Quarterly Update - Forest Investment Associates

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Quarterly Update Q1 | 2021

Summary Update

SUMMARY UPDATE — There is positive activity in general for all major

CONTENTS operating areas in North America. Pine products in the south saw increases

over the first quarter. The Pacific Northwest also saw increases in the first

quarter in Douglas-fir, while seeing a slight decrease in Whitewoods.

Northern hardwoods saw decreases overall and were lower than year

T i m b e r P r ic es

previous levels.

P r o duc t Pr ic es

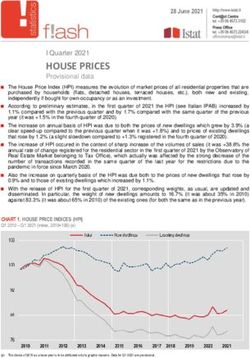

March housing starts were reported to be 1.739 million, which was 22.4%

T i m b e r la nd above February rate of 1.421 million, and 37.0% above the March 2020

M a rk et s rate of 1.269 million. Interest rates for 30-year fixed mortgages increased

over the first quarter of 2021, climbing to an average rate of 3.08%. Lumber

I nt er nat i on al

and panel prices retracted early in the fourth quarter of 2020; however,

U p dat e

prices once again reached all-time highs in February. The Random Lengths®

E c on om ic N e ws Framing Lumber Composite Price ended the quarter up 24.8% and prices

are almost 170% above what they were a year ago.

Q u a rt er l y

D as hb oa r d TIMBERLAND MARKETS — The headline deal of the first quarter was

Weyerhaeuser’s announcement that it had agreed to purchase 69,200

Forest acres in south Alabama from Soterra for $149 million. The deal, the largest

Investment

Associates

in the South in over a year, is set to close in the second quarter. Otherwise, it

was a quiet quarter for timberland transactions, although several offerings

15 Piedmont Center

Suite 1250 are on the market with bids expected in the second quarter.

Atlanta, GA, 30305

P (404) 261-9575

F (404) 261-9574

www .f or e s t in ve s t. c o m 1FOREST INVESTMENT ASSOCIATES Q1 | 2021

Timber Prices

SOUTHEASTERN — Demand for pine products generally increased over the first quarter. Timber Mart-

South reported marked increases for all pine products (4.9% in pine pulpwood, 5.5% in pine chip-n-

saw and 2.6% in pine sawtimber). Sawtimber ended the first quarter up 2.5% above last year’s level.

Pine chip-n-saw prices ended the quarter 4.7% above year-ago prices. Pine pulpwood was also up

compared to previous year values with a 3.3% increase.

Southeastern Timber Prices

$40

$35

Hardwood Sawtimber

$30 Pine Sawtimber

$25

$/Ton

$20 Chip-n-Saw

$15

Pine Pulpwood

$10

$5

Hardwood Pulpwood

$-

4Q19 1Q20 2Q20 3Q20 4Q20

Source: Forest2Market®

NORTHERN HARDWOODS — In the Pennsylvania wood markets, certain key species increased in

demand. According to the Pennsylvania Woodlands Timber Market Report, white ash prices

increased 6% during the fourth quarter (the most recent publicly reported pricing), ending the quarter

19% below year-ago levels. All other species saw a decrease in value, although Northern red oak and

Soft Maple were up 4.8% and 9.2%, respectively, compared to year ago prices. Black cherry and

white ash both saw decreases hovering around 18%. However, recent timber sale results indicate

that prices for black cherry, oaks, and hard maple are rapidly increasing during the first quarter.

Hardwood lumber and log demand in Pennsylvania and New York increased dramatically throughout

the first quarter in this region. Mills struggled to fill burgeoning orders as U.S.

homebuilding/remodeling continued its strong run while lumber and log exports continued to recover

significantly from logistical bottlenecks caused by the pandemic. Labor, trucking, and container

shortages hampered sawmills’ ability to get product to customers. Hard maple, white oak, red oak,

red maple, white ash, and black cherry were all in high demand with very robust pricing, showing a

strong rebound from the most recently reported public pricing of last year’s fourth quarter.

Wisconsin hardwood lumber and veneer log markets continued their strong run throughout the first

quarter. Competition for logs intensified as sawmills worked to build inventory ahead of the

traditional mud season, which usually arrives in March. The region saw strong domestic and export

www .f or e s t in ve s t. c o m 2FOREST INVESTMENT ASSOCIATES Q1 | 2021

demand for hard maple, yellow birch, basswood, and white ash lumber and logs. Boltwood markets

continued to be strong as flooring plants struggled to procure enough lumber to fill expanding order

files. Hardwood pulpwood demand continued to be weak as remaining mills struggled with pandemic

related demand issues.

Northeastern Hardwood Timber Prices

$900 $1,700

Red Oak, W. Ash, Maples ($/MBF

$1,600

$800

N. Red Oak $1,500

Black Cherry ( $/MBF Doyle)

$700 $1,400

$1,300

Hard Maple

Doyle)

$600 $1,200

$500 $1,100

Soft Maple $1,000

$400 $900

White Ash Black Cherry $800

$300

$700

$200 $600

4Q19 1Q20 2Q20 3Q20 4Q20

Source: Pennsylvania Woodlands Timber Market Report - Northwest Region

PACIFIC NORTHWEST — Pacific Northwest markets experienced increased demand carried into the

first quarter of 2021. Log Lines® reported that average delivered prices for Douglas-fir #2 logs

increased 3.9% over the quarter, ending the quarter 20.3% above year-ago levels. Whitewoods (i.e.,

true firs and hemlock) average delivered log prices decreased by 2.8% compared to the previous

quarter but ended the quarter 18% ahead of last year’s level.

Domestic sawmill log prices were relatively flat but overall stayed at very high levels. Spot regions

with large amounts of fire salvage logging activity remained at lower pricing with some mills

implementing quotas due to heavy supply. Delivered log prices for Douglas-fir sawlogs stayed around

$800 per MBF in Washington and $850 per MBF in Oregon. China export log buying activity started

to pick up with prices approaching chip and saw domestic pricing, but in general remained below

sawlog values. Japan export followed domestic price trends upwards and remain competitive.

www .f or e s t in ve s t. c o m 3FOREST INVESTMENT ASSOCIATES Q1 | 2021

Pacific Northwest Log Prices

$825

$775

Douglas-Fir, Sawmill #2

$725

$675

$/MBF

$625

$575

Whitewoods

$525

$475

$425

Mar-20 May-20 Jul-20 Sep-20 Nov-20 Jan-21 Mar-21

Source: Fastmarkets RISI - Log Lines®

Product Prices

LUMBER AND PANELS — Lumber and panel prices retracted early in the fourth quarter of 2020;

however, prices once again reached all-time highs in February. The Random Lengths® Framing

Lumber Composite Price ended the quarter up 24.8% and prices are almost 170% above what they

were a year ago.

Lumber and Panel Prices

$1,350

$1,250

$1,150

Composite Price Indices

Framing Lumber

$1,050 Composite Price

$950

$850

$750

$650

$550 Structural Panel

Composite Price

$450

$350

$250

Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21 Mar-21

Source: Random Lengths®

PULP AND PAPER— Pulp and newsprint had positive changes over the first quarter. The benchmark

(northern bleached softwood kraft) pulp price index increased 23.2% over the quarter, ending 25.1%

www .f or e s t in ve s t. c o m 4FOREST INVESTMENT ASSOCIATES Q1 | 2021

above year-ago levels. U.S. Newsprint (27.7 lb.) prices increased 6.6% over the quarter, falling 3.2%

below last year’s level. Freesheet increased by 1.8% and is slightly above year ago values at 0.5%.

Boxboard prices held flat over the quarter.

Pulp and Paper Prices ($/short ton)

$1,500 $800

$1,400 $750

NBSK, Freesheet, Boxboard

$1,300 $700

Newsprint

$1,200 $650

$1,100 $600

$1,000 $550

$900 $500

Mar-20 Apr-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Feb-21 Mar-21

US NBSK Index Uncoated Freesheet (20 lb repro)

Bleached Kraft Boxboard -SBS (C1S) U.S. Newsprint (27.7 lb) EAST

Source: Fastmarkets RISI

Timberland Markets

TRANSACTIONS — The headline deal of the first quarter was Weyerhaeuser’s announcement that it

had agreed to purchase 69,200 acres in south Alabama from Soterra for $149 million. The deal, the

largest in the South in over a year, is set to close in the second quarter. The deal signals strength in

timberland valuations despite the coronavirus pandemic of the past year, fetching $2,153 per acre.

TRANSACTIONS IN PROGRESS — While the Soterra deal was the only major closing of the first

quarter, there are several timberland offerings currently on the market in the South and Pacific

Northwest. Many of these offerings are taking bids early in the second quarter. Investors will be

closely monitoring the outcome of these transactions in the coming months. As vaccinations become

more widely available and travel restrictions ease, deal activity is expected to pick up in 2021.

www .f or e s t in ve s t. c o m 5FOREST INVESTMENT ASSOCIATES Q1 | 2021

International Update

The dawn of this new decade surprised with the unexpected volatility and uncertainty caused by the

global COVID-19 pandemic that brought economic and social activity to a halt worldwide. Yet as we

close the first quarter of 2021, glimmers of hope for a post-pandemic return to normal life begin to

appear. The approval of several vaccines in late 2020, coupled with often clunky and erratic, yet

gradually improving, vaccine deployment programs are encouraging signs that, although far from over,

there will be a future in which global life can get back to normal. Some challenges still lay ahead of us

before normal life can resume, such as uneven vaccine access and deployment programs between

countries and regions; as well as worrisome new variants of the virus that make the road to a post-

pandemic recovery a bumpy one.

And yet even among this challenging global outlook, forestry investments continued to show the asset

class’ resiliency and important contributions to the global supply chain of the mission critical role that

forest products play in our daily lives. Major fiber consumption centers such as China and the United

States continued to demand forest products at an increasing pace as their economies slowly

reopened. As global trade is reignited, and with a relatively inelastic global supply of wood flow from

sources such as Brazil, Chile, New Zealand, Australia and the US, positive log-price pressure has

started to manifest. Late 2020, China imposed a timber import ban on Australian logs, posing a major

challenge for the Australia to China log trade during the first quarter. Domestically though it has been

a very different story with Australia’s economy, especially in the construction sector, strongly

rebounding post-pandemic and driving local sawmills to significantly increase production by adding

shifts. A similar domestic story is also playing out in New Zealand where supply of forest products for

domestic home building is tight with building consents at record highs.

CHILE – Chile started the year strong with one of the world’s most efficient and effective COVID-19

vaccination programs. By the end of the first quarter 6.8 million Chileans, more than 35% of the

population, had received at least one dose of the vaccine, and 3.7 million Chileans had been fully

vaccinated. Yet the pandemic continued to be a challenge with 42,915 active cases at the end of the

quarter. The spike in active cases was generally attributed to the relaxation of social distancing during

Chile’s summer vacation in February combined with the arrival of more aggressive variants of the virus.

Authorities responded swiftly and firmly, reinstating strict mobility restrictions, and closing Chile’s

borders for the month of April. Midterm elections that were scheduled for April, which included the

selection of the group that will draft Chile’s new constitution as well as governors, mayors and

councilors, were postponed until mid-May. During 2020 Chile’s economy contracted by 6.0%, beating

IMF projections for a contraction of 6.25%. For 2021, the Chilean economy is projected to grow by

6.0% thanks to the strong rebound in global demand for Chile’s main exports, including copper and

forest products, as well as the positive effects of the vaccination campaign for Chile’s domestic

economy.

www .f or e s t in ve s t. c o m 6FOREST INVESTMENT ASSOCIATES Q1 | 2021

Chile’s forest industry exports of $4.9 billion USD during 2020 represented a drop of 12.6% versus

2019 and the lowest figure in the last five years mainly due to the global pandemic. However, during

the second half of 2020 and first quarter of 2021, the forest industry continued to operate very

dynamically with sustained improvements in domestic and external demand, as well as price increases

that confirm that Chile’s fiber and wood products markets have strongly recovered. The main category

of exported volume as of February 2021 (latest data available) was Pulp and Paper which represented

56% of total exports and an 18% increase compared to the average of the previous moving quarter

(November 2020 to January 2021). Sawn and Planed Wood represented 13% of total exported

amounts, while Moldings and Panels came in at 11% and 8% respectively. China and the U.S.

continued to be the main destinations for exports of Chile’s forest products exports.

BRAZIL – Brazil began 2021 with continued challenges related to the COVID-19 pandemic. As of mid-

January, the country’s second wave had solidly taken hold. As of end of the first quarter Brazil had a

total of 13.0 million confirmed cases and a seven-day average of 63,000 new cases. On a positive

note, Brazil’s official government body responsible for vaccine approval (ANVISA) has approved two

vaccines for deployment in the country. During the first quarter, approximately 25 million people,

almost 12% of Brazil’s population, had received at least one dose.

During 2020, the economy contracted by 4.1% driven mainly by the global pandemic. But within

Brazil’s economy, and regardless of the pandemic related challenges, the agricultural sector still

managed to grow by 2.0% during the year. After closing 2020 with inflation of 4.52%, during the first

quarter inflation expanded to 6.1%. In their latest COPOM meeting, the Brazilian central bank raised

interest rates by 75 bps to 2.75% and further increases during 2021 are expected to raise the rate to

5.0% by year-end, targeting inflation of 3.75% for 2021 and 3.5% for 2022. During the quarter, the

Brazilian Real depreciated by 9.62% to 5.70.

In the forest industry, upward price pressure for Brazilian pulp continued during the first quarter with

market analysts predicting a USD $670/ton hardwood pulp price estimate for the year, 30% above

previous forecasts. A stout price hike to USD $800/ton is expected for April and drove consumers in

Asia to attempt to secure inventory before price hikes. Once this price hike cycle concludes, and as

additional capacity comes online in 2022 to 2024, prices are expected to soften. Wood panel markets

continued their healthy expansion with moderate growth domestically but significant growth in export

markets, driven partially by the weaker BRL’s support for export-oriented volumes.

www .f or e s t in ve s t. c o m 7FOREST INVESTMENT ASSOCIATES Q1 | 2021

Economic News

HOUSING — U.S. homebuilding dropped to a six-month low in February as severe cold gripped many

parts of the country. March followed with the largest high since 2006 with 1.739 million units. This I

a 22.4% increase from February.

MORTGAGE RATES — After record low rates at the end of 2020, mortgage rates have trended

upwards through the first quarter of the year, ending at approximately 3.1%, slightly below levels

from a year ago.

JOBS — The March jobs report was well above economist expectations, with nonfarm payrolls rising

916,000. Gains were strongest in leisure and hospitality, while construction soared by 110,000.

CONSUMER CONFIDENCE — The consumer confidence index rose to 109.7 in March, the best

showing since it stood at 118.8 in March of last year as the pandemic was beginning to hit the

United States. The index stood at 90.4 in February.

INFLATION — The CPI rose 0.6% in March from the previous month and 2.6% from a year ago, slightly

higher than economist estimates. A surge in gasoline prices accounted for about half the gain amid

signs of an accelerating economic recovery.

TRADE DEFICIT — The U.S. trade deficit widened to $71.1 billion in February to a record high as solid

household and business demand kept imports running ahead of shipments to overseas customers.

INTEREST RATES — The Fed has committed to keeping interest rates stable for the time being,

irrespective of this year’s recovering economy. The benchmark 10-year yield rose more than 80 basis

points in the first quarter on expectations of strong economic growth, higher inflation and the

estimated $4 trillion in new debt to be issued this year.

OIL PRICES — Oil reached a high of approximately $65 a barrel during the first quarter.

U.S. DOLLAR — The U.S. Dollar remains relatively weak against a basket of major currencies, based

on ongoing loose Federal Reserve policy, a drop in Treasury yields and surprisingly soft US jobs

figures.

www .f or e s t in ve s t. c o m 8FOREST INVESTMENT ASSOCIATES Q1 | 2021

Quarterly Dashboard

Southeastern Timber Prices Northeastern Hardwood Timber Prices

$45 $1,200 $2,100

$1,100 $1,950

N. Red Oak, W. Ash, Maples ($/MBF)

$40

$1,000 N. Red Oak $1,800

Hardwood Sawtimber

$35

$900 $1,650

Black Cherry ($/MBF)

Black Cherry

$30 Pine Sawtimber

$800 $1,500

$25

$/Ton

$700 $1,350

$20 Chip-n-Saw

$600 White Ash $1,200

$15 Pine Pulpwood $500 $1,050

Hard Maple

$10 $400 Soft Maple $900

$5 $300 $750

Hardwood Pulpwood

$- $200 $600

1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 1Q21 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20

Source: Pennsylvania Woodlands Timber Market Report - Northwest Region

Source: Forest2Market®

Pacific Northwest Timber Prices Pulp and Paper

$1,500 $800

$900

$850 $1,400 $750

NBSK, Freesheet, Boxboard ($/Short Ton)

$800

Douglas-Fir, Sawmill #2

$1,300

$750 $700

Newsprint ($/Short Ton)

$700 $1,200

$/MBF

$650 $650

$600 $1,100

Whitewoods $600

$550 $1,000

$500

$900 $550

$450

$400

$800 $500

1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 1Q21

Mar-18 Jul-18 Oct-18 Feb-19 May-19 Sep-19 Dec-19 Mar-20 Jul-20 Oct-20 Feb-21

Source: Fastmarkets RISI - Log Lines® Source: Fastmarkets RISI

www .f or e s t in ve s t. c o m 9FOREST INVESTMENT ASSOCIATES Q1 | 2021

Quarterly Dashboard

Housing Starts 30 yr. Mortgage

1900 5.5%

1700

1500 4.5%

000's in thousands

1300

1100 3.5%

900

700

2.5%

Mar-16 Sep-16 Mar-17 Sep-17 Mar-18 Sep-18 Mar-19 Sep-19 Mar-20 Sep-20 Mar-21

Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18 Mar-19 Mar-20 Mar-21

Source: NAHB.org – http://www.nahb.org/ Source: The Federal Reserve

Lumber Inflation (CPI)

$380 3.0%

$360

2.0%

$340

$320 1.0%

Index (1982 = 100)

$300

0.0%

$280

$260 -1.0%

$240

-2.0%

$220

$200 -3.0%

$180

-4.0%

$160

$140 -5.0%

Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18 Mar-19 Mar-20 Mar-21 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18 Mar-19 Mar-20 Mar-21

Source: U.S. Department of Labor, Bureau of Labor Statistics Source: http://www.bls.gov/cpi/home.htm

www .f or e s t in ve s t. c o m 10You can also read