OUTLOOK AUGUST 2020 - INTERNATIONAL RESEARCH - BNP Paribas Real Estate

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

EUROPEAN PROPERTY MARKET

OUTLOOK AUGUST 2020

EXECUTIVE SUMMARY

REAL ESTATE IN UNCERTAIN TIMES

I N T E R N AT I O N A L R E S E A R C H

Real Estate for a changing world

BNP PARIBAS REAL ESTATE 1

CONTENT

4 THE ECONOMIC OUTLOOK

SYMMETRIC SHOCK: ASYMMETRIC REBOUND

7 EUROPEAN REAL ESTATE

GOING VIRAL

13 THE REGIONAL OUTLOOK

14 UK & IRELAND: PLAYING CATCH-UP

18 NORDICS: MIXED RESPONSE: SIMILAR OUTCOMES

22 GERMANY: LEADING EUROPE’S RECOVERY

26 FRANCE: PARIS REMAINS AN ATTRACTIVE MARKET

30 SOUTHERN EUROPE: AWAITING RE-OPENNG

34 BENELUX: CALM AND CONSISTENT

38 C EE: FOREIGN INVESTORS RETREAT

24 APPENDIX

2 EUROPEAN PROPERTY MARKET OUTLOOK AUGUST 2020

FOREWORD

In a period of uncertainty, investors seeking income and safety of capital

are likely to turn to real estate. Yet, more than ever, asset selection will

require greater discretion to make both those requirements a reality.

WE PRESENT OUR LATEST FORECASTS in a world where the social and economic backdrop has

substantially changed from that which prevailed during our previous publication in January. The

global economy has moved from worrying about systemic risk emanating from trade protectionism

to one underpinned by a health crisis, the issues of which have resulted in profound disruption.

We are now in a self-imposed global recession as governments struggle to contain the pandemic.

While most economists expect the recession to abate by the end of 2020, the path and speed of re-

covery remains unclear. The principal problem is a sharp, and potentially destabilising, expansion

in unemployment. European governments, aware of this risk, have moved swiftly to create buffers,

with unprecedented financial support for individuals and businesses. Growth in public spending

funded by the issuance of bonds would normally result in an increase in yields. Yet it coincides

with a period of exceptional demand for safe assets, a situation magnified by COVID-19, which has

resulted in a renewed squeeze on sovereign bond yields.

For real estate, the macroeconomic situation remains exceptionally favourable relative to other

asset classes such as equities (volatile) and bonds (low or negative yielding). However, the perfor-

mance of real estate investment is underpinned by the income that investors are able to generate

from the asset, which, in turn, depends on the health of corporate occupiers. This is where the

greatest negative impact of the pandemic on real estate is apparent. With so many corporate oc-

cupiers challenged financially, investors will increasingly focus on covenant strength and income

risk in their investment decisions.

In this report, we provide our view on the outlook for European real estate markets in this con-

text over the next five years. We see challenges around performance in the short term, although

nothing like those witnessed during the 2008/2009 financial crisis; and structural changes in the

long run. We continue to be optimistic about the long-term value of investing in real estate, but

our central view is that, in the short term, investors are likely to focus on prime assets in core

geographies.

SAMUEL DUAH

Head of Real Estate Economics

International Research

BNP PARIBAS REAL ESTATE 3

SYMMETRIC SHOCK:

OVER 90% OF SOVEREIGN BONDS

IN THE ADVANCED ECONOMIES The economic outlook

ASYMMETRIC

ARE YIELDING LESS THAN 2%.

THIS IS LIKELY TO GET WORSE OVER

THE NEXT TWO YEARS. MOREOVER

REBOUND

THIS IS SIGNIFICANTLY LOWER THAN

EUROPEAN PRIME PROPERTY YIELDS.

AT THE END OF 2019, ECONOMISTS AROUND THE WORLD WERE SURE about one thing:

2020 should be a year of continuity, even better than 2019 as the systemic risks faced

by the global economy (mainly Brexit and the trade war between the US and China)

began to diminish. The emergence of COVID-19 at the beginning of 2020 took the

world by surprise with its virulence, delivering a shock just as the global economy had

begun to stabilise.

The first impacts of the pandemic were both a disruption to the supply chain (with

a possible shortage of goods and the closure of borders) and a decrease in domestic

demand following the restrictions imposed by governments. The lockdown measures

introduced by European governments added global implications that are still difficult

to fully measure. Indeed, as activity and demand effectively stopped overnight, com-

panies were pushed towards unknown horizons, forcing governments to take unprece-

dented steps to protect jobs and incomes.

THE ECONOMIC OUTLOOK

A global recession, GDP (%) EXPECTIONS FOR MONETARY BLOCKS FINLAND*

-7.2 4.2 Disinflation in the short term

but what kind of recovery? AND SELECTED EUROPEAN COUNTRIES NORWAY*

-4.9 3.6 The mid-term outlook for inflation is more un-

SWEDEN

At the start of the lockdowns, the debate was certain than it has been for years. The contrac-

2020 2021 -6.1 4.3

not around the possible damage to the eco- tion in activity in Q2 should lead to disinflatio-

WORLD -3.7 5.6 DENMARK

nomy but on the shape of the recovery. If a glo- nary trends. In the long term, the implications

IRELAND* -5.9 5.1

bal and severe recession for 2020 was quickly UNITED STATES -4.9 4.8 are far reaching, as economies could move from

-6.8 5.3 NETHERLANDS

a reality, the generous and timely packages EUROZONE -9.0 5.8 UNITED KINGDOM

POLAND

disinflation to a strong increase in prices. Indeed,

-9.1 5.3 -5.9 3.7

put in place both by governments and central JAPAN -4.8 2.1 GERMANY -3.0 3.5 with the low levels of supply that we anticipate

BELGIUM

banks were expected to restart the economy. CHINA 2.5 8.1 -5.6 5.3 in the near future and the support of private de-

-11.1 5.9

But their final effects, particularly in the labour INDIA -4.7 9.5

CZECH REPUBLIC mand by governments, prices may rise natura-

-6.5 5.0

market, are still being discussed. RUSSIA -6.5 3.5

lly. Furthermore, with ongoing discussions about

SWITZERLAND HUNGARY

FRANCE AUSTRIA*

-4.0 4.5 supply chain re-organisation, we may see some

BRAZIL -7.0 4.0 -6.2 5.3

-11.1 5.9 -7.0 4.4 relocation of production sites to higher-cost lo-

The first economic data available since the ea- ROMANIA

sing of lockdown have been very positive. We -5.0 4.9 cations, which will impact profit margins and

have seen a strong rebound from the supply PORTUGAL* could cause further inflationary pressures.

-9.1 5.4 ITALY

side and the beginning of momentum on the

-12.1 6.1

demand side. However, this recovery is not yet SPAIN However, the outcome will be mainly determi-

secure and will depend on the sustainability of -12.5 6.3 ned by household confidence in the global eco-

demand. To this end, the holiday season will nomy and in their government’s measures. A

be critical to simultaneously rebuild confiden- resurgence of the virus or a sharp increase in

ce and increase consumption in the short term. unemployment may prevent any big-ticket ex-

In the longer run, the ability of countries to ab- Source: BNP Paribas Global Outlook & Eco Perspectives (July 2020); * Consensus Economics (July 2020) penses and increase saving ratios, leading to a

sorb the expected rise in unemployment throu- prolonged decrease in demand. Along with re-

gh sustainable demand, job creation or even duced energy prices, lower demand could drag

incentives to accelerate sectorial mobility will economies. Moreover, its less stringent and the threat of a second wave of the virus in the down inflation considerably, with outright price

drive the recovery. shorter lockdown measures and a bolder po- months ahead could weigh further on its nas- falls possible in some countries (Italy or Spain,

licy response should also improve the US re- cent economic recovery. for example).

In our base case scenario, we project that glo- covery. In Europe, Germany should outperform

bal GDP will contract by 3.7% in 2020, reco- other countries in the region as its lockdown Ultimately, the coming months will be crucial

vering sharply in 2021 to 5.6%. Although, the was only partial, and its fiscal policy should be for the global economy, and household confi-

shock is symmetric, we expect an asymmetric more effective in sustaining the momentum. In dence will be one of the key drivers. If all the

rebound within the European economy. contrast, the recovery in Spain and Italy could measures put in place either by central banks

be dragged down by a combination of heavier or governments end up creating inflation, the

We anticipate that the US will rebound faster pre-crisis public deficits and indebtedness, a final impact of the COVID-19 crisis on private

than both Japan and the broader Eurozone eco- higher share of tourism in their GDPs and a consumption is still difficult to estimate. We do

nomy. Due to its more flexible economy, the US greater prevalence of small and medium-sized not subscribe to a V-shaped recovery, rather

is likely to outperform most other advanced companies. While the U.K. is open for business, something more like a U-shaped recover.

BNP PARIBAS REAL ESTATE 5

THE ECONOMIC OUTLOOK

Avoiding a labour market depression By autumn, the main support schemes will have An attractive macro environment porate bond prices will be hit or any weakening

cease or been restructured, and unemployment for real estate investment in the ability of companies to refinance their

The recovery of the job market remains one of rates may increase dramatically across Europe. debt in the medium term.

the big uncertainties with regards to the ongoing Consequently, most countries are bringing for- What this increase in spending represents is

crisis. The short-term impact of the pandemic ward increased spending to reflate economies and a decisive shift in emphasis from influencing By increasing their balance sheets and buying

on the labour market seems inevitable and qui- prevent a destabilising increase in unemployment. the economy through monetary policy to direct government bonds, central banks are moving

te predictable, with bankruptcies and lay-offs in Some countries are better positioned than others spending. Central banks are taking a secondary to a supportive role in the economy. They are

almost every sector, yet the longer-term picture to service this new debt. The big five’s immediate but important supportive role. With many eco- letting government do the heavy lifting of re-

is still unclear. The extent of the rebound of the fiscal impulse will see Germany borrow €456.5 nomies unlikely to return to pre-crisis levels flating the economy by effectively underwriting

employment market will have some major con- billion, France €106 billion, Spain €45.7 billion for many quarters, monetary conditions will government-spending programs. That surety

sequences for the sustainability of the recovery. and Italy €61.3 billion. The UK will borrow £176.7 remain accommodative for a prolonged period. around is encouraging investors to buy more

Up to this point, governments have protected billion. To support the weaker economies, the Eu- bonds and pushing yields down. The massive

jobs through national employment support ropean Union introduced a €750 billion pandemic Central banks have quickly announced emer- issuance of debt may have negative implica-

schemes across Europe, but policymakers are response plan composed of €390 billion in grants gency securities purchase programmes (some- tions for fragile public finances long term. Yet

now recalibrating their support. In effect this and €360 billion in loans, and attached to a new times open-ended, as with the Federal Reser- in the medium term (2 to 3 years), we do not

will reveal that many companies are employing €1.074 trillion seven-year budget, the Multian- ve) and major rate cuts. These programs could expect government yields to increase much as

people that the current level of demand may nual Financial Framework (MFF). The final cost even be widened. The ECB may broaden the central banks are ready to do whatever it takes

not be able to support. of these schemes could be high for governments: scope to include ‘fallen angels’ (bonds that to protect the economy and to avoid any dis-

increasing the level of debt and prevent neces- were investment grade but have fallen into tortion.

sary expenditure in other areas of society. ‘junk’ status). We are not anticipating that cor-

HERE WE GO AGAIN: 2009 REVISITED • Unemployment Rate in Europe (%) LONG WAY DOWN • 10yr government bond yields (%)

2019 2020 2021 Poland Italy UK Spain France Germany

20% 8.00

18%

16% 6.00

14%

12%

10% 4.00

8%

6% 2.00

4%

2%

0

0%

Eurozone

Beligum

Republic

France

Germany

Italy

Netherlands

Poland

Portugal

Spain

Kingdom

Czech

United

-2.00

07 08 09 10 11 12 13 14 15 16 17 18 19 20* 21*

Source: Moody’s Source: Macrobond, BNP Paribas * Forecast

6 EUROPEAN PROPERTY MARKET OUTLOOK AUGUST 2020

GOING VIRAL

ALTHOUGH TOTAL RETURNS

MAY GO NEGATIVE IN 2020,

WE REMAIN OPTIMISTIC

European Real Estate

OF A STRONG RECOVERY

OVER THE FORECAST PERIOD.

INVESTMENT CONDITIONS: FROM HOT TO COLD

INVESTMENT ACTIVITY IN H1 2020 is clearly showing polarity. Most European mar-

kets witnessed solid investment activity in Q1 2020 and some countries even pos-

ted higher transactional volumes than in Q1 2019. Total volume of investment in Q1

was €69 billion, 46% higher than Q1 2019. The second quarter went in the opposite

direction with significant falls across Europe. Lockdown with the restrictions on mo-

vement remain a large factor behind the slower activity. Many transactions, particu-

larly low-scale deals, that do not involve lengthy negotiation periods, were simply

suspended. Many large deals that went through in Q2 were ones already completed

in practice, with signing a formality.

€102.1bn Real estate investors, by their very nature, tend to view property as a long term

in H1 2020 investment so are not likely to take a kneejerk reaction to the current environment.

Investors who do not need to transact will wait for better time to do so. It is probable

that some element of pausing will roll forward into Q3 before the market picks up

European investment again in Q4. Nevertheless, barring a surge in demand, 2020 (-34%) will likely see sha-

volumes rply reduced transaction volumes in Europe with true recovery potentially emerging in

2021 (+16%). Particularly hit here are cross-border transactions, with investors inhibi-

ted by travel restrictions. Countries such as Czech Republic (-61.0%), Ireland (-62.0%)

-6% than H1 2019

and U.K. (-33.0%), with significant cross-border investors will be the hardest hit.

BNP PARIBAS REAL ESTATE 7

EUROPEAN REAL ESTATE

LIQUIDITY AND VOLUME OF TRANSACTIONS the UK historically respond very quickly to chan- 2024. The Nordics may move from 5.2% in 2020

Investment volumes (€bn) Dry Powder (€bn) Loan-to-Value (%) ges in market conditions and have remained sta- to 4.89% in 2024. UK logistics yields will re-

tic compared to the rest of Europe for a long time. main flat across most of the period.

350 45.0%

London West End yields may expand to 3.65% by

40.0%

300 2021 before reducing to 3.50% by 2024. The greatest upward shift will occur in retail

35.0% yields over the forecast period. Our forecast

250

30.0% We anticipate that logistics prime yields will for retail focused on prime high street, which

200 25.0% cease compression because of the recession is somewhat insulated so we are anticipating

and remain stable. Although we do not forecast low upward shift; greater disparity may occur

150 20.0%

average yields, it is probable given the current in other retail segments, particularly shopping

15.0%

100 risk aversion that this will increase strongly in centres. Much of the impact here is front loaded

10.0% most markets. at the start of the forecast with some regions

50

5.0% (the UK and Southern Europe) experiencing

0 0.0% At European level, we expect prime logistics compression towards 2024. We anticipate at Eu-

07 08 09 10 11 12 13 14 15 16 17 18 19 yields to stabilise at 4.88% in 2020 before fa- ropean level, retail yields to post 3.69% in 2020

Source: BNP Paribas Real Estate

lling steadily to 4.76% by 2024. All regions, before expanding gradually to 3.73% by 2024.

Prime yields likely to stay at healthy lows The economic backdrop suggests that offices except for the UK, may experience further Europe’s gateway cities may see yields increase

may witness a short-term increase in prime compression post 2021 reflecting post-Covid from 3.72% in 2020 rising to 3.73% by 2024, sta-

Factors internal to the property sector are yields over 2020-2021 before compression re- investor demand. France and the Nordics are bility driven by their higher proportion of luxury

more likely to drive yield shifts. What we are sumes towards the forecast end 2023/24. At likely see the largest compression. France may retailers, a sector with few of the structural is-

still likely to see in Europe is ongoing conver- the European level, this will see yields increase see yields move from 4.2% in 2020 to 4% by sues afflicting other elements of retail.

gence of prime office yields in the core CBDs from 3.30% in 2020 to 3.32% in 2021 before de-

given the limited availability of product. clining to 3.15%. Germany is likely to be static

to 2021 at 2.73% before falling to 2.68%. France UNEVEN EFFECT • Average yield shift by sector, End 2019 – End 2021, (basis points)

In times of downturn the question as to what is may stabilise at 3.12% (2020-2021) before fa-

Office Retail Logistics

prime and what is secondary comes to the fore. lling to 2.82% in 2024. By 2024, the Nordics may

Historically, downturn in real estate has acted post 3.55%, Southern Europe 3.51% and Benelux 100

as a sorting mechanism between the two. What 3.54%. CEE may achieve 4.70% having experien-

80

may make this issue more complicated, for the ced the least compression of all. For all regions,

office sector especially, is if some of the issues even with compression we are anticipating hi- 60

surrounding design and usage (remote wor- gher yields at forecast end than in our previous

king) that have arisen during lockdown start to round. We also expect the gap between yields in 40

manifest in the market. At present, we do not the gateway city yields and secondary cities to

20

see that occurring over the forecast period but widen slightly by forecast end in 2024.

it will remain something to watch. We are now 0

less likely to see the gap between prime and The UK, London offices especially, continues to

feature in our scenario of compression even with -20

secondary yields narrow sharply, particularly Germany France UK Nordics CEE Southern Benelux

for retail. both Brexit and Covid-19 as backdrops. Yields in Source: BNP Paribas Real Estate Europe

8 EUROPEAN PROPERTY MARKET OUTLOOK AUGUST 2020

EUROPEAN REAL ESTATE

Total Return may go negative Logistics total returns are anticipated to be AWAITING CLARITY • 2yr Average (2020-2021) Office Total Return, (% P.A.)

before a sharp recovery more stable at 4.3% in 2020 for Europe as a

whole before increasing to 5.6% in 2024, a mi- Cap Growth Income Return Total Return Average

In our previous forecast round, we suggested dterm beneficiary of post Covid demand. The

10.0

that investors needed to accept lower returns only region likely to witness negative return in 5.2

3.9 3.9

from real estate going forward. The recession 2020 is France at -0.4%. Logistics overall re- 5.00

2.0

3.2 1.3 2.7

1.3 1.1 1.8 0.5

has all but guaranteed this. We now see pri- presents the most stable sector for total return 0.0

0

me total returns (-2.2%) as negative in 2020 on across the forecast period. -0.1

-1.4 -0.9 -1.6 -2.1 -0.9 -1.6

-0.6 -0.3

-1.2

-2.8 -3.0

average across Europe. What is positive about -5.0 -3.1

-4.8 -5.4

returns for the office sector is that we anticipa- The impact of Covid on our revised forecasts is -6.8

-10.0 -8.5

te a strong recovery. We think that prime total most strongly experienced in the retail sector.

returns will average 4.2% over the five-year European retail is likely to post -8% in 2020 and -15.0

forecast period across Europe. For the wider we may even see double digit negative retur-

Vienna

Berlin

Frankfurt

Hamburg

Munich

Paris - CBD

La Defense

Lyon

Marseille

Lille

London - City

London - WE

Birmingham

Edinburgh

Dublin

Copenhagen

Helsinki

Stockholm

Oslo

Prague

Budapest

Warsaw

Bucharest

Milan

Lisbon

Madrid

Barcelona

Brussels

Amsterdam

office market total returns will hold up rather ns in a number of the regions including France

better in 2020 (+1.3%) but with less strength (-21%), CEE (-17%), Southern Europe (-12%),

in the later stages of the forecast period, given Benelux (-11%) and the UK (-10%). The posi- Source: BNP Paribas Real Estate

the high level of yields, averaging 4.4% over tive dimension to this is that negative returns

the forecast period. Most regions are likely to are frontloaded in the forecast and are likely

stay positive. France’s total return is negative to reverse 2022 with all regions creating low,

in 2020 (-3.5%), market returns may end up the positive returns by 2024. The strongest region

strongest by 2024 at 9.0% may be France at 15% by 2024.

SEEKING A FLOOR • 2yr Average (2020-2021) Retail Total Return, (% P.A.) A RESILENT SECTOR • 2yr Average (2020-2021) Logistics Total Return, (% P.A.)

Cap Growth Income Return Total Return Average Cap Growth Income Return Total Return Average

10.0 10.0

7.2 8.2

8.0 7.3 7.4

5.00 0.3 0.6 0.2 0.8

1.6 6.5 6.7

5.7 5.8 6.1 6.0 5.6 4.7 5.9

5.5 5.2 5.5

6.0 4.9 3.9

5.0

0 3.5

4.4

-0.1 4.0 2.7

-5.0 -4.3 -3.5 -3.6

-4.6 -5.3 -5.3 2.0

-6.7

-10.0 -8.1 -7.9

-10.4 -10.1 0

-10.8

-15.0 -14.1 -2.0

-20.0 -4.0

Greater Paris

Berlin

Ruhr Area

Frankfurt

Hamburg

Munich

Midlands

Copenhagen

Helsinki

Stockholm

Warsaw

Bucharest

Prague

Budapest

Milan

Madrid

Barcelona

Brussels

Amsterdam

Rotterdam

Venlo

London

Greater Paris

Vienna

Berlin

Frankfurt

Hamburg

Munich

Central

Birmingham

Dublin

Oslo

Copenhagen

Helsinki

Stockholm

Prague

Milan

Rome

Madrid

Barcelona

Amsterdam

London

Source: BNP Paribas Real Estate Source: BNP Paribas Real Estate

BNP PARIBAS REAL ESTATE 9

EUROPEAN REAL ESTATE

SECTOR PROSPECTS

OFFICES relocation moves seen post 2009. Companies

seeking to downsize will have limited options

(previous forecast 4.1%) and 5.3% in 2024. We

continue to hold the outlook that for most re-

Occupiers will return to workplaces with a different perspective if they wish to take large modern space gions low vacancy will remain the prevailing

condition by the end of 2024.

The European market going forward continue to

WITH WEAK ECONOMIC ACTIVITY, employment situation is receding over Europe, a return to be characterised by lack of modern Grade A space We expect prime rental growth for European

growth is the true casualty of Covid-19. Cu- the office may not be complete by end of 2020. with large floorplates. The deepest impact from offices to range between -2.6% to +1.9% over

rrent forecasts for growth are sharply down- COVID-19 for offices may occur in the development the 2020-2024 forecast period. Gateway ci-

graded for 2020 and 2021. Spain is worst at If we look back to 2009, the European office mar- pipeline where future large-scale units may not be ties are likely to see -2.1% in 2020 recover to

-4.5% for 2020, although growth remains weak ket was in much worse state than currently is the needed if occupiers switch their requirements. 1.7% by 2024. Regionally, France will see sha-

across the forecast period for all countries. case. Large-scale vacancy, double digit in most rpest fall back in 2020 at -5.5% and also the

This matters a lot for the real estate occupa- cases such as London West End at 10%, Dublin Poor economic and job growth, combined with lowest growth at the end of the period at 0.4%

tional sector and our outlook for the occupa- and Amsterdam both over 20%. In addition, ex- lower transactional volumes and a delayed pi- in 20924. Germany will scale back from 4.8%

tional market. tremely weak, relocation driven take-up meant peline may create a larger vacancy rate increa- in 2019 to 0.6% in 2020, being the only region

demand was non-expansionary for a long time. ses than we expected at the start of 2020. The likely to stay positive in 2020 and across the

Many people are on enforced leave (whether region with the lowest vacancy, Germany, is whole forecast period. The region with the

retained on government funded programs or Presently, there is no surfeit of ultra-cheap likely to see vacancy increase from 4.4% (pre- strongest rental growth at the end of the fore-

not) from their places of work. Although this modern space that will foster the large-scale vious forecast 3.1%) in 2020 to 4.8% in 2021 cast may be the Nordics at 2.7% by 2024.

SUPPLY PUSH • Vacancy rate in selected European markets (%) DEEP DIVE • Take-Up by Regions (000’s)

Germany France UK Nordics CEE Southern Europe Benelux

Current Vacancy 2020 2021 2007

16,000

25.0

14,000

20.0

12,000

15.0 -41.5%

10,000

10.0 +25.1%

8,000

5.0

6,000

0.0 4.000

Central Paris

Berlin

Frankfurt

Hamburg

Munich

Lyon

Lille

Central

Birmingham

Manchester

Dublin

Copenhagen

Helsinki

Stockholm

Prague

Warsaw

Milan

Madrid

Barcelona

Brussels

Amsterdam

London

2,000

-

Source: BNP Paribas Real Estate 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020* 2021*

Source: BNP Paribas Real Estate

* Forecast

10 EUROPEAN PROPERTY MARKET OUTLOOK AUGUST 2020EUROPEAN REAL ESTATE

RETAIL tailing. It is clear that retailers without some with the restriction on travel. It may be slow

form of digital presence were least agile to to return if current travel restrictions persist.

Survival of the most agile respond to store closure, yet many pure play

retailers also struggled to meet demand (es- It is not surprising that we anticipate severe

pecially groceries). downward pressure in retail over the first two

RECESSION WILL ONLY MAGNIFY THE PRO- years of our forecast period. At European level,

BLEMS encountered by retail property during Retail was already undergoing structural rents may post an outcome of -5.8% in 2020

lockdown where apart from activities clas- changes. What may take longer are discus- and -2.7% in 2021. Rental growth may be 1.5%

sed as “essential”, shops closed for several sions over future leasing and rental arrange- by forecast end. The three regions under se-

months. Retailers are already reducing the ments. The income from retail property deri- vere pressure in 2020 are CEE (-15%), Benelux

number of stores and their headcount. More ves from retailer’s operational performance (-8.4%) and Southern Europe (-8.1%). CEE is li-

locations are likely to become less viable for and if closed, none is generated. At present kely to continue to see weak growth across the

mass-market retail through physical stores this is prompting many responses across Eu- forecast period. The strongest region by 2024

thereby increasing the number of secondary rope from property owners and will undoub- will be France at 5%.

locations (and pitches at micro level) for in- tedly shape longer-term prospects for the

vestors. The impact will vary by retail sector sector.

type although a commonality will be a redu-

ced pool of retailers to act as tenants. From Our forecasts look at retail in core cities. This

a business perspective, the crisis legacy for retail segment derives considerable revenue

retail may be closure in the debate over Om- from touristic spending as well as domestic

ni-channel as the optimal structure for re- shoppers. Touristic spending almost vanished

EUROPEAN RETAIL MARKET MOMENTUM NON-FOOD RETAIL TRADE VOLUME GROWTH (% y/y)

0.5 March April May

Rental Value Growth (2020 -2021), % p.a.

Vienna Helsinki

0.0 20

Hamburg Stuttgart

Dusseldorf 10 8 8 7

-0.5 Oslo Munich Berlin 5 6 6

Glasgow 3 4

Stockholm 0

Paris 0

-1.0 -2 -4 -3 -3 -1

London Birmingham Milan -10 -6 -6 -7 -7 -7 -7

-9

-1.5 Manchester

-12 -12

-14 -14

-20 -19

-22 -21

-2.0 Madrid -23

Dublin Copenhagen -30 -26 -26

Rome -32 -33 -32 -33

-2.5 Barcelona -40 -37 -37

-39

Amsterdam

-3.0 -50 -46

-50

-55 -54

-3.5 -60

Austria

Czech

Republic

Belgium

Denmark

Finland

France

Germany

Ireland

Italy

Netherlands

Poland

Spain

Sweden

UK

Prague

-4.0

-7.0 -6.0 -5.0 -4.0 -3.0 -2.0 -1.0 0.0 1.0 2.0

Capital Value Growth (2020 -2021), % p.a.

Source: BNP Paribas Real Estate Source: Eurostat

BNP PARIBAS REAL ESTATE 11EUROPEAN REAL ESTATE

LOGISTICS fests in labour shortages leading to an overall and the UK are not likely to see negative rental

slowing in delivery times. Often suppliers carry growth in 2020. Germany and the UK may see

Stocking Up inventories to cover demand spikes and tem- rental growth in the region of 1.0% over much

porary shortages. The current problems will of the forecast period, making them the most

open the way to increase the level of inven- stable regions for rents.

THE VIEWPOINT OF THE LOGISTICS MARKET as tories to guarantee supply for the end custo-

a clear beneficiary from European lockdowns mer and that in turn may prompt demand for

depends greatly on which segment of the in- more space in the long term. However In the

dustry one looks at. The consumer led segment short term, we are likely to see similar level of

is witnessing a spike in occupational demand demand for logistic space over the past three-

brought about by changes in consumption ha- years. Supply may increase despite slowdown

bits of the population over lockdown. How tem- in the construction of new warehouses.

porary the additional space sought by opera-

tors in essential activities and ecommerce will We anticipate that supply expansion will redu-

be depends on whether adjusted consumption ce the thrust on logistics prime rents, although

patterns stick. mainly experienced in the form of more incen-

tives. Rents will experience a negative impact

Long distance shipping and air transport ends over 2020 at -0.5% for Europe as a whole befo-

of the industry experienced significant disrup- re recovering in 2021 at 1.8%. Rental growth is

tion from controls on movement. Disruption likely to fade by 2024 at 0.8%. The three largest

to the manufacturing supply chain also mani- logistics markets in Europe, Germany, France

EUROPEAN LOGISTICS MOMENTUM INDIVIDUAL USING INTERNET TO ORDER GOODS AND SERVICES, 2019 (%)

3.0 Households with Internet Access Individuals shopping online

Rental Value Growth (2020 -2021), % p.a.

Milan South East 100

2.0 Prague Heathrow

Greater Paris Barcelona

Hamburg Frankfurt 80

1.0 North West Munich

Stockholm Berlin Midlands Oslo

60

Rotterdam Vienna Ruhr Area

0.0 Bucharest Venlo

Helsinki Madrid Lisbon 40

Poznan Breda

-1.0 20

Budapest Amsterdam Brussels

Warsaw

-2.0 0

Copenhagen

UK

Denmark

Sweden

Norway

Netherlands

Germany

Finland

France

Ireland

Belgium

Czech

Republic

Austria

Spain

Poland

Hungary

Portugal

Italy

Romania

-3.0

-4.0 -3.0 -2.0 -1.0 0.0 1.0 2.0 3.0 4.0 5.0

Capital Value Growth (2020 -2021), % p.a.

Source: BNP Paribas Real Estate Source: Eurostat; E-Commerce Europe

12 EUROPEAN PROPERTY MARKET OUTLOOK AUGUST 2020OUTLOOK

Regional

THE CURRENT RECESSION HAS THROWN UP THE DIFFERENCES

IN INVESTMENT ACTIVITY AND PERFORMANCE IN DIFFERENT

REAL ESTATE SECTORS AND MARKETS. AS SUCH THERE IS

A TRADE-OFF BETWEEN CAPITAL PRESERVATION AND

HIGHER RETURNS. CONSEQUENTLY, INVESTORS WILL NEED

RE-EXAMINE THE FUNDAMENTALS OF THE REAL ESTATE

SECTORS AT CITY LEVEL ACROSS EUROPE’S REGIONS.

BNP PARIBAS REAL ESTATE 13PLAYING CATCH-UP

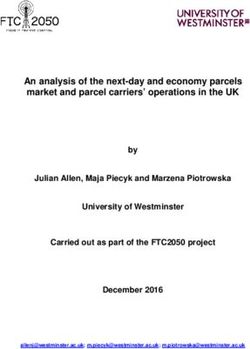

UNITED KINGDOM AND IRELAND

THE UK ENFORCED A FULL LOCKDOWN much later than than its their appetite for real estate, with not only existing deals being

European counterparts, while the Irish government was quick reviewed but also potential new deals put on hold indefinitely.

to announce its restrictions and lockdown measures to contain The nature of real estate activity meant that the lack of physical

the spread of COVID-19. Nonetheless, the economic impact will interaction and the inability to meet with clients would have a

still be significant for both economies, with UK GDP expected to detrimental impact on trading activity. We expect transaction

fall by 8.5% and Irish GDP by 4.9% in 2020. According to Moody’s levels to begin picking up somewhat in the third quarter; howe-

forecasts, Ireland will recover sooner than the UK, largely due ver, year-end investment volumes are still likely to be much

to the relatively strong position of its economy when entering lower than previously anticipated. UK investment will be down

the pandemic. by 26% compared to 2019 levels, reaching £35bn. Ireland had

enjoyed record levels of investment of late, so transaction vo-

In terms of real estate, Q1 investment volumes indicated that lumes were always likely to be lower in 2020. With the impact

both the UK and Ireland were on course for relatively healthy of the pandemic, and little or no activity over two quarters, we

2020 investment totals. However, as COVID-19 took hold across expect Irish investment volumes to total £1.8bn by year end,

the world with lockdowns enforced, investors began moderating considerably lower than last year.

INVESTMENT VOLUME (€bn) 5YR (2020-2024) AVERAGE TOTAL RETURN BY SECTOR (%, p.a.)

chart 2

UK Ireland Cap Growth Income Return Total Return

100 6.0 8.0

6.0 5.4

90 5.0

2.0 3.7

COVID-19 HAS ACCELERATED MANY

4.0

80 4.7

4.0 2.0 1.1

TRENDS, ONE OF WHICH IS THE

70

3.0 0

60 -2.0

RELIANCE ON E-COMMERCE. 50

61.2 2.0 -4.0

-1.1

THIS WILL POSITIVELY IMPACT 40 1.0 -6.0

UK Ireland UK UK Ireland

THE LOGISTICS SECTOR, AT THE 30

15 16 17 18 19 20* 21*

0

Offices Logistics Retail

COST OF THE RETAIL SECTOR. Source: BNP Paribas Real Estate * Forecast Source: BNP Paribas Real Estate

14 EUROPEAN PROPERTY MARKET OUTLOOK AUGUST 2020UNITED KINGDOM AND IRELAND

OFFICES

CENTRAL LONDON offices have shown relative strenth during FOR DUBLIN the office development pipeline was anticipated to

Brexit and are likely to be tested further. An advantage playing reach new highs in 2020. However, due to the halt in construc-

in Central London’s favour is the fact that it was at a different tion activity, approximately 40% of the planned deliveries have

stage of the cycle entering the pandemic, partly down to Bre- been postponed to 2021. Although this will help contain the fall

xit paralysis. As a result, we predict a lesser impact on yields, in rents, the nature of the lockdown is likely to cause some ren-

with prime office yields moving out by 10bps and reaching 3.60% tal adjustments this year, similar to those witnessed last year

by the end of 2020. Meanwhile, rental growth has been large- as occupiers began to reconsider their options. Dublin prime

ly down due to the imbalance of demand and supply. Despite office rents are expected to decline by 4% this year. Meanwhile,

construction sites being closed, which has constrained supply Dublin prime office yields have been relatively stable at 4.00%

further, the evaporation of demand means that an adjustment since 2017, largely reflective of increased and ongoing investor

in rental levels will occur as incentives had probably gone as far interest in the market. This is down to many reasons, including

as they could. It gives some respite that the impact is likely to strong fundamentals and, to some extent, the Brexit paralysis

be more muted than in previous downturns experienced by the that had engulfed the UK. Looking ahead, the pandemic will

market. Nonetheless, prime rents will fall in the City by 3.8%, in leave a mark on both markets, and we therefore expect Dublin

the West End by 9.5% and in Midtown by 7%. yields to also move out by 10bps this year.

TAKE-UP (000’s sqm) AND VACANCY RATE (%) PRIME RENTAL VALUE INDEX (2015 = 100) PRIME OFFICE YIELDS (%)

Take-up Vacancy rate Central London Birmingham Manchester Central London Birmingham Manchester

Edinburgh Dublin Edinburgh Dublin

1400 8.0% 400 9.0% 120 5.50

7.0% 8.0%

1200

7.0% 110 5.00

6.0% 300 4.75

1000

6.0%

5.0%

800 100 4.50

5.0%

4.0% 200

600 4.0% 4.00

3.0% 90 4.00

3.0%

400

2.0% 100 2.0%

200 1.0% 80 3.50

1.0% 3.50

0 0.0% 0 0.0%

19 20 * 21* 19 20 * 21* 70 3.00

Central London Dublin 15 16 17 18 19 20* 21* 15 16 17 18 19 20* 21*

Source: BNP Paribas Real Estate Source: BNP Paribas Real Estate Source: BNP Paribas Real Estate * Forecast

BNP PARIBAS REAL ESTATE 15UNITED KINGDOM AND IRELAND

RETAIL

A NUMBER OF FORCES have negatively impacted the retail sec- Street and Henry Street had been increasing due to their appeal,

tor to date and, for the UK in particular, one of the biggest fac- but this year will be tough on retailers and we anticipate that

tors has been business rates. Although the Chancellor offered prime rents will fall by 6.5% this year.

a relaxation of business rates early on in the lockdown, it will

not be enough to mitigate the damaging effects on the sector. The sector certainly looks like a challenging market in the cu-

As a result, we expect retail yields to increase across the UK, rrent climate, however it shouldn’t be completely written off.

with disparities across the regions. Central London prime high Retail too, just like the other sectors, will evolve, and become

street will somewhat retain its appeal, with yields moving out relevant again. Retailers are beginning to keep up with consu-

by 50bps to 3.50% by the end of the year. For Dublin, the huge mer trends and preferences, this is likely to become key in the

fall in trading will, like the UK, push a number of retailers over success of retailers going forward.

the edge. Even so, the nature of prime high street retail means

that the damage will not be as severe as in out-of-town shop-

ping centres. We forecast Dublin prime retail yields to also move

out by 50bps, a movement in yields which has been extended

further by the pandemic. Prime high street rents on Grafton

PRIME RETAIL RENTAL VALUE INDEX (2015 = 100) PRIME RETAIL YIELDS (%)

Central London Birmingham Manchester Central London Birmingham Manchester

Glasgow Dublin Glasgow Dublin

160 7.00

150

6.00

140

130 5.00

5.00

120

4.00

110

3.25

100

3.00

3.00

90

80 2.00

15 16 17 18 19 20* 21* 15 16 17 18 19 20* 21*

Source: BNP Paribas Real Estate Source: BNP Paribas Real Estate * Forecast

16 EUROPEAN PROPERTY MARKET OUTLOOK AUGUST 2020UNITED KINGDOM AND IRELAND

LOGISTICS

WHAT THE COVID-19 CRISIS HAS SHOWN is the extent to which trial sites. The increasing importance of e-commerce in retailing

online shopping has become essential and will continue to be the will continue to shift investor focus away from retail asset to logis-

case. We are highly likely to witness a rapid increase in e-com- tics. That said, the traditional manufacturing side of the industrial

merce volumes, something that is now being reflected in con- market is more exposed to the health of the global economy. For

sumer spending numbers after lockdown. Despite retailers now example, severely disrupted supply chains and a slump in global

opening their shop doors, many are still choosing to shop online. demand forced Tata Steel and Jaguar Land Rover to approach the

This will positively impact the logistics sector, with it likely to fare government to try to secure emergency funding. New car registra-

noticeably better than others. The supply of logistics property will tions are down 42% y-o-y. With Brexit uncertainty and global trade

continue to be restricted and, with demand continuing to be re- tension both ongoing, manufacturing and its supply chains could

latively strong, we expect yields to remain unchanged this year act as a brake on industrial market in the short to medium term.

for the UK at 4.00%. As demand continues to gather steam, we

forecast that yields will compress by 10bps in 2021. Overall, we are likely to see retailers continue to drive demand

for logistics space, and e-commerce facilities dominating logis-

Supply will be limited in the short-to-medium term, as such we tics take-up. Despite the economic headwinds, we remain posi-

could see the conversion of redundant shopping centres into indus- tive about the logistics sector.

PRIME LOGISTICS RENTAL INDEX (2015 = 100) PRIME LOGISTICS YIELDS UK (%)

Heathrow South East North West Midlands

130 5.00

4.50

4.0

4.00

120

3.50

3.00

110

2.50

2.00

100 1.50

1.00

90 0

15 16 17 18 19 20* 21* 15 16 17 18 19 20* 21*

Source: BNP Paribas Real Estate Source: BNP Paribas Real Estate * Forecast

BNP PARIBAS REAL ESTATE 17MIXED RESPONSE: SIMILAR OUTCOMES

NORDICS

THE NORDICS APPROACH to the pandemic has varied across coun- economy is expected to only contract by 3.6% in 2020. Sweden

tries. Norway was one of the first to curb activities in order to rein will likely come out of the pandemic in a better position than the

in the spread of COVID-19. Denmark, like Norway, was quick to rest of the Nordics, as investors have still been able to visit and

adopt tough measures to contain the spread of the virus. Although do deals. Nonetheless, we anticipate a reduction in transactions

early adoption of preventive measures was intended to buffer the this year with investment volumes for Sweden totalling €19bn.

economic impacts, the effects of the lockdowns have already left Norway has fast become a favourite among investors, with more

their mark. Finland initially took a relatively relaxed approach to overseas investors entering the market than ever before prior to

dealing with the pandemic, but subsequently applied stricter mea- the crisis. While this has been a positive, COVID-related restric-

sures in early April, potentially cutting off the capital from the rest tions will have a marked negative impact on Norway’s commer-

of the region. Finnish economic growth is expected to deteriorate cial real estate market, with the absence of overseas investors

most among the Nordic nations, with its growth contracting by 8% highly apparent. As a result, we expect investment trading levels

in 2020. Sweden was the outlier in not enforcing a strict lockdown; in Norway to fall by 35% this year to €58bn. Meanwhile, Finland’s

even so, despite the absence of strict restrictions, some retailers, investment volumes are projected to be down by 10% on 2019 le-

leisure venues and workplaces did close. However, the fact that vels at €4.2bn and, similarly, Denmark’s volumes will also shrink

Sweden kept its borders open will probably work in its favour: the by some 10% to reach €3.8bn by year end.

INVESTMENT VOLUME (€bn) 5YR (2020-2024) AVERAGE TOTAL RETURN BY SECTOR (%, p.a.)

Norway (LHS) Sweden (RHS) Cap Growth Income Return Total Return

Finland (LHS) Denmark (RHS)

14 3.5 10.0 8.3

7.3

12 3.0 8.0 6.7

6.1 5.7

6.0 4.3 4.0 4.6

2.9

0.5

10 8.9 2.5 4.0 2.4 2.8

2.0

THE LIGHT TOUCH RESPONSE 8

6

1.9

2.0

1.5

0

TO THE PANDEMIC IN A NUMBER

-2.0

4 1.0 -4.0

4.7

OF MARKETS WILL HELP THE NORDICS

Copenhagen

Helsinki

Stockholm

Oslo

Copenhagen

Helsinki

Stockholm

Oslo

Copenhagen

Helsinki

Stockholm

Oslo

2 0.6

0.5

REGION TO COME OUT OF THE 0

15 16 17 18 19 20* 21*

0

Offices Logistics Retail

PANDEMIC IN A BETTER SHAPE. Source: BNP Paribas Real Estate * Forecast Source: BNP Paribas Real Estate

18 EUROPEAN PROPERTY MARKET OUTLOOK AUGUST 2020NORDICS

OFFICES

THE SLOWDOWN IN INVESTMENT ACTIVITY has eradicated relatively modest. The halting of construction projects by the

the prospect of yield stability that was previously forecast. We lockdown means that supply will be even more limited. Even so,

now expect prime office yields to move out by 15bps on average this will not be enough to mitigate the downward pressure on

across the Nordics. Helsinki prime yields will move out the most, rents as many occupiers start to re-evaluate and readjust to the

by 20bps this year, as Helsinki is more in the later stage of the ‘new normal’ post COVID-19. Stockholm is anticipated to expe-

cycle than others, to reach 3.20%. Oslo and Copenhagen prime rience a moderate -1% adjustment in prime office rents, while

yields will go up by 15bps, while Stockholm prime yields will Copenhagen and Oslo prime rents are projected to both fall by

increase by 10bps by the end of 2020. 2%. Helsinki will see the largest adjustment with its prime rents

declining by 8.5%.

Occupiers faced with empty buildings due to the lockdown, as

shown by the uptick in vacancy rates, will push office tenants

to negotiate rents at a much lower level. We therefore forecast

a decline in rents in 2020 across the major Nordic office mar-

kets. Furthermore, even before the onset of COVID-19, the offi-

ce development pipeline for the Nordics for 2020 was already

TAKE-UP (000’s sqm) AND VACANCY RATE (%) PRIME RENTAL VALUE INDEX (2015 = 100) PRIME OFFICE YIELDS (%)

Oslo Stockholm Helsinki Copenhagen Oslo Stockholm Helsinki Copenhagen

Take-up Vacancy rate

% 150 5.00

900 16

800 14 140 4.50

700 12

130 4.00

600 3.75

10

500 3.50

120 3.50

8

400 1.90

6 110 3.00

300 3.00

200 4

100 2.50

100 2

0 0 90 2.00

19 20* 21* 19 20* 21* 19 20* 21* 15 16 17 18 19 20* 21* 15 16 17 18 19 20* 21*

Oslo Stockholm Helsinki

Source: BNP Paribas Real Estate Source: BNP Paribas Real Estate Source: BNP Paribas Real Estate * Forecast

BNP PARIBAS REAL ESTATE 19NORDICS

RETAIL

RETAIL WILL BE THE BIGGEST CASUALTY OF THE PANDEMIC 2019 was particularly tough, with leasing activity in the city de-

across the Nordics, pushing many retailers over the edge. As a clining and vacancy ticking up on even the most sought-after

result, prime retail yields are likely to move out on average by prime high street locations. The pandemic will only exacerbate

25bps across the region. E-commerce in the Nordics is not as some of the existing challenges for retail in Oslo.

mature as it is in countries such as the UK, with consumers still

preferring to shop in prime high streets and shopping centres. Looking ahead, the size and the role of physical stores will re-

main an uncertain aspect of retail. Over the past few years, the

This means that retail across the region will be able to weather Nordics retail sector has been growing while large mainland

this crisis better than its European counterparts. Helsinki prime European destinations have been struggling. Unfortunately, CO-

retail yields are forecast to move out by 20bps to 4.20% by the VID-19 will likely accelerate e–commerce penetration and hen-

end of 2020, while Stockholm will also witness yields increasing ce its impact on the retail sector. By the end of the forecast pe-

by 20bps to 3.60%, as will Copenhagen to 3.40% this year, from riod, we see Nordics retail challenged in a similar way as most

3.20% in 2019. Oslo’s yields will rise the most by year end, by European markets.

35bps to 4.35%. The retail sector in Oslo continues to struggle;

PRIME RETAIL RENTAL VALUE INDEX (2015 = 100) PRIME RETAIL YIELDS (%)

Oslo Stockholm Helsinki Copenhagen Oslo Stockholm Helsinki Copenhagen

120 5.00

115

4.50

110

4.0

105 4.00

4.0

100

3.50 3.4

95

3.2

90 3.00

15 16 17 18 19 20* 21* 15 16 17 18 19 20* 21*

Source: BNP Paribas Real Estate Source: BNP Paribas Real Estate * Forecast

20 EUROPEAN PROPERTY MARKET OUTLOOK AUGUST 2020NORDICS

LOGISTICS

AS E-COMMERCE HAS STILL BEEN RELATIVELY SLOW to pick up has been no excess space on the market. Helsinki has experien-

across the Nordic region, the demand for logistics has been re- ced limited development activity to date, and any deliveries that

latively moderate. Nevertheless, online retail sales as a propor- would have been expected this year have been halted. However,

tion of total retail sales in the Nordics are hovering around 10%, even with the shortfall in supply, the lack of further take-up in

which is about the point when the demand for logistics real logistics means we can predict some adjustment in rental levels

estate in the UK accelerated. Notwithstanding the current back- in the coming months. Prime rents will fall by 1.8% on average

drop, where COVID-19 has certainly dampened prospects across across the region, with Copenhagen experiencing a larger ad-

most property asset types, logistics is likely to perform the best justment in rental levels compared to the other Nordic markets.

across all sectors. We also expect demand to moderate, with yields moving out by

5bps on average across the region, while Oslo logistics yields

The lack of supply has definitely been an issue across the region. will remain stable this year.

Stockholm logistics has benefitted from demand outstripping

supply to date, while Copenhagen saw a slight uptick in availa- Looking ahead, the logistics sector across the region will gain

bility last year. However, with demand remaining robust, there greater interest among investors as they search for yields.

PRIME LOGISTICS RENTAL INDEX (2015 = 100) PRIME LOGISTICS YIELDS (%)

Oslo Stockholm Helsinki Copenhagen Oslo Stockholm Helsinki Copenhagen

130 7.50

7.00

120

6.50

6.00

110 5.60

5.50

5.25

5.00

100 5.00

4.50 4.7

90 4.00

15 16 17 18 19 20* 21* 15 16 17 18 19 20* 21*

Source: BNP Paribas Real Estate Source: BNP Paribas Real Estate * Forecast

BNP PARIBAS REAL ESTATE 21LEADING EUROPE’S RECOVERY

GERMANY

COMPARED WITH OTHER EUROPEAN COUNTRIES, Germany was tate market was on its way to a healthy 2020. However, the on-

relatively quick to impose a lockdown, thus preventing a faster set of the pandemic in the second quarter represented a turning

spread of the COVID-19 virus. At the same time, the economy point in overall economic and real estate development. When

almost came to a complete halt. To counteract the effects of its COVID-19 gained a foothold worldwide and lockdowns were en-

lockdown, the German government plans to spend up to €1.4 tri- forced, second quarter take-up not only declined but investment

llion on related aid. This includes immediate support for compa- volumes too compared to the same period last year. Virtual con-

nies and the self-employed, guarantees for loans, and numerous tact could not replace the physical interaction required for in-

measures in an economic stimulus package ranging from VAT vestment transactions. Even so, despite the Q2 fall in trading,

reduction to child bonuses. Although we expect the German eco- the 2020 half-year result was a new record for the investment

nomy to shrink by 6.5 % of GDP in 2020, the economy could grow market, almost entirely attributable to the outstanding figures

again by 5.0 % in 2021 with the support of the economic stimu- posted for Q1. We anticipate that investment volumes will pick

lus package. This assumption is largely consistent with the fo- up somewhat in the fourth quarter, but will still likely to be

recasts of the established German economic research institutes. lower than originally forecast for the full year. Of more concern,

Both the large investment volumes and the high take-up in the the decline in office space take-up is likely to be even more pro-

first quarter of 2020 clearly indicated that the German real es- nounced.

INVESTMENT VOLUME (€bn) 5YR (2020-2024) AVERAGE TOTAL RETURN BY SECTOR (%, p.a.)

Germany Cap Growth Income Return Total Return

80

73.4 5.61

6.0 5.32

70

4.0 2.10

GERMANY AT THE FOREFRONT 60

2.0

OF COVID-19 RESPONSE, 50 0

IS NORMALIZING QUICKLY -2.0

WITH ITS REAL ESTATE MARKET 40

15 16 17 18 19 20* 21* Office Logistics Retail

ALMOST COMPLETELY REACTIVATED Source: BNP Paribas Real Estate * Forecast Source: BNP Paribas Real Estate

22 EUROPEAN PROPERTY MARKET OUTLOOK AUGUST 2020GERMANY

OFFICES

THE OFFICE MARKETS OF THE ‘GERMAN BIG 7’ could experience main stable or even rise slightly. The amount of available space

a dichotomy this year. While the investment markets could pro- is still very limited, especially in central city locations, Munich

ve to be relatively crisis-proof, the occupier markets are likely to being the possible exception. The rental uplifts seen in Munich

be subject to slumps. Prime yields appeared stable at the end in the first quarter of 2020 will probably not be sustainable by

of the first half of 2020 and we do not expect them to rise until the end of the year. By the end of 2022, up to 1.2 million sqm of

the end of the year. For 2021 we anticipate stable prime yields new office space could enter the Munich market and raise the

and for 2022 we expect yield compression of 5bps in all seven vacancy rate from the current 2.6% to possibly 3.6%. We expect

markets. The only exception is Berlin, where prime yields could this development to peak at 4.2% at the end of 2024.

even fall by another 5bps in 2023.

Prime total returns range between 5% and a good 6% p.a. on

The situation is somewhat different in the occupier markets. average over the forecast period until 2024, with Stuttgart and

Office space take-up, in particular, could decline significantly Berlin leading the way with 6.4% and 6.3% p.a. respectively.

in the near future. On average across the Big 7, we forecast a

year-on-year decline of 25% to 30% in 2020. However, due to the

largely low vacancy rates in all markets, prime rents will re-

TAKE-UP (000’s sqm) AND VACANCY RATE (%) PRIME RENTAL VALUE INDEX (2015 = 100) PRIME OFFICE YIELDS (%)

Berlin Munich Hamburg Frankfurt Berlin Munich Hamburg Frankfurt

Take-up Vacancy rate

% 170 5.00

1100 8.0

1000 160

7.0

900 150

800 6.0

4.00

700 140

5.0

600 130

4.0

500

3.0 120

400 3.00 2.80

300 2.0 110

200

2.60

1.0 100

100

0 0 90 2.00

19 20* 21* 19 20* 21* 19 20* 21* 19 20* 21* 15 16 17 18 19 20* 21* 15 16 17 18 19 20* 21*

Berlin Frankfurt Hamburg Munich

Source: BNP Paribas Real Estate Source: BNP Paribas Real Estate Source: BNP Paribas Real Estate * Forecast

BNP PARIBAS REAL ESTATE 23GERMANY

RETAIL

THE PANDEMIC HAS ACCELERATED WHAT WAS ALREADY APPA- perties on the main shopping streets, we forecast stable prime

RENT in the bricks-and-mortar retail market, with the competi- yields (with a slight downside risk) to increase by 5bps. Accor-

tion with online retail exposing the limits of retailers’ ability to dingly, the retail sector has the lowest total returns compared to

pay rent. The numerous insolvencies in the sector since March office and logistics, averaging 1.8 to 2.3% p.a. over the forecast

2020 are harsh evidence of this battle. However, since our fo- period.

recast focuses on retail in the still sought-after prime locations,

the effects in this sector are not yet as severe as in outlying

locations or in some out-of-town shopping centres. Although we

expect rents in all Big 7 markets to fall by an average of 3% this

year and by less than 2% next year, prime rents could almost

return to the levels achieved at the end of 2019 by the end of

the forecast period. Due to product shortage and the, at least,

steady to good long-term development potential of retail pro-

PRIME RETAIL RENTAL VALUE INDEX (2015 = 100) PRIME RETAIL YIELDS (%)

Berlin Munich Hamburg Frankfurt Berlin Munich Hamburg Frankfurt

140 4.00

3.80

130

3.60

120

3.40

110 3.20

3.10

3.00

3.00

100

2.80

2.80

90 2.60

15 16 17 18 19 20* 21* 15 16 17 18 19 20* 21*

Source: BNP Paribas Real Estate Source: BNP Paribas Real Estate * Forecast

24 EUROPEAN PROPERTY MARKET OUTLOOK AUGUST 2020GERMANY

LOGISTICS

ONLINE RETAIL AS AN IMPORTANT DRIVER OF THE LOGISTICS already risen by 3% in the first half of 2020 and will remain sta-

INDUSTRY has been posting impressive growth rates for some ble until the end of the year. Over the entire forecast period, ren-

years now. These have been exacerbated by the pandemic, and tal growth in the five most important logistics regions in Ger-

many consumers who have become online dependent during many could average 1.2 % per year. We also anticipate a slight

the lockdown will not abandon this new behaviour, even with decrease in prime yields of 5 bps year on year until 2022. Only

the relaxation of lockdowns. This will have a correspondingly in the last year of our forecast period do we see an increase in

positive effect on the logistics sector. Although demand declined prime yields (+5 bps). This means that total return will be good,

in Q2 2020 due to the contact restrictions, we expect take-up to although not to the same level as expected in the office sector

be back at or in some cases even above the 10-year average by

the end of next year.

Due to limited supply, we anticipate prime rents to remain sta-

ble or slightly increase in some markets. In Frankfurt, this has

PRIME LOGISTICS RENTAL INDEX (2015 = 100) PRIME LOGISTICS YIELDS (%)

Berlin Munich Hamburg Frankfurt Berlin Munich Hamburg Frankfurt

160 6.00

150 5.50

140

5.00

130

4.50

120

4.00

110

3.70

100 3.50

90 3.00

15 16 17 18 19 20* 21* 15 16 17 18 19 20* 21*

Source: BNP Paribas Real Estate Source: BNP Paribas Real Estate * Forecast

BNP PARIBAS REAL ESTATE 25PARIS REMAINS AN ATTRACTIVE MARKET

FRANCE

WITH THE EASING OF FRANCE’S LOCKDOWN, the economy has 2019, with the contraction primarily reflecting the market slow-

been showing signs of strong activity, raising hopes for a V-sha- down and delaying of deals. As lockdown measures are eased,

ped recovery. However, though the hard data are positive, the transactions should pick up again over the second half of the

rebound appears to be largely a technical effect that should les- year and total investment volumes for full-year 2020 should

sen as the catch-up effect wears off. Now that supply has star- be around €24bn. During an economic slowdown, cross-border

ted to recover, the main uncertainty for the country is whether investment tends to reduce and we should therefore see an

demand can be sustained in the coming months. We foresee a increase in the share of domestic investment in 2020. Indeed,

U-shaped recovery (-11.1% in 2020, +5.9% in 2021). However, it France’s domestic investors now account for more than 60% of

will take longer for some of France’s regions to return to pre-cri- transaction volumes and this trend should continue at least un-

sis levels due to the differences among them. til the end of the year.

The French real estate investment market was hit hard by the With the uncertainties in the economic environment, some re-

COVID-19 crisis in Q2. Even so, thanks to a historically strong pricing may occur in the coming months, although not all asset

Q1, H1 2020 investment was down by just 21% compared to H1 classes will be impacted equally.

INVESTMENT VOLUME (€bn) 5YR (2020-2024) AVERAGE TOTAL RETURN BY SECTOR (%, p.a.)

France Cap Growth Income Return Total Return

45 6.0 5.7

41.5

40 3.6

4.0

35 2.0

0

30

THE LOGISTICS SECTORS IS LIKELY 25

-2.0 -0.7

TO CREATE THE STRONGEST -4.0

RETURNS BY SECTOR OVER 20

15 16 17 18 19 20* 21* Office Logistics Retail

THE FORECAST PERIOD Source: BNP Paribas Real Estate * Forecast Source: BNP Paribas Real Estate

26 EUROPEAN PROPERTY MARKET OUTLOOK AUGUST 2020You can also read