Uniquely ASEAN Renewable Energy - Weighing Climate Matters

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Uniquely

Regional Thematic | August 2022 MARKET DATELINE

PP19489/04/2022 (035080)

ASEAN Renewable Energy

Weighing Climate Matters

Regional Thematic

2 August 2022 Utilities | Renewable Energy

ASEAN Renewable Energy

Weighing Climate Matters

In this report, we focus on ASEAN’s renewable energy (RE)

development amidst elevated cost pressure and the potential of rising

Analysts

carbon pricing initiatives. As near-term priorities are on curbing inflation

without jeopardising economic growth, more effort is needed to achieve Sean Lim

climate change targets. Featured ideas: Tenaga Nasional (TNB), Yinson +603 9280 8867

(YNS), Solarvest (SOLAR) and Samaiden (Malaysia), Sembcorp Industries sean.lim@rhbgroup.com

(SCI) (Singapore), as well as Global Power Synergy (GPSC) (Thailand) for

their growing RE exposure and potential battery energy storage system

(BESS) application opportunities. Shekhar Jaiswal

Not ruling out fossil fuel yet. While developed countries move away from +65 6320 0806

fossil fuel dependence to RE, ASEAN leaders acknowledged that ASEAN shekhar.jaiswal@rhbgroup.com

will still need to consider fossil fuel in the short to medium term to meet its

fast growing electricity demand. Moreover, fossil fuel remains abundant in

this region. Unabated fossil fuel accounted for three-quarters of total Indonesia Research

generation, of which coal contributed to >40% of the region’s energy related +6221 5093 9888

emissions. Even with pledges not to have new coal plants, the region still rhb.id.research@rhbgroup.com

has c.90GW of existing coal plants with an average operating lifetime of 10

years coupled with another 18GW under construction. Athipu Visavaveja

Greater effort needed. The Russia-Ukraine crisis has increased the +66 2088 9827

urgency even in developed countries, to ramp up RE capacity and athipu.vi@rhbgroup.com

safeguard energy security from fossil fuel supply disruptions. Closer to us,

eight South-East Asian countries have announced carbon neutrality and net

zero emissions targets. Still, we have yet to see ASEAN governments

translating these targets into detailed policies for future implementations.

We believe ASEAN countries will not achieve their respective targets unless Table of contents

greater effort is put in place to accelerate the progress. According to the

ASEAN Renewable Energy 2

International Energy Agency (IEA), average energy investment pa in South- ASEAN Power Grid 5

East Asia has to be hiked up to USD190bn pa till 2030 from the 2016-2020 High Fuel Cost and Inflation Impact 11

average of USD70bn pa to meet current announced climate aspirations. Carbon Pricing 15

Another global record for RE addition in 2022. Global annual RE Indonesia 21

capacity addition is estimated by IEA to increase by 8% to 320GW in 2022 - Indonesia’s Renewable Energy Roadmap

and to remain stable in 2023. This is largely driven by the continuous growth - Abundant Coal Reserves Remain a National Focus

in China and acceleration of RE expansion in Europe despite the - Solar Power – The Most Feasible Alternative

continuation of supply chain disruption and construction delay as well as - Policies Supporting Renewables Transition

Malaysia 33

escalated raw material cost. The recent retracement of commodity prices in

- Malaysia’s Renewable Energy Roadmap

response to the weaker economic outlook could provide a breather to

- LSS Progress Remains Slow

overall project costing.

- Exploring Carbon Pricing

Elevated fuel subsidies challenge climate change goals. Elevated fuel - Featured Ideas

prices have led to higher subsidies, casting additional fiscal burden to Singapore 41

ASEAN countries. With the key priorities being keeping inflation at bay, we - Planning For a Low Carbon Future

are seeing a delay in fossil fuel subsidy reform to protect the economies - Progress On Adoption Of Renewable Energy

and the cascading effect is a relatively lower allocation of economic - Singapore’s Carbon Market & Pricing

resources to lower emission industry. - Featured Ideas

Rising carbon pricing initiatives. Singapore is the first to implement Thailand 56

- Thailand’s Renewable Energy Roadmap

carbon tax back in 2019 and to progressively increase over the years. We

- Initiatives Supporting Renewable Energy

are seeing more carbon pricing initiatives (either carbon tax or emission

- Thailand’s Electricity Supply Structure

trading) being scheduled for implementation or under considerations within - Major Renewable Energy Sources in Thailand

the ASEAN region. Indonesia, Malaysia, and Thailand have announced - Recent Developments

plans to implement carbon emissions trading. However, the timeline for - Featured Ideas

these implementations may be pushed back due to the uncertain economic

outlook amidst high inflationary environment, as evident by the Indonesian

Government’s recent postponement of carbon tax implementation.

% Upside P/E (x) P/B (x) ROAE (%) Yield (%)

Company Name Rating Target

(Downside) Dec-23F Dec-23F Dec-23F Dec-23F

Global Power Synergy Buy THB84.00 21.3 22.4 1.7 6.3 2.3

Solarvest Neutral MYR0.77 8.2 17.3 2.2 13.7 -

Tenaga Nasional Neutral MYR8.60 1.1 9.5 0.8 8.5 6.1

Yinson Buy MYR2.83 33.5 5.2 0.8 15.4 0.9

Source: Company data, RHB

P/E (x) P/B (x) ROAE (%) Yield (%)

See important disclosures at the end of this report Dec-23F

22.4 Dec-23F

1.7 Dec-23F

0.1 Dec-23F

0.0

1

Market Dateline / PP 19489/05/2019 (035080)

17.3 2.2 0.1 0.0

ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

ASEAN Renewable Energy

Not ruling out fossil fuel to cope with rising demand

Global electricity demand has recovered by 6% YoY in 2021 following a similar drop in 2020.

This is stronger than the earlier projection of 5%, in which the industrial sector contributed

the most, followed by the commercial, services and residential sectors. Global electricity

demand growth for 2022 is now at 3%, in line with the average 10-year growth rate pre-

pandemic. Demand growth will moderate to 2.6% and 2% in 2023 and 2024. Closer to us,

South-East Asia remains one of the fastest growing regions in the world in terms of electricity

demand. IEA projects this region’s electricity demand to grow close to 5% in the next three

years, relatively lower than the average in terms of electricity demand, at a CAGR of 6% in

the past 20 years.

Figure 1: Global change in electricity demand, 2015-2024

Source: IEA Electricity Market Report January 2022

While the developed countries move away from fossil fuel dependence to RE, ASEAN

leaders acknowledge that ASEAN will still need to consider fossil fuel in the short to medium

term to meet its fast growing electricity demand. Moreover, fossil fuel remains abundant in

this region and is the most cost-effective method. Some of the challenges faced by ASEAN

countries in increasing RE in the power mix is the high cost of upgrading and integrating the

systems that need more investment in grids, Internet of Things (IoT), technological know-

how, and quality energy infrastructure.

Rather than completely ruling out fossil fuel, ASEAN countries should instead explore ways

to utilise fossil fuel in an environmentally sustainable manner to act as a bridge to a carbon-

free energy future. Unabated fossil fuels accounted for three-quarters of total generation, of

which coal contributed to over 40% of the region’s energy-related emissions. The region

has a large and relatively young fleet of coal- and gas-fired power plants. Even with pledges

not to have new coal plants, the region still has c.90GW of existing coal plants with an

average operating lifetime of 10 years, coupled with another 18GW under construction.

Therefore, apart from early retirement, retrofitting and re-purposing the plant is another

option to be explored as it provides certain flexibility while maintaining electricity security.

RE capacity is set to break another global record in 2022

According to IEA, annual RE capacity additions increased by 6% to c.295GW in 2021,

largely led by the strong deployment in China, which accounted for 46% of global RE

capacity addition. This is despite the continuation of supply chain disruption and

construction delay as well as escalated raw material cost amidst higher commodity prices.

High raw material and freight costs have reversed the long term decreasing trend for solar

modules and wind turbines in 2021. We continue to see overall capex increasing by 15-25%

YoY in 2022. For ASEAN, the annual installation fell 40% YoY in 2021, no thanks to the

phase out of the generous feed-in tariff (FIT) scheme in Vietnam, which resulted in a drop

in deployment.

See important disclosures at the end of this report

2

Market Dateline / PP 19489/05/2019 (035080)

ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

Figure 2: Renewable net capacity additions by country and Figure 3: Global net renewable capacity additions by

region, 2019-2021 technology, 2017-2023

Source: IEA Renewable Energy Market Update Source: IEA Renewable Energy Market Update

Global annual RE capacity addition is estimated by IEA to increase by 8% to 320GW in

2022, and to remain stable in 2023. This is largely driven by the continuous growth in China

as well as acceleration of RE expansion in Europe. Following the Ukraine and Russia war,

we have seen a higher RE target being laid out by many European countries to reduce

energy reliance on Russia. Furthermore, European countries have been suffering from sky

high wholesale power prices in the past one year with much higher coal and gas prices. This

provides more incentive for governments to control energy prices via favourable and

supportive policies. Note that although some of these rates signed for utility scale PV and

onshore wind long-term contracts in certain European countries (ie Germany, Spain, Italy,

etc) are already are the highest in the past five years, they are still significantly below the

current wholesale energy prices. Closer to us, China maintains the lead in RE growth in

order to achieve its ambitious 1,200GW wind and solar PV target by 2030.

But greater effort is still needed to put in place to accelerate RE progress

ASEAN countries have set to achieve 35% share of RE (from a quarter currently) in installed

power capacity by 2025. In the latest edition of World Energy Outlook, IEA has made

projections and analysis under two main scenarios, namely:

i. The Stated Policies Scenario (STEPS) – reflects the countries’ current policy settings

based on a sector-by-sector assessment of the specific policies that are in place or

have been announced;

ii. The Sustainable Development Scenario (SDS) – delivers on the Paris Agreement

goal to limit the temperature to “well below 2°C”, alongside goals on energy access

and air pollution. This scenario is consistent with South-East Asia’s current announced

climate aspirations.

There are several key takeaways from IEA with this regard. ASEAN countries will not

achieve the target under STEPs unless greater effort is put in place to accelerate the

progress. Eight South-East Asia countries have announced carbon neutrality and net zero

emissions targets. Still, we have yet to see ASEAN governments translating these targets

into detailed policies for future implementations. Essentially, South-East Asia’s policy

choices will have huge implications for its future energy mix as depicted by IEA in the chart

below.

See important disclosures at the end of this report

3

Market Dateline / PP 19489/05/2019 (035080)

ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

Figure 4: Energy demand trends in South-East Asia by scenario, 2020-2050

Source: IEA Southeast Asia Energy Outlook 2022

Additionally, average energy investment pa in South-East Asia from 2016 to 2020 was

USD70bn, of which around 40% is attributable to clean energy technologies – mostly solar

PV, wind and grids. The amount has to be hiked up to USD130bn pa till 2030 under STEPs

and USD190bn pa under SDS. Currently, coal still contributed the largest portion in

electricity supply at 43%, followed by gas (31%) and RE (25%). With that the share of RE

in electricity demand is projected to increase to c.40% and 85% by 2050 in STEPS and

SDS. Currently bulk of the investments originate from public finances including state-owned

enterprises, which are predominantly involved in regulated businesses and the investments

are mostly on infrastructure and grid upgrade. As we have seen in the past two years, private

capital is gradually flowing in for clean energy assets. Other efforts including international

support are needed to boost innovation and energy efficiency as well as to develop

necessary infrastructure amidst continuous regulatory and financing framework

improvements.

To achieve a level of 85% in 2050, ASEAN countries need to deploy 1,100GW of renewable

capacity in the next 30 years. Wind and solar will continue to lead RE growth within the

region, reaching 18% share in electricity generation by 2030 and 44% in 2050. This is

equivalent to an average of 25GW additional solar or wind capacities pa till 2050. Beside

that we are seeing growth from a diverse range of RE options, including hydropower,

bioenergy and geothermal.

Figure 5: Average annual energy investment in South-East Figure 6: Power generation and shares of variable

Asia, 2016-2030 renewables in South-East Asia, SDS, 2020-2050

Source: IEA Southeast Asia Energy Outlook 2022 Source: IEA Southeast Asia Energy Outlook 2022

See important disclosures at the end of this report

4

Market Dateline / PP 19489/05/2019 (035080)

ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

Figure 7: Energy policies in ASEAN countries

Energy access Efficiency Renewables Fossil fuels Climate change targets

Brunei Reduce total energy Achieve 30% of electricity Reduce CO2 emissions from morning

consumption by 63% from generation from renewables by peak-hour vehicle use by 40% from

business-as-usual (BAU) levels 2035. the BAU level by 2035. Moving

by 2035. 60% EV share of total towards net zero by 2050.

annual vehicle sales by 2035.

Cambodia At least 70% of Cut energy consumption by 20% In an accelerated scenario, total Reduce greenhouse gas (GHG)

households (1m toe) and reduce emissions installed capacity by 2030 at 55% emissions 27% from baseline by

connected to the by 3 MtCO2 by 2035 and relative hydropower, 6.5% biomass and 2030 with international support.

national grid by to BAU. 3.5% solar PV. Official emissions reduction scenario

2030. reaching net-negative by 2030.

Outlines a vision of a carbon neutral

economy by 2050.

Indonesia Achieve 100% Reduce energy intensity by 1% Increase share of “new and Consider Reduce energy intensity by 1% per

electrification by per year to 2025. renewable energy” in primary accelerating year to 2025.

the end of 2024. energy supply to reach 23% by the phasing Set up the long-term strategy to

2025 and 31% by 2050. 52% out of coal in reach net zero emissions by 2060 or

share of renewables in electricity 2040s is sooner.

capacity additions from 2021 to conditional

2030. on

international

funding.*

Lao PDR Achieve Reduce final energy 30% share of renewables in total Conditional GHG emissions

electrification consumption by 10% from the primary energy consumption by reduction target to reach net zero in

rate of 98% by BAU level. 2025. 2050.

2025.

Malaysia Promote energy efficiency in the 31% share of renewables No new Reduce GHG intensity of GDP by

industry and buildings sectors installed capacity by 2025. coal-fired 35% by 2030 from the 2005 level,

with methods of standard setting, power increase to 45% reduction with

labelling, energy audits and plants.* enhanced international support.

building design. Carbon neutrality by 2050 *

Myanmar Achieve Reduce primary energy demand 20% share of renewables

electrification by 8% by 2030 from the 2005 installed capacity by 2025.

rate of 100% by level.

2030.

Philippines Achieve 100% Reduce 40% energy intensity by 15GW renewables installed No new Reduce GHG emissions by 70% from

electrification by 2030 from 2010 level. Reduce capacity by 2030. coal-fired the BAU level by 2030 with the

2022. energy consumption by 1.6% per power condition of international support.

year by 2030 from baseline plants

forecasts. Reduce energy beyond

intensity and total energy those

consumption by 24% relative to already

the BAU level by 2040. approved.

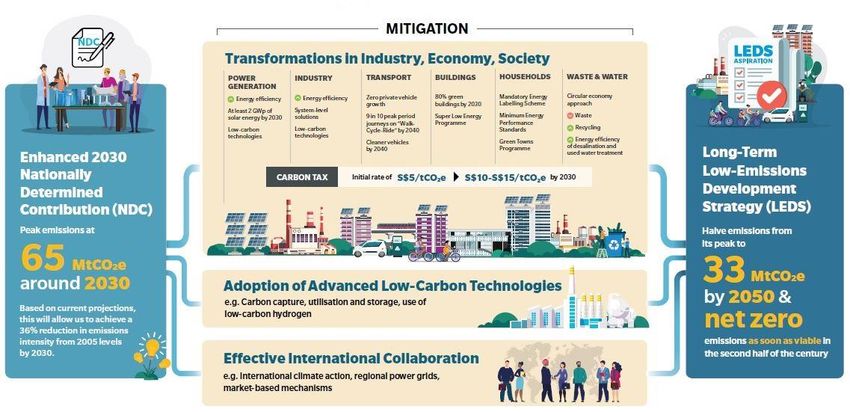

Singapore Improve energy intensity by 35% 2GW solar PV installed capacity Phase out Reduce GHG emissions by 16%

by 2030 from the 2005 levels. by 2030. unabated below BAU level by 2020. Stabilise

coal emissions with aim to peak around

generation 2030, at no higher than 65 MtCO2e.

by 2050.* Halve emissions from peak to 33

MtCO2e by 2050, to achieve net zero

emissions in the second half of the

century.

Thailand Reduce energy intensity by 30% Increase share of renewables to Reduce GHG emissions by 20% from

by 2036 from 2010 level. 30% in total final energy the BAU level by 2030, increase to

consumption by 2037; increase 25% with enhanced international

share of renewables-based support.

power to 36% in capacity and to Aim to reach carbon neutrality in 2050

20% in generation by 2037. and net zero GHG emissions by

Increase share of renewables in 2065. Reach net zero GHG

transport fuel consumption to emissions in 2050 with support of

25% by 2036 technology transfer/cooperation and

availability of financing.*

Vietnam Targets on renewables share in Phasing out Reduce GHG emissions by 9% by

TPES of 15–20% in 2030 and of coal-fired 2030 and by 27% from BAU level with

25–30% in 2050. 31-38GW solar power international support. Targets for

PV and wind installed capacity by generation GHG reductions from energy use:

2030. 4GW offshore wind by 2040s.* 15% by 2030 and 20% by 2045 from

installed capacity by 2030, Plan 31% BAU level. Make use of domestic

36GW by 2045. share of resources, along with international

coal cooperation, to achieve net zero

installed emissions by 2050.*

capacity by

2030

Note: * Though announced by government officials at COP26 or other opportunities, these statements were not yet formulated in detailed plans such as NDCs or

long-term strategies as of Apr 2022

Source: International Energy Agency (IEA)

See important disclosures at the end of this report

5

Market Dateline / PP 19489/05/2019 (035080)

ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

ASEAN Power Grid

Renewables need to be well integrated into the grid

As the share of renewables is expected to increase over the longer term, it is important to

integrate solar and wind into the system more efficiently. These renewables are highly

sporadic and dependent on weather. There are times when the wind does not blow as well

as times when the sun is covered by clouds and solar panels do not perform at night. Such

inconsistency in power generation could add pressure to the existing power supply systems

which are mostly catered for conventional fossil fuel-based generation. Solar energy peaks

during the day and tapers off at night when electricity demand increases. This would require

other electricity generators to ramp up energy production in a short span of time when the

sun sets. As such, it may not bode well for conventional generators, which require a longer

time to heat up and cool down and operate more efficiently for long hours continuously.

In planning for firm capacity, the amount of power generated that can be guaranteed to meet

demand at any given time is important to provide grid stabilisation. Hydropower is deemed

as a relatively stable source of renewable energy as it can be injected into the grid the

fastest, and hence, could be used to complement solar and wind to derive a more stable

output curve.

The national grid upgrade is needed to integrate RE to support a dynamic two-way energy

flow, while maintaining voltage stability. Essentially a smart grid is needed, equipped with

smart meters. The system should be able to perform data collection, monitor power plant

performance as well as execute and provide solutions to accommodate volatility arising from

renewable energy plants.

ASEAN power grid

The ASEAN Plan of Action for Energy Cooperation (APAEC) is the regional blueprint for the

energy sector – it is being used to set a sustainable energy landscape in ASEAN. This

blueprint comprises seven key programme areas under APAEC Phase II: 2021-2025,

strategies and action plans to transition into RE include:

i. The deployment of large-scale RE systems;

ii. Accommodating higher shares of RE in the ASEAN Power Grid (APG);

iii. Increasing infrastructure investment;

iv. Promoting smart grids to accelerate RE deployment;

v. Promotion of decentralised and distributed RE systems.

New and advanced RE technologies, such as waste-to-energy, RE-based hydrogen, energy

storage, concentrated solar thermal, and distributed renewables for energy access will also

be explored.

The APG is one of the major projects for regional integration. This grid has progressed

gradually from bilateral to sub-regional arrangements. Feasibility studies were carried out

to identify which interconnection projects were beneficial for the region. Moving forward, the

strategy is to accelerate the progress of these integration projects and initiate the expansion

of multilateral electricity trades. Another key focus is to integrate RE and other digital

developments into the grids to stabilise the APG’s performance.

To date, it was reported that seven of 16 power interconnection projects have been

completed. One programme conducted on a multilateral basis is the Lao PDR-Thailand-

Malaysia-Singapore Power Integration Project (LTMS-PIP). Recently, TNB has signed an

Energy Wheeling Agreement (EWA) for the sale, transmission and purchase of electrical

energy at 30-100MW from Lao PDR to Singapore through Thailand and Malaysia using the

existing interconnections facilities owned by all the countries involved. The EWA will be

effective for a period of two years beginning Jun 2022.

See important disclosures at the end of this report

6

Market Dateline / PP 19489/05/2019 (035080)

ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

Figure 8: ASEAN interconnection projects (updated in Apr 2020)

Source: ASEAN Centre for Energy’s 6th ASEAN Energy Outlook

BESS applications fit well

Additionally, storage is a necessity when thermal reserve capacity becomes limited in the

future. It can reduce and mitigate the curtailment of RE supply and convert intermittent solar

and wind generation into near-firm daily output, stabilising and smoothening electricity

output. A BESS collects energy from an electricity grid or renewable power sources, such

as solar and wind, and stores it using battery storage technology. Then, batteries discharge

and release the energy when necessary ie in peak demand, power outages, and/or in a

variety of other applications. By storing excess energy and providing reserve capacity, A

BESS can take the load off overloaded transmission & distribution (T&D) lines and prevent

congestion in transmission systems via storing excess energy and providing excess reserve

capacity. A renewable-based energy system may be fragile and vulnerable to irregular

power generation patterns without sufficient energy storage system (ESS) in place. Excess

electricity generated during the peak will be curtailed and wasted while a supply deficit will

happen during a lull.

Robust growth but rising cost could lead to project deferral

There are generally two main BESS applications – front-of-the-meter (FTM) and behind-the-

meter (BTM). FTM BESS is regarded as utility scale or grid-scale battery storage,

connecting to distribution/transmission networks or power generation assets. These utility-

scale storage capacity ranges from several megawatt-hours to hundreds. On the other

hand, BTM BESS are on-site solutions, connecting to the back of utility meters in residential,

commercial, and industrial sectors. It could also be integrated with a gas plant to extend its

lifecycle by optimising the turbine performance and reducing wear and tear.

According to Frost & Sullivan, the global grid battery storage capacity is likely to grow to

135GW by 2030 from 8GW in 2020. The market is estimated to grow at an impressive CAGR

of 23% to USD15.9bn by 2030 from USD2bn in 2020 led by continuous expansion in RE as

well as decline in technologies costs. Despite the bright outlook, we think that near-term

installation growth could slow down as a result of high inflation. Project developers have to

renegotiate contract prices with offtakers on rising cost, which could delay the

commissioning process. Additionally, there could be more project deferral and investors are

adopting a wait-and-see approach until prices trend down.

See important disclosures at the end of this report

7

Market Dateline / PP 19489/05/2019 (035080)

ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

Figure 9: BESS applications

Source: Integra Sources LL

Deployment of energy storage systems

Within the ASEAN region, Wärtsilä installed a 2.4MW/2.4MWh ESS, the first utility-scale

battery storage project in Singapore. The Finland-headquartered multinational energy

solutions provider’s project was supported by Singapore’s Energy Market Authority (EMA)

as well as energy utilities company SP Group. The ESS will participate in the wholesale

electricity market to provide services necessary to help integrate variable solar PV

generation into the grid while reducing peak demand.

Figure 10: Wärtsilä’s EMA-supported lithium-ion battery storage project

Source: Singapore’s Energy Market Authority (EMA)

See important disclosures at the end of this report

8

Market Dateline / PP 19489/05/2019 (035080)

ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

The EMA launched the Accelerating Energy Storage for Singapore (ACCESS) programme,

announcing the lithium-ion ESS trial project in 2017 and awarding it to locally-headquartered

engineering firm CW Group. CW Group and clean energy technology accelerator/incubator

Sunseap Energy Ventures picked out Wärtsilä as the technology provider and engineering,

procurement and construction (EPC) partner for the project.

Battery storage system at the Pasir Panjang Terminal: Singapore has set up a BESS to

manage peak consumption at the world's largest container transhipment hub. The project

at the Pasir Panjang Terminal is part of an SGD8m partnership between the EMA and PSA

Corporation. It is also part of the smart grid management system which can improve the

energy efficiency of port operations by 2.5% and reduce the port's carbon footprint by 1,000

tonnes of carbon dioxide equivalent (tCO2e) pa, akin to removing around 300 cars off the

road annually.

Slated to start in 3Q22, the system would provide energy to be used to run port activities

and equipment including cranes and prime movers in a more efficient way. The project had

been awarded to Envision Digital, a Singapore-based company providing artificial

intelligence and Internet technologies software, which developed a smart grid management

system that includes the BESS and solar PV panels. The platform uses machine learning

to provide real-time automated forecasting of the terminal's energy demand.

Figure 11: The battery storage system consists two battery containers and two

power conversion system (PCS) containers

Source: PSA Corporation Ltd

Whenever a surge in energy consumption is forecasted, the 2MWh battery energy storage

unit will be activated to supply energy to help meet demand. During other times, the unit can

be used to provide ancillary services to Singapore's power grid and generate revenue.

The insights from the project may also “validate” the possibility of commercial and industrial

users adopting BESS to serve multiple purposes, such as demand management onsite and

providing commercial ancillary services to support power systems. Insights from the project

will also be applied to the energy system at the Tuas Port, which will be the world's largest

fully-automated terminal, to be completed in the 2040s.

Sembcorp to build 200MW battery storage at Jurong Island: Sembcorp is building 200MWh

of battery storage systems on Jurong Island. The EMA issued an expression of interest

(EOI) in May 2022 to build 200MW/200MWh of battery storage, which resulted in the award

to Sembcorp. Sembcorp expects to complete work on the BESS deployment by the end of

this year. Sembcorp was one of EMA’s collaborators on a programme to accelerate the

deployment of energy storage in Singapore, which began in late 2018 and received the

authority’s support to build the country’s first distributed virtual power plant (VPP). EMA had

already identified the ability of energy storage to help integrate renewable energy and

enhance the overall reliability of the energy supply and grid.

See important disclosures at the end of this report

9

Market Dateline / PP 19489/05/2019 (035080)ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

Figure 12: Malaysia’s new capacity projection (MW) (2021-2039)

Source: Report on West Malaysia Generation Development Plan 2020 (2021-2039)

Malaysia is still lagging behind in terms of BESS applications. According to the country’s

Energy Commission (EC), the penetration limit for grids connected solar PV is set at 24%

of the estimated peak demand and will increase to 30% in 2035 to ensure continuity of

electricity supply in unexpected circumstances, and to cope with generation uncertainty and

availability from variable renewable energy (vRE). This is done by having new thermal

capacities to replace retired plants along the way. Besides this, the grid infrastructure would

be further strengthened and enhanced with technical enablers such as ESS. Five units of

BESS with a capacity of 100MW have been planned for installation annually into the system

from 2030-2034.

See important disclosures at the end of this report

10

Market Dateline / PP 19489/05/2019 (035080)ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

High Fuel Cost And Inflation Impact

The worst inflation in decades

With the continuous surge in commodity prices since mid-2021, fuel prices, both oil and gas,

have also spiked up in tandem with the gradual reopening of economies amidst geopolitical

uncertainties. In the past few months, we have seen acceleration of inflation across the

world, with many countries seeing the worst inflation in decades. The International Monetary

Fund (IMF) has predicted inflation to be worse in developing economies at an average of

8.7% in 2022, as compared to a projection of 5.7% in developed nations over the same

period. We see multiple repercussions arising from this monetary phenomenon and

countries around the world are facing challenges in resolving it.

Figure 13: Inflation rate, average consumer prices projection in 2022

Source: IMF

Ramping up clean energy is the solution?

Theoretically, increasing RE capacities and expediting energy transition process are the

long term solutions to reduce fossil fuel demand and thus lower its reliance. High fuel costs

may incentivise consumers to opt for electric cars in the longer run. Wind and solar are

intrinsically deflationary while fossil fuels are inflationary. The cost of generating electricity

from renewable sources has dwindled over the years, narrowing the gap with non-

renewable sources. This is mainly led by scalable granular technologies, greater innovation

to produce and deploy solar panels and wind turbines.

However, moving away from fossil fuel investment too aggressively may not be a good

option to cool down prices. The consistent underinvestment in the O&G space in the medium

term may cause prolonged supply shortages when fossil fuel demand is not being effectively

trimmed. The ultimate outcome could be O&G prices staying elevated for a longer period.

This probably explains why accelerating clean energy with more tax credits and increasing

higher oil production are both being proposed by the Biden administration to combat

inflation. US President Joe Biden has repeatedly emphasised the urgency to commit to

greenhouse gas (GHG) emission reductions while bringing down gasoline prices is also an

immediate task to be sorted. At the same time, the administration has asked Congress to

assess fees on idled wells and non-producing acres of federal lands to encourage oil

companies to produce more.

Highest emissions seen in 2021

According to IEA, global energy-related carbon dioxide emissions hiked by 6% in 2021 to

all time high of 36.3bn tonnes led by strong global economic rebound and higher reliance

on coal. The spike in gas prices have led to higher coal burning, offsetting the impact from

largest ever RE capacities growth. Emissions from coal also reached the highest level ever

at 15.3bn tonnes, accounted for over 40% of the overall growth in global CO2 emissions in

See important disclosures at the end of this report

11

Market Dateline / PP 19489/05/2019 (035080)ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

2021. This showcased that governments are forced to prioritise energy price affordability

and secure energy access, which could potentially overshadow clean energy development.

Global near-term emissions may continue to rise increase if world governments slow down

coal plant retirement plan to ensure stability and sustainability of energy supply. Meanwhile,

oil producers will spend more on upstream E&P to boost production leveraging on elevated

prices.

Figure 14: Total CO2 emissions from energy combustion and Figure 15: Change in CO2 emissions by fossil fuel, relative

industrial processes and their annual change, 1900-2021 to 2019 levels, 2019-2021

Source: IEA, Global Energy Review: CO2 Emissions in 2021 Source: IEA, Global Energy Review: CO2 Emissions in 2021

Fuel subsidy policies to challenge climate change goal

As long as fuel prices continue to stay elevated, we expect the high fuel subsidy to remain

a fiscal burden to most ASEAN countries which are oil importers, with certain degree of

subsidy in place. Fuel subsidies that reduce the price of fossil fuels are rather controversial

against the climate change strategy as it incentivises higher fuel consumption and therefore

increases carbon emissions. It will also result in an inefficient allocation of economic

resources and hinder growth. As such, clean energy development is also bogged down by

rising inflation given world governments will have relatively lesser financial capacity to grow

low emissions industry.

Subsidy reform is essential for better targeted social spending and it helps to reduce fossil

fuel reliance. At the Conference of the Parties (COP26) in 2021, 197 countries agreed to

accelerate efforts to phase-out inefficient fossil fuel subsidies. It is tough to promote subsidy

reform as it seems to be unfavourable, especially to the mass market, A more complicated

concern is the likelihood of higher inflation with a cascading effect to the overall economy.

For oil exporting countries like Malaysia, it is difficult to completely phase out subsidy.

Currently, the government is working to replace blanket fuel subsidy to targeted subsidy.

According to the Malaysia’s finance minister, Tengku Datuk Seri Zafrul Abdul Aziz, fuel

subsidy will reach MYR30bn in 2022. He also mentioned that for every MYR1 of fuel

subsidy, MYR0.53 go to the T20 (Top 20% earners), while only MYR0.15 benefit the B40

group. Therefore, a targeted subsidy will ensure the bulk of the fund is being channelled to

the targeted population.

See important disclosures at the end of this report

12

Market Dateline / PP 19489/05/2019 (035080)ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

Figure 16: Retail prices of oil products in selected countries, Figure 17: Fossil fuel subsidies in South-East Asia and oil

2020-2022 prices, 2010-2020

*Note: For Thailand, prices are weighted average monthly prices of ULG 95 and HSD Source: IEA Southeast Asia Energy Outlook 2022

B7 in Bangkok. For the Philippines, prices are common prices of RON 95 gasoline

and diesel in the first week of each month in Manila. For Malaysia and Singapore,

prices are for RON93-96. For Vietnam, prices are for RON below 93

Source: IEA Southeast Asia Energy Outlook 2022

According to Renewable Power Generation Costs in 2021, published by the International

Renewable Energy Agency (IRENA) in July this year, the levelised cost of electricity from

solar PV declined by 13% YoY , whilst onshore and offshore wind dropped by 15% and 13%

YoY in 2021. Meanwhile, the global weighted average cost of newly commissioned solar

PV, onshore and offshore wind power projects also fell in 2021 given the significant lag in

pass through to total costs. We think the escalation of raw material prices has not been

captured in 2021 due to time difference between financial investment decisions and

commissioning of the project. Generally, project cost of newly commissioned RE in 2021

has been locked in much earlier and even if there is a surge in costing, it would have been

sufficiently covered under the contingency allowances. As such, the magnitude of rising cost

pressure is largely being felt in 2022 when these new projects have to be kickstarted,

undergo procurement and construction phases. Recently, commodity prices have retraced

from the peak in response to rising recession risk and weaker economic outlook. This could

provide a breather to overall project costing.

Figure 18: Global weighted average total installed costs, capacity factors and LCOE of newly commissioned utility-scale

solar PV, onshore and offshore wind, 2010-2021

Source: Power Generation Costs in 2021, IRENA

See important disclosures at the end of this report

13

Market Dateline / PP 19489/05/2019 (035080)ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

Figure 19: Global weighted average LCOEs from newly commissioned, utility-scale renewable power generation

technologies, 2010-2021

Note: This data is for the year of commissioning. The t hick lines are the global weighted average LCOE value derived from the individual plants commissioned in each year.

The LCOE is calculated with project-specific installed costs and capacity factors. The single band represents the fossil fuel-fired power generation cost range, while the

bands for each technology and year represent the 5th and 95th percentile bands for renewable projects.

Source: IRENA Renewable Cost Database.

See important disclosures at the end of this report

14

Market Dateline / PP 19489/05/2019 (035080)ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

Carbon Pricing

Carbon pricing is now one of the most popular policy tools used to combat climate change.

It is about incorporating climate change cost into economic decision making in order to move

towards low emission or eventually net zero emissions.

Carbon tax is seen as a key policy instrument to combat climate change. It is imposed by

the government on GHG producers, which eventually incentivise them to lower emissions

or pursue cleaner approaches. The emission trading system (ETS) is also another rising

initiative which provides a platform for companies to trade emission units to meet their

emission targets.

There are generally two type of ETS schemes, namely cap and trade as well as baseline

and credit scheme. Under the cap and trade scheme, a cap is set and emissions are

monitored against this cap. Emission permits are either auctioned out or distributed for free

according specific criteria. Under a baseline and credit system, a baseline has to be set for

each emitting activity, usually based on historical emission and production rates. Polluters

that reduce their emissions below such level can earn “credits”, which can be monetised.

Started in 2005, the EU ETS is the world’s first international ETS. Operating as a cap and

trade system, EU is now at Phase 4 and the sectors covered include power and heat

generation, energy-intensive industrial sectors and aviation within Europe. The largest

carbon market by traded value, the EU ETS, saw record trading activity and prices in both

spot and futures markets in 2021. China launched its national ETS in 2021 and trading

commenced on the platform operated by the Shanghai Environment and Energy Exchange.

The first compliance cycle covers 2,162 power companies across the country, responsible

for a total of over 4bn tCO2e emissions annually (30% of national emissions).

Apart from ETS, carbon crediting mechanism is also playing an increasingly important role

in the energy transition journey. It refers to a system where tradable credits (typically

representing a tCO2e) are generated through voluntarily implemented emission reduction

or removal activities. Such mechanism is different to carbon taxes and ETSs, companies

could generate carbon credits to prove removal of emissions. In China, Chinese Certified

Emission Reduction (CCER) is the voluntary carbon credits that are certified by the Chinese

Government. Such activities include renewable power generation and waste-to-energy

projects, as well as forestry projects. With that in place, thermal generators will have to

transform their energy mix by investing in RE, to reduce emission via better technology

innovation (ie carbon capture and storage). Else, they would have to purchase emission

quota or certified carbon credit to offset (5% of annual quota in China).

Carbon pricing initiatives gaining traction

According to World Bank statistics, there are 68 carbon pricing initiatives implemented,

covering 12 GtCO2e, representing 23% of global GHG emissions in 2022. A closer look

reveals 36 of them are carbon tax while the remaining 32 are ETS. With more countries

pledging for net zero targets, we could expect more governments to adopt carbon pricing

instruments. Overall global pricing revenue increased by c.60% YoY to USD84bn in 2021

of which ETS revenue surpassed carbon tax revenue for the first time.

Rising carbon prices

Direct carbon prices have hit an all-time high in jurisdictions including the European Union

(EU), New Zealand, and etc in 2021 but experienced a dip in early 2022 following the

Russia-Ukraine war in February. Prices have started to recover but still remain below the

record high prior to the war. The hike was largely driven by more aggressive climate change

targets and policy changes amidst more stringent ETS regulations. According to State and

Trends of Carbon Pricing 2022 published by World Bank, carbon tax rates remained

relatively flat in 2020, but increased by an average of c.USD6/tCO2e in 2021. As of Apr

2022, average rates rose by another USD5/tCO2e. Most of these increases have been

previous scheduled, while some countries’ (Switzerland and Liechtenstein) 2022 hike was

led by an automatic adjustment mechanism due to the intermediate GHG targets not being

met.

See important disclosures at the end of this report

15

Market Dateline / PP 19489/05/2019 (035080)ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

Figure 20: Summary of national carbon pricing initiatives

Note: Carbon pricing initiatives are considered “scheduled for implementation” once they have been formally adopted through legislation and have an official, planned start

date. Carbon pricing initiatives are considered “under consideration” if the government has announced its intention to work towards the implementation of a carbon pricing

initiative and this has been formally confirmed by official government sources. TCI refers to Transportation and Climate Initiative. RGGI refers to the Regional Greenhouse

Gas Initiative.

Source: World Bank

Figure 21: Record high carbon tax rates in six jurisdictions Figure 22: Price evolution in select ETSs from 2008 to 2021

Note: Dotted line indicates scheduled price increases for those jurisdictions that have Source: State and Trends of Carbon Pricing 2022, World Bank

communicated future price trajectories.*Estimated path based on the government's

ambition to increase the tax rate by at least USD 1 per year, and to increase the rate

more rapidly from 2026 to reach USD30/tCO2e in 2030 and USD 120/tCO2e beyond

2050.**This is a low range projection as the Singapore government plans to reach a

carbon tax rate of SGD 50-80/tCO2e (36-58 USD/tCO2e) by 2030.***British Columbia

has committed to meet or exceed the federal benchmark carbon price.

Source: State and Trends of Carbon Pricing 2022, World Bank

See important disclosures at the end of this report

16

Market Dateline / PP 19489/05/2019 (035080)ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

Figure 23: Absolute emissions coverage, share of emissions covered, and prices for CPIs across jurisdictions

Note: Bubble size represents absolute covered total greenhouse gas emissions.

Note 2: *For CPIs that have multiple price levels, the price applying to the larger share of emissions is used.

Note 3: **This is a composite presentation representing total emissions covered by carbon pricing instruments under the Pan-Canadian Framework. It includes a combination

of ETS-like and carbon tax-like instruments, implemented at both provincial and federal levels.

Source: World Bank

Sweden has the highest carbon tax rate at EUR116.33 (c.USD137)/t of carbon emissions

in Europe, followed by Switzerland and Liechtenstein (EUR85.76) and Finland (EUR62).

Such taxes can be levied for different types of GHGs and each country will have a different

scope and regime.

Singapore is the first country in South-East Asia to introduce a carbon price. It was

introduced in 2019, at SGD5/tCO2e and is applicable on facilities that directly emit at least

25,000 tCO2e of GHG annually. We understand that the carbon tax is levied on the six

GHGs that Singapore is currently reporting to the United Nations Framework Convention on

Climate Change (UNFCCC), namely carbon dioxide (CO2), methane (CH4), nitrous oxide

(N2O), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs), and sulphur hexafluoride

(SF6). With that, the tax covers 80% of the total GHG emissions from about 50 facilities from

the manufacturing, power, waste, and water sectors.

See important disclosures at the end of this report

17

Market Dateline / PP 19489/05/2019 (035080)ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

Figure 24: Carbon prices as of 1 Apr 2022

Note: Nominal prices on April 1, 2022 are shown for illustrative purpose only. Prices are not necessarily comparable between CPIs because of (for example) differences in the

sectors covered and allocation methods applied, specific exemptions, and compensation methods.

Note 2: *The 2030 carbon price corridor is based on the recommendations in the report of the High-Level Commission on Carbon Prices.

Note 3: **Several jurisdictions apply different carbon tax rates to different sectors or fuels. In these cases, we have indicated the range of tax rates applied, with the dark blue

shading showing the lower rate and the combined dark blue and light blue shading representing the higher rate.

Source: World Bank

Voluntary carbon market (VCM)

Unlike the regulatory carbon ETS, which is mainly on certain industries and parties, the VCM

provides a platform that enables anyone to offset carbon emissions. Anyone who can be a

single person, multiple people, or an organisation can be a developer as long as they are

running an offset project. The project has to be certified on how much of carbon emissions

is avoided or removed, in which one carbon credit represents 1 tCO2e reduction. Generally,

the voluntary carbon credit (VCC) is stored in a registry owned or retained by the standard

that certified the project, and it eventually can be traded. However, it cannot be transferred

to a different registry or standard.

See important disclosures at the end of this report

18

Market Dateline / PP 19489/05/2019 (035080)ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

Figure 25: Voluntary carbon market mechanism

Source: Ernst & Young

One of the key concerns of VCM is that it may not have sufficient governance given that the

compliance market is mainly regulated by national or international public authorities while

the entities establishing the voluntary carbon credit are private entities, more often non-

governmental organisations (NGOs). They have their own criteria for the carbon offset to be

qualified in their respective registry in different names, ie American Carbon Registry (ACR),

Climate Action Reserve (CAR), Gold Standard, Plan Vivo, and Verra’s Verified Carbon

Standard (VCS).

Collaboration among the VCM stakeholders, ie project developers, governments, financial

institutions will happen to strengthen the credibility. Government involvement to provide

regulatory framework could increase the VCM’s credibility and stability. For instance,

Climate Impact X (CIX), Singapore’s voluntary carbon credits exchange is jointly founded

by Singapore Exchange, DBS Group, Standard Chartered, and Temasek, with two digital

platforms: the Carbon Exchange and the Project Marketplace.

Despite VCM is experiencing rapid growth and gaining unprecedented traction globally,

VCCs, the integration of VCM with compliance market has to be done in the longer run. This

also involves complying with emission reductions obligations ie VCC in compliance with

markets such as EU ETS.

Rising carbon pricing initiatives within the region

Singapore is the first to implement carbon tax back in 2019 and to progressively increase

over the years. We see more carbon pricing initiatives (either carbon tax or emission trading)

being scheduled for implementation or under considerations within the ASEAN region.

Indonesia, Malaysia, and Thailand have announced plans to implement carbon emissions

trading. However, the implementation timeline may be pushed back due to uncertain

economic outlook amidst a high inflationary environment, as evident by the Indonesian

Government’s recent postponement of carbon tax implementation.

See important disclosures at the end of this report

19

Market Dateline / PP 19489/05/2019 (035080)ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

Figure 26: ASEAN countries’ status on ETS and carbon tax

Countries Status Remarks

Brunei ETS or carbon tax under - Explored a preliminary scoping for carbon pricing which includes an emissions threshold

consideration as well as targeted sub-sectors

- Conducted a workshop on carbon pricing policies that aims at shaping the direction for

carbon pricing policy in the country as well as learning from the experiences of other

countries

Indonesia Carbon tax implemented - Passed a law on tax regulation harmonisation in Oct2021 which includes the

or scheduled, ETS under introduction of a carbon tax. The carbon tax was initially set to commence in Apr 2022

consideration but was pushed back to July in light of rising energy commodity prices. Recently, it was

postponed again due to constraints from uncertainty of inflation and macroeconomic

issues

- Carbon Pricing Roadmap also includes a longer-term plan for introducing an ETS and

a carbon crediting mechanism

- Looking to determine emission caps for coal-fired power stations in 2022

- Further assessing the potential application of a carbon price to other sectors (according

to sector readiness), with the aim of having a broad coverage carbon pricing policy mix

implemented by 2025.

- Working on regulations to guide the development and implementation of carbon pricing

instruments, including procedures on ETS implementation in the power sector.

Malaysia ETS or carbon tax under - Working to develop an ETS policy and implementation framework

consideration - Continues to consider the potential for implementing other carbon pricing policies,

including a carbon tax and voluntary carbon markets

Singapore Carbon tax implemented - Increasing carbon tax rate to SGD25/tCO2e (USD18/tCO2e) in 2024 and 2025, and

or scheduled, ETS under SGD45/tCO2e (USD33/tCO2e) in 2026 and 2027, to reach SGD50-80/tCO2e (USD37-

consideration 59/tCO2e) by 2030

- Placed schemes to financially support businesses’ decarbonisation efforts and will

continue to review the support measures for businesses to implement needle-moving

decarbonisation solutions to increase competitiveness

- Introduced high-quality international carbon credits to offset up to 5% of taxable

emissions which will commence in 2024

- A transition framework will also be introduced to give existing EITE companies more

time to adjust to a low-carbon economy

- Existing facilities in EITE sectors will receive transitory allowances for part of their

emissions, based on efficiency standards and decarbonisation targets

- The Government is currently consulting affected companies on the framework. Details

will be finalised by 2023, ahead of the increase of carbon tax level in 2024

Thailand ETS or carbon tax under - Developing rules and guidelines for carbon credit trading, expected to be released in

consideration 2022

Vietnam ETS or carbon tax under - Issued revised Law on Environmental Protection in Nov 2020 which confirmed the role

consideration of carbon pricing in Vietnam’s mitigation policy mix, provided the legal mandate for the

development of a domestic emissions trading scheme and a national crediting

mechanism, and assigned ministerial responsibilities

- Issued a decree in 2022 which provides a comprehensive set of regulations under the

revised Law on Environmental Protection and outlines a roadmap for the

implementation

- The decree sets forth rules for monitoring, reporting, and verification (MRV) systems

and includes provisions for developing a national ETS with a declining cap

corresponding to Vietnam’s NDC and the establishment of a national crediting

mechanism

- Anticipates launching a pilot ETS in 2026, before launching a full ETS in 2028

Source: The World Bank

See important disclosures at the end of this report

20

Market Dateline / PP 19489/05/2019 (035080)ASEAN Renewable Energy Regional Thematic

2 August 2022 Utilities | Renewable Energy

Indonesia

Indonesia’s Renewable Energy Roadmap

Clear government roadmap needs to be backed up by strong funding

Emissions reduction to mitigate the negative impact of climate change has become a shared

goal of the international community in recent years with more countries and businesses

around the world committed to net-zero emissions. The race to carbon or climate neutrality

coincides with exacerbating extreme weather events, falling renewable energy costs, and

increased awareness of climate change. To date, however, Indonesia is lagging behind

other countries by only targeting 2060 to achieve net-zero emissions despite its status as

an archipelago country that is vulnerable to climate change.

Through its Nationally Determined Contribution (NDC), Indonesia aims to reduce GHG

emissions by 29% (voluntarily), or 41% (with international support) compared to the

business-as-usual (BAU) scenario by 2030. Current NDC, however, is far from what is

needed to achieve the Paris Agreement.

The energy sector has become the second largest emitting sector in Indonesia by

contributing to c.35% of total emissions in 2021 and is projected to turn into the largest

emitter by 2030 if no decarbonisation efforts are carried out. Considering the climate

urgency, deep decarbonisation should become one of the Indonesian Government’s top

priorities for the next three decades. Decarbonisation should also be seen as an opportunity

to modernise the overall economy, avoid costs of climate damages, improve air quality,

prevent premature deaths, reduce healthcare costs, increase energy efficiency, secure

water and food availability, and preserve biodiversity.

Figure 27: Indonesia’s emissions cut target Figure 28: Source of emissions by sector (2030 projection) –

without decarbonisation scenario

Manufacturing

Peat Industry

decomposition 3%

10%

Waste

10%

Energy

Agriculture 50%

& forestry

13%

Peat fire

14%

Note: MtCO2e stands for millions of tCO2e Source: IETO 2022, RHB

Source: Indonesia Energy Transition Outlook (IETO) 2022, RHB

The pandemic has helped curb GHG emissions, mainly due to slowing economic activity.

However, to achieve the deep decarbonisation goal, structural changes are needed. The

changes, particularly, need to happen this decade to keep up with the race to zero

emissions. By 2030, Indonesia needs to see:

i. Almost half of electricity is sourced from renewable energy, up from c.12% today. Solar

power contributes the largest to total power generation at around 24%;

ii. Renewable installed capacity increase to 140GW, up from 10GW today. Solar PV

needs to grow by 10-11GW per year, around a sixth of the growth to come from rooftop

solar PV. Power grid to expand to more than 13GW with some inter-island connections

being established;

iii. Coal moratorium be imposed to peak carbon emissions by 2025. Phasing out of more

than 15-year-old-coal fired power plants will be carried out from 2025;

See important disclosures at the end of this report

21

Market Dateline / PP 19489/05/2019 (035080)You can also read