ENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING THE UK'S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Knowledge

Transfer

Network

Knowledge Transfer Networks

Accelerating business innovation:

Materials

a Technology Strategy Board programme

ENERGY MATERIALS: OPPORTUNITIES

AND CHALLENGES IN ATTAINING THE

UK’S 2020 TARGETS FOR NUCLEAR

ELECTRICITY GENERATION

www.materialsktn.net

AUTHOR Dr Kathryn P Jackson National Metals Technology Centre Ltd (NAMTEC) DISCLAIMER The views and judgements expressed in this report reflect the consensus reached by the author and contributors and do not necessarily reflect those of the organisation to which they are affiliated. Whilst every care has been taken in compiling the information in this report, neither NAMTEC nor the Materials KTN can be held responsible for any errors, omission or subsequent use of this information. FURTHER INFORMATION Please contact: Materials KTN Metals and Alloys Group National Metals Technology Centre Ltd (NAMTEC) University of Sheffield Advanced Manufacturing Research Centre Wallis Way Catcliffe Rotherham S60 5TZ T +44(0)114 222 1747 E info@namtec.co.uk

ENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

EXECUTIVE SUMMARY

Nuclear energy will have a significant role to seven threats have been identified: uncertainty

play in the UK’s future energy mix, providing in the economic climate; engagement of Tier 1

a zero-carbon base load alongside a mixture suppliers; supply of ultra large forgings; global

of renewables and low-carbon fossil fuel competition; manufacturing capabilities; culture

sources. The UK’s ambitions for nuclear of quality; and shortage of skills and loss of

energy in 2020 offer significant challenges knowledge. Overall, the UK is regarded as

and opportunities for UK manufacturing strong in terms of manufacturing capabilities,

industry; ambitious timescales for new builds

with some improvement in capacities required

will be progressed to replace existing fleet

in some areas.

which is close to decommissioning, which

will be followed by further expansion to Opportunities to alleviate these threats include

increase the UK’s nuclear capacity. The aim engagement with nuclear OEMs, development

of this Materials KTN review is to highlight the of the UK’s capacity for ultra large forgings,

opportunities and challenges for materials and support for Tier 2 to 4 suppliers, and training

manufacturing arising from the UK’s nuclear and skills. Knowledge transfer with other

new build programme in three areas: supply high value manufacturing sectors such as

of raw materials; manufacturing supply chain; oil and gas, aerospace and fossil fuel power

and operations and maintenance. This review generation will help the UK to develop

has been derived from a combination of a its capabilities and quality of culture in

stakeholder consultation and literature survey.

preparation for penetrating the market for

Four areas of potential risk arising from the nuclear new build.

supply of raw materials have been identified:

In the area of operations and maintenance,

availability of speciality alloying elements;

the UK has established capabilities for

availability of certain grades of stainless

operating and maintaining nuclear plant

steels; the impact of REACH regulations;

and maintaining the traceability of supply of developed through the UK’s civil nuclear

materials across the supply chain. The risk legacy. Challenges to the operations and

of supply of speciality alloying elements is maintenance of new build plant include limited

regarded to be low, whilst the availability of access to data and knowledge sharing on

down-stream materials is of greater concern materials for PWRs, and loss of knowledge

to the nuclear industry. through aging of personnel.

Opportunities for innovation to mitigate these Opportunities to mitigate these risks include

risks include consolidation of production of engagement with international knowledge-

specialised steel grades to mitigate supply sharing programmes, knowledge retention

chain bottlenecks and improve quality control, and storage, and development of condition

retention of scarce materials by closed-loop based monitoring. Knowledge transfer with the

recycling, and quality control of the supply aerospace and fossil fuel power generation

chain by monitoring and training. sectors will help to develop approaches to

In the area of the manufacturing supply chain, operations and maintenance.

www.materialsktn.net 3

ENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

ACKNOWLEDGEMENTS

This report has been written by the Materials

KTN Metals and Alloys Group in co-ordination

with the Materials UK Energy Materials Working

Group (EMWG). The author would like to

express her gratitude to the EMWG alongside

all other contributors to the stakeholder

consultation for their input to the report. The

contributors are listed below.

Steve Court Nuclear AMRC

David Hall Nuclear AMRC

Martin Ride Nuclear AMRC

Rob Mitchell Rolls-Royce plc

Juan Matthews UKTI

Chris Savage Nuclear Industry

Association (NIA)

Michael Burke Dalton Nuclear

Institute

4 www.materialsktn.net

ENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

CONTENTS

1 Introduction 7

1.1 Trends in the UK Nuclear Energy Landscape 8

1.2 Technology Overview 11

2 Supply of Raw Materials 16

2.1 Threats to Supply of Raw Materials 17

2.2 Opportunities to Alleviate Threats to Supply of Raw Materials 19

3 Manufacturing Supply Chain 21

3.1 Threats to Manufacturing Supply Chain 22

3.2 Opportunities to Alleviate Threats to Manufacturing Supply Chain 30

4 Operations and Maintenance 35

4.1 Threats to Operations and Maintenance 36

4.2 Opportunities to Alleviate Threats to Operations and Maintenance 38

5 Conclusions and Recommendations 41

References 44

www.materialsktn.net 5

ENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

ENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

1 INTRODUCTION

Nuclear power generation will have a Written by the Materials KTN in co-ordination with the

significant role to play in the UK’s energy Materials UK Energy Materials Working Group (EMWG),

the aim of this review is to provide a fresh perspective

mix in 2020 and beyond, providing a zero

on the threats and opportunities for the UK’s 2020

carbon base load to supplement a variety

nuclear targets, focussing specifically on materials

of renewable and low-carbon fossil fuel aspects. The review is based primarily on stakeholder

energy sources. The UK’s existing nuclear consultation, the contributors to which are listed in the

capacity of around 10GW is predicted Acknowledgements, with references to supporting

to be mostly be decommissioned by literature made throughout the text wherever possible.

2020, meaning that the initial focus of This review will build on the findings of previous

the nuclear new build programme is reviews of the manufacturing supply chain for nuclear.

to replace the existing capacity before The UK’s capability to deliver a new nuclear build

expanding capacity. This section outlines programme was reviewed by the Nuclear Industry

Association (NIA) in 2006 [1] and updated in 2008

the trends in the UK’s nuclear energy

[2]. The review gave a detailed evaluation of the

landscape towards 2020 which are driving

UK’s capability to deliver both the AREVA EPR and

the need for development in materials and Westinghouse AP1000 designs. A new issue of

manufacturing. the report is currently under review and is due to be

released later this year. The supply chain for a nuclear

new build programme was also reviewed by NAMTEC

in 2008 [3], which reviewed both the capability

and capacity of supply chains including aspects of

planning, construction, operation, maintenance, waste

management, and decommissioning of a nuclear

power station.

As part of the introduction, the trends in the UK’s

nuclear energy landscape are outlined in section 1.1.

The technology of future nuclear plant in the UK is

summarised in section 1.2, with the two major plant

designs (Westinghouse AP1000 and AREVA EPR)

considered in sections 1.2.1 and 1.2.2 respectively.

Opportunities and challenges arising from the supply

of raw materials, the manufacturing supply chain and

operations and maintenance are reviewed in sections

2, 3 and 4 respectively. Each section highlights the

threats arising in each of the areas and opportunities

to alleviate these threats through innovation and

knowledge transfer.

Conclusions and recommendations are given in

section 5. References are listed at the end of the

report, with hyperlinks to the original online sources

where possible.

www.materialsktn.net 1

ENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

1.1 TRENDS IN THE UK NUCLEAR ENERGY and widely regarded as safe; control of radioactive

LANDSCAPE waste is well understood and control systems and

structures are designed to fail-safe and minimise

The UK currently has ten operational nuclear power risk. Concerns over safety which were raised by the

stations, ranging in capacity from 434 to 1210 MW, Fukushima disaster in 2011 were investigated and

with a total installed capacity of around 10 GW (Table found to have no serious implications on the UK’s

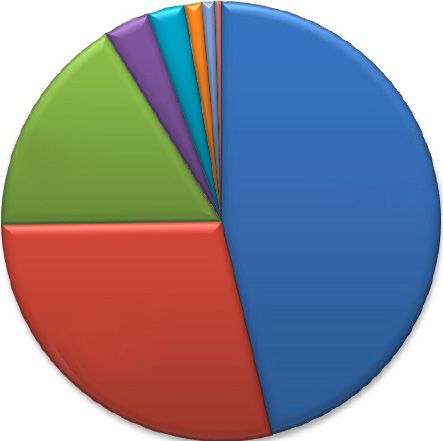

1). Nuclear provided 16% of the UK’s electricity plans for a nuclear new build programme [4]. It is

supply in 2010, the third largest contributor to the for these reasons that nuclear power will continue to

energy mix (Table 2, Figure 1). Nuclear energy has make a significant contribution to the UK’s energy

the advantages of being zero-carbon, economically mix for the foreseeable future, helping the UK to

competitive, and producing a steady and controllable achieve its carbon emissions targets whilst ensuring

base-load of supply. The technologies involved that supply continues to meet demand and mitigating

in nuclear power generation are well-established future price increases of electricity.

2 www.materialsktn.net

ENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

Year of

Installed commission or Cease

Operator Plant Reactor type

Capacity (MW) year operation generation

began

Dungeness B 1040 1983 2018 AGR

Hartlepool 1190 1984 2019 AGR

Heysham 1 1160 1984 2019 AGR

Heysham 2 1210 1988 2023 AGR

Hinkley Point B 870 1976 2016 AGR

British Energy

Sizewell B 1191 1995 2035 PWR

Hunterston B 890 1976 2016 AGR

Torness 1205 1988 2023 AGR

Oldbury 434 1967 2012 Magnox

Wylfa 980 1971 2012 Magnox

Total installed 10170

capacity (MW)

Table 1

Nuclear power stations

in the UK operational at

the end of May 2011 [5].

Cease dates from [6-7].

Primary and Secondary

GWh Percentage

Production

Gas 175,003 46

Coal 107,694 28

Nuclear 62,140 16

Other renewables 12,837 3

Wind 10,216 3

Oil 4,860 1

Hydro 3,603 1

Other 1,625 0

Total production 377,977

Table 2

Primary and secondary

production of electricity

in the UK in 2010 [5]

www.materialsktn.net 3ENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

UK Primary Electricity Production 2010, GWh

3,603

4,860

1,625

10,216

12,837

Gas

Coal

Nuclear

62,140 Other renewables

Wind

175,003 Oil

Hydro

Other

107,694

Figure 1

Primary and secondary production of

electricity in the UK in 2010 [5]

Seven of the ten nuclear power stations which are sources, possible scenarios for the future energy

currently operational in the UK are due to cease mix have been put forwards by the National Grid [8],

operation by 2020 (Table 1). The UK has steadily which predicted that the UK’s capacity for nuclear

reduced its nuclear capacity over the last two in 2020 could be between approximately 5 and 10

decades, with most of the older Magnox reactors GW, depending on the rate of growth of the various

reaching the end of their lives. The initial objectives for energy generation methods. In 2011 the Government

the nuclear new build programme to 2020 and beyond suggested that by 2030 new nuclear could contribute

are therefore to replace the UK’s existing capacity 10–15 GW, with up to 20 GW achievable if build rates

for nuclear. However, it is possible that the operation are higher [9]. Industry has announced ambitions

of the existing fleet may be safely extended for a to build 16 GW by 2025, and if one reactor could be

limited period of time to supplement supply whilst the completed each year from 2019 onwards, it would

new fleet is built. This will be dictated by materials be possible to reach around 20 GW by 2030 [9]. The

degradation issues, and hence understanding of total new build programme is predicted to consist of

materials will be essential to underpin any possible approximately 8 plants, with the first one likely to be

lifetime extension. Hinkley Point C (3,260 MW output) operated by EdF

The UK government is committed to a low-carbon Energy, which is currently the subject of a nuclear site

economy and transitions in the UK energy mix will licence application [10] due for completion before

make a significant contribution to this. The UK is the end of 2012. EdF will not give a target date for

setting a leading example for low-carbon energy generation until after it has made its final investment

generation by supporting innovation and development decision [11], but this is likely to be set a few years

of skills in energy technology which have the potential behind its previously stated date 2017. Electricity

to be a major facilitator of economic growth in the generated by nuclear is currently cost-competitive with

immediate term, whilst providing a sustainable, other electricity generation technologies, and recent

affordable and low-carbon energy supply in the longer independent studies indicate that new nuclear is likely

term. The coming decades will be an exciting and to become the least expensive generation technology

dynamic time for the UK’s energy industry, with the in the future [9].

low carbon transition mainly facilitated through rapid

Despite the UK’s clear commitment towards a nuclear

growth in offshore wind, carbon capture and storage

new build programme, progress has been hampered

and new nuclear.

by economic uncertainty and the Fukushima disaster.

Although the UK government has not defined targets Plans for the second plant at Wylfa in Anglesey had

for the UK’s future energy mix with the aim of leaving been expected to be submitted by Horizon Nuclear

the market open for competition from different energy power (joint venture of E.ON UK and RWEnpower).

4 www.materialsktn.netENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

However, in March 2012 Horizon withdrew its plans for 1.2 TECHNOLOGY OVERVIEW

nuclear new build at Wylfa due to uncertain economic

conditions and the accelerated nuclear phase out Two designs have passed generic design assessment

in Germany [12]. As a result, plans for nuclear new (GDA) in the UK and therefore can be used for

build in the UK have been delayed from the 15-year the UK’s new nuclear fleet: the Westinghouse

timelines that were initially projected in 2010, and AP1000 (1154 MWe) [13] and the AREVA European

a revised timeline of development is impossible to Pressurised Reactor (EPR) (>1650 MWe) [14].

predict with any certainty at this stage. The delays Both designs are Generation III+ pressurised

have placed additional pressure on the timescales for water reactors (PWRs) and are based on similar

completion and commissioning of the new nuclear technologies and materials. However, there are

plants, and extended safe operation of aging fleet may some fundamental differences in the designs which

be necessary to support the early build phases of the will have implications on the required capabilities of

new nuclear fleet. the supply chain, the manufacturing processes and

the method of construction. The technologies of

these two designs and the key issues related to their

manufacturing are summarised in this section.

Figure 2

Basic principle of operation of a pressurised

water reactor (PWR) based on [5]

Steam Generator

Pressurised

water reactor Steam

Control

rods

Turbine

Reactor

core Generator Electricity

Water

Condensor

Hot water

Containment Structure

www.materialsktn.net 5ENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

The basic principle of operation of a PWR is illustrated etc, and hence increases construction costs

in Figure 2. In a PWR the primary coolant (water) and complexity. The reactor pressure vessel is

is pumped under high pressure to the reactor core manufactured from ductile steel but as the plant is

where it is heated by the energy generated by the operated neutron flux from the reactor causes this

fission of atoms. The heated water then flows to a steel to become less ductile (radiation embrittlement).

steam generator where it transfers its thermal energy Eventually the ductility of the steel will reach limits

to a secondary system through a large number of determined by the applicable boiler and pressure

narrow tubes which act as a heat exchanger. This vessel standards, and the pressure vessel must be

generates steam in the secondary circuit which repaired or replaced. This might not be practical or

turns a steam turbine which, in turn, spins an electric economic, and so determines the life of the plant.

generator. After passing through the turbine the A further risk associated with PWRs is the need for

secondary coolant (water-steam mixture) is cooled ongoing cooling for one to three years after shut

down and condensed in a condenser before being down to avoid overheating and meltdown. If the

pumped back to the steam generator as feedwater, primary coolant is lost (as in the Fukushima disaster

prior to which it is sometimes preheated to minimise in 2011) the zirconium alloy used for casing the

thermal shock. The condenser maintains a vacuum nuclear fuel rods can reach very high temperatures

at the turbine outlet so that the pressure drop across (above 2200oC), at which it spontaneously explodes

the turbine, and hence the energy extracted from the in contact with water, producing hydrogen and oxygen

steam, is maximised. and therefore hydrogen explosions.

PWRs constitute the majority of all western nuclear power

plants and are favoured for the following reasons:

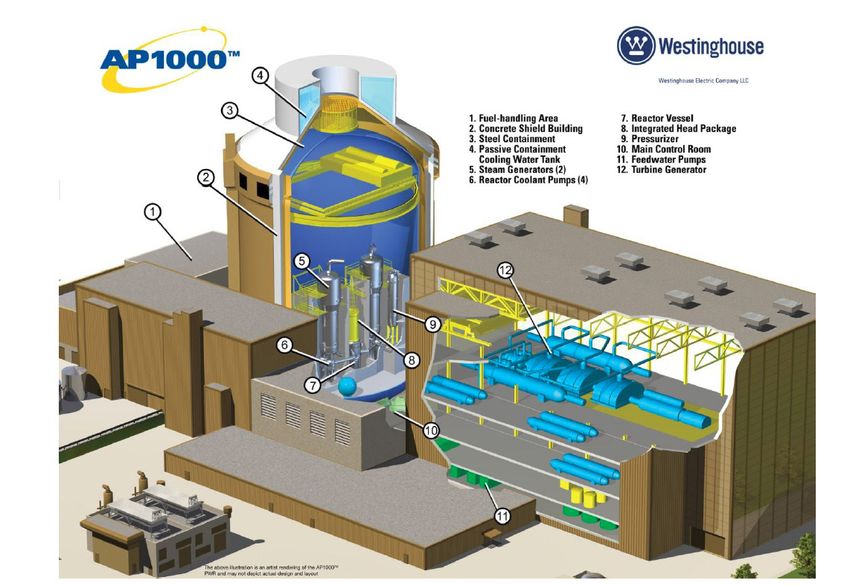

1.2.1 Westinghouse AP1000

|| The primary and secondary steam circuits are

separated, and hence the transfer of radioactivity The Westinghouse AP1000 is the only Generation

from the reactor core to the steam turbine is III+ reactor to receive Design Certification from

mitigated the U.S. Nuclear Regulatory Commission (NRC)

[13]. Around half of the world’s 440 nuclear plants

|| PWRs are inherently stable and therefore safer

are based on Westinghouse technology. The

than other designs because they produce

Westinghouse design is rated at 1154MW, slightly

less power as temperatures increase because

smaller than the APR at >1650 MWe, which

pressurised water is used as the moderator and

allows for modular construction (Figure 3). Safety

primary coolant

systems unique to the AP1000 include the passive

|| PWRs operate with a fail-safe design because containment cooling water tank held above the

in the event that power is lost the control rods reactor core for release in an emergency (4 on Figure

drop by gravity because they are held by 3) and the steel containment vessel which surrounds

electromagnets, and therefore shut down the the nuclear island (3 on Figure 3).

primary nuclear reaction Westinghouse achieved significant improvements

Whilst the design of the PWR offers a range of in the number of components, volume of materials

advantages in terms of safety and operation, this and construction time of the AP1000 in comparison

is accompanied by materials challenges. The high to earlier Westinghouse designs. The construction

pressure of the primary coolant water requires high period is approximately 36 months from the pouring of

strength piping, a heavy pressure vessel, reactor the first concrete to the loading of fuel. Savings in the

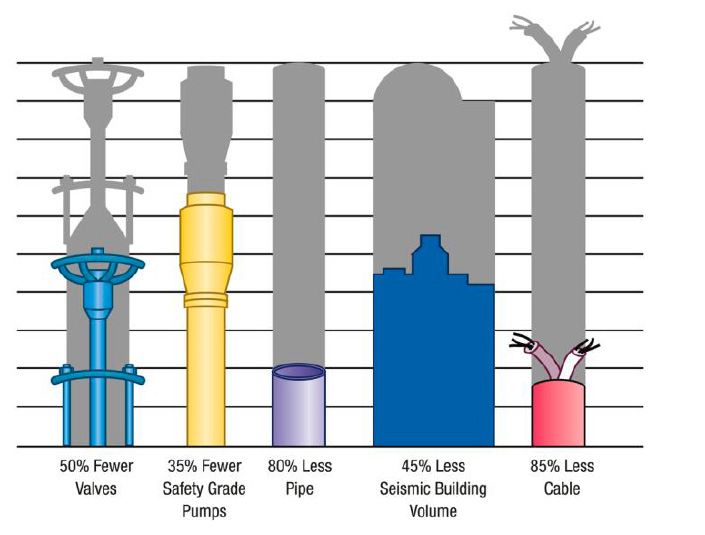

coolant pumps, pressuriser, steam generators, materials and construction are illustrated in Figure 4.

6 www.materialsktn.netENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

1. Fuel-handling Area 7. Reactor Vessel

2. Concrete Shield Building 8. Integrated Head Package

3. Steel Containment 9. Pressuriser

4. Passive Containment Cooling 10. Main Control Room

Water Tank 11. Feedwater Pumps

5. Steam Geneartors (2) 12. Turbine Genearator

6. Reactor Coolant Pumps (4)

Figure 3

Sectional 3D view of Westinghouse

AP1000 [16]. Image courtesy of

Westinghouse Electric Company

Figure 4

Savings in the materials and

construction of the Westinghouse

AP1000 [16]. Image courtesy of

Westinghouse Electric Company

50% Fewer 35% Fewer 80% Less 45% Less 85% Less

Valves Safety Grade Pipe Seismic Building Cable

Pumps Volume

7ENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

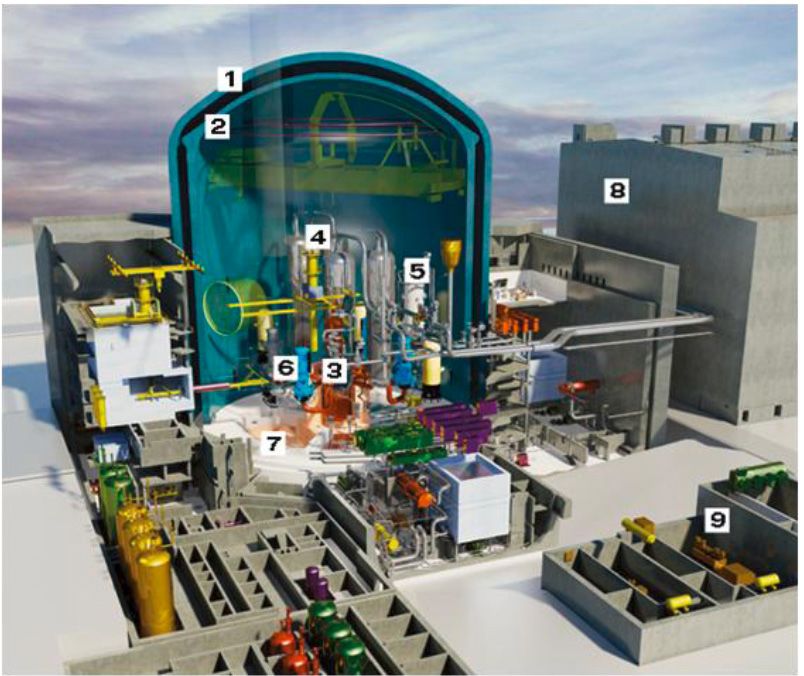

1.2.2 AREVA EPR

The AREVA European Pressurised Reactor (EPR)

(Figure 5) is the first Generation III+ reactor to be

deployed on an international scale, being built in

three different countries. The EPR is rated at a higher

capacity than the Westinghouse AP1000 at around

1650 MWe. The method of construction of the EPR is

therefore more strongly focussed on assembly on site

rather than modular construction off site. The EPR is

currently under construction in Finland (Olkiluoto), in

France (Flamanville) and in China (2 units in Taishan),

and is currently undergoing certification in the United

States and the UK [14]. EdF has applied for a nuclear

site licence for the AREVA EPR at Hinkley Point C,

and hence the EPR is likely to be the first Generation

III+ reactor built as part of the nuclear new build

programme in the UK.

Figure 5

Sectional 3D view of the AREVA

EPR [17]. Courtesy of AREVA.

© Image et Process – AREVA

1: Reactor building reinforced

concrete shell

2: Reactor building metallic liner

3: Reactor vessel

4: Steam generators

5: Pressuriser

6: Reactor coolant pumps

7: Corium spreading area

8: Turbine building

9: Diesel generators

8 www.materialsktn.netENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

2 SUPPLY OF

RAW MATERIALS

A wide range of materials will be used in 2.1 THREATS TO SUPPLY OF RAW MATERIALS

the UK’s new nuclear fleet. Beyond the Threats to the supply of raw materials for the UK’s

vast quantities of concrete used in the 2020 nuclear targets are reviewed in this section.

construction of the plant, the majority Four areas for potential threats are discussed below:

of materials will be steels, with coatings the availability of speciality alloying elements; the

used to enhance performance where availability of specific grades of stainless steel; the

necessary. Four areas of potential threats impact of REACH regulations; and maintaining the

traceability of materials through the supply chain.

in the supply of raw materials have been

identified: availability of speciality alloying 2.1.1 Availability of Speciality Alloying Elements

elements; availability of certain grades The availability of raw materials that constitute the

of stainless steel; the impact of REACH alloys used in nuclear plant has previously been

regulations; and maintaining traceability investigated by Oakdene Hollins on behalf of the JRC

of supply of materials through the European Commission in 2011 [18]. A total of 21

supply chain. Opportunities to alleviate speciality metals were identified used in a variety of

components in nuclear reactors. The starting point for

these threats include consolidation of

this review was to ascertain through the stakeholder

production of specialised steel grades, consultation whether any of these risks associated

retention of scarce materials through with the availability of speciality alloying elements are

closed-loop recycling; and quality control perceived to be a threat to the nuclear industry.

of the supply chain. These threats and The consensus of opinion obtained through the

opportunities are discussed below. consultation was that, although constraints in the

availability of these materials caused by economic

or political factors may cause increases in the prices

of these materials, these price increases can be

accommodated by the nuclear industry. Application

of alternative compositions of materials is generally

regarded as not an option for the safety-conscious

nuclear industry in which confidence in designs is

developed through lengthy testing of known materials;

the risks associated with substitution of materials

outweigh the cost increases associated with the

continued use of materials with constrained supply.

The levels of risk that have previously been associated

with the availability of raw materials are further

mitigated by decreases in demand in comparison

to earlier projections, which is likely to be a result

of constrained economic growth and the curtailing

of nuclear plans in several countries following the

Fukushima disaster. This suggests that demands

are not currently causing shortages or lead time

lengthening. However, if economic demand continues

www.materialsktn.net 9ENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

to be weak this may lead to some reductions in the quantities of certain specialised grades required

output, which could subsequently lead to price by individual manufacturers may not be enough to

increases. constitute a full melt (around 500 t) in themselves,

Where availability of raw materials could be perceived and therefore bottlenecks in supply may occur; (3)

as a risk for other industries, the nuclear industry is older grades that have largely been superseded by

in a strong position of influence to secure supply due newer grades elsewhere may still be used in some

to its large market size, ability to absorb increases in areas by the conservative nuclear industry where

cost, and its demand for primary products as well as tried-and-tested materials are not always substituted

by-products of extraction. For example, the largest by alternatives, hence leading to bottlenecks in supply

use of zirconium is in the nuclear industry for fuel (e.g. 304 has largely been superseded by 316 which

cladding due to its low neutron absorption coefficient, has superior corrosion resistance).

whilst a by-product of zirconium production is 2.1.3 Impact of REACH Regulations

hafnium which is also used extensively in the

nuclear industry due to its high neutron absorption The impact of REACH regulations is regarded

coefficient for nuclear shielding applications. Hence as a risk affecting the use and supply of raw

continued demand for zirconium helps to sustain materials for the nuclear industry. The introduction

the supply of hafnium, whilst the supply of both is of REACH regulations in Europe necessitates the

largely concentrated in the countries which have the rapid development and introduction of alternative

strongest nuclear programmes. materials or manufacturing processes which meet the

required safety and environmental standards, offering

2.1.2 Availability of Grades of Stainless Steels

opportunities for innovation across the manufacturing

Availability of certain grades of stainless steels supply chain. However, the rapid implementation of

was highlighted as a potential threat through the changes is at odds with the conservative and risk-

stakeholder consultation. The majority of steels aware nuclear industry, in which tried and tested

that are used in nuclear power stations are nuclear materials and processes are preferred to minimise

grades of low alloy steels (with limits on the content risk. An example of this is electroplating of cobalt in

of Cu, Ni, S and P due to radiation embrittlement). valves and pumps which may be replaced with vapour

More specialised grades that are used in nuclear deposition as a result of REACH regulations.

power stations include SA508 and SA533 (plate and

forgings for shelves, heads, bodies, primary pipework, 2.1.4 Maintaining Traceability of Supply of Materials

reactor pressure vessel (RPV), pumps and steam across the Supply Chain

generator), austenitic stainless grades 316 (used for A threat to the nuclear industry that has been

weld overlay cladding, typically 6mm thickness) and reiterated across other power generation sectors is

304, martensitic stainless grades 403, 410, 416 (pump the propensity for sub-standard materials to enter

shafts, turbine blades) and martensitic precipitation the supply chain, either as a result of deliberate

hardening grades 600 and 690 (steam generator counterfeiting or inadequate knowledge of quality

tubes, exchanger tubing, pressuriser). control procedures amongst suppliers. The threat

Three reasons have been highlighted why the is particularly acute for safety-critical components

availability of the above grades of steel for the UK’s such as high pressure and temperature steam supply

nuclear new build programme could be compromised: systems. OEMs generally have less control over

(1) demand from the UK may compete with growing the lower tiers of the supply chain, and materials

demand from other countries which simultaneously that originate from China or India are recognised as

execute ambitious nuclear new build programmes; (2) particularly strong risks.

10 www.materialsktn.netENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

2.2 OPPORTUNITIES TO ALLEVIATE THREATS TO have been highlighted for offshore wind [19] and

SUPPLY OF RAW MATERIALS combined cycle gas turbine power generation [20].

For example, improved retention of chromium,

Three opportunities to alleviate threats to the supply of molybdenum, vanadium and nickel through closed-

raw materials have been identified: (1) consolidation loop recycling of steels from a range of applications

of production of specialised steel grades; (2) retention could help to mitigate price increases and maintain

of scarce materials through closed-loop recycling; availability into the future. Note that closed loop

and (3) quality control of the supply chain. These recycling from the nuclear industry itself is unlikely to

areas are discussed below. be able to contribute to this due to the low number

2.2.1 Demand Aggregation of Specialised Steel Grades and long lifetime of nuclear plants, the need for careful

processing of radioactive waste, and the variety of

There is the potential to improve control over the designs that have been used in the UK’s nuclear

quality of raw materials and mitigate bottlenecks in legacy.

supply by consolidating the bill of materials to enable

the material for several components to be produced 2.2.3 Quality Control of the Supply Chain

in a single melt from a single known supplier, where Control of quality in the supply chain is an opportunity

the quality and composition are closely monitored. to alleviate risk arising from the supply of raw

Whilst diversity of suppliers for steel is desirable materials. The supply chain is already acutely aware

to reduce cost through open competition, it is of the need to monitor and control quality to prevent

possible that consolidation of requirements of some the infiltration of sub-standard or counterfeit material,

specialised grades for safety-critical applications which is particularly concerning for safety-critical

could help to control quality whilst also ensuring that and high integrity components such as the nuclear

bottlenecks in supply are mitigated by increasing the steam supply system (NSS) and secondary steam

total volume of material required from a single melt. circuit. The higher tiers of the supply chain already

This would require co-ordination across the supply take a pro-active approach towards monitoring and

chain to allow the materials requirements for a range improving quality from their suppliers, which includes

of components fabricated by a range of suppliers spot checks on material compositions alongside

to be brought together. Sourcing of materials for training of quality procedures to improve the skills of

components is currently carried out by a large number their suppliers. This approach is effective although it

of companies across the supply chain to meet their places additional demands on resources from top-tier

individual requirements and commercial sensitivity manufacturing companies, which are likely to become

restricts communication between these various facets increasingly challenged over the coming decade

of the supply chain. Hence consolidation of the as the nuclear supply chain expands. Ensuring the

bill of materials across the supply chain could be a availability of suitably skilled and qualified quality

challenge without the assistance of OEMs at the top engineers will help to alleviate this risk.

level.

2.2.2 Retention of Scarce Materials through Closed-

Loop Recycling

Whilst the availability of speciality alloying elements

is not considered to be a significant risk for the UK’s

2020 nuclear targets, the availability of materials

in the long term could be improved by retention

through closed-loop recycling. Similar opportunities

www.materialsktn.net 11ENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

3 MANUFACTURING

SUPPLY CHAIN

Manufacturing of components and sub- 3.1 THREATS TO MANUFACTURING

assemblies for the UK’s nuclear new SUPPLY CHAIN

build programme offers considerable The manufacturing supply chain for nuclear can

opportunities and challenges for the UK’s be categorised into at least four tiers: Tier 1 –

manufacturing industry. Seven areas of technology suppliers and architect engineers; Tier

potential threats have been identified: 2 – large companies with nuclear experience; Tier

3 – smaller mechanical or electrical equipment

uncertainty in the economic climate;

suppliers and niche service providers; and Tier 4

engagement of Tier 1 suppliers; supply of – raw material or basic component suppliers. The

ultra large forgings; global competition; origin of this hierarchy is the licensees, e.g. EdF

manufacturing capabilities; culture of Energy. Vendor companies such as AREVA and

quality; and availability of skills. Four Westinghouse are focused on design, engineering

opportunities to alleviate these threats and project management. In general, the number of

have been identified: engagement with companies at each tier and hence the propensity for

competition in the market place and diversification

nuclear OEMs; development of the

in manufacturing methods increases as the level of

UK’s capacity for ultra large forgings; the tiers increases (Figure 6). The supply chain for

support for Tier 2, 3 and 4 suppliers; nuclear is global, and hence UK companies that

and training and skills. These threats participate in the nuclear industry are competing on

and opportunities are discussed in this an international level.

section.

Figure 6

Nuclear new build market •EDF Energy/Centrica

structure. Based on a diagram •Horizon Nuclear Power

by Doosan Babcock in [21] Licensees •NuGeneration Ltd

•Nuclear Power Delivery UK

Tier 1 -

•Westinghouse

Technology •Toshiba

Suppliers, Architect •Shaw Group

Engineers •Laing O’Rourke

Tier 2 - •Civil Enabling Works

•Main Civil Contractors

Large Companies with

•Marine Works

Nuclear Experience •Infrastructure Works

•Mechanical Equipment Suppliers

Tier 3 -

•Electrical Equipment Suppliers

Smaller Mechanical or Electrical •EC&I Installation Companies

Equipment Suppliers, Niche Service Providers •Mechanical Installation Companies

Tier 4

12 www.materialsktn.netENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

Supply chain challenges are different for This was in spite of a clear commitment towards

Westinghouse and AREVA due to the sizes of the nuclear new build from the UK Government; it was

plants, the way that they are constructed, and economic rather than political factors that were the

their strategic plans for supply chain development. major influence on Horizon’s decision.

Westinghouse hopes to source everything locally

The consensus of opinion across the manufacturing

from the UK, which will present opportunities but

supply chain is that there is a need to develop their

place pressure on suppliers. The Westinghouse

knowledge and capabilities in preparation for a

AP1000 is smaller than the AREVA EPR at 1154 MW,

nuclear new build programme now, but investment to

and therefore can use modular construction. This

expand capacities is expensive and therefore will not

means that large sub-assemblies can be assembled

take place to its full extent until the market is at a more

off site, e.g. in shipyards, and there are significant

advanced state of readiness. In the first instance,

opportunities for plate materials, pipes and joists for

this will be after EdF Energy has achieved its nuclear

skid-mounted modules. UK shipyards are already

site license for Hinkley Point C and civil engineering

preparing to address this need through international

works are underway. The timing of investment poses

consortiums. In contrast, AREVA reactors are much

a challenge for UK companies in comparison to

larger (1500MW) and therefore must be fabricated

companies in other countries which already have

onsite. There is less opportunity for modular

large capacities and established track records in the

construction, but significant opportunities in terms

of pumps and pipework for the turbine island. The nuclear supply chain; UK companies need to develop

rapid expansion and upskilling required for nuclear the capabilities and capacities to manufacture

new build from both AREVA and Westinghouse for nuclear in enough time to win business whilst

will necessitate a high level of technology transfer, postponing large scale investment until a high level of

innovation of new technologies and investment in certainty is achieved to mitigate investment risk. The

capacities, and therefore the opportunities for the UK first UK contracts for Hinkley C are likely to be won in

supply chain are considerable. mid to late 2013.

This section considers the threats to the UK’s 2020 Whilst most companies are not yet ready for large

targets for nuclear arising from the manufacturing scale investment, some Tier 1 suppliers already have

supply chain. Seven areas of potential threats have the confidence at this stage to invest in capacity for

been identified through the stakeholder consultation: nuclear new build, and example being Rolls-Royce

uncertainty in the economic climate; engagement of which is planning to build a factory in Rotherham

Tier 1 suppliers; supply of ultra large forgings; global adjacent to the Nuclear AMRC [22]. The commitment

competition; manufacturing capabilities; culture of of companies such as Rolls-Royce will help to build

quality; and shortage of skills and loss of knowledge. confidence at lower tiers of the UK supply chain.

These are discussed further below. 3.1.2 Engagement of Tier 1 Suppliers

3.1.1 Uncertainty in the Economic Climate The engagement of Tier 1 suppliers is regarded

Uncertainty in the economic climate is an overarching as essential in securing the UK’s place in the

threat which is stifling investment at all tiers of the manufacturing supply chain for nuclear. It is

manufacturing supply chain for nuclear in response to recognised that the winning of major supply

increased risk. As highlighted in Section 1.1, in March contracts by leading Tier 1 suppliers such as Rolls-

2012 Horizon withdrew its plans for nuclear new Royce, Doosan Babcock, BAE Systems, Sheffield

build at Wylfa in the UK due to uncertain economic Forgemasters, Wyman Gordon and Balfour Beatty will

conditions and the accelerated nuclear phase out in help to ensure that more UK companies are recruited

Germany as a result of the Fukushima disaster [12]. as Tier 2 to 4 suppliers.

www.materialsktn.net 13ENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

It is widely regarded that the UK’s Tier 1 suppliers IFA and Firth Rixson, and large forgings such as the

are well prepared for engagement in the nuclear primary pipework for the pressuriser and main coolant

supply chain, and as a result there are no support pump through Sheffield Forgemasters Limited (SFL),

programmes specifically aimed at the top tier of the UK does not have the capacity to manufacture the

the supply chain, although Tier 1 suppliers are largest forgings required for nuclear, including casting

developing the technical capability to compete on the required size ingots.

cost, quality and delivery through membership of the

Nuclear Advanced Manufacturing Research Centre The number of suppliers of ultra large forgings is

(Nuclear AMRC) [23]. Whilst the UK’s capabilities and limited to a few suppliers worldwide, and individual

capacities to manufacture for nuclear have diminished large presses have a low throughput of around four

over the previous two decades, capabilities and pressure vessels per year, though the potential is

capacities have been retained particularly strongly greater than this. A summary of the world’s forging

amongst the top tier of the supply chain as a result capacity for large pressure vessels is given in Table 3.

of supply to the new build programmes of other The limited number of suppliers of ultra large forgings

countries, the ongoing maintenance programmes is generally not regarded as a bottleneck in the

of the UK’s existing nuclear fleet, and the UK’s nuclear new build programmes of the UK or other

nuclear submarines. Tier 1 suppliers are generally countries. Although in 2009 Westinghouse was

well equipped for nuclear new build in terms of restricted in that the AP1000 pressure vessel closure

accreditation for the nuclear industry, a culture of head and three complex steam generator parts could

quality, the relevant skills and expertise, and an only be made by Japan Steel Works, the demand for

established track record in the global market place. large forgings has been reduced by the curtailing of

The UK’s newest nuclear reactor, Sizewell B, which nuclear plans from several countries following the

was commissioned in 1995, allowed the UK to Fukushima disaster, and the capacity of many of

acquire and retain some knowledge of PWR systems, the forging presses is predicted to increase to 2013

although the designs of the new-build PWRs will have as a result of investment, as shown in Table 3. The

some considerable differences to Sizewell B and the manufacture of large forgings for nuclear new build

supply chain structure has changed significantly. is carefully scheduled to ensure that enough time is

3.1.3 Supply of Ultra Large Forgings allowed, for instance some large forgings for Hinkley

C have already been ordered from La Creuset forge in

The area that has been identified as the greatest

France and Japan Steel Works.

threat arising from Tier 1 supply in the UK is ultra-

large forgings, which require forging presses of A greater concern arising from the supply of ultra large

around 14-15,000 tonnes and capacity to accept forgings is that the UK’s incapacity to deliver in this

hot steel ingots of 500-600 tonnes [24]. A defining area may mean that the UK also loses opportunities to

feature of Generation III+ reactors is the need for supply at lower tiers of the supply chain. An example

larger integral forgings; around twice the amount of this would be the RPV head; if the forging of the

of large forgings are required by Generation III+ head takes place overseas, it is more likely that the

reactors than Generation II, and integral forgings are drive assembly for the control rods attached to the

preferred to welded split forgings. The UK does not RPV head will do also.

have the capability to deliver forgings of this size for

3.1.4 Global Competition

components such as the reactor pressure vessel

(RPV) head, steam generator and large turbine. Whilst The competiveness of UK suppliers in the global

the UK has the capability to deliver small to medium market for nuclear is highly renowned as a result of the

sized forgings through a range of suppliers such as UK’s long-established expertise developed through

14 www.materialsktn.netMATERIALS KTN TECHNICAL TEXTILES:

DEVELOPMENTS IN OLYMPIC CLOTHING AND TEXTILES

Table 3

Summary of world forging

capability for large pressure

vessels. Courtesy of Rob

Mitchell, Rolls-Royce plc [24]

Heavy forging Heavy forging by Max. ingot - tonnes

Country or region Company

press mid 2009 2013 (2013)

Japan Steel Works 14,000 t 14,000 t x 2 600 (650)

JCFC 13,000 t from 2010 500

Japan

Nil, uses forgings to

MHI

make RPVs

South Korea Doosan 13,000 t 17,000 t from 2010 540

China First Heavy

15,000 t, 12,500 t same 600

Industries (CFHI)

Harbin Boiler 8000 t same

China

Shanghai (SEC) 12,000 t 16,500 t 600

China Erzhong +

12,700 t, 16,000 t same 600

Dongfang

L&T 9000 t 15,000 t 600 (in 2011)

India BHEL 10,000 t

Bharat Forge 14,000 t

AREVA, SFARsteel 11,300 t same 250

Sheffield Forgemasters

10,000 t 15,000 t ? 500 ?

Limited

Pilsen Steel 100 MN (10,200 t) 12,000 t 200 (250)

Europe

Vitkovice 12,000 t same

Saarschmiede 8670 t 12,000 t (in 2010) 370

Nil, uses forgings to

ENSA

make RPVs

USA Lehigh 10,000 t same 270

OMZ Izhora 12,000 t 15,000 t 600

Russia

ZiO-Podolsk

South Africa DCD-Dorbyl

our nuclear submarines, design and operation of our However, competition in the expanding global market

existing nuclear power plants, our current participation place for nuclear against established suppliers

in nuclear supply chains for other countries, and our remains a formidable challenge for UK manufacturing

renowned expertise for high-value manufacturing companies. Expansion of UK companies to the

acquired through other sectors including oil and required capacities may take place at a late stage to

gas and aerospace. UK companies are preferred mitigate investment risk, placing overseas companies

to overseas suppliers in many areas of the nuclear that already have the required capacities in a stronger

supply chain due to our trusted culture for quality and position to penetrate supply chains for nuclear new

ability to deliver reliably to the required price, quality build. A specific challenge is developing an ‘export

and timescale. package’ derived from a fully integrated supply chain,

www.materialsktn.net 15ENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

from raw material to finished component manufacture. all forged components and tubing materials to supply

Components that will be required in large quantities its own needs and that of other countries, although

include extruded steel pipework, joists and plates. its rate of growth in the nuclear sector is lower than

Pumps and valves will offer significant opportunities, China’s.

with around 8000 valves in around 20 packages

3.1.5 Manufacturing Capabilities

required for the AREVA EPR and over 5400 valves

required for the Westinghouse AP1000. Improvement of manufacturing capabilities to achieve

the required quality standards for nuclear products

An example of the challenge associated with capacity

is a formidable challenge and opportunity for UK

expansion is the manufacture of stainless steel manufacturing companies at all tiers of the supply

pipework for the primary circuit. Sandvik Materials chain. This is because, whilst the technology and

Technology [25] and Valinox Nucléaire [26] are processes for manufacturing to the high integrities

established suppliers in this market, and it is a required for nuclear already exist elsewhere in the

considerable challenge for UK companies to compete global supply chain, these technologies are generally

alongside them even when the can already achieve proprietary and therefore the UK is required to

the required quality. A further example is the major innovate its own technologies that can achieve or

primary circuit large bore thick walled pipework, where exceed the required quality whilst also competing

Germany is already better placed in this market than on cost to achieve competitiveness in the global

the UK. market place. The nuclear industry is notoriously

The UK has strong competitors for nuclear new conservative and risk aware, which has stifled

build from within Europe where cost competiveness, development in some areas in recent years, but

capacity and track record are challenges. Italy is also plays to the UK’s advantage because there

regarded as more cost competitive than the UK, with is the opportunity to accelerate rapidly through a

four to six companies that are already established learning curve facilitated by knowledge transfer

in forging, casting and heat treatment for nuclear. with other high-value manufacturing sectors and

The Czech Republic and France are formidable innovation. Key challenges for manufacturing process

competitors, both with fully integrated supply chains development include high quality forgings, machining,

from supply of raw materials to manufacture, and the weld cladding, welding, fuel cladding and powder

ability to supply to the UK market whilst competing technologies. These challenges are summarised

on cost. Finland, Germany, Italy, Scandinavia and below.

Spain also have strongly established supply chains High Quality Forgings

for nuclear and are competitive in the supply of ASME

accredited materials for nuclear. A significant challenge is manufacture of forgings

that have the required properties and microstructure,

Outside Europe, many countries which already have are machined to tolerance, assembled by high

operational nuclear plant, e.g. China, Japan, India quality welds, and can maintain integrity in exposure

and Korea, have developed capabilities for supply to radiation, temperature, pressure, corrosion and

for nuclear through repairing and maintaining their erosion for 60 years.

own plants which were originally supplied by other

Machining

countries. China has a rapid rate of development for

nuclear but is more likely to focus its attentions on Machining to high tolerances including deep hole

supplying to its own nuclear new build programme boring is a key challenge area for manufacturing. The

than other countries. India is competitive on cost and recently-opened Nuclear AMRC is addressing this with

has its own forge with the capability to manufacture the use of state-of-the art machining centres and the

16 www.materialsktn.netENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

support of leading machining companies. online in 2013 for the UK to assist with material de-

risking in support of nuclear new build.

Weld Cladding

3.1.6 Culture of Quality

New methods of laser weld cladding are being

developed to deposit a lining of stainless steel in A culture of quality is paramount across all levels of

the primary steam supply system to protect from the nuclear supply chain. It is widely regarded that

corrosion and erosion. manufacturing companies that are already engaged

in high-value manufacturing for other sectors such

Welding

as oil and gas, aerospace and fossil fuel power

Welding poses some significant challenges for generation are well prepared for making the transition

manufacturing including narrow gap welding using to the nuclear industry, although it is perceived to be a

lasers and high-integrity transition welds between low greater challenge for small to medium size companies

alloy steels and transition steels at the connection of that are at lower tiers of the supply chain.

the pipework with the reactor. Two main internationally recognised accreditation

Fuel Cladding systems are used for nuclear: the American Society

of Mechanical Engineers (ASME) ‘N’ stamp and

The fuel cladding material currently used for PWRs

RCC-N developed in France. N-stamp accreditation

is Zircalloy due to its very low neutron absorption

means that the authorised vendor has produced the

coefficient, adequate strength and resistance to

commercial nuclear grade components in accordance

corrosion in the operating temperature range.

with the ASME Boiler and Pressure Vessel Nuclear

However, the temperature range of Zircalloy limits the

Codes and Standards. It applies to both design and

operating temperature range of the reactor, and if the

fabrication of components, but is only likely to be

material overheats it loses its strength rapidly due mandatory by companies and contractors involved

to ballooning whilst reacting with water to produce in the supply of safety critical components. RCC-N

hydrogen. If the hydrogen leaks into the surround is used outside the USA for nuclear mechanical and

building, it can produce an explosive mixture with air pressure components. Specifications of components

which is what caused the explosions in the Fukushima will be developed by the project lead contractors and

disaster of 2011. As a result alternative fuel cladding then fed down the supply chain ultimately arriving

materials are being researched in addition to coatings with the companies tasked with the production of the

which would slow down the rate of reaction of Zircalloy components. Suppliers will be required to provide

with water. One alternative material that is receiving a manufacturing and quality plan for approval which

attention is carbon-silicon carbide composites. This must then be adhered to during the manufacturing

has the potential to operate at up to 400oC higher than process. A summary of the two nuclear accreditations

Zircalloy. is given in Table 4.

Powder Technologies 3.1.7 Shortage of Skills and Loss of Knowledge

Powder based (hot isostatically pressed or HIP’d)

Availability of skills is widely recognised as a concern

technologies will have a significant role to play

for the UK manufacturing supply chain for nuclear. A

in the nuclear industry of the future as a result of

rapid increase in the numbers of skilled personnel

improvement in mechanical properties and reduction

of material wastage and hence cost. Work on code employed in the nuclear manufacturing sector will

case development for powder based technologies be required to facilitate the growth anticipated in the

are rapidly advancing and the Nuclear AMRC will be manufacturing supply chain, whilst also retaining the

bringing HIPing technology development capabilities knowledge of ageing personnel who are approaching

www.materialsktn.net 17ENERGY MATERIALS: OPPORTUNITIES AND CHALLENGES IN ATTAINING

THE UK’S 2020 TARGETS FOR NUCLEAR ELECTRICITY GENERATION

RCC-M ASME

Section III Rule for Construction of Nuclear Facility

Section 1 Nuclear Island Components

Components

A General Requirements NCA General requirements

B Class 1 components NB Class 1 components

C Class 2 components NC Class 2 components

D Class 3 components ND Class 3 components

E Small components None

G Core support structures NG Core support structures

H Supports NF Supports

J Storage tanks NC / ND 3800 – 3900

P Containment penetrations NE Class MC components

Z Technical appendices Appendices

Section 2 Materials Section II Materials

Section 3 Examination Methods Section V Non Destructive Examination

Section 4 Welding Section IX Welding and Brazing

Section 5 Fabrication Various parts of Section III

Table 4

Summary of RCC-M and

ASME nuclear accreditations.

Courtesy of David Hall,

Nuclear AMRC

retirement age or already retired from the UK’s earlier 3.2 OPPORTUNITIES TO ALLEVIATE THREATS TO

nuclear programmes. Some knowledge of methods MANUFACTURING SUPPLY CHAIN

of manufacture and drawings of components from In response to the threats to the manufacturing supply

the UK’s existing nuclear fleet has already been lost chain identified above, four opportunities to alleviate

as a result of retirement of personnel or ineffective these threats have been identified: engagement with

storage and retrieval of data, which will diminish the nuclear OEMs; development of the UK’s capacity

UK’s ability to take forwards our previous learning for ultra large forgings; support for Tier 2, 3 and 4

experiences for the economic and technical benefit suppliers; and training and skills. These opportunities

of future nuclear plant. Skills shortages that are are discussed further below.

recognised include accredited welding engineers

3.2.1 Engagement with Nuclear OEMs

and hands-on skills such as machining, fabrication,

inspection and testing. The more highly skilled Engagement of the UK supply chain with the

engineers are generally over 50 with fewer in the 20-30 OEMs for nuclear (AREVA and Westinghouse) will

age group, and hence there is a need for up-skilling help to prepare companies for the challenges and

of the younger demographic. The supply of forgings opportunities that the nuclear industry has to offer by

informing of the procurement procedures and work

and castings must be underpinned by metallurgical

packages, facilitating knowledge transfer and helping

knowledge, and currently there is a burden on OEMs

to raise the confidence of the nuclear OEMs in the

and Tier 1 suppliers to educate their supply chain

UK’s capabilities. The need to increase the level of

in these areas. This is can be a strenuous burden

expertise in the UK supply chain is recognised by

whilst also trying to expand their own capabilities. EdF Energy and its established suppliers in France,

The shortage of skills for nuclear will be further and hence EdF are working with the UK supply

compounded by competing demands from other chain with the support of UKTI, OND and the NIA in

growing industries such as oil and gas and other preparation for Hinkley Point C to help to develop

power generation sectors. UK expertise through partnerships with established

French suppliers [27]. This includes UK nuclear

suppliers’ forums, such as the one held by EdF in

18 www.materialsktn.netYou can also read