Wertschöpfungsund Arbeitsplatzeffekte von Gebäudeenergieeffizienzmaßnahmen unter Verwendung verschiedener statischer I-O-Tabellen

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

9. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

Wertschöpfungs- und Arbeitsplatzeffekte von

Gebäudeenergieeffizienzmaßnahmen unter

Verwendung verschiedener statischer I-O-Tabellen

Johannes Hartwig, Judit Kockat

Fraunhofer Institut für System- und Innovationsforschung ISI, Breslauer Str. 48, D-76139

Karlsruhe, johannes.hartwig@isi.fraunhofer.de

Kurzfassung:

Motivation und zentrale Fragestellung

Die vorliegende Arbeit quantifiziert die sektoralen Wertschöpfungs- und Arbeitsplatzeffekte

von Energieeffizienzmaßnahmen in Wohngebäuden und schätzt den Einfluss verschiedener

Input-Output (IO) -Tabellen auf diese Effekte ab. IO-Tabellen beschreiben in der

volkswirtschaftlichen Gesamtrechnung die Produktionsprozesse anhand der Werte der

eingehenden Waren und Dienstleistungen sowie des ausgehenden Produkte in einem

bestimmten Jahr.

Die Beurteilung von sektoralen Wertschöpfungs- und Arbeitsplatzeffekten wird in der Regel

entweder mit statischen oder dynamischen Input-Output (IO)-Modellen durchgeführt, welche

eine bestimmte Jahrestabelle als Basis verwenden. Diese Vorgehensweise lässt strukturelle

Änderungen beispielsweise in den Produktionsprozessen außen vor. Wir haben versucht,

diese Unsicherheit, welche sich durch die Wahl des Basisjahres ergibt, zu minimieren, indem

von einer Zeitreihe mehrere IO-Tabellen verwendet werden. Als Beispiel wurden die

Energieeffizienzmaßnahmen in deutschen Wohngebäuden untersucht. Hierfür wurden die

Zusammenhänge der damit verbundenen Finanzierungs-, Investitions- und

Konsumveränderungen aufgezeigt.

Methodische Vorgangsweise

Die Modellierung des Wärmebedarfs im Gebäudebereich erfolgte mit dem Modell EE-

Lab/INVERT auf Basis des deutschen Gebäudebestandes von 2010 [1]. Ausgehend vom

20-Prozent-Wärmeminderungsziel aus dem Energiekonzept der Bundesregierung [2] wurde

für das Jahr 2020 der zusätzliche Investitionsbedarf für Wohngebäudesanierungen ermittelt.

Die Unterscheidung zwischen Eigentümer und Nutzer erlaubt Zuordnung dieser

Gebäudeinvestitionen auf verschiedene Sektoren in den volkswirtschaftlichen Konsum- bzw.

Investitionsvektoren. Mittels der Input-Output-Analyse können dann diese direkten Konsum-

und Investitionseffekte um eine Abschätzung der indirekten Effekte erweitert werden.

Da die Input-Output-Tabellen in den Preisen des jeweiligen Jahres veröffentlicht werden,

müssen die Konsum- und Investitionsvektoren zunächst deflationiert werden, um dann eine

statischen Input-Output-Analyse [3] auf Basis der Jahrestabellen des statistischen

Bundesamtes von 1995 bis 2007 anwenden zu können. Die resultierenden

Wertschöpfungsveränderungen werden auf 2010er Euro-Werte wieder inflationiert, um eine

Vergleichbarkeit zwischen den Jahren sicherzustellen.

Seite 1 von 20

9. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

Die Arbeitsplatzeffekte werden mit Hilfe der Sattelitenaccounts des statistischen

Bundesamtes berechnet. In den Sattelitenaccounts sind den Löhnen und Gehältern aus der

IO-Tabelle die Anzahl der Arbeitnehmer (Vollzeitäquivalente) und die Anzahl der

Erwerbstätigen1, unterschieden nach Sektoren, zugeordnet. Dadurch ergibt sich für die

Arbeitsplatzeffekte eine andere Entwicklung als für die Wertschöpfungseffekte.

Ergebnisse und Schlussfolgerungen

Die Gebäudemodellierung ergab einen zusätzlichen Investitionsbedarf von 6,88 Mrd.

EUR2010. Bei einem Anteil von 26,4% Vermietern ergibt sich dadurch einen Mehrkonsum

des Bankensektors von 241 Mio. EUR2010 sowie 2,20 Mrd. EUR2010 an Mehrausgaben für

Miete.

Die größten positiven Effekte auf die Wertschöpfung gab es erwartungsgemäß im Bausektor

mit einer Steigerung von 7,9% (bezogen auf die Tabelle von 2007, siehe Abbildung 1). Auf

Rang zwei und drei der größten Effekten stehen mit sinkender Wertschöpfung die

Energiesektoren Strom- und Fernwärme (-8,7%) sowie Kohle (-7,3%), was auf die

Energieeinsparungen zurückzuführen ist. Das zweitgrößte Wachstum zeigt der Sektor

Wohnungswesen mit 1,1%. Ursache hierfür ist die Kapitalfinanzierung der

Effizienzmaßnahmen durch Miete. Die Sektoren Holz- und Kunststoffwaren und Anlagen

(Geräte) für die Stromerzeugung sind Vorleistungen für den Bausektor, wobei letzterer mit

z.B. Kabeln, Schaltern und Leuchten den größten Anteil der Vorleistungen beiträgt. Die

Effekte in diesen Sektoren sind daher indirekt und fallen deutlich schwächer aus. Bei den

Erwerbstätigen dominiert der Wachstumseffekt im Bausektor noch deutlicher aufgrund des

hohen manuellen Arbeitseinsatzes im sektoralen Vergleich.

10 120

Erwerbstätigenänderungen in Tsd. Personen*

8

100

Wertschöpfungsveränderung* in %

6

4 80

2

60

0

40

‐2

‐4 20

‐6

0

‐8

* unter Verwendung der IO‐Tabelle von 2007 * unter Verwendung der IO‐Tabelle von 2007

‐10 ‐20

Abbildung 1: Ergebnisse der sektoralen Wertschöpfungs- und Arbeitsplatzeffekte der

Gebäudeeffizienzmaßnahmen

Im Jahresvergleich zwischen den Basisjahren 1995 bis 2007 unterscheiden sich die

Wertschöpfungs- und Arbeitsplatzeffekte kaum in ihrer Richtung, aber in ihren quantitativen

Effekten, wie Abbildung 2 zeigt. Die Impulse der betroffenen Sektoren fallen umso stärker

1

ebenfalls Vollzeitäquivalente aber beinhaltet neben den Angestellten auch die

Selbständigen

Seite 2 von 209. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

aus, je weiter die Input-Output-Tabellen zurückliegen, weil die betroffenen Sektoren in den

älteren IO-Tabellen einen größeren Anteil an der Gesamtwertschöpfung einnehmen.

Interessant für weitere Analysen wäre eine Unterscheidung nach Preiseffekten und

technischem Fortschritt, was zusätzlich zur klassischen Input-Output-Analyse ergänzende

Mengengerüste und sektorale Preisniveaus erfordert.

0.40

0.35

0.30

Veränderungen im Vergleich zur Basis in %

0.25

0.20

0.15

Produktionswert

0.10 Erwerbstätige

Arbeitnehmer

0.05 Nachfrageimpuls

0.00

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Input‐Output‐Tabelle des Jahres ...

Abbildung 2: Vergleich der Gesamteinflusses der verschiedenen Input-Output-Jahrestabellen

Literatur

[1] Diefenbach, Nikolaus; Cischinsky, Holger; Rodenfels, Markus; Clausnitzer, Klaus-Dieter (2010): Datenbasis

Gebäudebestand. Datenerhebung zur energetischen Qualität und zu den Modernisierungstrends im deutschen

Wohngebäudebestand. 1. Aufl. Institut Wohnen und Umwelt GmbH (IWU). Darmstadt

[2] Öko Institut, Fraunhofer ISI: Klimaschutzszenario 2050. Erste Modellierungsrunde. Studie im Auftrag des

Bundesministeriums für Umwelt, Naturschutz, Bau und Reaktorsicherheit. Berlin, 2014.

[3] Miller, Ronald E.; Blair, Peter D (2009): Input-output analysis (2. ed.). Foundations and extensions. Cambridge Univ. Pr.

Keywords: Building insulation, Input-Output analysis, sensitivity analysis

1 Introduction

Assessing sectoral macroeconomic policy effects is generally based at least partially on

some sort of Input-Output (IO) model (West, 1995). IO tables are published on a yearly basis

in all Western countries offer a statistical description of production interdependencies and

demand quantities of an economy (Miller and Blair, 2009). The industry linkages are found in

the technical coefficients, showing the value of sectoral intermediate inputs to gross outputs

of each sector. IO tables are published in matrix forms.

Seite 3 von 209. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

However, since IO models are a mere statistical description of an economy, the technical

coefficients of a given year, supposed to represent the production recipes of one sector, are

prone to changes. Analyses over longer horizons which are based on one single year can

give a less accurate picture of the impacts of policy chances. IO analysis in its basic form is

static and transforming them into truly dynamical models requires a change in the technical

coefficients (Leontief and Duchin, 1986). Those coefficients can change quite substantially,

even for some industries, which are rather stable in their production technology, like the

construction sector (Pietroforte and Gregori, 2003). While there are possibilities to alter these

coefficients, Richter (1991) has shown in his overview that reasons for a change in those

technical coefficients may be due to technical changes in general, price changes or changes

in the product mix.

An understanding of how these coefficients may change over time requires a deep

understanding of the production technologies currently present in the sector as well as

forecasts or assumptions on future developments of those production technologies. If one is

concerned about the development of more than one sector at once, these technological

changes can become overwhelmingly difficult. Usually, this is the case in impact assessment

studies. Not only do effects compound, they overlap, and it requires more than detailed

insights into the structural composition of the sectors in question. This is more than often

asked for too much.

In this paper we embarked on this problem by another approach: we modelled future energy

demand in Germany’s residential buildings in a base2 scenario (Repenning et al., 2014), then

tried to achieve the heat demand reduction goal for 20203 as stated in the national energy

concept in an alternative scenario (BMU, 2011). The difference between those two scenarios

represents the impulse on the macro economy and is finally fed into a series of IO-tables

(Destatis, 2010) for a conventional static IO-analysis (Miller and Blair, 2009). The IO-tables

from the Federal Statistical Office served as a kind of sensitivity analysis of the

macroeconomic changes imposed by the detailed sectoral model of the real estate sector.

The changes in the detailed model of the housing sector, which we call for convenience

bottom-up model (bum) in the remainder,4 do not only concern the construction sector as

deliverer of building insulation installation services (the material required for this is supposed

to be contained in the intermediate deliveries of the construction sector). The bum changes

impact also on energy demand (which ought to be negative, as stated by the reduction

goals), rents and financial services for financing the extra insulation.

2

In the base scenario policy measures implemented until September 31st 2012 were

considered.

3

The heat reduction of 20% until 2020 was not to be achieved with realistic retrofit rates,

thus we arranged the scenario to stay on track for the 2050 primary energy reduction goal of

80%

4

We defined the notion of bottom-up due to the concrete demand forecasts, which in the

model of the housing sector is microeconomic, while Input-Output tables are

macroeconomic.

Seite 4 von 209. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

2 Methods

The heat demand was simulated with the model EE-Lab/INVERT, using the German building

stock of 2010 with updates for retrofit action from Diefenbach et al. (2010). A detailed

description of the model can be found in Kranzl et al. (2013)5.

The scenario was constructed according to the climate protection scenario 2050, a study for

the German Federal Ministry for the Environment, Nature Conservation, Building and Nuclear

Safety (Repenning et al., 2014). This report provides a detailed description of the

assumptions underlying this scenario regarding socio-economic developments like economic

growth, energy prices and population development. The energy saving goals of the German

government for 2020 defined the investment requirements for insulation in that scenario.

2.1 From efficiency measures to macroeconomic impulses

We restricted our analyis on only residential living space is included in the analysis, as

shown in the owner-user scheme of the building stock given in table 2-1. Non-residential

buildings and spaces are excluded, for several reasons. First, the buildings vary considerably

in their use and energy demand. In addition, more assumptions are necessary to cover the

investment decision processes of companies. Finally, company tenant payments are

intermediate inputs in the Input-Output (IO) tables and a true consideration would require a

manipulation of the technical coefficients. Though a manipulation of the matrix of

intermediate deliveries can be done with RAS-like algorithms (Junius and Oosterhaven,

2003), this is contra productive for a main focus of this paper: assessing the effect of using

IO tables from different years with the same policy impulses.

We have identified, that the energy saving measures chosen by the investor, which is mostly

the owner, have the following impulses on the macro economy.

investments cause the final demand (investment for firm-owned facilities and

consumption for private households)6 in the building sector to go up

financing the investment causes additional final demand (consumption) in the credit

businesses

increase of the rent accumulated over time causes an increase final demand in real

estate / housing (consumption)

5

www.invert.at

6

Note here that there is distinction between the microeconomic understanding of

investments, which are financial commitments whose use extends over a longer period and

the macroeconomic understanding of investments, which is done by firms. All financial

payments done by private households are categorized as consumption in macroeconomics.

Seite 5 von 209. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

energy savings reduce the final demand (consumption) in the energy sector

2-1: owner-user scheme for buildings

owner

private housing other

household industry companies

poo

private

owner-

household n/a n/a

occupier

private owner-

household occupier

user p2p h2p not in scope:

tenant private-to- housing-to- industry

private private buildings

owner-

not in scope:

companies occupier n/a

non-residential use

tenant

The private household as an owner-occupier invests in a measure increasing the energy

efficiency of the building envelope or in a renewable heating system. In the year of the

implementation of the measure the whole investment flows into the building installation

sector (CPA 45.3 - 45.5). Thus, final demand for building installations in the consumption of

the private households grows. In the following years, the private household saves energy

cost due to the implemented measure. Therefore, the expenditures for energy (CPA 40, 10)

rise in the consumption vector. For financing the investment there are three sources.

Energetic retrofit is supported by the government through subsidies. Another part of the

investment can be financed by credits and the rest from private savings. We assume that

50% of the investment is financed through credits. The service fee charged by the credit

intermediary is assumed to be 7% of the credit volume. This charge represents the impact on

the credit business’ final demand (CPA 65) in the year of the investment. The second

financing source, the savings, reduces the private households’ capital and may also lead to a

calculated value increase of the building. However, both of these effects are genuinely only

included in flow-of-fund analysis of national accounts, which are not published as regularly as

IO tables.7 Apart from that, the main impact of public subsidies - the third financing source -

takes place in the decision making phase for energetic retrofit, happening prior to the

7

A Social Accounting Matrix (SAM) for Germany was officially only published for the year

2000. It would have been inconsistent using Io tables differing yearly and one single SAM.

Seite 6 von 209. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

macroeconomic impact. Thus, the effect of subsidies on the macro economy is not in the

scope of this analysis.8

When a private landlord invests in efficiency measures in buildings the same approach is

taken with one addition: the increase in rent for energetic improvement. In the years following

the landlord, thus, receives up to 11% of the expenses according to BGB §559. These

additional rental expenses of the private occupier increase the consumption of the private

households for services for real estate and housing (CPA 70). We assumed that the landlord

elevates the rent by the maximum allowed, i.e. 11%. In reality, such an increase can not

always be realized, for example in shrinking areas. However, we need to use this rate, since

empirical data is not available.

2-2 CPA-No. and sector description

CPA-No. Sector description

10 Mining of coal and lignite

20 Manufacture of wood and wood products

25.2 Manufacture of plastic products

28 Metal products

31 Manufacture of electrical machinery and apparatus

40.1, 40.3 Electricity and steam supply

40.2 Gas manufacture and distribution

45.3 – 45.5 Building installation

51 Wholesale trade

52 Retail trade

60.1 Railway transport

65 Financial intermediation

67 Activities auxiliary to financial intermediation

70 Real estate activities

74 Other business activities

75.1 – 75.2 Public administration and defense

8

It could be argued that subsidies would alter the primary input matrix of the IO tables, but

this would not affect the construction sector, only the sector of rental services. Since we

deduct those subsidies from the increase of rents we made sure that the subsidies did not

artificially increase our results.

Seite 7 von 209. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

How does the investment influence the macroeconomic impulse if the landlord is a housing

association or company instead of a private owner? In contrast to the investment of a

private landlord, the investment of a company does not affect the consumption vector but

increases the capital investment in the building sector.

The final demand impulse, shown for 2010 in table 3, is the interface between the bottom-up

building simulation and the macroeconomic calculation.

2-3 Final demand impulse for 2010

Sector Additional expenses (in Mio. EUR2010)

Building installation 8,670

Electricity and steam supply -5,690

Financial intermediation 303

Auxiliaries to financial intermediation 3,665

2.2 From impulse to macroeconomic impact

For evaluating the macroeconomic impact we used the static Input-Output model (IO-model),

according to Holub and Schnabl (1994). The model

xt = Atxt + yt (1)

with At as the matrix of intermediate inputs and yt as the final demand vector of a given year

t. This model has the solution

x = (I - A)-1y (2)

(or x = Ly with the matrix M ≡ (I - A)-1 as the Leontief inverse) (Miller and Blair, 2009).

The current final demand vector yt consists of invest, consumption, government expenditures

and exports.

y = I + C + G + Ex (3)

It results from statistical data supplied by the German Federal Statistical Office (Destatis,

2010). We change the consumption component of this final demand vector using the

investment data for energy efficiency measures in buildings from the simulation model,

according to the final demand impulse scheme, as given by table 3. This new final demand

vector ytN results from the deduction of savings in heating expenses (h) and the addition of

the extra expenses for insulation (i), credit services (c) and rents (r). The subscript t denotes

the (base) year of the Input-Output-table, ranging from 1995 to 2007.9 The expenditure

changes are deflated to every year t with a common deflator d for all e:

9

A detailed explanation for the choice of this period is given below.

Seite 8 von 209. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

ytN = yt + dt[ei,c,r - eh] (4)

The change to the elements of the final demand vector ytN is described in detail in section

2.1, where each of the items from the list 2.1 corresponds to a value in e.

While ytN is given with price levels of the (base) year t, the inputs ei,c,r,h are given in price

levels of 2010, as the model of the real estate sector is calibrated against this year. Thus, we

inflated ei,c,r,h to each of the years t of the Input-Output-tables with a deflator dt. Since we are

mainly interested in changes evoked by the model (the additional extra expenses are the

direct effects and the model gives the indirect effects of the policy changes), we calculated

the respective ∆v for gross value added (GVA), which is given by the following equation:

∆v = v’ (I - A)-1 ytN /v’ (5)

After having obtained ∆v, these values were inflated with 1/dt to the price level of 2010 for

making the results comparable. We used the overall price level of the German Federal

Statistical Office, sine no official data on sectoral price levels in the required classification are

published. Furthermore, while an aggregated price level would seem desirable, it imposes

some serious problems in the price corrections of the inter-industry relationships, something

which we avoided by our approach. Nevertheless, there remains a problem of how to

distinguish changes in the quantity, prices and inflation, whose variations are normally

eliminated congruently, using the Laspeyres price chain index (Reich, 2008).

Sectoral labour requirements are published as a satellite account by the Federal Statistical

Office (in the primary input matrix only aggregate wages payments are found), which is the

row vector l’ (both for employed persons and employees). Underlying these figures is

sectoral labour productivity. Calculating the direct and indirect additional labour requirements

by the policy changes is done by the following equation (Leontief, 2008):

∆l = l’ (I - A)-1 ytN /l’ (6)

For the sensitivity analysis we vary the macroeconomic data set A by base year t. The varied

data sets form different starting points for the IO-Analysis. Our intent is to measure how

much the resulting sectoral gross output and employment will vary.

Thus, we applied the same (inflated) input data on the IO-tables from the Federal Statistical

Office from 1995 to 2007. Within this time span, the same sector classification (WZ 2003)

was used (Destatis, 2008). We decided not to extend the analysis to the IO-tables from 2008

to 2010, since it would have been necessary to split two of our input data:

the sector for generating electricity and heat, CPA (Classification of Products by

Activity) Code 40.1-40.3 (WZ 2003) is in the new classification (WZ2008) split into

CPA Code 35.1, 35.3 (grouped) and 37-39 and

the sector for renting CPA 70 (WZ 2003) is split into CPA 41 (WZ 2008) and CPA 68

(WZ 2008).

While especially for the latter case it could be argued that the effects of splitting are minor, as

the share which ought to be put into CPA 41 (WZ 2008), we do not want to produce any

artifact of the indirect effects of the impulses. Furthermore, it would be hard to distinguish

between the effects resulting from an updated data base and the effects which come from a

different sectoral classification.

Seite 9 von 209. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

Figure 1: Impulse flow in the IO-Table

For the illustration of the macroeconomic impact we chose the change in gross value added

and the gross output. The gross value added, is the value the sector directly produced

excluding the value that other sector generated previously. Whereas, the gross output shows

what each sector produces including the intermediate inputs. In other words: gross value is

gross output minus intermediate inputs.

The direct impacts of the additional investment are for example the building sector receiving

the retrofit investment or the energy sector loosing energy demand and income. These

effects are included in the final demand vector shown in table 3. Indirect effects are

calculated by employing equations 5 and 6 on the complete IO-Table. An increase in the

building sector will affect the dependent sectors, like manufacture of wood and wood

products sector and as their input requirements grow other sectors might be affected. These

indirect effects are included in the gross value added and in the gross output.

3 Results of the bottom-up building simulation

To analyze the effect of additional measures in energy efficiency in buildings, we need to

compare the KS80, reflecting the German energy saving goals, to a base scenario (base)

Seite 10 von 209. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

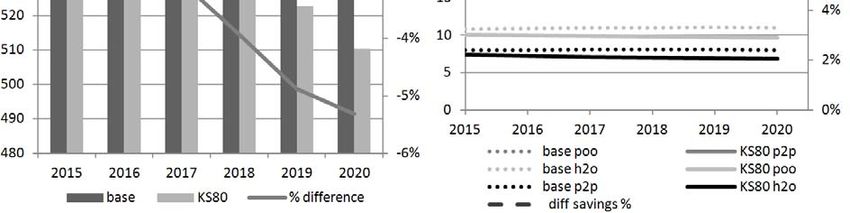

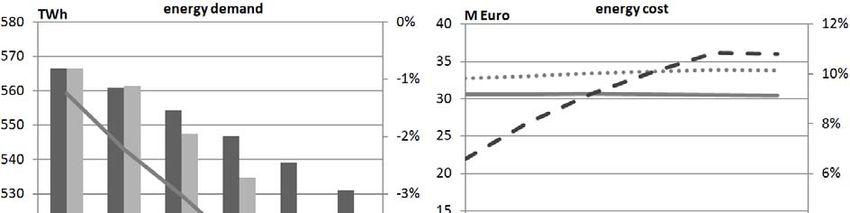

including only political action that has been decided on as of 31.September 2012. Figure 2

shows the steeper decline in KS80 as it spreads away from the base scenario ending up with

a difference of -5.5%. Interpreting these data, we have to keep in mind that the additional

efficiency measures in this scenario only kicked off in 2014. Thus, the 5.5% additional

savings represent 6 years of efficiency measures, where each year another approximately

1% of the stock. Each of these years more, additional annual energy savings are

accumulated, in this case almost 1%. This is will continue for 20 - 30 years based on the

retrofit and heating system exchange rate, since the measures have such long lasting effect.

Caused by the decrease in energy demand but also by the fuel switch, the energy savings

rise up to 11% until 2020, see figure 2. In absolute numbers the energy cost shift, meaning

that rising energy prices balance out the shrinking energy demand.

Figure 2: Energy demand (left) and energy cost (right) for KS80 and base scenario and percentage

difference

In all sectors the consumption of the private households outweighs the investment of

companies due to the higher share of privately owned buildings, i.e. around 80% of the living

space. The additional energy efficiency measures in scenario KS80 lead to an increased

annual national expenditure of 8.8 billion Euros in 2015 and similarly 8.7 billion Euro in 2020.

This includes the both expenditure categories, those of private households affecting their

consumption and those of companies increasing their investment. The term investment in the

national accounting meaning of the word only includes those expenditures that are made by

companies, where "investments" by private households are included in the consumption

section. This differentiation is made for further macroeconomic analysis, that may use the

data for an in depth review. In the building installation the consumption the households is

lower in 2015 that in 2020, whereas, the investment of the companies increase.

This is not a systematic development, but rather a temporary glance reflecting the additional

building expenses of one scenario compared to another. In the AMS scenario the renovation

rate was carried forward in a "natural" development dependent on the building age. In the

Seite 11 von 209. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

KS80 scenario the renovation rate was increased starting in 2014 trying (and failing) to

achieve the 2020 savings goal. Thus, the retrofits were many and the investments already

quite high in 2015. Hence, from 2015 to 2020 the number of retrofits did not increase as

much in the KS80 compared to the AMS. Subsequently the additional investment is also

lower.

The financial intermediation with its credit business development follows the one of the

building installation sector, due to the tie through constant parameters, the share of financing

and the profit margin, for both households and companies. The total real estate activities,

that is the sector including the rents, grow at the about same 170% as the energy savings

between 2015 and 2020.

3-1 Consumption and investment impulses

Sector Additional effect 2015 MEuro 2020 MEuro

Building installation consumption 8,107 6,884

investment 712 1,786

total 8,819 8,670

Financial intermediation consumption 284 241

investment 25 62

total 309 303

Real estate activities consumption 1,283 2,198

investment 922 1,467

total 2,205 3,665

Electricity and steam supply consumption -3,388 -5,690

4 Results of the macroeconomic analysis

Gross output, represented by the solid line in figure 3, increases by 0.34% in 2020 when

applying the IO-Table of 1995, i.e. assuming that the national economy in 2020 will be

structured like in 1995. The illustration shows the declining impact of the efficiency measures

when the different structures of 1995 until 2007 are assumed. Applying the IO-Table of 2007

merely leads to an increase of 0.206%. The impacts on employed persons and employees10

are both declining, though the gap between the two widens, being 0.01 percentage points

with the table of 1995 and 0.53% with the one of 2007. It seems like the indirect effects

cause more freelancers to be employed.

10

Employed persons include freelancers

Seite 12 von 209. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

Figure 3: Changes compared to each baseline year

Final demand development represents the direct effect or the impulse (or ytN in equation 4).

So there is a shrinking impact of the direct effects over time, which is only a result of a

different composition of y in equation 3. Indirect effects are calculated with equations 5 and 6

for gross value added and employment and include both the direct effects and changes due

to the different intermediate delivery matrices in the base years (the A-matrix of equation 1).

While indirect impacts are higher, using the IO-Tables from 1995 to 2001, the picture

changes after 2001: the impact on gross output is lower than the final demand impulse. This

is due to the growing influence of the energy savings, causing a higher effect on gross output

over time. In addition, the input coefficients of the IO-tables provide further explanation. The

construction sector needs less intermediate deliveries in 2007, i.e. 42.6% of the gross output

of the sector, than in 1995, 54.3%. In the energy sector a reverse trend can be observed with

the share in 1995 being 41.2% of its gross output and 49.2% in 2007, indicating that the

indirect effects triggered by this sector rise.

Not only the share of intermediate inputs changes; the structure of the coefficients changes

as well. Analyzing the energy sector, the total input share of the coal sector is 14.7% in 1995

compared to 4.7% in 2007. There is a shift of energy carriers away from coal towards gas

and electricity. The intra-industry production within the energy sector, i.e. the intermediate

deliveries that remain within the sector, has a share of 1.6% in 1995 compared to 19.3% in

2007. This development of indicators indicates that over time the own energy need of the

sector increases.

The declining impact is not resulting of a decline in importance of the sectors which received

an impulse, as can be seen from figure 4. The share of the sectors of overall private

consumption is relatively stable; for real estate activities it is around 20%, for financial

intermediation between 3% and 4%, for building installation between 4% and 5% and, for the

sector receiving a negative impulse, electricity and steam supply, it is around 2%.

Seite 13 von 209. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

Figure 4: Sectoral consumption shares

This means, on the other hand, that the declining overall impact of the suggested policy

impulses is mostly due to changes in the matrix of intermediate deliveries (the A-matrix in

equation 1). Apparently, the sectors involved in the final demand change trigger less and less

intermediate deliveries. Nevertheless, the basic structure of production does not change

fundamentally, as a common fundamental structure of production in modern economic

systems is supposed (Simpson and Tsukui, 1965). This becomes evident in the following

detailed analysis of sectoral changes in gross value added and employment.

Figure 5: Changes in sectoral gross value added

Seite 14 von 209. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

Figure 5 gives the resulting changes of sectoral gross value added for the Input-Output-table

of 2007, which has been calculated with equation 5. The solid stacks are the values obtained

by using the Input-Output-Table from 2007; the thin lines give the range (minimum and

maximum values) and averages for all analyses from 1995 and 2007. We only showed

sectors with a change either bigger or lesser than 0.5%. The numbers are the CPA-numbers

of the sectors.

What can immediately be seen from figure 5 is that the values for the table from 2007 are in

the majority of cases the minimum from all analyses. This observation is quite in line the

aforementioned decreasing impact of the policy changes, due to a lesser weight of the

sectors included in the direct impacts.

Figure 6: Changes in sectoral requirements for employed persons

The direct and indirect impacts on employed person requirements on a sectoral level are

given by figure 6. They have been calculated by equation 6. We only considered sectors with

a change bigger than 1500 or less than minus 500 persons.

5 Discussion

The results of the Input-Output analysis indicate that the construction sector is above-

average interrelated in the economy, if one looks at the average of intermediate delivery

input share of all sectors, compared to overall production. Where the average over all sectors

from 1995 and 2007 is between 0.419 and 0.447, the input share for the building installation

sector is between 0.526 and 0.573. Thus, the building installation sector is among the 20% of

the most interrelated sectors in the German economy.

Seite 15 von 209. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

This is supported by the findings from Pietroforte and Gregori (2003), who showed for the

German pre-reunification period a larger impact for the German construction sector,

compared to other OECD countries. The peak in 2005 of overall production output can be

interpreted as a statistical artifact of the building boom, something which is even more

striking regarding the subsequent relative decline of the production output gain.

The analysis for a single year is blurred by cyclical behaviour of the economy. Recognizing

such business cycles is a general problem in macroeconomic analysis. A business cycle can

be characterized by an expansion and a subsequent contraction, the former separating the

latter by a peak and a trough, reversely, and lasts on average about 7 years, with 6 years of

expansion and 1 year of recession (Mostaghimi, 2010). While taking account of the period

from 1995 to 2007 in our analysis, these 13 years would be roughly equivalent to 2 full

business cycles. So while analyzing different IO-tables, it may be possible leveraging out the

influence of the business cycles on our results with average values. This supports a higher

robustness of the results. Furthermore, the real estate market (and its immense impact on

the construction sector) is probably prone to a time lag from the overall business cycle

(Schmoll, 2007).

Usually, the demand for housing services is income-dependent and changes both in income

and prices are depicted by the income elasticity of demand (Schmoll, 2007). The same

usually applies to other demand categories, but with different income elasticities. In our

analysis we did not account for possible elasticity changes, so demand is totally inelastic in

our case. This is not uncommon for IO analysis, since they do not refer to any underlying

microeconomic model. However, in going from a static IO-based model to a dynamic model,

this feedback effect should be accounted for (and also possible rebound effects from energy

savings (Berkhout et al., 2000)). It should be noted, though, that this would require the real

estate market being a perfect market, which is quite far from reality (Schmoll, 2007).

Energy demand reduction was calculated as a percentage change from the electricity and

steam supply sector (see equation 4). A simplification was chosen as those sectors also

contain electricity and steam distribution, whose demand admittedly does not shrink linearly

with overall electricity demand. However, since no better data basis was available to account

for this fact, this simplifying approach was justified. Furthermore, the standard assumption in

IO-analysis is operation under full capacity utilization, so it is hard to find a better way with

dealing with this fact in the theoretical framework of the static IO-analysis. Distributional

demand from non-consumers is part of the intermediate delivery matrix of the respective

sector, supporting our linear approach.

Ecological modernisation measures are treated no other than general real estate

modernisation and annually 11% of it can be assigned to rent increases, according to §559

BGB. However, interest subsidy loans have to be accounted for (Jaeger, 2014). Since this

decision is subject to the current price level in the region of the real estate and the socio-

economic situation of the tenant has to be accounted for, it is not always given that rents

increase accordingly. Thus, there is some uncertainty in this decision, which we cannot

consider in our analysis.

The matrix of technical coefficients, which is the first (and main) driver for inter-temporal

differences in gross value added changes, is, like the whole Input-Output-model, descriptive

and not normative. That is, an efficient allocation of goods is already assumed, as well as full

Seite 16 von 209. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

capacity utilization. This is important to notice, since changes in the technical coefficients

may stem wither from volume changes (which is equivalent to a change in the production

recipes of the sectors) or from price changes of the intermediate goods (Richter, 1991).

However, with only taking the official Input-Output-tables as analytical device, it is not

possible to separate these two effects.

The size of the manipulated sectors being the second driver for intertemporal differences in

gross value added changes leaves room for interpreting the consumption shifts in observed

utility. However, this needs a much more thorough inspection and interpretation as what this

analysis could possibly deliver. An analysis is not possible to do with solely relying on

aggregate data, such as a representative household. Different household types are known to

exhibit quite different consumption patterns (Wier et al., 2001), which are heavily influenced

by income, but also by other socio-cultural and demographic factors as e.g. household size.11

Furthermore, possible price effects in the final demand vectors can also only be separated if

one possesses additional information.

6 Conclusions

Based on the results presented in sections 3 and 4 we quantified the gross economic output

and the number of employed persons to grow about 0.27 % and 0.30 % on average, caused

by additional energy efficiency measures in buildings. We also found that the effect

decreases over time due to the structure of the economy as represented by the different

Input-Output (IO)-Tables. Thus, the impact on the gross output shrinks by 0.13 %pts,

whereas the number of employed persons only shrinks from 0.35 % to 0.28 %, depending on

base year macroeconomic structure. This overall impact on the macro economy mainly

triggered by an 8.3 % increase of the gross value added in the buildings sector, whilst the

energy sector decreases by around 8%.

We consider two implications of the presented results. Firstly, the positive macroeconomic

impact can contribute to the profitability of building retrofit. Due to their large investment and

long cycle efficiency measures in buildings are often unattractive with inherent long term risk

and, if ambitious, possible failure to be profitable for the investor. However, the invested

money is not lost; it is fed back into the economy and leads to increased production and

employment. Secondly, when comparing different studies assessing the macroeconomic

impact of measures in the building sector, one has to be aware of the range of 0.07%pts

(employed persons) to 0.13%pts (gross output) that results vary depending on the year they

are based on. This error range is only valid for the building in Germany and base years

between 1995 and 2007. We did not cover product or process improvements that are

triggered by increased production, i.e. retrofit.

11

The impact of socio-cultural variables on energy consumption is of minor importance (Wier

et al., 2001), but placement does play a role.

Seite 17 von 209. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

Our method has its clear limitations: static IO-analysis cannot take price effects into account

which constitute a feedback from price changes (and possible economies of scales) to

physical quantities, which is excluded by the Non-Substitution Theorem imposed by the

production function (Duchin and Steenge, 2007). This limitation is also important concerning

income elasticity effects for the consumer, which would have to be implemented

exogenously. Finally, aggregation errors are also unavoidable in IO-studies (Rueda-

Cantuche et al., 2013) and one could consider splitting the energy savings to different

sectors. We decided not to as this would have imposed further assumptions on the interface

between the bottom-up model and the IO-table.

Capital flows are not part of the official IO-publications from the German Federal Statistical

Office, so we had to establish own assumptions on capital flow effects. Furthermore, we did

not extend our analysis to the most recent IO-tables, since they are published with a different

classification of economic sectors. We could not distinguish in our analysis whether observed

effects are caused by price or quantity changes, which is only possible with a decomposition

analysis drawing on further external assumptions. We restricted our analysis to changes in

2020. The bottom-up model would allow further time steps, but since IO-analysis becomes

less accurate over time, the evaluation of effects becomes less valid.

The limitations of our study are also beneficial as the results are easily reproducible and we

are not concerned with the validity of external assumptions since we stick strictly to the basic

framework. Nevertheless, our approach of using a time series of IO-tables offers one

cornerstone for a challenge to the vast majority of IO-studies: the issue of sensitivity analysis

(Dietzenbacher et al., 2013). Normally, IO-studies (or studies based on the IO-methodology,

like CGE models (Rose, 1995)) either take the last table published or a table in a year where

business cycle influences are thought to be minimal. We conclude that our approach gives

more insight and a more balanced view of possible indirect macroeconomic effects.

References

Berkhout, H., Muskens, J. C., and Velthuijsen, J. W. (2000). Defining the rebound effect.

Energy Policy, 28:425–432.

BMU (2011). Das Energiekonzept der Bundesregierung 2010 und die Energiewende 2011.

Technical report, Bundesministerium für Umwelt, Naturschutz und Reaktorsicherheit -

Federal Ministry for the Environment, Nature Protection and Nuclear Safety.

Destatis (2008). Klassifikation der Wirtschaftszweige mit Erläuterungen. Technical report,

Statistisches Bundesamt (Federal Statistical Office).

Destatis (2010). Volkswirtschaftliche Gesamtrechnungen. Input-Output-

Rechnung. Fachserie 18 Reihe 2, Statistisches Bundesamt (Federal Statistical Office).

Diefenbach, N., Cischinsky, H., Rodenfels, M., and Clausnitzer, K.-D. (2010). Datenbasis

Gebäudebestand. Datenerhebung zur energetischen Qualität und zu den

Modernisierungstrends im deutschen Wohngebäudebestand. Technical report, Institut

Wohnen und Umwelt GmbH (IWU).

Seite 18 von 209. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

Dietzenbacher, E., Lenzen, M., Los, B., Guan, D., Lahr, M. L., Sancho, F., Suh, S., and

Yang, C. (2013). Input-output analysis: the next 25 years. Economic Systems

Research, 25(4):369–389.

Duchin, F. and Steenge, A. E. (2007). Mathematical models in input-output economics.

Rensselaer Working Papers in Economics, 703:1–32.

Holub, H.-W. and Schnabl, H. (1994). Input-Output-Rechnung: Input-Output-Analyse.

Einführung. Oldenbourg.

Jaeger, G. M. (2014). Wohnraummiete. In Usinger, W. and Minuth, K., editors, Immobilien,

Recht und Steuern. Handbuch für die Immobilienwirtschaft, volume 4. Boorberg.

Junius, T. and Oosterhaven, J. (2003). The solution of updating or regionalizing a matrix with

both positive and negative entries. Economic Systems Research, 15(1):87–96.

Kranzl, L., Hummel, M., Müller, A., and Steinbach, J. (2013). Renewable heating:

Perspectives and the impact of policy instruments. Energy Policy, 59:44–58.

Leontief, W. (2008). Input-output analysis. In Durlauf, S. N. and Blume, L. E., editors, The

New Palgrave Dictionary of Economics, volume 4. Palgrave Macmillan.

Leontief, W. and Duchin, F. (1986). The future impact of automation on workers. Oxford

University Press.

Miller, R. E. and Blair, P. D. (2009). Input-Output analysis. Foundations and extensions.

Cambridge University Press, 2 edition.

Mostaghimi, M. (2010). Economic measurement and forecasting. In Free, R. C., editor, 21st

century economics: a reference handbook, number 1, pages 287–295. Sage

Publications.

Pietroforte, R. and Gregori, T. (2003). An input-output analysis of the construction sector in

highly developed economies. Construction Management and Economics, 21:319–

327.

Reich, U.-P. (2008). Additivity of deflated input-output tables in national accounts. Economic

Systems Research, 20(4):415–428.

Repenning, J., Matthes, F., Blanck, R., Emele, L., Döring, U., Förster, H., Haller, M., Harthan,

R., Henneberg, K., Hermann, H., Jörß, W., Kasten, P., Ludig, S., Loreck, C.,

Scheffler, M., Schumacher, K., Eichhammer, W., Braungardt, S., Elsland, R., Fleiter,

T., Hartwig, J., Kockat, J., Pfluger, B., Schade, W., Schlomann, B., Sensfuß, F.,

Athmann, U., and Ziesing, H.-J. (2014). Klimaschutzszenario 2050. 1.

Modellierungsrunde. Studie im Auftrag des BMUB. Technical report, Öko-Institut,

Fraunhofer ISI.

Richter, J. (1991). Aktualisierung und Prognose technischer Koeffizienten in

gesamtwirtschaftlichen Input-Output-Modellen. Physica-Verlag.

Rose, A. (1995). Input-output economics and computable general equilibrium models.

Structural Change and Economic Dynamics, 6:295–304.

Seite 19 von 209. Internationale Energiewirtschaftstagung an der TU Wien IEWT 2015

Rueda-Cantuche, J. M., Dietzenbacher, E., Fernández, E., and Amores, A. F. (2013). The

bias of the multiplier matrix when supply and use tables are stochastic. Economic

Systems Research, 25(4):435–448.

Schmoll, F. (2007). Staat und Markt - die volkswirtschaftliche Perspektive. In Fritz Schmoll, c.

E., editor, Basiswissen Immobilienwirtschaft, volume 2. Grundeigentum-Verlag.

Simpson, D. and Tsukui, J. (1965). The fundamental structure of input-output tables, an

international comparison. The Review of Economics and Statistics, 47(4):434–446.

West, G. R. (1995). Comparison of input-output, input-output + econometric and computable

general equilibrium impact models at the regional level. Economic Systems

Research, 7(2):209–227.

Wier, M., Lenzen, M., Munksgaard, J., and Smed, S. (2001). Effects of household

consumption patterns on CO2 requirements. Economic Systems Research,

13(3):259–274.

Seite 20 von 20You can also read