7 GLOBAL RESOURCES CONFERENCE 2019, LONDON - MARCH 6TH, 2019 - ARCELORMITTAL

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

7

Daniel Fairclough, Head of Global IR

Global Resources Conference 2019, London Hetal Patel, General Manager IR

March 6th, 2019

Highly Restricted 0

Disclaimer

Forward-Looking Statements

This document may contain forward-looking information and statements about ArcelorMittal and its subsidiaries.

These statements include financial projections and estimates and their underlying assumptions, statements

regarding plans, objectives and expectations with respect to future operations, products and services, and

statements regarding future performance. Forward-looking statements may be identified by the words “believe”,

“expect”, “anticipate”, “target” or similar expressions. Although ArcelorMittal’s management believes that the

expectations reflected in such forward-looking statements are reasonable, investors and holders of

ArcelorMittal’s securities are cautioned that forward-looking information and statements are subject to numerous

risks and uncertainties, many of which are difficult to predict and generally beyond the control of ArcelorMittal,

that could cause actual results and developments to differ materially and adversely from those expressed in, or

implied or projected by, the forward-looking information and statements. These risks and uncertainties include

those discussed or identified in the filings with the Luxembourg Stock Market Authority for the Financial Markets

(Commission de Surveillance du Secteur Financier) and the United States Securities and Exchange Commission

(the “SEC”) made or to be made by ArcelorMittal, including ArcelorMittal’s latest Annual Report on Form 20-F on

file with the SEC. ArcelorMittal undertakes no obligation to publicly update its forward-looking statements,

whether as a result of new information, future events, or otherwise.

1

Structural transformation

Improved business and improved industry means ArcelorMittal well positioned for success

Global Steel Industry ArcelorMittal Balance sheet ArcelorMittal Portfolio

▪ Trade responses to ▪ Net debt reduced ▪ Action2020

unfair competition ▪ Votorantim acquired

▪ IG rating recovered

▪ Capacity reduced ▪ ILVA acquired

▪ Deleveraging to

▪ Consolidation occurring continue ▪ Essar in process

Strengthened Strengthened Strengthened

2

Safety is our priority

LTIF* rate in 2018 was the lowest since the ArcelorMittal merger

3.1

2.5

1.9

1.8

1.4

1.0

0.85 0.85 0.81 0.82 0.78

0.69

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018**

* LTIF = Lost time injury frequency defined as Lost Time Injuries per 1.000.000 worked hours; based on own personnel and contractors; A Lost Time Injury (LTI) is an incident that causes an

injury that prevents the person from returning to his next scheduled shift or work period. Lost Time Injury Frequency Rate (LTIFR) is the number of Lost Time Injuries per million man-hours.

** Data does not include the LTIFR for Ilva, which came into the scope as from November 1, 2018. Ilva LTIFR for the final two months of 2018 was 8.2, and the total LTIFR for the group inclusive

of this was 0.73x for the FY 2018

3

Sustainable Development – key to our resilience

Driven by our vision to make steel the material of choice for the low carbon and circular economy

• Product innovation including S-in-motion® solutions for automotive

R&D Driven

Innovation • Steligence®, a radical new concept for the use of steel in construction awarded Steelie

award for ‘Excellence in Life Cycle Assessment’

• To low carbon and circular economy through Carbon Smart technology like the LanzaTech

project on Carbon Capture and utilisation at Gent, Belgium

Contribution

• Design of our new headquarters in Luxembourg showcasing that steel components in are

re-usable

• Drive the development of environmental and social certificate schemes for steel and

Development mining production

• Providing customers new levels of complete mine-to-metal reassurance

4

2018: strategic progress and improved financials

Improved operating conditions more than offset operational disruptions

Financial Highlights

IG rating

Recovered investment

• 20.3% increase in operating income

grade credit rating with

• 22.1% improvement in EBITDA all 3 agencies

• Steel shipment volumes declined

1.6% (-3.0% adjusted for scope) 0.69x LTIF rate

• Net income of $5.1bn, representing a Best safety performance since

12% ROE ArcelorMittal’s merger

• Shareholders’ equity increased to

$44.1bn $4.4bn $0.6bn

Investment in Net Pension and

• Net debt/ LTM EBITDA now 1.0x

working capital OPEB liability

• Recommended increase in base reduced

dividend to $0.20/sh significantly

5

2018 financial results reflect better markets

Steel divisions benefitted from improved steel spreads partially offset by lower volumes

• 2017 to 2018 EBITDA by segment ($bn)

0.5 NAFTA: Europe:

10.3

EBITDA +45.1% to $2.5bn EBITDA +7.0% to $3.8bn

-0.1 Shipments +1.0% to 22Mt Shipments +0.2% to 41Mt

0.3 EBITDA/t +43.7% to $112/t EBITDA/t +6.8% to $93/t

0.4 BRAZIL: ACIS:

EBITDA +55.4% to $1.5bn EBITDA +36.9% to $1.4bn

12-15

Shipments +5.8% to 11.5Mt Shipments -10.3% to 11.7Mt

0.8

EBITDA/t +46.9% to $134/t EBITDA/t +52.7% to $120/t

Mining:

EBITDA -9.2% to $1.3bn

Iron ore shipments +5.5% to 37.6Mt; Coal shipments -10.7%

8.4

FCF breakeven level remains at $40/t CFR China 62% Fe

FY17 NAFTA ACIS Europe Brazil Mining Others FY18

6

Production impacted by operational disruptions

Nonrecurrence should provide support for 2019 volumes

• Crude steel production in 2018 v 2017

• Estimated disruption loss of ~2Mt in 2018

• (scope adjusted for Votorantim and Ilva acquisitions) (Mt)

• 1.0Mt of production losses identified as

project related and 0.9Mt as unplanned NAFTA -0.9

outages

Brazil 0.5

• Operational issues faced largely in ACIS

and NAFTA during 2018 Europe 0.2

• Volume disruptions incurred at other

ACIS -1.7

segments earlier in 2018 were recovered

• Focus in 2019 to ensure non recurrence

of such issues which should provide

support for 2019 volumes

Unplanned outages 0.9

Project related 1.0

2018

7

Volumes impacted Action2020 progress

Continued gains in cost/mix improvement offset in part by shipment losses

• 3 years into the Action 2020 improvement plan to Action 2020 cumulative EBITDA improvement ($bn)

structurally improve EBITDA by $3bn

• 2018 cost/mix gains of $0.4bn:

Volume

➢ Digital transformation in Europe 3.0

Cost/Mix

➢ Ukraine (coke oven battery savings)

1.0

➢ Brazil (cost & mix improvement)

➢ South Africa (improved efficiencies from

debottlenecking production and top line 1.5 1.6

optimisation) 0.3

• Volume progress reversed due to operational 0.9 2.0

1.6

disruptions loss of $0.3bn 1.2

0.9

• $1.6bn cumulative savings from Action 2020 plan

• Company remains focussed on achieving its 2016 2017 2018 2020F

Action2020 targets Target

8

Stronger balance sheet

Significant working capital investment in 2018; release expected in 2019

Capital deployment in 2018

Net debt to EBITDA

Investment

in working ~$4.4bn 3.0

capital 2.8

2.3

Net M&A $0.4bn

spend 2.2 2.3 2.2 1.8

1.2

Growth 1.0

capex $0.3bn

Cash

returned to

ArcelorMittal $0.3bn

shareholders Dec 31, Dec 31, Dec 31, Dec 31, Dec 31, Dec 31, Dec 31, Dec 31, Dec 31,

2010 2011 2012 2013 2014 2015 2016 2017 2018

9CAPITAL ALLOCATION

10Capital allocation to support strategic goals

Building strong foundations for future returns

Building the strongest platform for consistent capital returns to shareholders

Targeting $6bn net debt – a level of debt

Resilient

Robust balance sheet that should support positive FCF* and IG

credit metrics at all points of the cycle platform

Whilst investing in high-return

To grow FCF

Invest in strengths opportunities with focus and strict

discipline potential

Progressively increase base dividend with

Returns to Consistently

a commitment to returning a percentage

shareholders of FCF on attainment of debt target return cash

* Free cash flow refers to cash flow from operations less capex

11Investment plan focussed on high-return projects

Additional capex planned in 2019 to fund ILVA as well as mix & cost improvement projects

Committed to high-return projects (capex, $bn)

UNIQUE opportunities

in CORE markets

0.4 0.1

0.5

Move MIX to most

attractive end markets

4.3

Incremental budget approved including carry-over

3.3

Increase

COMPETITIVENESS 2018 ILVA Brazil & Other 2019F

Mexico Strategic

Projects

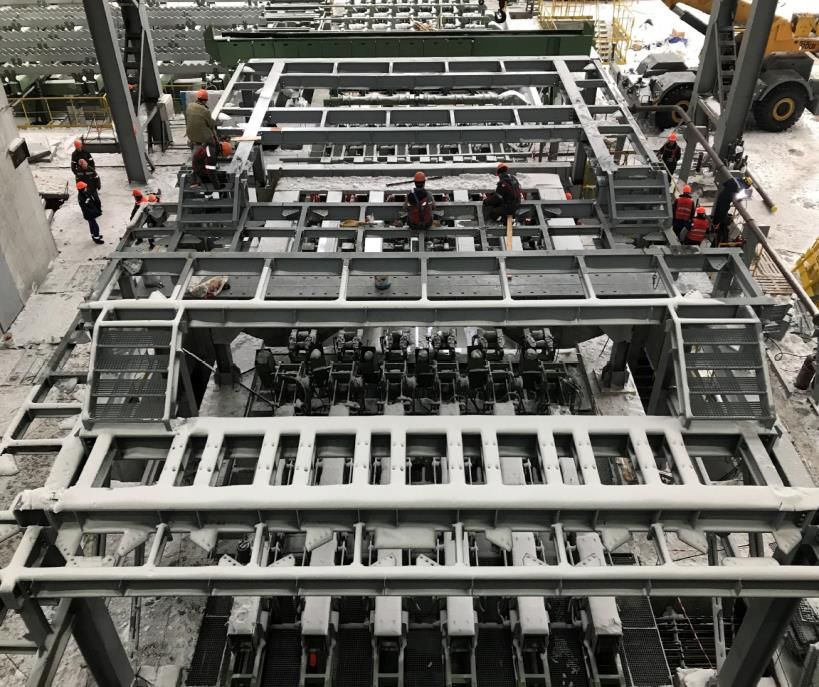

12Mexico: HSM project

High return mix improvement with future optionality

Project summary: US$1.0bn 3Yr investment commitment

Construction of a new 2.5Mt hot strip mill

• HSM project to optimize capacity and improve mix

➢ $1bn project initiated in 4Q’17; expected completion in 2020 (Mt) ASC (Million tonnes; flat products)

➢ New 2.5Mt hot strip mill to increase share of domestic market (domestic 20

17.2 16.6

15.7 16.2

HRC spreads are significantly higher vs. slab exports) 15

John Deere India54%

➢ Includes investments to sustain the competitiveness of mining operations 52% 50% 50%

10

and modernizing its existing asset base

5

• ArcelorMittal Mexico highly competitive low cost domestic slab Share captured by Imports

• Growth market, with high import share 0

2015 2016 2017 2018

➢ Mexico is a net importer of steel (50% flat rolled products import share)

➢ ASC estimated to grow 2.0% CAGR 2015-25; growth in non-auto +2.2%,

supported by industrial production and public infrastructure investment

• Potential to add $250 million in EBITDA on completion

Project status:

• Deep foundations nearly complete (demobilizing in February); building

erection progressing on schedule; mill cranes on site, other equipment in

transit

13Brazil: Vega high added value capacity expansion

High return mix improvement in one of the most promising developing markets

Project summary: 3Yr investment to expand rolling capacity →

increase Coated / CRC capacity and

• HAV expansion project to improve mix construction of a new 700kt continuous

➢ Completion expected 2021 with total capex spend of ~$0.3bn annealing line (CAL) and

John continuous

Deere India galvanising

combiline (CGL)

➢ Increase Galv/CRC capacity through construction of 700kt continuous

annealing and continuous galvanising combiline

➢ Optimization of current facilities to maximize site capacity and

competitiveness; utilizing comprehensive digital/automation technology

➢ To enhance 3rd generation AHSS capabilities and support our growth in

automotive market and value added products to construction

• AM Vega highly competitive on quality and cost, with strategic location and

synergies with AM Tubarão

• Investment to sustain ArcelorMittal Brazil growth strategy in cold rolled and

coated flat products to serve domestic and broader Latin American markets

• Strengthening ArcelorMittal’s position in key markets as automotive and

construction through value added products

• Potential to add >$100mn to EBITDA

14Votorantim consolidates our position in Brazil longs

Multi-year acquisition project concluded in April 2018

• Culmination of a multi-year process that

Creating the new market leader in Brazil longs

began in 2014

• Consolidating the Brazil long products

market

Minas Gerais

• ArcelorMittal now the #1 long products

producer with annual crude steel capacity of Monelevade

5.1Mt.

Juiz de Fora

• Acquired production facilities are

geographically complementary, enabling Rio de Janeiro

Sao Paulo

higher service level to customers, economies Piracicaba

of scale, higher utilization and efficiencies.

Resende plant Barra Mansa plant

• ~$110m of identified synergies on track to be

fully captured in 2019

Resende Barra Mansa

15ILVA project to turnaround and restore tier-1 status

Multi-year acquisition project concluded in November 2018

• Culmination of a multi-year process that began in 2014 ILVA capex commitment through 2024 (€ bn)

• Improvement plan now underway to:

2.40

• Increase production to 6Mt near term; then to 8Mt 2.10

0.30

post completion of environmental plan 1.25

• Capture identified synergies (€310m) and realise 1.15

asset’s potential Industrial capex

includes annual

• Focus on: maintenance

Enviromental Industrial Total capex Riva funds Net capex

• Health and safety: Top priority to improve H&S utilised

performance underway

• Investment program underway: Coverage of the

raw materials stockyards progressing in-line with

the accelerated timetable

• Performance and operations: identify gaps with

ArcelorMittal sites and take actions; adopt Progress at the raw material stock yard

ArcelorMittal commercial approach

• Integration: use benchmarking

16Essar: Adding a new high-growth pillar

Essar brings scale, turnaround opportunity and growth optionality

• Essar provides ArcelorMittal an opportunity to buy a producing, Essar Steel main production

profitable, cash generating asset at below replacement costs facilities at Hazira, Gujarat;

10Mtpa nominal capacity (current

• ArcelorMittal received approval for acquisition of Essar* production 6.5Mtpa)

• Upfront payment of $5.7bn** to ESIL creditors with a further

$1.1bn** capital injection into the business to kickstart

turnaround

• ArcelorMittal aims to increase shipments to 8.5Mt in medium

term, with long term target of 12-15Mt through additional

brownfield capacity expansion

• Iron ore pelletising integration in East India provides optionality:

14Mtpa pellet capacity → currently being expanded to 20Mtpa

• ArcelorMittal & NSSMC to finance their “India JV” through

combination of partnership equity (1/3) and debt (2/3)

• Investment in the “India JV” expected to be equity accounted

1 2 3 4 5

One of the largest single Service centres in

Complete basket of flat Access to Port

High quality raw material Largest pellet capacity in India location for flat steel in India competitive locations

steel produtcs

* In-line with Essar Steel India Limited’s (ESIL) corporate insolvency process, the Company’s Resolution Plan must now be formally accepted by India’s National Company Law Tribunal

(‘NCLT’) before completion **at 73.2 Indian rupees / $1 .

17OUTLOOK

18Global steel demand

Global Apparent Steel Consumption (ASC) growth of +0.5% to +1.0% forecast in 2019F

Estimated ASC growth 2018 v 2017* Forecast ASC growth 2019F v 2018*

US +1.7% US +0.5% to +1.5%

EU28 +2.9% EU28 +0.5% to +1.0%

China +3.5% China -0.5% to -1.5%

Brazil +7.3% Brazil +3.5% to +4.5%

CIS +1.8% CIS +1.0% to +2.0%

Global ex China +2.1% Global ex China +2.0% to +3.0%

Global +2.8% Global +0.5% to +1.0%

Source: *ArcelorMittal estimates

19Position to Deliver Value

Global diversified industry leader focussed on maximising per-share value

• Unique global portfolio ArcelorMittal

Secure position in mature developed markets High-growth, with attractive Access to

• Industry leader in product and (with growth exposure e.g. Mexico) with

emphasis on HAV leadership

market structure and gradual

evolution towards HAV

growth

markets

process innovation

• Action2020 plan to structurally

EUROPE

BRAZIL

NAFTA

improve profitability

INDIA

ACIS

• Investing with focus and discipline

in high return opportunities

• Investment grade balance sheet

Mining

• Progressively returning cash (capturing the full value-in-use chain)

Investment Grade Balance Sheet

20APPENDIX

21Appendix

• SECTION 1 | Cash needs.……………………………………………………. 23

• SECTION 2 | Trade.………………………………………………………....... 25

• SECTION 3 | Financials results..…………………………………………….. 29

• SECTION 4 | Steel investments..…………………………………………………… 40

• SECTION 5 | Macro highlights……………………………………………….. 46

• SECTION 6 | Industry leadership……………………………………………. 49

• SECTION 7 | Auto ……………………………………………………………. 54

• SECTION 8 | Group highlights ………………………..…………………..…. 67

22CASH NEEDS

23Cash needs

Cash needs* to increase in 2019 largely due to increased capex spend on high return opportunities

• Cash needs to increase to $6.4bn in Below-EBITDA cash needs ($ billions)

2019 6.4

• The $1.4bn increase Vs. 2018 reflects:

1) $1bn increase in capex (including 1.5

5.0

$0.4bn carryover from 2018)

Taxes**, pension and other 1.1 0.6

2) Cash taxes deferred from 2018

3) Non recurrence of certain cash Net interest 0.6

gains in 2018

• Unplanned working capital investment in

2018 is expected to be released in 2019 4.3

Capex 3.3

• As a result, Company should achieve

more significant net debt progress in

2019

2018 2019F

* Cash needs of the business consisting of capex, cash paid for interest and other cash payments primarily for taxes and excluding for these purposes working capital investment

** Estimates for cash taxes in 2019 largely reflect the taxable profits of 2018

24TRADE

25EU trade Comprehensive solution for unfairly trade imports required Trade cases (Flat steel): • All key flat rolled steel products Anti-dumping and countervailing duty cases have been implemented • Monitoring for unfairly traded imports ongoing Safeguard duties: • On January 17, 2019, EU Member states approved the European Commission’s (EC’s) final safeguard measures on steel with implementation to begin February 4, 2019 • Final measures include immediate “relaxation”, increasing quota by 5% (calculated on base years of 2015-2017), with further 5% relaxation in July 2019 and another 5% in July 2020, subject to review • Final measure give country-specific quotas to main steel exporters to EU; remaining residual quote for other countries to be quarterly, however countries with own quota can consume residual quote once they have used up their own • Certain 'developing' countries with a share of imports of

NAFTA trade

Comprehensive solution for unfairly trade imports required

Trade cases:

• All key flat rolled steel products AD/CVD cases have been implemented.

• Anti-circumvention investigations initiated by DOC for CRC and CORE imports from China (through Vietnam); final affirmative

determination received May 17, 2018

• On June 12, 2018, the US industry filed anti-circumvention petitions with DOC for CRC and CORE imported from Korea and Taiwan

(through Vietnam).

Section 232 US:

• March 23, 2018: 25% tariffs imposed on all steel product categories began for most countries

• June 1, 2018: 25% tariffs imposed on steel products in Europe, Canada & Mexico (no change despite agreement on NAFTA as still

awaiting Canada) with the following exceptions:

• South Korea: Quota of 70% of 2015-2017 av. export volumes into US

• Brazil: Quota of 2015-2017 average export volumes into US - 70% for finished products; 100% for semi-finished products

• Argentina: Quota of 135% of 2015-2017 average exports

• Australia: completely exempt from tariffs and quotas

• August 30, 2018: Trump issued a proclamation whereby there is now a product exclusion request process in place for countries

where there is a quota, i.e. S. Korea, Argentina and Brazil

• Turkey: duties doubled to 50% from 25% due to currency devaluation

Canada and Mexico response to Section 232:

• Canada: 25% retaliatory tariffs on US imports for most steel products, Provisional safeguard measures announced on October 11,

2018 on 7 steel products (hot rolled, prepaint, rebar, wire rod, energy tubulars, plate and stainless wire)

• Mexico: 15-25% retaliatory tariffs on US imports for most steel products; Safeguard duties of 15% already in place for countries with

no free trade agreement

27FINANCIAL RESULTS

28Operating results for 4Q’18

Quarterly results impacted by sequential seasonal slowdown and operational issues

• EBITDA: $2.0bn (-8.9% vs.4Q’17); 12M’18 $10.3bn

EBITDA progression ($bn)

(+22.1% YoY)

• Steel performance lower QoQ: impacted by negative

price-cost effect and lower steel shipments (-1.5%) to +22.1%

20.2Mt

10.3

• Mining performance higher QoQ: Impacted by -8.9%

higher marketable iron ore shipments (+16.8% QoQ);

2.7 8.4

12M’18 at 37.6Mt (+5.5% YoY)

• Net income: at $1.2bn vs $0.9bn in 3Q’18 2.1

2.0

• Working capital release of $0.4bn in 4Q’18

$102/t $133/t $96/t $99/t $122/t

• Net debt of $10.2bn as of Dec 31, 2018 as compared

to $10.1bn as of Dec 31, 2017

4Q’17 3Q’18 4Q’18 12M’17 12M’18

Note: YoY refers to 12M’18 vs. 12M’17; QoQ refers to 4Q’18 v 3Q’18; 29Steel performance for 4Q’18

Steel-only EBITDA increased YoY but declined QoQ (in all segments)

12M’18 steel-only EBITDA up +28.4% YoY primarily Steel only EBITDA ($bn) and EBITDA/t ($/t)

due to positive price-cost effect (PCE) with all segments

improving -34.3%

+28.4%

2.4

4Q’18 steel-only EBITDA down 34.3% vs. 3Q’18 9.0

1.9

• ACIS: EBITDA down -55.7% Negative price-cost 1.6 7.0

effect and lower shipments (operational issues in

Kazakhstan) $89/t $119/t $79/t $82/t $107/t

• Brazil: EBITDA down -37.2% Negative price-cost

effect 4Q’17 3Q’18 4Q’18 12M’17 12M’18

• NAFTA: EBITDA down -33.2% Lower steel

shipments and negative price-cost effect 3Q’18 to 4Q’18 steel only EBITDA ($mn)

• Europe: EBITDA down -14.0% Performance

primarily impacted by negative price-cost effect

-247

2,448 -165

-122 -57

-249 1,608

3Q’18 NAFTA Brazil Europe ACIS Others 4Q’18

Note: YoY refers to 12M’18 vs. 12M’17; QoQ refers to 4Q’18 v 3Q’18 30Mining performance for 4Q’18

Mining profitability positively impacted by higher shipment volumes and iron ore prices

• Mining performance:

Mining EBITDA ($mn)

• 4Q’18 EBITDA improved 22% QoQ primarily due

to higher market priced iron ore shipments

(+16.8% QoQ) +22% -9.2%

• FY’18 EBITDA declined 9.2% YoY primarily due to 343 1,407

weaker coal performance driven by lower 281

volumes. 1,278

• Growth: Market priced iron ore shipments grew

5.5% in 2018 YoY

3Q’18 4Q’18 12M’17 12M’18

• Focus on quality: ongoing commitment on quality,

service and delivery

Marketable iron ore shipments (Mt)

• Cost focus maintained: FCF breakeven remains

$40/t

+16.8% +5.5%

10.0 37.6

8.5

35.7

3Q’18 4Q’18 12M’17 12M’18

Note: YoY refers to 12M’18 vs. 12M’17; QoQ refers to 4Q’18 v 3Q’18 314Q 2018 EBITDA to net results

Positive net income in 4Q 2018

BASIC EPS 4Q’18

($million) Weighted Av. No. of shares (in millions) 1,014

Earnings per share $1.18

Includes $0.1bn in

currency translation

gains following disposal Includes $0.8bn deferred tax

of MacSteel benefits recorded mainly in

(723) Luxembourg on expected higher

future profits

227 (140)

(215)

29

1,951

(556) 620

Related to

acquisition of 1,193

ILVA and ILVA 1,042 Primarily

remedies

MTM on

MCB 573

EBITDA D&A Impairment Exceptional Operating Income Net interest Forex Pre-tax Taxes and Net income

net of items income from expense and other income non-

purchase investments fin. result controlling

gains interests

324Q 2018 EBITDA to free cashflow

FCF positive $1.0bn

($million)

(211)

430

(1,156)

2,170

1,951

1,014

EBITDA Change in Other Cash flow from Capex Free cash flow

working financing operations

capital* costs

* Change in working capital: cash movement in trade accounts receivable plus inventories less trade and other accounts payable

333Q’18 v 4Q’18 Net debt

Net debt declined – September 30, 2018 vs. December 31, 2018

($million)

32 37

1,014

Includes

699 $0.1bn forex

gain

10,516

10,196

Primarily includes $1bn

investment for the Uttam

Galva and KSS Petron debts,

offset by MacSteel disposal

($0.2bn)

Net debt at Free cash flow M&A Minority dividends Forex and other Net debt at

Sept 30, 2018 Dec 31, 2018

34FY 2018 EBITDA to net results

Healthy net results for the full year 2018

BASIC EPS 2018

($million) Weighted Av. No. of shares (in millions) 1,015

Include $0.6bn for

Earnings per share $5.07

acquisition of ILVA and

ILVA remedies and

remedy package required

Includes income from

for Votorantim acquisition Includes $0.8bn

(2,799) Calvert and Chinese

deferred tax benefits

investees and

Erdemir dividend recorded mainly in

Luxembourg on

expected higher

(810) 652 (615) future profits

(117)

(1,595)

10,265 168

BF dismantling in Florange

($0.1bn); new CLA in US Primarily forex and MTM on

(including signing on bonus) 6,539 MCB partially offset by

($0.1bn); settlement fees premium on early repayment 5,149

($0.1bn); offset in part by $0.2bn

4,981

of bonds

PIS/Cofins tax credits in Brazil

EBITDA D&A Impairment Exceptional Operating Income Net interest Forex Pre-tax Taxes and Net income

net of items income from expense and other income non-

purchase investments fin. result controlling

gains interests

35FY 2018 EBITDA to free cashflow

FCF positive $0.9bn despite $4.4bn investment in working capital in 2018

($million)

(4,384)

10,265 (1,685)

(3,305)

4,196

891

EBITDA Change in Other Cash flow from Capex Free cash flow

working financing operations

capital* costs

* Change in working capital: cash movement in trade accounts receivable plus inventories less trade and other accounts payable

36FY 2017 v FY 2018 Net debt

Net debt stable - December 31, 2017 vs. December 31, 2018

($million)

76

119

101

226

891

423

10,142 10,196

Primarily includes $1bn

investment for the Uttam

Galva and KSS Petron debts,

offset by MacSteel disposal

($0.2bn) and sale of

tangibles assets ($0.2bn)

Net debt at Free M&A ArcelorMittal Dividend Minority Forex Net debt at

Dec 31, 2017 cash flow Share buy paid to AM dividends and other Dec 31, 2018

back shareholders 37Liquidity and debt maturity

Investment grade rated by all three rating agencies

Liquidity at Dec 31, 2018 ($bn) Debt maturities at Dec 31, 2018 ($bn)

7.9

Other loans

Cash 2.4 1.0 Commercial paper

1.3

Bonds

0.3

1.3 0.5 0.2

Unused credit lines 5.5

1.9

1.5 0.3 1.6

1.3

0.9

0.5

Liquidity at 2019 2020 2021 2022 2023 ≥2024

Dec 31, 2018

Liquidity lines Debt Maturity: Ratings*:

• $5.5bn lines of credit refinanced with • Continued strong liquidity • S&P: BBB-, stable outlook

5 year maturity Dec 19, 2023

• Average debt maturity →

• Moody’s: Baa3, stable outlook

4.0 years

• Fitch: BBB-, stable outlook

*Investment grade credit rating upgrades: S&P in February 2018, Moody’s in June 2018 and Fitch in July 2018

38STEEL INVESTMENTS

39Indiana Harbor - USA Footprint

Footprint optimization complete

• Current configuration uncompetitive structural

changes required across all cost elements

• #1 aluminize, 84” hot strip mill (HSM), #5 continuous

galvanizing line (CGL), and steel shop No.2 now idled;

all planned asset consolidation now complete

• Investments totalling ~US$200m:

• New caster at No.3 steelshop installed &

commissioned 4Q’16 and restoration of 80” hot strip

mill and IH finishing complete

• Project completed in 2018

No. 3SP: New #2 Caster

Indiana Harbor Plant 80”HSM: 5 Walking Beam Furnace No. 3SP: New #23SP:

No. Caster

Newcommissioning

Downcomer

40Kryvyi Rih – New LF&CC 2&3

Kryvyi Rih investments to ensure sustainability & improve productivity

• Facilities upgrade to switch from ingot to continuous casting

route; additional billets capacity of 290kt/y

• Industrial target:

• Step-by-step steel plant modernization with state-of-art

technology

• Product mix development

• Supportive target:

• Cost reduction

• Billet quality improvement for sustaining customers

• Better yield and productivity

• Project completion expected in 2019

Construction

site of LF&CC

2&3

41ArcelorMittal Poland Sosnowiec Wire Rod Mill

Long products strategy to grow HAV

• Sosnowiec is a double strand rolling mill located in Sosnowiec, Poland.

• The investment will introduce new and innovative techniques for the

production of high quality wire rod for high demanding applications

(automotive app., steel cords, welding wires, cold heading screws,

suspension springs, special ropes)

• Investment features and benefits:

• Splitting intermediate mill stands / new motors / drives avoiding twisting

• Modernized finishing blocks for rolling speed increasing up to 100m/s

• New state of art air distribution system and ring distributor

• New water boxes with accurate process control

• Reduced tensile strength variation, improved grain size/ surface quality

• Scope of equipment to be installed in WRM Sosnowiec in 2018:

• New guiding equipment for finishing blocks, new water boxes (traversing

type), new laying heads (new type), new fans for air cooling conveyors, new

air distribution system for fans, new automation control system for water

boxes and fans (water and air cooling)

• Project completion expected in 2019

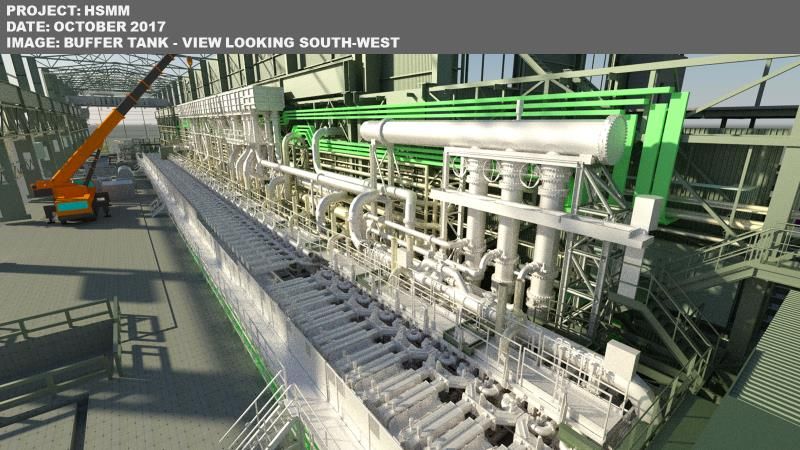

42Dofasco - Hot strip mill modernisation

Investments to modernize strip cooling & coiling flexibility to produce full range of target products

• Replace existing three end of life coilers with two state

of the art coilers and new runout tables. The strip

cooling system will be upgraded and include

innovative power cooling technology to improve

product capability

• Benefits of the project will be:

• Improved safety

• Increased product capability to produce higher

value products

PROJECT: HSMM

• Cost savings through improvements to coil quality, DATE: OCTOBER 2018

unplanned delay rates, yield and improved energy IMAGE: COILER AND INSPECTION AREA CIVIL CONSTRUCTION

efficiency

• Project completion expected in 2020

43Burns Harbour – Walking beam furnaces

Expands surface capability to provide sustained automotive footprint

• Install 2 latest generation walking beam furnaces,

including recuperators & stacks, building extension &

foundations for new units

• Benefits associated to the project:

• Hot rolling quality and productivity

• Sustaining market position

• Reducing energy consumption

• Project completion expected in 2021

44MACRO HIGHLIGHTS

45Regional inventory

Inventory levels in key regions in line with historical averages

German inventories (000 Mt)* US service centre total steel inventories (000 Mt)

(latest data point: Dec-2018) 5.0 (latest data point: Dec-2018)

1,400 Germany Stocks 13,000 3.4

4.0 USA (MSCI)

Months supply (RHS) 3.2

1,200 Months Supply (RHS)

11,000 3.0

3.0

1,000 2.8

9,000

800 2.0 2.6

7,000 2.4

600 1.0

2.2

400 0.0 5,000 2.0

Brazil service centre inventories (000 Mt) China service centre inventories** (Mt/mth) with ASC%

Flat stocks at service centres Flat and long (latest data point: Dec-2018)

1,400 (latest data point: Dec-2018) 7.0

25 50%

Months Supply (RHS)

1,200 6.0 20 40%

1,000 5.0

15 30%

800 4.0

10 20%

600 3.0

400 2.0 5 10%

200 1.0 0 0%

* German inventories seasonally adjusted **Source: WSA, Mysteel, ArcelorMittal Strategy estimates

46Chinese exports

Chinese exports declined 8% YoY to 70Mt in 2018

(latest data point: Jan-2019)

12

Exports of steel products

Imports of steel products

10

Net-trade

8

6

4

2

0

-2

-4

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

• Jan’19 finished steel exports of 6.2Mt up +11.0% MoM (Dec’18 at 5.6Mt)

• Jan’19 exports up +33.1% vs Jan’18 (4.7 Mt)

• 12M’18 finished steel exports of 70Mt down 8.0% vs 12M’17

Source: ArcelorMittal Corporate Strategy team analysis 47China addressing capacity issues

Supply side reform progressing – global overcapacity still a concern

• Chinese government committed to tackle overcapacity and

environmental issues

Target achieved to cut 140Mt

• Capacity reduction target met: 140Mt capacity cut achieved permanent capacity by end of

by end of 2018 2018

• Steel replacement policy in favour of EAF v BF; no new

capacity to be built → ratio 1:1 for EAF and 1:1.25 for BF-

BOF

• Industry operating at high rates of capacity utilisation → Additional ~120Mt illegal

higher domestic steel spreads induction furnace capacity

closed

• Stronger domestic fundamentals plus global trade restrictions

→ reduced incentive to export

• 3yr Blue Sky Campaign (2018-2020) with stringent emissions

standards

• Winter capacity constraints supporting fundamentals through Steel exports reduced

seasonally weaker demand period; delayed start in 2018, but

overall expectation that 2018/2019 policy will be broadly

similar YoY

48INDUSTRY LEADERSHIP

49Leadership through innovation continues

R&D strength to drive innovation and maintain industry leadership position

Revolutionary technology in Carbon

Steligence®: A radical new concept for

Capture & Utilization (CCU) to convert

the use of

BF carbon gas into bioethanol

steel in construction

• In partnership with LanzaTech, €150m project

• Aims to deliver significant architectural and

in Gent, Belgium, broke ground Jun’18 with

sustainability benefits to construction

commissioning expected in mid 2020

customers

• Significant potential to revolutionize blast

• Awarded the Steelie in the ‘Excellence in Life

furnace carbon emissions capture and

Cycle Assessment’ category in October 2018

support decarbonization of the transport

sector

Automotive: Recognized leader

by automotive customers

• Consistently ranked #1 in technology

by the majority of OEMs

• Addressing automotive platforms of

the future with new projects for rapidly

growing Electric Vehicle (EV) market

50Industry Leadership: Automotive

Global leader in automotive steel and solutions

• 2018 R&D spend $0.3bn

• Automotive R&D ~1/3 of this budget

• 1,400 full time researchers

• 10 worldwide research centres in Europe / Americas

including 6 dedicated to automotive

• Majority of OEMs in EU & NAFTA rank ArcelorMittal #1

in Technology – Steel will remain key material for the

body structure application

• Leader in AHSS* in both EU & NAFTA with the broadest

12-15

portfolio of AHSS grades

• Achieved significant recognition from automakers for

commitment to innovation, performance, quality and

supplier diversity:

• (Ford; Honda R&D Americas Award; GM Supplier IMPACT

Diamond Award; GM Supplier Quality Excellence for AM/NS

Calvert; Nissan’s Supplier Diversity Award; and Automotive World’s first inner & outer door ring system – a co-engineering feat

between ArcelorMittal, Honda R&D Americas and Magna - unveiled

News’ PACE Award Finalist for inner and outer door ring at WCX18 for 2019 Acura RDX

system in 2019 Acura RDX

ArcelorMittal Tailored Blanks Division produced 2 millionth door

ring on Oct. 26, 2018

*AHSS: Advanced High Strength Steels

51Industry Leadership: Steligence®

A radical new concept for the use of steel in construction

• Steligence® is based on extensive scientific research,

independently peer-reviewed

• Makes the case for a holistic approach to construction

that breaks down barriers, encouraging collaboration

between construction industry professionals

• Designed to resolve the competing demands of

creativity, flexibility, sustainability and economics

• Delivers efficiencies, benefits and cost savings to

architects, engineers, construction companies, real

12-15

estate developers, building owners, tenants and urban

planners

• Will facilitate the next generation of high performance

buildings and construction techniques, and create a

more sustainable life cycle for buildings

• Our new Headquarters building is designed to

showcase the Steligence® concept

52Industry Leadership: Transformation technologies

Technology to potentially revolutionise the capture of BF carbon gas and convert it into bioethanol

• €150million project between ArcelorMittal & LanzaTech in Gent, Belgium, broke ground June 2018

• Technology to potentially revolutionise the capture of BF carbon gas and convert it into bioethanol

• Licensed by LanzaTech, a proprietary microbe feeds on carbon monoxide to produce bioethanol, to be used as

transport fuel or potentially in the production of plastics

• Annual production of bioethanol from this demonstration expected to reach around 80m litres, which will yield an

annual CO2 saving equivalent to 600 flights from London to New York

• The new installation will create up to 500 construction jobs over the next two years and 20 to 30 new permanent

direct jobs. Commissioning and first production is expected by mid-2020

12-15

53AUTO

54No1 in automotive steel: Maintaining leadership position

Group continues to invest and innovate to maintain leadership

• ArcelorMittal is the global leader in steel for automotive with S-in motion®

strongest position in Europe and North America

• Global R&D platform provides a material competitive

advantage

• Proven record of developing new products and affordable

solutions to meet OEM targets

• Advanced high strength steels used to make vehicles lighter,

safer and stronger

• Automotive business backed with capital with ongoing

investments in product capability and expanding our

geographic footprint: AM/NS Calvert

• AM/NS Calvert JV: Enhancing our NAFTA automotive

franchise

• VAMA JV in China: Auto certifications progressing

• Dofasco: Galvanizing line expansion

• Europe: AHSS investments

55Global presence and reach

Global supplier with increasing emerging market exposure

Locations, by region

Automotive production facilities

Alliances & JV

Commercial teams

R&D centers

Vehicle production 2018

by region

> 20 M veh

> 15 M veh & < 20 M veh

> 10 M veh & < 15 M veh

> 5 M veh & < 10 M veh

> 2.5 M veh & < 5 M veh

> 1 M veh & < 2.5 M veh

> 1 M veh & 0.1 M veh

< 0.1 M veh

Source: LMC figures for Western and Eastern Europe and Russia; IHS figures for all other regions; personal cars and light commercial vehicles < 6t

NB: Middle East & North Africa region: Iran, Uzbekistan, Kazakhstan, Morocco, Egypt

South East Asia region: Indonesia, Philippines, Thailand, Vietnam, Pakistan 56Automotive growth in developed world

North American production at healthy levels,

EU28 & Turkey production with modest growth

North America and EU28 + Turkey vehicles production

million units

• North American production:

- modest decline in the short term

but still healthy production levels

- expected to regain the 17m unit

production level around 2022

driven by population growth,

portfolio expansion and

localization

• EU28 & Turkey production: modest

growth expected with uncertainty linked

to Brexit and US Tariffs

57Automotive emerging market growth

Strong growth expected in India, China and Brazil

China vehicle production (‘000s)

35,000 33,940

China

33,000 • China production to grow by ~26% by 2026

31,000

(from 27mvh in 2018 level 34mvh by 2026)

29,000

27,000

26,955 • India production to increase ~70% by 2026

25,000

(from 4.8mvh in 2018 to 8.2mvh in 2026)

Brazil, India & Russia vehicle production (‘000’s)

9,000 • Brazil production growth expected to

8,000 Russia India Brazil 8,230

7,000

continue and reach 3.9mvh in 2026 (~40%)

6,000

5,000 4,754

4,000

3,952 • Russia production is expected to recover

3,000

2,748

2,000 2,395 and reach 2.4mvh in 2026 (~46%)

1,000 1,635

0

Source: IHS 58ArcelorMittal S-in motion®

Demonstrating the weight saving potential of new products

› ArcelorMittal generic steel solutions include BIW, closures, chassis parts and seats

S-in motion® S-in motion® S-in motion® S-in motion® S-in motion® S-in motion® S-in motion® S-in motion® S-in motion®

ICE C-Segment Electric Plug-in Hybrid D-Segment Mid-size Mid-size Light Pick-up Truck

C-Segment C-Segment EU market Sedan SUV Commercial Trucks Cabs

NA market

-70kg (-18%) vs -60kg (-15%) vs -50 kg (-16%) vs -98 kg (-25%) vs -86 kg (-23%) vs -102 kg (-20%) -45kg (-20%) -174 kg (-23%) -54 kg (-17%)

current ICE current ICE current PHEV BIW and closures current Mid-size vs current SUV About 140 parts vs current vs current

baseline baseline baseline current baseline sedan baseline baseline upgraded Pick-up baseline cab baseline

Twist beam Suspension Control arms Front subframes Pick-up frame NA rear subframe Front seat

Up to 17% of -4 kg (-18%) Up to 26% of potential Up to 15% -55 kg (-23%) vs -5.9 kg (-20%) vs -2 kg (-18%) vs

mass-savings for using flat and weight-savings of mass-savings current Pick-up current D-segment current C-segment

C-segment long products on C-segment frame baseline baseline seat baseline

vehicles vehiclesContinuous innovation

Steel to remain material of choice for automotive

Jet Vapor Deposition (JVD) line : Jetgal ® Steel remains material of choice

• JVD line is a breakthrough technology to

produce Jetgal®, a new coating for AHSS steels

for automotive industry

New press hardenable steels (PHS) Usibor®2000 &

Ductibor®1000

• Bring immediate possibilities of 10% weight

saving on average compared to conventional

coated PHS produced by ArcelorMittal

• Electric vehicles (EV) to favour lightweight

3rd Generation AHSS products (CR/GI/GA) designs (similar to traditional vehicles)

980HF & 1180HF • EV employ AHSS to achieve range goals

• HF / Fortiform® provide additional weight

reduction due to enhanced mechanical properties

compared to conventional AHSS

The mass-market Tesla Model 3 body and

chassis is a blend of steel and aluminium,

Electrical steels

unlike the Tesla Model S which is an aluminium

iCARe®, 2nd Generation body (Source: Tesla website+)

• Family of electrical steels for electrified powertrain

+ https://www.tesla.com/compare

optimization and enhanced machine performance,

Save*, Torque** and Speed*** are specifically http://automotive.arcelormittal.com/ElectricVehiclesImpactOnSteel

designed for a typical electric automotive

application.

* Save (Steels with very low losses): Ideal for the efficiency of the electrical machine. Their key role is maximize the use of the current coming from the battery.

** Torque (Steels with high permeability): They achieve the highest levels of mechanical power output for a motor or current supply for a generator

*** Speed (Steels for high speed rotors): Specific high strength electrical steels which maintain high level of magnetic performance. They allow the machine to be more compact and have a higher power density. 60

-Continued investment in R&D

Supports portfolio of next generation auto steels

Fortiform® Third-generation UHSS for cold

MartINsite® A family of cold rolled fully

stamping. Fortiform® and HF steel martensitic steels with current

HF Grades grades allow OEMs to realize tensile strengths from 900 to 1700

lightweight high-strength structural MPa. ArcelorMittal’s MartINsite®

elements using cold forming cold roll family of fully martensitic

methods such as stamping. steels is perfect for anti-intrusion

Commercially launched in Europe parts such as bumper and door

in 2014 and available in North beams. Some are also available

America at Calvert in with an electrogalvanized

coating or with Jetgal®.

Press hardenable steels (PHS) / hot JVD is a breakthrough process, In

Usibor® 2000 stamping steels offer strengths up to JVD -Jetgal® production and product

development.

2000 MPa. Usibor® 2000 and

Ductibor®1000 Ductibor® 1000 can also be combined Jetskin® Jetgal® : JVD zinc coating applied

thanks to laser welded blanks (LWB) to steel grades for the automotive

to reduce weight while achieving industry. Developed for steels

optimal crash behavior. Both currently including UHSS Fortiform®;

available in Europe; Usibor® 2000 is Jetskin® : JVD zinc coating

commercially available in Europe and applied to steel grades for

available for qualification testing in industrial applications such as

North America; Ductibor® 1000 is household appliances, doors,

commercially available in Europe and drums and interior building

North America applications.

612019 Chevy Silverado

reduces weight and increases strength with AHSS

• Chevrolet claims its all-new 2019 Silverado is 450 pounds (204 kg)

lighter, supported by extensive use of mixed materials.

• For example, a higher-grade alloy is used in the

roll-formed, high-strength-steel bed floor,

contributing to a bed that is more functional

and lighter weight.

• The safety cage features significant use of

advanced high strength steels, each

tailored for the specific application.

“This use of mixed materials and advanced

manufacturing is evident throughout the

Silverado, resulting in a significant reduction

in total vehicle weight and improved

performance in many measures.”

Source: Chevrolet’s press release about its all-new Silverado, December 2017.

62Automotive Industry Leadership

Audi switched back to steel for its new A8 model

• Audi switched back to steel

for its 2018 A8 model, with a

body structure made up of

more than 40% steel

including 17% PHS

New Audi A8 2018 model

“There will be no cars made of aluminium alone in the future.

Press hardened steels (PHS) will play a special role in this development.

PHS grades are at the core of a car’s occupant cell, which

protects the driver and passengers in case of a collision.

If you compare the stiffness-weight ratio,

PHS is currently ahead of aluminium.”

Dr Bernd Mlekusch, head of Audi’s Leichtbauzentrum

63Volvo XC40

2018 European Car of the Year, makes use of AHSS and boron steels for safety

Hot-formed boron steel accounts for 20% of the XC40’s total body weight

• The safety cage around the occupants of Volvo’s new XC40 is almost entirely

made from steel including hot-formed boron grades.

• The steel cage provides maximum occupant protection in all types of crash

scenarios.

Volvo Car Group President & CEO Håkan AHSS makes up most of the XC40’s safety cage

Samuelsson at the European Car of the [Images courtesy Volvo Car Group]

Year award ceremony

64RAM pick-up truck

2019 Dodge RAM 1500 frame uses 98% high-strength steel

• “New (Ram 1500) frame features

98% high-strength steel to improve

durability, weight, and rigidity for

improved handling.”

“The new 2019 Ram includes 54% AHSS in the

truck bed and cab, and 98% in the frame, and is

credited with a 225 lb. (102 kg) weight savings

overall, along with 25% fuel economy and 20%

towing capacity improvements,” Mike Manley,

head of Ram brand during 2019 NAIAS press

conference

Source: RAM 1500 announcement

65VAMA greenfield JV facility in China

Well positioned to supply growing Chinese auto market

VAMA: Valin ArcelorMittal Automotive target

• State-of-the-art production facility capacity of 1.5Mt

areas and markets

• Well-positioned to serve growing automotive market

FAW-VW &

• VAMA has successfully completed homologation on UHSS/AHSS BMW

with most key auto OEMs Daimler &

Nissan

Latest developments 2018:

Beijing

• VAMA top products (Usibor® 1500, Ductibor®500, DP980 and

DP780) are approved by large number of end users and sold to

Tier 1 stamper market.

• Overall positive progress in product development and

Geely, VW, GM, KIA,

homologation by auto OEMs. VAMA started series supply of BYD, Changan,

SAIC & Chery

Suzuki, CFMA &

exposed products since 2017Q4 FAW-VW Shanghai

• VAMA received Best Supplier award from International & local Changfeng, Fiat,

stamper DPCA, Dongfeng,

VAMA Honda, JMC & Suzuki

Loudi

SAIC, Toyota, GM,

Honda, Nissan & BYD Guangzhou

• Central office in Changsha with satellite offices in proximity

to decision making centers of VAMA’s customers

Furnace of CGL and CAL on both sides VAMA HQ in Loudi city, Hunan Province

BYD: Build Your Dreams; CFMA: Changan Ford Mazda Automobile; SAIC: Shanghai Automotive Industry Corporation; JMC: Jiangling Motors Corporation 66GROUP HIGHLIGHTS

67Group performance FY18 v FY17

Improved performance driven by positive price-cost effect offset by lower volumes

• Crude steel production decreased by 0.6% to 92.5Mt with decreases in ACIS (-

EBITDA ($ Millions) and EBITDA/t

11.3%, due to operational disruptions in Ukraine and Kaz.) and NAFTA (-3.9%, $102/t $133/t $96/t $99/t $122/t

including BF reline delay in Mexico), offset in part by Brazil (+9.4%, scope effect of

Votorantim) and Europe (2.1%, scope effect of ILVA). +22.1%

• Steel shipments for FY18 were 83.9Mt, - 1.6% vs FY17, primarily due to lower steel -28.5%

shipments in ACIS (-10.3%) offset in part by Brazil (+5.8%, including Votorantim), 10,265

8,408

NAFTA (+1.0%) and Europe (+0.2%, including Ilva offset by impact of a flood in 2,141 2,729 1,951

Asturias (Spain), power outage in Fos (France) and slower ramp-up after BF reline in FY17 FY18

4Q17 3Q18 4Q18

Poland).

• Steel shipments for FY18 excl. Votorantim (in 2Q18) and Ilva (in 4Q18) were 82.5Mt, Average steel selling price $/t

-3.0% vs. FY17, driven by lower ACIS shipments (-10.3%) and Europe (-1.2%), +13.5%

offset in part by Brazil (+0.5%) and NAFTA (+1.0%).

-1.4%

• Sales for FY18 increased by 10.7% to $76bn, primarily due to higher average selling

709 779 768 682 775

prices (ASP) (+13.5%) offset in part by lower steel shipments (-1.6%).

• Impairment charges net of purchase gains for FY2018 were $810m (include $0.7b

primarily related to Ilva and the remedy asset sales for the Ilva acquisition and 4Q17 3Q18 4Q18 FY17 FY18

Votorantim remedies). Exceptional items for FY18 were charges of $117m: $113m in Steel shipments (000’t)

charges related to a BF dismantling in Florange (France), $60m in charges related to

-1.5% -1.6%

the new collective labour agreement in the US (including a signing bonus), a $146m

provision taken in 1Q18 in respect of a litigation case that was paid in 3Q18 offset in

part by PIS/Cofins tax credits related to prior periods recognized in Brazil of $202

20,996 20,538 20,236 85,242 83,854

million.

• EBITDA up 22.1% primarily driven by improved operating conditions (positive price-

cost effect), offset by the impact of lower market priced iron ore prices.

4Q17 3Q18 4Q18 FY17 FY18

68Group performance 4Q18 v 3Q18

Performance declined primarily driven by lower volumes

• Crude steel production decreased by 2.2% to 22.8Mt with decreases in ACIS (-

EBITDA ($ Millions) and EBITDA/t

16.4%, due to operational disruptions in Kazakhstan) and NAFTA (-12.2%, $102/t $133/t $96/t $99/t $122/t

including BF reline delay in Mexico), offset in part by Europe (6.8%, scope effect of

ILVA) +22.1%

• Total steel shipments in 4Q18 were 1.5% lower at 20.2Mt primarily due to lower -28.5%

steel shipments in ACIS (-10.6%, impacted by operational issues in Temirtau, 10,265

2,729 8,408

Kazakhstan), NAFTA (-6.2%) and Brazil (-1.4%), offset in part by a 4.0% 2,141 1,951

improvement in Europe (due Ilva acquisition consolidated Nov 1, 2018). Excluding FY17 FY18

the impacts of Ilva, steel shipments were 4.2% lower as compared to 3Q18

4Q17 3Q18 4Q18

• Sales in 4Q18 declined 1.0% to $18.3bn primarily due to lower steel shipments (- Average steel selling price $/t

1.5%) and lower ASP (-1.4%), offset in part by higher market-priced iron ore +13.5%

shipments (+16.8%)

-1.4%

• Impairment charges net of purchase gains for 4Q18 and 3Q18 were $215m and

709 779 768 682 775

$509m, respectively, and primarily relate to Ilva and the remedy asset sales for the

Ilva acquisition

4Q17 3Q18 4Q18 FY17 FY18

• Exceptional gains for 4Q18 were $29m primarily related to $202 million for

PIS/Cofins tax credits related to prior periods recognized in Brazil, offset in part by Steel shipments (000’t)

$113m in charges related to a BF dismantling in Florange (France), and $60m

-1.5% -1.6%

related to the new collective labour agreement in the US (including a signing

bonus).

• EBITDA declined 28.5% primarily due lower volumes 20,996 20,538 20,236 85,242 83,854

4Q17 3Q18 4Q18 FY17 FY18

69NAFTA performance 4Q18 v 3Q18

Performance declined due to lower steel shipments and negative price-cost effect

EBITDA ($ Millions) and EBITDA/t

• Crude steel production decreased by 12.2% to 5.0Mt in 4Q18, $57/t $135/t $96/t $78/t $112/t

primarily due to market slowdown and blast furnace reline delay

in Mexico +45.1%

-33.2%

• Steel shipments in 4Q18 decreased by 6.2% to 5.2Mt, primarily

due to seasonality and weak market conditions in the US 2,471

744 1,703

292 497

• Sales in 4Q18 decreased by 9.5% to $4.9bn, primarily due to 4Q17 3Q18 4Q18 FY17 FY18

lower steel shipments and lower ASP -1.5% (flat products down

-0.7% and long products down -4.0%) Average steel selling price $/t

+14.8%

• Exceptional charges for 4Q18 were $60m primarily related to -1.5%

the new collective labour agreement in the US (including a

signing bonus) 852

748 896 882 742

• EBITDA in 4Q18 decreased by 33.2% to $496m, primarily due

to lower steel shipment volumes and negative price-cost effect 4Q17 3Q18 4Q18 FY17 FY18

Steel shipments (000’t)

-6.2% +1.0%

5,150 5,512 5,173 21,834 22,047

4Q17 3Q18 4Q18 FY17 FY18

70NAFTA

Improvement

leading producer with 28.1Mt /pa installed capacity

Crude steel achievable capacity (million Mt)

16.3 100.0%

Flat 82.0%

Flat

6.2 5.6

Long Long 18.0%

USA Canada Mexico NAFTA

Number of facilities (BF and EAF)

NAFTA No. of BF No. of EAF

USA 7 2

Canada 3 4

Mexico 1 4

Total 11 10

Note: IH Bar facility closed in June 2015; Georgetown wire rod facility closed in August 2015, Vinton and LaPlace sold in 2Q 2016 71Brazil performance 4Q18 v 3Q18

Performance declined primarily due to a negative price-cost effect

EBITDA ($ Millions) and EBITDA/t

• Crude steel production increased by 1.0% to 3.2Mt in 4Q18 $112/t $144/t $92/t $91/t $134/t

• Steel shipments in 4Q18 decreased by 1.4% to 3.1Mt, driven +55.4%

by seasonally weak domestic demand -37.2%

• Sales in 4Q18 increased by 15.5% to $2.4bn, due to the 445 990

1,538

341 280

negative impact of hyperinflation accounting in Argentina in

3Q18 (recorded as a nine-month year-to-date accumulated 4Q17 3Q18 4Q18 FY17 FY18

impact), offset in part by lower ASP (-3.7%) and lower steel

shipments (-1.4%). Average steel selling price $/t

+7.7%

• Exceptional gain for 4Q18 was $202m related to PIS/Cofins tax -3.7%

credits related to prior periods recognized in Brazil.

685 714 687 667 719

• EBITDA in 4Q18 decreased by 37.2% to $280m, primarily due

to a negative price-cost effect. 4Q18 includes a one-time

provision of $17 million for employee related charges in Brazil. 4Q17 3Q18 4Q18 FY17 FY18

Steel shipments (000’t)

-1.4% +5.8%

3,052 3,097 3,053 10,840 11,464

4Q17 3Q18 4Q18 FY17 FY18

72You can also read