The Benchmark Wealth It's a Feeling - Absa Stockbrokers

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Benchmark

Absa Wealth Management April, 2018

Wealth

It’s a Feeling.

Special Features

Monetary Policy:

Curiouser and curiouser

South AfricaThe Most

Unequal Country In The

World

Wealth Trends

The 2018 Knight Frank

Wealth Report

Contents

Winston’s Word 2

House View 3

Monetary Policy: Curiouser and curiouser 10

South AfricaThe Most Unequal Country In The 12

World

Fiduciary Focus 14

Focus on Philanthropy 16

Wealth Trends 18

News Roundup 20

What did The Economist Say 21

Fund Performance 24

Smarty Boxes 26

Disclaimer 30

Winston’s Word

We catch up on the events currently shaping the global economy, at a

challenging time.

There is more evidence that South Africa The economy grew by 1.3% in 2017

is on an improved growth path. Hot on compared with a revised 0.6% in 2016, as

the heels of Moody’s’ decision to keep the reported by Statistics South Africa

sovereign credit rating unchanged at one (StatsSA) on 06 March 2018.

notch above junk, fellow ratings agency

Standard & Poor’s (S&P) raised its gross What these numbers demonstrate is an

domestic product (GDP) growth forecast economy on the mend. Even the official

for South Africa to 2% for 2018, from 1% unemployment rate has eased,

previously. It also revised its forecast for decreasing to 26.7% in the fourth quarter

2019 up to 2.1%, from 1.7% before. of 2017 from 27.7% in the previous

period. In spite of this however, the

Both these decisions are due to improved country remains highly unequal as the

investor sentiment following the positive World Bank recently reported – read more

political changes that led to the swearing on its findings’ in the “South Africa, The

in of Cyril Ramaphosa as the country’s Most Unequal Country in the World”

new president. A more favorable inflation feature. We also feature the “2018 Knight Winston Monale

outlook has also given the South African Frank Wealth Report” which sees South Managing Executive, Wealth

Reserve Bank (SARB) room to ease Africa’s ultra-wealthy (people with US$50 Management: Africa

monetary policy, and that is exactly what million or more in net assets) growing by

the Monetary Policy Committee 20% over the next five years following a

(MPC) did, cutting the repo rate by 25 14% rise in 2017.

basis points to 6.5% and the prime

lending rate to 10%. The last time the All of this and more in this month’s

central bank cut the repo rate was in July edition of The Benchmark. Enjoy.

2017 in a surprise move that left the rand

on the back foot. Back then, SARB

Governor, Lesetja Kganyago stated that

inflation remained a risk amid a

deteriorating economic growth outlook.

Since then, the domestic economy has

recovered some ground, growing by 3.1%

between October and December 2017,

the highest rate since the second quarter

of 2016, after expanding by a revised

2.3% in the third quarter.

House View

Local Economic and Market Outlook

Local Macroeconomic Outlook Local Market Outlook

GDP Outlook Bonds

South Africa’s real gross domestic In recent months, rand denominated

product (GDP) surprised on the upside in bonds have enjoyed good support from a

the fourth quarter of 2017, registering an resilient rand and renewed optimism

economic growth figure of 1.3% year-on- regarding the growth outlook of the

year, which is 0.4% points higher than South African economy. Fiscal

consensus estimates. consolidation measures and the decision

by rating agency Moody’s to leave the

Recent growth drivers have reflected local credit rating unchanged at one notch

more of a cyclical recovery than a lasting above investment grade with a stable

uptrend. The notable growth in the outlook momentarily lowered the risk

Keorapetse Leballo

agricultural sector mainly from subsiding premium attached to these securities.

Investment Strategist, GI&S

draught effects is expected to moderate

as the shock becomes fully absorbed in Looking ahead, we envisage limited room

forthcoming GDP prints. for further yield compression on the back

of: twin deficits from the fiscal and

The recent rally of the rand is also current balances; a negative output gap;

forecast to weaken mining industry and low corporate profitability levels that

production levels and anchor trade will likely induce benign capital spending

deficits over the next few quarters to and higher costs of servicing debt. Our

come. Fiscal consolidation measures weaker outlook for the rand and a pick-up

announced in the previous budget in inflation rates from current levels also

statement infer subdued government suggests a tactical overweight in inflation-

spending that is likely to reduce the linked bonds over the next 12 months.

recent GDP growth momentum.

Listed Property

We look towards improved business and We have marginally reduced our exposure

consumer confidence figures, to local property in an attempt to take Ricardo Smith

expansionary Purchasing Manager’s some currency risk off the table. This Investment Strategist, GI&S

Indices and an up-tick in global economic asset class is rapidly increasing its

activity to bolster local economic activity offshore earnings exposure, thereby

over the next two years. To this end, we inducing multiple layers of rand-hedge

have marginally revised our previous GDP attributes which we are already obtaining

forecasts from 1.4 percent to 1.6 percent from our offshore equity and local high

in 2018 and from 1.7 percent to 1.8 cap equity allocations.

percent in 2019. Considering that this asset class has

recently dipped, we still hold some

Inflation Outlook allocation that will allow us to participate

On the 28th of March 2018, the South on the upside in the event that prices of

African Reserve Bank’s (SARB) Monetary these counters re-rate at higher levels.

Policy Committee (MPC) announced their Interest rate geared earnings and

decision to cut the repo rate by 25 basis- currency-hedged growth continues to

points. The MPC’s decision comes on the justify a cautious yet long SA REIT

back of: an improved inflation outlook; an position within the asset allocation

over-valued currency; and low demand portfolios.

pull inflationary threats stemming from

decreasing household credit extensions.

House View

Global Economic Outlook

Equities to declare a breakout in employee

Valuations in the equity market appear compensation. Furthermore, historic

stretched in the absence of a strong trends reveal that transition from higher

earnings catalyst in maintaining the 2017 employee compensation into actual

rally of the All Share index. Lofty price economy-wide inflation is itself a slow and

earnings multiples are expected to non-linear process.

continue exerting downward pressure on

dividend growth rates, while the volatility Any reduction in the unemployment rate

of the rand remains set to threaten below the current 4 percent is likely to

foreign earnings on rand-hedged counters translate in hyper-inflationary threats that

in the short term. would force the Federal Open Market

Committee (FOMC) to raise interest rates

Increasing global inflationary pressures sharply. Nonetheless, inflationary

conversely point toward renewed tailwinds should slowly gather in the

weaknesses in the value of the rand coming years, amidst increasing

which is expected to bode well for economic activity.

counters with foreign earnings exposure

over the next 12 to 18 months. Euro area

Furthermore, improved global economic The Eurozone economy enjoyed a broad-

prospects are also expected to contribute based recovery last year, with

positively to the medium term return consumption boosted by rising Increasing global

outlook of this asset class. employment. Some of this growth has inflationary pressures

eased, as evidenced by the latest conversely point toward

We recommend shorting financials in Eurozone PMI Composite and renewed weaknesses in

favour of consumer staples on the back of Manufacturing indices. the value of the rand

increasing risk premiums and low which is expected to

household credit extensions. Given rising However, in-spite of the recent short- bode well for counters

inflationary headwinds and moderating term decline in these indices, they remain with foreign earnings

dividend growth rates, we are currently at historically elevated levels, and they

exposure over the next

pricing in a real return outlook that is continue to signal robust growth ahead

12 to 18 months.

much softer than that of the previous for the Eurozone. We forecast the Euro

year. area’s economy to expand by 2.2% year-

on-year and 2.0% year-on-year in 2018

Global Economic Outlook and 2019 respectively.

United States Asia

The latest US wage data surprised With cyclical indicators continuing to

economists to the upside triggering a trend upwards, prospects for the

bout of inflation optimism amongst Japanese economy remain positive. A

market participants. However, the upside more favourable domestic and external

came mainly from a minority subset of economic backdrop has made us more

the sampled workforce, supervisory positive about the trajectory of Japanese

employees, whose wage growth tends to corporate profits. Dividend payout ratios

be volatile. Excluding this group, gains are also on a steady upward trend – a

were more muted, in line with previous nascent sign that government reforms to

trends. alter corporate behaviour and improve

shareholder returns may be starting to

Wage gains would need to broaden bear fruit.

materially over the coming months for us

4House View

Global Market Outlook

While Japan has managed to pull itself out portfolios. This ultimately means that an

of sustained deflation, core inflation still investor looking to grow assets above

remains well below the Bank of Japan’s 2 inflation will have to accept an investment

percent target. We therefore see no portfolio that will be reasonably correlated

change to the Bank of Japan’s to equity markets over time.

accommodative stance as we move into

2018. We also expect Japanese fiscal

policy to continue to support economic

growth.

Global Market Outlook

The bond market, which until six months

ago seemed vulnerable to the threat of

deflation, now looks better equipped to

handle the reality of more rate hikes.

Yields across all maturities likely have

further to rise still; an era of low yields

seems to be coming to an end.

Furthermore the period of calm enjoyed

As with all such

by markets since last year was finally moments, investors can

shattered in February, with global stock take a while to find their

markets experiencing a sharp pullback. feet as perceived norms

The health of the global economy and the are inverted.

resulting corporate profitability, however,

remain positive for global stock markets.

As with all such moments, investors can

take a while to find their feet as perceived

norms are inverted. However, with the

prospects for economic growth still

looking firm, and signs of overheating still

substantially absent, equities continue to

offer the most attractive returns.

Valuations are high in the US stock

market, but more normal elsewhere. Even

assuming some medium-term headwind

from valuations, the excess returns

available from stocks look attractive in a

strategic context relative to high-quality

bonds. Equity still offers attractive long-

term, risk-adjusted returns.

Although equity markets are not the only

source of investor returns, it is stocks that

are going to provide the bulk of the long-

term returns and volatility to investmentHouse View

Economic Summaries

Local Global

Growth The economy of South Africa is likely to Prospects for the world economy seem a bit

expand at less than full potential over the brighter over the next two years, as evidenced

next two years. Sub-investment ratings, a by a pickup in leading economic indicators

volatile currency and poor corporate across major world economies. However,

profitability levels, are expected to increase fiscal policy uncertainties and low household

the cost of servicing debt, where companies consumption rates continue to threaten the

will be forced to either cut capital spending, medium term global economic outlook. Global

undergo debt stress or reduce labour force. economic activity is now forecast to expand

We therefore expect unemployment rates to by 4.0% and 3.8% over the next two years

remain stubbornly above 25% over the respectively.

foreseeable future.

Inflation Challenges to CPI moderation or even a low Notwithstanding historically low

and stable inflation print continue to linger. unemployment rates, policy makers continue

These challenges stem from stubbornly high to remain concerned by weak demand

meat price inflation, increasing administered pressures which are forecast to anchor global

costs and pass through inflationary core inflation rates well below target.

headwinds from oil price normalisation. We Conversely, low US unemployment rates, a

therefore expect inflation to remain weak US dollar and renewed growth

uncomfortably range bound over the medium optimism and above target inflation rates

term, with strong upside limitations from currently infer restrictive Fed interest rate

benign consumption propensities. policy intervention over the short to medium

term.

Exchange Although the rand is still undervalued against A gradual removal of excess monetary supply

rates the dollar from a purchasing power parity and resilient economic conditions are set to

perspective, faltering growth and a high benefit G10 currencies relative to their

inflation differential with our trading partners, emerging market counterparts. Restrictive

make it unlikely for the currency to Fed policy is set to correct any short-term

strengthen above the ZAR10 level again. We devaluation of the US dollar, while an

are currently pricing in a rand depreciation increasing current account surplus in the euro

that is broadly in line with inflation area suggests a renewed appreciation in the

differentials between SA and G10 economies. euro against most G10 and emerging market

currencies.

6House View

House View Matrix

House view matrix

Asset Class View Rationale

SA Equities Neutral The absence of a strong earnings catalyst with a number of counters already

trading above fair value currently mutes short-term appetite. We favour rand

hedged stocks on the back of a correction in G10 currencies to improve the

medium term return outlook.

SA Property Bearish Interest rate geared earnings and currency-hedged growth continues to justify

a cautious yet long SA REIT position within the asset allocation portfolios. The

recent dip in performance and limited room in yield compression has led to the

marginal reduction in exposure to this asset class.

SA Bonds Neutral Weak economic activity and increasing inflation expectations favour a duration

neutral strategy. High budget deficits and growing threats a weaker rand

outlook is conversely prone to bid yields high in the medium term.

SA Cash Bullish The risk-reward profile of cash and short-term maturity bonds appears

fundamentally strong relative to other asset classes. We expect short-term

yields to appreciate slower than long term yields in response to currency and

macroeconomic risks.

Commodities Bearish US monetary policy normalisation and shifts from industrialisation to

consumption led economic policies in China are set to keep the commodity risk

premium unattractive for extended time periods. Increased exposure towards

energy commodities may be justified by planned production cuts.

DM Equities Neutral A strengthening dollar is expected to undermine US equity earnings while the

ongoing pick up in global inflation should lead to better pricing power and

attractive nominal returns for developed market equities. Long developed

market equities relative to emerging market counterparts.

DM Bonds Bearish Valuations indicate that these securities are currently trading at a significant

premium, where real returns appear to be particularly stretched on the back of

increasing inflation expectations.

DM Property Bearish Due to low diversification benefits, this asset class remains a tactical call as it

carries a high level of systematic risk relative to the DM equity index. Limited

room for yield compression anchors yet another reason we remain reluctant to

hold offshore REITS over the medium term.

Source: GI&S Africa, March 2018House View

Key Macroeconomic Projections

Economic Forecasts

Real GDP (%) Consumer prices (%)

2017E 2018F 2019F 2017E 2018F 2019F

Global 3.9 4.0 3.8 2.1 2.3 2.3

Advanced 2.1 2.1 1.8 1.8 1.8 1.8

Emerging 5.2 5.3 5.2 2.6 2.9 2.9

United States 2.2 2.3 1.9 2.1 2.2 2.0

Euro area 2.3 2.2 2.0 1.5 1.5 1.6

Japan 1.5 1.6 1.2 0.5 0.6 1.1

United Kingdom 1.5 1.3 1.3 2.7 2.4 2.2

China 6.8 6.4 6.2 1.6 2.2 2.0

Brazil 1.0 2.4 2.3 3.5 4.0 4.5

India 6.3 7.6 7.6 3.1 4.6 4.5

Russia 2.0 1.8 1.5 3.7 4.1 4.3

South Africa 1.3 1.6 1.8 4.7 5.2 5.3

Source: Barclays, GI&S Africa, Bloomberg March 2018

Currency Forecasts

Time USDZAR EURZAR GBPZAR

Spot 11.83 14.58 16.63

1 month 11.88 14.67 16.72

3 months 12.00 14.88 16.93

6 months 12.17 15.19 17.22

1 year 12.51 15.84 17.81

2 years 12.90 16.84 18.65

3 years 13.52 18.16 19.86

Source: GI&S Africa, Bloomberg, March 2018

8House View

Market Forecasts

Market Forecasts

2015 2016 2017 2018F 3 Yr. Ann F

South Africa – ZAR denominated

Equities – JSE All Share 5.1 2.6 21.0 8.2 10.4

Bonds – Beassa ALBI -3.9 15.4 10.2 7.4 6.2

Property – JSE SA Listed Property 8.0 10.2 17.2 6.2 8.3

Cash – STeFI Composite 6.5 7.4 7.6 6.3 6.9

Commodities – Bloomberg commodity 0.9 -1.4 -7.9 -2.1 0.3

Alternatives- ASISA SA MA Low Equity 7.6 3.6 8.4 7.3 6.5

Global market – Base currency

United States – S&P 500 1.4 12.0 21.8 8.7 9.1

United Kingdom – FTSE 100 -1.3 19.1 12.0 10.6 8.0

Europe – Euro Stoxx 50 7.3 4.7 10.1 6.9 9.0

Property – S&P Developed Property 0.9 5.4 13.2 3.1 4.6

Source: GI&S Africa, March 2018

Strategic Asset Allocation

High Medium Low

Local Equities 33.95% 26.25% 19.95%

Offshore Equities 24.25% 18.75% 14.25%

Local Property 8.87% 6.86% 5.21%

Offshore Property 0.00% 0.00% 0.00%

Local Bonds 11.73% 9.07% 6.89%

Offshore Bonds 0.00% 0.00% 0.00%

Commodities 0.00% 0.00% 0.00%

Alternatives 18.20% 14.07% 10.69%

Cash 3.00% 25.00% 43.00%

Source: GI&S Africa, March 2018Monetary Policy

Curiouser and curiouser

The decision of the Monetary Policy Committee (MPC) of the South African

Reserve Bank (SARB) to cut the repo rate by 25 basis points (bp) from

6.75% to 6.50% came as no surprise to the market.

Although the local interest rate market 2019 and 5,1% in 2020 with core

had almost fully priced in the rate cut and inflation (which excludes food, fuel and

consensus in the polls of information electricity) of 4,6% in 2018 and 4,9% in

providers such as Bloomberg and both 2019 and 2020.

Thomson Reuters were for lower rates,

the MPC outcome was never a foregone Very positively, inflation expectations

conclusion. The fact that four of the moderated in the first quarter of the year

committee’s seven members voted for and the SARB has always stressed the

more relaxed policy while three voted to importance of well-anchored inflation

retain the status quo, leads one to believe expectations. If inflation is expected to

that there was much to ponder and move higher then price setting behaviour Craig B Pheiffer

debate around the MPC table. Indeed if (on goods and labour) is self-fulfilling and Chief Investment Strategist,

Alice in Wonderland was in town and pushes inflation higher. While the SARB Absa Stockbrokers and Portfolio

peered at that table through her looking has a preference for inflation expectations Management

glass, she would not have been surprised to be anchored at the midpoint of the

by the final result but she may have cried target range at 4,5%, the improvement in

“curiouser and curiouser” at one or two of average expectations for 2018 of 5,2%

the assumptions and forecasts of the from 5,7% and for 2019 of 5,3% from

committee. 5,9% was welcomed. Average

expectations for inflation in 2020 were

The MPC’s revised inflation outlook was introduced at 5,4% while five-year

always going to take centre stage, as it inflation expectations reached their

should for an inflation-targeting central lowest point in the eight year history of

bank, but of particular interest was how the survey at 5,3%. The overall When all of the numbers

the SARB was going to assess the impact assessment of the MPC was that the risks had been crunched, the

of the VAT rate hike and the continued to the inflation forecast were more or less inflation outlook had

strength of the rand on the future path of evenly balanced. The rand was considered improved moderately

inflation. When all of the numbers had to be moderately overvalued but to pose although the MPC

been crunched, the inflation outlook had a lesser risk to the inflation outlook. admitted that the low

improved moderately although the MPC point in the inflation cycle

admitted that the low point in the As the King in “The King and I” might say,

had been reached in Q1

inflation cycle had been reached in Q1 none of this so far could be considered a

2018 at a forecast rate of

2018 at a forecast rate of 4,1%. This “puzzlement”. What is a bit “curiouser”

though is the link between the output of

4,1%.

implies that the 4,0% y/y increase

recorded in February was very likely the the SARB’s primary policy forecasting tool,

nadir for consumer price inflation. From the Quarterly Projection Model (“QPM”)

that low point, the SARB expects the next and actual policy. There is clearly a

peak in inflation to come in Q1 2019 at qualitative input to policy decisions that

5,5% and then soften again as the VAT the seven committee members provide

rate hike falls out of the base. The and the governor has been at pains to

increase in VAT is expected to add 0,6 explain that the MPC will not necessarily

percentage points to the inflation rate for slavishly or mechanistically follow the

the year following the rate hike to 15%. model’s directive. At recent meetings the

Overall, the SARB expects the headline QPM has been pointing to monetary

CPI to average 4,9% in 2018, 5,2% in policy tightening of between 50bp and

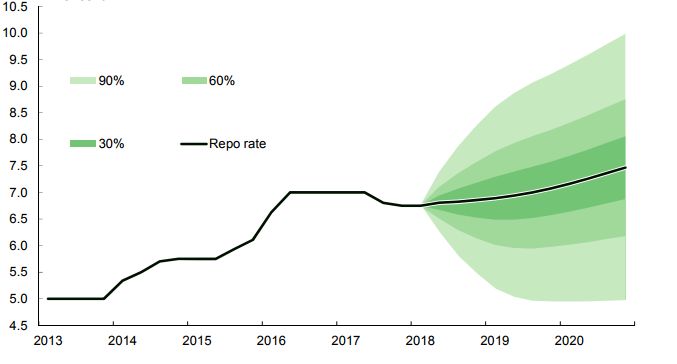

10Monetary Policy

Curiouser and curiouser

The SARB’s fan chart forecast of the repo rate (%) from the QPM

Source: SARB Interest Rate Forecast accompanying the MPC Statement of 28 March 2018

75bp by end-2019 and at the last Given the improving picture painted by possible. The SARB pegs its decisions on

meeting the policy path implied by the the SARB, the “stumble” in GDP growth in the latest available data and its two year

model was 25bp of tightening by end- 2019 is a little at odds with that positive outlook and oft times this is open to a

2019 and 50bp of tightening in 2020. The outlook. While the MPC acknowledged different interpretation by the market and

model does target the mid-point of the that risks to the growth forecasts were opens the door for some uncertainty

inflation target range but even so, the moderately to the upside, they did when the governor steps up to the

MPC policy outcome is in the opposite reiterate that sustained levels of higher podium to pronounce on policy.

direction to the model outcome. The growth would be dependent on sustained Nevertheless, South Africa is blessed with

SARB’s fan chart of the probable outcome levels of confidence, higher levels of an independent central bank that is

investment and real structural reforms by

of the repo rate reflects a rising trend over transparent and constantly evolving to be

the next few years yet the MPC saw fit to government. During the National Budget, even more open. Today we are privileged

reduce the repo rate in light of its the Finance Minister forecast annual GDP to have the SARB publish the economic

improved inflation outlook and the growth rates of 1,5%, 1,8% and 2,1% for assumptions that drive their thinking and

general reduction in inflation the next three respective years. This talks we also get to know how the MPC voting

expectations. to a little more of an even-paced recovery went down – all things we didn’t have

than the version envisaged by the SARB. before. Now we just have to figure out

Another bit of “puzzlement” is the SARB’s Time will tell who is right but at these how the QPM fits into it all.

forecast growth rates for the next few rates of growth South Africa won’t be

years. Factoring in greater confidence and able to make any dent into its hefty

a growing global economy, the SARB unemployment rate.

upped its domestic growth outlook for

2018 from 1,4% to 1,7% but cut its Most times the central bank would like

forecast for 2019 from 1,6% to 1,5%. For the market not to be surprised by its

2020 the central bank pencilled in growth policy decisions but with input variables

of 2,0%. changing by the minute, that’s not alwaysSouth AfricaThe Most Unequal Country In The

World

Since the dawn of democracy in 1994, Consumption growth

consumption inequality in South Africa South Africa also lags its peers on the

has been on the rise making the country inclusiveness of consumption growth.

one of the most unequal in the world, Inclusiveness in this case is examined by

according to the World Bank’s findings comparing the rate of consumption

detailed below. growth for the bottom 40% of the

population to that of comparator

Analysis of the distribution of countries as well as Sub-Saharan Africa

consumption expenditure per capita in and the world. The result: the bottom

the recent Living Conditions Survey 40% had consumption growth of 3.5%

2014/15 found that the country had a between 2006 and 2011, with a

Gini coefficient of 0.63 in 2015, the deceleration of 1.4% for the period

highest in the world and an increase since between 2011 and 2015. This does not

1994. Further analysis of consumption compare well with the median for the

expenditure trends provides evidence that world (3.9%) or, in the later period, with

Zukelwa Solomon

the very poor (those in the bottom 10%) Sub-Saharan Africa. South Africa’s BRICS

Collateral Writer, GI&S

grew at a slower pace than the rest of the partners (Brazil, Russia, and China) fare

population between 2006. better than South Africa in terms of

inclusiveness of growth.

12South AfricaThe Most Unequal Country In The

World

Wealth inequality The wages between the two extremes are opportunity in South Africa is high relative

Wealth inequality is also high and has highly unequal - those with highly paid to its comparators. This is further

been growing over time. The net wealth jobs earn nearly five times the average compounded by low intergenerational

inequality is even higher than wage in low skilled jobs, yet they mobility, which is an obstacle to

consumption inequality in South Africa, constitute less than a fifth of the total inequality reduction. Intergenerational

although there is strong correlation working population. Thus, while a mobility in South Africa is low in

between levels of inequality in segment of the population enjoys wages comparison to other countries indicating

consumption and wealth, with wealth that are on average equal to workers an enduring link between life outcomes

remaining an important source of long- living in developed economies, the wages for a given generation versus those of the

run inequality. Analysis of wealth of those at the lower end of the previous generation.

inequality based on data from four rounds distribution are comparable to those seen

of wealth surveys carried out by the among the poorest countries. The In summary, though overall, poverty

University of South Africa (UNISA) persistence of high wage gaps is levels in South Africa are lower today

between 2008 and 2015 suggests that associated with the skills premiums and compared to 1994, the World Bank says

the top percentile of households had differences between unskilled, semi- the country’s efforts to reduce poverty by

70.9% of the wealth and the bottom 60% skilled, and high-skilled workers. With 2030 will depend on gross domestic

had 7% - richer households are almost 10 wages rising for skilled workers, the product (GDP) growth and the reduction

times wealthier than poor households. stagnation of wages for semiskilled of income inequalities, the former being

workers fuels the increase in wage affected by access of the poorest groups

Financial inclusion inequality. In fact, workers in the middle to economic opportunities, and fiscal

Ownership of financial assets features of the distribution have witnessed an redistribution. South Africa has slow

prominently among the factors that erosion in the growth of their wages over growth to poverty elasticity (that is how

influence wealth inequality. For the poor, time, relative to the rest of the workforce much poverty falls for each percentage

financial assets represent 36% of total in the labour market. This is related to the point in economic growth) due to the

assets compared to 75% for the rich. shrinkage of semi-skilled employment and extremely high level of income inequality.

Moreover, those with lower incomes and their returns which points to the Projected sluggish growth, coupled with

young to middle age groups have high existence of a “missing middle” in the recorded improvements in access of the

rates of indebtedness. This prevents labour market. poor to education (and eventually, skilled

many segments of the population from jobs) is likely to somewhat reduce

participating in asset accumulation and Unequal opportunities: inequality and poverty in the coming

wealth building. Race and human capital Inequality of opportunity, measured by years (baseline scenario). Poverty rates

(education) have very high returns for the influence of race, parents’ education, (at the lower bound national poverty line)

wealth generation, even higher than in parents’ occupation, place of birth, and are projected to decrease from 40% of

the case of income or consumption gender influence opportunities, is high. In the population in 2016 to 33% in 2030

inequality. a society where there is equality of despite slow growth, as inequality would

opportunity, these factors should not be fall, with a Gini coefficient dropping from

Labour market relevant to reaching one’s full potential: 62.8 in 2017 to 59.5 in 2030.

The labour market is effectively split into ideally, only a person’s effort, innate

two extreme job types. At one extreme is talent, and choices in life would be the

a small number of people with highly paid influencing forces. Analysis of the

jobs in largely formal sectors and larger proportion of children with access to a

enterprises, at the other extreme is most basic service, adjusted by how equitably

of the population, who work in jobs that the service is distributed among groups

are often informal and pay less well. The differentiated by circumstances (via a

highly paid jobs are highly sticky: once Human Opportunity Index), shows that

people find these jobs they are unlikely to opportunities among children in South

give them up. The less well-paying jobs Africa vary widely depending on the types

are more fluid, more likely to employ new of service. An estimation of the inequality

entrants into the labour market, and more of opportunity index and its ratio to

likely to witness exits from employment. overall inequality found that inequality ofFiduciary Focus

Section12J Investments

History How does section 12j work?

The 2008 South African Budget Review Sec 12J of the ITA allows an investor

found that one of the main challenges to (individuals, companies and Trusts) a

the economic growth of small and 100% tax deduction in respect of any

medium-sized businesses was access to investment into a VCC subject to certain

equity finance. Through Section 12J, the conditions. The full amount invested in a

South African Government aims to VCC is 100% deductible from taxable

stimulate the economy and promote income in the year in which the

investment in South African private investment is made. This benefit is

companies, whilst providing tax benefits received when tax returns are filed. If the

to investors. Section 12J is designed to investment is held for a minimum period

encourage individual and corporate of 5 years, the tax benefit received at the

Ajanta Mayku

investors to invest in a range of smaller, date of investment will become

Team Leader: Advisory

higher-risk trading companies by permanent.

Specialists, Wealth and

investing through the Venture Capital

Investment Management

Companies (VCC). The VCC regime is subject to a 12 year

sunset clause and ends on 30 June 2021.

Section 12J was introduced into the Government will then review the efficacy

Income Tax Act (ITA) on 1 July 2009. – It of the regime and decide if it should be

didn’t really gain traction because the tax continued.

deduction by the investor was recouped

when the investor sold the shares. The Example: A typical client/investor, a

qualifying investment was initially R20M. natural person pays tax at 45%. The

In 2014, legislation was adjusted to make investor invests R100 into a 12J company

the tax deduction permanent if the shares and will receive a “refund” from SARS of

were held for 5 years. The investment R45. If the investor holds the investment

threshold increased to R50M. for 5 years, this benefit becomes

permanent.

Section 12J in a nutshell

CGT will be payable at the end of 5 years

There are three parties. upon exiting the investment. The base

• Qualifying Investors will invest in an cost will be zero. SARS is of the view that

approved VCC in exchange for the if 100% is claimed against taxable income

issue of venture capital shares and initially, you can’t then receive the benefit

investor certificates. of “double deducting”.

• The approved VCC will, in turn, invest

in qualifying investee companies in

exchange for qualifying shares.

Section 12J in a Nutshell

14Fiduciary Focus

Section12J Investments

Who qualifies to be an investor? consulting, auditing, or accounting. party administrators?

(professional industries); • Larger VCC companies, such as

Any taxpayer qualifies to invest in an • Operating casinos or other gambling Westbrook try to reduce investor risk

approved VCC. The approved VCC must related activities including any other and usually approach SARS with a

games of chance; template transaction in order to ensure

issue investor certificates to its investors,

• Manufacturing, buying or selling liquor, that they get a binding ruling on the

which will provide SARS with the proof

tobacco products or arms or investment strategy.

when the investor claims the relevant tax ammunition; or

deduction. No deduction will be allowed • Any trade carried on mainly outside the Legislative changes and no track record

where the taxpayer is a connected person Republic. of actual returns in most cases.

to the VCC at or immediately after the

acquisition of any venture capital share in There are no special tax rules for investee What happens in 2021?

that VCC. There is no minimum companies. The general tax rules will

investment amount in terms of apply. Treasury will assess the efficacy of the

legislation, however many companies section 12J regime. No investor will be

stipulate a minimum – usually R500 000. Risks of sec 12j granted a deduction after this date. Up till

There is no limit on the amount which can Feb 2021, an investor will receive the

be invested. Within the Section 12J asset managers, deduction and the fund will run for

there are those that are involved in high another 5 years.

Who qualifies to be an investee? risk, startup companies. However, clients

don’t have to take that type of high risk to It will need to be demonstrated to SARS

Investee must be a resident company and enjoy the tax benefits of a Section 12J that section 12J is promoting investment

must not be a controlled group company investment. Many of the top asset into SMEs in SA so that the regime is

in relation to a group of companies. The managers have capital protection as a key extended.

company’s tax affairs must be in order (a focus. Some of the potential risks are:

tax clearance certificate must be After 5 years, an Investor does not

requested from SARS to support this Investment risk necessarily have to exit. It depends on the

requirement). The company must be an • Consider the underlying investment exit mechanism of the asset manager and

unlisted company (section 41 of the Act) and associated risk. their commitment to liquidity after a

or a junior mining company. A junior • Consider the track record of the asset

term.

mining company may be listed on the managers – most VCC’s have an

Alternative Exchange Division (AltX) of investment committee.

the JSE. • VCC’s are often young companies with

no proven track record. Risk is

mitigated by the income tax relief since

During any year of assessment, the sum the capital invested is only a % of the

of the “investment income” derived by face value of the investment.

the company must not exceed 20% of its

gross income for that year of assessment. Liquidity risk

• Consider how liquidity will be created

The company must not carry on any of at the end of term.

the following impermissible trades: Any • Top asset managers will have a proper

industry except: exit strategy/mechanism.

• Any trade carried on in respect of

immoveable property, except trade as Compliance risk

a hotel keeper (includes bed and • The investment manager must

breakfast establishments); maintain the section 12J status for

• Financial services activities such as investors to ensure that they retain

banking, insurance, money-lending and their tax deduction. Consider the due

hire-purchase financing; diligence process.

• Provision of financial or advisory • Consider the compliance measures

services, including legal, tax advisory, which are in place. Example: Board of

stock broking, management Directors – are they independent or 3rdFocus on Philanthropy

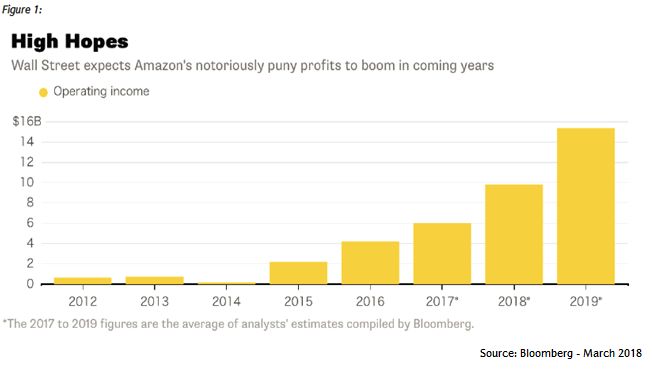

World’s Richest Man, Amazon’s Jeff Bezos Gives More to Charity

It was back in October last year when Jeff Amazon engages in the retail sale of

Bezos’ wealth surpassed the $100 billion consumer products and subscriptions in

mark. At the time of writing this article, it North America and internationally. It

was sitting at a cool $112 billion - operates through the North America,

according to Forbes annual rich list (06 International, and Amazon Web Services

March 2018). This makes the founder (AWS) segments. The company sells

and CEO of Amazon the world’s richest merchandise and content purchased for

man, a position he has held many-a-time resale from vendors, as well as those

before. offered by third-party sellers through

retail Websites. It also manufactures and

Much like the other members of the sells electronic devices, including kindle e-

global rich-list, Bezos is no stranger to the readers, fire tablets, fire TVs, and echo. In

world of philanthropy. Earlier in January, addition, it also provide Kindle Direct

he and his wife, MacKenzie Bezos donated Publishing, an online service that lets

$33 million to a scholarship fund independent authors and publishers

Zukelwa Solomon

(TheDream.US) for young choose a royalty option and make their

Collateral Writer, GI&S

“Dreamers." The grant is the largest in the books available in the Kindle Store, along

organisation’s history and will give 1,000 with its own publishing arm, Amazon

undocumented immigrant graduates of Publishing. It also offers programs that

US high schools with Deferred Action for allow authors, musicians, filmmakers,

Childhood Arrivals (DACA) status the application developers and others to

opportunity to go to college. publish and sell content.

DACA provides a level of amnesty to Amazon’s success as a business has been

certain undocumented immigrants, many nothing short of amazing. At the end of

of whom came to the US as children - January, the company was rated as the

with a six-month delay for recipients. The world's most valuable brand, knocking At the end of January, the

program was formed through executive Google from the top spot down to third company was rated as

order by former US President Barack while Apple maintained a tentative hold the world's most valuable

Obama in 2012 and allowed certain on second place. This is according to the brand, knocking Google

people who came to the US illegally as Brand Finance Global 500 report. It placed from the top spot down

minors to be protected from immediate a value on the Amazon brand at $150.8 to third while Apple

deportation. Recipients were able to billion, a 42% jump from last year's maintained a tentative

request “consideration of deferred action” report. Apple received a brand valuation hold on second place.

for a period of two years, which was of $146.3 billion, up 37%, with the

subject to renewal. The Donald Trump Google brand owned by Alphabet at

administration however is phasing out the $120.9 billion, up 10% for a year earlier.

DACA program but Congress has been at

odds over what should happen to It has not always been a rosy picture for

“Dreamers” set to lose their deportation Amazon, however. Amazon was founded

protection status. in 1994, first traded publicly in 1997, and

didn’t turn a profit until 2001. Further,

The issue of immigration is a subject very over the past five years, Amazon’s

close to Bezos. His adoptive father, average profit margins have languished at

Miguel Bezos fled to the US from Cuba about 1%.

alone when he was 16 years old as part of As Bloomberg puts it however, Bezos has

Operation Pedro Pan. As a result, Bezos been sacrificing profit for growth and has

says his $33 million donation is in his successfully persuaded Wall Street that

honor. Jeff Bezos himself was born in Amazon is best served pouring money

Albuquerque, in the US state of New into the logistical nuts and bolts that have

16Focus on Philanthropy

World’s Richest Man, Amazon’s Jeff Bezos Gives More to Charity

turned his company into the Wal-Mart of answers and that they also do not accept

the web. More recently, however, it as inevitable but rather they share the

investors have found solace in the belief that putting their collective

company’s profitable cloud services resources behind the country’s best talent

business, which has helped offset losses can, in time, check the rise in health costs

in e-commerce. while concurrently enhancing patient In an effort to slow the

satisfaction and outcomes. pace of runaway

Another area where Jeff Bezos has been healthcare costs,

looking for success is healthcare, and he’s The Amazon-Berkshire-JPMorgan tie-up Amazon, Berkshire

giving it a shot. In an effort to slow the will focus on technology solutions to Hathaway and JPMorgan

pace of runaway healthcare costs, provide high-quality and transparent Chase plan to join forces

Amazon, Berkshire Hathaway and health care. Bezos is however not in denial to change how health

JPMorgan Chase plan to join forces to that the healthcare system is complex care is provided to their

change how health care is provided to and much like the DACA donation

combined 1 million US

their combined 1 million US employees. mentioned earlier, the new company will

employees.

The plan is the first big move by Amazon be free from profit-making incentives and

in the healthcare sector after months of constraints. That’s as it tries to find ways

speculation that the internet behemoth to cut costs and boost satisfaction with

might make an entry. the healthcare plan for employees of

Amazon, Berkshire Hathaway and

US healthcare costs continue to rise year JPMorgan Chase.

over year despite efforts to curb them,

and with many experts believing that the

fault lies with too-high prices, Berkshire

Hathaway Chairman and CEO, Warren

Buffett, says increasing healthcare costs

are “a hungry tapeworm on the American

economy.” He adds that their companies

do “not come to this problem withWealth Trends

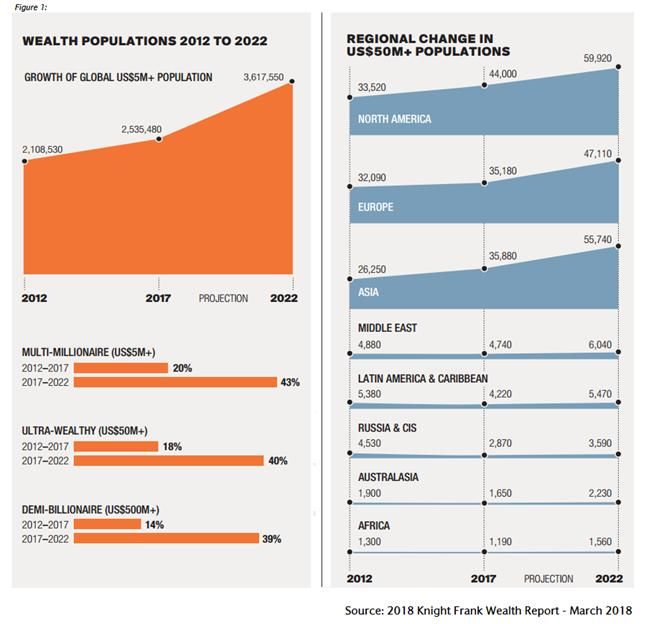

The 2018 Knight Frank Wealth Report

The latest edition of the annual Knight people with US$50 million or more in net

Frank Wealth Report is out and the mood assets that took the total population to

for South Africa appears to be on the 35,180. A 15% rise in Asia’s ultra-wealthy

mend. cadre took its population to 35,880.

South Africa: Europe:

The country is forecast to see a 20% Europe’s 10% growth in its ultra-wealthy

uplift in its ultra-wealthy population population last year may seem

(people with US$50 million or more in net counterintuitive given the political

assets) over the next five years following challenges facing the region. Yet many

a 14% rise in 2017. In the wake of the European countries saw a marked

election of Cyril Ramaphosa as head of upswing in economic performance last

the governing party, the African National year, with the euro zone outperforming

Congress (ANC), investor and consumer the United Kingdom (UK) and United

confidence in South Africa is expected to States (US) economies in terms of gross

Zukelwa Solomon

improve as a change in political leadership domestic product (GDP) growth. The

Collateral Writer, GI&S

can also affect ultra-wealthy populations. European Central Bank (ECB) also held off

Nevertheless, the report finds that tightening monetary policy, unlike central

wealthy South Africans are still likely to banks in the UK, Canada and the US.

continue moving money abroad and However, as James Roberts, Knight

acquiring dual citizenship, although they Frank’s Chief Economist, explains, the

are now also more likely to stay resident ECB is set to taper its quantitative easing

in the country since they are supportive programme this year.

of the new ANC leader.

South America:

This is a view that also finds support in Latin America and the Caribbean also saw

the fact that Cape Town has taken the a bounce back in ultra-wealthy This is a view that also

second place in the Prime International populations in 2017, with a 20% rise after finds support in the fact

Residential Index (PIRI) 100, recording the 22% decline seen since 2012. The that Cape Town has

almost 20% growth year on year. total number of ultra-wealthy individuals taken the second place in

According to the report, the Atlantic in the region (4,220) is still lower than in the Prime International

Seaboard is attracting buyers from 2012 (5,380), but the figure is expected Residential Index (PIRI)

overseas as well as from elsewhere in to grow by 30% over the next five years. 100, recording almost

South Africa, however both new and Brazil, the biggest wealth hub in the 20% growth year on year.

existing stock are in short supply. region, also saw strong growth last year.

Ian Bremmer, Head of Eurasia Group, a

The global context: leading political risk consultancy, told The

When shifting the focus to the rest of the Wealth Report: “It’s largely an economic

globe, the report has found that although recovery story. The stock and bond

the super-rich populations are on the rise markets have performed extraordinarily

Europe is slipping down the ranks of the well this past year. While the ultra-

world’s wealthiest regions. North America wealthy took a hit in 2016, there was a

remains the world’s largest wealth region clear rebound in 2017. Note that this was

with some 34% of the world’s ultra- happening at the same time as the

wealthy based there. In fact, their ranks Brazilian real was going through an

rose by a further 5% last year, taking the important devaluation. So in dollars, there

total to 44,000. Europe, however, failed to was a real improvement.”

fend off a strong Asian challenge,

narrowly losing its second place spot USA:

despite a 10% rise in the number of In the US, new tax policies aimed at

18Wealth Trends The 2018 Knight Frank Wealth Report trying to encourage more corporates to impact on ultra-wealthy populations, ignored. It warns that there may well be a move money onshore may have although it can take some time for the point where growth in the ultra-wealthy ramifications for the whole economy and, changes to be felt,” explains Winston populations does not automatically in turn, for ultra-wealthy populations. In Chesterfield, Director of Custom Research continue on its currently upward late 2017, President Donald Trump at Wealth-X. trajectory. announced a raft of tax changes, including an ultra-low 15.5% tax rate for Beyond 2018: This year, the report expects growth to companies bringing their money onshore. Looking ahead, the Knight Frank Wealth strengthen further as the International He also cut corporation tax to 21%, as Report expects ultra-wealthy populations Monetary Fund (IMF) is predicting that well as cutting some income tax rates to continue to grow in the medium term the global economy will expand by 3.7%, and boosting family allowances. Under as there are likely to be an increasing which if correct would be the highest rate current economic forecasts, the US is number of economic and geopolitical of growth since 2011. In this context, expected to see a 38% rise in its ultra- headwinds, not least monetary tightening ultra-wealthy individuals are encouraged wealthy population over the next five across the board. Even when conditions to think of moving away from safe haven years. However, the change to are negative, wealthy populations tend to investments and towards risk-facing corporation tax could have an impact in show signs of resilience, however, there assets, which typically perform strongly in the future, especially if it encourages are societal changes taking place over the cyclical upswings. more investment across the US. “In terms longer-term and the report cautions that of fiscal policy, changes in corporation tax the reaction to wealth inequality is a and capital gains tax have the largest pressure that should not be necessarily

News Roundup

What Happened at Home and Abroad?

SA Avoids Moody’s Credit World Bank Loans Ethiopia Naspers Raises $9.8Bn in

Ratings Downgrade $600Ml for Infrastructure Tencent Share Disposal

In line with expectations, ratings agency, Ethiopia is in line for a $600 million loan Naspers has reduced its investment

Moody’s left South Africa’s (SA’s) credit from the World Bank to fund roads and holdings in China’s Tencent to by 2% to

rating unchanged at ‘Baa3’, the lowest other infrastructure projects in urban 31.2% to strengthen its finances and

rung of investment grade and upwardly areas. This is to help expand sustainable invest over time in its classifieds, online

revised the outlook on the economy to urban infrastructure and services, as well food delivery and fin-tech businesses

Stable from Negative previously. as promote local economic development. globally. It sold 190 million shares in

Tencent via an accelerated book-building

process and raised $9.8 billion.

DRC Q4 Mining Revenue S&P Doubles SA GDP Growth

More Than Doubled Forecast to 2%

Facebook Stock Tanks on

Standard & Poor’s (S&P) Global Ratings

Data Scandal

Democratic Republic of Congo (DRC) says

its 2017 mining sector revenue rose has raised SA’s gross domestic product

35.6% to $822.2 million while revenue (GDP) growth forecast for 2018 from 1% Facebook has announced a series of

from the oil and gas sector jumped by to 2%, but warned it is still not enough to changes to give its users more control

103% to $203.9 million, helped by higher decrease SA's high unemployment over their data. This follows a massive

prices for key exports such as copper and rate. The ratings agency says the scandal where data from 50 million users

cobalt. improved outlook is due partly to was improperly harvested to target US

strengthening domestic and foreign and British voters in close-run elections.

investor sentiment. The news wiped more than $100 billion

Zim Indigenisation Limited to from Facebook’s stock market value.

Diamond, Platinum Son of Angolan Ex-President

Charged with Fraud M&R Board Rejects Buyout

Staying with mining, over in Zimbabwe

Bid from Germany’s ATON

the government has changed its

empowerment law (Indigenisation and José Filomeno dos Santo, the son of

Economic Empowerment Act) to limit Angola's former President, José Eduardo The independent board of engineering

majority ownership by state entities to dos Santos has been formerly charged of and construction company, Murray &

only diamond and platinum mines and fraud following the alleged illegal transfer Roberts (M&R) has rejected a buyout bid

not the entire mining sector as previously of $500 million from the country’s central from Germany’s ATON GmbH. ATON

proposed. bank into a corporate account at HSBC in which already owns a third of M&R had

the United Kingdom (UK). made a cash offer price of 15 rand per

share - a 56% premium to M&R’s closing

Absa Feb PMI Back In Positive price on 22/03/2018.

Territory

SA’s seasonally adjusted Absa Purchasing

Managers’ Index (PMI) which is compiled

by the Bureau for Economic

Research (BER) improved to above the

break-even mark of 50 index points to

50.8 in February from 49.9 points a

month earlier.

20What did The Economist Say?

The Economist offers authoritative insight and opinion on international

news, politics, business, finance, science, technology and the connections

between them. Below are some extracts of the stories that caught our

attention.

What Zuckerberg Should Do: Facebook’s business relies on three

elements: keeping users glued to their

Facebook Faces A screens, collecting data about their

Reputational Meltdown behaviour and convincing advertisers to

This is how it, and the wider industry, pay billions of dollars to reach them with

should respond targeted ads. The firm has an incentive to

promote material that grabs attention

LAST year the idea took hold that Mark and to sell ads to anyone. Its culture

Zuckerberg might run for president in melds a ruthless pursuit of profit with a

2020 and seek to lead the world’s most Panglossian and narcissistic belief in its

powerful country. Today, Facebook’s own virtue. Mr Zuckerberg controls the

founder is fighting to show that he is firm’s voting rights. Clearly, he gets too

capable of leading the world’s eighth- little criticism.

biggest listed company or that any of its

2.1bn users should trust it. In the latest fiasco, it emerged that in

2013 an academic in Britain built a

News that Cambridge Analytica (CA), a questionnaire app for Facebook users,

firm linked to President Donald Trump’s which 270,000 people answered. They in

2016 campaign, got data on 50m turn had 50m Facebook friends. Data on

Facebook users in dubious, possibly all these people then ended up with CA.

illegal, ways has lit a firestorm. Mr (Full disclosure: The Economist once used

Zuckerberg took five days to reply and, CA for a market-research project.)

Today, Facebook’s

when he did, he conceded that Facebook Facebook says that it could not happen

founder is fighting to

had let its users down in the past but again and that the academic and CA

broke its rules; both deny doing anything show that he is capable

seemed not to have grasped that its

wrong. Regulators in Europe and America of leading the world’s

business faces a wider crisis of

confidence. After months of talk about are investigating. Facebook knew of the eighth-biggest listed

propaganda and fake news, politicians in problem in 2015, but it did not alert company or that any of

Europe and, increasingly, America see individual users. Although nobody knows its 2.1bn users should

Facebook as out of control and in denial. how much CA benefited Mr Trump’s trust it.

Congress wants him to testify. Expect a campaign, the fuss has been amplified by

roasting. the left’s disbelief that he could have won

the election fairly.

Since the news, spooked investors have

wiped 9% off Facebook’s shares. [The rest of this article appears in the 24

Consumers are belatedly waking up to February 2018 print edition of The

the dangers of handing over data to tech Economist]

giants that are run like black boxes.

Already, according to the Pew Research Overpriced: Why Africa’s Poor

Centre, a think-tank, a majority of

Americans say they distrust social-media

Pay High Prices

Africa’s economic paradox

firms. Mr Zuckerberg and his industry

need to change, fast.

“WE FEEL so hungry,” says Agatha

Khasiala, a Kenyan housekeeper,

The addiction gameWhat did The Economist Say?

grumbling about the price of meat and mobile phones, GDP almost doubled.

fish. She has recently moved in with her They may also be less pricey than

daughter because “the cost of everything economists reckon, because poor people

is very high”. The data back her up. The buy second-hand clothes or grow their

World Bank publishes rough estimates of own food.

price levels in different countries, showing

how far a dollar would stretch if A more intriguing explanation comes from

converted into local currency. On this food prices. The relative cost of food,

measure, Kenya is more expensive than compared with other goods, is higher in

Poland. poor countries. In Africa, the absolute cost

is sometimes high, too. Nigerians would

This is surprising. The cost of living is save 30% of their income if they bought

generally higher in richer places, a their food at Indian prices, finds a recent

phenomenon best explained by the study by the OECD, a think-tank. Meat

economists Bela Balassa and Paul costs more in Ghana than in America.

Samuelson. They distinguished between

goods that can be traded internationally (The rest of this article appears in the 15

and many services, like hairdressing, that March 2018 print edition of The

cannot. In rich countries, manufacturing Economist)

is highly productive, allowing firms to pay

high wages and still charge internationally The Threat To World Trade:

competitive prices. Those high wages also

drive up pay in services, which must The Rules-Based System Is In

compete for workers. Since productivity is Grave Danger

low in services, high pay translates into Donald Trump’s tariffs on steel and

high prices, pushing up the overall cost of aluminium would be just the start

living.

Among developing

DONALD TRUMP is hardly the first economies, however,

Among developing economies, however, American president to slap unilateral

the relationship between prices and

the relationship between

tariffs on imports. Every inhabitant of the

prosperity is less clear-cut. Prices in Chad, Oval Office since Jimmy Carter has prices and prosperity is

for instance, are comparable to those in less clear-cut.

imposed some kind of protectionist curbs

Malaysia, where incomes are 14 times on trade, often on steel. Nor will Mr

higher. Fadi Hassan of Trinity College Trump’s vow to put 25% tariffs on steel

Dublin finds that in the poorest fifth of and 10% on aluminium by themselves

countries, most of them in Africa, the wreck the economy: they account for 2%

relationship goes into reverse: penniless of last year’s $2.4trn of goods imports, or

places cost more than slightly richer ones. 0.2% of GDP. If this were the extent of Mr

A paper in 2015 from the Centre for Trump’s protectionism, it would simply be

Global Development (CGD), an American an act of senseless self-harm. In fact, it is

think-tank, accounts for various factors a potential disaster—both for America

which could explain differences in prices, and for the world economy.

including state subsidies, geography and

the effects of foreign aid. Even then, As yet it is unclear exactly what Mr

African countries are puzzlingly expensive. Trump will do. But the omens are bad.

One explanation is dodgy statistics. Unlike his predecessors, Mr Trump is a

African countries may be richer than they long-standing sceptic of free trade. He

seem. When Nigeria revised its figures in has sneered at the multilateral trading

2014 to start counting industries such as system, which he sees as a bad deal for

22You can also read