Quarterly Global Outlook Q2 2019 It's All About Trade! - UOB

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Quarterly Global Outlook Q2 2019 It's All About Trade!

CONTENT

04

EXECUTIVE SUMMARY CHINA � 32

It's All About Trade!

HONG KONG � 33

10 INDIA � 34

FX, INTEREST RATE & COMMODITIES FORECASTS

INDONESIA � 35

11 JAPAN � 37

SINGAPORE FOCUS I

MAS April 2019 Preview: MALAYSIA � 38

Monetary Policy Is Likely To Stay Pat In April

MYANMAR � 39

14 PHILIPPINES � 40

SINGAPORE FOCUS II

Singapore Budget 2019: Mildly Expansionary SINGAPORE � 41

With A Focus On Social Measures

SOUTH KOREA � 42

15 TAIWAN � 43

CHINA FOCUS

Opportunities From Guangdong-Hong Kong-Macao THAILAND � 44

Greater Bay Area

VIETNAM � 45

23

FX STRATEGY AUSTRALIA � 46

USD Increasingly On Shaky Ground

As FED Signals End To Hiking Cycle EUROZONE � 47

NEW ZEALAND � 48

26

RATES STRATEGY UNITED KINGDOM � 49

A More Nuanced Path Ahead For Singapore Rates

UNITED STATES OF AMERICA � 50

28

COMMODITIES STRATEGY FX TECHNICALS � 51

Gold Is Best Poised To Strengthen

As FED Signals End To Hiking Cycle COMMODITIES TECHNICALS � 56

Information as of 22 March 2019

GlobalEcoMktResearch@UOBgroup.com

www.uob.com.sg/research

Bloomberg: UOBR

Scan the QR Code for a list of all our reports

EXECUTIVE SUMMARY

It's All About Trade!

China Leads Asian Export Contraction As US-China Trade War Drags On

Source: Bloomberg, UOB Global Economics & Markets Research

50

40

30

20

10

0

-10

-20

-30

Mar 16 Jul 16 Nov 16 Apr 17 Aug 17 Dec 17 May 18 Sep 18 Jan 19

Malaysia Export Growth Thailand Export Growth Taiwan Export Growth

South Korea Export Growth Singapore NODX Growth China Export Growth

Last March, exactly a year ago, US As China’s growth and activity slowed Finally, the global “synchronized”

President Donald Trump announced his down, Asia’s export contraction intensified. slowdown across China, Asia and Europe

plans to start imposing tariffs on Chinese Asian central banks (except the PBoC), appears to have started to boomerang

goods to reduce the ballooning US trade which had tightened monetary policy en- back to the US. Various macroeconomic

deficit with China, effectively triggering mass last year, are now forced to consider figures like retail sales, payrolls and PMI

the start of the US-China trade war. unwinding the untimely rate hikes. Going have turned more volatile for the US. The

By last August, both the US and China forward, we see Bangko Sentral ng US Federal Reserve’s (FED) has clearly

had imposed mutual tariffs on USD 50 Pilipinas (BSP), Bank Negara Malaysia turned dovish as they dropped the dot

bn of exports to each other. Since then, (BNM), Bank Indonesia (BI) and Reserve plot. In addition, the FED also guided that

President Trump’s threat on imposing a Bank of India (RBI) leading rate cuts they are looking to stop Balance Sheet

higher 25% tariffs (from the existing 10%) across Asia. The Monetary Authority of Reduction (BSR) by Sep this year. Bottom

on USD 200 bn block of Chinese exports Singapore (MAS) is also now seen staying line, we no longer expect any more rate

did not materialize, but damage is clearly on hold in April. hikes from the FED in this cycle.

done to global trade and growth.

Outside of China, Germany narrowly However, lest one gets overly pessimistic;

Needless to say, China bore the brunt of the escaped a technical recession in late 2018 it is worth noting that the trade contraction

export contraction as the US-China trade but Italy unfortunately did not escape that induced global growth moderation has

war exacerbated the on-going slowdown. outcome. The Eurozone is China’s largest clearly intensified. But it is important to

China conceded to a lower growth target trading partner and an accelerated growth note that this growth moderation is still

range of “about 6.0% to 6.5%” for this year, slowdown in China will weigh on Eurozone a far cry from the very severe global

compared to “around 6.5%” for last year. growth prospects. As such, the European recession during the 2008/09 Global

Alongside the downgrade in growth target, Central Bank (ECB) not only lowered its Financial Crisis.

China has also announced broad fiscal 2019 Eurozone growth forecast from

stimulus, including a larger-than-expected 1.7% to 1.1%, but also signaled that it

VAT cut, widening the budget deficit to will keep policy rate unchanged till early

2.8% of GDP (from 2.6% in 2018). From next year. To ease funding pains, the ECB

6.6% last year, we see China GDP growth announced yet a third tranche of Targeted

falling to 6.3% this year. Long Term Refinancing Operation (TLTRO

III).

Quarterly Global Outlook 2Q2019

04 UOB Global Economics & Markets Research EXECUTIVE SUMMARY

Rates Strategy Over the near term, the PHP, IDR and Singapore Focus I

A More Nuanced Path Ahead INR are still at risk alongside the CNY and MAS April 2019 Preview:

For Singapore Rates KRW. While the MYR, THB and TWD can Monetary Policy Is Likely

Given that we no longer see any more FED count more on their strong current account To Stay Pat In April

rate hikes going forward, Fed Fund Rates surpluses. Meanwhile, the expected MAS We expect the MAS to keep monetary

will top out at 2.5% in this cycle. As such, April pause supports our view of mild policy parameters unchanged in their

3M US Libor is seen hovering around SGD weakness. Finally, VND is the outlier upcoming April 2019 meeting. This means

current level of 2.65% until end 2019. whose outlook has clearly improved. USD/ keeping the appreciation slope, width

VND spot appears to be stabilizing around and center unchanged. We view current

Needless to say, the impact of US Libor 23,200 as Vietnam is positioned to benefit monetary policy to be appropriate despite

on local rates will be lesser now that the from the manufacturing capital outflow recent economic softness, given that core

FED’s hiking cycle is coming to an end. away from China. inflation pressures will likely persist into

Particularly for Singapore, the currency 2H19. We view core inflation to cross its

factor, as well as domestic funding _________________________________ 2.0% handle as early as July 2019.

dynamics now comes into play to better

support SG rates. Overall, we see both 3M Commodities Strategy _________________________________

SOR and Sibor continuing their gradual Gold Is Best Poised To Strengthen

rise from around 1.95% now to 2.10% by As FED Signals Singapore Focus II

end 2019. End To Hiking Cyclee Singapore Budget 2019:

Amongst the major commodities, we Mildly Expansionary With

_________________________________ believe that gold is set to rally further as we A Focus On Social Measures

reach the end of the FED’s current hiking We observe that the budget is mildly

FX Strategy cycle. In addition, the return of net long expansionary with a focus on social

USD Increasingly On Shaky Ground position and possible renewed allocation measures. Into FY2019, Singapore’s

As FED Signals End To Hiking Cycle of China’s reserves into gold are further overall budget balance is projected to see

In the previous quarterly report, we warned positive drivers. Overall, we turn positive a deficit of $3.5 billion, or 0.7% of GDP.

that cracks have started to appear in the on gold from neutral and now expect gold Ministries’ total expenditures are expected

strong USD amour. The latest dovish to rally further from USD 1,300 / oz now to to be 1.6% higher at $80.3 billion, while

FOMC has cemented this turn in USD rise towards the USD 1,450 / oz level by operating revenue is estimated at $74.9bn

lower. However, this retreat in the USD is the end of the year. (+1.7% higher vs FY2018). We view

not expected to be a straight line down, but the budget’s thrusts and social policies

may be a choppy affair. With regards to Brent crude oil, the on- continue to suggest the government’s

going disciplined supply cut from OPEC pre-emptive nature in addressing long-

Specifically, because of growth and Russia is able to help offset concerns term challenges of ageing, social mobility,

moderation, expectations for rate hikes of global growth slowdown. The further inequality, economic transformation,

for both the ECB and RBA have now loss of production in Iran and Venezuela and climate change, while reinforcing its

been pushed back from late 2019 to next is also another supportive factor. role as a market-enabler in supporting

year in 2020. As such, while we remain Consequently, Brent is likely to drift higher Singapore’s business environment.

confident that both the EUR and AUD are towards the top end of its USD 65 to 75 /

in the process of bottoming, we have to bbl trading range as well as maintain its _________________________________

acknowledge the weaker growth outlook mild backwardation.

will limit the immediate gains in the EUR China Focus

and AUD. As for LME Copper, given the increasing Opportunities From Guangdong-

global moderation in growth, it is Hong Kong-Macao

In Asia, central banks are now seen premature to expect further strength. Greater Bay Area

paring back some of the untimely rate In fact, recent Copper strength in 1Q19 On 18 February 2019, China unveiled

hikes from last year, as further export may not be sustainable given slowdown the outline plan for the Guangdong-Hong

contraction, growth slowdown and weaker in PMI as well as export contraction. The Kong-Macao Greater Bay Area (GBA) to

inflation trajectory start to bite. As such, prevailing cash premium may also be a be developed into a vibrant world-class

Asian currencies are not yet able to take temporary side effect of China’s tightening cluster and amongst others, a globally

advantage of the tapering off of FED rate of scrap import requirements. Industrial influential international innovation and

hikes. Furthermore, investors are likely to demand for copper may also ease in the technology hub.

remain cautious and stay sidelined ahead near term due to downward pressure on

of the key elections in Thailand, Indonesia the electronics and automobile sectors. Physical connectivity is enhanced with the

and India. In short, it will still take some Thus, we maintain our existing neutral opening of the 55 km Hong Kong-Zhuhai-

time before Asian currencies benefit from forecast of LME Copper for USD 6,000 to Macao Bridge (HZMB) in October 2018 and

the dovish FED and turn higher. 7,000 / MT. the final 26 km phase Hong Kong section

of the Guangzhou-Shenzhen-Hong Kong

Hereafter is a brief synopsis of key Focus Express Rail Link (XRL) in September

pieces as well as key FX and Rates views. 2018. Further projects completion will

Quarterly Global Outlook 2Q2019

EXECUTIVE SUMMARY UOB Global Economics & Markets Research 05

facilitate people, goods, services, capital still expected to hike rates next year. Also, come to a successful trade agreement.

and information flows. in the context of a Euro-area slowdown However, in view of the negative economic

(rather than a recession) one may find it fundamentals, we prefer to stay cautious

The economies of Guangdong, Hong hard to argue for a crisis-era EUR/USD on the CNY until we can assess the merits

Kong and Macao are significantly different below 1.10. Market-based indicators of the upcoming US-China trade deal.

from one another and this allows value to such as the interest rate differentials and For now, we maintain our USD/CNY point

be created by leveraging on their diverse risk reversals continue to point to further forecasts for 6.70 in 2Q19, 6.75 in 3Q19

strengths. In addition, the generally more stabilization in EUR/USD. Overall, we stay and 6.80 in 4Q19 and 1Q20.

mature economies of Hong Kong and positive on EUR/USD with point forecasts

Macao will set as benchmarks but also at 1.15 in 2Q19 and 3Q19, 1.18 in 4Q19, USD/SGD: Since the last policy meeting

stand to gain from faster growth rate of its and 1.20 in 1Q20. EUR/USD remains our last October, the S$NEER continued

mainland peers in the combined entity of conviction trade in the G-10 space. to persist within the stronger half of the

GBA. policy band, averaging +1.5% above the

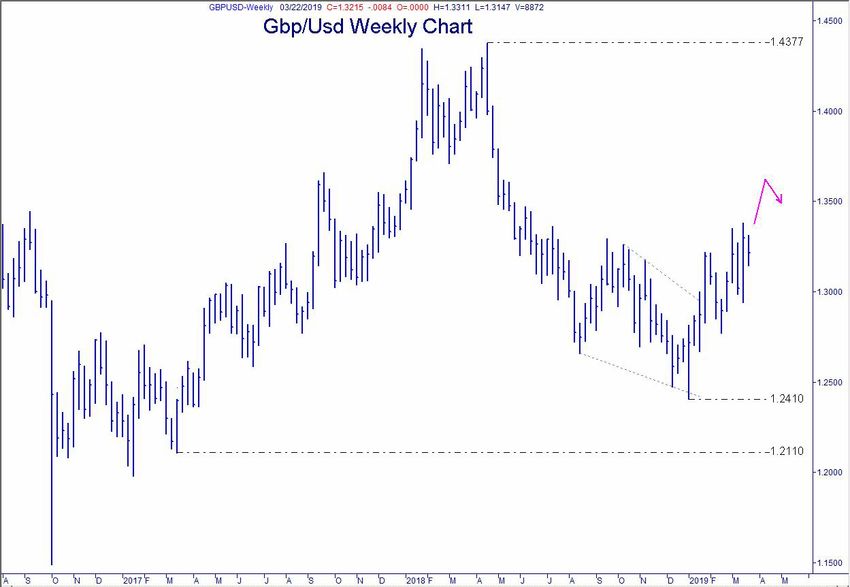

GBP/USD: Even with an immediate policy midpoint, in part due to markets’

Comparing to other “Bay Areas” around cliff-edge Brexit is averted on 29-Mar, it expectations of further tightening from

the world, there is much potential for GBA remains uncertain whether Theresa May MAS come April. So, if MAS stays on

given the specializations of various cities can get her deal approved within the hold this time round, this will limit further

within GBA and the tightened connectivity 2-week extension. GBP/USD is likely to S$NEER strength going forward. Overall,

will help to further synergize these cities’ stay volatile and sensitive to headlines. our expectation of MAS staying on hold

capabilities. Overall, we stay cautious on the GBP until in April reinforces the existing higher

the uncertainty of the Brexit fog clears. trajectory in USD/SGD, in line with

As the GBA will remain at the planning In terms of point forecasts, we see GBP/ gradual CNY weakness as well. However,

stage in the immediate period with USD at 1.28 in 2Q19, 1.30 in 3Q19, 1.30 with latest dovishness from the FED, we

focus on improving integration, there in 4Q19 and 1.32 in 1Q20. moderate the point forecasts lower, now

will be substantial leeway given to local expecting USD/SGD to finish the year at

governments over how they will pursue AUD/USD: The AUD/USD was resilient 1.37 from 1.38 previously.

these goals. We think the vague targets in 1Q19 – having snapped back from a

are in recognition of the challenges in “flash crash” in early January and endured USD/HKD: Once again, the HKD has

integrating the region which covers three a dramatic shift in RBA from hawkish to fallen to the weak side convertibility limit of

different customs, legal systems and neutral in February. Going forward, we 7.85 against the USD. As of early March,

currencies. reiterate a higher trajectory in AUD/USD. the HKMA has resumed intervention yet

A dovish Fed lightens the pressure on again to limit HKD weakness at 7.85. It is

_________________________________ the AUD/USD as the wide interest rate likely that the HKMA will need to continue

differential between Australia and US its intervention and drive 3M HKD Hibor

GLOBAL FX may start to abate or even reverse. The higher. Overall, we can expect USD/HKD

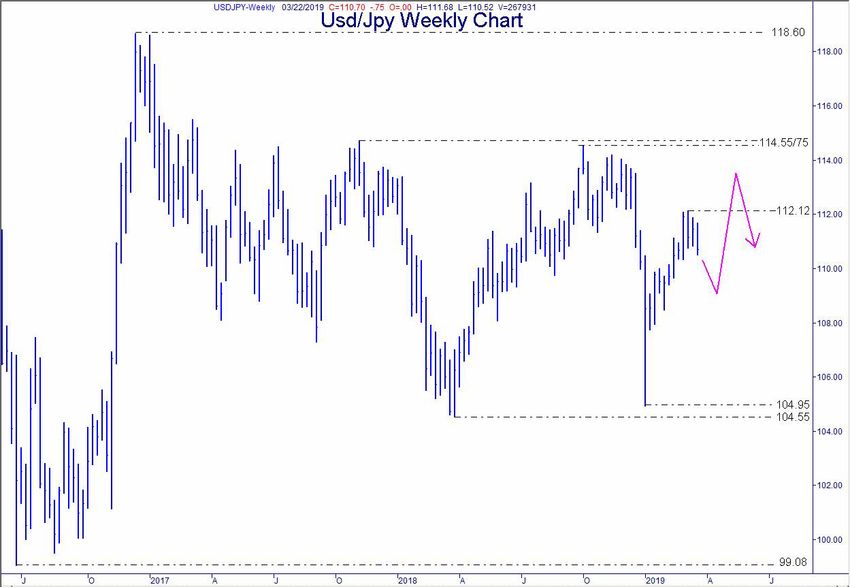

USD/JPY: With an overall more risk- key positive trigger for further upside in to drift back down towards 7.80 once the

conducive environment spurred by the AUD/USD remains that of a US-China Libor-Hibor gap has narrowed sufficiently.

positive momentum behind US-China trade agreement which looks increasingly Our point forecasts for USD/HKD are 7.85

trade talks and a very “patient” Fed, USD/ likely in 2H19 in our view. Our point in 2Q19, and 7.80 in 3Q19, 4Q19 and

JPY has recovered over 6% from the forecasts are now at 0.72 in 2Q19, 0.72 1Q20.

lows of 104.87 during its “flash crash” in 3Q19, 0.73 in 4Q19, and 0.74 in 1Q20.

in early Jan. A potential US-China trade USD/TWD: The TWD has been very

agreement in 2Q19 could bolster risk- NZD/USD: Going forward, we expect the stable in 2019. Year-to-date, USD/TWD

taking sentiments further, taking USD/ up move in NZD/USD to continue. The has been confined in a narrow 20 pips

JPY above 112. Domestically, amidst a latest dovish shift in Fed would likely be range between 30.70 and 30.90 against

weak growth coupled with low inflation a tailwind for the currency pair, supporting the USD. Going forward, with subdued

outlook, it is likely the BOJ will reassert NZD higher. We reiterate our previous set domestic inflation and weaker growth

its dovish monetary policy bias across of forecasts and expect NZD/USD at 0.69 outlook, we factor in mild weakness of

2019. Even as the Fed has signaled a in 2Q19, 0.70 in 3Q19, 0.71 in 4Q19, and TWD against the USD. Our point forecasts

potential end to the current hiking cycle, 0.72 in 1Q20. are now at 31.00 in 2Q19, 31.20 in 3Q19,

the still wide rate differential between US and 31.30 in both 4Q19 and 1Q20.

and Japan (255bps in the 10-year) would

likely be supportive for USD/JPY. Taken ASIAN FX USD/KRW: A peaking in the global

together, we reiterate our gradual upwards USD/CNY: By now it is abundantly clear electronics cycle has taken its toll on

trajectory in USD/JPY. that the economic slowdown in China the KRW. Year-to-date, the KRW is the

has intensified. However, the CNY had weakest Asian currency and has dropped

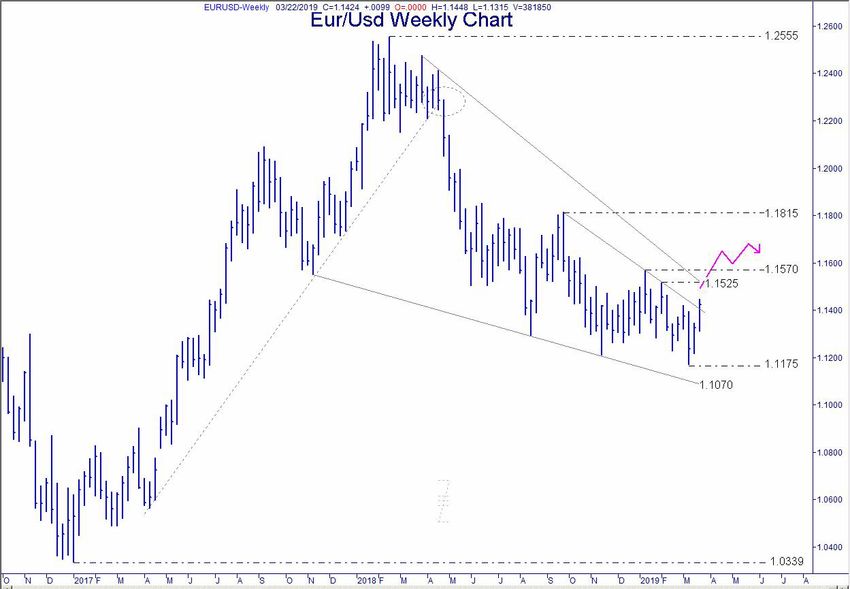

EUR/USD: The FED has handed the in fact strengthened across 1Q19. This 1% against the USD, at 1,125 per USD.

monetary policy baton to the ECB as the contrarian strength in the CNY might The lack of progress in the second US-

FED has probably reached its peak in the be due to positive expectations that North Korea Summit in late February

current interest rate cycle while the ECB is the US-China trade talks will eventually was also a dampener on sentiments.

Quarterly Global Outlook 2Q2019

06 UOB Global Economics & Markets Research EXECUTIVE SUMMARY

In addition, the KRW is not expected against further THB strength, which may think INR may face pressure from further

to receive any near-term support from dent Thai export competitiveness. Officials rate cuts from RBI, higher oil prices and

the BOK, which is likely to stay on hold are also likely to defer any potential rate uncertainties from the upcoming elections,

throughout 2019. If anything, markets see hike to 3Q, to allow for more time for the though part of the expected weakness is

a growing case of a rate cut although BOK economy to adjust to the uncertain trade offset by a dovish Fed. As such, we expect

has pushed back against that. In view of outlook. Overall, we still reiterate our INR to pare some of its recent gains. Our

moderating domestic fundamentals, we modestly higher view of USD/THB. Our point forecasts are now at 68.80 in 2Q19,

still maintain our view for a higher USD/ point forecasts for USD/THB are 31.80 by 69.20 in 3Q19, and 69.50 in both 4Q19

KRW for the next few quarters but the end-2Q19, 31.90 by end-3Q19, and 32.00 and 1Q20.

trajectory is now shallower than before as for end-4Q and 1Q20.

the Fed has signaled the end of its rate _________________________________

hike cycle. The USD/KRW point forecasts USD/PHP: Given that the central bank is

are now at 1,130 in 2Q19, 1,140 in 3Q19, likely to focus on stimulating economic GLOBAL INTEREST RATES

and 1,145 in both 4Q19 and 1Q20. growth, we expect as much as 50bps of FOMC: The FOMC kept its policy Fed

rate cut, in the next two quarters (25bp Funds Target Rate (FFTR) unchanged at

USD/MYR: We keep to the view of a firmer each in 2Q and 3Q). As such, the rate cuts, the 2.25%-2.50% range in Mar (2019), as

USD/MYR but adjust our USD/MYR point together with the persistent twin deficits widely expected but the big surprise was

forecasts lower to 4.06 in 2Q19, 4.08 are likely put pressure on the PHP. We that the updated Mar 2019 dot-plot chart

in 3Q19, and 4.11 in 4Q19 and 1Q20 update our view of a higher USD/PHP to showed a dramatically lowered rate hike

(Previous point forecasts were 4.10, 4.15 53.0 in 2Q19, 53.5 in 3Q19 and 4Q19 and trajectory which indicates that the Fed

and 4.18 respectively). Prevailing spot 54.0 in 1Q20. Prevailing spot reference will not hike rates in 2019 (from 2 hikes

reference rate is 4.06. This takes into rate is 52.8. previously) and the Fed also announced

consideration the strong start for Asian its intention to taper its balance sheet

FX to date, potential upside if a US-China USD/VND: Despite positive momentum in reduction (BSR) program from May 2019

deal is struck, and domestic support US-China trade talks in the 1Q19, the VND and to conclude the BSR at the end of Sep

factors including current account surplus did not track other Asia FX gains against 2019. With the FOMC literally doubling

and stable flows. the USD. Instead, the USD/VND pair down on their patience approach, we have

remains in a small range around 23,200. revised our expectations and we now think

USD/IDR: Indonesia’s GDP has not Going forward, we still expect USD/VND to the Fed is done with the current rate hike

recovered on a sustainable basis. Amidst track other USD/Asians higher. However, cycle, i.e. no more hikes in 2019. And with

the increasing external sector uncertainty the weakness in the VND is likely to a mild US technical recession potentially

from the US-China trade war, export be cushioned by Vietnam’s favorable rearing its head in 2020, we expect the

contraction has resumed and current macroeconomic performance. This is Fed to CUT policy rate by a nominal 25bps

account deficit has widened yet again. As especially so when Vietnam is expected in 3Q 2020 and will leave the door open to

such, we see renewed rate cuts from BI, to be a key beneficiary of manufacturing do more if the slowdown is exacerbated.

effectively unwinding some of rate hikes capital reallocation away from China. A major caveat to this projection is that

from last year’s cycle. Renewed rate cuts As such we reiterate a modestly higher US inflation stays in check (around 2%)

from BI will reduce the yield support for USD/VND trajectory, with point forecasts despite robust wage growth since Oct

the IDR. As Indonesia has both a fiscal at 23,300 in 2Q19, 23,400 in 3Q19, and 2018.

and current account deficit, this will make 23,500 in 4Q19 and 1Q20.

the IDR vulnerable to renewed weakness. ECB: The ECB kept interest rates

However, the upcoming rate cuts may also USD/MMK: After a 18% depreciation unchanged at the March meeting, but

be viewed positively from the investment against the USD between last April and updated its forward guidance for a rate

community as being positive for growth, October, the MMK has since stabilized hike. It now expects its key interest rates

triggering renewed investor in-flows and largely consolidated in a 1,500 to “to remain at their present levels at least

thereby supporting the IDR. Overall, the 1,600 per USD range. Going forward, through the end of 2019”. We did expect

expected weakness in IDR is partially we still expect the MMK to remain under a delayed rate hike to be flagged in due

offset by a dovish Fed. As such, we pressure from a persistent current account course, but definitely was not expecting

reiterate a modestly higher trajectory for deficit which will widen from 5.3% of GDP the ECB to formally change the date

USD/IDR. Our point forecasts for USD/ in 2018 to 5.7% in 2019 and 5.9% in 2020. guidance as soon as the March meeting.

IDR are 14,100 for 2Q19, 14,200 for 3Q19 As such, USD/MMK is forecast to be at We were previously looking for the ECB

and 14,300 for 4Q19 and 1Q20. 1,530 in 2Q19, 1,540 in 3Q19, and 1,560 to hike rates later this year, but have now

in 4Q19 and 1Q20. pushed back our rate hike call, seeing no

USD/THB: A resilient Thai economy move earlier than 2Q next year.

amidst trade headwinds, strong current USD/INR: The INR has been on a roar in

account surplus together with the BoT March, gaining from 71.00 to 68.80 per BOE: Members of the BoE’s nine-strong

flagging further rate hikes added to USD currently, a strong 3% move in three MPC voted unanimously to leave rates

appreciation pressures on the THB in weeks. Strong net inflows in local bond and unchanged at 0.75% during the March

1Q19. Going forward, with exports growth stock markets contributed to the strong meeting. The asset purchase facility

moderating, authorities will be on the alert currency performance. Going forward, we remained steady at GBP435bn as well.

Quarterly Global Outlook 2Q2019

EXECUTIVE SUMMARY UOB Global Economics & Markets Research 07

The BoE has suggested rates could go BOJ may still need to do more “tweaks” account deficit, which is partly addressed

in either direction, given the varied Brexit to monetary policy to reassert its easy by keeping monetary policy stance not too

outcomes. If the British Parliament passes monetary policy position, just like what it loose.

Theresa May’s Brexit deal next week did in the July 2018 MPM.

and there is a short technical extension BOK: Despite lower-than-expected

to Article 50 to pass the necessary inflation, a rate cut does not appear

legislation, the BoE could resume its ASIAN INTEREST RATES imminent at this point unless the growth

tightening cycle soon as data suggests a PBoC: In line with policymakers’ target and employment outlook deviate

hike is appropriate. If Brexit continues to to boost bank lending to small/micro significantly to the downside from our

delay, a rate hike in the summer could be and private companies, we maintain our base case. The focus remains on using

likely. After all, the MPC raised rates last expectation that there could be another fiscal tools to drive the growth outcome

August, just eight months before Brexit. two reserve requirement ratio (RRR) rather than monetary policy. As such, we

If, however, there is a no deal, the BoE cuts this year, following the broad-based maintain our expectation that the BOK will

might have to cut rates as early as the next 100bps reduction in January and the 4 stay on hold throughout 2019.

meeting on 2 May. But until we get more “targeted” RRR cuts in 2018. The next

clarity, the BoE is likely to stay firmly on RRR reduction is likely to take place in BNM: The US Fed’s ultra-dovish tone in

the sidelines. early-2Q19 given soft economic data so the March FOMC statement, lends more

far. However, we see low probability of flexibility for BNM to consider easing

RBA: As widely expected, the RBA held a PBoC rate cut in the next 3-6 months rates in view of the external headwinds

its OCR at 1.50% in March. The RBA has given the proactive fiscal and monetary and weaker domestic sentiment. We are

reaffirmed its mounting concern over the policy measures in place so far. pencilling in a 25bps cut in the Overnight

consumption outlook as households are Policy Rate (OPR) to 3.00% this year.

besieged by falling property prices, weak MAS: While we expect the MAS to keep

income growth and high debt. Since the its policy parameters unchanged in their BOT: The Bank of Thailand (BOT) is

weak GDP results, financial markets are upcoming April 2019 meeting, we think expected to hike the policy rate from

pricing in a rate cut this year as a done- that an eventual tightening is still on the 1.75% to 2% in 2H 2019. A rate pause

deal. We still think that the most likely cards. Should our call for the MAS to would give the MPC more time to fully

scenario is still for an unchanged policy stay pat in April come to pass, a token assess the situation. There is no urgency

rate in 2019. tightening into October will likely occur to to tighten monetary policy aggressively,

address the rising price pressures, in line whilst inflationary pressure is modest.

RBNZ: The RBNZ kept the OCR steady with MAS “primary objective of promoting Current monetary conditions remain

at 1.75% in February. Unlike the previous medium term price stability”. accommodative and commensurate with

statement in November 2018, the latest the needs of the Thai economy.

accompanying press release included the RBI: In response to address the falling

line that “The direction of our next OCR inflation environment, RBI cut its BSP: Given the improving inflation

move could be up or down.” in its opening benchmark repo and reverse repo to outlook, moderate growth prospects,

paragraph. The concluding paragraph was 6.25% and 6.00% respectively in its Feb and a new BSP Governor who is seen

the same where “We will keep the OCR at MPC meeting. We expect inflation is likely as an advocate of growth, we expect the

an expansionary level for a considerable to stay benign and average 3.4% in 2019, central bank to unwind some of last year’s

period to contribute to maximising hovering above 4.0% in 4Q19. Still, this tightening as a pre-emptive move over

sustainable employment, and maintaining means that India’s inflation environment is the next few months. We project a total of

low and stable inflation.” We are retaining likely to remain sub-4.0% for the first nine 50bps cut in interest rate toward year-end,

our call for the RBNZ to be on hold at least months, thus likely prompting the central taking the overnight reverse repo rate to

until early 2020. bank to inject one more 25bps cut to its 4.25% by end of 2019.

repo and reverse repo rate into 2019, most

BOJ: Among the G10 central banks, BOJ likely in either June or August. SBV: The State Bank of Vietnam (SBV) is

continues to be the least likely to normalize expected to maintain refinancing rate at

its easy monetary policy anytime soon, BI: BI is likely to keep interest rate 6.25% until Jun 2020. At the current policy

and it remains premature for the BOJ to unchanged until Q3 2019. Afterwards, rate, the monetary policy stance remains

talk about normalizing/tapering its easing given stable inflation and a more stable conducive to the continuation of economic

program too, because Japan is still far IDR, we see room for BI to normalize growth. The strong growth eases pressure

away from its 2% inflation target. The its policy rate by a cumulative 50bps in on the SBV to add more stimuli to achieve

projected weaker growth environment and Q4 2019. Real interest rate has been 2019 growth target of 6.7%.

likelihood of downside price pressures in relatively high and by reducing slightly the

2019 adds further challenges to BOJ’s rate hikes done in 2018, we believe this

monetary policy. One persistent point growth-supporting gesture is a welcome

of contention that is unhelpful to BOJ’s development by the markets. That said

“fight” is the projected annual pace of we do not foresee a full unwinding of

JGB buying continues to be well below the 175bps hikes in the last cycle given

its official target of JPY80tn. We think the the ongoing concern over the current

Quarterly Global Outlook 2Q2019

08 UOB Global Economics & Markets Research EXECUTIVE SUMMARY

Real GDP Growth Trajectory

y/y% change 2018 2019F 2020F 1Q18 2Q18 3Q18 4Q18 1Q19F 2Q19F 3Q19F 4Q19F

China 6.6 6.3 6.3 6.8 6.7 6.5 6.4 6.4 6.3 6.3 6.3

Eurozone 1.8 1.3 1.4 2.4 2.1 1.6 1.1 1.1 1.2 1.3 1.4

Hong Kong 3.0 2.2 2.3 4.6 3.5 2.8 1.3 1.6 2.0 2.5 2.8

Indonesia 5.2 5.2 5.4 5.1 5.3 5.2 5.2 5.1 5.3 5.2 5.2

Japan 0.8 0.5 -0.8 1.3 1.5 0.1 0.3 0.3 0.3 1.7 0.0

Malaysia 4.7 4.6 4.7 5.4 4.5 4.4 4.7 4.5 4.6 4.8 4.6

Philippines 6.2 6.2 6.5 6.6 6.2 6.0 6.1 5.9 5.9 6.2 6.5

India 7.0 7.0 7.2 8.1 8.0 7.0 6.6 6.5 7.1 7.2 7.9

Singapore 3.4 2.5 2.0 4.7 4.2 2.4 1.9 1.5 2.2 2.9 3.4

South Korea 2.7 2.5 2.5 2.8 2.8 2.0 3.1 2.6 2.5 2.4 2.4

Taiwan 2.6 2.2 2.3 3.2 3.3 2.4 1.8 2.0 2.1 2.3 2.5

Thailand 4.1 3.8 4.0 5.0 4.7 3.2 3.7 3.5 3.8 3.9 3.9

US (q/q SAAR) 2.9 2.0 1.3 2.2 4.2 3.4 2.6 1.2 2.0 1.2 0.9

Note that India’s annual growth refers to its fiscal year print

Source: CEIC, UOB Global Economics & Markets Research

Quarterly Global Outlook 2Q2019

EXECUTIVE SUMMARY UOB Global Economics & Markets Research 09

FX, INTEREST RATE & COMMODITIES FORECASTS

FX 22 Mar 19 2Q19F 3Q19F 4Q19F 1Q20F RATES 22 Mar 19 2Q19F 3Q19F 4Q19F 1Q20F

USD/JPY 111 111 112 113 113 US Fed Funds Rate 2.50 2.50 2.50 2.50 2.50

EUR/USD 1.14 1.15 1.15 1.18 1.20 USD 3M LIBOR 2.61 2.65 2.65 2.65 2.65

GBP/USD 1.31 1.28 1.30 1.30 1.32 US 10Y Treasuries Yield 2.53 2.45 2.60 2.70 2.70

JPY Policy Rate -0.10 -0.10 -0.10 -0.10 -0.10

AUD/USD 0.71 0.72 0.72 0.73 0.74

EUR Refinancing Rate 0.00 0.00 0.00 0.00 0.00

NZD/USD 0.69 0.69 0.70 0.71 0.72

GBP Repo Rate 0.75 0.75 0.75 0.75 0.75

DXY 96.3 95.9 95.7 94.1 93.2

AUD Official Cash Rate 1.50 1.50 1.50 1.50 1.50

USD/CNY 6.70 6.70 6.75 6.80 6.80 NZD Official Cash Rate 1.75 1.75 1.75 1.75 1.75

USD/HKD 7.85 7.85 7.80 7.80 7.80

CNY 1Y Benchmark Lending 4.35 4.35 4.35 4.35 4.35

USD/TWD 30.81 31.00 31.20 31.30 31.30 HKD Base Rate 2.75 2.75 2.75 2.75 2.75

USD/KRW 1,130 1,130 1,140 1,145 1,145 TWD Official Discount Rate 1.38 1.38 1.38 1.38 1.38

USD/PHP 52.61 53.00 53.50 53.50 54.00 KRW Base Rate 1.75 1.75 1.75 1.75 1.75

PHP O/N Reverse Repo 4.75 4.50 4.25 4.25 4.25

USD/MYR 4.06 4.06 4.08 4.11 4.11

SGD 3M SIBOR 1.94 2.00 2.05 2.10 2.10

USD/IDR 14,158 14,100 14,200 14,300 14,300

SGD 3M SOR 1.94 2.00 2.05 2.10 2.10

USD/THB 31.73 31.80 31.90 32.00 32.00

SGD 10Y SGS 2.03 2.10 2.20 2.30 2.30

USD/MMK 1,515 1,530 1,540 1,560 1,560

MYR O/N Policy Rate 3.25 3.00 3.00 3.00 3.00

USD/VND 23,203 23,300 23,400 23,500 23,500

IDR 7D Reverse Repo 6.00 6.00 6.00 5.50 5.50

USD/INR 68.83 68.80 69.20 69.50 69.50

THB 1D Repo 1.75 1.75 2.00 2.00 2.00

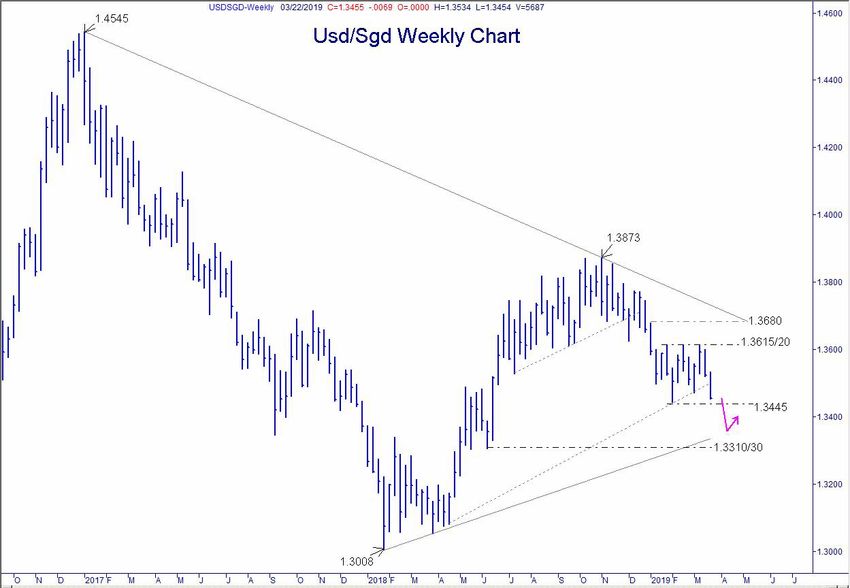

USD/SGD 1.35 1.35 1.36 1.37 1.37 VND Refinancing Rate 6.25 6.25 6.25 6.25 6.25

EUR/SGD 1.53 1.55 1.56 1.62 1.64 INR Repo Rate 6.25 6.25 6.00 6.00 6.00

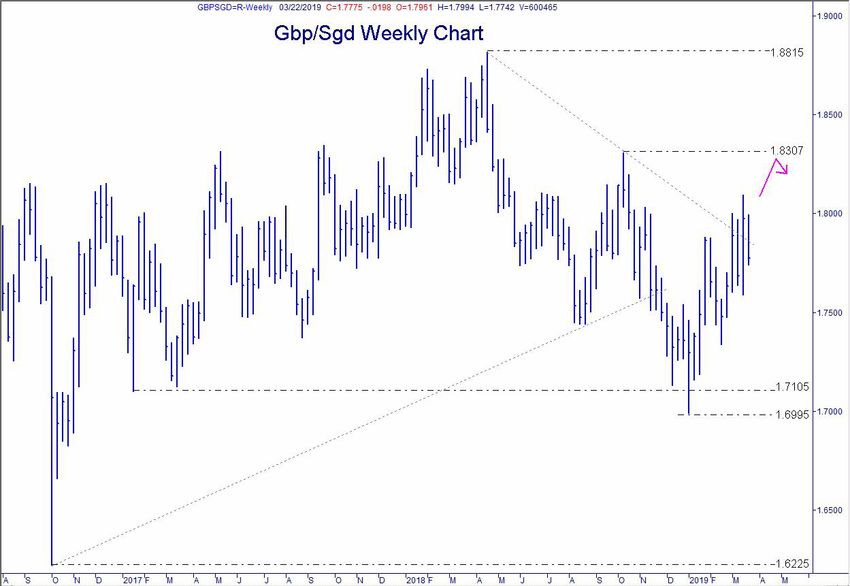

GBP/SGD 1.77 1.73 1.77 1.78 1.81

COMMODITIES 22 Mar 19 2Q19F 3Q19F 4Q19F 1Q20F

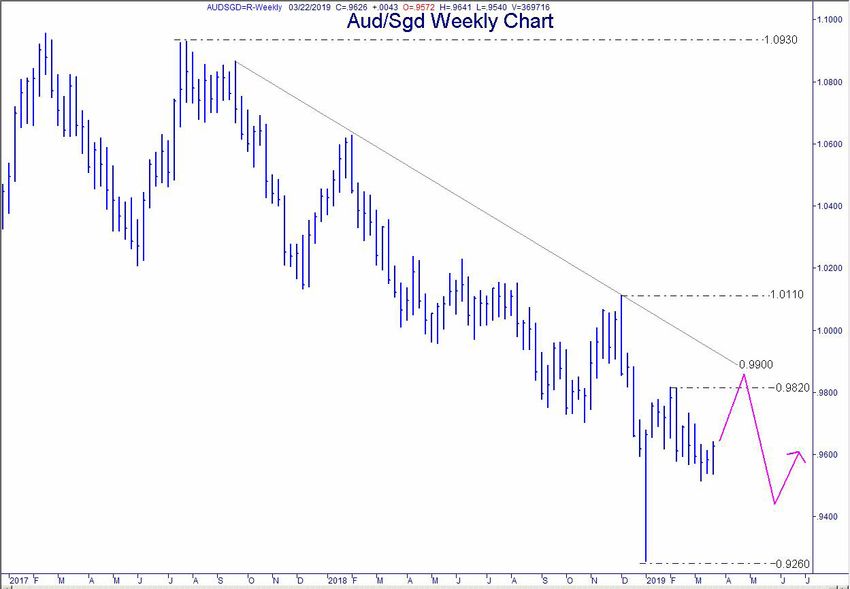

AUD/SGD 0.96 0.97 0.98 1.00 1.01

Gold (USD/oz) 1,310 1,350 1,380 1,400 1,450

SGD/MYR 3.01 3.01 3.00 3.00 3.00

Brent Crude Oil (USD/bbl) 68 65-75 65-75 65-75 65-75

SGD/CNY 4.97 4.96 4.96 4.96 4.96

6,000- 6,000- 6,000- 6,000-

JPY/SGDx100 1.22 1.22 1.21 1.21 1.21 LME Copper (USD/mt) 6,421

7,000 7,000 7,000 7,000

Quarterly Global Outlook 2Q2019

10 UOB Global Economics & Markets Research

SINGAPORE FOCUS I

MAS April 2019 Preview: Monetary Policy Is Likely To Stay Pat In April

We expect the MAS to keep monetary policy parameters unchanged in their upcoming April 2019 meeting. This means keeping the

appreciation slope, width and center unchanged.

We view current monetary policy to be appropriate despite recent economic softness, given that core inflation pressures will likely

persist into 2H19. We view core inflation to cross its 2.0% handle as early as July 2019.

An eventual monetary tightening in 2019 still remains on the cards. Should our call for the MAS to stay pat in April, a token tightening

into October will likely occur to address the rising price pressures, in line with MAS “primary objective of promoting medium term price

stability”.

A Synchronised Slowdown

Factors such as the US-Sino trade Exhibit 1: Industrial Production Growth Is Tapering Across Key Asian Economies

tensions, fading global tech sector and Source: Macrobond, UOB Global Economics & Markets Research

slower Chinese economic activity have

been quoted as key reasons for the recent

economic slowdown. In the US, we have

already seen softer consumer spending

and government expenditure amid the

longest government shutdown in history

that invariably injected negative spillover

effects to overall growth. In China, the mix

of weakness in its external front, tighter

access to credit and slowing producer

prices are drivers that likely dragged risk

appetite and overall growth prospect.

In Europe, growth stayed lacklustre at

0.9% q/q saar in 4Q19 led by stagnant

performance in the German economy,

although growing optimism for a “soft

Brexit” could buoy risk appetite in the Exhibit 2: Export Growth Turned Negative For Many Asian Economies

near-term.

Source: Macrobond, UOB Global Economics & Markets Research

Collectively, these factors can serve to

inject further external weakness especially

in Asia, which many economies like

Singapore remain to be export-oriented.

Even in many Asian economies, softer

trade and manufacturing prints have

already been observed as early as

last year. The economies that seen a

contraction in manufacturing activities

include Singapore (-3.1% y/y), Taiwan

(-1.9% y/y) and Philippines (-0.7% y/y),

even as export growth in many key Asian

economies tuned to negative growth

prints. For that matter, the World Trade

Organisation (WTO) cited that global trade

Quarterly Global Outlook 2Q2019

SINGAPORE FOCUS I UOB Global Economics & Markets Research 11growth is expected to slow to 3.7% in 2019

(from 3.9% in 2018) with downside risks Exhibit 3: Inflation Pressures Are Easing Across Asia

if trade conditions continue to deteriorate Source: Macrobond, UOB Global Economics & Markets Research

into the year. Kindly see Exhibit 1 and 2 for

further illustration.

Elsewhere, global inflation pressures

continue to fade on the back of lower

food and oil prices on a year-on-year

basis. Specifically, growth in Brent crude

oil on a year-on-year basis has fallen

for three consecutive months (the last

time it happened was during the 2016 oil

price rout), while growth in food prices

as measured by the United Nations FAO

food index declined for nine consecutive

months into February 2019. As a result,

inflation pressures across many key Asian

economies continued to soften into early

2019, especially seen in Philippines and

Exhibit 4: Implied Probability For A Dec 2019 Fed Rate Hike

China which saw their Feb inflation print

hitting its 12-month low while Malaysia Source: Bloomberg, UOB Global Economics & Markets Research

saw its first deflation print since Nov 2009.

100

Closer to home, Singapore’s inflation 91.5%

90

pressures are muted as well, with headline

inflation print below its 0.5% handle for 80

three consecutive months. See Exhibit 3 70

for further illustration. 60

50

Taking A Leaf From 40

Other Central Banks’ Books

30

Weaker-than-expected growth prospects

amid stalling inflation pressures are likely 20

0.6%

the key factors that persuaded policy 10

makers to iterate dovish tones in their 0

latest rhetoric. Taking the lead was the US May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Jan-19 Feb-19

Federal Reserve which surprising updated

its March 2019 dot-plot chart in showing

a dramatically lowered rate hike trajectory, Asian central banks in particular are environment in 2017/8 into a period of a

suggesting that the Fed will likely not hike observably quick in adjusting their policy rather anaemic growth environment led

rates in 2019. The Fed also announced tone since then. Particularly, Bank Negara by sustained uncertainties surrounding

its intention to slow its reduction in Malaysia (BNM) has kept its Overnight the US-Sino trade negotiations, slowing

holdings of US Treasuries from the Policy Rate (OPR) unchanged at 3.25% in Chinese economy and a fading technology

current level of US$30bn per month to its latest March MPC meeting, though the boom. This insipid economic growth pace

US$15bn beginning in May 2019 and to overall tone is perceived to be cautious is also met with softening commodity

conclude the balance sheet reduction particularly on the emphasis of downside prices led by lower energy and food

(BSR) program at the end of Sep 2019. growth risks from unresolved trade prices, which had invariably depressed

In addition, the updated Fed economic tensions, heightened uncertainties in the inflationary pressures across many Asian

forecasts showed that the Fed lowered the global and domestic environment, and economies. Singapore, being a price-

2019 GDP growth and inflation forecasts prolonged weakness in the commodity- taker, is also faced with such a paradigm,

and raising unemployment rate forecasts related sectors. Other central banks though also coupled with the recent

slightly. Market-watchers’ response to the which highlighted increased downside economic weakness seen in its recent

gradual turn of economic environment has risks to growth into 2019 – 2020 include fundamental prints.

been observed from the tapering of rate Bangko Sentral Ng Pilipinas (BSP), Bank

hike probability expectations into year- of Thailand (BOT), Central Bank of Taiwan Recent Singapore-Centric

end, which fell from a high of 91.5% in Nov (CBC) and the Reserve Bank of India Prints To Dissuade Tightening

2018 to 0.6% in March 2019. Kindly refer (RBI). Crucially, the synchronised slowdown

to our recent reporreport - US Mar 2019 seen across the globe has also negatively

FOMC: Fed Signals End Of Rate Hike In a nutshell, the global economy has likely affected Singapore. Recent Singapore’s

Cycle for further analysis. moved on from its coveted ‘Goldilocks” economic prints had largely disappointed

Quarterly Global Outlook 2Q2019

12 UOB Global Economics & Markets Research SINGAPORE FOCUS Imarket expectations. These includes

January’s data of industrial production UOB S$NEER

(-3.1% y/y, first contraction since December Source: Macrobond, UOB Global Economics & Markets Research

2017) and NODX (-10.1% y/y, clocking

130

three straight months of contraction).

128

Moreover, inflation pressures remains

muted with January’s CPI at +0.4% y/y 126

while core CPI slowed to 1.7% y/y. For 124

that matter, official forecast for headline 122

inflation in 2019 has been shaded down 120 MAS lifted the

slope "slightly"

to 0.5 – 1.5% from 1.0 – 2.0%, while core 118 in two

Lower imported sessions.

inflation outlook at 1.5 – 2.5% remains 116 inflation and Upward

MAS flattened slope to

unchanged. 114 MAS maintained the defacto 2.0% weaker growth

"neutral". GDP to

pressure on

per annum S$NEER appreciation outlook saw the core CPI to be

MAS flattening its expand at a more led by higher

112 amid supportive global growth and modest pace.

slope "slightly" wages.

We note that the mandate of the Monetary 110

upward wage pressures

Authority of Singapore (MAS) remains Apr-11 Apr-12 Apr-13 Apr-14 Apr-15 Apr-16 Apr-17 Apr-18

to be to promote “medium term price UOB S$NEER Perceived Mid-point Upper Band Lower Band

stability as a sound basis for sustainable

economic growth”. Specifically, the MAS

does not have an explicit inflation target, outlook then”, adding that the current further tightening at this juncture.

but nevertheless has concluded that “a central bank’s stance is “appropriate”

core inflation rate of just under 2.0%, while incoming data is “pretty much as As such, we revise our outlook for the

which is close to its historical mean, is expected, and unchanged”. Note that MAS to keep monetary policy parameters

consistent with overall price stability in the Monetary Authority of Singapore has unchanged in their upcoming April

the economy1”. Empirical core inflation, reiterated a 2019 growth outlook range of 2019 meeting. This means keeping the

which strips out costs of accommodation slightly below 2.5%. appreciation slope, width and center

and private road transport, has softened unchanged. We view current monetary

to 1.7% y/y in January 2019 from 1.9% y/y To Tighten Now Could Be A policy to be appropriate despite recent

in December 2018, while headline inflation Pre-Emptive Move To economic softness, given that higher core

continued to stay below its 0.5% handle Address Higher Inflation inflation pressures will likely persist into

for the third straight month. To that end, Singapore policy makers have 2H19. Should our outlook come to pass, we

tightened monetary policy “measured still view an eventual monetary tightening

Our econometric model suggests that adjustment” in April and October 2018 in the later part of 2019. Barring further

Singapore’s core inflation will eventually by slightly increasing the slope of the negative setbacks from global economic

cross its 2.0% handle in July 2019, and policy band from a neutral zero percent uncertainties, a tightening in October 2019

trend higher to touch 2.5% at end-year previously to our current estimate of a will likely occur in response to the higher

and average 2.0% for the year. This is 1.0% appreciation to-date. At that time, the core inflation print at above 2.0% in 2H19,

starkly different from our initial estimate language in the policy statements centred in line with MAS “primary objective of

for core inflation to cross its 2.0% handle around Singapore’s steady expansion path promoting medium term price stability”.

as early as 1Q19 given the slower-than- in 2018 with output slightly above potential

expected climb in Food, Healthcare, while core inflation is to see “modest but Still, a pre-emptive monetary tightening

Communications and Recreation & continuing pressures, before levelling off in the upcoming April MPC meeting could

Culture prices. Still, we continue to see at just below 2% over the medium term”. still happen, though it is not in our base-

higher inflation pressures into the year, case view. Singapore policy-makers could

given the supportive domestic labour However, accounting for the weaker- pay attention to the gradual rise in core

market conditions which should underpin than-expected economic prints seen inflation in the later part of 2019, which

wage growth, though the likely delay of amid a softening inflation outlook, we in turn see it imperative to inject another

core inflation to cross its critical 2.0% see risks to our initial call for an April’s “measured adjustment” and “slightly

handle into 2H19 could mean less impetus monetary policy tightening. We note that increase” the S$NEER policy slope to

for MAS to tighten monetary policy at this incoming economic prints have been address the eventual rise in domestic

juncture. disappointing which suggest further prices. Still, we think this case to be

headwinds to Singapore’s1Q19 growth unlikely, given the likelihood for further

Moreover, in the issue of slowing growth, outlook. Moreover, even while MAS kept downside to domestic economic growth

MAS chief Ravi Menon added that its core inflation outlook unchanged at as Singapore’s “domestic-oriented sectors

“downside risks have clearly increased” 1.5% - 2.5%, our model suggests that a remained sluggish” while “sluggishness in

and policy buffers to respond are “much core inflation print of above 2.0% will only trade volumes (is) set to continue in the

smaller today”. On MAS decision into come in 2H19. In a nutshell, we observe next few months2”. Moreover, we agree

April, Mr Menon added that “what we will that Singapore economic fundamentals with MAS Chief Ravi Menon’s comment

do depends on the growth and inflation and inflation climate appear softer than that the current monetary policy remains

1 The Monetary Authority of Singapore, Frequently Asked previously anticipated in 2018, which in “appropriate” at this juncture.

Questions on Singapore’s Monetary Policy Framework,

October 2018. turn could suggest some policy inertia for 2 The Monetary Authority of Singapore, Recent Economic

Developments in Singapore, March 2019

Quarterly Global Outlook 2Q2019

SINGAPORE FOCUS I UOB Global Economics & Markets Research 13SINGAPORE FOCUS II

Singapore Budget 2019: Mildly Expansionary With A Focus On Social Measures

Fiscal Position FY2018 - FY2019

S$ Billion

Overall Budget

Surplus/Deficit 2.12 -3.48

Special

Net Investment 15.30 Transfer

Returns Contribution 16.44 9.00 17.17

Example

Example CPF & MediSave Top-ups

Investment reurns Wage Credit Scheme

from MAS, GIC Long-Term Care Support Fund

and Temasek 73.67 78.99 74.90 80.25 Merdeka Generation Fund

Rail Infrastructure Fund

Operating Total

Revenue Expenditure

FY2018 FY2019

For FY2018, the Finance Ministry is expecting an overall budget surplus of S$2.1 billion, or 0.4% of GDP. Into FY2019, Singapore’s

overall budget balance is projected to see a deficit of S$3.5 million, or 0.7% of GDP. We observe that the budget is midly expansionary

with a focus on social measures. The budget has introduced three key thrusts: (1) Deepening Enterprise Capabilities, (2) Deepening

Worker Capabilities and (3) Encouraging Strong Partnership. Other initiatives including the S$6.1 billion Merdeka Generation

Package, increase in defence, security and diplomacy spending to 30% of Singapore’s total expenditure, and tweaks to tax

regulations. Social initiatives include the S$3.1 billion for long-term care support and the S$1.1 billion Bicentennial Bonus.

Revenue Collections For FY2018

Percent of Total Revenue

0.5% Others

2.0% Withholding Tax

2.0% Statutory Board Contributions

Corporate Income Tax 21.9% 3.6% Betting Taxes

3.9% Motor Vehicle Taxes

4.3% Custom & Excise Taxes

6.2% Assets Taxes

Personal Income Tax 15.9%

6.3% Stamp Duty

8.8% Fees & Charges

9.2% Other Taxes

Goods & Services Tax 15.3%

Total Expenditures For FY2018 & FY2019

S$ million

Defence 15.5 FY2019

14.8

Budgeted

Education 13.2

13.1

Health 11.7 FY2018

10.6 Revised

Transport 10.7

11.7

6.7

Home Affairs 6.7

Trade & Industry 4.4

4.7

3.3

National Development 4.1

3.0

Social & Family Development 2.8

2.8

Environment & Water Resources 2.1

Culture, Community & Youth 2.1

2.0

2.0

Manpower 1.8

Communications & Information 1.0

1.2

1.0

Prime Minister’s Office 0.9

Finance 1.0

0.9

0.8

Organs of State 0.7

Law 0.6 Note: The expenditure estimates do not include Special Transfers and

0.4 spending from Government Endowment and Trust Funds.

0.5

Foreign Affairs 0.5 Source: Singapore Budget 2019, Global Economics & Markets Research

For Full Report, please refer to our website www.uobgroup.com.sg/research

Quarterly Global Outlook 2Q2019

14 UOB Global Economics & Markets Research SINGAPORE FOCUS IICHINA FOCUS

Opportunities From Guangdong-Hong Kong-Macao Greater Bay Area

China

Zhaoqing

Guangzhou

Huizhou

Guangdong Province Foshan Dongguan

Greater Bay Area

Shenzhen

Zhongshan

Jiangmen

Hong Kong

Macau

Zhuhai

The Guangdong-Hong Kong-Macao Greater Bay Area (GBA) On 18 February 2019, China unveiled the outline plan for the

consists of Hong Kong SAR, Macao SAR and nine cities Guangdong-Hong Kong-Macao Greater Bay Area (GBA) to be

in Guangdong (Guangzhou, Shenzhen, Zhuhai, Foshan, developed into a vibrant world-class cluster and amongst others, a

Huizhou, Dongguan, Zhongshan, Jiangmen and Zhaoqing). globally influential innovation and technology hub.

The economies of Guangdong, Hong Kong and Macao are

significantly different from one another and this allows value to be

created by leveraging on their diverse strengths. In addition, the

70 million

POPULATION

generally more mature economies of Hong Kong and Macao will

not only be set as benchmarks but also stand to gain from faster

growth rate of its mainland peers in the combined entity of GBA.

Comparing to other “Bay Areas” around the world, there is much

Boasting a population of 70 potential for GBA given the specializations of various cities within

million and land area of nearly GBA and the tightened connectivity will help to further synergize

55,907 sq km, it accounts for these cities’ capabilities.

12.5% of China’s GDP.

At US$1.6 trillion in 2018, we expect the nominal GDP of the GBA

to rise to US$2.7 trillion by 2025 (assuming a conservative nominal

55,907

growth of 7.5% per annum) to become the largest Bay Area in the

world and further rise to US$4.0 trillion in 2030.

sq km

LAND AREA As the GBA will remain at the planning stage in the immediate

period with focus on improving integration, there will be substantial

The nine Mainland cities leeway given to local governments over how they will pursue

12.5 percent

account for nearly a quarter of

Mainland’s total trade while the

region accounts for 39.2% of

these goals. We think the vague targets are in recognition of the

challenges in integrating the region which covers three different

customs, legal systems and currencies.

OF CHINA'S GDP trade in China, Hong Kong and

Macao combined.

Quarterly Global Outlook 2Q2019

CHINA FOCUS UOB Global Economics & Markets Research 15Greater Bay Area Plan: Moving Into Acceleration Phase

China unveiled the outline plan for the Guangdong-Hong Kong- The plan identifies Hong Kong SAR, Macao SAR, Guangzhou

Macau Greater Bay Area (GBA) on 18 February 2019, with the and Shenzhen as the core cities to lead the GBA development.

aim to develop the region into a vibrant world-class cluster. This is important because the plan will lift the status of the

Special Administrative Regions (SARs) of Hong Kong and

The key targets include: Macao in China’s economic development.

1. developing the region into a globally influential innovation

and technology hub, Through the "one country, two systems" model, investors

2. nurturing a dynamic economic region with a cluster of will be able to leverage on Hong Kong’s advantages as the

cities that complement each other in terms of people, most internationalised city within the GBA with developed

capital, goods, services and information, financial/legal infrastructure, to participate in the GBA growth.

3. deepening cooperation between mainland China, Hong It is conceivable that Hong Kong’s status as an international

Kong and Macao, financial hub will be further strengthened in this current GBA

4. establishing a quality living circle for living, working and framework, including its role in further internationalisation of the

travelling and RMB while it will continue to serve the GBA in other areas such

5. acting as a catalyst for the Belt and Road Initiative (BRI) as shipping, trade, aviation, financial services, and as a magnet

for attracting international talent.

The 11 cities in the GBA are situated along the Maritime Silk

Road of the BRI and share the same goal to further open In the immediate period to 2022, the GBA plan aims to achieve

up China’s trade and investment, through enhancement in coordinated regional development where the framework for an

infrastructural connectivity, economic and trade cooperation international first-class bay area and world-class city cluster

as well as people-to-people exchanges with different regions. should be essentially formed. By 2035, the GBA is envisioned to

Hong Kong and Macao will thus become important platforms for become an innovation-driven economic system. As the GBA will

joint participation in the BRI. remain at the planning stage in the immediate period with focus

on improving integration, there will be substantial leeway given

to local governments over how they will pursue these goals. We

think the vague targets are in recognition of the challenges in

integrating a region which covers three different customs, legal

systems and currencies.

Greater Bay Area: Key Milestones

The GBA has received much attention since last year (2018). will realise the GBA target of ‘one-hour living circle’ i.e. bringing

Spun off from the earlier mainland-focused Pearl River Delta all major cities within the GBA in a travel radius of one hour, in

(PRD) economic zone (which did not include SARs of Hong order to speed up regional development.

Kong and Macao in its earliest configuration), the GBA was

set as a national strategy in 2016. In July 2017, the National These two major cross-boundary infrastructure projects are a

Development and Reform Commission (NDRC) and the huge boost to the physical connectivity in the GBA. This will be

governments of Guangdong, Hong Kong and Macao signed further strengthened by two more bridges over the Pearl River

the "Framework Agreement on Deepening Guangdong-Hong which are currently under construction. 1) The second Humen

Kong-Macao Cooperation in the Development of the Bay Area". Bridge that will link Guangzhou and Dongguan is scheduled for

completion in 2019, and 2) the Shenzhen-Zhongshan Bridge

The increasing interest on GBA came along with the opening of to connect these two major cities on the eastern and western

the 55 km Hong Kong-Zhuhai-Macao Bridge (HZMB) in October sides of the PRD is expected to come into operation in 2024.

2018 and the final 26 km phase Hong Kong section of the

Guangzhou-Shenzhen-Hong Kong Express Rail Link (XRL) in The recently proposed Zhuhai-Shenzhen bridge and high-

September 2018. The Guangzhou-Shenzhen and Guangzhou- speed rail project will add further to the list of plans to link up the

Zhuhai sections of the XRL were completed in 2011-12. The various economic nodes of the GBA and hence its attractiveness

HZMB cuts travelling time between Zhuhai and Hong Kong to as well as its upside potential.

under an hour from four hours previously while the completion

of the final 26km of the Hong Kong section in the XRL integrates

commuters in Hong Kong into China’s national rail network. This

Quarterly Global Outlook 2Q2019

16 UOB Global Economics & Markets Research CHINA FOCUSCreating Synergies Through The Strengths Of The Diverse GBA Cities

The economies of Guangdong, Hong Kong and Macao are Hong Kong Is A Services-Driven Economy

significantly different from one another and therein lie their With Deep Specialisation In Trade And Finance

complementarity nature and potential: Guangdong province is Source: CEIC, UOB Global Economics & Markets Research

primarily manufacturing-based (secondary industry is 39% of

GDP) with diverse capabilities among its cities; Hong Kong Hong Kong Economic Structure (% Share of GDP, 2017)

on the other hand, has always been predominantly services- Manufacturing Construction

driven; and Macao’s economy is mainly driven by tourism and 1% 5%

Others Wholesale &

related services. The integration of these varied cities through 32% Retail Trades

enlarged and integrated connectivity, regulation etc will create 21%

value and synergies by leveraging on their diverse strengths. Accommodation

& Food

Services

Guangdong’s Large Manufacturing Sector 3%

Is The Key Driver Of Its Economy Real Estate, Transport,

Prof & Business Storage, Postal

Source: CEIC, UOB Global Economics & Markets Research & Courier

Service

11% 6%

Guangdong Economic Structure (% Share of GDP, 2017) Information &

Financial & Communication

Primary Insurance s

Tertiary: Others Industry

18% 3%

21% 4%

Tertiary: Real

Estate Secondary:

Industry

9% Tourism And Gaming Accounts For The Bulk Of Macao’s Economy

39%

Tertiary:

Source: CEIC, UOB Global Economics & Markets Research

Financial

Intermediation

8% Macao Economic Structure (% Share of GDP, 2017)

Secondary:

Construction Utilities Wholesale,

Construction

3% 1% Retail, Repair,

Tertiary: Hotel

Manufacturing

4% Hotels &

& Catering Tertiary: Tertiary: Restaurants

Service Wholesale & Transport, 0%

12%

2% Retail Trade Storage & Post Transport,

10% 4% Storage &

Communication

s

3%

Public Admin, Financial Int,

Social & Real Estate,

Personal Serv Renting &

incl Gaming Business

Industry Activity

59% 21%

Guangdong: Large Diverse Manufacturing Base And A Driver Of Innovation And Technology

Technology will continue to be a major driver of the GBA growth. to create more value for the manufacturing industries and has

Harnessing Guangdong’s position as one of the fastest growing the potential to propel China’s high-tech export share in the

provinces in China and a leader in advanced manufacturing and coming years (from current 30%).

innovation in the country, the GBA plan aims to turn the region

into an international innovation and technology hub, cementing By province, Guangdong has the highest R&D expenditure which

its status as one of the major high-tech manufacturing centers accounted for 13.3% share of total R&D expenditure in China in

of the world. 2017. The R&D expenditure in the province has continued to

rise over the years to reach 2.5% of Guangdong’s GDP in 2017.

The large and diverse manufacturing base in the Guangdong Guangdong is also ranked highly in urban fixed asset investment

cities ranges from high-tech manufacturing in Shenzhen, white with US$553.6 bn (39.6% of Guangdong’s GDP) recorded in

goods in Zhongshan and Foshan, and automobiles in Jiangmen. 2017. By sector, around 28% of the urban FAI in Guangdong is

The GBA will be able to capitalize on the various supply chains in manufacturing while real estate accounted for 36%.

Quarterly Global Outlook 2Q2019

CHINA FOCUS UOB Global Economics & Markets Research 17You can also read