South Africa - 120 Days of Lockdown - COVID-19 Impact on CPG & Retail 24 July 2020 - Trade Intelligence

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

COVID-19 Impact on CPG & Retail South Africa – 120 Days of Lockdown 24 July 2020

Content

• COVID–19 Update

• Latest Category Performance

• Beauty Update

• Liquor’s Six Week Respite

• Changing the Approach to Retailer and Brand Loyalty

• IRI COVID-19 Global Update

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 2

Be ready for anything

• On lockdown day 120, we are in the COVID-19 peak period. As a form of normality sets in, we see the impact of cash-strapped and unemployed

consumers in the slowing of Grocery sales. This trend is similar to Grocery trends across other countries.

• Cigarettes remain banned and a recent University of Cape Town (UCT) study revealed that 11% of smokers had quit smoking. 56% of these

respondents quit due to price hikes and not as a result of the ban itself Despite the ban, smokers easily locate cigarettes and with the loss of the

multinational brands, local manufacturers are gaining share. Once the ban is lifted, there is likely to be a price war and an increase in excise taxes.

One thing is certain, the Cigarette industry in SA is in disarray.

• Growth over the total lockdown period has slowed from 7% to 5.6% and as consumers’ continue to struggle, we expect this trend will continue.

• Edible Groceries continues to grow with Snacks, Spreads and Yoghurt seeing renewed boosts as schools returned, for a brief period.

• Soap, Sanitizer and Vitamins remain at the top of consumers lists, however Cleaning products, Wipes and Personal Care are declining.

• Within Beauty, Face Care and Hair Care’s initial strong lockdown growth slowed after salons re-opened, but has remained ahead of pre-lockdown

levels. Cosmetics is declining as consumers continue to spend more time at home, however compulsory masks in SA has driven the market towards

Eye make up, which now accounts for 22% (up from 18%) of the category, with Lip dropping to 8% from 11%.

• Liquor’s six week respite was not enough to bolster the Liquor manufacturers, or to prepare unknowing shoppers for the second Liquor ban.

Growth was at 9% in value. The value growth was driven by inflation and up-trading into larger packs.

• Wine is the only category to show growth among both LSM groups and gained share at the expense of Beer.

– This is mainly driven by inflation on Beer after several years of flat/low inflation.

– Box Wine had low/no inflation, whereas Bottled Wine prices increased by well over 10%, driving the value growth amongst LSM 7-10.

– Large packs were popular during this period.

• The alcohol ban had a positive impact on Non-Alcoholic Beverages (NAB). Already a growing category as consumers became more mindful of their

alcohol consumption, NAB have grown 17% YTD vs LY, with a direct switch from alcoholic beverages is evident.

• As we settle into this new normal, retailers and manufacturers need to change their approach to loyalty. Given the challenges of the industry, is loyalty

even a reasonable expectation? See our summary on the latest IRI UK Whitepaper and to learn more, visit our website for the full report.

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 3

COVID-19 Update

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 4

SA now ranks within the top 5 on COVID-19 cases, though deaths remain

comparatively low

# Cases Deaths

0 50000 100000 150000 200000

1 USA 4 170 333 147 342

2 Brazil 2 289 951 84 207

3 India 1 292 209 30 660

4 Russia 800 849 13 046

5 South Africa 408 052 6 093

6 Peru 371 096 17 654

7 Mexico 370 712 41 908

8 Chile 338 759 8 838 637 231 globally

9 Spain 317 246

15 685 177 globally +6% vs. last week

28 429

+11% vs. vs last week

10 UK 297 146 45 554

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 5

https://www.worldometers.info/coronavirus/#countries 24th July 2020

South Africa has >400k cases of COVID-19 and deaths have surpassed 6,000.

Gauteng has the most cases and is in the middle of peak

Source (22th July 2020):

https://sacoronavirus.co.za/2020/07/21/update-on-covid-19-21st-july-2020/ © 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 6

https://www.news24.com/news24/southafrica/investigations/infographics-gautengs-done-more-covid-19-tests-than-any-province-is-that-why-it-has-more-cases-20200712

SA COVID-19 Timeline

Jan 30 WHO declares global health emergency

Mar 5 First South African tests positive for Coronavirus

Mar 15 Ramaphosa declares a National State of Disaster

Mar 26 Global cases: 500k Mar 26 Start of SA lockdown. Liquor and tobacco banned

Mar 27 First death in South Africa SA spent 35

Apr 2 Global cases: 1 million

days in

Apr 10 SA lockdown extended

level 5

Apr 27 Global cases: 3 million

lockdown SA spent

May 1 SA lockdown level 4 begins

31 days

May 14 All online retail sales open (excl Liquor & Tobacco)

in level 4

Apr 27 Global cases: 5 million

SA has spent

Jun 1 SA lockdown level 3 begins; alcohol sale unbanned

54 days in

Jun 81 SA records 50k cases

Jun 22 SA records 100k cases level 3 (to date)

Jun 27 Global cases: 10 million; deaths: 500k

Jul 6 SA records 200k cases

Jul 12 SA alcohol ban announced with immediate effect

Jul 21 Global cases: 15 million

Jul 23 SA records 400k cases

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 7

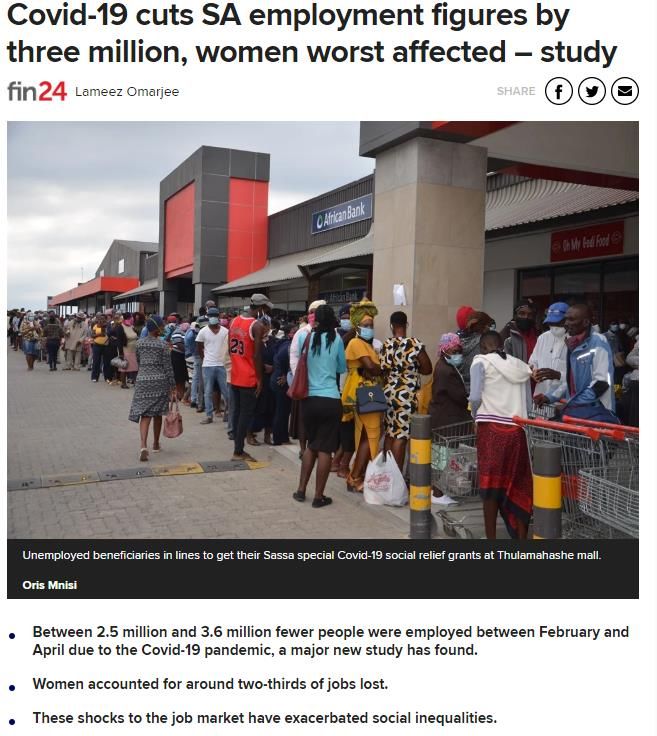

Lockdown related job losses have been significant, however online job ads are

slowly recovering. The tourism industry remains restricted in the short term

https://www.businessinsider.co.za/job-ads-south-africa-2020-7

https://www.businessinsider.co.za/when-will-foreign-tourism-local-leisure-travel-be-allowed-2020-7

https://www.news24.com/fin24/economy/covid-19-cuts-sa-employment-figures-by-three-million-women-worst-affected-study-20200715

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 8

The alcohol ban and new curfew rules have significantly impacted the restaurant

industry, with many participating in a peaceful protest on Wed the 22nd of July

https://www.dailymaveric

k.co.za/article/2020-07-

22-restaurants-and-

taverns-collapse-

hospitality-industry-

desperate-to-stave-off-

disaster/#gsc.tab=0

https://www.businessinsi

der.co.za/see-

restaurant-workers-

across-sa-take-to-the-

streets-to-protest-

lockdown-stranglehold-

2020-7

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 9

Despite the tobacco ban, South Africans continue to smoke…at a premium

Price per Pack

R31 R114 to R300

(pre-lockdown) (during lockdown)

30% of respondents tried to quit

• 56% said it was due the soaring prices

• Only 11% tried to quit due to the sales ban itself

• More than 70% of smokers who quit did so during Level 5 Lockdown

• More than a quarter of people who quit during lockdown indicated that

they would start smoking again after the sales ban is lifted

Of the respondents who continued smoking:

• 93% indicated that they had been able to purchase cigarettes through

informal channels, such as friends and family (27%), spaza shops

(25%), street vendors (11%) and WhatsApp groups (8%)

• The daily consumption of cigarettes decreased from 16.4 cigarettes

pre-lockdown to 13.1 cigarettes in June 2020

• Half of the respondents smoked less during lockdown than before

*The research was conducted by the Research Unit on the Economics of Excisable Products

(REEP), an independent research unit based at UCT and was based on >23,000 respondents, lockdown, 15% smoked more, and 35% smoked the same amount

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 10Multinationals have been the biggest losers during lockdown and as a result, may

enter into a price war to make quick gains after the ban is lifted

The Cigarette industry’s landscape will be changed forever

“Markets have been captured by local companies and, to a lesser extent, by imported

cigarettes, significantly reducing their market share. The prediction is that, once the

sales ban is lifted, there will be a price war, in which the multinationals will aim to get

some of their market share back and the non-multinational companies will aim to hold

on to their markets.

A permanent increase in the excise tax would encourage quitters to remain non-

smokers. Of course, critics of higher excise taxes would say that it encourages illicit

trade. The evidence, in South Africa and elsewhere, has shown that illicit trade is less a

tax problem, and more an enforcement problem.”

Ironically, this will lead to lower prices, making it a lot cheaper to smoke, pushing

sales. Government’s stated goal of keeping South Africans healthy, and

encouraging them to quit smoking could be undone

https://businesstech.co.za/news/lifestyle/418429/south-africas-cigarette-ban-could-backfire-spectacularly-research/

https://www.bizcommunity.com/Article/196/168/206473.html

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 11Latest Category

Performance

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 12Declines continue into the latest week and overall value growth is slowing

Total Edible & Non-Edible Groceries (incl. Liquor)

Weekly Actual Value sales

Lockdown growth vs. YA: +5.6%

22/03/2020 29/03/2020 05/04/2020 12/04/2020 19/04/2020 26/04/2020 03/05/2020 10/05/2020 17/05/2020 24/05/2020 31/05/2020 07/06/2020 14/06/2020 21/06/2020 28/06/2020 2020-07-05 2020-07-12 2020-07-19

Last Yr This Yr Poly. (This Yr)

Panic

Lockdown Level 5 Lockdown Level 4 Lockdown Level 3

Buying

Liquor Included Liquor Excluded Liquor Included Liquor Excluded

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 13Edible Groceries – staples continue to grow but Canned Cood, Fresh Meat and Maize

declined over the latest week

March April May June Jun28th Jul 05th Jul 12th Jul 19th

Baking Ingredients Baking Ingredients

Ice Cream Ice Cream

Wheat Flour Wheat Flour % Value

Edible Groceries

Yoghurt Yoghurt

Biscuits Biscuits

growth vs. YA

Frozen Veg/Potato Frozen Veg/Potato

Spices & Seasoning Spices & Seasoning Scale:

Condiments & Sauces Condiments & Sauces

Cheese >100

Cheese

Dry Pasta Dry Pasta 70 to 100

Snacks Snacks

50 to 70

Sugars & Sweetners Sugars & Sweetners

Spreads Spreads 30 to 50

Cereals Cereals 11 to 30

Oil Oil

0 to 10

Canned Food Canned Food

Confectionery Confectionery -10 to 0

Soup & Stock Soup & Stock -30 to -10

Fresh Meat Fresh Meat

-30 to -50

Bread Bread

Frozen Meats Frozen Meats < -50

Rice Rice

Maize Maize

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary.

© 2020 14 Inc. (IRI).

Information Resources

Confidential and Proprietary.Shoppers continue to purchase Soaps and Sanitizers and stock up on Vitamins and

medication for winter. Juice and CSD’s continue to struggle throughout July

March April May June Jun28th Jul 05th Jul 12th Jul 19th

Soaps & Sanitiser Soaps & Sanitiser

% Value growth vs.

Household Cleaning Household Cleaning YA

Non-Edibles

Wipes Wipes

Scale:

Personal Care Personal Care

Toilet Paper Toilet Paper >100

70 to 100

Oral Care Oral Care

50 to 70

Vitamins Vitamins

30 to 50

Medicinal Medicinal

11 to 30

Pet Pet

0 to 10

-10 to 0

-30 to -10

-30 to -50

March April May June Jun28th Jul 05th Jul 12th Jul 19th

Beverages

< -50

Milk Milk

Coffee & Tea Coffee & Tea

Juice Juice

CSDs & Water CSDs & Water

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 15Spreads moves up on the ranking as most schools returned last week.

Consumers purchase baking/indulgent products again, similar to trends in May

Top Value Growth Categories vs. Year Ago by Week

Latest 9 weeks of Lockdown

May 24th May 31st Jun 7th Jun14th Jun21st Jun28th Jul 05th Jul 12th Jul 19th

Baking Ingredients Baking Ingredients Spirits Spirits Soaps & Sanitiser Vitamins Vitamins Wheat Flour Vitamins

Ice Cream Ice Cream Wine Wine Baking Ingredients Baking Ingredients Soaps & Sanitiser Rice Soaps & Sanitiser

Wheat Flour Soaps & Sanitiser FABs Soaps & Sanitiser Household Cleaning Soaps & Sanitiser Dry Pasta Soaps & Sanitiser Baking Ingredients

Soaps & Sanitiser Wheat Flour Ice Cream Household Cleaning Dry Pasta Biscuits Medicinal Vitamins Spreads

Sugars & Sweetners Yoghurt Beer Coffee & Tea Wheat Flour Cheese Frozen Veg/Potato Wipes Medicinal

Biscuits Biscuits Soaps & Sanitiser Wheat Flour Frozen Veg/Potato Dry Pasta Cheese Oil Wheat Flour

Yoghurt Frozen Veg/Potato Yoghurt Yoghurt Spices & Seasoning Oil Spreads Frozen Meats Dry Pasta

Snacks Spices & Seasoning Wheat Flour Dry Pasta Cheese Medicinal Oil Soup & Stock Coffee & Tea

Spices & Seasoning Condiments & Sauces Baking Ingredients Oil Spreads Sugars & Sweetners Spices & Seasoning Yoghurt Sugars & Sweetners

Confectionery Cheese Sugars & Sweetners Frozen Meats Frozen Meats Spreads Condiments & Sauces Dry Pasta Frozen Veg/Potato

Non-Edible Baking/Indulgent Edible Groceries Liquor

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 16Beauty Update

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 17The Beauty industry is struggling globally, especially Cosmetics & Fragrance

• In France, demand for beauty care products remains lower than

last year

• In Italy, there is lower demand for perfumery, make-up &

body care vs. previous year

• Overall Beauty is growing in the US, driven by Personal

Cleansing and Hair Care, but Cosmetics & Fragrance are seeing

declines

• In the Netherlands, demand for Face & Body Care, as well as

Fragrance are starting to see growth, but Hair & Beauty

Accessories continue to decline

• Demand for Cosmetics & Fragrance has dropped in the UK

• Fragrance is seeing the biggest decline of all Non-Edible

categories in Spain

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 18Face Care and Hair Care’s initial strong lockdown growth slowed after salons re-

opened, but has remained ahead of pre-lockdown levels

Value Growth vs LY

Cosmetics Haircare Face care

Value Trend Pre-Lockdown -6% 7% 16%

Cosmetics Haircare Face care Lockdown Pre Salons Open -15% 20% 21%

Lockdown Post Salons Open -28% 11% 11%

Lockdown starts

Beauty categories reopen

Salons reopen

A South African retailer

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 19Compulsory masks in SA have driven the cosmetics market towards Eye make up,

which now accounts for 22% of the category with Lip dropping to 8%

35% 35% 34%

10% 11% 11%

24% 25% 25%

12% 11% 8%

19% 18% 22%

2019 2020 Pre Lockdown 2020 Post Lockdown

Eyes Lips Unspecified Nails Face

A South African retailer

https://labusinessjournal.com/news/2020/jul/06/lipstick-sales-fall-when-mask-use-surges/ © 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 20Liquor’s Six Week Respite

Performance and the impact on Non-Alcoholic

Beverages

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 21After 7 weeks of trading, Liquor was banned again on Sunday 12 July 2020

https://www.news24.com/news24/southafrica/news/happiness-levels-in-sa-

took-a-dive-after-alcohol-ban-reimposed-study-20200720

https://www.businessinsider.co.za/the-lockdown-alcohol-options-government-

ignored-2020-7

https://www.thesouthafrican.com/news/new-alcohol-ban-when-effective-july-

2020/

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 22Total Liquor recorded 9% growth in value vs. YA during the 6 weeks of sales,

mainly driven by the first two weeks of stock up

6Wk Alcohol Sales Period Jun 7th Jun14th Jun21st Jun28th Jul 05th Jul 12th Jul 19th % Value growth vs.

Wine YA

Beer Scale:

FABs

>100

Spirits

70 to 100

50 to 70

30 to 50

11 to 30

6Wk Alcohol Sales Period Jun 7th Jun14th Jun21st Jun28th Jul 05th Jul 12th Jul 19th 0 to 10

Rum -10 to 0

Gin -30 to -10

Other Spirits -30 to -50

Whisky < -50

Brandy

Vodka

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 23Sales amongst LSM 1-6 was 7% lower vs. YA, whereas LSM 7-10’s spend was up

15% vs. YA, driven by the growth in the initial stock up period

Liquor Value share of Total Grocery Spend (excl. Tobacco)

LSM 1 - 6 LSM 7 - 10

10,0 10,0 9,9

8,5

7,8

6,8

5,7 5,6 5,6 5,3

5,1 4,6 4,9 4,9

Full Period 07/06/2020 14/06/2020 21/06/2020 28/06/2020 05/07/2020 12/07/2020

Total Growth: +0.95%

Grwth vs YA

LSM 1-6 -7% +48% +1% -16% -41% -23% -6%

LSM 7-10 +15% +94% +49% -3% -32% -9% -4%

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 24Wine is the only category to show growth among both LSM groups and gained

share at the expense of Beer

Value Share of Total Liquor Value Growth % YA

6 weeks to 12/07/2020 6 weeks to 12/07/2020 LSM 1-6

LSM 7-10

LSM 1-6 LSM 7-10

Total Liquor

13 12

17 16

Fabs Fabs

40 43

42 42 Spirits Spirits

22 19 Beer Beer

28 26

25 27 Wine

16 Wine

13

Last Year This Year Last Year This Year

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 25Strong wine growth was driven by low priced Boxed Wine, while Beer sales suffered

due to price increases. Large packs were popular

Top 15 items in terms of value sales by category over the 6 weeks of Alcohol Sales

WINE BEER

• Of the top 15 Wine items, 13 were Box Wine (vs. 11 last yr) • Of the top 15 Beer items, 9 were larger pack sizes of

• 7 of the Box Wine items had price deflation vs. last year 500ML or more (vs. 6 LY)

• Comparatively; bottled wine had high price inflation with • After several years of flat / low inflation, 8 Items saw

many items seeing price increases >10% price increases of more than 10% vs. last year

– Of these, 4 had inflation >20%

SPIRITS FABs

• Of the top 15 items, 5 were Gin items (vs. 3 LY) • Similarly to Beer, 5 of the top 15 items were 500ML

or bigger vs. only 2 last year

• 9 items saw inflation below 10%

• 4 Items saw price inflation greater than 10%

– Of these, 2 had inflation >20%

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 26The six week gap of Liquor sales provided some relief to manufacturers

and retailers, mainly due to the initial Liquor cabinet re-stocking

• The initial two stock up weeks was the primary driver of growth over the sales period.

During the last four weeks, sales were declining, with the exception of ever popular

Gin

• Liquor was flat in value at 0.95% growth over the 6 week sales period. This

constrained growth was driven by cash-strapped LSM 1-6 and the lack of social

occasions

• Wine was the only category to show growth among both LSM groups and gained

share at the expense of Beer

– Growth was as a result of inflation in Beer, after several years of flat/low inflation

– Box Wine had low/no inflation, whereas Bottled Wine prices increased by well

over 10%

• Large packs were popular during this period as thirst quenchers and the attractive

prices per litre

• Liquor had stronger performance over lockdown vs. YA in UK, AU and NZ than in SA.

Cash-strapped customers in SA didn’t get an opportunity to re-stock their liquor

cabinets before the 2nd ban

• What has the impact been on Non-Alcoholic Beverages?

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 27Shoppers have switched to Non-Alcoholic Beverages during the Liquor bans to get

their taste fix

Sales are up 17% for the YTD 2020 vs YA

Total Non-Alcoholic Beverages

-7% vs. YA -45% vs. YA 139% vs. YA -27% vs. YA 89%

vs. YA

301

221

Stock Issues/Confusion over ban

89

38 43

-8 -7 -10 -11

-30 -23 -29 -33 -22

-53 -49 -49

-69

03/22/20 03/29/20 04/05/20 04/12/20 04/19/20 04/26/20 05/03/20 05/10/20 05/17/20 05/24/20 05/31/20 06/07/20 06/14/20 06/21/20 06/28/20 07/05/20 07/12/20 07/19/20

Panic

Lockdown Level 5 Lockdown Level 4 Lockdown Level 3 LL 3.2

Buying

Alcohol Sales Banned

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 28Notable spikes in Non-Alcoholic Beer (NAB) and Cider sales during Level 4 and

Level 3.2

Lifting of the alcohol ban in Level 3(.1) saw a decline in sales of NAB (compared to pre-lockdown levels). With socialising not

allowed and eating out limited, the occasions for these drinks was missing

While the category faced some challenges this year, it is still on a growth trajectory. Although growth is slowing vs. last year

(95% vs. 2018; driven by NPD), the ongoing alcohol ban may cause further sales increases in the second part of this year.

NonAlcoholic Beer NonAlcoholic Cider NonAlcoholic G&T NonAlcoholic Wine

Alcohol Sales Allowed

Stock Issues

01/05/20

01/12/20

01/19/20

01/26/20

02/02/20

02/09/20

02/16/20

02/23/20

03/01/20

03/08/20

03/15/20

03/22/20

03/29/20

04/05/20

04/12/20

04/19/20

04/26/20

05/03/20

05/10/20

05/17/20

05/24/20

05/31/20

06/07/20

06/14/20

06/21/20

06/28/20

07/05/20

07/12/20

07/19/20

Lockdown Level 5 Lockdown Level 4 Lockdown Level 3 LL 3.2

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 29Changing the Approach to

Retailer and Brand Loyalty

IRI UK Whitepaper: COVID-19 edition

For the full article go to our website

https://www.iriworldwide.com/en-sa/insights/publications/changing-the-approach-to-brand-and-retailer-loyalt

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 30Is Loyalty still a reasonable expectation, given the even more challenging state of

the retail industry?

During a period of high emotion and uncertainty, our interactions with brands and retailers

will have either reinforced or challenged some of our existing beliefs.

Aspects of the shopping experience that had perhaps been previously overlooked.

• For example, in store safety;

– How quick were retailers to implement social distancing?

– How safe do I feel in-store?

– Are shopper numbers controlled within the store? This thought pattern can then extend further to contemplate corporate responsibility:

how are staff being looked after?

– How are they promoting their brand through media during these complex times?

– What changes to their advertising approach have I noticed?

• Then there are more practical considerations that consumers won’t have needed to consider before when making a brand choice:

– I used to shop en route to work but which shop is closest to home now? How long is the wait to enter the supermarket?

– What are stock levels like? What if they don’t have what I need, I don’t want to make multiple trips?

– Has my financial situation changed and therefore can I still afford to shop at the same places?

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 31Many shoppers have been forced to shop in new ways and via channels that could be completely

new. This creates an opportunity to convert brand sightseers into lifelong shoppers of value

Make an emotional connection Changing product ranges would

with your customers have impacted our choices

• Feeding the family is a bigger thought process than ever • Many range decisions were made in an emergency to

before maintain availability

• Make sure shoppers understand how the retailers are • As we stabilise, a broader, more flexible range will become

working for the safety and benefit of staff & the public more important

• Greater transparency from retailers and manufacturers will • IRI anticipates the rate of innovation to return to pre-

help to drive trust and a deeper connection that will build COVID-19 levels, as retailers and suppliers look to maintain

loyalty for the coming months and years share and deliver against emerging shopper needs, while

offering a flow of new and exciting products

• Example: In SA, customers noted less promotions, however, • However, the innovation launch model and criteria for

the number of weeks on promotion are similar or higher in success will need to change

half of the categories analysed during lockdown – A customer pull rather than a manufacturer led push

– Promotions were pulled back to curtail bulk buying and strategy will be necessary. With shoppers reluctant to

maintain availability for customers. Explaining this dwell in store browsing aisles, innovation must meet a

rationale to customers could avoid distrust clear need and be compelling to grab attention

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 32Simply measuring customer loyalty is not enough. Retailers can take their

understanding further and change, influence and predict customer behaviour

The 6 levers of targeted marketing

Upsell

Second

RevenueStep

Loss Cross Fourth Step

There are many in variations Sell There are many in

Management Fourth Step Reward & Retention

Churn

First Step passage of lorem ipsum Third Step variations passage of lorem

Management

There are many in available but the majority There

Therearearemany

many inin

Upsell ipsum available~but the

variations passage of lorem slightly variations

variationspassage

passageof oflorem

lorem Brand

majorityCategory

ipsum available but

ipsum available but the the Penetration

slightly

ipsum available but the

majority

majority

majority

slightly

slightly

slightlywho have the

Identify customers The target here is to identify and Identify and target the customers

potential to stop shopping with us target the customers that are highly that we want to maintain in order to

Identify customers with a trend of Identify customers with a propensity

based on historic behaviour. likely to buy more expensive products maximize their lifetime value.

spend reduction at a basket or to buy in additional categories

from the same category and therefore

category level. based on lookalike behaviours. Group customers based on their

Create a bespoke ‘churn flag’ increase the value of the basket

spend and frequency.

Recommend the best Personalised Incentivize customers to purchase in

Provide recommendations based on

offers to re-gain share of wallet ADDITONAL categories with Recommendations are based on

their previous shopping patterns.

(basket level and product specific) Personalized product offers preferred items.

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 33The ability to quickly respond and pre-empt customer behavior is

what sets the industry leaders apart from the rest

In Conclusion

• Shoppers are reassessing where to shop and what to buy as they attempt to navigate

through this continued uncertainty

• Throughout the lockdown period, consumers have made significant changes to their

shopping behaviour and as restrictions are eased, how we adapt will differ across

households. Our responses will be individual. Because of that, arguably what we thought

we knew about shoppers is brought into question and it is vital for retailers and brands to

connect with the changing needs of their shoppers

• At IRI, we help some of the world's most successful retailers and brand owners to navigate

this data at speed using IRI’s Liquid Data™ Platform. FMCG businesses have fast access

to the insights allowing decision-makers to take instant tactical action, as well as plan more

strategically to improve profit and growth for their business

For the full article go to

our website For the full article go to our website

https://www.iriworldwide.com/en-sa/insights/publications/changing-the-approach-to-brand-and-

retailer-loyalt

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 34Growths from around the Globe

Global data up to 12 July 2020

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 35IRI COVID-19 Dashboard Menu Link

Go to our website for more detail →

Latest insights from the IRI Demand Index and IRI Inflation Tracker include:

• In the UK, France, Germany and the Netherlands, consumer demand in CPG remains elevated for total CPG compared to a year ago. In Italy, demand has

remained stable for the past week compared to last year.

• In the UK, Netherlands and Germany demand for grocery is outpacing non-edible, while in France and Italy, non-edible is growing more than edible. In

Germany, demand for non-edible is decreasing, driven by lower demand for hygiene products, cosmetics/body care products and laundry detergents.

• Each country indicates different category trends in edible but figures overall suggest demand is slowing down as we begin to return to some kind of normality. In

the UK, demand is ahead of last year for beers, wines & spirits, fresh meat and frozen although sales growth is down, while in France frozen, alcohol and beverages

are down versus a year ago but up week on week. In Italy, every category saw demand slow down compared to a year ago, dropping into negative except for

packaged food.

• Other highlights in consumer demand for non-edible categories are beauty care products in France, which remain lower than last year, and in Italy where there

is lower demand for perfumery, make-up and body care versus the previous year. In the Netherlands demand for facial and body care is back to growth.

• Prices continue to increase in all these countries. The UK being the country with the highest inflation. In the Netherlands, the UK and France, alcoholic

beverages are leading price increases. Frozen food also has strong inflation in Italy and the UK (with a peak in the country on ice creams/frozen desserts).

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 36© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 37

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 38

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 39

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 40

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 41

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 42

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 43

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 44

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 45

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 46

Insights and Strategic

Guidance for Better Decisions

IRI’s Online Resources Include Real-Time

Updates and Weekly Reports Which Track

the Impact of the Virus on CPG and Retail

The IRI COVID-19 Info Portal

Includes COVID-19 impact analyses, dashboards

and the latest thought leadership on supply chain,

consumer behavior, channel shifts for the U.S.

AND international markets

The COVID-19 Dashboard and

The IRI CPG Demand Index™

Accessible through the insights portal

and tracks the daily impact of COVID-19.

This includes the new IRI CPG Demand

Index™, top selling and out of stock

categories across countries, and

consumer sentiment on social media.

© 2020 Information Resources Inc. (IRI). Confidential and Proprietary. 47CONTACT US IRI South Africa

Level 1, Block D, Aintree Park

FOR MORE Doncaster Road, Kenilworth

Cape Town, 7708

INFORMATION +27 21 700 7420

Follow IRI on Twitter: @IRIworldwide

© 2020 Information Resources Inc. (IRI).

© 2020 Information Resources Inc. (IRI). Confidential

Confidential and

and Proprietary.

Proprietary. 48 48You can also read