ANALYSIS OF THE 2019 NATIONAL BUDGET AND PROJECTED IMPACT ON SOCIO-ECONOMIC DEVELOPMENT - PARLIAMENT OF ZIMBABWE POST-BUDGET SEMINAR GODFREY ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ANALYSIS OF THE 2019

NATIONAL BUDGET AND

PROJECTED IMPACT ON

SOCIO-ECONOMIC

DEVELOPMENT

PARLIAMENT OF ZIMBABWE

POST-BUDGET SEMINAR

GODFREY KANYENZE (Dr.),

LEDRIZ

RAINBOW TOWERS HOTEL

26 NOVEMBER 2019

The Policy Objectives & Focus Long-term development agenda under the New Dispensation: Vision 2030 which seeks to transform the country into an Upper Middle Income Society by 2030. Medium term plan: Transitional Stabilisation Programme (TSP) – October 2018 to December 2020. The TSP`s immediate objective is macro and fiscal stabilisation and laying a solid foundation for attaining the triple ‘S’ growth - strong, sustainable and shared. Annual Plan / Budget, with the 2019 focusing on ‘Austerity for Prosperity’ – tension in the means (austerity) and ends (prosperity). Essentially, austerity entails cutting back on aggregate demand, which ultimately will affect growth, employment and poverty. Austerity is pro-cyclical and not counter-cyclical.

Key issues from Consultations

Key objectives and priorities from consultations include:

i. Decisively dealing with fiscal indiscipline through use of austerity measures;

ii. Removal of pricing and policy distortions;

iii. Improving foreign currency generation and establishing efficient and optimal

mechanisms for its allocation;

iv. Jobs creation, particularly for the youths, being the new entrants into the labour

market;

v. Promotion of productivity and export growth through incentives;

vi. Efficient public service delivery and not just input;

vii. Parastatals reforms and privatisation for a private sector led economy;

viii. International re-engagement, clearance of debt arrears and investment

promotion;

ix. Investing in research and development;

x. Empowerment of Provinces and Districts;

xi. Gender equity promotion;

xii. Promotion of good governance;

xiii. Fighting corruption; and

xiv. Turn Zimbabwe into the gateway for investment into Africa.

Stakeholders’ emphasis on co-ordinated, predictable and consistent policies, void of

reversals to promote confidence building and forward planning.

Having raised the key priorities from consultations, the Budget Statement indicates that due to limited fiscal space during the tenure of the TSP, the 2019 Budget will primarily target macro-economic and fiscal stabilisation and implementation of high impact projects and programmes. Clearly therefore, the 2019 Budget is about implementing an austerity programme, akin to ESAP II. Given the resemblance with ESAP I, it is important to draw lessons from experiences with Structural Adjustment Programmes (SAPs) that were implemented in the 1980s and 1990s. Budget statement correctly observes that realising the above requires unity of purpose, high level of competencies, as well as commitment and full participation of all stakeholders during implementation of TSP and the 2019 Budget – the big question is do we have these requisites at the moment? Paragraph 18, page 6 of the Budget Statement makes the following plea: “I, therefore, appeal to all implementing agencies to apply themselves diligently for the success of this Budget and the Transitional Stabilisation Programme, as we move a step towards attaining an ‘Upper Middle Income Society by 2030’. Is this sufficient given past experiences?

Policy Thrust The primary objective of the 2019 Budget is to stabilise the economy, targeting the ‘twin deficits’ of fiscal and current account, major sources of economic vulnerabilities, including inflation, sharp rise in indebtedness, accumulation of arrears and foreign currency shortages. In view of the limited fiscal space against high demands, focus on quick-win flagship projects and programmes across key sectors of the economy. The 2019 Budget to prioritises infrastructure rehabilitation and development to support productive sectors. Value addition and beneficiation strategy will also be supported to maximise benefits in terms of employment and incomes. Removal of various policy and price distortions which undermine efficiency and promote corrupt and rent seeking practices. Measures to reduce expenditures and mobilise more resources through taxes to entail pain and sacrifice, hence the theme of the 2019 Budget of ‘Austerity for Prosperity’.

Lessons from Structural Adjustment Programmes (SAPs) Lessons can be drawn from the experiences of Structural Adjustment Programmes (SAPs) with the mantra of ‘stabilize, privatize, and liberalize.’ Empirical evidence suggests that macroeconomic stabilization was often achieved following the implementation of orthodox reforms, but at the expense of sustained levels of investment, economic growth, employment and poverty reduction – ‘the stabilization trap.’ Muqtada (2010) reports on the relationship between the stability variables and GDP growth based on panel data for 80 developing countries and reveals that: • “nearly two decades of stabilization reforms have in fact reduced the inflation levels in most countries of the world; • with the exception of a few countries, growth of GDP is observed to be low or inadequate during the 1980s and much of the 1990s; • despite substantial declines in inflation rate and budget deficit, hence arguably better macroeconomic stability, investment-to-GDP ratio (I/GDP) has failed to gain momentum; • I/GDP as a single variable tends to explain growth better than “stability” variables; and • Current account deficit is negatively related to growth but not robustly,” (page 3).

Analysis by the World Bank supports the pro-cyclical nature of stabilization. Results contained in two seminal reports ‘Economic Growth in the 1990s: Learning from a Decade of Reform’ (World Bank, 2005); and ‘The Growth Report: Strategies for Sustained Growth and Inclusive Development’ (World Bank, 2008). As the 2005 report notes; “The principles of … ‘macroeconomic stability, domestic liberalization, and openness’ have been interpreted narrowly to mean ‘minimize fiscal deficits, minimize inflation, minimize tariffs, maximize privatization, maximize liberalization of finance,’ with the assumption that the more of these changes the better, at all times and in all places - overlooking the fact that these expedients are just some of the ways in which these principles can be implemented,” (World Bank, 2005: 11). The World Bank reports argue that by focusing on macroeconomic stability, deregulation and privatization, conventional macroeconomic policies typically confuse means for ends. In this respect, the report argues that: “In retrospect, it is clear that in the 1990s we often mistook efficiency gains for growth … Expectations that gains in growth would be won entirely through policy improvements were unrealistic. Means were often mistaken for goals – that is, improvements in policies were mistaken for growth strategies, as if improvements in policies were an end in themselves. Going forward, the pursuit of policy reforms’ sake should be replaced by a more comprehensive understanding of the forces underlying growth. Removing obstacles that make growth impossible may not be enough: growth-oriented action, for example on technological catch up, or encouragement of risk taking for faster accumulation, may be needed,” (World Bank, 2005b: 11).

While it was clear that to achieve higher levels of growth and employment required substantially increased resources and expenditures (e.g. on physical and social infrastructure), the stabilization measures continued to squeeze the fiscal space needed to achieve such expenditures. Hence, conventional approaches often miss the fact that social goals are not only ends in themselves, but are also capital inputs, the very means to productive life, economic growth and further development. In the aftermath of the global crisis of 2008-09, the IMF has entered the debate, accepting that a rethink of macroeconomic policy is required. In an appropriately titled paper, “Rethinking Macroeconomic Policy,” it laments that “…we thought of monetary policy as having one target, inflation, and one instrument, the policy rate. So long as inflation was stable, the output gap was likely to be small and stable and monetary policy did its job. We thought of fiscal policy as playing a secondary role, with political constraints sharply limiting its de facto usefulness. And we thought of financial regulation as mostly outside the macroeconomic framework,” (see Blanchard et.al, 2010: 3). An IMF Working Paper published on 3 January 2013 titled “Growth Forecast Errors and Fiscal Multipliers,” co-authored by its chief economist, Olivier Blanchard and Daniel Leigh, a research-department economist, argues that the IMF recommended slashing budgets too fast early in the euro crisis, starving many economies of much-needed growth. It observes that: “Forecasters significantly underestimated the increase in unemployment and the decline in domestic demand associated with fiscal consolidation.”

State of the Economy and Outlook Cumulative impact imbalances, especially the ‘twin deficit’ that have gone for too long without being addressed weighed down economic performance. Growth of 4% in 2018, below the 6.3% projected under TSP; 3.1% in 2019 (9.0% in TSP); and 7.5% in 2020 (9.5% in TSP). Nominal GDP for 2018 now US$24.6 billion, from a previous level of US$21 billion due to rebasing. Following rebasing, per capita GDP for 2017 up from US$1 235 to US$1 508, and projected to reach US$1 642 by end of 2018, placing Zimbabwe in lower middle income status.

GDP Growth Rates

Limited & shrinking fiscal space…firing on one cylinder The fiscal space diamond is an analytical tool, a visual representation of the sources, and potential increases or decreases in resources derived through fiscal instruments. Plotted over four axis signifying different key components of revenue, with each axis scaled as a percentage of GDP, the diamond illustrates the aggregate fiscal space available to governments. The key fiscal instruments or ‘pillars’ of the fiscal diamond are: • external grants/aid (Overseas Development Assistance - ODA) or debt relief; • domestic revenue mobilisation through tax administration or tax policy reforms; • deficit financing through domestic and external borrowing; and • ‘Reprioritization’ (expenditure switching) and raising efficiency of expenditures. Zimbabwe has not had the advantage of accessing all the four pillars of the fiscal space diamond. In the absence of re-engagement with the international community, official aid is off-budget.

Fiscal Space for Development: The fiscal space diamond

1. Official Development

Assistance (% of GDP)

4. Reprioritization & 2. Domestic

Efficiency of Revenues

Expenditures Mobilization

(% of GDP) (% of GDP)

3. Deficit Financing

(% of GDP)Public Finances Revenue collected during the nine months to September 2018 amounted to US$3.8 billion, against a target of US$3.4 billion, and projected at US$5.5 billion by year end. Total expenditures during the nine months to September 2018 of US$6.5 billion, against a target of US$4.1 billion. Expenditure outturn to year end estimated at US$8.2 billion against a budget of US$5.3 billion, implying an expenditure overrun of US$2.8 billion. The 2018 Budget Deficit is projected at US$2.86 billion (11.7% of GDP), against a target of US$793 million. The large cumulative deficit is due to unbudgeted expenditures involving employment costs, support to agriculture, and some capital expenditure. Deficit financed by issuance of Treasury Bills and recourse to the overdraft facility at the Central Bank.

Budget Deficit & Borrowing Requirements

2009 2010 2011 2012 2013 2014 2015 2016 2017*

Revenue

(US$m) 933.6 2339.1 2921.0 3495.8 3741.0 3727.2 3737.1 3502.2 4338.5

Expenditure

(US$m) 898.1 2143.0 2898.9 3505.3 3987.4 3911.6 4119.6 4923.2 6045.0

Budget

deficit 35.5 196.1 22.1 -9.6 -246.4 -184.4 -382.5 -1421.0 1706.5

Deficit/GDP

(%) 0.4 1.9 0.2 -0.1 -1.6 -1.2 -2.3 -8.5 9.9Fiscal deficit and revenue collection: a comparative analysis (World Bank,

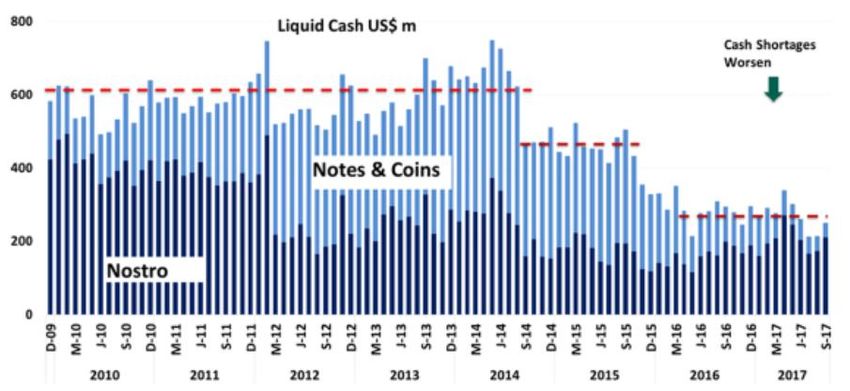

June 2017)Fiscal expansion in 2016 triggered a liquidity crunch, prompting banks to limit cash withdrawals. Sudden rise in the fiscal deficit in 2016 is related to the Reserve Bank Debt Assumption Act of July 2015, which required government to take liability of an estimated $1.35 billion debts incurred by the RBZ before 31 December 2008. Fiscal deficits had to be financed through domestic borrowing, which put the financial sector under considerable pressure, leading to liquidity shortages. Of the US$2.1 billion Treasury bills and bonds issued in 2016, only US$356.3 million (17%) was to finance the budget deficit, with US$1.7 billion (81%) for outstanding legacy debt. As a result of the expansionary fiscal stance, government debt to the banking sector increased steeply after 2015, culminating in a prolonged financial crisis that severely limited credit to the economy and resulted in cash shortages, prompting banks to limit cash withdrawals and import payments as they had depleted their US dollar reserves.

Issuance of Treasury Bills went into over-drive, quadrupling from US$2.1 billion in 2016 to a cumulative US$7.6 billion, by end of August 2018. During the period January to August 2018 alone, Government issued Treasury bills and bonds worth US$2.5 billion. Resultantly, outstanding Government Securities stood at US$6.2 billion as at end of August 2018. While the ratio of Treasury Bills to GDP was at 4.4% in 2014, it increased sharply to 36.5% by end of August 2018. Government’s overdraft facility at the Central Bank to finance the deficit at US$2.3 billion as at end of August 2018, is three times higher than the statutory limit of US$762.8 million. Regrettably, the overdraft facility increased by US$1.11 billion for the period January to September 2018 and is projected to close the year at US$2.5 billion, well above the stipulated statutory limit. It also violated the requirement of Section 11(1) of the Reserve Bank Act [Chapter 22:15], which states that borrowing from the Reserve Bank shall not exceed 20% of the previous year’s Government revenues at any given point.

Trends in Liquid Cash Availability

Inflation Outlook Significantly, annual inflation, which had dropped from 3.7% in 2012 to 1.6% in 2013, slumped into a deflation at -0.2% in 2014 and -2.4% in 2015 largely reflecting a depreciating South African rand - Zimbabwe’s major trading partner - and weakening domestic demand. It however trended upwards throughout 2016, averaging -1.6% in 2016 and 0.9% in 2017 (0.8% in September, 2.2% in October, 3% in November & 3.5% in December 2017). Economy is now out of the deflation, rising in 2018 as follows: 3.5% in January, 3% in February, 2.7% in March, 2.71% in April 2018, 2.71 in May , 2.91 in June, 4.3% in July, 4.8% in August, 5.39% in September 2018, spiking to 20.85% in October 2018. SADC macro-economic convergence target of inflation of 3-7%. General price hikes driven by foreign exchange rate premiums associated with the mis-match between electronic bank balances and available foreign exchange. The upsurge in annual inflation rate is mainly driven by food and non-food items such as transport services.

Unsustainable public debt… Total Debt (debt distress): The economy is saddled with a high debt overhang with an estimated public debt stood of US$17.69 billion as at end of August 2018, of which domestic debt accounted for 54% up from 49%, while external debt moved down from 51% to 46%. By end of 2018, it is estimated that the public debt statutory limit of 70% is likely to be breached. Emergence of domestic debt from as low as US$275.8 million in 2012 to US$9.5 billion. Consistent with the Arrears Clearance Strategy agreed with creditors in Lima in October 2015, Zimbabwe settled its overdue obligations to the IMF amounting to US$107.9 million on 20 October 2016. As a result the IMF Board remove sanctions on Zimbabwe related to remedial measures applied on account of overdue financial obligations to the Poverty Reduction and Growth Trust (PRGT). The remedial measures removed related to: i. Declaration of non-cooperation with the IMF; ii. Suspension of technical assistance; and iii. Removal of Zimbabwe on the list of PRGT-eligible countries.

External debt arrears amount to about US$5.6 billion, which is split

between:

• Multilateral creditors, US$2.2 billion.

• The Paris Club, an informal group of creditor nations, US$2.7

billion.

• Non-Paris Club creditors, US$700 million.

Bali Arrears clearance strategy agreed to in October 2018 to prioritize

the US$US$2.4 billion owed to the creditors of choice as follows:

US$680 million to the AfDB; US$1.4 billion to the World Bank; and

US$308 million to the European Investment Bank.

The Minister of Finance & Economic Development has indicated

arrears should be cleared in 12 months. In the context of austerity, this

will even limit further the fiscal space for social development.The 2019 Fiscal Framework With nominal GDP projected at US$31.6 billion in 2019, revenues are estimated at US$6.6 billion for 2019: retentions (US$400 million or 6%), taxes (US$6.037 billion or 91.5%), and non-tax (US$162 million or 2.5%). Expenditures are projected at US$8.2 billion: with capital expenditures estimated at US$2.018 billion (or 24.6%), leaving US$6.1 billion for current expenditures (74.4%). The budget deficit is projected at US$1.6 billion or 5% of GDP in 2019; 4.1% in 2020, and 3% in 2021. Restructuring the Treasury bills to longer tenure in consultations with market players. No further acquisitions of non-performing loans by Zimbabwe Asset Management Company (ZAMCO) – Parliament needs to do an audit of what non-performing loans were acquired.

To address the risk of a higher Budget deficit for 2018 and 2019, Government

introduced the 2% intermediated money transfer tax, with effect from 13

October 2018.

From 2019, Budget to invariably focus more on output, results, and impact

(theory of change), service delivery and accountability.

Government is reducing recourse to Central Bank lending from the 20% of

previous year’s revenues statutory limit, to a maximum of 5% confined for

purposes of smoothening cash flow mismatches.

Package of wage and nonwage expenditure rationalisation measures as

follows:

• Effective 1 January 2019, a 5% cut on basic salary for all senior positions

from Principal Directors, Permanent Secretaries and their equivalents up

to Deputy Ministers, Ministers and the Presidium. Extended to basic

salaries of those in designated posts in State Owned Enterprises (CEOs,

Executive Directors and equivalent grades), including Constitutional

Commissions and grant aided institutions;

• Henceforth, the 13th Cheque to be computed based on Basic Salary only

(excluding housing and transport allowances) (bonuses have amounted to

US$174.6 million);• Government to cut the 46 Embassies & Consulates around the world staffed by around 581 home based and locally recruited staff to reduce the US$65 million being incurred in line with the capacity of US$50 million annually; • Cabinet decision of December 2017 to terminate employment contracts of 3 188 Youth Officers to be implemented (US$5.2 million for cash-in-lieu of notice, & US$17.7 million for pension benefits); • The remaining 2 917 Youth Officers to be retired by end of December 2018. However, need to check with 2011 and 2015 Civil Service Audits that pointed to the existence of irregularly employed people; • Retirement of Government officials above the age of 65; • As approved by Cabinet on 5 December 2017, the administration of the Public Service Payroll and Pension to become a Treasury responsibility, with effect from 1 January 2018; • Biometric Register for Civil Servants with effect from 1 January 2019; • All Government pool/project vehicles to be parked at the work stations or the nearest police station after designated working hours, during weekends and public holidays; • All Government pool vehicles to be transferred and centrally managed through CMED Pvt Ltd. Entities with capacity to maintain their fleet will be excluded from this directive; • Government Ministries and Departments to remit all revenue collected into the Consolidated Revenue Fund, with immediate effect. Outstanding balances to be deposited into the Consolidated Revenue Fund by 23 November 2018.

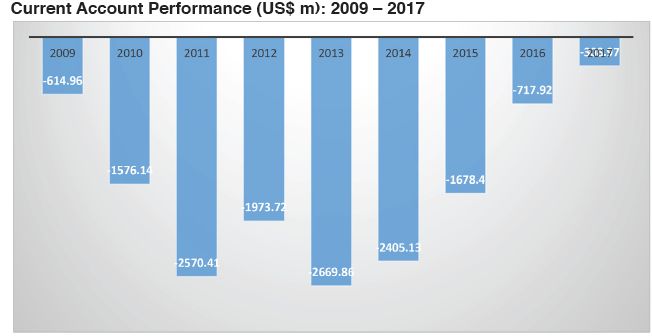

Current Account Deficit

Global Competitiveness, Ease of Doing Business, Economic Freedom and

Corruption Perception Rankings, 2007/08-2017/18

Heritage

Foundation Transparency-

Index of International

WEF Global WB Ease of Economic Corruption

Period Competitiveness Doing Business Freedom Perception

2007/08 129/131 154/183 150/179

2008/09 118/121 160/183 145/147 166/180

2009/10 132/134 156/183 175/179 146/180

2010/11 136/139 157/183 178/179 134/178

2011/12 132/142 170/183 175/177 154/183

2012/13 132/144 172/185 175/184 163/176

2013/14 131/148 170/189 176/178 157/177

2014/15 124/144 171/189 175/178 150/168

2015/16 125/140 155/189 175/178 125/140

2016/17 126/138 161/190 175/180 154/176

2017/18 124/137 159/190 174/180 157/180Measures to address the current account deficit include the following:

i. Supporting export oriented production e.g. horticulture;

ii. Strategically manage available foreign currency by prioritising import

substitution production e.g. retooling and raw materials;

iii. Decisive action on revival of ZISCO Steel and Cold Storage Commission, local

drug manufacturing etc. to boost exports while limiting on import demand;

iv. Value addition and beneficiation in mining and agriculture;

v. Review import duty dispensation for some of the projects and programmes,

e.g. National Project Status.

Operationalisation of the Monetary Policy Committee by the first quarter of 2019.

The multi-currency system to remain in place, with the US dollar being the

currency of reference, out of the currency basket.

Gradual movement towards a more efficient and optimal foreign currency

allocation system, e.g. a Foreign Currency Allocation Committee to promote

efficient management of foreign currency inflows.

Build adequate foreign currency reserves, including gold reserves, to provide an

anchor for preservation of exchange value. To be supported by the

operationalization of the Sovereign Wealth Fund.Overvaluation of the USD, 2010-15 (%)

50

45 45

40 40

35

32

30

25 24

20

15

13

10

5 4

0

2010 2011 2012 2013 2014 2015

Source: Reserve Bank of Zimbabwe unpublished data.FDI flows into selected Southern African economies, US$m

2012 2013 2014 2015 2016 2017

Botswana 487 398 515 679 129 401

Mozambique 5,629 6,175 4,902 3,867 3,093 2,293

Namibia 1,122 770 441 1,247 361 416

South Africa 4,559 8,300 5,771 1,729 2,235 1,325

Zambia 1,732 2,100 1,489 1,305 663 1,091

Zimbabwe 400 400 545 421 372 289

Southern Africa 7,330 11,677 16,370 19,028 11,437 3,836

Source: UNCTAD 2018 World Investment Report.Implementing the Gender Responsive Budgeting Strategy and the National Gender Policy – has assumed the status of a cliché. Speeding up of ease of doing business reforms, including the long awaited operationalisation of the Zimbabwe Investment and Development Agency, ZIDA.

‘Weak-institutions trap’ (WIT)

• It takes ‘strong’ institutions which are the critical factor in

sustaining growth beyond the initial take-off or ‘growth

acceleration’.

• Zimbabwe has been caught in WIT for a long time – resulting in

the country’s poor long-run growth record, weak poverty

reduction - all attributed to weak institutions, including

institutions of the State.

• Long-term and sustained growth can only come about under

conditions of sound macroeconomic fundamentals or growth

oriented political institutions.

37Public Enterprise Reforms

Public enterprises’ contribution to the economy down from around

60% to about 2%.

70% of these entities are technically insolvent.

Rolling out our parastatal reforms on a roll out template which

categorises the entities under the following:

i. State Owned Enterprises to be partially privatised through JVs

and/or listing;

ii. State Owned Enterprises to be fully privatised; and

iii. State Owned Enterprises facing liquidation.

The 2019 Budget proposes the privatisation of at least 5 public

enterprises, namely Tel-One/Net-One/Telecel, ZIMPOST and POSB with

the expected proceeds of at least US$350 million.Budget Sectoral Allocations An estimated US$310 million in fiscal transfers is earmarked for support to Provincial Councils for 2019 in line with the Constitutional requirement that 5% of revenues goes to Provincial Councils. Actual allocations per province to be based on (i) Population profile; (ii) Poverty profile; and (iii) Infrastructure quality and deficit. US$989.3 million to the Ministry of Lands, Agriculture, Water, Climate and Rural Resettlement. US$53 million towards payment of compensation to former white farm owners, whose disbursement will be targeted. Target to allocate 12.6% of the total budget to infrastructure development programmes (excluding agriculture), up from 10.2% of the 2018 Budget.

Based on the Transitional Stabilisation Programme, the

following projects have been accorded high priority:

i. Dualisation and upgrading of Harare-Beitbridge road - “A

road is an economy”;

ii. Expansion of Hwange 7 & 8;

iii. Expansion of Robert Gabriel Mugabe International

Airport;

iv. Upgrading and Modernisation of Beitbridge Boarder Post;

v. Kunzvi Dam & Conveyancing Infrastructure;

vi. Gwayi Shangani Dam and Conveyancing Infrastructure;

and

vii. Lupane Provincial Hospital.Key initiatives include the following:

i. Setting up industrial parks;

ii. Establishment of innovation hubs and spin

off industries;

iii. Incubation of science and technology based

industries; and

iv. Promote research and development for

modernisation and industrialisation.Budget Allocation by Ministry / Sector (%) of Total Expenditures Ministry / Sector 2018 2019 Primary & Secondary Education 12.9 11.0 Lands, Agriculture, Water & Rural Resettlement 8.4 9.6 Health & Child Welfare 6.8 6.7 Defence & War Veterans 6.1 5.3 Public Service, Labour & Social Welfare 3.0 3.2 Industry & Commerce 0.3 0.5 Women’s Affairs, Community Development & SME Development 0.3 0.4 Energy & Power Development 0.2 0.2 Zimbabwe Anti-Corruption Commission 0.1 0.1

The allocations to primary and Secondary Education, at 12.9% in 2018 and 10.2% in 2019 are way below the 20% stipulated in the Dakar Declaration. Worse still, 93.7% (2018) and 90.2% (2019) of the allocation to Primary and Secondary Education are for employment costs. The allocations at 8.4% (2018) and 9% (2019) are close to the 10% stipulated in the Maputo Declaration. The allocations of 6.8% (2018) and 7.1% (2019) for health are way below the requirement of 15% in the Abuja Declaration. The allocations for the Ministries Responsible for Women’s Affairs, and Industry & Commerce are way below what would be required given heir mandate for empowering the disadvantaged groups, transitioning informality to formality and business development. In the National Social Protection Policy Framework (NSPPF), the target was to consider as eligible for all forms of social assistance in the short to medium term all the 500,000 households which are deemed to be below the Food Poverty Line. On the basis of the US$US$19,298,000 allocated for social welfare in 2018, each household would get a meagre US$38.60 per year and US$70.55 in 2019. On the basis of the 415,900 vulnerable children to be reached with educational support, the US$23,485,000 allocated to child welfare in 2018 works out at US$56.47 per child per year for 2018, while the US$31,592,000 allocated for child welfare yields a support level of US$75.96 per child per year.

Proposed Strategic Objectives and Thrusts A. Macroeconomic stability: fiscal reforms for fiscal and debt sustainability, and reprioritization of expenditures • Rationalisation of expenditures and improving the expenditure mix. • Expedite State-Owned Enterprise (SOE) Reforms. • Create fiscal space for development: accelerate re-engagement; expand the tax-base; reprioritize and enhance efficiency of expenditures, and seek debt relief. • Accelerate cost and ease of doing business reforms and promote policy coherence and consistency (adopt broad-based indigenization, bring land distribution to a closure, adopt secure land tenure system - 99-year leases -, and secure property rights). • Enhance external arrears clearance, debt resolution and the re-engagement process to facilitate access to external financing; and strengthen national debt management capacity.

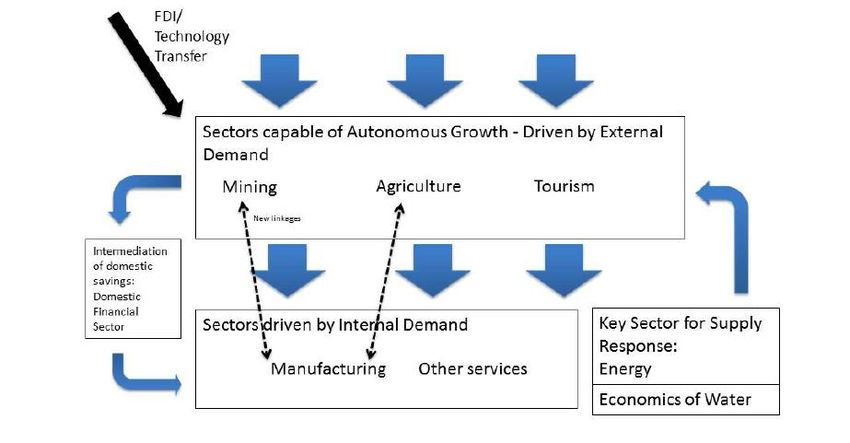

B. Building Linkages by Leveraging Natural Resources: Promote Inclusive, Pro- poor Growth: Re-build Sectoral Linkages through Value Chains and Clusters • In this current phase of recovery, the mining sector is emerging as the main sector capable of autonomous growth. • The restructured agricultural sector also has potential of supply-response to improved conditions, as well as tourism. • However, growth in the manufacturing sector appears more dependent on the internal demand generated by the two main driving sectors (agriculture and mining). • Hence, the quality of policy in the mining and agricultural sector will in the main be the major determinants of the rate of growth of the economy.

Schematic illustration of linkages in the post-crisis Zimbabwean economy (World Bank, 2012)

Schematic illustration of linkages in the post-crisis Zimbabwean economy (World Bank, 2012)

There is plenty of potential to turn the trend around and find new and

strengthen existing sources of sustainable growth (ILO, 2016).

Agriculture: Regain lost productivity and strengthen linkages to industry;

Agriculture has unique opportunities (the 9 commodity industry groups or

clusters), namely, (i) horticulture; (ii) livestock and meat; (iii) legumes and

oilseeds; (iv) tree crops; (v) grains; (vi) cotton; (vii) tobacco; and (ix) forestry and

timber.

Mining: We missed the commodity boom, but the potential remains;

Manufacturing: Highly correlated with agriculture –high potential for regaining

ground;

Services: Focus on areas of high potential –tourism, infrastructure, financial

services.Value chains mapping…

The Confederation of Zimbabwe Industries (CZI) has identified 18

sustainable value chains to drive re-industrialization as follows:

1. Asbestos-to-roofing/piping-to-construction materials value chain;

2. Diamond-to-Jewellery-to-ornament value chain;

3. Gold-to-Jewellery-to-ornament value chain;

4. Chrome ore-to-Chromium-to-Chrome plated goods value chain;

5. Iron ore-to-billet-to-foundry-to-fabricated steel product value

chain;

6. Limestone-to-Quarry-to-Cement-to-Construction;

7. Coal Bed Methane-to-Gas-to-Plastics & allied value chain;

8. Cotton-to-clothing value chains;

9. Soya-to-white meats value chains (incorporating stock-feeds for

the beef industry);

10. Tobacco-to-cigarette value chains;11. Maize-to-mealie meal value chain (incorporating stock-

feeds for the beef industry);

12. Wheat-to-bread value chain (incorporating stock-feeds);

13. Barley/sorghum-to-beer value chain;

14. Beef-to-milk-to-leather value chains;

15. Horticulture production-to-can/packet/bottle value chains

(non-GMO);

16. Regional-assembly-finishing value chains (including

automotives, plastics, paper and ICT);

17. Beverages value chain (including tea); and

18. Pharmaceuticals Pharmacy Hospital Patient Value Chain.Spatial Linkages:

Infrastructure (transport,

power, ICT) and LED

Forward Linkages:

Intermediate products =>

Backward Manufacturing; Logistics ;

Linkages other sectors (agriculture ,

Inputs: forestry, fisheries, etc.)

Mining: Concentration,

Capital goods smelting, refining => metal/alloy Fiscal linkages:

Consumables

Resource rent capture (RRT) &

Services

deployment: long-term

human & physical

Knowledge Linkages infrastructure development

HRD: skills formation

R&D: tech development

Geo-knowledge (survey)Enhancing Transparency and Accountability and

Promoting Artisanal Miners in Chile

Enhancing transparency and accountability around mineral revenues: The

example from Chile is useful where the Government adopted a Transparency

and Access to Public Information Law for all public agencies. In terms of

reporting the Finance Ministry regularly publishes information on production

volumes, prices, mineral export values, royalties and special taxes and

audited financial statements and annual reports are regularly published.

An example of formalisation would entail linking artisanal miners to

established mining houses as was done in Chile where the government set up

the Empresa Nacional de Mineria (ENAMI), (the sixth largest copper exporter

in Chile), whose Board of Directors is made up of the Minister of Mining, a

representative of the Minister of Finance, a representative of the President, a

representative of COCHILCO, the copper advisory agency and SONAMI, an

industry association comprising small, medium-sized and large copper

producers, with a mission of providing technical, financial, and metallurgical

production and trading services that ASM miners require in order to be

competitive.C. What shall we Laisser

do with faire ? Forbid ?

informality?Institutional and Policy Strategies for Addressing

Informality

• Given the heterogeneity of the informal sector, there is no ‘one-

size-fits-all’ policy response valid across countries and within a

country.

• Considering its size in developing countries, policy makers should

consider the impact of every policy decision on the informal

economy.

• In addition, people making a living in the sector should be consulted

to gain inside knowledge.

• The policy measures should be based on an understanding of the

reasons why people work in the informal economy, namely,

whether informality is a choice or rather is due to exclusion from

the formal sector.Ways out of informality:

• Policy guidance from the new ILO R204 (Transition

from the Informal to the Formal Economy

Recommendation, 2015).

• The need for integrated strategies.

Informal Formal

Economy economyThe significance of the new R204

First international standard to provide both a normative and a

developmental framework :

Focusing on the informal economy in its entirety and

diversity;

Indicating a clear orientation and practical guidance for

moving out of informality and transitioning to the formal

economy through integrated strategies;

Encapsulating good practices in transition to formality and at

the same time open to policy innovations;

A Recommendation adopted through a strong tripartite

(governments, employers and workers) consensusGuiding principles of R204

i. tailored approaches to respond to the diversity of

situations and the specificity of national

circumstances;

ii. coherence and coordination across a broad range

of policy areas: employment and income

opportunities, social protection and rights;

iii. A balanced approach combining incentives with

compliance.A typology of formalization Formalization of economic units – Registration of economic units – Increased compliance – Extension in application of labour and social security regulation Formalization of jobs – Extension of application of labour regulation – Extension of coverage of social security – Registration of employment relationship – Registration of own-account endeavours Productive job creation in the formal economy – Most new entrants have access to employment in the formal economy – Increased formal employment intensity of growth.

• For individuals (workers and/or employers) • For society at large

– Improved access to rights at work, social – Broadening the tax base (increasing the

security and decent working conditions; scope of public action, reducing tax

– Better access to representation and national rates, etc.);

policy dialogue;

– Increased equity with regard to the

• For enterprises contribution to public budget and to

– Better access to credit and other productive benefits of redistributive policies;

factors, including through public

– Increased efficiency and sustainability

programmes;

of preventive & compensative measures

– Expanded access to markets: participation in to address risks;

public procurements, access to imports and

exports through formal channels; – Fairer competition in national and

international markets

– Reduction of the influence of corruption,

greater respect for commercial contracts, etc. – Greater social cohesionLAC countries have made progress!

D. Building a Democratic Developmental State

What is needed is the ability of the state to use its

autonomy to consult, negotiate and build

consensus with social partners, at the same time

building capacity to effectively implement economic

policies.

• This state capacity, will only come through the

building of a ‘democratic developmental state’

63E. Need for a Social Contract & Implementation of Agreed Positions:

In view of the trade-offs in policies (e.g. containment and reduction of the

share of revenues taken up by employment costs), arrears clearance etc.

there is need for Zimbabwe to negotiate and implement a Social

Contract.

A Social Contract helps restore good faith (trust) amongst the social partners;

make them accountable to each other; help parties subordinate sectarian

interests to national interests; develop and share a common vision; and

inculcate a smart-partnership win-win mind-set.

Furthermore, there is an urgent need to implement the agreed TNF protocols

such as the Kadoma Declaration, the Principles of the TNF and the

National Productivity Institute launched in February 2003 to spearhead

the promotion of a culture of productivity.The technical challenges are often overshadowed by the political. There is nothing more difficult to carry out … than to initiate a new order of things. For the reformer has enemies in all who profit from the old order and only lukewarm support from those who would benefit from the new. (Machiavelli, The Prince, 1513)

THANK YOU!

You can also read