LIBOR TRANSITION: LENDING WITH ALTERNATE AND ALTERNATE-ALTERNATE RATES - June 16th, 2020 10 AM, US Eastern Daylight Time

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

LIBOR TRANSITION: LENDING WITH ALTERNATE AND ALTERNATE-ALTERNATE RATES June 16th, 2020 10 AM, US Eastern Daylight Time

1

OPENING REMARKS DAN

ROSENBAUM

Partner, Retail and

Business Banking

Dan.Rosenbaum@oliverwyman.com

INDUSTRY PANELIST

Timothy J. Bowler

President of ICE Benchmark

Administration

OLIVER WYMAN HOSTS

Dan Rosenbaum Adam Schneider

Partner, Retail and Business Banking Partner, Lead LIBOR Platform

Dan.Rosenbaum@oliverwyman.com Adam.Schneider@oliverwyman.com

Umit Kaya Esther Bruegger

Partner, Finance & Risk Principal, Finance & Risk

Umit.Kaya@oliverwyman.com Esther.Bruegger@oliverwyman.com

© Oliver Wyman 3

LIBOR TRANSITION: LENDING WITH ALTERNATE AND

ALTERNATE-ALTERNATE RATES – AGENDA

1 Opening Remarks Dan Rosenbaum

2 Why Alternates to the Alternate? Adam Schneider

3 Intercontinental Exchange: USD Bank Yield Index

Timothy J. Bowler

ICE Benchmark Administration

4 The Million (Trillion?) Dollar Question: How Do We Lend?

Umit Kaya

Esther Bruegger

5 Closing Remarks Dan Rosenbaum

© Oliver Wyman 4

2

WHY ALTERNATES TO

THE ALTERNATE? ADAM

SCHNEIDER

Partner, Lead LIBOR

Platform

Adam.Schneider@oliverwyman.com

WHILE SOFR WAS RECOMMENDED BY ARRC IN 2017 TO REPLACE USD

LIBOR, ITS USE IN LENDING HAS BEEN MORE CONTROVERSIAL

2017: ARRC identifies SOFR 2019: ARRC issues guidance Mid-2020: Minimal use of SOFR in

as its recommended rate on how to use SOFR in lending lending; ARMs by end of year

2018 2020 2022

2017 2019 2021

2018: SOFR published by the 2019: ARRC Calendar 2021: lots of SOFR

NY Federal Reserve April; swaps details workings lending needed – or another

start trading; futures in May of SOFR ARMs rate to emerge?

Compounding the move to SOFR: while the ARRC recognizes the need for a term rate, it also urges

lenders to consider using a compounded or average SOFR

But while SOFR should be relatively easy to Those who are able to use SOFR should not wait for

incorporate into derivatives, participants in many the term rates in order to transition […] the ARRC

cash products may find use of an overnight rate believes it should be possible to use compound or

unfamiliar […] To address this issue, the ARRC has simple averages of SOFR and that many users will

explicitly included a goal of producing a forward- come to find it more convenient to do so once they

looking term rate for use in cash products. become more familiar with the new environment.

– ARRC Second Report, March 2018 – ARRC’s User’s Guide to SOFR, April 2019

© Oliver Wyman 6

WHY DOES SOFR HAVE WIDE ACCEPTANCE IN DERIVATIVES MARKETS

BUT LESS SO IN LENDING?

Criteria Lending Swaps

Anchored in observable transactions

Acceptable to regulators / IOSCO compliant

Sufficiently deep liquid underlying market that is sustainable

Published daily

Good representation of funding conditions Overnight funding NA

Incorporates banks’ own credit spread NA

Term rate

Available in different tenors expected 2021

NA

Inherent volatility, can be

Not highly volatile reduced through averages

NA

Complexity will be reduced by

Can be integrated into existing infrastructure availability of term rates

© Oliver Wyman 7

IN REACTION TO THESE CONCERNS, THE NY FED IS FACILITATING INDUSTRY DISCUSSION ON A CREDIT SENSITIVE SPREAD OVER SOFR REGIONAL BANKS SOUND ALARM OVER NEW INTEREST RATE BENCHMARK October 17th, 2019 Executives from 10 regional banks sent a letter to the federal banking regulators last month expressing concern that […] SOFR on a standalone basis “is not well suited to be a benchmark for lending products” • Following this letter, the Fed/FDIC/OCC met with signatories on February 25, 2020 to discuss ways to support the transition of loan products from LIBOR. This meeting led to the creation of Credit Sensitivity Group Workshops to discuss potential challenges of lending with SOFR. • On June 4th 2020, the NY Fed held a Credit Sensitivity Workshop1 which discussed adding a credit sensitive spread over SOFR 1. https://www.newyorkfed.org/medialibrary/media/newsevents/events/markets/2020/csg-first-workshop-public-agenda.pdf © Oliver Wyman 8

THE NY FED ALSO HAS INDICATED IT WILL NOT OPPOSE ALTERNATIVES

TO SOFR THAT ARE IOSCO-COMPLIANT

US FED’S LIBOR-TRANSITION POWELL: AMERIBOR ‘FULLY

PANEL WOULD BACK ANY ACTIVE APPROPRIATE’ FOR BANKS WHEN

BENCHMARK THAT’S ROBUST, IT REFLECTS COST OF FUNDING

IOSCO-COMPLIANT

June 3rd, 2020

May 18th, 2020

“We have been clear that the ARRC’s

The US Federal Reserve panel overseeing the recommendations and the use of SOFR are

transition from tarnished LIBOR said it would voluntary and that market participants should

support any active benchmark — not just the seek to transition away from LIBOR in the

Secured Overnight Financing Rate — as an manner that is most appropriate given their

alternative if the rate is robust and complies specific circumstances,” Powell said…“While

with international principles. [AMERIBOR] is a fully appropriate rate for the

banks that fund themselves through the

It said it supports rates that meet three American Financial Exchange or for other

criteria: They are robust, compliant with the similar institutions for whom AMERIBOR may

2013 [IOSCO] benchmark principles, and reflect their cost of funding, it may not be a

available for use before official support for natural fit for many market participants.”

LIBOR is to be withdrawn at the end of 2021.

© Oliver Wyman 9

THE LENDING CONTENDERS TODAY WE

Various types of SOFR using existing

LOOK AT

1 overnight rates, e.g. compounded in

arrears, in advance

2

Variation of existing floating rate

reference rates, e.g. Prime, CMT

3 ICE Bank Yield Index

4 AFX AMERIBOR ICE Bank Yield Index

5 Term SOFR

6

Potential other contenders, e.g.

outcome of Credit Sensitivity Group

© Oliver Wyman 103

ICE: USD BANK YIELD

INDEX TIMOTHY J.

BOWLER

President of ICE Benchmark

AdministrationUSD BANK YIELD INDEX ICE Benchmark Administration Timothy J. Bowler, President JUNE 2020

Background

• U.S. dollar LIBOR has been widely used in lending transactions over the past thirty years.

• Lenders and borrowers have generally expressed comfort in the economic premise behind U.S. dollar LIBOR as the

benchmark:

• Allows lenders to extend credit based upon marginal unsecured bank funding cost; while

• Facilitating competitive credit markets where the borrower does not need to take its specific lender’s, or a small group of

lenders’, cost of funds risk.

• The transition to risk free rates has raised questions on the risks related to moving away from LIBOR to overnight rates and, in

the case of U.S. dollars, secured rates for lending arrangements.

• For lenders these risks include a potential:

• Divergence between realized marginal funding cost and the yields on overnight rates; and

• Increased usage in undrawn liquidity facilities; particularly during a period of stress.

• For borrowers these risks include a potentially:

• Less competitive lending market; and

• Reduced access to undrawn lending facilities.

INTERCONTINENTAL EXCHANGE 13Credit Benchmark Rationale

Risk free rates (e.g. UST & SOFR) and marginal unsecured bank borrowing costs are different and can diverge

INTERCONTINENTAL EXCHANGE 14Bank Yield Index - Introduction

• In order to help facilitate the transition away from LIBOR and to meet the needs of lenders who want to retain

a credit sensitive benchmark and borrowers who value term settings, IBA developed the Bank Yield Index.

• The Bank Yield Index is a forward-looking, credit-sensitive benchmark designed specifically as a potential

replacement for LIBOR for U.S. dollar lending activity.

• The index uses unsecured bank debt transactions for the construction of an unsecured bank yield curve. The

input data includes:

• Bank funding transaction data (yields on deposits, CDs and CP transactions, i.e. does not require expert

judgment); and

• Yield data on bank bonds transactions sourced from TRACE (adjusted to money market basis).

• IBA determines term settings from the unsecured bank yield curve similar to the term settings that are found

in LIBOR today (e.g. one month, three months).

• IBA is currently testing the concept with funding data inputs from fourteen USD LIBOR Panel Banks.

INTERCONTINENTAL EXCHANGE 15Bank Yield Index - Methodology

IBA collates bank funding transaction data and secondary market transaction data, and calculates the Bank Yield

Index. This involves:

1. Aggregation of eligible transactions over initial five day window; increasing the window if necessary to meet minimum

aggregate trade count and volume thresholds (currently $15B and 100 discrete transactions 1);

o IBA chose a five day window to ensure a diverse and robust data set that reflects average bank yields

o Minimum funding volumes and transaction counts are set to ensure a representative benchmark

2. Calculation of a fitted unsecured bank yield curve using a regression analysis across all eligible data points;

3. Review of transaction data points against fitted curve to identify extreme outliers for exclusion (currently any trades over

200bps above or below the curve are excluded), and the curve fitting is repeated using the remaining transactions; and

4. Determination of 1M, 3M and 6M Index rates from the fitted bank yield curve.

1IBA also uses minimum trade count thresholds for various maturity buckets across the yield curve. Further detail can be found on the IBA website here:

https://www.theice.com/publicdocs/IBA_US_Dollar_ICE_Bank_Yield_Index_Fourth_Update.pdf

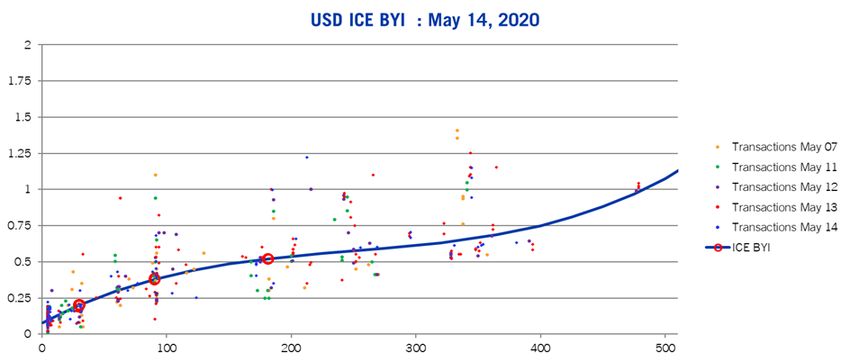

INTERCONTINENTAL EXCHANGE 16Bank Yield Index – Example calculation from May 14

Yield

Days

The dots in the chart are transaction data points sourced over 5 business days (May 7 to May 14) which are

used to derive a best-fit bank yield curve. From this yield curve “average” one-month, three-month and six-

month points can be determined (red circles) and used as the Index settings.

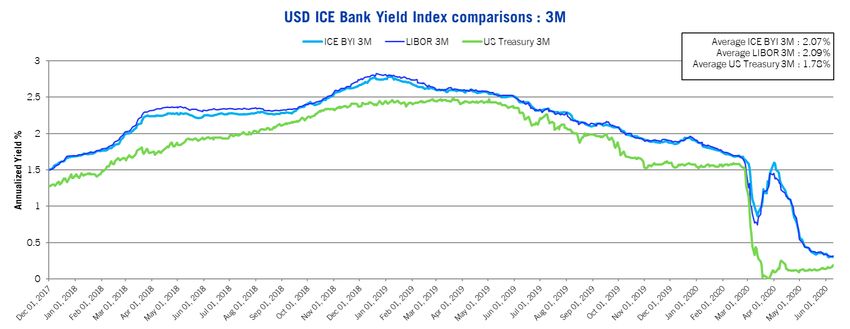

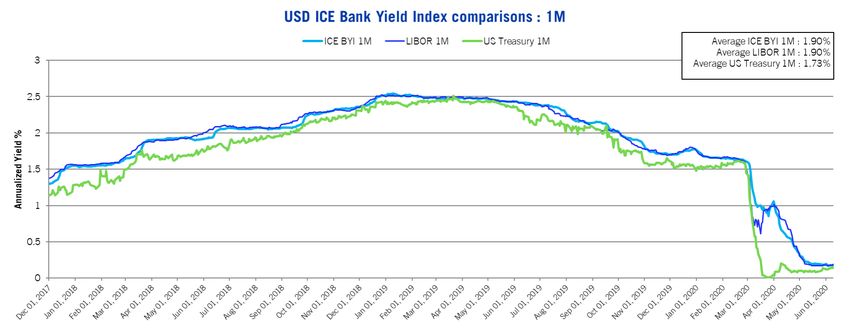

INTERCONTINENTAL EXCHANGE 17Bank Yield Index – Correlation With Other Indexes

Comparison of test results to U.S. dollar LIBOR and Treasury Yields : 1 Month

INTERCONTINENTAL EXCHANGE 18Bank Yield Index – Correlation With Other Indexes

Comparison of test results to U.S. dollar LIBOR and Treasury Yields : 3 Month

INTERCONTINENTAL EXCHANGE 19Bank Yield Index – Input Data Over The Testing Period

Review of data sourced to build the Bank Yield Index test rates from December 2017

INTERCONTINENTAL EXCHANGE 20Bank Yield Index – Input Data Over The Testing Period

Review of data sourced to build the Bank Yield Index test rates from December 2017

INTERCONTINENTAL EXCHANGE 21Bank Yield Index – Supplement to SOFR

The Bank Yield Index can also be calculated as a spread to SOFR rates

• Collate the transactions over a rolling collection window, as

in the preliminary methodology.

• Determine a Transaction Credit Spread for each transaction

by subtracting the contemporaneous risk free market rate

(e.g. Term SOFR for the same day) from the unsecured

bank debt yields observed (i.e. determine the credit spread).

• Create a fitted credit spread curve to the data points. (Blue

line on chart)

• Determine Bank Yield Credit Spreads from the fitted yield

curve. (Red circles on the chart)

• Add the Credit Spreads to the current term risk free rate

(e.g. Term SOFR today) to determine the Bank Yield Index.

• This realized spread to risk free rates can also be

added to compounded and in arrears SOFR

calculations.

INTERCONTINENTAL EXCHANGE 22Bank Yield Index - Next Steps

1. Engage with members of the Credit Sensitivity Group (GSG) hosted by the New York Fed to seek advice on key

aspects of the Bank Yield Index, including:

• Input data used, including:

• how to best create a nexus to SOFR rates, and

• should funding and bond data be used or only funding data;

• Time period used to calculate the rates (i.e. is the rolling 5-day window appropriate or should a shorter or longer

window be used).

2. Update the Bank Yield Index methodology based upon feedback received from the CSG.

3. Obtain commitments from banks to provide their funding data to IBA on a daily basis to build the Index.

4. Once steps 1-3 are complete, establish a U.S. domicile from which the Bank Yield Index would be produced on

an on-going basis.

INTERCONTINENTAL EXCHANGE 23About Intercontinental Exchange

Intercontinental Exchange (NYSE: ICE) is a Fortune 500 company formed in the year 2000 to modernize markets. ICE serves

customers by operating the exchanges, clearing houses and information services they rely upon to invest, trade and manage

risk across global financial and commodity markets. A leader in market data, ICE Data Services serves the information and

connectivity needs across virtually all asset classes. As the parent company of the New York Stock Exchange, the company is

the premier venue for raising capital in the world, driving economic growth and transforming markets.

Trademarks of ICE and/or its affiliates include Intercontinental Exchange, ICE, ICE block design, NYSE and New York Stock

Exchange. Information regarding additional trademarks and intellectual property rights of Intercontinental Exchange, Inc. and/or

its affiliates is located at http://www.intercontinentalexchange.com/terms-of-use. Key Information Documents for certain

products covered by the EU Packaged Retail and Insurance-based Investment Products Regulation can be accessed on the

relevant exchange website under the heading “Key Information Documents (KIDS).”

Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995 -- Statements in this press release regarding

ICE's business that are not historical facts are "forward-looking statements" that involve risks and uncertainties. For a discussion

of additional risks and uncertainties, which could cause actual results to differ from those contained in the forward-looking

statements, see ICE's Securities and Exchange Commission (SEC) filings, including, but not limited to, the risk factors in ICE's

Annual Report on Form 10-K for the year ended December 31, 2019, as filed with the SEC on February 6, 2020.

INTERCONTINENTAL EXCHANGE 24Important Information and Disclaimers

ICE Benchmark Administration Limited (IBA) is authorised and regulated by the Financial Conduct Authority for the regulated activity of administering a

benchmark, and is authorised as a benchmark administrator under the EU Benchmarks Regulation (Regulation (EU) 2016/1011 of 8 June 2016). ICE, LIBOR,

ICE LIBOR, ICE Swap Rate and ICE Benchmark Administration are trademarks of Intercontinental Exchange, Inc. (ICE) and/or its affiliates. All rights in these

trademarks are reserved and none of these rights may be used without a written license from ICE and/or its affiliates, as applicable.

The contents of this presentation, all associated data and information and all discussions in connection with it should not be disclosed, transmitted, distributed or

disseminated, either directly or indirectly through any third parties, to any person or entity without the express written consent of IBA. Any person receiving this

presentation in error should inform IBA immediately, destroy and disregard this presentation and not disclose, share, use or rely on it in any way. The

information and data contained herein constitutes valuable information and property owned by IBA, its affiliates, licensors and/or other relevant third parties.

ICE and IBA reserve all rights in the methodologies (patent pending) and information and data disclosed in this presentation, and in the copyright in this

presentation. None of these rights may be used without a written licence from ICE and/or its affiliates, as applicable.

This presentation is not, and should not be taken as or relied upon as constituting, financial, investment, legal, tax, regulatory or any other form of advice,

recommendation or assurance. Data and outputs relating to the ICE bank yield index are provided for information and illustration purposes only, might not be

accurate or reliable and may not be used for any other purpose. In particular, they are not currently intended for use as, and IBA expressly prohibits their use as,

an index by reference to which the amount payable under a financial instrument or a financial contract, or the value of a financial instrument, is determined, or

as an index that is used to measure the performance of an investment fund with the purpose of tracking the return of such index or of defining the asset

allocation of a portfolio or of computing the performance fees. Such outputs should not be used as a benchmark within the meaning of the EU Benchmarks

Regulation or otherwise.

The ICE bank yield index methodologies disclosed in this presentation are subject to changes in response to feedback from market participants and other

stakeholders and IBA's further development work, which might alter the information and data shown in this presentation. There is no guarantee that IBA will

continue to test the ICE bank yield index, be able to source data to derive the index or publish the index in the future. Users of LIBOR should not rely on the

potential publication of the ICE bank yield index when developing and executing transition or fallback plans.

None of IBA, ICE, or any of its or their affiliates accepts any responsibility or will be liable in contract or tort (including negligence), for breach of statutory duty or

nuisance, for misrepresentation or under antitrust laws or otherwise, or in respect of any damage, expense or other loss you may suffer arising out of or in

connection with the information and data contained in or related to this presentation or any use that you may make of it or any reliance you may place upon it.

All implied terms, conditions and warranties and liabilities in relation to the information and data are hereby excluded to the fullest extent permitted by law. None

of IBA, ICE or any of its or their affiliates excludes or limits liability for fraud or fraudulent misrepresentation or death or personal injury caused by negligence.

Trace Reporting and Compliance Engine and TRACE are trademarks of Financial Industry Regulatory Authority, Inc. (FINRA), in the US and/or other countries.

All rights reserved. See http://www.finra.org/industry/trace for further details regarding TRACE. The U.S. Dollar ICE Bank Yield Index is not associated with, or

endorsed or sponsored by, FINRA.

SOFR is published by the Federal Reserve Bank of New York (New York Fed) and is used in this presentation subject to New York Fed Terms of Use for Select

Rate Data (available at https://www.newyorkfed.org/markets/reference-rates-terms-of-use). New York Fed has no liability for your use of the data contained in

this presentation. The ICE bank yield index is not associated with, endorsed or sponsored by the New York Fed.

INTERCONTINENTAL EXCHANGE 254 UMIT KAYA

THE MILLION Partner, Finance & Risk

Umit.Kaya@oliverwyman.com

(TRILLION?) DOLLAR

QUESTION: HOW DO

WE LEND? ESTHER

BRUGGER

Principal, Finance & Risk

Esther.Bruegger@oliverwyman.comWITH ~$350BN OF REVENUES TIED TO LIBOR IN 2019, THE INDUSTRY

IS FACING A COMPLEX PRICING PROBLEM FRAUGHT WITH RISK

Outstanding USD LIBOR balances year end 2019

$5.9 TN

~$8.5TN

LIBOR balances for loans &

FRNs

~$350BN

$1.5 TN

$1.2 TN

Estimate of interest revenue

tied to LIBOR loans and FRNs

Commercial Loans Consumer Loans FRNs

Source: BIS, Bloomberg, FRB: Z.1 Release, Bank 10-K 2019 Financial Statements, Oliver Wyman Analysis

© Oliver Wyman 28ALTHOUGH SOFR HAS BEEN THE MOST VISIBLE ALTERNATIVE, OTHER

OPTIONS HAVE EMERGED WITH VARYING CHARACTERISTICS

SOFR1 ICE Bank Yield Index2 AMERIBOR3,4,5,6,7,8

Anchored in observable transactions

Acceptable to regulators / Fed (in statement on IOSCO

TBD

IOSCO compliant compliant rates)

Sufficiently deep liquid underlying +$15BN of transactions

+$1TN of daily transactions ~$2.5BN of daily transactions

market that is sustainable over 5 days

Under development,

Published daily

expected late 2020

Good representation of funding Marginal funding cost Marginal funding cost of

Overnight funding

conditions of large banks regional and community banks

Incorporates banks’ own credit spread

Term rate Under development,

Available in different tenors Under development

expected 2021 expected late 2020

Inherent volatility, can be

Not highly volatile Less volatile than SOFR Less volatile than SOFR

reduced through averages

Can be integrated into existing

Complexity will be reduced by availability of term rates

infrastructure

Active derivatives market Currently active TBD Under development

1. ARRC: https://www.newyorkfed.org/arrc; 2. U.S. Dollar ICE Bank Yield Index Test Rates: https://www.theice.com/iba/Bank-Yield-Index-Test-Rates; 3: AMERIBOR Methodology: https://ameribor.net/; 4

AMERIBOR In the News, AFX Press Release - Federal Reserve Chairman Powell Statement re AMERIBOR as a Replacement for LIBOR: https://ameribor.net/; 5. AMERIBOR in the News, AFX Press Release - AFX

Announces Record AFX Monthly Volume: : https://ameribor.net/; 6. AFP Report on AMERIBOR: https://www.afponline.org/docs/default-source/default-document-library/afpex-summer-f2-libor.pdf?sfvrsn=0;

7. CBOE AMERIBOR Futures: https://www.cboe.com/products/futures/ameribor-futures; 8. HISTORICAL OVERNIGHT AMERIBOR® RATES: https://ameribor.net/

© Oliver Wyman 29LIBOR DECOUPLES FROM THE RISK-FREE RATE DURING CRISES

Spread of 1-month LIBOR to 1-month SOFR compounded in arrears

4.5%

4.0%

3.5%

3.0%

2.5%

2.0%

1.5%

1.0%

0.5%

0.0%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Source: Bloomberg, Oliver Wyman analysis

© Oliver Wyman 30USING ALTERNATIVE RATES FOR LENDING PRESENTS NEW DYNAMIC

PRICING CHALLENGES

Implied margins to keep interest revenues equal for a 1M LIBOR +200 bps loan

Financial crisis: Post Crisis: Expansion: Pandemic: Forward-Looking

Falling rates Flat rates Rising rates Falling rates (Present–2025)

(2008–2009) (2010–2014) (2018–2019) (Mar ‘20-Present)

1M LIBOR +200 bps +200 bps +200 bps +200 bps +200 bps

1M SOFR

compounded in +270 bps +211 bps +210 bps +259 bps +215 bps

arrears

1M AMERIBOR

compounded in Not available Not available +201 bps +250 bps Not available

arrears

1M Bank Yield

Not available Not available +198 bps +196 bps Not available

Index

Source: Blomberg, ICE, AFX, Oliver Wyman analysis using LIBORITHMICSTM

© Oliver Wyman 31ON A FORWARD-LOOKING BASIS, THE UNCERTAINTY AROUND THE

RATE ENVIRONMENT WILL HAVE AN IMPACT ON SPREADS

Implied margin over SOFR for a LIBOR+200 bps floating rate loan

repricing monthly

Margin to keep interest revenues

constant under forward rates + 215 bps

Margin to keep interest revenues

constant with simulated rate uncertainty + 232 bps

Source: Bloomberg, Oliver Wyman Analysis

© Oliver Wyman 32PRODUCT FEATURES SUCH AS FLOORS CAN PARTIALLY REPLACE

HAVING TO CHARGE HIGHER MARGINS

Implied margin over SOFR for a LIBOR+200 bps floating rate loan

repricing monthly

Margin to keep interest revenues

constant under forward rates + 215 bps

Margin to keep interest revenues

constant with simulated rate uncertainty + 232 bps

Margin to keep interest revenues

constant with simulated rate uncertainty + 211 bps

and 75 bps SOFR floor

Source: Bloomberg, Oliver Wyman Analysis

© Oliver Wyman 33HOWEVER, FLOORS DO NOT WORK AS WELL IN ALL RATE

ENVIRONMENTS AND OTHER FEATURES SHOULD ALSO BE CONSIDERED

Illustrative analysis under different rate environments: Impact of Commentary

floors and spread adjustments for SOFR pricing of a term loan

50 • The gap between LIBOR

25 and SOFR can be

0 substantial and sustained in

-25

crisis situations

-50 • Spread adjustments and

rate floors can address

-75

some of the shortfall

-100

• Floors work well in low rate

-125

environments, but are less

-150

effective under high rates

2004

2012

2020

1999

2000

2001

2002

2003

2005

2006

2007

2008

2009

2010

2011

2013

2014

2015

2016

2017

2018

2019

• For lines of credit, the

problem is exacerbated due

Difference between LIBOR and SOFR to the embedded

drawdown optionality

Difference between LIBOR and SOFR with 100 bps floors

Source: Bloomberg, Oliver Wyman Analysis

© Oliver Wyman 34LOAN PRICING NEEDS TO DEAL WITH MULTIPLE RATE STRUCTURES – A

COMPLEX UNDERTAKING; WE HIGHLIGHT 5 KEY ACTIONS

There are good reasons to Product design will have to Product development will need

use most of these rates for incorporate client and bank to carefully consider multi-rate

particular types of lending strategy offerings and monitor risks

Collect client perspectives

Compounded Product development

• Understand client preferences,

SOFR in advance including operational constraints • Develop multi-rate offering as

• Understand market dynamics and needed

Compounded client price sensitivity • Assess downstream implications

SOFR in arrears

• Address analytics needs in a timely

Develop bank strategy fashion

Prime 5 Key

CMT • Determine FTP methodology and

Actions IRRBB strategy

• Release product design guidelines for

AMERIBOR businesses as needed

Monitor risks

• Assess and manage financial

Term SOFR Assess market environment implications

• Collect regulatory expectations and • Involve risk management across all

guidelines stages of product development

Bank Yield Index

• Review peer and industry

developments and innovation

© Oliver Wyman 355

CLOSING REMARKS DAN

ROSENBAUM

Partner, Retail and

Business Banking

Dan.Rosenbaum@oliverwyman.comCONTACT US

Dan Rosenbaum Adam Schneider

Dan.Rosenbaum@oliverwyman.com Adam.Schneider@oliverwyman.com

Umit Kaya Esther Bruegger

Umit.Kaya@oliverwyman.com Esther.Bruegger@oliverwyman.com

© Oliver Wyman 38You can also read