000 households presented as homeless-

biggest factors cited include: Accommodation

not reasonable, sharing breakdown/family

dispute and loss of rented accommodation

• Single males (33%) and families (32%) were the

biggest presenters of homelessness

• Average weekly rent is £75 in social sector vs.

£94 in private sector in NI

Source: NISRA, DfC, LPS, District Council Building Control via LPS, ONS, DCLG, CSO, DECLD & UUEPC analysis @UlsterUniEPC

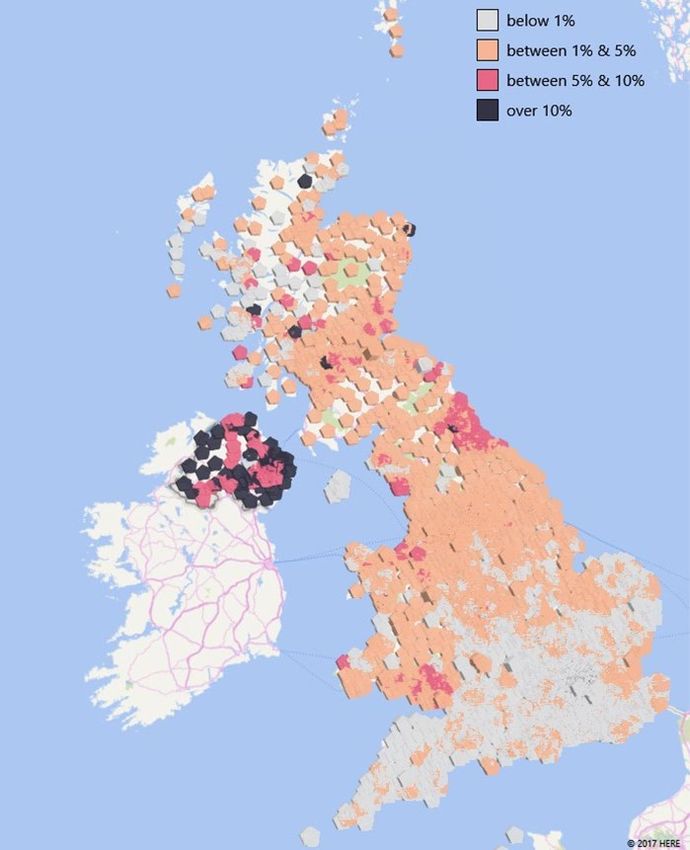

Negative equity- A bigger concern for NI

% of mortgages in negative equity; June 2017

• A much bigger problem for NI residents

compared to other UK regions.

• 40% of buyers from 2005-2008 were in

negative equity in 2013.

• By mid 2016- no of total homeowners in

negative equity has fallen from 68,000 to

25,000 (equivalent to 10% of total

homeowners).

• Average negative equity balance is £32,000

• Continued growth in consumer credit,

anaemic wage growth, rising inflation,

gradual interest rate rises- NI more at risk

of difficulties in any UK wide economic

slowdown

@UlsterUniEPC

Source: UK Finance, CMLSource Property Pal, Rightmove

What real value looks like

(Sept 20th 2018)

What a £200k house looks like in different local cities

Belfast Manchester Edinburgh

Dublin London Cambridge

@UlsterUniEPCThe economic outlook:

Global themes

@UlsterUniEPCOutlook summary (all opinions matter)

Forecaster: 2018 2019 2020 2021

0.6% 0.4% 0.2% 0.4%

1.5% 1.0% 1.0%

0.9% 1.1% - -

0.8% 1.2% - -

1.1% 1.2% 1.3% 1.9%

Source:

UUEPC Autumn 18 Outlook

Ulster Bank (September 2018)

Dankse Bank/Oxford Economics Quarterly Sectoral Forecasts Q2 2018

EY Economic Eye Summer 2018

PwC Economic Outlook Summer 2018

1.0% 1.0% 0.8% 1.1% @UlsterUniEPCHouse price outlook

3-4% growth in coming years- but slowing thereafter

@UlsterUniEPC

Source: UUEPC Autumn Outlook 2018Final thoughts

‘Housing crisis’- different mechanisms

Is the market functional?- more than just a supply problem

• Supply- conventional explanation that UK doesn’t build enough homes (particularly in certain areas i.e

London/SE)

• Demand-Lack of demand in certain areas leaving empty/vacant homes

• Distributional- wealthy older people with spare rooms- building isn’t solution here- focus should be on

downsizing

• Quality- Areas with old towns and period properties left to decay over time. Acute in private rental sector-

encourage landlords to renovate

• Cost/crisis- Supply/demand isn’t driving prices- the amount of cash funnelled into the economy at low interest

rates is. Credit issue is driving the gap between homeowners/property shareholders and renters. Tenants of

social housing have lost out- in a functional market they could buy a home. An intergenerational problem of

wealth vs non wealth.

• Rising prices benefits downsizers, leaving wealth to next generation/ bank of mum and dad. People may also

use their housing equity as a ‘cash machine’ to buy a better car or build an extension- fuelling consumer

spending

Source: Ed Conway; Sky News, UUEPC analysis

@UlsterUniEPCIn summary – consumer behaviour key to watch

• The outlook is highly uncertain, all forecasts are conditional on the assumptions they are making about tariffs, migration

policy etc. The UUEPC forecasts already projected a slow down, though weaker post Brexit they do not suggest a recession

• Uncertainty only adds to worries of over dependence on consumers and on other NI weaknesses around inactivity and

productivity – there is much work to do under the new Programme for Government/ Industrial Strategy (assuming there is a

govt!)

• For NI the uncertainties of Brexit, whatever its long term impacts (which cannot be known at this point) will likely have some

property impacts

• Recent rises likely to be a combination of factors with pent-up demand and returning confidence / affordability dominating

• BUT- the inflation wage journey is the critical one to watch. Rising housing costs possible (mortgages, rates, fuel etc.).

• In macro terms weaning off consumer dependency is desirable it is still a tough transition

• In summary strong demand, but there are risks to plan for and mitigate

• NI’s labour market success over last 6 years is not to be ignored

@UlsterUniEPCThank You

Jordan Buchanan: Economist

Ulster University Economic Policy Centre

Email: j.buchanan@ulster.ac.uk

Twitter: @jbuchanan0707

LinkedIn: Jordan Buchanan

Telephone: 02890 368 362

@UlsterUniEPCYou can also read