ARS Investment Partners, LLC - Q1

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Q1 | 2021 ARS Investment Partners, LLC

PRESENTATION OUTLINE

Differentiated

Firm Overview

Investment Strategy

Investment Philosophy Appendix

Investment Outlook

2

Overview Philosophy Outlook Strategy Appendix

FIRM OVERVIEW

Originally founded 16 professionals, Single investment

in 1971, ~$1.55 billion with the Investment philosophy and process

in assets under Committee averaging drives all strategies

management 37+ years experience

A broad spectrum of Principals share the Demonstrated thought

strategies to meet a same values and invest leadership throughout

range of client profiles alongside our clients our history

3

Overview Philosophy Outlook Strategy Appendix

KEY DIFFERENTIATORS

“It is worth noting that few institutional money managers invest their own money along

with their clients’ funds. The failure to do so frees these managers to single-mindedly

pursue their firms’, rather than their clients’, best interests.”

SETH KLARMAN

High-conviction, forward-looking point of Differentiated portfolios with high active

view expressed through our Outlook share and low correlation to peers

and benchmark

Highly experienced team with demonstrated Partnership model aligns interests

thought leadership of clients and team

4Overview Philosophy Outlook Strategy Appendix

SEASONED MANAGEMENT AND INVESTMENT TEAMS

Operating Committee

Stephen Burke Sean Lawless Kristen Niebuhr

Managing Partner Partner COO & CCO

37 yrs. 37 yrs. 37 yrs. 37 yrs. 37 yrs. 37 yrs.

INDUSTRY INDUSTRY INDUSTRY INDUSTRY INDUSTRY INDUSTRY

Michael Schaenen Andrew Schmeidler Arnold Schmeidler

Senior Partner Partner Senior Partner

Investment Policy Committee

Brian Barry Stephen Burke Sean Lawless Nitin Sacheti

Portfolio Manager Managing Partner Partner Portfolio Manager

37 yrs.

18 yrs. 8 yrs. 37 yrs. 4037 yrs.

yrs. 1437 yrs.

yrs. 37yrs.

34 yrs. 37yrs.

15 yrs. 37

16 yrs.

yrs. 37 yrs.

1 yr.

INDUSTRY

INDUSTRY INDUSTRY

AT FIRM INDUSTRY

INDUSTRY ATINDUSTRY

FIRM INDUSTRY

INDUSTRY INDUSTRY

AT FIRM INDUSTRY

INDUSTRY INDUSTRY

AT FIRM

Michael Schaenen Andrew Schmeidler Arnold Schmeidler Ross Taylor

Senior Partner Partner Senior Partner Partner

61 yrs. 22 yrs. 29 yrs. 25 yrs. 62 yrs. 50 yrs.

37 yrs. 12 yrs.

INDUSTRY AT FIRM INDUSTRY AT FIRM INDUSTRY AT FIRM

INDUSTRY AT FIRM

5Overview Philosophy Outlook Strategy Appendix

CORE PHILOSOPHY

“Our philosophy is to buy the most assets, cash flow and earnings for the fewest dollars,

among leading companies that stand to be the beneficiaries of global capital flows.”

ARNOLD SCHMEIDLER, SENIOR PARTNER

Securities trade in an Opportunities to invest The best investments

auction market with in good businesses are often initially

inherent inefficiencies exist regardless of accompanied by higher

resulting in mispricing market direction levels of discomfort

of securities

There is often an inverse Undervalued companies Investment risk is

relationship between the with identifiable earnings- viewed as overpaying

popularity of a security growth catalysts offer for a business or

and its value attractive absolute returns incorrectly projecting

without excessive risk its future earnings

6Overview Philosophy Outlook Strategy Appendix

A DIFFERENTIATED INVESTMENT PHILOSOPHY AND APPROACH

Define global

environments and Evaluate and Construct and

who will be the select individual implement

beneficiary of securities portfolios

capital flows

RISK ASSESSMENT AND MANAGEMENT

Ongoing Industry Business

Scenario Analysis Selection Valuation Support

7Overview Philosophy Outlook Strategy Appendix

STRICT ADHERENCE TO SELL DISCIPLINE

Investment thesis is no Price target is realized Earnings impairment

longer supported

Portfolio guideline Better relative opportunity Risk management

compliance and control

8Overview Philosophy Outlook Strategy Appendix

A BROAD RANGE OF STRATEGIES TO MATCH CLIENT NEEDS

Small Cap Equity

AUM: ~$15M

Asset Classes

All Cap Equity 6

AUM: ~$700M • ARS Focused

Small Cap

Strategy

Core Equity 5 • ARS Focused

POTENTIAL RETURN

AUM: ~$350M ETF Strategy

• ARS Focused

Asset Allocation 4 • ARS Core All Cap Strategy

AUM: ~$190M Equity Strategy

Alternatives 3 • ARS Tactical Sector

AUM: ~$90M Allocation ETF Strategies

• ARS Tactical

2 Asset Allocation

Fixed Income • ARS Multi-Strategy Balanced Strategy

AUM: ~$20M

• Papyrus Capital

Fund, L.P. Strategies

1

• ARS Core Fixed

Income Strategy POTENTIAL RISK

Non-discretionary assets and customized portfolios ~$185M.

This graph is shown for illustrative purposes only. While directionally accurate, our strategies do not necessarily exhibit a linear and geometric progression in the relationship

between risk and return. Assets under management figures are as of March 31, 2021.

9Overview Philosophy Outlook Strategy Appendix

Outlook

Investment Outlook The Outlook

10Overview Philosophy Outlook Strategy Appendix

THE SIX CRITICAL TRANSFORMATIONS

“The global COVID-19 pandemic shows few signs of relenting – in fact, in addition to its

dual burden on lives and livelihoods, it is triggering civil unrest, new concerns about

economic inequality, geopolitical tensions, and many other effects. The pandemic is

more than an epidemiological event; it is a complex of profound disruptions.”

McKinsey Global Institute

The Monetary and Fiscal The Geopolitical and The Digital

Transformation Political Transformation Transformation

The Social and Societal The Climate The Educational

Transformation Transformation Transformation

11Overview Philosophy Outlook Strategy Appendix

OUR OUTLOOK

Macro Considerations

• Six critical transformations are occurring • Pent-up demand from consumers,

simultaneously and changing how we live, learn, corporations, and government is driving

work and govern economic activity in 2021 and beyond

• Technological advances continue to • Potential for “economic scarring” or long-term

reshape society and accelerate the rate of negative impact for large segments of global

change of new tech, while creating new population is elevated

businesses with large total addressable markets

• Markets will be driven by earnings growth

• Massive monetary and fiscal policy response rather than multiple expansion

working through global economy stoking inflation

• Potential tax and regulatory changes pose

fears which should be transitory

headwinds for earnings

• Policy initiatives continue to favor equities.

• Global system adjusting to changes in

Government bonds are offering the most

monetary policies, politics, terms of trade,

unattractive risk/reward returns in memory

and COVID-19

• Global recovery is uneven due to the various

• Adjustments in global supply chains

pre-COVID and post-COVID health and

including on-shoring, re-shoring, and

economic policy responses

improving resiliency and adaptability

• Increasing impact of climate change on society

12Overview Philosophy Outlook Strategy Appendix

THE RESTART: PENT-UP DEMAND

Personal Savings Rate

Percent, Quarterly, Seasonally Adjusted

20.0%

18.0%

16.0%

14.0%

12.0%

10.0%

8.0%

6.0%

4.0%

2.0%

0.0%

59

62

65

68

71

74

77

80

83

86

89

92

95

98

01

04

07

10

13

16

19

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

n-

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Ja

Source: St. Louis Federal Reserve. December 2020

13$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

$7,000,000

$0

Oct-51

Jan-53

Apr-54

Overview

Jul-55

Oct-56

Jan-58

Apr-59

Jul-60

Oct-61

Jan-63

Apr-64

Jul-65

Source: St. Louis Federal Reserve. December 2020

Oct-66

Jan-68

Apr-69

Philosophy

Jul-70

Oct-71

Jan-73

THE RESTART: PENT-UP DEMAND

Apr-74

Jul-75

Oct-76

Jan-78

Apr-79

Jul-80

Oct-81

Jan-83

Apr-84

Outlook

Jul-85

Oct-86

Jan-88

Apr-89

Jul-90

Oct-91

Jan-93

Apr-94

Jul-95

Total Capital Expenditures

Oct-96

Jan-98

Apr-99

Strategy

Jul-00

Oct-01

Percent, Quarterly, Seasonally Adjusted, Millions of Dollars

Jan-03

Apr-04

Jul-05

Oct-06

Jan-08

Apr-09

Jul-10

Oct-11

Jan-13

Apr-14

Jul-15

Appendix

Oct-16

Jan-18

Apr-19

Jul-20

14Overview Philosophy Outlook Strategy Appendix

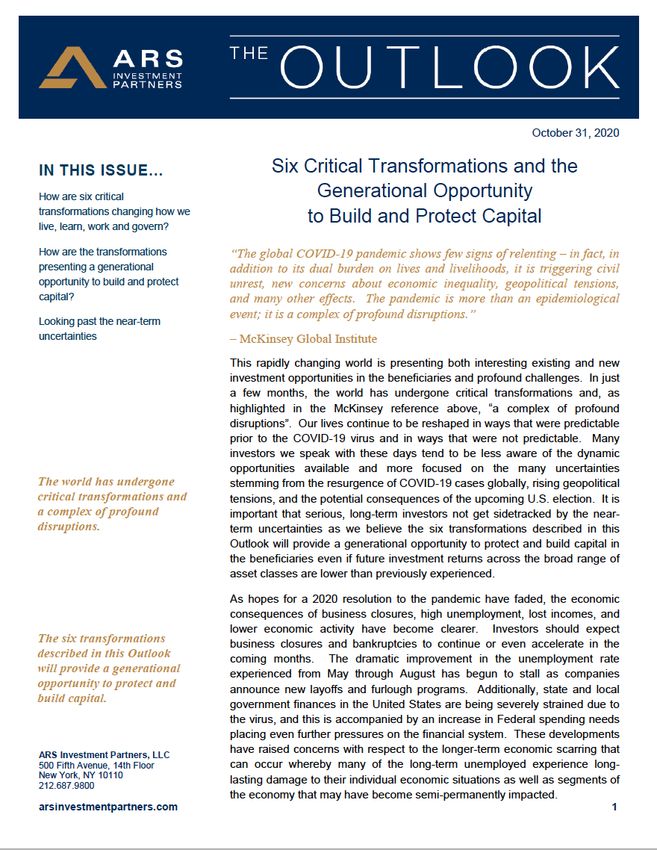

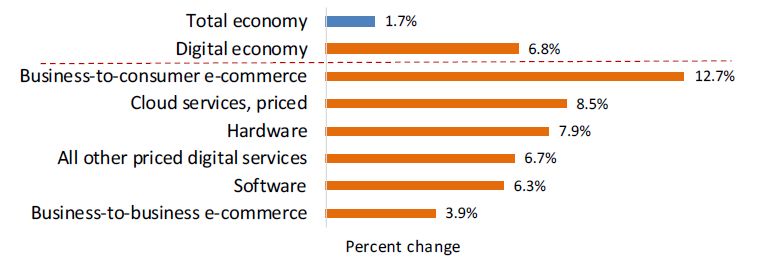

THE GROWTH OF THE DIGITAL ECONOMY

Digital Economy Current-Dollar Value Added and Share of Total GDP

Source: U.S. Bureau of Economic Analysis, New Digital Economy Estimates

15Overview Philosophy Outlook Strategy Appendix

THE GROWTH OF THE DIGITAL ECONOMY

Real Gross Output Index

Real Gross Price Index

Source: U.S. Bureau of Economic Analysis, New Digital Economy Estimates

16Overview Philosophy Outlook Strategy Appendix

THE GROWTH OF THE DIGITAL ECONOMY

Components of the Digital Economy: Real Value-Added Average Annual Growth, 2006-2018

Source: U.S. Bureau of Economic Analysis, New Digital Economy Estimates

17Overview Philosophy Outlook Strategy Appendix

OUR OUTLOOK

Areas of Focus

Technology Companies Healthcare Companies

• Benefiting from unprecedented innovation ― • Technology-enabled breakthroughs

particularly those that are integral to the • Strong product pipelines

introduction of 5G

• Growing dividends

• ARS is focused on the beneficiaries including:

‒ Telecommunications • Better insulated from potential

‒ Cloud price interference

‒ Semiconductor and equipment Dividend Growers

‒ Mobile communications

• Strong balance sheets that will continue to

‒ Network infrastructure

attract capital in a low-interest environment

‒ Software services

‒ Cybersecurity Special Situation Investments

‒ Connectivity solutions

• Business models distinctly positioned to

‒ Autonomous driving and display

benefit from major economic trends

Industrial and Materials Investments Emerging Themes

• Well-defined end-market demand, including

• Technology that drives changes in education

defense and infrastructure supported by

and healthcare

state and local governments

18Overview Philosophy Outlook Strategy Appendix

OUR OUTLOOK

Company Characteristics

• Those corporations with “embedded advantages”

• Top-line growth in a low-growth environment

• Market share gainers

• Increasing free cash flows

• Improving margins

• Ability to increase pricing power

• Growing dividends

19Overview Philosophy Outlook Strategy Appendix

OUR OUTLOOK

Potential Risks in the System

• Policy response overheats global economy • Inequality being exacerbated by policy

causing inflation and a tightening of monetary response

conditions at a vulnerable time for economy

• Rising deficits and debt servicing costs for

• Global supply chain disruptions due to the United States

COVID-19 pandemic

• Central bank policy missteps in normalizing

• Geopolitical — China’s aggressions in the South monetary policy

China Sea, shifting global alliances and tensions

• Demographic challenges in many nations

in other parts of world including the Middle East

• Political dysfunction in developed nations

• Global debt increasing and straining

government balance sheets • Another pandemic in the next few years

• Rate and magnitude of change in interest rates, • Struggle to vaccinate large segments of the

inflation rates and currencies is too sudden for global population creates wider divergences

markets to absorb in rates of recovery

20Overview Philosophy Outlook Strategy Appendix

THE OUTLOOK ―HIGHLIGHTS FROM FEBRUARY 2021

Pent-up demand will support economic activity

in the second half of 2021.

Globally, governments have provided stimulus

equal to more than 33% of global GDP and

this figure continues to rise. The liquidity

injected into the system has allowed the global

economy to absorb the shock of the pandemic

and rebound from the brink of a severe

recession, if not, a depression.

There are investable ideas present in virtually

all market environments, and investors should

be able to achieve attractive absolute and

relative returns over time by owning the

businesses that are the beneficiaries of the

secular trends.

ARS communicates its key investment themes

to clients through The Outlook ― in continuous

publication for more than 40 years.

CLICK HERE FOR MORE INSIGHTS:

arsinvestmentpartners.com/outlook-insights/

21Overview Philosophy Outlook Strategy Appendix

Differentiated Investment Strategy

ARS Focused

All Cap Strategy

22Overview Philosophy Outlook Strategy Appendix

A DIFFERENTIATED INVESTMENT PHILOSOPHY AND APPROACH

Focused All Cap — Portfolio Construction and Security Selection

High-conviction, Strong active share Leverages proprietary

absolute-return approach leading to low correlation macro and fundamental

research process

Opportunistic Unconstrained by sector Best ideas represented

investment approach weightings and market in 25 – 30 holdings

capitalization

23Overview Philosophy Outlook Strategy Appendix

EVALUATE AND SELECT INDIVIDUAL SECURITIES

INVESTMENT PROCESS Identify those undervalued companies that

Focused All Cap will be the beneficiaries of capital flows

Screens Characteristics

VALUE • Price/Earnings • Value metrics must be supportive of what we would be

• Price/Free Cash Flow willing to pay if we were to acquire the entire corporation

• Price/Sales

• Market Value versus Asset Value

• Return on Invested Capital

GROWTH • Earnings Growth Rate • Historic EPS growth rates are significantly higher than

• Asset Value Growth benchmark average

• Dividend Growth Rate • Expected catalysts

• Product Cycle

SOFT • Institutional Ownership Composition • High barriers to entry

• Relative Value to Peers • Target managements whose interests are aligned

• Insider Ownership with shareholders

• Relative Value to Indices • Favor dividend programs

• Analyst Coverage • Buy shares with light institutional and analyst following

• Relative Historic Valuation • Hidden assets

• Dividend Yield • Good management teams

• Use of Free Cash Flow

All screens are tailored to specific industries.

24Overview Philosophy Outlook Strategy Appendix

REPRESENTATIVE ARS FOCUSED ALL CAP HOLDINGS*

COMMUNICATION SERVICES FINANCIALS HEALTH CARE

ALPHABET INC. (GOOGL) 4.80% JPMORGAN & CHASE CO. (JPM) 3.47% ASCENDIS PHARMACEUTICAL (ASND) 2.35%

CHARTER COMMUNICATIONS (CHTR) 3.44% BIOHAVEN PHARMACEUTICAL (BHVN) 3.98%

INFORMATION TECHNOLOGY

DISH NETWORK CORP. (DISH) 2.22%

APPLE INC. (AAPL) 4.60% MATERIALS

LIBERTY LATIN AMERICA LTD. (LILAK) 3.10% CLEVELAND CLIFFS INC. (CLF) 3.78%

INTRUSION INC. (INTZ) 3.95%

CONSUMER DISCRETIONARY LAM RESEARCH CORP. (LRCX) 4.00% MARTIN MARIETTA MATERIALS (MLM) 2.56%

AMAZON.COM INC. (AMZN) 4.34% MICRON TECHNOLOGY INC. (MU) 4.63% MP MATERIALS CORP (MP) 3.19%

GENERAL MOTORS CO. (GM) 3.91% MICROSOFT CORP. (MSFT) 5.07% CASH

NVIDIA CORP. (NVDA) 2.50% USD 3.73%

INDUSTRIALS

FEDEX CORP. (FDX) 2.17% NXP SEMICONDUCTORS NV (NXPI) 3.67%

L3HARRIS TECHNOLOGIES INC. (LHX) 3.04% PAYPAL HOLDINGS INC. (PYPL) 2.64%

PARKER HANNIFIN CORP. (PH) 3.70% QUALCOMM INC. (QCOM) 2.98%

RAYTHEON TECHNOLOGIES (RTX) 3.02% TUFIN SOFTWARE TECH. LTD. (TUFN) 2.00%

VICOR CORP. (VICR) 1.82% VISA INC. CLASS A (V) 2.30%

XPO LOGISTICS INC. (XPO) 3.06%

Sector weights (%)

ARS Russell 3000 38.32%

25.63%

16.81%

13.56% 12.26% 13.50%

9.94% 9.81% 11.68%

8.25% 9.53%

6.33%

3.47% 2.93% 3.73%

Communication Consumer Industrials Financials Information Healthcare Materials Cash

Services Discretionary Technology

March 31, 2021

*These holdings are supplemental information to the GIPS-verified presentation. Holdings are subject to change. Indices are unmanaged, do not incur expenses and are not available

for direct investment. See Disclosure Notes.

25Overview Philosophy Outlook Strategy Appendix

ABSOLUTE RETURNS AND COMPOUNDING OF CAPITAL

Focused All Cap Market Capture and Total Risk/Reward, Informa Investment Solutions

(period ending March 31, 2021)

Upside capture Risk/return characteristics

(since inception, January 1993) (since inception, January 1993)

ARS Russell 3000 13

40.00

29.76% 28.58%

30.00 12 ARS

20.00

Annualized Returns

11

10.00

Downside Market Capture

89.53%

0.00 10

Upside Market Capture

104.12%

-10.00 Russell 3000

9

-20.00

-30.00 -26.17% 8

-29.08% 15 17 19 21 23

-40.00 Standard Deviation

Market Capture and Risk/Return statistics are calculated by Informa on a gross-of-fees basis. See Disclosure Notes.

26Overview Philosophy Outlook Strategy Appendix

HIGH-CONVICTION INVESTING

Focused All Cap Quartile Ranking Bar, Informa Investment Solutions (PSN) All Cap Core

(period ending March 31, 2021; inception January 21, 1993)

Year-to-Date 1 Year 3 Years* 5 Years* 10 Years* Since Inception*

RETURN RANK RETURN RANK RETURN RANK RETURN RANK RETURN RANK RETURN RANK

ARS Focused All Cap

4.19% 86 72.44% 17 17.13% 26 18.74% 5 10.84% 92 12.29% 20

(gross of fees)

(net of fees) 3.92% — 70.63% — 15.90% — 17.55% — 9.89% — 11.37% —

Russell 3000 6.35% 65 62.53% 47 17.12% 29 16.64% 33 13.79% 25 10.38% 60

90

80

70

60

50

40

30

20

10

0

-10

Year-to-Date 1 Year 3 Years 5 Years 10 Years Since Inception

Performance rankings from Informa PSN are shown on a gross-of-fees basis.

*Performance numbers are annualized for all time periods over 1 year. See Disclosure Notes.

27Overview Philosophy Outlook Strategy Appendix

Appendix

Strategy Composite Strategy

Performance Definitions

Professional

Biographies

28Overview Philosophy Outlook Strategy Appendix

ARS FOCUSED ALL CAP COMPOSITE PERFORMANCE

Composite

Asset-Weighted Return

Period Composite Benchmark Composite Firm

Ending Number of Composite 3-Year 3-Year Assets Assets

12/31 Gross Net Russell 3000 Portfolios Dispersion Ex-Post St. Dev. Ex-Post St. Dev. ($ in Millions) ($ in Millions)

1993* 12.43% 11.39% 10.41% 1 — N/A N/A 5.62 144.76

1994 3.64% 2.80% 0.19% 1 — N/A N/A 21.11 163.23

1995 29.55% 28.36% 36.80% 2 — N/A N/A 27.21 217.34

1996 12.07% 11.06% 21.82% 2 — N/A N/A 30.35 247.56

1997 31.62% 30.51% 31.78% 2 — N/A N/A 39.77 321.72

1998 18.25% 17.27% 24.14% 2 — N/A N/A 45.52 376.14

1999 33.97% 32.87% 20.90% 2 — N/A N/A 51.46 470.38

2000 4.09% 3.29% -7.46% 2 — N/A N/A 55.41 526.99

2001 -1.71% -2.41% -11.46% 2 — N/A N/A 97.84 540.94

2002 -16.44% -17.01% -21.54% 2 — N/A N/A 85.09 439.66

2003 33.70% 32.85% 31.06% 2 — N/A N/A 117.15 548.82

2004 13.59% 12.85% 11.95% 1 — N/A N/A 32.77 596.36

2005 31.48% 30.55% 6.12% 1 — N/A N/A 41.56 809.13

2006 18.25% 17.49% 15.72% 1 — N/A N/A 48.87 1,043.06

2007 33.60% 32.78% 5.14% 1 — N/A N/A 62.83 1,398.39

2008 -42.91% -43.27% -37.31% 5 — N/A N/A 93.71 1,031.74

2009 27.59% 26.81% 28.34% 3 — N/A N/A 66.25 1,369.87

2010 26.62% 25.74% 16.93% 6 2.84 N/A N/A 120.52 1,589.65

2011 -8.30% -8.88% 1.03% 6 — 21.16% 19.35% 91.12 1,286.20

2012 3.62% 2.93% 16.42% 6 — 17.49% 15.73% 70.38 1,125.16

2013 31.19% 30.23% 33.55% 4 — 15.36% 12.53% 57.74 1,181.07

2014 2.28% 1.50% 12.56% 5 — 11.21% 9.29% 61.52 1,182.90

2015 -0.37% -1.11% 0.48% 3 — 11.05% 10.58% 47.19 1,039.85

2016 9.16% 8.28% 12.74% 3 — 11.19% 10.88% 49.56 892.23

2017 32.62% 31.23% 21.13% 3 — 10.42% 10.09% 65.30 1,084.27

2018 -14.56% -15.45% -5.24% 4 — 12.95% 11.18% 62.26 984.94

2019 35.74% 34.74% 31.02% 3 — 14.09% 12.21% 71.93 1,208.76

2020 34.80% 33.38% 20.89% 3 — 20.26% 19.41% 92.58 1,447.81

*This period represents a partial year performance (1/21/93 – 12/31/93) and the return is not annualized. 29

Performance data for both gross and net of fees reflect the reduction of transaction costs. Net of fees reflects the deduction of

advisory fees. Performance is GIPS-verified through 12/31/2018. The investment advisory fees are described in Part 2A of the Form

ADV. Performance results reflect the reinvestment of dividends and income. Past performance is not indicative of future results.

Index information is provided for illustrative purposes only. Indices are unmanaged, do not incur expenses and are not available for

direct investment. See Disclosure Notes.Overview Philosophy Outlook Strategy Appendix

PROFESSIONAL BIOGRAPHIES

Stephen Burke Michael Schaenen

Managing Partner Senior Partner

Stephen Burke joined ARS in June of 2007. Previously, he was the CEO Michael Schaenen entered the investment business in 1960 as a

of Deutsche Asset Management’s $165 billion Institutional Business in registered representative at Bache & Co. Prior to joining ARS, Michael

the Americas, serving the Defined Benefit, Insurance, and Cash was the founding partner of Schaenen Wood & Associates (“SWA”), an

Management segments. Stephen joined Deutsche after a 21-year career asset management firm whose total assets under management

at the Mellon Financial Corporation where he served as Vice Chairman exceeded $1.25 billion by 1993, at which point SWA was acquired by

of Standish Mellon Asset Management and was responsible for KeyCorp. Michael left SWA in 1995, forming Schaenen Fox &

institutional sales, marketing, and client services. Before joining Associates, which later became Somerset Capital Advisers, LLC.

Standish, he was the President of Dreyfus’ Marketing and Advertising Among his previous roles, Michael was a General Partner at

Division. Stephen holds a BA from Gettysburg College. Oppenheimer & Co. Michael received a BA in Psychology from Amherst

College.

Arnold Schmeidler

Senior Partner P. Ross Taylor III

Prior to founding ARS Investment Partners, LLC, Arnold Schmeidler was Partner

Vice President at A.W. Benkert & Company. He earned a BS in

Economics from New York University and an MS in Finance from Ross Taylor’s professional investing experience began in 1984 as a

Columbia University, where he studied under David Bonbright, a protégé portfolio manager. Prior to joining ARS, Ross was the Chief

of David Dodd (Graham & Dodd). Over the course of his career, he has Investment Officer for Somerset Capital Advisers, LLC beginning in

been quoted and/or interviewed by such publications as Barron’s, 2009. He previously served as a Managing Director and Principal of

Forbes, Fortune, Institutional Investor, International Herald Tribune, Caxton Associates, LLC (“Caxton”). At Caxton he managed an active

Money Magazine, The New York Times, The Wall Street Transcript, and equity product utilizing a value-driven strategy. Prior to joining Caxton,

The Wall Street Journal. Ross worked at U.S. Trust Company, rising to Senior Vice President

and Manager of Institutional Equity and Balanced Investing. Before

that Ross worked at Management Asset Corporation from 1986 to

1987, and Brundage, Story, and Rose from 1984 to 1986. Ross

received a BS in Economics from the University of Puget Sound and

an MBA from the Wharton School of the University of Pennsylvania.

30Overview Philosophy Outlook Strategy Appendix

PROFESSIONAL BIOGRAPHIES

Sean Lawless, CFA Kristen Niebuhr

Partner Chief Operating Officer

Sean Lawless entered the industry in 1987, primarily specializing in Chief Compliance Officer

investment manager selection and due diligence for families and Kristen Niebuhr joined ARS in 2017 and has over 30 years of

institutions. At ARS, Sean is lead portfolio manager responsible for experience in the financial services industry. At ARS she serves as the

developing multi-strategy portfolios. Prior to joining ARS, Sean joined Chief Compliance Officer and Chief Operating Officer. Previously,

Artemis Wealth, LLC (and its predecessor firm Modern Asset Kristen was Director of Practical Compliance at MarketCounsel, a

Management) in 2006 and provided investment advisory services using compliance consulting firm. Prior to that role, she served as President

a manager of managers approach. Previously, Sean was Head of of Source Financial Advisors, launched in September of 2012.

Multimanager – Americas for HSBC and a voting member of the Global Beginning in 2009, she served as Chief Administrative Officer of

Multimanager Investment Committee that was responsible for setting Alexandra & James, a holding company encompassing A&J Advisory

policy and manager selection for HSBC’s global sub-advisory Services (an RIA), Lebenthal (a B/D), A&J Family Wealth Management

businesses. He is a CFA charter holder, a member of the CFA Institute (a family office), and Smith Divorce Strategies (a divorce financial

and the New York Society of Security Analysts and received a BS in planning firm). Before joining A&J, Kristen started in 2007 with the

Economics from Southern Connecticut State University. newly-formed Constellation Wealth Advisors, overseeing their advisory

and broker-dealer operations. From 2001 through 2007, she had her

Andrew Schmeidler own consulting firm, specializing in start-up and ongoing support to

Partner advisors and hedge funds. From 1995 through 2001, she was Director

Andrew Schmeidler joined ARS in 1992 and has over 25 years of of Operations and Compliance at Schaenen Capital Management

portfolio management and research experience. Andrew served as Vice (which became Somerset Capital Advisers, LLC). She spent 1987

Chairman of A.R. Schmeidler & Co. Inc. prior to the business through 1995 in various roles at Merrill Lynch and Smith Barney. She

combination with ARS. He continues to manage accounts for received a BA in Economics from Boston University.

corporations, foundations, and high net-worth clients. Earlier in his

career at A.R. Schmeidler/ARS, he was a portfolio manager and

research analyst covering multiple sectors with a focus on the banking

and semiconductor capital equipment industries. In 2002 he returned to

ARS after spending two years as a founding member and Senior Vice

President of GasPedal Ventures, LLC, an internet incubator and

business development consultancy. Andrew has a BA in Government

from Skidmore College.

31Overview Philosophy Outlook Strategy Appendix

PROFESSIONAL BIOGRAPHIES

Brian Barry, CIMA Tom Winnick

Portfolio Manager Director of Business Development

Brian Barry joined the investment industry in 2003 and ARS in 2013. Tom Winnick joined ARS in 2020 as Director of Business Development

Previously, Brian worked at Bank of America in various investment responsible for the firm’s distribution effort. Tom has 30 years of

roles. Most recently, he was a Vice President and Portfolio Manager for experience in sales and distribution for financial institutions. Prior to

U.S. Trust and was responsible for advising high net worth and joining ARS, he was Managing Director in The Private Client Group at

institutional clients. Before joining U.S. Trust, he served as an Associate Oppenheimer Funds where he was responsible for distribution through

in the Consulting Services Group and was responsible for manager Private Banks, Trust Banks and Family Offices in the mid-Atlantic

search, selection and ongoing due diligence of investment products. He region. He previously served as Senior Vice President, Institutional

began his career as an Analyst within Banc of America Securities’ Services, at Franklin Square Capital Partners where he launched the

Corporate and Investment Bank. Brian received a BA in History and firm’s efforts to distribute to RIAs, Private Banks and Trust Companies.

Economics from the College of the Holy Cross and an MBA in Prior to Franklin Square, Tom was Managing Director at Dreman Value

International Finance from New York University’s Stern School of Management where he was responsible for all distribution and

Business. marketing efforts. Previously, Tom was President at DWS Distributors

where he held responsibility for all facets of intermediary distribution

Nitin Sacheti including sales and account management for the Broker Dealer, Banks

Portfolio Manager and Independent Channels. From 1993 to 2002, Tom held various sales

management and leadership responsibilities with Dreyfus Service

Nitin Sacheti joined ARS in 2020. Prior to joining ARS, he was the Corporation including creating their Financial Institutions Group,

Founder and Portfolio Manager of Papyrus Capital, an intrinsic value launching their separately managed account platform and overseeing

focused, long/short equity fund. Before founding Papyrus, Nitin was a the national key account group. He received a BA in Business

Senior Analyst with Equity Contribution at Charter Bridge Capital where Management from Temple University.

he managed the firm’s investments in the technology, media and

telecom sectors as well as select consumer investments. Previously, Sara Near

Nitin was a Senior Analyst at Cobalt Capital, managing the firm’s

Business Development Associate

technology, media and telecom investments. Prior to Cobalt, he was a

Senior Analyst at Tiger Europe Management. Nitin began his investment Sara Near joined ARS is 2020. She received her BA in Neuroscience

career in 2006 at Ampere Capital Management, a consumer, media, with a concentration in chemistry from Amherst College. She continued

telecom and technology focused investment firm, initially as a Junior her education at University College London and later, in 2020, wrote a

Analyst, later becoming Assistant Portfolio Manager. He received a BA thesis under Professor Robert Marx (Ph.D.). Previously in 2018, Sara

in Economics from the University of Chicago and was a visiting worked at Brown University’s Liu Laboratory researching epilepsy that

undergraduate student in Economics at Harvard University. arises from focal cortical dysplasia and genomics.

32Overview Philosophy Outlook Strategy Appendix

STRATEGY DEFINITIONS

ARS Core Fixed Income Asset Allocation (continued)

ARS Core Fixed Income Strategy ARS Tactical Asset Allocation Balanced Strategy

Our approach is to earn an appropriate level of income consistent Draws elements from our Core Equity, All Cap and Core Fixed Income

with the preservation of principal. We do not lower the standards for strategies to generate returns while reducing volatility and downside risk.

creditworthiness in the search for extra yield because we have

seen far too often that this approach leads to excessive loss of capital. ARS Core Equity

ARS Core Equity Strategy

Alternatives Invests in those companies we deem high-quality, with strong balance

ARS Multi-Strategy sheets and reasonable earnings growth. These companies have

A custom portfolio designed to meet a client’s specific needs by above-average dividend yields with the prospect for dividend growth.

investing in proprietary and third-party-managed strategies. Strategy The strategy intends to be well-diversified across sectors.

allocations are tailored to a client’s profile, focused on liquidity, income,

growth, and risk tolerance. In an effort to achieve superior risk-adjusted All Cap

returns, ARS may use traditional or alternative investment strategies in ARS Focused ETF Strategy

constructing the portfolio. Leverages our macro-outlook by constructing a portfolio that utilizes

Papyrus Capital Fund, L.P. ETFs to express our views. The strategy concentrates on sector,

A long/short strategy seeking to compound partner capital by investing industry and sub-industry ETFs that we feel provide the greatest

in mis-priced public securities, mostly equities, in the technology, media, exposure to our highest conviction themes.

telecom and consumer sectors with an emphasis on intrinsic value ARS Focused All Cap Strategy

generation over time. We seek to identify the best-positioned and undervalued companies

across market capitalization ranges and include investments

Asset Allocation characterized as growth and/or value in their orientation. Our primary

ARS Tactical Sector Allocation ETF Strategies goal is to build the purchasing power of portfolios over time.

Leverages our investment philosophy and process, while providing a

strategy that more closely tracks the benchmarks with limited turnover. Small Cap

Our ETF strategy offers important benefits for the implementation and ARS Focused Small Cap Strategy

management of client portfolios including exposures to broad markets, We believe market inefficiencies create mispricings and under-

sectors and geographies with enhanced liquidity and transparency. valuations, which can be substantial in smaller capitalization stocks. We

employ a private equity valuation approach in assessing public market

equities to identify U.S. micro- to small-cap companies with

capitalizations typically ranging from $100 million – $2.5 billion trading at

discounts of 50% or more from intrinsic value.

33Overview Philosophy Outlook Strategy Appendix

DISCLOSURE NOTES

Past performance is not indicative of future results. is designed to take into account variations reflecting conditions across regions, market

capitalization sizes, sectors, style segments and combinations. The Bloomberg

Definition of the Firm – ARS Investment Partners, LLC (“ARS”) was originally Barclay’s Intermediate US Government/Credit Bond® is a broad-based flagship

founded as A.R. Schmeidler & Co., Inc. in 1971 and is majority-owned by Artemis US benchmark that measures the non-securitized component of the Bloomberg Barclay’s

Corporation. Artemis US Corporation is 100% owned by Artemis Corporation, an US Aggregate Index with less than 10 years to maturity. The index includes

Ontario, Canada entity, which is in turn 100% owned by Artemis Investment investment grade, US dollar-denominated, fixed-rate treasuries, government-related,

Management Corporation, a financial services firm headquartered in Toronto, Ontario, and corporate securities. All Blended Benchmarks are rebalanced monthly.

Canada. Mr. Miles Nadal is the controlling shareholder of Artemis Investment

Management Corporation. ARS is a registered investment adviser under the Composite Definitions – ARS Focused All Cap includes all fee-paying, discretionary

Investment Advisers Act of 1940. ARS Investment Partners, LLC claims compliance institutional portfolios managed by ARS in a Focused All Cap strategy with an

with the Global Investment Performance Standards (GIPS) and has prepared and absolute return-oriented focus having a minimum initial portfolio size of $5 million

presented this report in compliance with the GIPS Standards. ARS Investment (amount lowered from $10 million on 7/1/2010). The Focused All Cap strategy

Partners, LLC has been independently verified for the periods 1/1/2000 through requires that equity, equity-like securities, and cash represent a target of 90% of the

12/31/18. The verification report(s) is/are available upon request. Verification portfolio value. If a portfolio does not have at least 90% of its value in these assets,

assesses whether (1) the firm has complied with all the composite construction the portfolio will be removed from the composite for the entire period and will be

requirements of GIPS standards on a firm-wide basis and (2) the firm’s policies and included in the composite again if its allocation is aligned with the above parameters

procedures are designed to calculate and present performance in compliance with for one full period. The composite was created in January 2007. Effective 7/1/2010,

GIPS standards. Verification does not ensure the accuracy of any specific composite the composite was redefined to include taxable accounts which had previously been

presentation. Benchmark returns are not covered by the report of independent excluded. Effective 1/1/17 a model fee of 1.05% was used to calculate net returns.

verifiers. Management believes that the returns prior to 2000 are accurate, but due to ARS Core Equity includes discretionary institutional portfolios managed by the Firm

a lack of firmwide client data, GIPS compliance cannot be claimed prior to 1/1/2000. and invests in companies with above-average dividend yields and strong balance

sheets, typically with clear prospects for dividend growth. For periods prior to 1/1/17,

Benchmark Definitions – The Russell 3000® measures the performance of the the composite is made up of 100% wrap portfolios, which may include, but is not

largest 3,000 US companies representing approximately 98% of the investable US limited to broker, investment advisory, custodial, and administrative fees. As of 1/1/17,

equity market. The Russell 3000® is constructed to provide a comprehensive, the composite began using non-wrap accounts. Also, as of 1/1/17, we no longer had

unbiased and stable barometer of the broad market and is completely reconstituted any wrap accounts. The composite was created in October 2011. Effective 1/1/17 a

annually to ensure new and growing equities are included. The S&P 500® includes model fee of 1.25% was used to calculate net returns. ARS Focused Small Cap

500 leading companies and covers approximately 80% of available market invests in companies with market capitalizations typically ranging from $100 million to

capitalization. The S&P Mid Cap 400® is designed to measure the performance of $2.5 billion. The portfolio is long biased, aiming to control risk via cash levels, prudent

400 mid-sized companies, reflecting the distinctive risk and return characteristics of shorts, inverse ETFs and option strategies. This composite was created in July 2018.

this market segment. The S&P Small Cap 600® seeks to measure the small-cap Net returns are calculated using a 1.25% model fee. ARS Focused ETF leverages our

segment of the U.S. equity market. The index is designed to track companies that macro outlook by constructing a portfolio that utilizes ETFs to express our views. The

meet specific inclusion criteria to ensure that they are liquid and financially viable. The strategy concentrates on sector, industry, and subindustry ETFs that we feel provide

Russell 2000® includes approximately 2,000 of the smallest securities based on a the greatest exposure to our highest conviction secular trends. This composite was

combination of their market capitalization and current index membership. The Russell created in June 2017. A model fee of 0.70% is used to calculate net returns. ARS

2000® is constructed to provide a comprehensive and unbiased small-cap barometer Tactical Sector Allocation Balanced ETF leverages our investment philosophy and

and is completely reconstituted annually to ensure larger stocks do not distort the process, while providing a strategy that more closely tracks the benchmarks with

performance and characteristics of the true small-cap opportunity set. The MSCI All limited turnover. This composite was created in December 2016. The Strategy seeks

Country World Index (ACWI) ex US® is designed to represent performance of the full a balance of current income and capital growth. The strategy strives for a 60/40

opportunity set of large- and mid-cap stocks across 23 developed (ex. US) and 26 balance between equity and fixed income ETFs with a 25% variance. A model fee of

emerging markets. It covers more than 3,000 constituents across 11 sectors and 0.70% is used to calculate net returns. ARS Tactical Sector Allocation Growth ETF

approximately 85% of the free float-adjusted market capitalization in each market. The leverages our investment philosophy and process, while providing a strategy that

index is built using MSCI’s Global Investable Market Index (GIMI) methodology, which more closely tracks the benchmarks with limited turnover.

34Overview Philosophy Outlook Strategy Appendix

DISCLOSURE NOTES

The primary objective is capital appreciation and growth. This composite was created Performance returns are in U.S. Dollars. Periodic returns are geometrically linked. The

in December 2016. A model fee of 0.70% is used to calculate net returns. composite rates of return have been calculated within ARS Investment Partners, LLC.

A complete list and description of the composites managed by ARS is available upon

Investment Management Fees – The investment management fees that apply to the request.

portfolio composites are as follows: Equity Accounts which include the ARS Core

Equity, ARS Focused All Cap, ARS Focused Small Cap & ARS Tactical Asset The information in this document is believed to be correct at the time of compilation,

Allocation (ARS Balanced Strategy & ARS Equity Strategy) – 1.25% per annum of the but no warranty of accuracy or reliability is given and no responsibility arising in any

first $1 million and 1.00% per annum of the next $20 million and to be discussed other way for errors and omissions (including responsibility to any person by reason of

thereafter; ARS Core Equity Account – 1.00% per annum, ETF Accounts which negligence) is accepted by ARS its officers, employees or agents. The information

include the ARS Tactical Sector Allocation ETF Strategy & ARS Focused ETF contained herein is current as of the date hereof but may become outdated or

Strategy, ARS Fixed Income ETF Strategy & ARS Growth Allocation ETF Strategy– subsequently may change. ARS does not undertake any obligation to update the

0.70% per annum of the first $5 million and 0.50% per annum of the next $20 million information contained herein in light of later circumstances or events. This document

and to be discussed thereafter; Institutional Accounts which include the ARS Tactical contains general information only and is not intended to be relied upon as a forecast,

Asset (Balanced) Strategy– 0.80% per annum of the first $25 million and 0.70% per research, investment advice, or a recommendation, offer or solicitation to buy or sell

annum of the next $25 million and to be discussed thereafter. Fixed Income Accounts any securities or to adopt any investment strategy. Nothing in this presentation

which include the ARS Core Fixed Income Strategy– 0.50% per annum of the first $15 constitutes financial, legal, or tax advice. This information is property of ARS and is

million and 0.35% per annum of the next $15 million and to be discussed thereafter. intended only for intended recipients and their authorized agents and representatives

The management fees for certain clients may differ from the above schedule because and may not be reproduced or distributed to any other person without prior written

those clients’ fees are grandfathered or because of relationships with the applicant or consent. Any distribution to social media is a willful violation of the confidential and

other accounts. For institutional accounts, certain asset or fee minimums may apply. regulatory strictures that govern this document.

Internal Dispersion – Internal dispersion is calculated using the asset-weighted Composite performance is shown gross of fees. The historical index performance

standard deviation of annual returns of all portfolios in the composite for the entire results are provided exclusively for comparison purposes only. It is not possible to

year. Dispersion is not presented for periods less than one year or when there were invest directly in an index. It should not be assumed that any account holdings will

five or fewer portfolios in the composite for the entire year. The Annualized 3-Year correspond directly to any comparative index reflected herein.

Standard Deviation is not presented for composites with less than a 36-month return.

Also, the standard deviation is not presented and not is required, for periods prior to The information contained herein (1) is proprietary to Informa Enterprise Solution PSN

2011. and/or its content providers; (2) may not be copied or redistributed; and (3) is not

warranted to be accurate, complete, or timely. Other data provided may be based

Basis of Presentation – Rates of return presented are computed using a time- upon information received from third parties which is believed to be accurate, but no

weighted rate of return methodology that adjusts for external cash flows. Total rate of representation is made that the information provided is accurate and complete. Please

return calculations includes realized and unrealized gains and losses, plus income, be sure to refer to your custodial account statement(s) as the true and accurate record

and cash and cash equivalents held. Gross performance returns are presented after of your portfolio holdings and transactions.

transaction costs and before investment management fees and all operating costs.

Net performance returns are presented after transaction costs and actual investment All data is subject to change.

management fees and before all operating costs. However, gross performance for the

ARS Core Equity Composite is presented as gross and net performance is actual Not FDIC-Insured. Not Bank-Guaranteed. May Lose Value.

investment management fees and after all operating costs and the gross returns are

presented as supplemental information. Operating costs include custodian and

administrative fees. Additional information regarding policies for valuating portfolios,

calculating performance, and preparing compliant presentations are available upon

request. Performance results for periods of less than a year are not annualized.

35You can also read