Cape Town Building Resilience in Informal Settlements - Connected Places Catapult

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

October 2020 Cape Town Building Resilience in Informal Settlements

Building Resilience in Informal Settlements 1 Executive summary Welcome to Connecting Places Catapult: Urban Links Africa (ULA) market analysis. ULA is an ambitious programme, funded by the UK government through the Global Challenges Research Fund (GCRF) and delivered by Innovate UK and Connected Places Catapult. We work closely with six cities - Nairobi, Mombasa and Kisumu in Kenya; and Cape Town, Johannesburg and eThekwini (Durban) in South Africa - to tackle some of their key urban challenges and improve citizens’ lives. ULA does this by facilitating a sustainable collaboration between the UK, South Africa, and Kenya, bringing together cities and tech ecosystems through equitable partnerships and industry investment. We share here foundational research and analysis which describes the urban challenges we are focusing on and their context in each country. Through discussion with city stakeholders we have finalised three urban challenges (one for each ULA city) in South Africa, and four urban challenges across the three Kenyan cities. The key challenges in South Africa are: • Cape Town: building resilience in informal settlements • Durban: improving solid waste management and reducing pollution • Johannesburg: adopting sustainable mobility approaches The four key challenges selected to be addressed across the three Kenyan cities of Mombasa, Kisumu and Nairobi are: • Solid waste management • Flooding • Wastewater management Traffic management and active mobility In this section of the document, we will give an overview of Cape Town. We examine the innovation potential of Cape Town comparing it with its global peers, examining its innovation ecosystem and business attractiveness. We then discuss initiatives that governments, private, local and international NGOs and other stakeholders have undertaken to address building resilience in informal settlements. We examine recent and ongoing projects which attempt to tackle these problems in order to ensure that the collaborators we are supporting as part of ULA are able to learn from and build upon the efforts of others.

Cape Town 2 Contents 1 Cape Town Overview 3 1.1 Benchmarking Cape Town’s Innovation Potential 5 1.2 Summary 6 1.3 Performance Review 7 1.4 Innovation Ecosytem 8 2 Resilience in Informal Settlements 12 2.1 Provision of basic services 14 2.2 Health and Safety 14 2.3 Inaccessibility 14 2.4 Who is doing what in the area and what are the opportunities? 15

0 Cape Town 3

Cape Town Overview

With a population of 4mn, Cape Town is the second most populous city

in South Africa after Johannesburg. It is also the legislative capital of

South Africa, with South Africa’s parliament situated in Cape Town. A

popular tourist destination, the city is known for its harbour and for

landmarks such as Table Mountain and Cape Point.

Cape Town’s economy has grown and diversified since the ending of Apartheid to establish itself as

one of South Africa’s leading gateways for capital and technology. As well as attracting international

tourists with its natural beauty, the city is attracting investors, large corporations and increasingly, start-

ups. The City has real pockets of excellence in terms of talent, technology and entrepreneurship,

spanning healthcare, biotechnology, port logistics and environmental science.

0 Cape Town 4

However, the attraction to Cape Town has resulted in high levels of density in the city. Cape Town’s

unusually high-density stems from a very large number of informal settlements of which there are

more than 175,000 in the Cape Town Metropolitan area.

These informal settlements lack sufficient access to basic services and infrastructure including

electricity, water and sanitation. Thus, preventing them from living safe and healthy lives.

This report discusses how to build resilience in informal settlements and considers the potential for

innovative solutions to be developed locally in addressing these challenges. In the first section we

discuss Cape Town’s innovation potential comparing and benchmarking the city against its global

peers and examining its innovation ecosystem.

In the second section of the report we discuss resilience in the informal settlements and the issues

residents face in accessing basic services. We discuss the various initiatives local and international

organisations have taken to address these challenges including a deeper dive into a low-cost housing

project focused case study.

0 Cape Town 5

Benchmarking Cape Town’s Innovation Potential

The trade and tourism capital of South Africa, Cape Town has successfully taken advantage of

significant economic growth and diversification following the end of apartheid to build its global

influence and establish itself as one of Southern Africa’s leading gateways for capital and technology. Its

relatively transparent governance system, its high quality of life relative to other cities in the region,

pluralism and openness to immigration and its abundant natural assets have all raised appeal not only

to visitors and residents, but also to investors, large corporates and, increasingly, start-ups. Cape Town

now has real pockets of excellence in terms of talent, technology and entrepreneurship, spanning

healthcare, biotechnology, port logistics and environmental science. However, many of the city’s

segregated spatial structures remain intact, requiring ongoing policies, investments and innovations to

combat entrenched inequalities and economic and social exclusion.

This ‘outside in’ note draws on available international benchmarks to capture Cape Town’s current

performance relative to cities in the Global South, leading cities in Sub-Saharan Africa and similar

‘peers’ globally - specialised, mid-sized trade hubs with similar lifestyle, productivity and labour market

dynamics.

Table 1: Which cities globally is Cape Town most like?iii

Global rank

Theme Most similar cities

(raw data)

115th / 300 Tel Aviv, Israel; Porto Alegre, Brazil; Hanoi,

Population

(4.0m) Vietnam

219th / 300 Valencia, Spain; Marseille, France; Medellín,

Economic size (GDP)

($75bn) Colombia

São Paulo, Brazil; Valencia, Spain ; Brisbane,

Innovation intensity* 68th / 107

Australia

Caracas, Venezuela ; Buenos Aires, Argentina ;

Sector mix** N/A

Lisbon, Portugal

Transport infrastructure Casablanca, Morocco, Belo Horizonte, Brazil ;

performance 161st / 185

Guatemala City

*No. of recognised technology-enabled start-ups, scale ups and established corporates per resident.iii **Share of economic output

across industry sectors

0 Cape Town 6

With a population of over 4 million people, Cape Town’s economic size is currently on a part with 3rd

tier European cities, revealing the negative impact of low skills, underemployment and a sector mix

that has yet to turn decisively towards more knowledge-intensive industries. Yet thanks to a cadre of

ambitious entrepreneur-led small and medium enterprises in the creative and IT industries, Cape

Town’s innovation intensity is comparable both to established ecosystems in the Global South such as

São Paulo, and also to other emerging innovation hubs that have seen significant growth in venture

capital funding in recent years, such as Brisbane and Valencia. Cape Town’s sector mix is most similar

to other cities that ally large business and finance industries with a high reliance on trade and tourism,

such as Lisbon and Buenos Aires.

Summary

Figure 1: Cape Town Ecosystem Dynamics

Economic & demographic SCALE &

fundamentals OPPORTUNITY

10

Urban sustainability 8

and resilience Target Consumer base

6

SYSTEMS

READINESS 4

2

Effectiveness Enabling

0

of city systems infrastructure

Openness to Innovation deployment

investment climate

Cape Town compared to global peers

INNOVATION

Cape Town compared to Sub-Saharan African leaders Ecosystem dynamics ENVIRONMENT

Cape Town compared to mix of Global South cities

Based on 120 metrics and 750 data points. Peers and Sub-Saharan African peers selected based on population size, productivity,

global and regional status, and visibility in global benchmarks.

Global peers (other specialised, mid-sized trade hubs with similar lifestyle assets, productivity and disparity dynamics): Barcelona,

Colombo, George Town, Hanoi, Panama City, Tel Aviv, Xiamen

Sub-Saharan African leaders: Abidjan, Accra, Dar es Salaam, Johannesburg, Lagos, Luanda, Nairobi

In the next cycle, the benchmarking data points to important imperatives for Cape Town to:

• Create more business opportunities and facilitate access to funding for low- and middle-income

households and enterprises

• Improve infrastructure and systems to integrate the informal economy

• Build on its visitor success and expand the reach of its other economic sectors in order to

strengthen appeal to other customers, investors and consumers

0 Cape Town 7

• Continue to invest in education and infrastructure to ensure companies’ skills and technological

requirements are met

Performance Review

Among cities in the Global South, Cape Town stands out most obviously for its more favourable

governance and the effectiveness of its city systems. Given its medium size, the city faces fewer of the

scale challenges that have overwhelmed other megacities in Asia and Africa, and its investment in

infrastructure through utilities upgrading schemes and the expansion of its efficient bus rapid transit

system has led to significant incremental improvements in citizens’ quality of life.

Cape Town’s all-round mobility system is promising, but performance continues to be held back by

severe congestion and low uptake of public transport relative to other cities. The city now sits just

outside the top 50 globally, and 6th out of 27 Global South cities, for the performance, maturity and

innovativeness of its mobility system. However, it is among the top 30 most congested cities in the

world, dragging down productivity, with more than 150 hours lost to congestion every yeariv.With more

than 60% using private transport to commute, Cape Town also still ranks only 16th out of 18 Global

South cities for the share of people commuting via active or public transport, partly because of the

prohibitively high cost of transport for those on low incomes and the inadequate transport network in

connecting peripheral areas to the metropolitan core. As bus rapid transit systems require high

densities to be economically viable, Cape Town’s BRT has also tended to underperform in terms of

ridership and economic viability, with an average daily ridership 3 times lower than the African

averagev.

Cape Town stands out in the region for its technology infrastructure. The roll-out of 1,300km of fibre-

optic cables and Wi-Fi provision in public spaces means it now places 8th out of 28 Global South cities

for access to Wi-Fi hotspots and just outside the top 10 out of 60 Global South cities for its average

fixed broadband speed, top in sub-Saharan Africa.

Where Cape Town falls behind its peers is for scale and global reach to achieve catalytic growth in

advanced industries. Despite its appeal to real estate investors and visitors, Cape Town is still outside

the top 100 for networked HQ presence of internationally trading knowledge firms, and falls well

behind for its productivity and employment growth prospects, while other cities internationally (such

as Hanoi, Colombo and Xiamen) have used their proximity to large growth markets to achieve more

rapid inroads to diversify and grow their economies in recent years.

Cape Town’s ability to scale and showcase innovation is also hindered by very high levels of poverty. Cape

Town ranks 7th out of its global peers for the share of households earning less than $7,500 and has a Gini

coefficient of 0.58 which is substantially higher than established global citiesvi. The severity of inequality

is both a barrier to human development and constrains the size and stability of the local market and

consumer base for start-ups to grow and scale. Cape Town still has far fewer rapidly scaling and globally influential

firms compared to Global North cities with some similar assets.

Cape Town possesses some systems opportunities, but infrastructure and investment barriers persist.0 Cape Town 8

Figure 2: Cape Town’s performance relative to best performing peer across key indicators

BEST

PERFORMING Hanoi Colombo Barcelona Tel Aviv Barcelona Panama City

PEER

100%

80% Gap to top-

performing

peer

60%

40%

20%

0%

t

00

m

s)

*

ity

k

ty

en

or

r is

bp

ci

r

ns

,0

fo

ct

m

tri

ic

20

(m

te

se

st

n

ec

om

ba

in

ve

>$

d

te

el

n

on

ee

ur

in

ta

io

g

ng

es

sp

e

in

ec

of

at

t

ni

a

in

ov

al

cy

et

nd

st

r

ta

ea

re

le

n

n

en

ob

la

er

In

n

of

ea

ci

ra

t

tio

In

of

fi

cy

rr

tu

Ef

la

t

de

en

na

s

pu

co

ar

or

to

Po

d

sp

-b

an

e

ss

an

nc

se

ro

Tr

ie

C

Ea

sil

Re

SCALE & INNOVATION SYSTEMS

OPPORTUNITY ENVIRONMENT READINESS

Innovation Ecosystem

Cape Town’s overall innovation environment is promising with the 2nd highest number of innovative

companies behind Lagos, Cape Town is home to 12% of Africa’s registered innovative companies, and

also has the 4th highest share of globally recognised firms headquartered in Africa (see figure 3). It is

among the top 3 ecosystems in Africa for the number of recognised innovation hubs (accelerators,

incubators and co-working spaces), with more than 25 hubs dedicated to support start-ups.

Access to funding in Cape Town has been improving. Cape Town’s funding landscape is quite diverse

and is becoming more similar to that of more mature ecosystems, made up of angel investors, family

offices and venture capital firms. The city places an impressive 7th out of cities in Global South for the

amount of venture capital invested per person, behind only the likes of Bangalore, Pune, São Paulo,

and Nairobi. Start-ups benefit from high proximity to a large number of wealthy families that often

invest in VC-backed companies. Partly as a result of these social networks and personal connections,

Cape Town start-ups raise an estimated US$ 20,000 in seed funding annually, almost double that of

Johannesburg. vii. The 5-year pattern in venture capital deals is also positive but rapidly developing

ecosystems elsewhere in sub-Saharan Africa have even faster momentum.

Cape Town boasts one of the most established and globally recognised ecosystems in Africa.0 Cape Town 9

Figure 3: Cape Town’s share of total African innovative companies and globally recognised companies

Share of African globally More established regionally

recognised innovative companies

30%

Lagos Greater

influence

25% worldwide

20%

Nairobi

15%

Cairo

Cape Town

10%

Johannesburg

5%

Accra

Kampala

0%

Share of African innovative

0% 2% 4% 6% 8% 10% 12% 14% 16% companies

Cape Town stands out for its urban tech environment. It ranks 1st among its global peers for its share of

start-ups specialised in sectors relating to urban technology, such as CivicTech, electric vehicles, smart

cities, and last mile transportation. This partly reflects the government’s tendency to use technology to

improve its systems and tackle urban challenges such as crime or water shortages. Cape Town is 6th

out of 15 Global South cities for the deployment of “smart city applications”, technological applications

based on data collection and analysis to streamline public services operations through better resource

allocation. And in terms of sensors and data-collecting devices, the effectiveness of digital

communication networks, and the presence of open data platforms, Cape Town ranks an impressive

3rd among cities in the Global Southviii. Examples include the deployment of sensors in water utilities,

electrical smart meters, and RFID tags on garbage cans to track real-time demand and improve basic

services delivery or the use of acoustic sensors to detect gun shots and alert the policeix.

In addition, Cape Town’s innovation ecosystem is now strongly specialised in financial services

(FinTech, InsurTech, digital payments), with more than 20% of tech-enabled companies operating in

these activities. Other niches include disruptive tech (Internet of Things, Machine Learning, Artificial

Intelligence) and retail tech. These sectors also receive the highest volumes of early-stage investment.

Although smaller, EdTech is a growing sector in Cape Town, fostered in part by Injini, an EdTech Open

Innovation Cluster. Other sectors in which Cape Town companies are hungry for innovation given

competitive pressures include logistics, oil and gas, and maritime - mostly located around the harbour -

and creative industries (film, fashion, animation) around the Woodstock Exchange which is Cape

Town’s flagship creative hang-out.

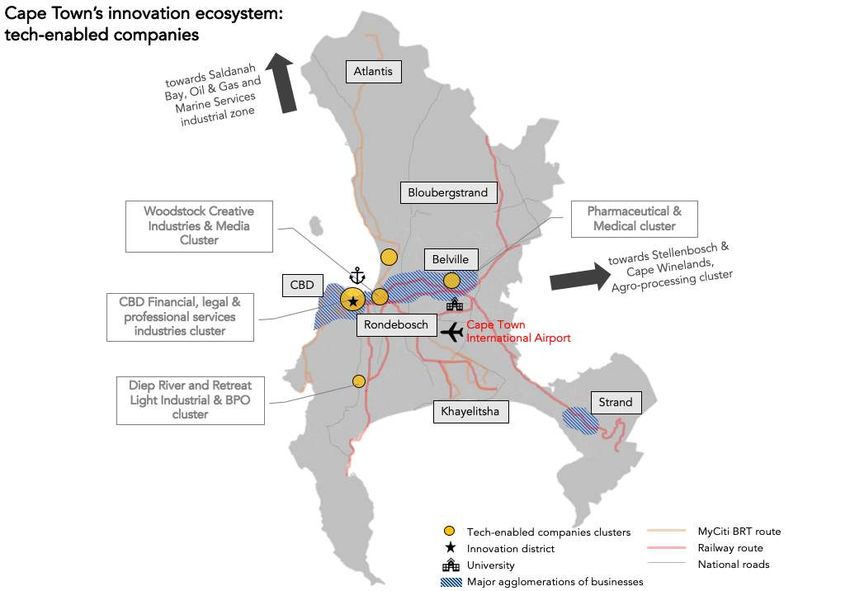

Cape Town’s innovation economy is concentrated along a 20km corridor of the N1 between the CBD

and Belville in the East. These two districts have the highest job densities in the metropolitan region,

and form the two major clusters of customers and clients for innovation. Around 50% of registered

tech-enabled start-ups, scale-ups and established firms are located within 5km of CBD, and 40% are

within 2km, demonstrating the role that the metropolitan core has played over the last 10-15 years.

Locating there, start-ups and entrepreneurs benefit not only from proximity to global companies and

investors, and improved safety and urban fabric, but also better connectivity, as all railways and BRT

routes end in the CBD.0 Cape Town 10

Map 1: Tech-enabled Companies in Cape Town

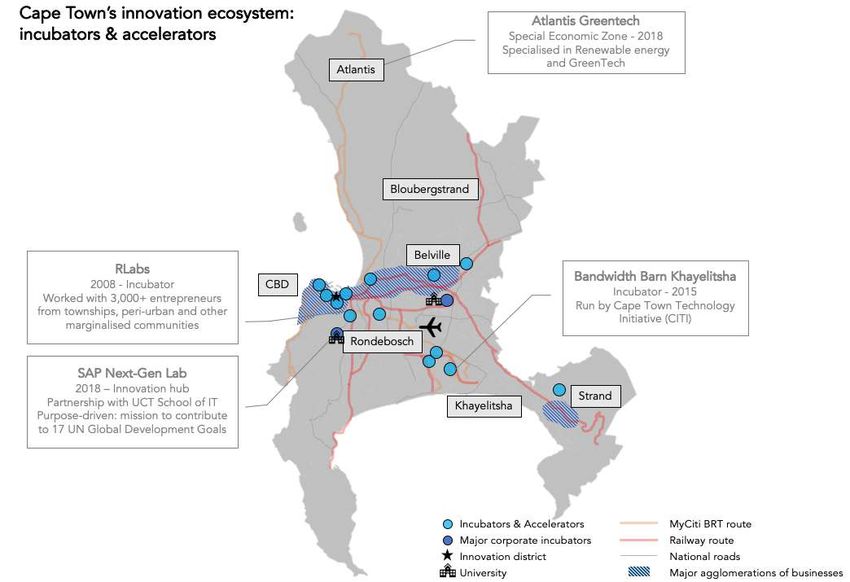

Incubators and accelerators are more evenly spread in the urban core, along major transport links, and

have also expanded more towards townships in recent years, as illustrated by the second branch of the

Bandwidth Barn in Khayelitsha, 30 km south east of the CBD. Clear efforts are visible to support

entrepreneurs from township and other marginalised communities.

Map 2: Incubators and Accelerators in Cape Town0 Cape Town 11

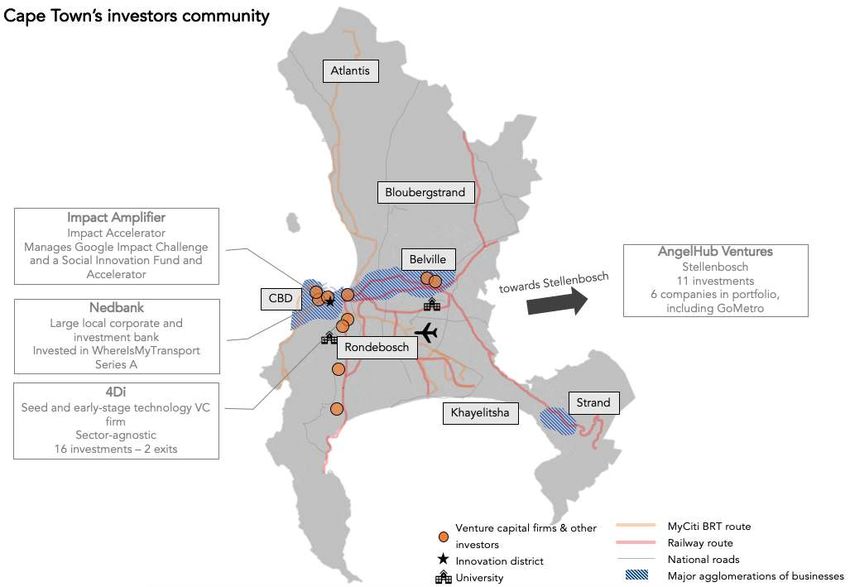

However, access to capital is a clear physical and opportunity barrier for aspiring start-ups at the

fringes - venture capital firms and other investors in Cape Town are very strongly located in the

western, affluent districts of the city. The investor landscape is also marked by a growing number of

impact investors, aiming to combine investment with social and environment impact. Many impact

investors present in Cape Town invest in community empowerment, focusing on informal settlements

and marginalised communities to tackle economic exclusion, by supporting entrepreneurship and job

creation.

Map 3: Investors Community in Cape Town

Outside Cape Town metropolitan municipality, the innovation ecosystem in Stellenbosch plays an

important role in the region - and contributes to the concept of “Silicon Cape”. With a proactive and

prestigious university, the University of Stellenbosch, major VC investors such as AngelHub Ventures,

and a booming start-up scene and liveability advantage, the neighbouring city also brings many

complementary capabilities to Cape Town’s innovation eco-system.0 Cape Town 12

Resilience in Informal

Settlements

With a density of 5,200 people per square kilometre, Cape Town is more dense than the average global

city, and is by far the densest city in South Africa, well ahead of Johannesburg and eThekwini (Durban).

Cape Town’s unusually high density by South African standards stems more from the very high density

levels in informal settlements, with sometimes more than 10,000 people per square kilometre

(significantly denser than the average for cities in the global South), than from the density of the city

centre and wealthy inner city and suburban areas. Many of Cape Town’s wealthiest suburbs have a

density of around 3,000 people / sq. km.

While dense compared to other South African cities, Cape Town is less dense than other global south

peers

Figure 4: Population density in Cape Town and global and Sub-Saharan peers.

People per sq.km

16,000

14,000

12,000

10,000

8,000

Global South average

6,000

World average

4,000

2,000

0

m s

ity

a

rg

am

Ba wn

bi

r g wn

da

ap bo

n

Sa i

ra

Xi v

ol n

e s no

o

vi

on

ja

e

ro

ha Acc

bu

Pa Lag

C

an

am

om

To

lA

e o To

la

id

Ha

el

ai

a

es

Lu

Ab

Te

rc

N

e

e

nn

na

C

C

ar

G

Jo

D

Source: Demographia World Urban Areas, 15th edition, April 2019

The main challenge arising from density is therefore a mismatch between the density of formal and

informal settlements, which in turn impacts upon equality of provision of basic services, including

electricity, water and sanitation. Over the years, Cape Town has been investing in improving its

informal settlements, and with about 97% of the population having access to electricity, Cape Town

now ranks 15th out of 40 cities in the Global South for the proportion of households hooked up to the

electricity grid. However, it is important to note that not all households are connected to the city’s grid

and many in informal settlements suffer from poor connection to such systems.0 Cape Town 13

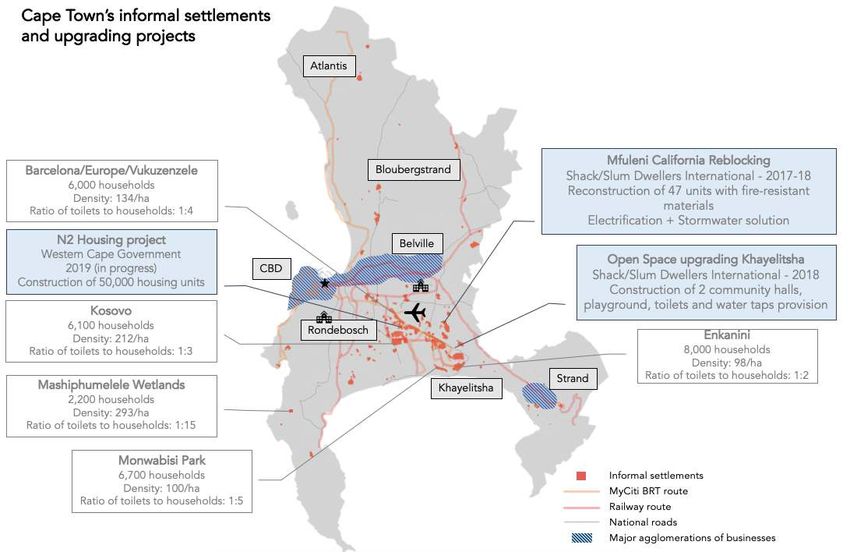

There are more than 175,000 informal settlements identified in the Cape Town metropolitan area.

They vary in size from a handful of households to communities of almost 8,000. The settlements are

spread across the city, including small “pockets” or backyard accommodation even in the wealthiest

parts of the city, but concentrate mostly along the south east corridor. Mitchell’s Plain and Khayelitsha,

the most densely populated informal settlements in Cape Town, are also some of the areas with the

lowest income. The absence of social and innovation infrastructure in these locations is a key priority

to the wider development path of the region.

Map 4: Informal Settlements and Upgrading Projects in Cape Town

Source: City of Cape Town. Data from 2015. Non-exhaustive map of current projects.

Approximately 7.5 million people (almost one-quarter of Cape Town residents) are locked out of the

formal property marketx. Due to the legacy of township planning and issues of economic exclusion,

many people can’t afford ‘well-located’, formal housing. As a result, they self-build.

Although highly creative and resourceful, the settlements present a range of issues due to the lack of

basic infrastructure, inadequate housing quality, personal dangers and environmental risks. Housing

might be located on land assigned for other purposes or on top of existing infrastructure. Backyard

dwellings, for example, a uniquely South African phenomenon, where informal shacks are erected in

the yards of other properties.

Settlements are serviced by unpaved roads and narrow paths, unnamed and without street lighting.

These forms of density make informal settlements difficult places to access in order to implement

appropriate services and infrastructure.0 Cape Town 14

Provision of basic services

Inaccessibility effects the provision of basic services such as chemical toilets or communal water

sources. Although 21% of Cape Town’s households are informal, they only received 1% of the City’s total

capital allocation for water and sanitation, according to social campaign group the Social Justice

Coalitionxi.

Peripheral placement makes access to basic services difficult for some inhabitants. The lack of access to

functional services increases the likelihood of violence to township inhabitants. For example, it was

found that between 2003 and 2012, an average of 635 sexual assaults on woman travelling to and from

an estimated 5,600 toilets in Khayelitsha township in Cape Town were reported each yearxii. Eleven

residents were murdered over a single weekend in 2017 in Marikana. Marikana being a notorious

dangerous and poorly lit settlement where police are reportedly not prepared to patrol after dark for

safety fearsxiii.

Health and Safety

Many informal settlements provide unsafe environments that are highly vulnerable to disasters and

extreme weather conditions due to the nature of building practices and materials. Dwellings in

informal settlements tend to be constructed using cheap, easily available but highly flammable and

conducting materials such as plastic, cardboard, iron sheets or untreated wood. This makes them

highly permeable to the elements and the spread of fire that devastates communities. In 2015 alone,

over 5,000 fires were reported in South African informal settlementsxiv. With limited access to

electricity, communities use paraffin for fuels and candles for lighting instead. Such practices lead to

issues of air pollution within settlements, as well compounding fire risks through the prevalence of

open flames.

Inaccessibility

The unplanned nature of developments and issues with density, impede the ability of both residents

and the city council to mitigate risks. Shacks could be built on top of, or obscuring, fire hydrants for

example. Formal fire trucks would struggle to access certain areas owing to the lack of wide, well-paved

roads. Thus, removing a much-needed emergency resource for the community. It was found that the

inaccessible narrow driveways and the absence of sufficient water supply in the Imizamo Yethu area

were main factors hampering efforts of fire fighters to tackle a large fire in the informal settlement in

2017. The fire killed four people, destroyed 2,194 dwellings and displaced over 9,700 inhabitantsxv.0 Cape Town 15

Who is doing what in the area and what are the opportunities?

The City of Cape Town Integrated Development Plan 2017 –2022 (IDP) has elements which seek to

address the challenges of inappropriate density. The IDP states how the City seeks to work with

communities to develop service delivery models for informal settlements, including sustainable

delivery of basic services such as electricity, water, sanitation and refuse removal, as well as services for

communal areas such as public spaces and recreational areas.

In order to achieve this the IDP seeks to:

• work with affected communities to explore and develop models of service delivery that are

appropriate to improve living conditions in informal contexts;

• commit resources to creating a sense of place and promoting security of tenure for residents

in less formal areas;

• improve the existing basket of basic services rendered to informal settlements by increasing

transversal management and service integration across City departments;

• explore resource-efficient and feasible solutions where current service delivery mechanisms are

not possible;

• continue to provide electricity, water, sanitation and refuse services to backyard dwellers in City-

owned rental stock or on City land; and

• explore models for the sustainable and compliant delivery of services to backyard residents on

private land.

Source: (Source: Five Year Integrated Development Plan, July 2017 – June 2022 – City of Cape Town.)xvi

As well as the City of Cape Town and the Western Cape government, NGOs and the

beneficiary communities, aim to transform marginalised areas and informal settlements into

more economically and socially integrated neighbourhoods through site-and-service

(expanding infrastructure and services provision), formalisation of backyard dwellings,

starter housing and in-situ upgrades of informal settlements. Other stakeholders include the

Shack/Slum Dwellers International (SDI) Alliance, which works on consolidation and

relocation of many informal settlements as well as their formalisation and reblocking. Table 2

(below) lists many of these key organisations.0 Cape Town 16

Case study: Empower

Shack

Empower Shack is a project by Urban Think Tank, an

international interdisciplinary design practice that focus

on social architecture and informal development. Their

Empower Shack project is bringing low-cost housing to

residents of Cape Towns’ informal settlements.

Source: https://www.dezeen.com/2014/03/07/empower-shack-urban-think-tank-housing-south-africa-slums/

Empower Shack aims to reshape the approach to informal settlement upgrading by offering an

urbanisation scheme that combines housing upgrades with a safer urban environment. The project

was first started in Khayelitsha, Cape Town’s second largest township in 2012. It has since built several

prototypes of alternative slum housing, demonstrating an adaptable method of designing safe and

accessible housing units within urban plans.

Empower Shack’s two-storey structures are arranged around a sanitation core, providing water and

toilets on site. The homes have a water-tight exterior and provide electricity. The designers are

exploring different configurations to adapt to the needs of different residents, extending up to three

storeys if necessary. Micro-financing schemes are also built into the planning tools, so residents can

take out small, ethical loans when building an Empower Shack or adding another storey.0 Cape Town 17

Source: https://www.dezeen.com/2014/03/07/empower-shack-urban-think-tank-housing-south-africa-slums/

The project is addressing several challenges of inappropriate density. The low-cost buildings occupy a

smaller portion of the usual slum dwelling footprint, leaving fire break spaces that give emergency

services easy access.

Urban Think Tank hope its project influences government housing policy offering diversity and access

to housing in South Africa’s gap market.

Table 2: Key players and Developments in the Area

Organisation Overview Website

International organisations

ICLEI – Local ICLEI – Local Governments for Sustainability is https://africa.iclei.org/

Governments for a global network of more than 1,750 local and

Sustainability regional governments committed to

sustainable urban development0 Cape Town 18

National organisations

Federation of the A women-led nationwide federation practicing https://www.sasdiallian

Urban and Rural Poor daily savings, enumeration, pragmatic ce.org.za/about/fedup/

(FEDUP) partnerships with the State. They are involved

in community-led housing development, land

acquisition and informal settlement upgrading.

The Informal ISN is a bottom up amalgamation of https://www.sasdiallian

Settlement Network settlement level and national level ce.org.za/about/isn/

(ISN) organisations of the urban poor. These

organized collectives engage leadership

structures at the settlement level, such as

crises and development committees and civic

organisations. They mobilize the community

around issue based community led

development planning.

Isandla Institute Isandla Institute promote and contribute to http://www.isandla.org.

systems and practices of urban governance. za/en/

They provide a voice on urban development

issues, producing research on issues such as

informal settlements upgrading and urban

governance.

Local organisations

Our Future Cities NPO An independent non-profit organization http://ourfuturecities.co

working across the fields of urban /

development which include housing, transport,

public space, sustainability and planning.

Development Action A non-Profit organisation supporting and https://www.dag.org.za/

Group advocating community led development

addressing economic, social and spatial

imbalances.

Ikhayalami Nonprofit Organization whose primary aim is to https://www.ikhayalami.

develop and implement affordable technical org/

solutions for informal settlement upgrading.

Ikhayalami’s areas of focus include: research

and development, upgrading of shelters,0 Cape Town 19

infrastructural development, community

facilities.

People’s PEP provides technical housing assistance to http://peoplesenvironm

Environmental the South African Homeless People’s entalplanning.org.za/

Planning (PEP) Federation and subsequently the Federation

of the Urban Poor (FEDUP).

Green Cape A non-profit organization that support https://www.greencape.

businesses and investors in the green co.za/

economy. They recently signed a

memorandum of understanding with Internet

Service Provider: ThinkWifi to deliver WiFi-

enabled solar street lights in informal

settlement Witsand.

https://www.itweb.co.za/content/Gb3Bw7W83

KAM2k6V

CORC CORC provides support to networks of informal https://www.sasdiallian

settlements around specific issues: land, ce.org.za/about/corc/

evictions, informal settlement upgrading, basic

services and citizenship; and savings

PDG Cape Town based consultancy involved in https://www.pdg.co.za/

urban systems, planning processes, survey

methodologies, data management tools,

decision-making frameworks, spatial analysis

tools, maturity models and infrastructure

investment plans

Social Justice Coalition Social justice campaign group. they are https://sjc.org.za/

involved in upgrading informal settlements0 Cape Town 20

Local projects

Urban Think Tank: Project focusing on the construction of living http://u-

Empower Shack environments: micro-financing, renewable tt.com/project/empowe

project energy, water management, and skills training. r-shack/

Including structured community workshops,

enumerations, affordability assessments and

microfinance contracts.0 Cape Town 21

ii Population and Economic Size data: JLL Global 650 (2018), data from 2017

Innovation Intensity: The Business of Cities analysis based on Crunchbase data, retrieved March 2019.

Sector Mix: Brookings Global Metro Monitor Data 2015

Transport Infrastructure Performance: IESE Cities in Motion Index 2019.

iv TomTom Traffic Index 2019

v Lall, Somik Vinay, J. Vernon Henderson, and Anthony J. Venables. 2017. “Africa’s Cities: Opening Doors to the World.” World Bank,

Washington, DC

vi McKinsey Urban World (2016) ; https://www.westerncape.gov.za/assets/departments/treasury/Documents/Socio-economic-

profiles/2017/city_of_cape_town_2017_socio-economic_profile_sep-lg_-_26_january_2018.pdf

vii OC&C Strategy (2018) Tech entrepreneurship ecosystem in South Africa

viii McKinsey Global Institute (2018) Smart Cities: Digital Solutions for a more livable future. Available at:

https://www.mckinsey.com/~/media/mckinsey/industries/capital%20projects%20and%20infrastructure/our%20insights/smart%20

cities%20digital%20solutions%20for%20a%20more%20livable%20future/mgi-smart-cities-full-report.ashx

ix https://iotsecuritywatch.com/en/2020/03/05/smart-city-cape-town-seeks-to-tackle-challenges-with-new-technologies/ ;

https://news.sap.com/2013/11/holistic-approach-of-sap-urban-matters-program-delivers-sustainability-results-for-cape-town/ ;

https://www.iol.co.za/news/south-africa/western-cape/city-of-cape-town-uses-new-tech-to-fight-vicious-gun-violence-17051231

x http://u-tt.com/project/empower-shack/

xi https://www.reuters.com/article/us-safrica-slums-sanitation/dying-for-a-pee-cape-towns-slum-residents-battle-for-sanitation-

idUSKCN12C1WA

xii https://www.reuters.com/article/us-safrica-slums-sanitation/dying-for-a-pee-cape-towns-slum-residents-battle-for-sanitation-

idUSKCN12C1WA

xiii https://sjc.org.za/wp-content/uploads/2018/09/sjc_annual_report_2017_2018.pdf

xiv https://www.researchgate.net/publication/286817204_Fire_risk_in_informal_settlements_in_cape_town_South_Africa

xv https://www.sciencedirect.com/science/article/abs/pii/S2212420918307623?via%3Dihub

xvi https://issuu.com/sixolilegade/docs/budget_2017-18_annexure_11_idp_new_0 Cape Town 22 Stuart Harper Stuart.harper@cp.catapult.org.uk Bob Burgoyne Bob.burgoyne@cp.catapult.org.uk Borane Gill boranegille@thebusinessofcities.com Visit our website cp.catapult.org.uk Follow us on Twitter @CPCatapult Email us info@cp.catapult.org.uk

You can also read