Western Uranium & Vanadium's Sunday Mine Complex is right - InvestorIntel

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Western Uranium & Vanadium’s Sunday Mine Complex is heading in the right direction to re-open soon The USA is the world’s largest producer of nuclear power, accounting for more than 30% of worldwide nuclear generation of electricity. In 2018 the country’s nuclear reactors produced 807 billion kWh, about 20% of total electrical output. All this was produced by 98 operating nuclear power reactors in 30 states, operated by 30 different power companies. All of this requires uranium. As the world’s development and population grow so does the demand for energy and energy storage. The vanadium redox flow battery (VRFB) could be the answer as the batteries are fully containerized, non-flammable, reusable, use 100% of the energy stored and can last up to 20 or 30 years. Combined with the vanadium used in steel hardening, then the world is sure to need more vanadium each year. Western Uranium & Vanadium Corp. (CSE: WUC | OTCQX: WSTRF) is a near term producer that has acquired uranium and vanadium mineral assets in western Colorado and eastern Utah, USA. The Company has one of the largest U.S. uranium and vanadium in- situ resources. The total uranium resource is 70,000,000 lbs. +/- and the total vanadium resource is 35,000,000 lbs. +/- grading between 1.4-2.2%. The resource is spread over several properties as shown below. Projects summary with resource and locations

Western Uranium & Vanadium projects summary

The Sunday Mine Complex update

Western Uranium & Vanadium’s key focus is currently the Sunday

Mine Complex vanadium project located in western San Miguel

County, Colorado. The Complex covers approximately 3,800 acres

and 221 unpatented claims. The Complex consists of five

individuals connected underground mines with historic

production, and they are already fully permitted.

The Company made an announcement late last year that they are

going to open the Sunday Mine Complex. The Company has now

provided an update to shareholders regarding their previously

announced plan. Over the past several months the evaluation of

equipment and personnel requirements and availability have

been undertaken, as well as preliminary mine planning and

budgeting, pursuing project funding options, and expanding

vanadium marketing opportunities. The Project will be

commenced within weeks of satisfactory project funding.

Catalysts and work ahead will include :

The identification of high-grade zones.

Long hole drilling and bulk sampling from the

underground mine workings from the Sunday Mine Complex.

The expansion of resource estimates with a new defined

high-grade vanadium resource.

Delivery of samples to various processors and end users

for analysis.

Negotiation of vanadium Term Contracts to catalyze mine

production.

These goals are expected to be completed during the following

six to nine months.

High-grade uranium and vanadium seams at the Sunday Mine

Complex

George Glasier, President, CEO, and Director said: “All of our

assets are in North America, in the Western United States. We

have got the highest grade vanadium probably in the world.

That is why we have got a competitive advantage.”

Western Uranium and Vanadium’s focus will be to bring the

Sunday Mine Complex into production in the near term,

and recent funding of CAD$3,836,340 is a big step in the right

direction.

No matter what commodity you are in, the grade is what

matters. It means a project will be lower cost and find it

easier to attract funding. When it comes to vanadium the

Company certainly has that. With uranium, they have got the

technology that is also making them a low-cost producer. With

both the right tech and grades you have the advantage to keepyour costs lower than your competitors. As a final bonus, a re-start mine is a low capital expenditure. This means Western Uranium and Vanadium have the trifecta of high grade/low cost, technology and skills to extract, and a low CapEx. Vanadium demand set to surge from the high strength steel sector Vanadium demand will continue to strengthen due to demand for higher strength steel from the steel industry, as well as incremental new demand from Vanadium Redox Flow Batteries (VRFBs). Vanadium is one of the 35 minerals deemed critical to US national security. It has multiple uses in today’s modern world from being used in steel manufacturing, VRFBs, tools, and even nuclear power plants. Around 85% of vanadium production is used as a steel strength additive. Even Henry Ford used vanadium in his car manufacturing process and it is used to harden re-bar steel in building construction and tool making. VRFBs have unique characteristics that make them ideal in the energy storage space. A VRFB typically is charged using renewable energy such as wind turbines or solar panels. The VRFB has several unique characteristics that give them an advantage for large scale commercial energy storage. They can charge and discharge at the same time, and they can last up to 25-30 years with continued daily use. On the supply side, there will be some new supply from existing producers such as Bushveld, AMG and Largo Resources over the next 3 years. The question is whether this can keep

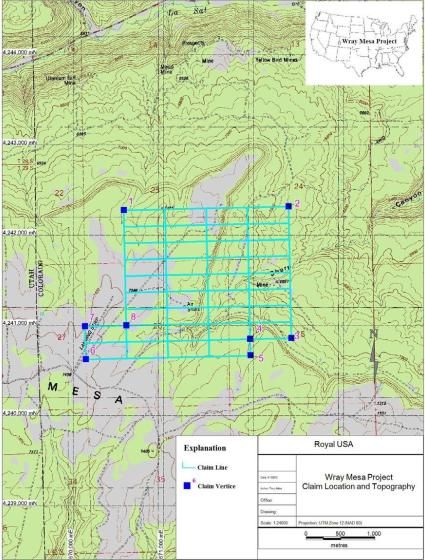

up with surging demand and what happens post 2021. The graph below forecasts demand will outstrip supply, especially after 2021. Vanadium total demand forecast to outstrip supply 2019-2025 Vanadium total demand forecast to outstrip supply 2019-2025 United Battery Metals Corp. (CSE: UBM) is a vanadium and uranium exploration company in North America. United Battery Metals flagship vanadium project is their exploration stage uranium-vanadium Wray Mesa Project. The Wray Mesa Project The Wray Mesa Project is located in Colorado, USA 380 km from the state capital of Denver, and comprises over 3,000 acres and covers more than 107 contiguous claims. The Company states: “Because of the presence of uranium and vanadium in the region, the project area, along with the parts of southwest Colorado and southeast Utah, has been intensively

studied by both public and private-sector investigators. Principally leading the public sector workers were geologists of the USGS and of the Atomic Energy Commission (AEC) during the 1940’s through the 1970’s.” The Wray Mesa Project location and topography map China has been leading the demand surge for vanadium for both

higher strength steel rebar and for VRFBs. Both of these demand drivers look set to continue. It is also significant to note that the world is moving towards electrification of the transport sector. This means an additional huge demand for electricity and energy storage. United Battery Metals strives to be a leader and an eventual producer of vanadium. If United Battery Metals Corp. can prove up a good size vanadium resource then they can position themselves to be a North America’s vanadium producer in the 2020’s to meet the expected vanadium demand surge. Glasier on Western Uranium & Vanadium’s processing technology and high-grade Sunday Mine “All of our assets are in North America. In Western United States. We have got the highest grade vanadium probably in the world. That is why we have got a competitive advantage. Grades are everything no matter what commodity you are in. If you have the grades you have the low cost. That’s what we have certainly in vanadium. With Uranium we have got the technology which makes us the low cost producer. So again it’s the issue of your grades and your technology that drive your cost to the lower percentage of your competitors.” States George Glasier, President, CEO and Director of Western Uranium & Vanadium Corp. (CSE: WUC | OTCQX: WSTRF), in an interview with InvestorIntel’s Tracy Weslosky. Tracy Weslosky: You are one of the few stocks that actually

made people money last year. Can you tell us what made Western Uranium & Vanadium different from many of your competitors? George Glasier: Obviously it’s our vanadium content. Vanadium was the hottest commodity last year. It went from $10 to over $30 and we have got a large high-grade vanadium resource. I credit most of it to the fact that we were in the right commodity at the right time. Tracy Weslosky: Many of our readers have been following the Sunday Mine Complex. We are very excited about the progress towards production. Can you tell us what’s happening? George Glasier: We had an announcement late last year that we are going to open the mine primarily to sample and sent samples to a number of vanadium customers. We are still on track to do that. The best time to open the mine is in the spring. We are working on that. I would say that within the next several months we will see the opening and the beginning of the process, first to sample and then to define the high- grade vanadium resource that was left, without mining the uranium. Tracy Weslosky: Would you mind giving our audience kind of an overview about your competitiveness and include how you are based in North America. George Glasier: All of our assets are in North America. In Western United States. We have got the highest grade vanadium probably in the world. That is why we have got a competitive advantage. Grades are everything no matter what commodity you are in. If you have the grades you have the low cost. That’s what we have got certainly in vanadium. With Uranium we have the technology which makes us the low cost producer. So again it’s the issue of your grades and your technology that drive your cost to the lower percentage of your competitors. That’s where we are…to access the complete interview, click here Disclaimer: Western Uranium & Vanadium Corp. is an advertorial

member of InvestorIntel Corp. Billions approved for nuclear reactors catalyst for uranium price (and share) uptick? No matter whether you love it or hate it, it looks like nuclear energy is here to stay. Nuclear is quite cheap, it’s clean, it can help meet global energy needs, and it is supported by many governments around the globe. This is mostly because nuclear power emits no carbon. Due to climate change and harmful pollution, many countries are phasing out fossil fuels, especially coal. Since 1971 nuclear has avoided the release of an estimated 56 giga-tonnes of carbon dioxide. That’s almost two years of total global emissions from fossil fuels. This only leaves a few main energy sources such as nuclear, and renewables (solar, wind, and hydro-power). The problem is not all renewables are yet capable of carrying the entire energy demand load on their own. This is why many governments are in favour of nuclear. For example, President Trump stated: “Nuclear is a way that we get what we have to get, which is energy. I’m in favor of nuclear energy, very strongly in favor of nuclear energy.” Nuclear Power reactors – 71 under construction – China to invest US$12 billion in new reactors There are ~455 nuclear reactors operating around the world. On top of that, there are another 71 reactors under construction (covering 12 countries), 165 planned, and 315 proposed. Japan

recently announced that they will bring back online 15 nuclear plants. China is driving much of the growth, and soon India may follow. For example just last week it was announced that China plans to invest US$12 billion in new reactors. Then this week China announced plans to build up to 20 floating nuclear power plants. One advantage of a floating plant is it will not be affected by earthquakes, tsunamis maybe? Chinese planned floating nuclear power plant (artists impression) More than a dozen countries including the US get over 25% of their energy from nuclear power, and this is increasing. Despite having the most generators in the world, the US is expecting four to six new generators to come online by 2020. More nuclear plants means uranium demand should be strong The graph below forecasts uranium to go into deficit starting 2019. Recent uranium price increases are starting to support

this.

Uranium demand versus supply forecast

Expect a lot more action from the Trump administration in

expanding U.S. nuclear energy programs as one billion dollars

has been earmarked for the development of new advanced

reactors. Just this past week the Trump administration

announced $3.7 billion in new loan guarantees to support the

completion of the first new U.S. commercial nuclear reactors

in a generation, calling the expansion of nuclear energy “the

real” Green New Deal. This will be further great news for the

uranium miners.

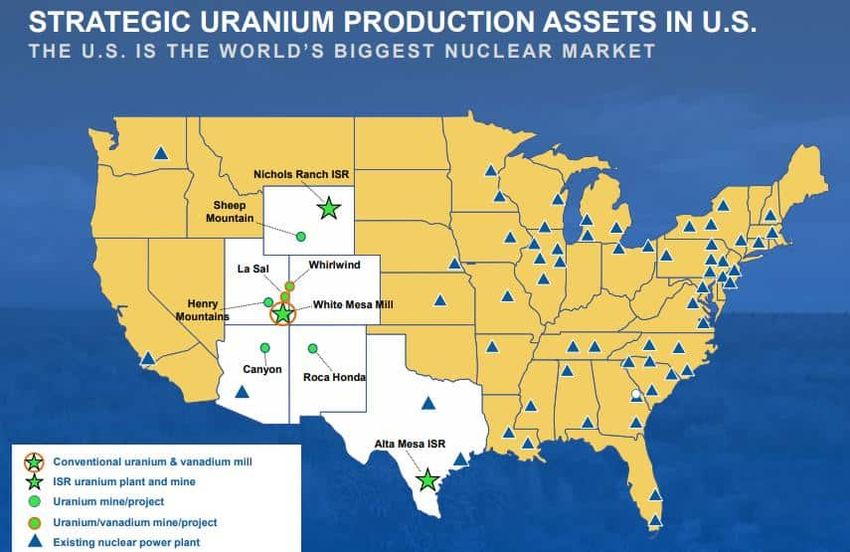

Below are a few uranium companies that we follow.

Blue Sky Uranium Corp: (TSXV: BSK | OTCQB: BKUCF) – One

of Argentina’s best-positioned uranium & vanadium

exploration companies with more than 4,500 km2 (450,000

ha) of prospective tenements.

Energy Fuels Inc: (NYSE American: UUUU | TSX: EFR) – Is

a leading, US-based, integrated producer of uranium that

also has a vanadium resource that recently started

production.

United Battery Metals Corp : (CSE: UBM) – A vanadium anduranium exploration company with 107 contiguous mining

claims over 3000 acres.

Western Uranium & Vanadium Corp: (CSE: WUC | OTCQX:

WSTRF) – Is a near-term producer that acquired uranium

and vanadium mineral assets in western Colorado and

eastern Utah.

The largest uranium producer

in the USA is now world

newest vanadium producer

The market for both uranium and vanadium looks strong with a

need to supply uranium for nuclear reactors and vanadium’s

demand for not only steel hardening but also for vanadium

redox flow batteries (VRFB). These batteries can offer almost

unlimited energy capacity simply by using larger vanadium

electrolyte storage tanks. The development of VRFB could one

day be deployed on a massive scale to store energy from wind

and solar, thereby potentially eliminating the need for fossil

fuels. Just imagine a battery the size of a city block

supplying electricity to 30,000 end users.

Energy Fuels strategic US assets of uranium assets plus their

White Mesa MillEnergy Fuels Inc. (NYSE American: UUUU | TSX: EFR) is a leading, US-based, integrated producer of uranium and vanadium. In fact, Energy Fuels is currently the largest uranium producer in the USA, and the only vanadium producer in the USA, from their 100% owned La Sal Complex of uranium/vanadium mines in Utah. Vanadium production is ramping up quickly In January 2019, the Company informed the market it had resumed vanadium production at its 100%-owned White Mesa Mill making the Company the newest vanadium producer in the world. Just 5 weeks later Energy Fuels announced great news that they are now producing high-purity vanadium at commercial rates of approximately 175,000 to 200,000 pounds of V2O5 per month and the shipments of vanadium have commenced for sale to customers. The Company expects to reach full production rates of 200,000 to 225,000 pounds of high-purity V2O5 per month by the end of Q1-2019 or sooner.

Initial quantities are being allocated for conversion to ferro-vanadium that will be sold into spot metallurgical markets, with the expectation the Company will continue to sell finished vanadium product into the metallurgical industry, as well as other markets that demand a higher purity product, including the aerospace, chemical, and potentially the vanadium redox flow battery industry. Mark S. Chalmers, President and CEO of Energy Fuels commented: “We are extremely pleased with Energy Fuels’ vanadium production to date. We believe our methodical ramp-up is paying dividends, as we are now producing an excellent vanadium product at increasingly higher rates and purities. The Company has discussed vanadium sales with potential buyers for the past several months, and now that we are producing commercial quantities of finished product, we are beginning to make shipments that will initially be converted and sold as ferro-vanadium. We expect to continue the planned ramp-up, and we will provide markets with further updates on our vanadium production at the Mill, as well as on our vanadium test mining program at the La Sal Complex, in the coming months.” In an enthusiastic letter to shareholders on March 14, 2019, CEO Mark S. Chalmers told shareholders about last year being an exciting year for the company achieving a number of significant milestones and will continue to pursue a strategy of building Energy Fuels into a uranium mining and energy company of major global significance. On a lighter note last year’s letter to shareholders he said: “Energy Fuels might be small, but we’re mighty!” and ended that letter with a goal to be “larger and mightier” in 2019. This year he has a new saying for shareholders: “Energy Fuels punches above its weight!” 2018 results On March 12, 2019 the Company also announced their results for

the year ending 2018:

$31.7 million of total revenue was realized by the

Company during the year.

A gross profit of $12.4 million was realized by the

Company, representing a 39% gross profit margin on

mining and milling activities.

A net loss attributable to the Company of $25.4 million

during the year.

650,000 pounds of U 3 O 8 sales were completed by the

Company at an average realized price of $47.37 per

pound. Uranium sold at contract prices averaged

$61.30/lb and at spot prices averaged $25.07/lb.

Uranium inventory as of 493,000 lbs.

The Company commenced vanadium production from the pond

solutions at its 100% owned White Mesa Mill in late

December 2018, and the first batches of finished

vanadium product were produced in January 2019.

With an enthusiastic CEO, a company punching above its weight,

quality US assets, ~175,000 to 200,000 lbs of V2O5 per month

production, strong uranium production/sales/inventory and with

expansion potential; Energy Fuels Inc. is looking attractive

to investors wanting exposure to uranium and vanadium.

What the Mining Industry can

Learn from the Boston Red Sox

The mining industry can learn a lot from the Boston Red Sox. I

just learned that lesson at PDAC 2019, the greatest mining

show on Earth. More than 25,000 people attended in Toronto to

meet, mingle, learn, look at core, party, buy, sell andschmooze. I’ve been attending the mining show annually since 1992. I’ve missed two years. Before I go I have a list of goals that I want to achieve. Overall, it was a very good year at the show as I ticked off all the items on my to-do list and as always found a few more. Wandering the booths and hallways and seminars, one of the things I learned was that there is a dearth of good projects under development. Simply put, we are consuming metals and not replacing them, causing analysts to believe the world will be in a deficit position over the next few years. This 2015 infographic from the Visual Capitalist makes the case for the coming copper crunch or you can read it in The Mining Journal. Similar alarms are being sounded for silver and gold. The shortages in the battery metals (nickel, manganese, lithium, graphite and of course perennial bridesmaid cobalt) are obvious as the world decentralizes grid electricity. Refined zinc metal output is expected be 13.81 million tonnes in 2019. The problem is, the output estimate for 2019 is lagging behind the expected metal usage of 13.88 million tonnes for the year. We are consuming the metals faster than the mining companies can replace them. How does this relate to Boston Red Sox, winners of last year’s World Series? The Bosox over many years invested heavily in scouts to find a larger pool of young possible players, signed players at a young age, developed them patiently through the system, and brought them to the major leagues at the appropriate time. Not downplaying Steve Pearce’s World Series, the most important players on Boston’s championship run throughout the season and the playoffs were homegrown, like Mookie Betts, Andrew

Benintendi, and Jackie Bradley Jr., Xander Bogarts was signed when he was 16 years old and made major contributions to the team’s success. The cost of finding and developing young talent is far less than the cost of trying to acquire that talent once developed. Look at Bryce Harper’s USD$330 million contract with the Phillies after spending the first 7 years of his professional career in Washington. In Year 1 of that Washington contract, Harper was paid a total of $3 million and had a tremendous year, earning a spot in the All-Star game and winning NL Rookie of the Year. His 7 years in Washington were very cost- effective for the team and the returns he provided. Once developed, he priced himself out of the Washington budget. There’s also Mannie Machado who in 2012 was paid $112,786 by the Baltimore Orioles. Drafted and developed by Baltimore, Machado provided Baltimore with gaudy numbers and strong defence. For you data geeks, his Wins Above Replacement (WAR) is 5.7. He was a bargain for what he contributed to the team. He just signed a 10-year, USD$300 million contract with the San Diego Padres, priced out of Baltimore’s budget. Finding, drafting and developing your own players allows a team to control costs, keep these players under contract for a (relatively) low cost for an extended period of time, provides some degree of economic stability for the team, and de-risks the overall organization. And that is one of the things that’s missing in the mining industry. There are few large projects in development to replace the copper, gold, copper, nickel, tin, silver, and battery metals that are needed. The majors have failed to invest in their minor league systems, leading them to have to effect risky M&A transactions to replace lost ounces. This failure to invest in development started in about 2013, after the mining industry blew up following an acquisition

spree. You remember Kinross’ 2010 free agent acquisition of Red Back Mining to acquire ownership of Tausita Gold Mine in Maruitania? Kinross paid $7.1 billion for an asset that was written down by $3.2 billion in 2013, crushing Kinross’ share price with it. There are other examples as well, but this write-down was massive and caught the market’s eye. Fear crept into the market and brought an end to M&A activity. Following the fear came severe cost-cutting. The majors dramatically scaled back in all areas of operations, including not investing in the intermediates and juniors. If the juniors aren’t being funded they can’t explore (scout), the number of development opportunities shrinks, which reduces the number of opportunities for the intermediates to shepherd good projects along. And that decreases the odds that a major deposit would be found. And that of course means that fewer deposits are making it to the Major Leagues. The cost of acquiring already-developed properties is extremely expensive. Grabbing proven ounces is what is driving the current $17.8 billion attempted takeover of Newmount Mining by Barrick Gold. It’s like the Phillies acquiring Bryce Harper for $330M after he was cheaply developed by Washington. The Bosox are 6/1 favourites to win the World Series again, due mainly to the core of highly talented home-grown inexpensive players. It would be cheaper for the majors in the mining industry to invest more broadly in the juniors, knowing there will be winners and losers along the way, than to continue relying upon free-agent signings.

Blue Sky’s CEO on vanadium, plus having ‘one of the largest districts of potential uranium’ in the world “We just put out our PEA (for the Ivana Uranium-Vanadium deposit at Amarillo Grande Project). Our PEA indicates, if it was in production today it would be one of the lowest cost uranium production in the world and with a strike length of over 145 kilometers. This entire district that we control has the potential to be one of the largest uranium districts in the planet, very significant discovery.” States Nikolaos Cacos, President, CEO and Director of Blue Sky Uranium Corp. (TSXV: BSK | OTCQB: BKUCF), in an interview with InvestorIntel Corp. CEO Tracy Weslosky. Tracy Weslosky: We are both at PDAC 2019. I am an ardent fan of the uranium sector in general. Can you tell us what your most competitive advantage for all of you investors out there looking at uranium presently is? Nikolaos Cacos: We just put out our PEA (for the Ivana Uranium-Vanadium deposit at Amarillo Grande Project). Our PEA indicates, if it was in production today it would be one of the lowest cost uranium production in the world and with a strike length of over 145 kilometers. This entire district that we control has the potential to be one of the largest uranium districts in the planet, very significant discovery. Tracy Weslosky: One of the largest districts of potential uranium on the planet. Is that correct? Nikolaos Cacos: That is correct, yes.

Tracy Weslosky: Okay. We have a global shortage of uranium, yes? Nikolaos Cacos: We have a shortage of uranium. I think more and more around the world, especially emerging markets, economies are looking at uranium and nuclear power because it is green, it is efficient and it is safe. As that demand continues to grow the shortage is going to be more and more exacerbated and the price of uranium is going to start moving up, as we have seen in the last year a 50% appreciation in the uranium. Tracy Weslosky: If a new investor was coming and they were looking at Blue Sky Uranium, what would you want to leave them with? I know you are obviously in Argentina, which would be a competitive advantage. Can you talk to us about your competitive advantages for new investors looking at Blue Sky? Nikolaos Cacos: If you are an investor, a new investor, you are looking to make money. The best way to make money is before something really begins to takeoff. You look at the fundamentals, you look at the management team and you look at what assets that we have got. We have got all three…to access the complete interview, click here Disclaimer: Blue Sky Uranium Corp. is an advertorial member of InvestorIntel Corp.

You can also read