Growth in Africa: The opportunity beyond beer - Distell

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Forecasting the future

Growth in Africa:

The opportunity beyond beer

DECEMBER 2019

14|03|2017

I N T E R I M F I N A N C I A L R E S U LT S

Creating memorable moments.

A S AT 3 1 D E C E M B E R 2 0 1 8

Crafting a better future.

Our brands

Our top 15 brands generate 70,2% of total revenue and have recorded strong growth

Hunter’s Savanna Bernini Amarula Gordon’s Gin Klipdrift Richelieu

Scottish Leader Three Ships Viceroy 4th Street Autumn Harvest Drostdy-Hof Nederburg Original

Crackling Paarl Perlé

1 4 | 0 3 | 2OF

OUR REPERTOIRE 0 1 BRANDS:

7

Resonates with a broad spectrum of consumers with different taste profiles; plays across the price continuum; and

is enjoyed at mixed-gender drinking occasions worldwide.

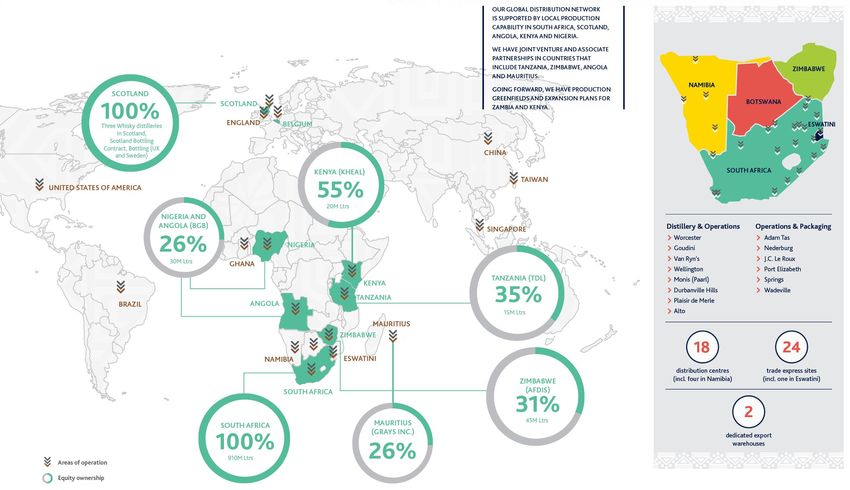

WHERE WE OPERATE

14|03|2017

Africa macro dynamics

Key facts

Strong population growth

• Represents 16% of the world’s population but consumes 5% of the

• 1.3 billion people, growing to 2.5 billion world’s beverage alcohol

by 20501

• Ave alcohol consumption: 6l vs. 6.3l global average

• 2.4% p.a. growth in the short term2

• 65% of global population growth

• 19 years median age of population GDP 2018 ($bn) GDP growth ('18 - '23)

Mozambique 14

Rapid urbanisation Zambia 26

Zambia 1,5%

• Urban population to grow from 41% South Africa 2,1%

Kenya 88

Nigeria 2,6%

to 59% from 2015 - 2050 Angola 114

Mozambique 3,3%

South Africa 368

Improved (known) political stability Angola 4,0%

Nigeria 422 Kenya 5,7%

• Heavy election schedule in 2019/2020

• Rising number of democratic regimes Grocery spend 2018 ($bn) Population (mm)

Emerging middle class / consumer demand Algeria 31 Kenya 51

Angola 39 Tanzania 56

• 376 million to 582 million people from 2013 - 2030

South Africa 61 South Africa 57

Egypt 67 Egypt 97

Strong positive GDP outlook into the mid & long-term

Kenya 77

• 3.7% p.a. real growth long term2 Ethiopia 109

Nigeria 80

Nigeria 196

Source: UN World Population Prospects 2018; McKinsey Global Institute “Lions on the move – realizing the potential of Africa’s

economies; Deloitte – The Deloitte Consumer Review Act: A 21st Century view; Deloitte – African Powers of Retailing, New horizons for

Growth; Oxford Economics; EIU: Africa Trade Report 2018; International Trade Centre (ITC)

1 As compared to 2015 population. 2 2018 – 23 CAGR

African growth & share trends

KENYA

%Chg Volumes %Chg Volumes

NIGERIA

Region 2013 - 2018 2018 - 2023

56 Central America 32.4% 22.3%

40 48 48

Middle East 17.4% 16.7%

2 Africa 10.3% 12.0%

13 2

South America -4.5% 7.7%

Southern Europe 10.5% 6.7%

GHANA*

1

Nordic Countries 1.4% 6.6%

26 23 76 Central Europe and

Balkans 1.6% 5.5%

3 Caribbean 6.5% 4.1%

68 2

ANGOLA

Asia -8.2% 2.6%

TANZANIA

Australasia -0.1% 1.7%

30

North America 1.2% -0.8%

1 18 North West Europe -0.9% -1.2%

5

64 2 CIS -16.8% -6.4%

3 77

Eastern Europe and

Baltics -10.8% -20.6%

4 8 18

MOZAMBIQUE

* In mature developed markets beer 53 The total African alcoholic beverage market is

share of LAA drops down to average 58 9

30%-40%. Ghana is an exception, as 29 expected to grow by 12% in volume by 2023 –

bitters (traditional drink) is massive. 19 more than double Europe as well as other

NAMIBIA SOUTH AFRICA

Source: IWSR / Distell Source: IWSR developed markets in decline.

Addressable market sizes

South Africa’s has the 2nd largest addressable alcohol market after Nigeria. Despite its size and

attractiveness for investment, growth in household incomes and market size will lag the likes of Nigeria

CORE ADDRESSABLE POPULATION*

Country, Million, 2018, 2023

8

7

Investment Attractiveness Score

South Africa

8.9; (10.7) Ethiopia

Nigeria Kenya

6 Tanzania

1.8; (3.5) 0.40; (1.5)

17.8; (24.7) 1.2; (2.4)

1.8; (3.1) 1.5; (3.0)

Zambia Ghana Ivory Coast

5 0.45; (0.64)

1.8; (2.6)

Angola Mozambique

4 The core addressable Total

0.16; (0.48)

market is the alcohol Adult

consuming adult

Alcohol Consuming Adults

population excluding

the marginalised class Core Addressable Population

3

0,0 0,5 1,0 1,5 2,0 2,5 3,0 3,5

Household income growth (%), 2019-2023, constant local currency, 2005

6

*Core addressable population excludes population segment that are considered as marginalised ( Population that cannot afford branded goods on a regular basis). However, they may make infrequent purchases

Sources: CGIDD; WHO; Deloitte analysis, RMB

Spirits, wine and RTDs 50% of consumption but growing

ahead of beer

Most of the alcohol consumption growth in leading Africa markets will come from value & standard price segments, as the

informal/unrecorded segment declines – with premiumization being a strong longer term opportunity

ANGOLA ((MILLION LITRES

NIGERIA ((MILLION LITRES

5 YR 5 YR

ABSOLUTE ALCOHOL)

+2,4% CAGR CAGR

ABSOLUTE ALCOHOL)

+4,1%

99 186

90 6 0 2

3 Spirits 3.3% 158 15 Spirits 3.7%

11

RTDs 2.1% RTDs -0.1%

Spirits Wine Spirits Wine

Wine 1.1% Wine 2.7%

RTDs Beer RTDs Beer

Beer 1.6% Beer 3.1%

2019 Value Standard Premium 2023 2019 Value Standard Premium 2023

KEY DRIVERS

KENYA ((MILLION LITRES

5 YR

ABSOLUTE ALCOHOL)

+5,9% CAGR

71 Premiumisation: Shift from

2 1 informal to branded items

Spirits 6.2%

56 11

Rise of female consumers

RTDs 6%

Mixed gender occasions

Spirits Wine

RTDs Beer

Wine 4.9% Income growth broadens

repertoire beyond beer

Beer 2.8%

Beer share of alcohol can

2019 Value Standard Premium 2023 drop to 30%-40% as markets

Note: RTDs excludes Beer mature

Source: GlobalData, IWSR

Key consumer trends in Africa

As markets mature in Africa,

alcohol consumption is set to

01 Female consumption

•

•

To grow significantly with economic participation

Mature markets = 4 litres LAA per capita & 2 litres in low income countries

grow and expand in repertoires & • Cider/RTD’s trends growing whilst brands offering more options targeted at females

demographics

02 Premiumisation

• Per capita consumption increase & growth in value (60% higher in mature markets vs. low

income markets)

• Informal liquor decline as formalisation grows with branded goods

03 Consumer repertoire expanding beyond beer

•

•

Beer = 65% of absolute alcohol consumed in Africa – can reduce to 45% as markets mature

Wine: Key entry level category to win share from beer

• Whisky established as a category; showing good growth potential

04 Pack Size and Flavour options

• Beers moving to shared pack formats; RTD’s & FABs introducing more flavour options

Total Brand Experiences

05 •

•

Increased foreign competitor activity resulting in more personalised brand experiences

Local insight and brand investment driving choice

The female opportunity

Internationally:

• Females represent 85% of consumer buying decisions

• Considered the largest market opportunity in the world

• Controlling $20 trillion in annual consumer spending globally

• Expected to rise to $30 trillion within next 5 years

• Influencing drink choices of male counterparts through the consolidation of a

more unisex drinking culture

South Africa:

• 21-million female consumers expected in local market by 2025

• Will increase labour force participation

• Currently 9.5-million (2019) >> 11-million (by 2025)

• Increasing this segment’s spending power

• Strong bottle-serve culture, but making collective decisions on drinks

favouring vodka, gin, Cognac, cider, champagne and wine.

Females represent an exciting opportunity based on

unmet needs-SA segmentation example

Currently satisfied by Female-specific and mixed More potential exists to delight Distell’s approach to winning

traditional offers gender demand moments unmet needs with female consumers

OFF PREMISE, MIXED GENDER OCCASIONS

• Open to unique and

Close Connections Savour & Treat time unusual taste

experiences,

• Desire to explore &

Bold experiment.

Interpretations

Ciders/FABS

• Health & Wellness

Weekend Release

• Manifestations of

moderation offer

Mindful

Consumption

Spirits

ON PREMISE, FEMALE-SPECIFIC OCCASION Building meaningful Brand and marketing

connections in a hyper

offerings tapping into trends:

connected & digital world

amplifying premium - Engaging brand

credentials, purpose and propositions

Real brand story-telling

Connections - Tailored offerings

Wines

Girl’s Night OutSignificant opportunity for leading female empowerment

indicators to improve: SA vs. rest of Africa

• Bar religion & societal norms, the most important driver of future female consumption is financial freedom

• 1. Access to secondary education; 2. Being employed; and 3. Earning a good salary

LABOUR FORCE

GENDER INEQUALITY ESTIMATED EARNED ACCOUNT AT A FINANCIAL POPULATION WITH SECONDARY

PARTICIPATION

INDEX INCOME INSTITUTION EDUCATION**

20I7 20I5, ‘000 PPP$ 20I5

RATE* 2005-2015

2005-2015

United States 0.189 43.9 95.0% 55.7% 95.5%

Kenya 0.549 2.5 52.0% 62.4% 29.2%

Tanzania 0.537 2.3 17.0% 79.5% 11.9%

Ethiopia 0.502 1.3 21.0% 77.2% 11.2%

South Africa 0.389 9.1 69.0% 47.9% 74.2%

Angola N/A 5.1 22.0% 75.3% N/A

Nigeria N/A 4.4 34.0% 50.4% N/A

• In terms of gender inequality index, Kenya has an index score of 0.55 and is the highest of Distell’s African countries indicating a generally marginalized female workforce in terms of income

• The population of females with secondary education was 29.2% on average, and this is expected to continue to grow into the future indicating a growing base of informed female cohort that could

generate a market for Distell in the future once income levels and biases improve

*Include female population above age 15+

**Include female population above age 25+

Source: United Nations Development Programme (UNDP)Our Africa performance -June 2019 results

SOUTH AFRICA AFRICA (excl SA) KWA Holdings EA

incl BLNS excl BLNS

-0,9% +56%

+10,3% +28,6% Volume

Volume

Volume Volume

+47%

+9,5% Revenue

+20,0% +40,7%

Revenue Revenue Revenue • Growth driven by mainstream spirits and

wines led by Kibao, Hunters Choice, Cellar

Cider & RTD revenues up 11,5%

Cider & RTD Revenues up 15,6% Cask & 4th Street

• Led by Savanna, Extreme and Bernini

Spirit Revenues up 37,2% • Acquired property in Tatu City to double

• Successful Esprit launch

Wine Revenues up 11,3% local production capacity

Spirit Revenues up 11,6%

• Doubled revenue and tripled EBITDA since

• Strong double-digit growth from Vodka and • Exceptional double-digit volume and revenue acquisition

Gin led by Cruz, Old Buck and Gordon's growth across all key markets except Angola

• High single-digit Whisky growth led by and Namibia KES Jun-15 Jun-19

Bain's, Scottish Leader and Harrier • Growth in Spirits category led by Kibao, Volumes ('000 Li) 9,077 14,998

• Brandy under pressure due to pricing Hunters Choice & Best Whisky

Wine Revenues up 3,2% • 1 4led|by0 Savanna

RTD growth 3 | 2 0&1Hunter’s

7 Revenue 4,419,091 8,184,556

• Growth from Drostdy-Hof and Nederburg • Nigeria & Kenya additional local production EBITDA 261,394 1,013,136

• Volumes impacted by pricing (input costs) established; Angola & Ghana planned

EBITDA % 5.9% 12.4%

Margin improvement in all 3 categoriesInvesting behind an African manufacturing footprint

FUTURE DEVELOPMENTS

• SA: Northern Mega DC R1610m

• Africa: Angola & KWAL Tatu City CAPEX

• Mozambique & Zambia 2015 - 2019

SA CAPACITY BUILD

investigation 480m L/pa cider

70m L/pa BIB

60 m L/pa RB

50 m L/pa NRB

NIGERIA KENYA

ANGOLA

WADEVILLE

14|03|2017

NEDERBURG SPRINGSKey lessons from Africa

Local brands key

Building local RTM & customer affinity

Local Production vs. Export model

Africa not one continent

Prudent risk management is imperative

Measured capital allocation – not betting the farm

Local partnerships to ensure localisation & beneficiationYou can also read