PROGRESS UPDATE ON STRATEGY AND FUTURE PLANS - JAMES CAMPBELL JUNE 2012

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

PROGRESS UPDATE ON STRATEGY AND FUTURE PLANS JAMES CAMPBELL JUNE 2012

2

STOP PRESS!

• STEINMETZ FOREVERMARK JUBILEE PINK

• Saxendrift diamond selected for display at the

TOWER OF LONDON as part of Queens Diamond Jubilee

• The cushion cut, pink-brown diamonds weighing 35.60

carats, was cut from a 179.60 carat rough diamond that was

sold into the Company’s BENEFICIATION joint venture with

Steinmetz Diamond Group (“SDG”)

FOCUS ON DIAMOND VALUE MANAGEMENT

3

AGENDA

• WHO IS ROCKWELL?

– Beneficiation and Rough Diamond Production

– Operations and Resources

– Team First diamonds recovered from bulk x-ray machine at Saxendrift

– Capital structure and shareholding

• PROGRESS UPDATE

– Performance overview

– Strategic review

– Progress with turnaround

– Investments and Technology Projects

– Valuation Gap

• WAY FORWARD

– Operational targets

– Growth objectives

– Diamond sector fundamentals

– Priorities and outlook

FOCUS ON DIAMOND VALUE MANAGEMENT

4 WHO IS ROCKWELL?

5

BENEFICIATION JOINT VENTURE: SIGNIFICANT VALUE ADD

BENEFICIATION

ROUGH POLISHED

VALUE ADD

105 ct Type II 35 ct D color internally +62% on initial rough

A, Middle flawless

Sold for $230,000/ct sale price

Orange

212 ct yellow, +50% on initial rough

102 ct vivid yellow

Middle Orange sale price

128 ct yellow,

81 ct vivid yellow Not yet sold

Middle Orange

Steinmetz Diamond Group (SDG) profit share agreement (>2.8 carat stones)

• MARKET RELATED PRICES for diamonds sold into JV + 50% profit share

• Realized revenue of $7.8m in F2012

• ±25% of revenue from beneficiation, expected to increase

FOCUS ON DIAMOND VALUE MANAGEMENT

6

ROCKWELL ROUGH DIAMOND PRODUCTION: AVERAGE US$/CARAT

World Diamond Average

Small diamonds used in lower

$90/carat price point and pavé jewellery

7

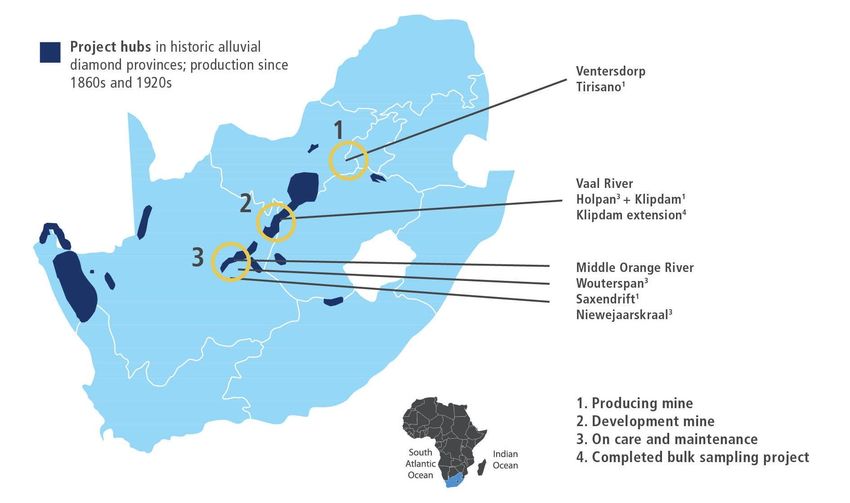

ROCKWELL OPERATIONS AND PROJECT LOCALITIES:

NORTHERN CAPE AND NORTH WEST PROVINCES, SOUTH AFRICA

FOCUS ON DIAMOND VALUE MANAGEMENT

8

EXTENSIVE DEPOSITS TO BENEFIT FROM DIAMOND FUNDAMENTALS

Volume (m3) Value (USD)

See www.rockwelldiamonds.com for detailed 43-101 Mineral

Category Carats Reserves & Resources: At 28 February 2011.

Feb 28 2011 millions Estimates completed by Rockwell’s Manager, Resources, G.A. Norton, (Pr.

Sci. Nat.), a qualified person who is not independent of the Company.

Probable reserves 4,565,400 22,827 46.3 Reviewed by T.R. Marshall, PhD, (Pr. Sci. Nat.), Marshall, an independent

qualified person

Indicated resources 34,787,600 675,412 489.6

Inferred resources 82,062,000 828,641 1,141.1

1,677.0

Processing capacity 43-101 value

Operation Carats per month Life of Mine (years)

(m3 p.m. ) (US$ per carat)

Middle Orange River:

150,000 750 2,029 5

Saxendrift

Vaal River:

Klipdam: 90,000 Klipdam: 850 Klipdam: 1,229 Klipdam: 2

Holpan* and Klipdam

Ventersdorp:

90,000 1,400 606 18

Tirisano

FOCUS ON DIAMOND VALUE MANAGEMENT

9

LEADERSHIP TEAM WITH CREDENTIALS TO DELIVER VALUE

Board of Directors:

Group Technical

Mark Bristow (Chairman) CFO

Manager

Dave Copeland Gerhard Jacobs,

BAcc, MBA Glenn Norton,

Richard Linnell BSC (Hons)

Willem Jacobs

Sandile Zungu

Johan van’t Hof Mining and corporate experience with Geological, mineral resource

Stephen Dietrich junior and senior mining companies with management and production

operations in SA, Australia and Canada. experience in alluvial diamond deposits,

Knowledge of public listed mining diamond and coal exploration. Qualified

Companies. person and Pr.Sci.Nat.

President and CEO COO

Diamond Marketing & Sales

James Campbell, Michael Hunt, Manager

BSc (Hons ) ARSM, MSc (Advanced Chemical

MBA (Dunelm) Engineering) Jeffrey Brenner

Seasoned diamond executive with >30 yrs in diamonds incl. mgt. roles at A leading international diamantaire and

career spanning over 20 years at De Orapa (world’s largest diamond mine) &

specialist in valuation, marketing and

Beers and 4 years as Managing The Oaks (De Beers’ smallest mine).

Director of African Diamonds plc. Operations Manager at Pangea sales of rough diamond production from

FIMMM, C.Eng, C.Sci and Pr.Sci.Nat. DiamondFields plc from 2007. alluvial deposits.

Group HR/IR Manager

Corporate Development

Richard Mhlonto,

Nat Dip (HR Management Stéphanie Leclercq

Dr Kurt Petersen, & Development) BSc, CFA

Ph.D. (Stellenbosch)

Extensive HR & Industrial Relations >12 yrs in investor relations and

management experience including

Expert in economic diamond metallurgy. corporate development. Worked as a

organizational and structural design

Contracted to Rockwell for fiscal 2012. sell side analyst and in-house IRO

initiatives as well as strategy

development and implementation. across industry sectors.

FOCUS ON DIAMOND VALUE MANAGEMENT

10

CAPITAL STRUCTURE AND SHAREHOLDING

Top shareholders (% shares in issue)

Number of shares

Strategic:

Shares outstanding 47,942,746 • Daboll (Steinmetz) 21.3%

Warrants - • Godia Capital 8.3%

• Middle East Investors 7.1%

Options ($0.90-9.45) 2,121,931

Institutional:

Convertible Debt (~$0.56) 3,499,257

• Conus Partners 6.9%

Fully Diluted 53,563,934 • Earth Resources (ERIG) 3.6%

• Craton Capital 2.6%

• Wells Capital 1.6%

Other:

• Etruscan 2.6%

• Mark Bristow 1.2%

FOCUS ON DIAMOND VALUE MANAGEMENTPROGRESS UPDATE

12

FISCAL 2012 PERFORMANCE OVERVIEW

• Substantial progress with REPOSITIONING of Rockwell by new management

• Beneficiation continues to add value: 64% INCREASE in beneficiation revenues to $7.8m

• Saxendrift performance trending up: Direct result of DIAMOND VALUE MANAGEMENT strategy

– 26% INCREASE in rough diamond sales to US$17.5m with 22% increase in average carat value

• Long term production asset BROUGHT ON STREAM: Tirisano mine ramp up making progress

– One time cost of ramp up of $6.7m charged to earnings

• Operating profit of $7.3m: Mining costs DOWN 4% despite impact of Tirisano costs

• Net loss of $13.7m: Impact of STRATEGIC DECISIONS place Rockwell on a SOLID FOOTING

with cleaner balance sheet

– Flow through to financials as mines continue to improve production with lower unit costs

– Midamines settlement and associated costs ($1.5m) and asset impairment ($4.9m)

• CONTOPS implemented in January 2012 at Saxendrift and Klipdam

• Net cash balances of $9.9M preserved to fund growth

• Investments positioned Rockwell to deliver further IMPROVEMENTS and pursue GROWTH OPPORTUNITIES

in fiscal 2013

FOCUS ON DIAMOND VALUE MANAGEMENT13

STRATEGIC REVIEW CATALYZED CORPORATE TURNAROUND

• STRATEGIC REVIEW initiated after management changes in December 2010

• To achieve key CORPORATE OBJECTIVE: increasing annual production of

high-quality gemstones to 120,000 carats in 5 yrs

• TURNAROUND commenced with appointment of new management team

in June 2011

– CEO + COO with >50 years joint diamond experience

– DIAMOND VALUE MANAGEMENT: Brought focus on quality and

embedding new work culture throughout operations

• Comprehensive OVERHAUL of business focused on

– Optimizing the productive mines to deliver better returns

– Driving down costs

– Improving metallurgical processes

– Focus on recovery of diamonds as part of diamond value management

• Next phase: LEVERAGE PRODUCTION PROFILE by developing asset

inventory + possible M&A opportunities

FOCUS ON DIAMOND VALUE MANAGEMENT14

PROGRESS ON STRATEGIC REVIEW

• Understanding of GEOLOGY found to be rigorous with NI 43 101 reports on all properties

• Production issues in plant environment addressed through increased focus on DIAMOND PROCESSING

METALLURGY

• SAXENDRIFT: Completion of new FIT FOR PURPOSE in field screen and bulk x-ray pilot project

– ON SCHEDULE: Delivering positive recovery performance and results

– New process technologies: BLUEPRINT for future mine development

• KLIPDAM: Economics for remaining LOM improved

– Mine plan adjusted to Rooikoppie with less intense earthmoving requirements

• TIRISANO: Ramp up in progress

– Short term impact on profitability: $6.7m = Full operating and ramp up costs expensed

• HOLPAN: Put on care and maintenance in May 2011

– Was delivering marginal results and reaching end of LOM

– Options to bring this asset to account under consideration

FOCUS ON DIAMOND VALUE MANAGEMENT15

CORPORATE LEGACY ISSUES RESOLVED

• RECAPITALIZATION in Q3: Private placement raised $7.8m + $6.5m from sales of non-core and underutilized assets

– Partly deployed: Implement technology improvements at Saxendrift and complete Tirisano plant

– Solid business case to underpin all further use of funds

• RESOLUTION of Midamines dispute: Final settlement of $1.2m paid

– Company is not aware of any other outstanding litigation

• FINALIZATION of an agreement with AVR: Effectively unwinds 2008 BEE deal (Northern Cape operations)

– Included acquisition of AVR’s Jasper Mine: contiguous to Saxendrift Mine with potential to extend LOM

– In negotiations to introduce other BEE groupings

• STRENGTHENED Board of Directors:

– Chairman: Mark Bristow

– Non-executives + audit committee: Johan van ‘t Hof and Stephen Dietrich

• In depth analysis of ASSET REGISTER to ensure accurate reflection of assets in balance sheet

– $4.9m impairment of property, plant and equipment

FOCUS ON DIAMOND VALUE MANAGEMENT16

DIAMOND VALUE MANAGEMENT: TANGIBLE BENEFITS IN Q4

• SAXENDRIFT: 42% increase in rough diamond sales to US$17.5m with 32% increase in carats sold

– 50% increase in carats produced and 5% drop in unit cost

• TIRISANO: Ramp up in progress with revenue of US$0.5m

– Good progress with wet front end

• STRATEGIC DECISIONS: Holpan mine on care and maintenance and trial mining at Klipdam Extension ceased

• Cost per carat DOWN 6%: Total mining costs down 3%

– Despite impact of Tirisano and upward pressure due to fuel, wages and maintenance costs

• CASH POSITIVE with net cash of $9.9m: After funding capex of $4.0m

Production Sales and inventories

Value of Sales Average value

Volume (m3) Carats Mining costs Sales (carats) Inventories (carats)

(US$) (US$ / carat)

Fourth quarter

661,627 4,043 10,370,000 6,030,376 5,795 1,041 114

fiscal 2012

FOCUS ON DIAMOND VALUE MANAGEMENT17

TECHNOLOGY PROJECTS AT SAXENDRIFT: IN FIELD SCREEN

• CHALLENGE:

– High sand content in gravel and productivity

impact when processing wet gravels

• SOLUTION:

– 3.0m x 8.0m Dabmar Bivitec screen

commissioned in November 2011

– Designed to treat sandy and wet gravels at

required processing rates

• IMPACT:

– Running at > 95% efficiency and operating at

17% above design throughput

– Monthly volumes up 30% (incl. impact of contops

and increased bottom cut off)

FOCUS ON DIAMOND VALUE MANAGEMENT18

TECHNOLOGY PROJECTS AT SAXENDRIFT: BULK X-RAY

• CHALLENGE:

– Low efficiencies in traditional pan plants and final

recovery

• SOLUTION:

– High throughput Bourevestnik (BV) sorter and

one BV single particle sorter to improve

concentrate efficiency and final sorting of

diamond bearing ore (capex $1.5m)

• IMPACT:

– Recovery in first 4 weeks: 316 stones = 1,109

carats have been recovered

– 14 stones >10 carats with largest weighing 76.4

carats

FOCUS ON DIAMOND VALUE MANAGEMENT19

TECHNOLOGY PROJECTS AT TIRISANO: WET FRONT END

• CHALLENGE:

– Current dry front-end cannot

deal with wet, clay rich

gravels

• SOLUTION:

– High water volume monitoring

and screening plant

(capex $200k)

• IMPACT:

– Currently being production

commissioned

FOCUS ON DIAMOND VALUE MANAGEMENT$m

0

2

4

6

8

10

12

14

16

18

20

Opening cash and

cash equivalents

Cash Generated

by Operations

Net changes in

working capital

Proceeds of

Private Placement

Proceeds of

convertible bond

Proceeds from

sale of assets

Capex: Tirisano, Saxendrift and

purchase of mineral property

interests

Movement in

ACHIEVE SHORT TO MEDIUM TERM OBJECTIVES

reclamation deposits

CASHFLOW: INVESTING IN CAPACITY FOR GROWTH

BALANCE SHEET PROVIDES REQUIRED WORKING CAPITAL TO

Other cash flows

Closing cash and

cash equivalents

FOCUS ON DIAMOND VALUE MANAGEMENT

20CORRELATION: RESOURCES TO PRODUCTION

1.5

1.4 Klipdam Recovered Grade vs. Resource Grade

1.3

Grade ct/100m³

1.2

1.1

1.0

0.9

0.8

0.7

Mine Grade 43101 Grade Budget Grade

0.6

0.5

Q3 2009

Q4 2009

Q1 2007

Q2 2007

Q3 2007

Q4 2007

Q1 2008

Q2 2008

Q3 2008

Q4 2008

Q1 2009

Q2 2009

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Q3 2011

Q4 2011

3.0

Saxendrift Recovered Grade vs. Resource Grade

2.5

Mine Grade 43101 Grade Budget Grade Linear (Mine Grade)

Grade ct/100 m³

2.0

1.5

1.0

0.5

0.0

Jul 09

Jul 10

Jul 11

Apr 09

Apr 10

Apr 11

Apr 12

Aug 08

Jan 10

Jan 11

Jan 12

May 08

Nov 08

Oct 09

Oct 10

Oct 11

FOCUS ON DIAMOND VALUE MANAGEMENT22

INDEPENDENT VALUATION: CONFIRMED VALUATION GAP

Weighted market value estimate:

Adjusted book value / Fair Market Value of Properties

$62m

using discounted cashflow 70

Saxendrift

60

($15.5m -

$16.1m) Adjusted book value method

Wouterspan Guideline public company method

($47.4m - 50

Trading price method

$54.8m)

40

40%

Niewejaarskra

al ($37.4m - 30

$42.5m)

20

30%

Holpan Tirisano 10

($281,000) Klipdam ($17.6m -

($3.6m) 30%

$20.0m)

0

Resource properties: $121.9m - $137.3m

Adjusted book value: $149.5m - $165.0m

Additional details contained in “Additional Information”

FOCUS ON DIAMOND VALUE MANAGEMENT23

PEER GROUP REVIEW OF DIAMOND JUNIORS:

FURTHER CONFIRMATION OF ROCKWELL’S VALUE UPSIDE

Average price/carat sold (US$) Price: Tangible Book Value

1200 7

6

1000

5

800

4

600

3

400

2

200

1

0

0

Diamond- Firestone Lucara Mountain Namakwa Rockwell Stellar Trans Hex

corp Province Diamonds Diamond- Firestone Lucara Mountain Namakwa Rockwell Stellar Trans Hex

corp Province Diamonds

Enterprise value ($m) Market Cap: Resource value

$500 12%

$400 10%

$300 8%

$200 6%

$100 4%

$- 2%

Diamond- Firestone Lucara Mountain Namakwa Rockwell Stellar Trans Hex 0%

$(100) corp Province Diamonds

Diamond- Firestone Lucara Mountain Namakwa Rockwell Stellar Trans Hex

corp Province Diamonds

Source: Company websites, ThomsonReuters

FOCUS ON DIAMOND VALUE MANAGEMENTWAY FORWARD

25

OPERATIONAL TARGETS FOR FISCAL 2013

CASH OPERATING

PRODUCTION GRADE COST/m3 CAPITAL REVENUE/CARAT

MINE

(m3) (carats/100m3) EXPENDITURE (US$)

BUDGET F2012

At name plate In line with F2012

KLIPDAM Stable $7.32* $10.72 Minimal

capacity (90 000) YTD

Increase to 150

In line with two

SAXENDRIFT 000 with new in- Stable $8.42 $8.27 $400,000

year average

field screen

Ramping up to Gradual

In line with stated

TIRISANO 90,000m3 p.m. improvement to $10.38** $20.11 $750,000

prices of $700

06/2012 1.8 by 06/12

- ZAR/CAD exchange rate of 8.00 - Full implementation of contops at all operations for F2013

- Corporate expenses budgeted to remain stable

- Beneficiation (stones > 2.8 carats) not included in average price per carat expectation

* Change of mining plan ** Ramp-up

FOCUS ON DIAMOND VALUE MANAGEMENT26

GROWTH PLAN: CREATE CRITICAL MASS AND SCALE

Further upside potential from Jasper Mine

Reviewing additional capital requirement to fund expansion with preference for internal cash flows

140,000 1,000,000

120,000 Production targets

800,000

Volume / month (m3)

Total carats / year

100,000

80,000 600,000

60,000 400,000

40,000

200,000

20,000

- -

F2012A F2013 F2014 F2015 F2016 F2017 F2018

Niewejaarskraal Wouterspan Tirisano Klipdam Saxendrift Other Total Production / month

300,000,000

Revenue targets *

250,000,000

Revenue / year ($m)

200,000,000

150,000,000

100,000,000

50,000,000

0

F2012A F2013 F2014 F2015 F2016 F2017 F2018

Other Niewejaarskraal Wouterspan Tirisano Klipdam Saxendrift

Projected production based on mine plans in November 2010 preliminary assessments (Tirisano,

Wouterspan and Niewejaarskraal) and prefeasibility study (Saxendrift). Refer to Saxendrift resource

statement on www.rockwelldiamonds.com

* Based on budgeted carat values for 2013 and 2.5% annual price increases

FOCUS ON DIAMOND VALUE MANAGEMENT27

REVIEW OF INVESTMENT OPTIONS: VALUE CREATION POTENTIAL

NPV / Capital Expenditure (times) Rockwell Diamonds Inc Capital Development

(Bubble Size = Capital Requirement)

12 R 900 Niewejaarskraal

R 800

10 Wouterspan

R 700

NPV (ZAR millions)

8 R 600 Saxendrift

Extension IFS

R 500 Only

Tirisano

6 Expansion

R 400

4 R 300

Saxendrift

R 200 Extension

2 Complete Plant

R 100

0 R0

Wouterspan Niewejaarskraal Saxendrift Tirisano 0 50 100 150

Extension Expansion

Resource Size m (millions)

3

Projected production based on mine plans in November 2010 preliminary assessments (Tirisano,

Wouterspan and Niewejaarskraal) and prefeasibility study (Saxendrift). Refer to Saxendrift resource

statement on www.rockwell diamonds.com.

FOCUS ON DIAMOND VALUE MANAGEMENT28

STRONG FUNDAMENTALS FOR DIAMOND SECTOR

• Diamond DEMAND in carats forecast to grow at 6% p.a. to 2020 ROCKWELL PRODUCTION PROFILE BIASED

TOWARDS LARGE STONES

– OUTPACING annual SUPPLY growth of 2.8%

100%

– CHINESE and INDIAN MIDDLE CLASS to double by 2020 % of carats exceeding 2 cts

90%

% of revenue exceeding 2cts

• ECONOMIC UNCERTAINTY currently impacting sentiment in diamond market 80%

– Industry OVERSTOCKED with expensive rough diamonds 70%

– Resulting in pricing slowdown, especially for smaller stones 60%

• Growing SCARCITY of +2CT diamonds 50%

– Globally: Currently represents 5% of diamond PRODUCTION and 50% 40%

of sales VALUE for producers 30%

20%

10%

0%

Saxendrift Klipdam Tirisano

• ROCKWELL PRICING against current market

– SMALLER STONES: Reduction of ±20%

– >2 CARATS : Stable pricing

– LARGE SPECIALS: Strong demand

FOCUS ON DIAMOND VALUE MANAGEMENT29

PRIORITIES AND OUTLOOK: FISCAL 2013

PRIORITIES: CEMENT TURNAROUND PROGRESS OUTLOOK: POSITIVE LONG TERM FUNDAMENTAL

• KLIPDAM: Achieve volume targets and improve lower • INCREASING DEMAND from China and India and

unit costs under leadership of new Mine Manager reducing supply

• SAXENDRIFT: Optimize mine plan + continue optimizing • Prices and demand expected to continue

in field screen INCREASING

• TIRISANO: Ramp up to full production + complete wet • Rockwell’s BALANCE SHEET provides working

front end + improve availability of earthmoving fleet capital for short to medium term plans

• BEE: Complete process to introduce new partner and • Ongoing review of potential corporate actions for

secure funding GROWTH

• CORPORATE: Deploy bulk X-ray technology at • Continue adding value through BENEFICIATION joint

Saxendrift for bulk sampling and other projects venture with Steinmetz

• GROWTH: Planning and feasibility of Wouterspan using • Deliver on OPERATIONAL PRIORITIES to start

new technology blueprint seeing financial benefits

FOCUS ON DIAMOND VALUE MANAGEMENT30

FORWARD LOOKING STATEMENTS

Except for statements of historical fact, this presentation release contains certain "forward-looking information" within the meaning of applicable securities law. Forward-

looking information is frequently characterized by words such as "plan", "expect", "project", "intend", "believe", "anticipate", "estimate" and other similar words, or

statements that certain events or conditions "may" or "will" occur. Although the Company believes the expectations expressed in such forward-looking statements are

based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the

forward-looking statements.

Factors that could cause actual results to differ materially from those in forward-looking statements include uncertainties and costs related to exploration and

development activities, such as those related to determining whether mineral resources exist on a property; uncertainties related to expected production rates, timing of

production and cash and total costs of production and milling; uncertainties related to the ability to obtain necessary licenses, permits, electricity, surface rights and title

for development projects; operating and technical difficulties in connection with mining development activities; uncertainties related to the accuracy of our mineral

resource estimates and our estimates of future production and future cash and total costs of production and diminishing quantities or grades if mineral resources;

uncertainties related to unexpected judicial or regulatory procedures or changes in, and the effects of, the laws, regulations and government policies affecting our mining

operations; changes in general economic conditions, the financial markets and the demand and market price for mineral commodities such and diesel fuel, steel,

concrete, electricity, and other forms of energy, mining equipment, and fluctuations in exchange rates, particularly with respect to the value of the US dollar, Canadian

dollar and South African Rand; changes in accounting policies and methods that we use to report our financial condition, including uncertainties associated with critical

accounting assumptions and estimates; environmental issues and liabilities associated with mining and processing; geopolitical uncertainty and political and economic

instability in countries in which we operate; and labour strikes, work stoppages, or other interruptions to, or difficulties in, the employment of labour in markets in which we

operate our mines, or environmental hazards, industrial accidents or other events or occurrences, including third party interference that interrupt operation of our mines or

development projects.

For further information on Rockwell, Investors should review Rockwell's annual Form 20-F filing with the United States Securities and Exchange Commission

www.sec.com and the Company's home jurisdiction filings that are available at www.sedar.com.

This presentation also uses the terms 'indicated resources' and 'inferred resources'. Rockwell Diamonds Inc. advises investors that although these terms are recognized

and required by Canadian regulations (under National Instrument 43-101 Standards of Disclosure for Mineral Projects), the U.S. Securities and Exchange Commission

does not recognize them. Investors are cautioned not to assume that any part or all of the mineral deposits in these categories will ever be converted into reserves. In

addition, 'inferred resources' have a great amount of uncertainty as to their existence, and economic and legal feasibility. It cannot be assumed that all or any part of an

Inferred Mineral Resource will ever be upgraded to a higher category. Under Canadian rules, estimates of Inferred Mineral Resources may not form the basis of feasibility

or pre-feasibility studies, or economic studies except for Preliminary Assessment as defined under 43-101. Investors are cautioned not to assume that part or all of an

inferred resource exists, or is economically or legally mineable.

The securities of Rockwell being offered have not been, nor will be, registered under the U.S. Securities Act and may not be offered or sold within the United States or to,

or for the account or benefit of, U.S. persons absent U.S. registration or an applicable exemption from U.S. registration requirements. This information does not constitute

an offer or sale of securities in the United States. Prior to making any investment decision, investors should consult a professional advisor.

FOCUS ON DIAMOND VALUE MANAGEMENTADDITIONAL INFORMATION

32

SUSTAINABLE DEVELOPMENT

• Supporting LOCAL ECONOMIC DEVELOPMENT

– LOCAL BENEFICIATION: 85% of diamonds in South Africa

– Provided STARTUP CAPITAL and mentorship for construction and brickmaking factory

• SAFETY: Committed to providing safe working environment

– ONE MILLION LTI FREE hour record at Saxendrift

• Employment: 683 full time employees

– Total of 79 new jobs created with conversion to CONTOPS in Northern Cape

• Corporate Social Investment

– Supporting LOCAL ORGANIZATIONS focused on under privileged children, education

and feeding schemes for elderly

• Managing ENVIRONMENTAL impact: REHABILITATION as

land is mined

FOCUS ON DIAMOND VALUE MANAGEMENT33

INDEPENDENT VALUATION1: CONFIRMED VALUATION GAP

1. The valuation, dated February 28, 2011, conducted by Jennifer Lucas, MBA, CBV, ASA,

Adjusted book value method of Evans & Evans Inc.

using discounted cashflow 1. Valuation of 74% of mine

2. Discount rates:

Operation Value range Wouterspan, Tirisano and Niewejaarskraal: 25.36% to 28.96%

Klipdam, Holpan and Saxendraft: 22.36% to 24.96%

Wouterspan3 $47.4m - $54.8m 4. Adjustments to balance sheet of Rockwell to evaluate fair value of net assets at

February 28, 2011

Tirisano3 $17.6m - $20.0m

Midpoint of fair

Fair Market Value2

Klipdam3 $3.6m Value Value

Valuation method market value Weighting Weighting

($m) ($m)

Holpan3 $281,000 ($m)

Trading price

Niewejaarskraal3 $37.4m - $42.5m 25.28 40% 10.11 40% 10.1

method5

Saxendrift3 $15.5m - $16.1m

Resource properties $121.9m - $137.3m Guideline public

15.80 30% 4.74 25% 3.95

Adjusted book value 4

$149.5m - $165.0m company method6

5. Valuation using average trading price of Rockwell for the

10 and 90 days preceding the valuation date Adjusted book

6. A guideline public company method comparing Rockwell’s 157.25 30% 47.18 35% 55.04

value method

average dollar value per enterprise

value of reserves and resources to eight peer group

companies Total 62.00 69.10

FOCUS ON DIAMOND VALUE MANAGEMENTYou can also read