Investor Information SUPPLEMENTAL - Published May 3, 2021 - Suncor

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SUNCOR ENERGY Investor Information SUPPLEMENTAL Published May 3, 2021 SUNCOR ENERGY

Table of Contents 1. Energy Sources 2. Processing, Infrastructure & Logistics 3. Consumer Channels 4. Sustainability 5. Technology Development 6. Integrated Model Calculation 7. Glossary SUNCOR ENERGY 2

SUNCOR ENERGY

Appendix

Energy

Sources

3

202003-038

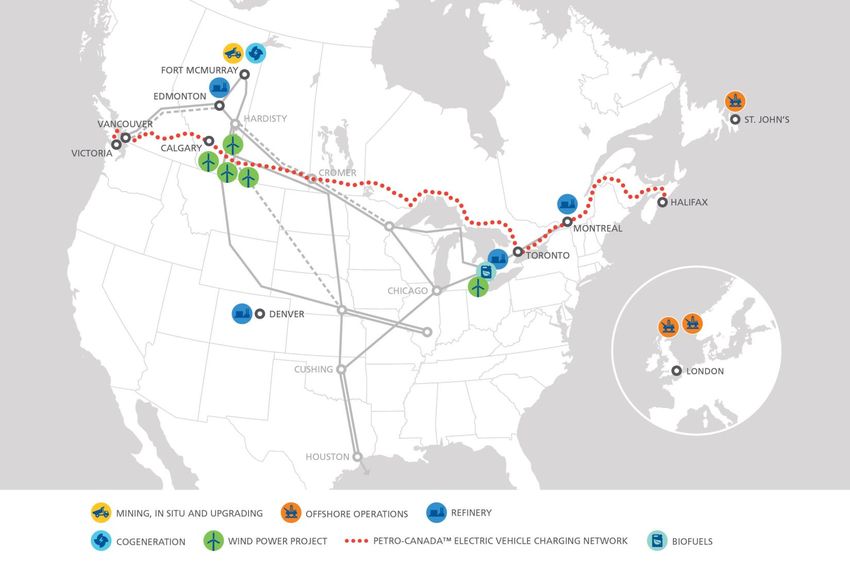

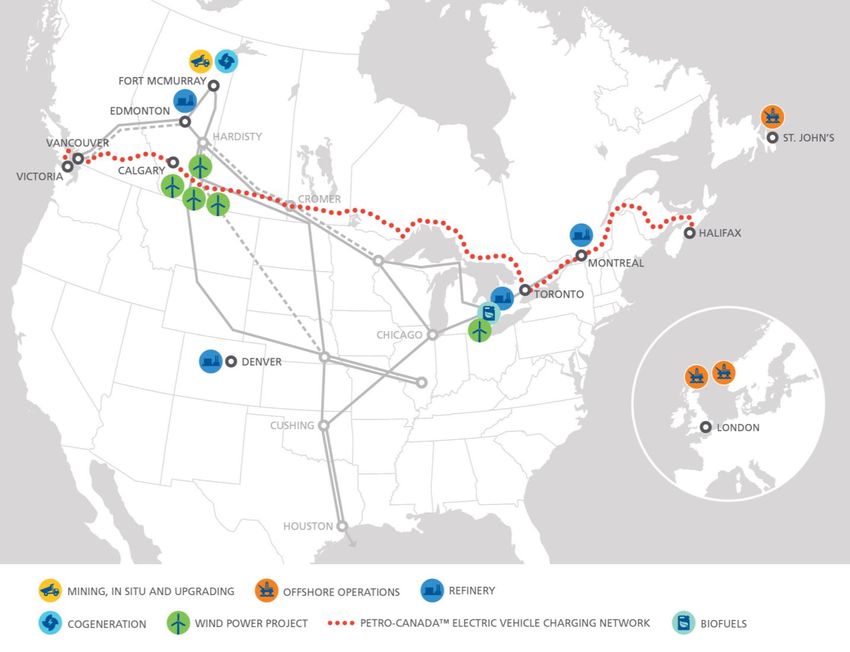

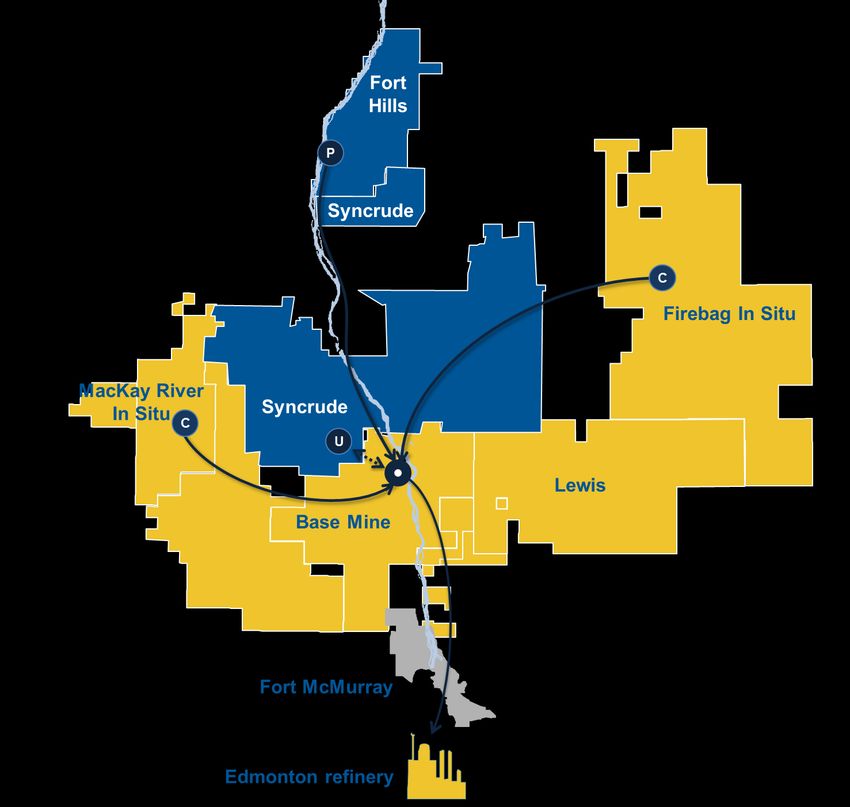

Oil Sands Energy Sources

*All values net to Suncor

In Situ Mining

Firebag Base Plant

215,000 bpd capacity 350,000 bpd capacity

Suncor WI 100% Suncor WI 100%

2,743 mmbbls 2P reserves1 1,246 mmbbls 2P reserves1

Note: Millennium and North Steepank Mines

do not supply full 350,000 bpd of capacity

as significant in-situ volumes are sent

through Base Plant

MacKay River Syncrude

38,000 bpd capacity Syncrude operated

Suncor WI 100% 205,600 bpd net coking capacity

497 mmbbls 2P reserves1 Suncor WI 58.74%

1,160 mmbbls 2P reserves1

Future opportunities Fort Hills

ES-SAGD Firebag Expansion Suncor operated

Lewis (SU WI 100%) 105,000 bpd net capacity

Meadow Creek (SU WI 75%) Suncor WI 54.11%

1,418 mmbbls 2P reserves1

First oil achieved in January 2018

SUNCOR ENERGY 1 See Slide Notes and Advisories. 4

Regional synergy opportunities1 for existing assets

Crude logistics

Upgrader feedstock optionality from multiple oil sands assets

Crude feedstock optionality for Edmonton refinery

Supply chain

Sparing, warehousing & supply chain management

Consolidation of regional contracts

(lodging, busing, flights, etc.)

Operational optimizations

Unplanned outage impact mitigations Situ

In Situ

Turnaround planning optimization

Process and technology sharing

100% WI

Joint ownership

Base mine upgrader and terminal

U Syncrude upgrader

Assets and resource developments C In situ central processing facility

Lease development and asset utilization optimization P Fort Hills primary/secondary extraction

Pipelines

SUNCOR ENERGY 1 See Slide Notes and Advisories 5

Long life, low decline reserves base

Typical attributes1 of North American oil plays

Initial Decline Sustaining Operating Reservoir Recovery

Illustrative annual FFO2 profiles3 capital rate costs cost risk factor

Mining High Very low Low Medium Very low Very high

~90% of Suncor’s 2021

production guidance

In Situ Medium Low Low Low Low High

Offshore

~10% of Suncor’s 2021 High Medium Medium Very low Medium Medium

production guidance

Tight Oil Low Very high High Medium High Low

50 Years

Beneficial attribute Challenging attribute

SUNCOR ENERGY 1, 2, 3 See Slide Notes and Advisories 6

Offshore with ~300 million barrels of 2P reserves1

East Coast Canada North Sea

Hibernia

ExxonMobil operated Buzzard (UK)

Suncor working interest 20% CNOOC Petroleum Europe Limited operated

73 mmboe 2P reserves1 (Suncor WI) Suncor working interest 29.9%

2020 avg net production: 23.2 mbbls/d 60 mmboe 2P reserves1 (Suncor WI)

2020 avg net production: 25.9 mboe/d

Hebron

ExxonMobil operated

Suncor working interest 21.0% Golden Eagle (UK)

113 mmboe 2P reserves1 (Suncor WI)

CNOOC Petroleum Europe Limited operated

2020 avg net production: 29.7 mbbls/d

Suncor working interest 26.7%

12 mmboe 2P reserves1 (Suncor WI)

2020 avg net production: 7.8 mboe/d

Terra Nova Divestiture announced - effective Jan 1, 2021

Suncor Energy operated

Suncor working interest 37.7%

19 mmboe 2P reserves1 (Suncor WI)

Oda (Norway)

2020 avg net production: 0 mbbls/d

Spirit Energy operated3

Suncor working interest 30%

3 mmboe 2P reserves1 (Suncor WI)

White Rose First oil achieved March 2019

Cenovus operated 2020 avg net production: 7.5 mboe/d

Suncor working interest 27.5%2

4 mmboe 2P reserves1 (Suncor WI)

2020 avg net production: 6.7 mbbls/d

SUNCOR ENERGY 1, 2, 3 See Slide Notes and Advisories 7

E&P – Investing in high value, low risk projects

Recent performance Sanctioned projects1

mboe/d Fenja (Norway)

120 • 17.5% working interest

Oda • 6 mbbls/d anticipated net peak production

100 Hebron

White Rose

80

Hibernia

Buzzard Phase 2 (UK)

60 Terra Nova • 29.9% working interest

Golden Eagle • Production anticipated to offset natural declines

40 Buzzard

20 West White Rose Project4 (ECC5)

• ~26% working interest

0

2012 2013 2014 2015 2016 2017 2018 2019 2020

• 20 mbbls/d anticipated net peak production

$billions Terra Nova Asset Life Extension4 (ECC5)

2.5 112 109

99 • 37.7% working interest

• Extend asset life by approximately a decade

2.0

• Expect to produce additional 30 million barrels

64 (Suncor WI)

1.5 71 FFO2

Free funds flow3

54 Capital spend

52

1.0 44 42 Brent ($US/bbl) Future opportunities

0.5

• Rosebank – UK (40% Suncor WI)

• Near field developments including subsea

-

tie-backs, field extensions and infill drilling

2012 2013 2014 2015 2016 2017 2018 2019 2020

SUNCOR ENERGY 1, 2, 3, 4 See Slide Notes and Advisories 8

Power Generation

Generating power for internal use & sale to the grid, including EV

applications; currently 5th largest power producer in Alberta.

2,400

MW

1,400

MW

CURRENT CURRENT + SANCTIONED PROJECTS1

Cogen: 96%; Renewables: 4% (online by YE 2025)

Cogen: 89%; Renewables: 11%

MW Working interest nameplate capacity

Net capacity for grid export

Net internal consumption

SUNCOR ENERGY 1 See Slide Notes and Advisories. 9

SUNCOR ENERGY

Appendix

Processing,

Infrastructure &

Logistics

10

202003-038Operations & Consumer Network

29 year

Oil Sands

Reserve Life

Index1

~25 mmbbl

storage

Western

Canada

~1,875

PetroCanada

sites2 ~15 mmbbl

storage

Eastern

Canada

Only

refinery in

Colorado

~10 mmbbl

storage

Central US &

Gulf Coast

OIL & REFINED PRODUCT STORAGE (SUNCOR OPERATED)

CURRENT PIPELINES PROPOSED PIPELINES3

SUNCOR ENERGY 1, 2, 3 See Slide Notes & Advisories 11Upgrading

Upgrading processes heavy bitumen into a

lighter, higher value product with a density Upgrading Process

similar to that of WTI.

LOW

Once upgraded, the product can flow on a VALUE

Mined & In-Situ Bitumen

HEAVY

pipeline without the addition of diluent. OIL (10° API)

Total Suncor Net

Upgrading Capacity: ~555 kbpd1

Coking, hydroconversion,

• Base Plant thermal cracking &/or

~15 – 20% yield loss

– 2 Upgrading Units hydrocracking

through upgrading process

• U1: 110 kbpd

• U2: 240 kbpd

– Produces sour & sweet SCO & diesel

HIGH Sour Synthetic Crude Oil Optional: Hydrotreating

• Syncrude (Gross values below – Suncor WI 58.74%) VALUE (30 - 35° API) (remove sulfur)

LIGHT

– 3 Upgrading Units OIL

• U1: 100 kbpd

• U2: 100 kbpd

• U3: 150 kbpd Sweet Synthetic Crude Oil

Refinery

– Produces sweet SCO (30 - 35° API)

• Edmonton Refinery

– 30 kbpd coking capacity

SUNCOR ENERGY 1 See Slide Notes & Advisories 12Suncor’s proven oil sands reliability journey

Suncor Base Plant upgrader reliability

Multi-year journey to reach >90% reliability

91% 90%

1 91% 90%

2

90%

86%

83% Firebag to

81% Base Mine

79% interconnect

pipeline fully

operational

Suncor began focusing on upgrader reliability initiatives in 2011

Culture – Operational excellence mindset

Process – Integrated maintenance strategy/approach

Infrastructure – Asset integration between Firebag and Base Plant

2012 2013 2014 2015 2016 2017 2018 2019 2020

Syncrude plant reliability In 2019, Syncrude achieved 2nd best

annual production in asset’s history

A similar multi year journey targeting >90% reliability 3

with 85% utilization4

2016/17 2018/19 >2021 (Target >90% reliability)

Collaboration Culture Infrastructure

Suncor’s active involvement in 31 technical/management Two bi-directional pipelines connecting Syncrude & Suncor’s Base Plant

Syncrude’s reliability secondees from Suncor sharing

improvement plan operational discipline learnings Better utilization of existing assets:

• Normal operations - Transfer of sour synthetic and bitumen between assets

• Planned and unplanned outages - Asset and production optimizations

Sharing technical & reliability Process synergies

best practices and support to Leveraging service & materials Construction completed and in-service in Q4 2020

improve productivity, reliability economies of scale

and reduce costs Maintenance planning & execution

coordination

SUNCOR ENERGY 1, 2, 3, 4 See Slide Notes & Advisories 13Market Access

Suncor has made strategic investments in refineries and current/proposed

logistics infrastructure to mitigate Alberta egress limitations & market disconnects

Fort McMurray ~750 Alberta

egress bottleneck

does not impact

the ability to move

Suncor barrels1

146 Edmonton

Hardisty Enbridge Line 3

Potential Markets

Regina Central & Eastern

Vancouver Cromer Canada, US Midwest

& Gulf Coast

137

Montreal

TMEP Potential Superior

Markets

Asia & California 85

Sarnia

Steele City Chicago

98

Commerce

Patoka

City

San Francisco

Cushing

Los Angeles

Pipelines

(current and forecasted gross capacity2)

Feeder lines

Houston/Texas City Trans Mountain Pipeline, TMPL (300 mbpd)2

Suncor refinery capacity

mbpd Trans Mountain Expansion , TMEP – Proposed3 (+590 mbpd)2

Industry approximate rail Express, Platte and Rocky Mountain (280 mbpd)2

mbpd loading capacity in TransCanada Keystone (590 mbpd)2

AB/SK

Enbridge Mainline (2,600 mbpd)2

Enbridge Line 3 – Proposed3 (+370 mbpd) 2

Enbridge Line 9 (300 mbpd)2

Flanagan South Pipeline (585 mbpd)2

Marine opportunities

SUNCOR ENERGY 1, 2, 3 See Slide Notes & Advisories 14SUNCOR ENERGY

Appendix

Consumer

Channels

15

202003-038Refined Product Markets

~500 mbpd

Product sales in

20201 Edmonton

refinery services

region from BC

to Ontario

20% Montreal and

Sarnia have a

local market

Canadian reach over 22mm

Export

consumer fuel capability

people5

market2 to US

Pacific NW

~315

Wholesale Cardlock

Locations3 Commerce

City’s asphalt Commerce City is

market only refinery in

stretches into Colorado & largest

Utah & Nevada 44 owned

refinery in the US

~1,560 retail

stations in Rockies

PetroCanada CO

retail sites4

~50%

North American

retail sites Suncor

owned

SUNCOR ENERGY 1, 2, 3, 4, 5 See Slide Notes & Advisories 16Refinery Feedstock & Products1

2020 refinery feedstock 2020 refined products

(~40% equity feedstock & ~100% inland crude)

1%

4% 6%

8% 10% 5% 5% 6%

8%

14%

10% 10%

20% 6%

37% 30%

59% 50%

52%

37%

34% 42%

76%

37%

21%

36%

22%

28%

48% 46%

42% 42%

4% 34% 35%

24% 22%

16%

12%

Montreal Sarnia Edmonton Denver Total Montreal Sarnia Edmonton Denver Total

Heavy Sour Sweet Other Feedstock Asphalt

Other (Bunker, Chemicals, LPGs, etc.)

Distillates (Diesel & Jet Fuel)

Gasoline

SUNCOR ENERGY 1 See Slide Notes & Advisories 17Refinery Characteristics

Throughput Nelson %OS Crude

Refinery Capacity Complexity Processing Key Markets Feedstock Advantages Product Advantages

(mbpd) 1 Index Rating Ability

Western Directly connected to oil sands production; ability Large market reach with international export capability via

Edmonton 146 9.8 100%

Canada to process multiple crude types. tidewater; in-line product blending minimizes inventory.

Integrated with Montreal refinery to supply large local market

Tied into western market for oil sands crude; crude

GTA & in the surrounding area; Sarnia refinery has a partial

Sarnia 85 10.8 80% source flexibility between mid-west and oil sands

Midwest USA ownership in refined products pipeline to the Greater Toronto

crude.

Area; direct access to international waters.

Large tanks storage capacities for crude and finished products;

access to large domestic markets through pipelines, rail and

Strong feedstock optionality with access to Western

Montreal & trucking; ability to optimize feedstock to Montreal and Sarnia

Montreal 137 9 30% Canadian, US, and tidewater crudes via pipeline, rail

GTA refineries as well as products to Ontario and Quebec; synergy

and marine.

with Parachem (chemicals market) and access to international

waters.

Bulk of crude from Colorado and local basins

Commerce Supplies 1/3 of jet fuel used at Denver International Airport via

resulting in transportation and pricing advantages;

City 98 7 20% Colorado direct pipeline; Colorado's largest producer & supplier of

optionality for North Dakota, Wyoming, Montana &

(Denver) paving-grade asphalt.

Western Canadian crude.

OS = Oil Sands

GTA = Greater Toronto Area

SUNCOR ENERGY 1 See Slide Notes & Advisories 18Refining & Marketing

R&M funds from operations1 Refinery utilization vs. US average

Capturing the value at all differentials Percent of refining capacity

FFO1 ($C billions) WTI – WCS ($US/bbl) Suncor US Average2

Full turnaround at

$4 $28 100% the Edmonton

refinery Q2 2018

$3 $21

90%

$2 $14

80%

$1 $7

US$/Cdn$

FX > $0.90

(2012 – 2014)

$0 $0 70%

2012 2013 2014 2015 2016 2017 2018 2019 2020 2012 2013 2014 2015 2016 2017 2018 2019 2020

SUNCOR ENERGY 1, 2 See Slide Notes & Advisories 19Suncor 5-2-2-1 Index

To help investors and analysts model Suncor’s Refining and Marketing (R&M) business, we have designed an indicative

5-2-2-1 gross margin based on publicly available pricing data. This is a single value that incorporates refining, product

supply and rack forward businesses, but excludes the impact of first-in, first-out (FIFO) accounting.

Q1 2019 Example

Gross Margin WTI + NYH 2-1-1 73.15 40% 29.26

= Product Value – Crude Value WTI + Chicago 2-1-1 70.25 40% 28.10

WTI 54.9 20% 10.98

Product Value Seasonal Factor 6.50

Product Value ($US/bbl) 74.85

= NYH 2-1-1 (40%) + Chicago 2-1-1 (40%) + WTI (20%) + Seasonal Factor

SYN 52.6 40% 21.04

WCS 42.5 40% 17.00

Crude Value WTI 54.9 20% 10.98

= SYN (40%) + WCS (40%) + WTI (20%) Crude Value ($US/bbl) 49.00

Gross Margin ($US/bbl) 25.85

FX ($US/$C) 0.75

New York Harbor (NYH) 2-1-1 & Chicago 2-1-1 Average Refinery Production (mbbls) 44,000

1

These regional benchmark cracking margins are indicative of Gross Margin excl-FIFO ($C millions) 1,515

Suncor’s western and eastern refining margins. Each 2-1-1 formula

represents the spread between 2 barrels of WTI crude oil and 1 Edmonton

barrel each of gasoline and ULSD. WTI is added to cracking Turnaround

margins to represent full product value.

Seasonal Factor

An estimate of USD $6.50/bbl in Q1/Q4 and USD $5.00/bbl in

Q2/Q3 reflect the grade quality and location spreads for refined

products sold in the company’s core markets during the winter and

summer months, respectively.

WTI = West Texas Intermediate crude oil at Cushing

SYN = Sweet Synthetic crude at Edmonton

WCS = Western Canadian Select at Hardisty

(CAD millions)

SUNCOR ENERGY 1 See Slide Notes & Advisories 20R&M gross margin calculation example – Q1 2019

FIFO1 impact calculation example – Q1 2019

Q4 2018 Q1 2019

Dec-18 49.00 70% 34.30 Dec-19 58.15 70% 40.71

WTI ($US/bbl) 60% 30.79 60% 34.32

Nov-18 56.70 30% 17.01 Nov-19 55.00 30% 16.50

Dec-18 6.00 70% 4.20 Dec-19 48.20 70% 33.74

WCS ($US/bbl) 20% 1.50 20% 9.47 Q1 2019 vs. Q4 2018

Nov-18 11.05 30% 3.32 Nov-19 45.35 30% 13.61

SYN ($US/bbl)

Dec-18 17.70 70% 12.39

20% 4.52

Dec-19 58.30 70% 40.81

20% 11.45

FIFO gain of

Nov-18 34.10 30% 10.23 Nov-19 54.80 30% 16.44 US$460M/C$615M

Average inventory cost/bbl 36.81 55.24

Inventory barrels1(mmbbls) 25 25

Inventory Value ($US) 920 1,381

Realized GM/bbl vs. NYH 2-1-1 benchmark – Q1 2019 49.65

All Suncor refineries

35.25

25.39

19.10

NYH

NYH 2-1-1

2-1-1 C$

US$

Benchmark Benchmark Crude Product mix, location Realized FIFO impact Realized

crack crack differential differential & other GM (LIFO) GM (FIFO)

SUNCOR ENERGY 1 See Slide Notes & Advisories 21First-in, first-out (FIFO) inventory gains and losses

Crude & products inventory & timing

The amount of time between purchase of feedstock to sale of refined product has direct correlation to FIFO impact

Edmonton

Commerce City

Montreal / Sarnia

45

Average (~ 1.5 months)

Average number of days

Crude logistics time1 – Time between purchase of feedstock to receipt at refinery gate in inventory across

Products storage time1 – Time between product processed and shipment beyond refinery gate refineries1

*Transit & storage time will vary depending on market & operating conditions

Composition of average inventory barrel FIFO impact

Illustration of how to calculate prices used for FIFO impact Key rules of thumb

Commodity mix in inventory1 The change in inventory value each quarter

indicates the magnitude of the FIFO impact

Prior reporting Current reporting

quarter price quarter price

A decrease in inventory value reflects a loss

WTI (~60%)

70% 70% Associated with a decreasing business environment

last month of the last month of the

quarter price quarter price

An increase in inventory value reflects a gain

WCS (~20%) Associated with an increasing business environment

30% 30%

Middle month of the SYN (~20%) Middle month of the

quarter price quarter price

SUNCOR ENERGY 1 See Slide Notes & Advisories 22SUNCOR ENERGY

Appendix

Sustainability

23

202003-038Water Stewardship

Our water use is guided by three principles

Conserve Reuse & recycle Return clean water to watershed

Corporate fresh water consumption intensity (m3/m3 production)2

0.90

0.82 0.86

1 0.74

Impact of 2016 Fort Hills

wildfires ramp-up

0.46

Oil Sands MacKay

Firebag

Base Plant River Base Plant optimization

& sale of lubricants business

92% 96% 100%

2015 2016 2017 2018 2019

Water technology highlights3

Water Technology Development Centre High Temperature Reverse Osmosis Non-aqueous extraction

$145M collaboration at Firebag to accelerate Project to develop treatment membranes that New solvent technologies in mining could

wastewater treatment technologies. could reduce the infrastructure & energy reduce or eliminate the need for water and

2019 JWN Energy Excellence required for SAGD4 water treatment tailings ponds and reduce GHG intensity

Awards winner.

SUNCOR ENERGY 1, 2, 3, 4 See Slide Notes & Advisories 24Tailings Management Tailings Composition

With the growth of Oil Sands Base operations, the volume of fluid

tailings has increased over time fines/clay 3%

Previous fluid tailings treatment methods kept volumes stable & water

allowed us to reclaim a tailings pond & make another one trafficable 76% sand

20%

PASS1 is a step-change to treat all fluid tailings by 2043

Base Plant Tailings Treatment Profile2 bitumen 50%2

Oil sands reclaimed

400

Stability

(treatment = production) 1st tailings pond –

Wapisiw Lookout (2010)

200 2019 volume of tailings

2.3x treated vs. tailings

0

produced4

Commercially implemented in 2018, PASS technology is expected to treat >50% of tailings volumes,

fast-tracking reclamation, reducing our environmental footprint & lowering costs2

SUNCOR ENERGY 1, 2, 3, 4 See Slide Notes and Advisories 24Personal & Process Safety

Positive trends in process safety, continued focus on personal safety

Loss of Primary Containment (LOPC) Recordable Injury Frequency (RIF1)

Tier 1 and Tier 2 process safety events Injuries per 200,000 hours worked

200 0.6

150

0.4

100

0.2

50

0 0

2015 2016 2017 2018 2019 2015 2016 2017 2018 2019

Suncor and contractor RIF 5-year trend

LOPC 80% decline in process safety events over the last 5

years (180 to 38)

Lost Time Injury Frequency (LTIF2)

Injuries per 200,000 hours worked

RIF1, LTIF2 improving over time, but

0.06

2019 performance above trend

RIF performance decline led by hand injuries; mitigation 0.04

measures focused on root causes, corrective/preventive

action and communication of incident learnings

0.02

LTIF performance decline led by slips, trips and falls and

line of fire incidents; mitigation measures focused on safety

processes, PPE, mandatory traction aids, and hazard 0

assessment 2015 2016 2017 2018 2019

Suncor and contractor LTIF 5-year trend

SUNCOR ENERGY 1, 2 See Slide Notes & Advisories 26Indigenous & Community Relationships

We aim to increase Indigenous participation in energy development

Partner with businesses Improve workforce development Partner with youth

Spent with indigenous

$3.4B businesses since 2016 3.4

(cumulative spend)

East Tank Farm Deal 2.5

Partnership 1.6

$1B Canada’s largest Indigenous energy partnership

0.9

First Nations ownership

49% Fort McKay & Mikisew Cree First Nations

0.4

25 year Revenue stream

Supports community investment 2016 2017 2018 2019 2020

Suncor’s Adelaide Wind Farm 42

Petro-Canada Retail Stations

25% interest by Aamjiwnaang First Nation owned or leased by First Nations

(cumulative)

42

38

PetroNor

26 27

Suncor has 41% interest in James Bay Cree company 23

2001-2016 2017 2018 2019 2020

SUNCOR ENERGY 27SUNCOR ENERGY

Appendix

Technology

Development

28

202003-038New Technologies Realize Multiple Benefits1

Examples of potential current technologies to meet multiple objectives

across our business

Lower costs Lower GHGs Reduce water, tailings & land footprint

Next Generation SAGD2

Thermal solvent processes (Solvent Plus, EASE3/ESEIEH®4)

Steam-solvent technologies (ES-SAGD5)

IN SITU Steam & gas co-injection (NCG6)

Wellbore enhancements

Late Life SAGD2

Waterless extraction processes (NAE7)

MINING & Froth treatment technologies (PFT8)

EXTRACTION Tailings processes & wetland reclamation (PASS 9, DPL/EPL10)

Autonomous haul systems (AHS11)

REFINING & Partial upgrading (PURE12) / Integrated Bitumen to Diesel

UPGRADING Renewable fuels & diluent

CORPORATE Data analytics/artificial intelligence

SUNCOR ENERGY 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12 See Slide Notes and Advisories 29Leading Deployment of Mining Technologies

Fort Hills - Higher quality, fungible product Autonomous Haul Systems (AHS)

Paraffinic Froth Treatment in secondary extraction ✓ Greater reliability, efficiency & productivity

Bitumen froth mixed with solvents to remove water and minerals Designed to run 24/7 with no ‘breaks’

✓ Lower costs

~$1/bbl opex savings1

✓ Safer operations

Shipped

Minimizes human interface in the mine, obstacle detection

>75% bitumen directly to

market

~10% asphaltenes

2% water & sediment

mine pit Fort Hills Mine

Status: deployed Q4 2020

Number of Trucks: ~50

✓ Partially upgraded

Higher value due to reduced asphaltenes content Millennium Mine

Status: deployment schedule ~2023 - 2025

✓ Lower GHG emissions Number of Trucks: ~100

In line with the average crude refined in the U.S.

✓ Less diluent required

~20% diluent mix vs. ~30% for in situ barrel transportation

✓ Fungible product

Meets pipeline, refinery specifications, no further upgrading

SUNCOR ENERGY 1, 2 See Slide Notes & Advisories 30New Cogeneration Facility Sanctioning1

Heat required for

mining operations

Economically Robust

HIGH

%

TEEN

IRR2 independent of oil price & pipeline egress

Natural gas

INPUTS

Water

$1.4B Capital investment over 4 years

Increase revenue from power sales

0

Lower sustaining capital by replacing aging asset

Sustainably Minded

Annual emission reductions3

2.5MT ~25% progress toward GHG goal

Electricity Steam

Vehicle emissions equivalent4

OUTPUTS

550K ~15% of Alberta’s vehicles5

Low-carbon power sold to grid,

displacing coal fired power Technologically Progressive

Power Low-carbon power added to Alberta grid

consumed

by retail 800MW Displacing higher intensity coal power

& wholesale

customers

SUNCOR ENERGY 1, 2, 3, 4, 5 See Slide Notes & Advisories 31SUNCOR ENERGY

Appendix Model

Integrated

Calculation

32

202003-038Integrated Model

2019 / 2020 AVERAGES OF PRODUCTS SOLD TO MARKET

REFINED PRODUCTS

~50% FFO1

456 kbpd2

SYNTHETIC CRUDE OIL

OFFSHORE ~25% FFO1 GASOLINE (45%)

~15% FFO1

BITUMEN 315 kbpd2 DISTILLATES (45%)

~10% FFO1 ASPHALT (5%) OTHER (5%)

104 kbpd2

138 kbpd2

HIGH

BASE PROCESSING,

VALUE

ENERGY INFRASTRUCTURE CONSUMER

ENERGY

SOURCES4 & LOGISTICS5 CHANNELS6

SOURCES3

Sale of Refining hydrocarbons into

Sale of unprocessed Processing & using extensive

infrastructure, logistics & trading consumer products & marketing

unprocessed energy products,

to optimize product movement to wholesale & retail consumers

energy products majority at US

at Brent pricing to across value chain

Gulf Coast

global markets heavy pricing

P H Y S I C A L I N T E G R A T I O N S T R A T E G Y

Agile & informed model to capture margin by processing & moving energy across the value chain

SUNCOR ENERGY 1, 2, 3, 4, 5, 6 See Slide Notes & Advisories 33500

Asset Value Maximization Converting

hydrocarbons into

$150.00

2019 / 2020 AVERAGES1 ($CAD) consumer products

(Refer to pages 34 - 37 in Supplemental IR Deck for full reconciliation)

Product Value Transportation Cost 456

Product Margin Processing Cost kbpd2

400 Royalty Cost $120.00

Feedstock Cost

Upgrading bitumen to ~1/3 margin from

higher value product physical integration,

marketing & logistics

300 315 $90.00

kbpd $89

Globally priced per bbl

$36

offshore production per bbl

200

$69 $53 $60.00

per bbl per bbl Minimizing $62 $25

exposure to low per bbl per bbl

value bitumen

138 $43 $18

$53/bbl

100 per bbl per bbl $30.00

kbpd

104

$37/bbl

kbpd Majority

$25/bbl

sold at

US Gulf

$16/bbl

Coast at

global

heavy

pricing

0 $-

OFFSHORE SALES BITUMEN SALES SYNTHETIC CRUDE OIL REFINED PRODUCT

to market to market SALES SALES

to market to market

MA J O R IT Y O F P H Y S IC A L L Y IN T E G R A T E D V O L U ME S

SUNCOR ENERGY 1, 2 See Slide Notes & Advisories 34Corporate Summary Calculation1

2019 / 2020 Average Funds from Operations (FFO)2 Breakdown ($CAD)

Volume Margin FFO

(kbpd) ($/bbl) ($M)

Offshore E&P 104.3 52.61 1,998

Bitumen 137.7 17.61 857

SCO 315.4 24.86 2,867

Refined products 455.7 35.95 6,034

Total operating gross margin 11,770

Income Taxes (447)

Corporate adjusted items:

FIFO gain (loss) 52

Intersegment profit (eliminated) realized (75)

Corp segment FFO (adjusted to pre-tax) (1,343)

Other revenue (costs) - net (2,096)

Exploration, reclamation & financing expense (655)

Other (non-cash addbacks) 154

Consolidated Suncor Funds Flow from Operations 7,347

Reported Funds Flow from Operations (avg of 2019-20) 7,347

SUNCOR ENERGY 1, 2 See Slide Notes & Advisories 35Integrated Model – Volumes Calculation1

FY2020 FY2019 20/19 AVG SOURCE

VOLUMES (Sales) (mbbls/d)

a E&P 102.6 106.0 104.3 Q4 2020 Report P65

Bitumen

b OSO 67.5 102.2 84.9 Q4 2020 Report P63

c FH 58.1 85.3 71.7 Q4 2020 Report P63

SCO

d OSO 304.8 311.3 308.1 Q4 2020 Report P63

e Syncrude 163.1 172.3 167.7 Q4 2020 Report P63

Equity Volumes Sent to Refiners

f Equity crude 168.4 190.0 179.2 2019 AIF P21; 2020 Actuals.

g Bitumen % 5% 15% 10%

h SCO 159.2 161.5 160.4

i Bitumen 9.2 28.5 18.9

VOLUMES (Sales to Market - excluding internal transfers)

j E&P 102.6 106.0 104.3

k Bitumen 116.4 159.0 137.7

l SCO 308.7 322.1 315.4

m Refining 435.6 475.9 455.7 Q4 2020 Report P72

SUNCOR ENERGY 1 See Slide Notes & Advisories 36Integrated Model – Margin Calculation1

MARGIN / BBL ($CAD) FY2020 FY2019 20/19 AVG SOURCE

E&P (Brent pricing)

n Average price realized 52.57 85.54 69.46

o Royalties (2.52) (7.64) (5.14)

Q4 2020 Report P65

p Transportation costs (2.64) (1.94) (2.28)

q Operating costs (8.45) (10.37) (9.43)

r Margin 38.96 65.60 52.61 = Average price realized + royalties + transportation + operating costs (n + o + p + q)

Bitumen (majority Maya pricing)

s Average price realized 28.44 52.05 42.58

t Royalties (0.32) (1.70) (1.15)

Q4 2020 Report P64

u Transportation costs (6.07) (6.34) (6.23)

v Operating costs (20.14) (15.88) (17.59)

w Margin 1.91 28.13 17.61 = Average price realized + royalties + transportation + operating costs (s + t + u + v)

SCO

x Average price realized 48.19 75.43 62.03

y Royalties (0.45) (4.49) (2.50)

Q4 2020 Report P64

z Transportation costs (4.36) (4.75) (4.56)

aa Operating costs (29.45) (30.76) (30.12)

ab Margin 13.93 35.43 24.86 = Average price realized + royalties + transportation + operating costs (x + y + z + aa)

Refined Product Sales

ac Average price realized 72.76 105.68 89.22

ad Feedstock cost (net of FIFO) (44.16) (68.92) (56.54) 5-2-2-1 Calculation

ae FX (US:CAD) 0.75 0.75 0.75

af WTI (US$/bbl) 39.40 57.05 48.23

Q4 2020 Report P15

ag WCS (US$/bbl) 26.85 44.25 35.55

ah SYN (US$/bbl) 36.25 56.45 46.35

ai R&M gross margin (inclusive of marketing & logistics activities) 4,029 7,008 5,519 Q4 2020 Report P72

aj Adj - FIFO gain (loss) (519) 623 52 2019 Annual Report P41; 2020 cumulative per quarterly report

ak R&M gross margin (LIFO) 4,548 6,385 5,466

al R&M gross margin/bbl (LIFO) 28.60 36.76 32.68

am Transportation costs (0.87) (0.69) (0.78)

an Operating costs (5.50) (5.35) (5.43) Q4 2020 Report P72

ao Value chain margin/bbl 5.13 13.71 9.47

ap R&M margin/bbl (incl. value chain margin) 27.37 44.42 35.95

SUNCOR ENERGY 1 See Slide Notes & Advisories 37Integrated Model – Funds from Operations Calculation1,2 Funds flow from operations model FY2020 FY2019 20/19 AVG SOURCE aq Brent sales 1,459 2,538 1,998 ar Bitumen (majority Maya) sales 81 1,633 857 as SCO sales 1,570 4,165 2,867 at Refined product sales 4,351 7,717 6,034 au Total operating gross margin 7,487 16,053 11,770 av Current income taxes 659 (1,552) (447) Q4 2020 Report P47 aw Add: Corporate adjusted items ax FIFO gain (loss) (519) 623 52 ay Intersegment profit (eliminated) realized 126 (276) (75) Q4 2020 Report P28 az Corp segment FFO (adjusted to pre-tax) (1 402) (1 285) (1,343) Q4 2020 Report P54 (FS) & P41 (FFO) ba Other revenue (costs) - net (2,077) (2,116) (2,096) bb Exploration, reclamation & financing expense ( 479) ( 830) (655) Q4 2020 Report P54 (FS) & P41 (FFO) bc Other (non-cash addbacks) 106 201 154 Q4 2020 Report P41 bd Consolidated Suncor funds from operations 3,875 10,818 7,347 be Reported funds from operations 3,875 10,818 7,347 -2.3 Other revenues and costs bh Reported OS + EP + RM segment revenues 12,072 21,292 12,072 Q4 2020 Report P54 bi Calculated revenues 11,503 20,186 15,845 bj Total Other revenues 569 1,106 837 bk Reported OS + EP + RM segment costs 11236 13740 13,740 Q4 2020 Report P54 bl Calculated costs 8,590 10,519 9,554 bm Total Other costs 2,646 3,221 2,934 Acronyms FS Financial Statements FFO Funds from (used in) Operations OS Oil Sands EP Exploration & Production RM Refining & Marketing Corporate Corporate & Eliminations SUNCOR ENERGY 1, 2 See Slide Notes & Advisories 38

SUNCOR ENERGY

Appendix

Glossary

39

202003-038Glossary1 Alkylate (Alkylation): A refining operation that takes low value derivatives from the catalytic cracking and other processes and unites them in the presence of an acid catalyst to produce a very high octane, low vapor pressure gasoline blending component. Aromatics: Hydrocarbons characterized by their uniform carbon ring structure and their often pleasant aroma. Commercial petroleum aromatics are benzene, toluene, and xylene. These three are often referred to by the acronym BTX. These chemicals are used as high octane components in gasoline. Aromatics have been judged to be undesirable in some finished motor fuels with various state and federal regulations geared toward reducing their levels. CARB diesel fuel in the state of California mandates a low aromatics composition. Asphalt: A dark-brown-to-black cement-like material containing bitumen as the predominant constituent obtained by petroleum processing, used primarily for road construction. It includes crude asphalt as well as the following finished products: cements, fluxes, the asphalt content of emulsions (exclusive of water), and petroleum distillates blended with asphalt to make cutback asphalts. Note: The conversion factor for asphalt is 5.5 barrels per short ton. Barrel: Term used as the standard measurement of volume for crude oil and large quantities of refined products in the petroleum industry. A unit of volume equal to 42 U.S. gallons – often abbreviated as bbl. Benchmark Crude: A widely accepted grade of crude oil used as a standard in trading. Other grades would be traded at a price differential according to the quality differences. Examples would be WTI, Brent, Dubai and Arab Light. Brent: Blend of crude oil from a critical group of North Sea fields, Brent is the standard contract for ICE crude oil futures trading, and the most commonly referenced crude in Europe. It’s described as the European counterpart of WTI, and its morning performance is often a harbinger for the NYMEX opening. London’s ICE Brent contract is the benchmark crude for international oil physical and futures trading. Catalytic Cracking: The refining process of breaking down, via heat and pressure, the larger, heavier, and more complex hydrocarbon molecules into simpler and lighter molecules, primarily gasoline. Catalytic cracking is accomplished by the use of a catalytic agent and is an effective process for increasing the yield of gasoline from crude oil. Coker: An oil refining unit in which heavy feed such as flasher bottoms, cycle oil from a fluid catalytic cracker, or thermal cracked gas oil is subjected to high temperatures. This causes the feed to crack, creating lights oils. Coke – solid, densely packed carbons – builds up in the reactors of the unit and periodically needs to be removed. Crack Spread: Term applied to the differential between what a typical refined products mix would yield, and the value of crude. The common crack spread features a per bbl reference derived of 66.6% unleaded gasoline and 33.4% No. 2 oil. The resulting average is compared to the WTI number for the resulting “crack spread.” Crack spreads of 3:2:1 use three parts gasoline, two parts of distillate to one part of crude. SUNCOR ENERGY 1 See Slide Notes. 40

Glossary1 (continued) Crude Distillation: An oil refinery unit that separates crude oil into different products according to their individual boiling point ranges. Distillation allows for the materials to be separated without being subjected to conditions that would cause cracking or decomposition. Delayed Coking: A process by which heavier crude oil fractions can be thermally decomposed under conditions of elevated temperatures and pressure to produce a mixture of lighter oils and petroleum coke. The light oils can be processed further in other refinery units to meet product specifications. The coke can be used either as a fuel or in other applications such as the manufacturing of steel or aluminum. Distillation: The most basic refining operation that heats the crude oil and condenses the cuts in a fractionating column in order to separate the various petroleum products for further processing. Feedstock: Any of the raw or semi-finished materials which move to the various units of a refinery or petrochemical plant. Crude is a feedstock, but the term is mainly used to describe raw materials after the distillation process which in turn go on to more sophisticated units at the refinery. VGO, naphtha, condensate and straight run residual fuel are commonly referred to as feedstocks. Gasoil (VGO): Commonly, the European term used for diesel fuel and heating oil. Hydrotreating: A refining unit whereby processed material from the crude units are treated in the presence of catalysts and hydrogen, often to remove sulfur and other unwanted substances. The hydrotreater is often the critical unit for producing jet fuel and low-sulfur diesel. Liquefied Petroleum Gases (LPG): A group of hydrocarbon-based gases derived from crude oil refining or natural gas stream fractionation that are often liquefied, through pressurization, for ease of transport. They include: ethane, propane, normal butane, and isobutane. Uses of these fuels include: home heating, industrial, automotive fuel, petrochemical feedstocks and for drying purposes in farming. Natural Gas (NG): A naturally-occurring raw material often produced in conjunction with crude oil that is processed through a variety of facilities to yield natural gas liquids. It is a commercially acceptable product for industrial and residential consumption and is shipped via pipeline. Petrochemical: An intermediate product derived from crude and natural gas processing that is used in production of a wide range of products, including plastics. Also the facility that processes these intermediate products. Petrochemical plants are often integrated with major refineries. Rack Market: Petroleum products sold at the wholesale level from primary storage. Refers to loading racks where tanker trucks fill up. SUNCOR ENERGY 1 See Slide Notes. 41

Glossary1 (continued) Reforming: An oil refining unit in which naphthas are changed chemically to increase their octane level. Paraffins convert to iso-paraffins and naphthenes, and naphthenes change to aromatics. The catalyst used is usually platinum, though sometimes palladium. Sour Crude Oil: Crude oil is considered ‘sour’ if it contains ≥ 0.5% sulfur. Spot Price: The current value of any product on a volume basis. Sulfur: A yellowish nonmetallic element, sometimes known as “brimstone.” It is naturally occurring at various levels of concentration in many fossil fuels whose combustion releases sulfur compounds that are considered harmful to the environment. Some of the most commonly used fossil fuels are categorized according to their sulfur content, with lower sulfur fuels usually selling at a higher price. Note: No. 2 Distillate fuel is currently reported as having either a 0.05% or lower sulfur level for on-highway vehicle use or a greater than 0.05% sulfur level for off-highway use, home heating oil, and commercial and industrial uses. This also includes Ultra Low Sulfur Diesel (

Advisories

Forward-Looking Statements – This presentation contains certain expected synergies and the ability to sustain reductions in costs; the measures are included because management uses the information to

“forward-looking statements” within the meaning of the United States ability to access external sources of debt and equity capital; the timing analyze business performance, leverage and liquidity and therefore

Private Securities Litigation Reform Act of 1995 and “forward-looking and the costs of well and pipeline construction; Suncor’s dependence may be considered useful information by investors. See the “Non-

information” within the meaning of applicable Canadian securities on pipeline capacity and other logistical constraints, which may affect GAAP Financial Measures Advisory” section of the Q1 MD&A.

legislation (collectively, “forward-looking statements”), including the company’s ability to distribute products to market; mandatory

statements about: Suncor’s strategy and business plans; expected production curtailments being greater or imposed for longer than Funds from operations (previously referred to as cash flow from

operating and financial results; reserves estimates and reserve life anticipated; the timely receipt of regulatory and other approvals; the operations) is defined in the Q1 MD&A, for the three months ended

indices; future opportunities in Oil Sands and regional synergy timing of sanction decisions and Board of Directors’ approval; the March 31, 2021 is reconciled to the GAAP measure in the Q1 MD&A,

opportunities for existing assets; expectations for sanctioned E&P availability and cost of labour, services, and infrastructure; the for 2012 to 2020 is reconciled to GAAP measures in Suncor’s annual

projects, including anticipated peak production; expected benefits satisfaction by third parties of their obligations to Suncor; the impact of management’s discussion and analysis (MD&A) for the respective

from sanctioned and identified power generation projects; nameplate royalty, tax, environmental and other laws or regulations or the year. Free funds flow (previously referred to as free cash flow) is

capacities; expected utilization of assets; expectations on refinery interpretations of such laws or regulations; applicable political and defined in the Q1 MD&A, and is reconciled, as applicable for 2019 to

feedstocks and refined products; potential future pipelines and market economic conditions; risks associated with existing and potential 2020 in the 2020 MD&A, for 2015 to 2018 to the GAAP measure in

access expectations; the assumption that Suncor's 5-2-2-1 index will future lawsuits and regulatory actions; improvements in performance Suncor’s 2018 annual MD&A, and for 2014 to the GAAP measure in

continue to be an appropriate measure against Suncor's actual of assets; and the timing and impact of technology development. Suncor’s 2016 annual MD&A; and the estimated impact of the LIFO

results; expectations for and potential benefits of the cogeneration method for the three months ended March 31, 2021 is defined and

facility, Suncor/Syncrude interconnecting pipelines, autonomous haul Although Suncor believes that the expectations represented by such reconciled in the Q1 MD&A.

trucks, PASS, paraffinic froth treatment, high temperature reverse forward-looking statements are reasonable, there can be no

osmosis and non-aqueous extractions; tailings treatment capacity; assurance that such expectations will prove to be correct. Suncor’s Reserves– Unless noted otherwise, reserves information presented

that the East Tank Farm deal will provide a twenty five year revenue Management’s Discussion & Analysis (MD&A) ended March 31, 2021 herein for Suncor is presented as Suncor’s working interest (operating

stream to the two Alberta First Nations; statements about Suncor’s and dated May 3, 2021 (the Q1 MD&A), Annual Report for the year and non-operating) before deduction of royalties, and without

investments in its lower-carbon technology portfolio and in ended December 31, 2020 (the 2020 Annual Report) and its most including any royalty interests of Suncor, and is at December 31,

technologies, including the expected benefits therefrom; potential recently filed Annual Information Form/Form 40-F and other 2020. For more information on Suncor’s reserves, including definitions

future free funds flow growth projects, including the timing and impact documents it files from time to time with securities regulatory of proved and probable reserves, Suncor’s interest, location of the

thereof, and free funds flow improvement and cash flow upside authorities describe the risks, uncertainties, material assumptions and reserves and the product types reasonably expected please see

potential; statements about Suncor’s GHG intensity reduction goal other factors that could influence actual results and such factors are Suncor’s most recent Annual Information Form dated February 24,

including the expected impact of sanctioned projects; expectations, incorporated herein by reference. Copies of these documents are 2021 available at www.sedar.com and Form 40-F dated February 25,

targets and potential opportunities with respect to Syncrude; capital available without charge from Suncor at 150 6th Avenue S.W., 2021 available at www.sec.gov. Reserves data is based upon

and production guidance; planned maintenance and the timing Calgary, Alberta T2P 3E3, by calling 1-800-558-9071, or by email evaluations conducted by independent qualified reserves evaluators

thereof; and goals with respect to reliability, safety, cost management request to invest@suncor.com or by referring to the company’s profile as defined in NI 51-101.

and sustainability, that are based on Suncor’s current expectations, on SEDAR at www.sedar.com or EDGAR at www.sec.gov. Except as

estimates, projections and assumptions that were made by Suncor in required by applicable securities laws, Suncor disclaims any intention BOE (Barrels of oil equivalent) – Certain natural gas volumes have

light of its experience and its perception of historical trends. Some of or obligation to publicly update or revise any forward-looking been converted to barrels of oil on the basis of six thousand cubic feet

the forward-looking statements may be identified by words such as statements, whether as a result of new information, future events or to one boe. This industry convention is not indicative of relative market

“planned”, “estimated”, “target”, “goal”, “illustrative”, “strategy”, otherwise. Suncor’s actual results may differ materially from those values, and thus may be misleading.

“expected”, “focused”, “opportunities”, “may”, “will”, “outlook”, expressed or implied by its forward-looking statements, so readers are

“anticipated”, “potential”, “guidance”, “predicts”, “aims”, “proposed”, cautioned not to place undue reliance on them. Impact of the COVID-19 Pandemic: The COVID-19 pandemic is an

“seeking” and similar expressions. Forward-looking statements are not evolving situation that will continue to have widespread implications

guarantees of future performance and involve a number of risks and Suncor’s corporate guidance includes a planned production range, for our business environment, operations and financial condition.

uncertainties, some that are similar to other oil and gas companies planned maintenance, capital expenditures and other information, Actions taken around the world to help mitigate the spread of COVID-

and some that are unique to Suncor. Users of this information are based on our current expectations, estimates, projections and 19 have and will continue to have significant disruption to business

cautioned that actual results may differ materially as a result of, assumptions (collectively, the Factors), including those outlined in our operations and a significant increase in economic uncertainty. Our

among other things, assumptions regarding: the current and potential 2021 Corporate Guidance available on www.suncor.com/guidance, operations and business are particularly sensitive to a reduction in the

adverse impacts of the COVID-19 pandemic; commodity prices and which Factors are incorporated herein by reference. Suncor includes demand for, and prices of, commodities that are closely linked to

interest and foreign exchange rates; the performance of assets and forward-looking statements to assist readers in understanding the Suncor’s financial performance, including crude oil, refined petroleum

equipment; capital efficiencies and cost savings; applicable las and company’s future plans and expectations and the use of such products (such as jet fuel and gasoline), natural gas and electricity.

government policies; future production rates; the development and information for other purposes may not be appropriate. The timing of an economic recovery is currently uncertain. This could

execution of projects; assumptions contained in or relevant to result in reduced utilization and/or the suspension of operations at

Suncor’s 2021 Corporate Guidance; product supply and demand; certain of our facilities, buyers of our products declaring force majeure

market competition; future production rates; assets and facilities not Non-GAAP Measures – Certain financial measures in this or bankruptcy, the unavailability of storage, and disruptions of pipeline

performing as anticipated; expected debottlenecks, cost reductions presentation – namely funds from operations, free funds flow, and last and other transportation systems for our products, which would further

and margin improvements not being achieved to the extent in, first out (LIFO) – are not prescribed by GAAP. All non-GAAP negatively impact Suncor’s production or refined product volumes,

anticipated; dividends declared and share repurchases; the sufficiency measures presented herein do not have any standardized meaning and could adversely impact our business, financial condition and

of budgeted capital expenditures in carrying out planned activities; and therefore are unlikely to be comparable to similar measures results of operations.

risks inherent in marketing operations (including credit risks); presented by other companies. Therefore, these non-GAAP measures

imprecision of reserves estimates and estimates of recoverable should not be considered in isolation or as a substitute for measures

quantities of oil, natural gas and liquids from Suncor’s properties; of performance prepared in accordance with GAAP. All non-GAAP

SUNCOR ENERGY 43Slide Notes

Slide 4------------------------------------------------------------- determined. The ALE project is currently being evaluated with all may not be reflective of actual utilization rates. See Forward-

(1) Reserves are working interest before royalties. See Reserves in the stakeholders to determine the best option to integrate and optimize Looking Statements and Impact of the COVID-19 Pandemic in the

Advisories. The estimates of reserves for individual properties potential funding to recover the remaining resources from the Terra Advisories.

provided herein may not reflect the same confidence level as Nova project. Slide 19-------------------------------------------------------------

estimates of reserves for all properties due to the effects of (5) Refers to East Coast Canada (ECC). (1) Funds from operations (FFO) is a non-GAAP financial measure and

aggregation. Suncor’s total 2P Reserves (gross) for Canada are is calculated as cash flow provided by operating activities excluding

7,064 mmboes at December 31, 2020. Slide 9------------------------------------------------------------- changes in non-cash working capital. See Non-GAAP Measures in

Slide 5------------------------------------------------------------- (1) Represents possible future opportunities currently being evaluated. the Advisories.

(1) Represents possible future opportunities currently being evaluated. There can be no assurance these opportunities will be pursued. See (2) Source: US Energy Information Administration

There can be no assurance these opportunities will be pursued. See Forward-Looking Statements in the Advisories. Slide 20------------------------------------------------------------

Forward-Looking Statements in the Advisories. Slide 11 -------------------------------------------------------------- (1) Average refinery production is based on the twelve months ended

Slide 6------------------------------------------------------------- (1) As at December 31, 2020 and assumes that approximately 7.04 billion March 31, 2019.

(1) Attributes are generalizations based on Suncor’s analysis of its own barrels of oil equivalent (boe) of proved and probable reserves (2P) are Slide 21-------------------------------------------------------------

projects and industry data. produced at a rate of 593.4 mboe/d, Suncor’s average daily production (1) Inventory barrels are an illustrative approximation and actual results

(2) Funds from operations (FFO) is a non-GAAP financial measure. See rate in 2020. Reserves are working interest before royalties. See will vary depending on market and operating conditions. See

Non-GAAP Measures in the Advisories. FFO is calculated as cash Reserves in the Advisories. Forward-Looking Statements in the Advisories.

flow provided by operating activities excluding changes in non-cash (2) 1,877 retail and wholesale sites are operated under the Petro-Canada Slide 22-------------------------------------------------------------

working capital. brand as of December 31, 2020. (1) Crude logistics time, products storage time, commodity mix in

(3) Annual FFO profiles are based on representative project economics (3) Proposed future pipelines. There can be no assurance this pipeline will inventory and average number of days in inventory are an illustrative

be built with the capacity indicated or at all. See Forward-looking

(development capital, operating and sustaining costs) using approximation and actual results will vary depending on market and

Statements in the Advisories.

consistent assumptions for future oil prices (including adjustments operating conditions. See Forward-Looking Statements and Impact

Slide 12-------------------------------------------------------------

for quality, transportation and marketing costs), tax and royalty of the COVID-19 Pandemic in the Advisories.

(1) Nameplate capacities as at December 31, 2020. Nameplate

rates. Actual FFO may differ materially. See Forward-Looking Slide 24------------------------------------------------------------

capacities may not be reflective of actual utilization rates. See

Statements in the Advisories. (1) Approximately 92% of the water used by our mining and extraction

Forward-Looking Statements and Impact of the COVID-19 Pandemic in

Slide 7----------------------------------------------------------- operations in 2019 was recycled tailings water. At our Firebag in situ

the Advisories.

(1) Reserves are working interest before royalties. See Reserves in the site, approximately 96% of the water used is recycled. The make-up

Slide 13----------------------------------------------------------

Advisories. The estimates of reserves for individual properties is drawn from recycled wastewater from our oil sands upgrading and

(1) Excludes the impact of operations being shut-in due to forest fires in

provided herein may not reflect the same confidence level as utilities operations, surface run-off water collected within the facility

the Fort McMurray region during the second quarter of 2016.

estimates of reserves for all properties due to the effects of (2) Excludes the impact of the planned major turnaround impact in boundary and from groundwater wells. At our MacKay River in situ

aggregation. Suncor’s 2P Reserves (gross) for total Canada, North facility, close to 100% of the water is recycled and MacKay River

2018.

Sea UK and Norway North Sea, respectively, are 7,273 mmboe and has zero liquid discharge. The majority of make-up water comes

(3) Targets based on current business plans and business environment

86 mmboe as at December 31, 2020. Sum of displayed 2P reserves from groundwater, most of which is too high in salt and mineral

expectations. Actual results may differ materially from these targets.

is 284 mmboe; remaining 2P reserves is displayed on slide 8 are See Forward-Looking Statements in the Advisories. content to be used for potable water or agriculture.

made of sanctioned projects. (2) Fresh water consumption intensity in 2016 was adversely impacted

(4) Syncrude utilization rates are calculated using intermediate sour

(2) Suncor’s 27.5% working interest is for the White Rose base project. by wildfires, which reduced the industrial water recycle rates and

production.

Suncor’s working interest in the White Rose growth lands is extended the Upgrader 2 unplanned turnaround by more than one

Slide 14-------------------------------------------------------------

26.125%. month. Fresh water consumption intensity in 2017 decreased due to

(1) Based on Suncor’s forecast of market access capacity available to

(3) Photo source: Norwegian Petroleum Directorate. the sale of our Lubricants business in Mississauga, Ontario on

industry and Suncor’s planned production profile. See Forward

Slide 8---------------------------------------------------------- February 1, 2017 and further optimization of the wastewater recycle

Looking Statements in the Advisories.

(1) Represents possible future opportunities currently being evaluated. rates at Oil Sands Base operations, including modifications and

(2) Approximate total pipeline capacities based on publicly sourced

There can be no assurance these opportunities will be pursued. improvements to the industrial wastewater system. Intensity

information available at www.capp.ca and www.enbridge.com

Actual peak production and anticipated recoveries may vary from increased in 2018 and 2019 due to the ramp up of the Fort Hills

(3) Proposed future pipeline. There can be no assurance this pipeline

those expected. See Forward-Looking Statements in the Advisories. project, which is building up water inventory for recycling.

will be built with the capacity indicated or at all. See Forward

(2) Funds from operations (FFO) is a non-GAAP financial measure. See (3) Actual results may differ materially. See Forward-Looking

Looking Statements in the Advisories.

Non-GAAP Measures in the Advisories. FFO is calculated as cash Statements in the Advisories.

Slide 16-------------------------------------------------------------

flow provided by operating activities excluding changes in non-cash (4) SAGD refers to steam assisted gravity drainage.

(1) 503.4mbbl/d refined products sales average for 2020.

working capital. Slide 25 --------------------------------------------------------------

(2) Based on Kent (a Kalibrate company) survey data for year-end

(3) Free funds flow is calculated by taking funds from operations (1) Refers to Permanent Aquatic Storage Structure (PASS).

2019.

(previously referred to as cash flow from operations) for E&P and (2) Based on current business plans, which are subject to change.

(3) 316 PETRO-PASS wholesale sites, as of December 31, 2020. Expected benefits of PASS may not be achieved. See Forward-

subtracting E&P capital and exploration expenditures, excluding

(4) 1561 retail sites are operated under the Petro-Canada brand. Looking Statements in the Advisories.

capitalized interest, all as indicated for the applicable year in (5) The Montreal and Sarnia refineries have a local reach of over 20

Suncor’s respective Annual Reports. Management uses free funds (3) Fluid tailings inventory represents fluid tailings production net of fluid

million people in accordance to population numbers retrieved from tailings treated.

flow to measure financial performance and liquidity. Free funds flow

Statistics Canada 2016 census. (4) Statistic applies to Oil Sands Base. PASS accounts for ~75% of the

is a non-GAAP measure. See Non-GAAP Measures in the

Slide 17------------------------------------------------------------- 2019 treatment volumes.

Advisories. (1) Upgrading volume percentages are based on historical averages Slide 26-------------------------------------------------------------

(4) At West White Rose Project discussions are ongoing with the

and subject to change with operating and market conditions. See (1) RIF refers to recordable injury frequency.

operator and various levels of government to determine the future of

Forward-Looking Statements and Impact of the COVID-19 (2) LTIF refers to lost time injury frequency.

the project. At Terra Nova, the company is preserving the floating

Pandemic in the Advisories.

production storage and offloading unit quayside and deferring the

Slide 18------------------------------------------------------------- continued …

asset life extension until an economically viable path forward can be

(1) Nameplate capacities as at January 1, 2021. Nameplate capacities

SUNCOR ENERGY 44You can also read