Sohn Conference | May 8th 2017 - Dylan Adelman The Wharton School - Sohn Investment Conference

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Sohn Conference | May 8th 2017

Dylan Adelman

The Wharton School

dylana@wharton.upenn.edu

Introduction Dylan Adelman

dylana@wharton.upenn.edu

A contrarian thesis inside of a contrarian thesis?

• The standard contrarian thesis on eBay is excellent. The company is a

stable grower falsely seen as a melting ice cube, has temporary unpopularity,

is aggressively repurchasing undervalued shares, has a fast-growing earnings eBay Financial Snapshot ($b)

stream from StubHub, and trades at a reasonable valuation.

Share price (5/03/17) $33.15

• This is not the standard contrarian thesis. Two additional factors indicate Shares outstanding 1.083

that eBay has 46% upside from current levels. These factors relate to eBay’s Market capitalization 35.90

post-spinoff operating agreement with PayPal (“Merchant of Record”) and Net cash 2.20

to its Classifieds Group segment (“Classifieds”). 5-year IRR equals 24%.

Enterprise value 33.70

• 46% upside? This excludes the merits of the standard contrarian thesis. EPS (LTM) $1.91

eBay’s Marketplaces and StubHub segment are given more conservative Free cash flow (LTM) 2.165

valuations than sell-side consensus estimates in this presentation.

P/E 17.36x

• Bonus Prize: Part I of this pitch doubles as a short thesis on PayPal. FCF yield 6.03%

2

Part I Merchant of Record

“It’s important to realize that losing even half the eBay

volume might have destroyed PayPal as a business […]

eBay owned the platform and the checkout line. In

hindsight, it’s a miracle they didn’t thrash PayPal.” –

David Sacks, First COO of PayPal (2014)

Merchant of Record Dylan Adelman

dylana@wharton.upenn.edu

Not quite the Shakespeare play.

eBay-PayPal Relationship Everyone Else in 2017

• eBay acquired PayPal in 2002 to serve as its merchant • All major e-commerce sites are merchants of record.

of record. This provided costless new users to PayPal Some of these payment processors, such as Alibaba’s

while giving eBay an in-house payments processor. AliPay, have gained traction outside their websites.

• As eBay’s merchant of record, PayPal intermediates • The downsides to being a merchant of record are the

every transaction. Buyers pay PayPal, and PayPal pays risks of chargebacks and customer service costs. The

the seller. PayPal takes a ~3.5% fee from the buyer upside is a 2.5% spread on gross merchandise volume.

and pays a ~1% fee to the acquiring merchant bank For the largest e-commerce sites, being a merchant of

that processes in bulk. The spread is PayPal’s profit. record is thus a substantial profit center.

eBay can become a merchant of record by serving as its own payment intermediary, rather than

outsourcing to PayPal. This would provide a 2.5% profit spread on eBay’s ~84 billion GMV.

5

Merchant of Record Dylan Adelman

dylana@wharton.upenn.edu

Someone forgot to disclose “key customer risk.”

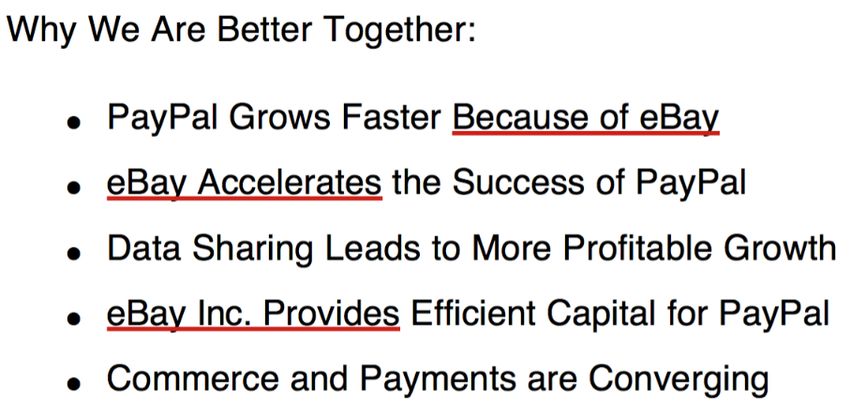

Benefits to PayPal Benefits to eBay

• In response to a proxy for splitting eBay and PayPal

led by Carl Icahn, management noted on 3/24/14:

“Tightly integrated with eBay, PayPal can grow faster and more profitably

than it would as a standalone company. Adoption and use of PayPal on

eBay enables innovation and growth off of eBay. For example, eBay

?

delivers about 30% of PayPal's new users at virtually no cost, more than

30% of PayPal's revenues and approximately 50% of PayPal's profits.

PayPal's growth and leadership in mobile payments has occurred precisely

because of this strong base of PayPal users on eBay.” – 3/24/14

Why does eBay continue this one-sided relationship? 6

Merchant of Record Dylan Adelman

dylana@wharton.upenn.edu

It pays to read the footnotes.

eBay’s July 2015 spinoff of PayPal was the first step to ending this one-sided relationship. The pre-spin

relationship between both companies is frozen by an operating agreement that is valid until July 2020.

• Question: once eBay can end the merchant

of record relationship with PayPal, how do “Following the three (3) year anniversary of the Effective

we know that they actually will? Time, eBay shall be permitted to declare itself as a Merchant

of Record for transactions effected by third Persons in up to

• Answer: because of this cheeky clause in two (2) Covered Jurisdictions as selected by eBay in its sole

Section XIV of the operating agreement… discretion (each, a “Test Jurisdiction”) […] – Section XIV

“It’s not really a question of if they will do it, but when.

eBay will become a merchant of record, but the more

interesting question is whether they will continue to offer

PayPal as an option at all.” – GLG Payments Expert

The eBay-PayPal operating agreement allows eBay to begin merchant of record trials three years after the spinoff.

Read between the lines: why would this footnote exist if eBay did not want to be a merchant of record?

The catalyst for value realization is the announcement of test jurisdictions as a merchant of record in mid-2018.

7Merchant of Record

The hangover that PayPal can’t sleep off.

Assumptions

84.26B = LTM GMV

3.47% = PayPal take rate

1.0% = back-end fees (84.26)*(1.034)*(3.47% - 1%)*(50%)*(1 - 25%)

50% = SG&A costs = 8.57 billion

25% = tax rate (1.14)*(10% - 3%)

3% = terminal rate

10% = discount rate

Rationale

• 3.47% – this is the last reported figure for PayPal’s overall transaction take rate (in 2014). This number blends in

the 0% take rate on various Braintree platforms (i.e. Venmo). The true on-eBay take rate is much closer to 4%.

• 1.0% – based on GLG experts’ commentary. This comprises various fees for credit and debit transactions that

include network fees, interchange fees, acquirer fees, and fraud fees. eBay’s size enables negotiating lower rates.

• 50% – haircut to account for incremental hires, customer service expenses, and ironing out the kinks.

8Part II eBay Classifieds

“I look for economic castles protected by unbreachable moats.” – Warren Buffett

eBay Classifieds Dylan Adelman

dylana@wharton.upenn.edu

Good luck disrupting this, Silicon Valley.

How much would you pay for a business with the

following characteristics?

• Nationwide monopoly in ten countries with zero

reinvestment required to keep competitive position

• 60% operating margins on ~800M revenue with a

high degree of operating leverage

• 280 million person monthly user base that is price

insensitive, sticky, and has no alternative options

• Massive and still-underpenetrated total addressable

market that will enable top-line growth of 10-15%

for the next decade

• Recession-proof and holds no inventory

Let’s ask the sell side! 11eBay Classifieds Dylan Adelman

dylana@wharton.upenn.edu

The problem with sell-side bandwagoning.

Market View Reality

• “Concerns about eBay’s growth are valid considering Classifieds LTM Revenue = $804M StubHub LTM Revenue = $964M

that it makes its money from its marketplaces and

ticketing services. It does not have significant revenue

outside of the two.” – 4/11/17

• “We've assigned the standalone eBay a narrow moat

rating, down from our previous wide moat rating for

the consolidated eBay/PayPal entity.” – 10/26/15 Estimated EBIT margin = 60% Estimated EBIT margin = 30%

Estimated EBIT = $482M Estimated EBIT = $289M

Classifieds contribute 67% more EBIT than StubHub

“I was always baffled by Wall Street’s focus on StubHub over Classifieds. I think it’s

because they buy their Knicks tickets on StubHub, but never buy any used items on

Marktplaats. And why would they? It’s a Dutch website.” – GLG Classifieds Expert

The market is not accounting for eBay Classifieds. 12eBay Classifieds

But really, when will Craig Newmark monetize?

Assumptions

804M = LTM revenue

10% = 2017-27 CAGR (804)*(1.110)*(70%)*(1 - 25%)

70% = EBIT margin (422*10) + = 11.96 billion

25% = tax rate 9

(1.1 )*(10% - 4%)

4% = terminal rate

10% = discount rate

Rationale

• 422 – free cash flow produced by classifieds in 2017. (804)*(70%)*(1-25%) = 422M.

• (422*10) – value of interim payments before terminal period. Because the growth rate equals the discount rate,

they cancel out during the projection period. 1.1/1.1 = 1, 1.12/1.12 = 1, 1.13/1.13 = 1, and so on.

• 10% – growth has trended at 10-15% over the last five years. Comparable firms (Schibsted and Naspers) estimate

15% growth over the long-term due to continued market penetration, monetization, and new listing verticals.

• 70% – based on operating margins of mature peers owned by Schibsted (i.e. Leboncoin and Finn).

13Part III Marketplaces & StubHub

“[There is] a difficulty that the public marketplace has

in valuing cash cows, let’s call them, businesses that are

growing slowly […] but generate an enormous amount

of free cash flow.” – John Malone (2016)Marketplaces

The world’s largest store of pez dispensers.

Assumptions

7.28B = LTM revenue

30% = EBIT margin (7.28)*(30%)*(1 - 25%)

25% = tax rate = 23.40 billion

3% = terminal rate 10% - 3%

10% = discount rate

Rationale

• 3% – Marketplaces can be visualized as a perpetual bond. Current revenue growth guidance is 5-7% annually.

This projection has revenue growth at 3% in perpetuity for conservatism. Clearly, this is not a melting ice cube.

• 30% – this operating margin adjusts for temporarily inflated SG&A due to the structured data inititave.

• 25% – eBay’s historic tax rate is 20% due to its international earnings mix. 25% is used for conservatism.

• Note that the Marketplaces and StubHub projections are far more conservative than Street estimates.

16StubHub

The best place to buy Hamilton tickets at a 300% markup.

Assumptions

964M = LTM revenue

10% = 2017-27 CAGR (964)*(1.110)*(30%)*(1 - 25%)

30% = EBIT margin (217*10) + = 6.15 billion

25% = tax rate 9

(1.1 )*(10% - 4%)

4% = terminal rate

10% = discount rate

Rationale

• 217 – free cash flow produced by StubHub in 2017. (964)*(30%)*(1-25%) =217M.

• 10% – grew nearly 40% last year. Management is guiding for 10-15% annual growth. The acquisition of TicketBis

opens international markets. The underpenetrated and large total addressable market offer a long growth runway.

• 30% – estimate backed out from known Marketplaces margins and likely Classifieds margins. This EBIT margin

will likely increase over time due to StubHub’s operating leverage, pricing power, and market consolidation.

17Part IV Valuation & Conclusion

Valuation Dylan Adelman

dylana@wharton.upenn.edu

Were you expecting a balanced three-statement model?

Marketplaces + StubHub + Classifieds + Merchant of Record + Excess Cash = eBay

23.40 + 6.15 + 11.96 + 8.57 + 2.20 = 52.28 billion fair value

Current Price: $33.15 | Target Price: $48.27

Upside: 46%

19IRR Dylan Adelman

dylana@wharton.upenn.edu

The expected average annual return of eBay over the next five years.

IRR = organic growth + FCF yield + multiple expansion + revaluation

IRR = 5.0% + 6.0% + 3.3% + 9.2% = 23.5%

5-year IRR = ~24%

Rationale

• 5.0% – weighted average of estimated 5-year growth rates across Marketplaces, StubHub, and Classifieds.

• 6.0% – current free cash flow yield. This return will be amplified by ~$1B in share buybacks in 2017.

• 3.3% – slight multiple expansion from 17x to 20x EPS due to ~35% of earnings coming from faster-growth

StubHub and Classifieds segments. Multiple expansion assumed over five-year period: (20/17)^(1/5)-1.

• 9.2% – upside from readjustment to fair value over next five years: (48.27/31.15)^(1/5)-1.

• If multiple expansion and revaluation occur within a year, the one-year IRR will equal 85%.

20“My house is filled with this crap

Shows up in bubble wrap

Most every day

What I bought on eBay”

- “Weird Al” Yankovic (2003)Special Thanks

Nad Kilani Tong Lap Him

Justin Ang Rufino Mendoza

Frank Geng Pratyusha Gupta

Jordan Meer Deependra Mookim

The Sohn Conference Foundation

Global Platinum Securities

Gerson Lehrman Group

Casa BalearSohn Conference | May 8th 2017

Dylan Adelman

The Wharton School

dylana@wharton.upenn.eduYou can also read