MOL GROUP INVESTOR PRESENTATION - August 2017

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MOL GROUP INVESTOR PRESENTATION August 2017

MOL GROUP IN BRIEF

INTEGRATED OIL & GAS COMPANY

Upstream Downstream Consumer Services Gas Midstream

CEE International R&M Petchem

CAPITAL MARKETS OVERVIEW BUSINESS/ASSETS OVERVIEW

Tickers: MOL HB; MOLB.BU Countries of operation: 33

Main listings: Budapest, Warsaw Number of employees: 26,000

Number of shares: 102.4mn Production (mboepd): 110

Free Float: 45% Reserves SPE 2P (MMboe): 459

MCAP (1 Aug 2017): USD 8.9bn Refineries and Petrochemical

facilities: 4+2

Liquidity (last 6M average): USD 10.2mn

Refinery capacity (mbpd): 417

Corporate bonds outstanding:

MOLHB 6 1/4 09/26/19 USD 500mn Steam cracker (ethylene) capacity (ktpa):

MOLHB 2 5/8 04/28/23 EUR 750mn 890

Dividend yield (2017): 3% No. of Service Stations: 1,900+

HSE - TRIR: 1.3 Retail transactions per day: 1,000,000

MEMBERS OF

2

AGENDA

1 Investment Case & Financial Framework

2 Q2 2017 Recap

3 Downstream

4 Consumer Services

5 Exploration and Production

6 Financials, Governance, Others

3

INVESTMENT CASE & FINANCIAL FRAMEWORK

MOL GROUP 2030: A VISION, A STRATEGY AND ONE

OVERRIDING OBJECTIVE

MOL 2030

BUILD ON EXISTING LEAD THE INDUSTRIAL LEVERAGE ON CEE

STRENGTHS TRANSFORMATION LEADERSHIP

DIVERSIFY AWAY FROM USE EXISTING MARKET

RESILIENT INTEGRATED FUELS… PRESENCE AND

BUSINESS MODEL CUSTOMER BASE

…AND GROW

HIGH-QUALITY (PETRO)CHEMICAL BUILD A CRITICAL

LOW-COST ASSET BASE EXPOSURE MARKET SHARE

SYSTEMATIC SAFETY TRANSFORM RETAIL CONQUER

AND EFFICIENCY INTO TOMORROW’S

CONSUMER SERVICES MARKETS

BEST-IN-CLASS INVESTMENT STORY

5

CONSERVATIVE MACRO ASSUMPTIONS FOR 2017-21

KEY MACRO ASSUMPTIONS EBITDA SENSITIVITY TO KEY EXTERNAL DRIVERS

Sensitivity1 Est. Clean CCS EBITDA % of Group

impact (USD mn) EBITDA 2016

H1 5Y 2017 2018-

2015 2016

2017 AVG E 21E +/‐ 50 USD/Mcm

~30 1.4%

Brent Gas Price (NCG2)

40- 40-

crude 52 44 52 75

60 60

(USD/bbl)

+/‐ 10 USD/bbl 4%

MOL

Brent price

~80

Group

5.0- 4.0-

Refining 6.1 5.7 6.5 4.7

6.0 5.0

Margin +/‐ 100 EUR/t

(USD/bbl) Integrated ~100 5%

Integr. petchem margin

Petchem 500- 400-

680 613 562 471 +/‐ 1 USD/bbl

margin 600 500

(EUR/t) MOL Group ~110 5%

refinery margin

NB:

- Sensitivity calculated for the 2017-21 period on average

- Gas price sensitivity is the net impact of E&P sensitivity (around USD 50m) and an offsetting Downstream sensitivity

- Crude price sensitivity is the net impact of Upstream sensitivity (around USD 150m, including all liquids sensitivity and also the oil price-linked gas

production sensitivity) and an offsetting Downstream sensitivity

1 Ceteris paribus for current assets assuming full re-pricing of portfolio; all other premises and volumes remain unchanged

2 Largest German trading point for natural gas (operated by NetConnect Germany) 6

SOLID, CONSISTENT EBITDA GENERATION

RESILIENT INTEGRATED BUSINESS MODEL IN A HIGHLY VOLATILE ENVIRONMENT

EXTERNAL ENVIRONMENT* VS MOL CLEAN CCS EBITDA (USD MN)

100% 800

85%

600

70%

55% 400

40%

200

25%

10% 0

Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17

Clean CCS EBITDA (r.s.) MOL Group Refining Margin Integrated Petchem Margin Brent

* The quarterly % values of the Refinery Margin, Petchem Margin and Brent price are measured against their respective

maximum values (100%) in the period of Q1 2012 – Q2 2017

100% equals to the following values:

MOL Group Refining Margin: 6.8 USD/bbl; Integrated Petchem margin: 760 EUR/t; Brent crude: 119 USD

7

HIGH QUALITY, LOW COST ASSET BASE

VERY LOW BREAK-EVEN PRICES IN BOTH UPSTREAM AND DOWNSTREAM

E&P UNIT OPEX1 (USD/BOE) MOL 2030

45

40

35

30

MOL will build on existing

USD/bbl

25 strengths

20

15

Continued relentless focus

10 on efficiency...

5

0

...to maintain competitive

H2 2013 H1 2014 H2 2014 H1 2015 H2 2015 H1 2016 H2 2016 cost position...

Range MOL Group Average MOL ...and top-tier margins in

CLEAN CCS-BASED DS UNIT EBITDA2 (USD/T) the sector...

120

...to ensure each business

100 segment achieves cash

80 neutrality even at the very

bottom of the cycle

USD/t

60

40

20

0

2012 2013 2014 2015 2016

Range

MIN MOL Group Average MOL + SN

(1) Range contains Enquest, Premier, OMV, Lundin, DNO, PGNiG

(2) Unit EBITDA range is based on volume sold and includes ELPE, Lotos, OMV, PKN, Tupras

8

CONSTANT DRIVE FOR EFFICIENCY

SUCCESSFUL EFFICIENCY PROGRAMS WITH MAJOR EBITDA CONTRIBUTION

DOWNSTREAM EFFICIENCY PROGRAMS AND CLEAN CCS EBITDA (USD MN)

~500

1,500 ~ 1,400‐1,500

~500

1,000 874

500 350

0

2011 2014 2017

NEW UPSTREAM PROGRAM (USD MN, MBOEPD)

CONTROLLABLE ~‐18% ORGANIC CEE +5%

OPEX CAPEX PRODUCTION

‐51%

877

681

81

432

79

77

2015 2016 2014 2015 2016 2014 2015 2016

9

SUSTAINED CASH GENERATION

IN 2016 AND IN THE NEXT 5 YEARS

CLEAN-CCS EBITDA (USD BN)

2.5

2.3 2.5

2.2 2.2 2.3+

0.7 2.0‐2.2

0.7

1.9

1.6 1.2

1.7

1.5

0.7 0.9 1.3 H1

0.7

0.3 0.3 0.3 0.2 0.2

‐0.3 ‐0.3 ‐0.1 ‐0.1 ‐0.2

2012 2013 2014 2015 2016 2017 YTD 2017‐21E

Average

Upstream Downstream Gas Midstream Corporate & Other (incl. intersegment) Group total

Robust EBITDA and cash generation to sustain in 2017-21E on the back of the existing

asset base

10DS: OUTSTANDING „MID-CYCLE” FCF GENERATION

WITH CONTINUOUS FOCUS ON EFFICIENCY IMPROVEMENT

CLEAN CCS EBITDA (USD MN)

1,453 1,400-1,500

~150 ~160

~410 400-500

~170

~340 ~1000

874

24

500

350

2011 NDSP Macro* 2014 NxDSP Offsetting Macro 2,3 2016 Macro NxDSP 2017 Normalized Simplified

delivered items 1 CAPEX FCF

(1) Offsetting items were incurred in 2016 and were mostly related to availability issues (unplanned shutdowns) in both petchem and refining

(2) Including offsetting items and the reversal of previous offsetting items 11

(3) Based on normalised downstream margin assumptionsGRADUAL EBITDA TRANSFORMATION

TOWARDS „HIGHER-VALUE”, STABLE CONSUMER SERVICES CASH FLOW

EBITDA TRANSFORMATION IN 2013-2030 (USD MN)

Consumer services EBITDA (USD mn)

600 40%

Weight in Group EBITDA (%), right axis

550

500 450‐500

30%

450 30%

400 ~23%

350

307

300 20%

250 221 14%

200

151 9%

150 10%

7%

100

50

0 0

2013 2015 2016 2021E 2030E

Consumer Services EBITDA more than doubled in 4 years, to triple by 2021 (vs.

2013) and to grow further through 2030

Consumer Services cash flows typically trade at materially higher multiples

(~10x EV/EBITDA for listed peers 1 and ~11.5x implied EV/EBITDA in M&A 2) vs.

integrated oils (~5-6x EV/EBITDA) or downstream cash flows

(1) Peer group includes: Alimentation Couche-Tard, CST Brands, Casey’s General Stores, Sunoco, Cross America, Murphy USA, Petrol 12

(2) Retail/distribution M&A transactions in 2014-16; Source: Bank of America Merrill Lynch ResearchE&P DELIVERS SUBSTANTIAL FCF IN 2016-21

WITH MATERIAL FLEXIBILITY ON THE CAPEX SIDE

EBITDA, CAPEX AND FCF EXPECTATIONS (2016-21, USD MN) KEY MESSAGES

Brent @ 60

USD/bbl Next 5Y post-tax free

+USD

Less than 20% of cash-flow shall cover

~750mn

the total Upstream reserve replacement

EBITDA

CAPEX pool is necessary to maintain

Brent @ 50 committed

between 2017-21

today’s production @ 50

USD/bbl

USD/bbl

Next 5Y post-tax free

2,000-2,200 cash-flow shall be

sufficient for 100% reserve

replacement @ 60

USD/bbl

3,500-3,900

1,500-1,700

~600

900-1,100 268

1,200- 1,400

EBITDA CAPEX Simplified Tax & FCF 2016 FCF Total FCF FCF to FCF to

FCF other

1 (post-tax) delivered 2016 - 21 maintainshareholders

production

2017-21 expected 2016 actual

13STRONG „SUSTAIN” CAPEX DISCIPLINE

SUSTAIN CAPEX (USD BN)1

Organic US Organic DS Organic GM Organic C&O (incl. intersegment) Group total

1.8 1.7

1.6

1.4

1.3

1.2 0.9

1.2

1.0 1.0 1.0‐1.1

Around 1.0

1.0

0.7 0.7

0.8 0.5 0.4

0.6

0.4 0.7

0.4 0.4 0.5 0.5

0.2 0.4 H1

0.0

2012 2013 2014 2015 2016 2017 YTD 2017‐21E Average

USD 1.0-1.1bn sustain CAPEX annually on average in 2017-21 with continued strong

discipline

E&P spending plans realigned to reflect new oil price reality and the benefit of

cost deflation

(1) Fact & 2017 guidance represent total organic spending of MOL Group 14ROBUST SIMPLIFIED FREE CASH FLOW

ACROSS THE CYCLE AND ACROSS ALL BUSINESS SEGMENTS

SIMPLIFIED FREE CASH FLOW1 (USD BN)

Organic US Organic DS Organic GM Organic C&O (incl. intersegment) Group total

1.5

1.8

1.6

1.1 1.2

1.4 1.1

0.0 1.3+

1.2 0.2

1.0‐1.1

1.3

1.0 0.9

0.8 1.2

0.5

0.6 1.0

0.3 0.9

0.4 H1

0.2 0.3

0.1

0.2

0.2 0.2 0.2 0.2 0.2

0.0

‐0.2 ‐0.2 ‐0.2

‐0.3 ‐0.3

‐0.2

‐0.4

2012 2013 2014 2015 2016 2017 YTD 2017‐21E Average

15

(1) Simplified Free Cash Flow = Clean CCS EBITDA – Organic CAPEX (excluding transformational spending)TRANSFORMATIONAL CAPEX

MOL 2030 STRATEGY IMPLEMENTATION

TRANSFORMATIONAL CAPEX (USD BN) MOL 2030

Refining/Chemicals transformational capex:

tbd Consumers

a total of ~USD 4.5bn until 2030

Up to USD 1.9bn spending in

petchem/chemicals in 2017‐21

tbd E&P

Steam cracker integration and

debottlenecking and new product entries

0.4 INA‐Refining

2017‐2021 projects adding USD 250‐300mn

EBITDA at mid‐cycle margins (10‐15%

~2.6 Chemicals, 2022‐2030E targeted IRR)

Potential E&P reserves replacement

(production stabilisation)

Consumer services transformational

~1.9 Chemicals, 2017‐21E

spending

Potential INA refining capex (Rijeka heavy

2017‐30E residue upgrade) subject to

fiscal/regulatory environment

16FCF TO COVER STRATEGIC CAPEX IN 2017-21

AND TO CREATE HEADROOM FOR ADDITIONAL TRANSFORMATIONAL SPENDING

NEXT 5-YEAR CASH FLOW GENERATION AMBITIONS, 2017-21 (USD BN)1

10‐11 ‐1.4‐1.6

‐5.0‐5.5

‐2.0

‐1.0‐1.3

~0.6

Clean CCS EBITDA Funding cost/tax/FX Sustain Capex Transformational Dividends FCF‐post‐dividend Optionality/Flexibility

Capex

Substantial FCF generation over sustain capex in the next 5 years...

...which may fully cover (phase-1) transformational capex, dividends, small M&A,

and more

(1) Excluding changes in working capital 17INCREASING DISTRIBUTION TO SHAREHOLDERS

SECOND CONSECUTIVE YEAR WITH DOUBLE-DIGIT DPS INCREASE

DIVIDEND PAYMENTS (HUF BN)

Special dividend

Regular dividend MOL was one of the very few integrateds

13 who could increase DPS in 2016....

...and can comfortably cover dividends

55 58 and capex from cash flows even at USD

45 46 47 50

35/bbl oil price

2012 2013 2014 2015 2016 2017

DIVIDEND PER SHARE (HUF) MOL 2030

3.6 3.5 Dividend

2.5% 2.9% 3.3% 3.0% yield1

+1% +2%

Cash dividend is the primary distribution

Special dividend +10%

channel to shareholders

Regular dividend

128 Maintain rising trend in dividend stream

and DPS

Improving yields - growing importance

625

567 in investment story

455 462 462 485

2012 2013 2014 2015 2016 2017

18

(1) Calculated with publication date (AGM) share pricesROBUST BALANCE SHEET, AMPLE HEADROOM

REMAIN A PRIORITY IN „MOL 2030”

NET DEBT TO EBITDA (X) MOL 2030

2.5

1.96 Net debt/EBITDA to be in 1.0-2.0x tolerance

2.0

1.72 range on a forward-looking basis under

1.66

1.5 1.44 1.38

„normal” circumstances (covenant

1.31

threshold at significantly higher levels)

0.97

1.0 0.88

0.79 0.74 0.75

Credit metrics to remain commensurate

with investment grade credit rating

0.5

Higher/lower leverage may be tolerated

temporarily and/or for strategic reasons,

2008 2009 2010 2011 2012 2013 2014 2015 2016 Q1 H1

2017 2017 but would trigger action plan to bring it

back to target range

AVAILABLE LIQUIDITY (30.06.2017)

Maintaining strong liquidity and

USD 3.5bn comfortable financial headroom also

3.5

0.3 remain priority

3.0 0.1

2.5

2.0

1.5 3.0

1.0

0.5

0.0

Undrawn Marketable Cash Total available

facilities securities liquidity 19SIMPLER SHAREHOLDER STRUCTURE1

HIGHER FREE FLOAT AND LIQUIDITY

Considerable increase in free-float and liquidity following the CEZ divestment (of 7.4% MOL shares)

Crescent also exited fully in Q2 2017

AGM approved 8-for-1 stock split from September 2017

MOL Plc & MOL Investment Ltd. (treasury shares)

9.3%

UniCredit Bank AG

3.6%

ING Bank N.V.

4.7% Foreign investors (mainly institutional)

34.8%

OTP Bank Plc.

4.9%

Free‐float

OmanOil (Budapest) Limited

45.1%

7.1%

Domestic institutional investors

Hungarian State (MNV Zrt.) 5.7%

25.2% Domestic private investors

OTP Asset Management 3.4%

1.2%

(1) Shareholders structure as of 30 June 2017 20MOL 2030 WORKS WITH OR WITHOUT INA

FOCUS ON SECURING RETURN ON INVESTMENT

NET DEBT (USD MN), NET DEBT/EBITDA

INA: WHAT IS UNCHANGED?

(X) AND FCF (USD MN) IN 2016*

The priority is to maximise the value of the

Full consolidation of INA INA investment:

INA as Discontinued ops

Keeping and operating INA (on fully

market-based conditions and with a

controlling position for MOL) or

Selling/monetizing the investment

Legal proceedings continue

2 064 0.97 0.96 1 140 INA: WHAT HAS CHANGED?

1 713 980

MOL 2030 strategy can be and will be

implemented with or without INA

Croatia is an EU member state since 2013,

reducing the risk of any extreme, non-

Net Debt Net Debt/EBITDA Simplified FCF**

EU-conform scenario

Decreasing relative importance of INA

First arbitration completed; all Croatian

claims rejected

* Pro-forma financials as of 31 December 2016 show INA as „discontinued operations”, while all other P&L and Balance Sheet

lines represent MOL Group excluding INA 21

** Simplified FCF = Clean CCS EBITDA less Organic CAPEXSUNSTAINABLE DEVELOPMENT; HSE COMMITMENT

“SUSTAINABILITY PLAN 2020” AND RANKING INCLUSIONS

SD GOVERNANCE SD PLAN 2020

Sustainable Development Committee of MAIN OBJECTIVE: achieve and maintain an

Board of Directors since 2006; MOL Group internationally acknowledged leading position

CEO is a permanent member (top 15%) in sustainability performance.

Executive level Thematic Sustainability FOCUS AREAS: Climate Change, Environment,

Committee in place since 2013 Health & Safety, Communities, Human Capital

and Ethics & Governance

Highest ranking individual responsible for

sustainability is SD & HSE Senior VP, directly ACTIONS: 36 in total, of which 11 new actions

reporting to the Group CEO defined solely to improve SD performance

SUSTAINABILITY INDICES AND RANKINGS TRIR*

In 2016 MOL became component of the Dow

1.8

Jones World Sustainability Index, constituent

of the FTSE4Good Emerging Index 1.5 1.4

1.3

(maintained in 2017), and included in the

RobecoSAM Sustainability Yearbook for the

second consecutive year.

MOL is a constituent of MSCI ESG Emerging LEVEL B

Market Index since 2014.

In 2016 MOL Group received a 94%

percentile ranking (outperformer) by 2013 2014 2015 2016

Sustainalytics and obtained level B (above * Total Recordable Injury Rate

industry & regional average) in the CDP

22

Climate Change rankingThis page was left blank intentionally

23Q2 2017 RECAP

MATERIALLY UPGRADED FY 2017 FCF GUIDANCE

WITH THE ESSENTIAL FUNDAMENTAL BUILDING BLOCKS IN PLACE

2017

2016 H1 2017

TARGETS

RESILIENT

GROUP CLEAN Upgraded to

INTEGRATED CCS EBITDA

USD 2.15 BN USD 1,297 MN

USD 2.3 BN+

BUSINESS

MODEL

GROUP CAPEX Cut to around

USD 1.0 BN USD 357 MN

(ORGANIC) USD 1.0 BN

FINANCIAL

DISCIPLINE

Upraded to

SIMPLIFIED FCF* USD 1.15 BN USD 940 MN

USD 1.3 BN+

SYSTEMATIC

SAFETY &

EFFICIENCY NXDSP USD 130 MN ON TRACK USD 160 MN

HIGH-QUALITY OIL & GAS

LOW-COST 112 MBOEPD 110 MBOEPD ~ 110 MBOEPD

PRODUCTION**

ASSET BASE

MOL 2030: NET DEBT/EBITDA 0.97X 0.75XROBUST FCF GENERATION CONTINUED IN Q2 2017

IN A FAIRLY SUPPORTIVE EXTERNAL ENVIRONMENT

FINANCIAL HIGHLIGHTS

Clean CCS EBITDA rose 20% to USD 684mn in Q2 2017, bringing H1 EBITDA to USD 1.3bn (+20% YoY)

Simplified free cash flow was up 30% YoY to USD 436mn in Q2 2017, as organic capex was slightly up (USD

248mn); H1 simplified free cash flow jumped by 42% to USD 940mn

Full-year 2017 guidance is upgraded to above USD 2.3bn Clean CCS EBITDA, while organic capex

guidance is reduced to around USD 1bn, implying at least USD 1.3bn simplified free cash flow for the year

Upstream EBITDA grew strongly YoY and the segment continued to generate a massive amount of FCF

(USD 158mn in Q2 only), also supported by some non-recurring revenues

Refining strength offset softer petchems, as Downstream posted flat Clean CCS EBITDA of USD 327mn in

Q2

Consumer Services continued to benefit from strong volumes growth and non-fuel contribution, as

EBITDA rose by 17% to USD 95mn in Q2 2017 (the highest on record)

Credit metrics materially improved in Q2 (Net debt/EBITDA to 0.75x, net gearing to 21%) on the strong

cash generation, some working capital release and despite the HUF 58bn dividend payment. S&P revised

the outlook to positive from stable on MOL’s credit rating.

OPERATIONAL HIGHLIGHTS

Key licence agreements were signed for core technologies of the flagship „Polyol Project”, marking the

first milestone along this major petchem transformational journey

Oil and gas production declined by 2% QoQ in Q2 2017 to 109 mboepd, driven by lower UK and Croatia

The consortium of MOL Group, E.ON Group, HEP, Petrol, BMW and Nissan (the NEXT-E project) received

EUR 19mn EU funding to build a charging network (of 250+ units) for electronic vehicles in the CEE region

26SOLID EBITDA GROWTH (+20%) IN Q2 2017

HIGHEST Q2 EBITDA SINCE 2011

SEGMENT CLEAN CCS EBITDA (USD mn) Q2 COMMENTS

+20% +11% Downstream

614 684 Strong refinery margins were offset by softer

571 petchem margins and lower petchem sales

587

506 219 228

169 488 Consumer Services

Fuel volumes, margins and rising non-fuel

337 324 327 contribution all remained tailwind in Q2 2017

Upstream

55 95

81

30 70 ‐4 37 Also helped by some non-recurring revenues

‐46 ‐55

Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017 Gas Midstream

US DS CS GM C&O (incl. inters) Higher capacity bookings offset lower tariffs

SEGMENT CLEAN CCS EBITDA YTD (USD mn) H1 COMMENTS

+20% Downstream

1,297 Record-high H1 EBITDA on very strong refining

1,078 Consumer Services

447

315

Both fuel and non-fuel enjoyed sustained growth

618 652 Upstream

Higher oil prices, lower costs boosted EBITDA

97 107

129 150

‐82 ‐58 Gas Midstream

H1 2016 H1 2017

Strong volumes (cold weather) drove EBITDA

US DS GM CS C&O (incl. inters) growth

27OUTSTANDING SIMPLIFIED FCF IN 2017 YTD

UPSTREAM DRIVING THE YOY GROWTH IN FCF GENERATION

SIMPLIFIED FCF* (USD mn) Q2 COMMENTS

Group-level simplified FCF (Clean CCS EBITDA less

+30% ‐14%

organic capex) rose by 30% in Q2 2017 to USD

505 436mn

163 436 Upstream continued to post more than impressive

336

329 37 346 158 FCF growth

289

Downstream FCF was down on higher capex

265 159 191 (partly driven by maintenance schedules)

45

71

Positive momentum in FCF generation in

63

27 70 32 Consumer Services intact in Q2

‐16

‐56 ‐62

Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017

US DS CS GM C&O (incl. inters)

SIMPLIFIED FCF* YTD (USD mn) H1 COMMENTS

+42%

Group-level simplified FCF generation jumped by

940 42% in H1 2017 to USD 940mn, already exceeding

the original full-year guidance

665 321

74 Upstream turned into a material FCF contributor

and increased FCF by more than 4x YoY despite

492 480

rather low oil and gas prices

102 115 Downstream FCF was around stable YoY

95 102

‐98 ‐78

Consumer Sevices and Gas Midstream FCF

H1 2016 H1 2017 continued to rise in H1

US DS CS GM C&O (incl. inters)

28

* Simplified Free Cash Flow = Clean CCS EBITDA – organic CAPEXDS: STRONG & STABLE CCS EBITDA IN Q2 2017 YOY

AS IMPROVING R&M CONTRIBUTION OFFSET SOFTER PETCHEM

CLEAN CCS EBITDA YoY (USD mn) COMMENTS

13 Stronger middle distillate and

337 67 34

30 327 heavy product spreads and more

69

favourable wholesale margins in

258

Petchem 166 133 R&M

Shrinking integrated margin (IM)

by 11% in petchem

R&M 171 194

Lower volumes on Slovnaft

turnaround and small-scale

availability issues

Clean CCS R&M price Petchem price Volumes Other Clean CCS CCS EBITDA

EBITDA & margin & margin EBITDA modification Q2 2017 Other items: Higher OPEX on

Q2 2016 Q2 2017 & one‐off

rising natgas prices and weaker

EUR affecting petchem

CLEAN CCS EBITDA YTD (USD mn) COMMENTS

45 6 0.8 USD/bbl complex margin

618 132 59 652 627

25 expansion and higher realized

256

prices in R&M…

Petchem 326 … only partly offset by the 117

EUR/t drop in the integrated

petchem margin

395

R&M 292 Other items: Higher OPEX on

rising natgas prices and weaker

Clean CCS R&M price Petchem price Volumes Other Clean CCS CCS EBITDA EUR affecting petchem

EBITDA & margin & margin EBITDA modification H1 2017

H1 2016 H1 2017 & one‐off

29CS: STRONG GROWTH LEADS TO BEST EVER Q2

GROWTH IN FUEL CONSUMPTION DRIVES VOLUMES AND EARNINGS

QUARTERLY EBITDA (USD mn) EBITDA YoY (USD mn)

17% 74%

6 7 98 95

112

95 18 2

81 81

67

47 55

Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017

EBITDA Q2 Fuel volume Non‐fuel Others EBITDA FX EBITDA Q2

2016 & margin margin Q2 2017 2017

(Reported) (Constant (Reported)

FX)

KEY FINANCIALS (USD mn) EBITDA YTD (USD mn)

9 8 155

Q2 2016 YoY H1 2016 YTD

Q2 2017 H1 2017

Restated Ch % Restated Ch % 25 5

129

EBITDA 95.4 81.4 17 150.2 128.8 17

150

EBIT 74.6 59.7 25 108.0 86.4 25

CAPEX and

24.7 36.0 (31) 34.8 44.4 (22)

Investments

EBITDA H1 Fuel volume Non‐fuel Others EBITDA FX EBITDA H1

2016 & margin margin H1 2017 2017

(Reported) (Constant (Reported)

FX)

EBITDA up 17% YoY mainly on the back of higher Continued roll-out of Fresh Corner supports non-fuel;

volumes and stronger margins M&A contributes

Investments related to the continued roll-out of Fresh Higher OPEX partly driven by increases to minimum

Corners during Q2 make up more than 2/3 of total wage in Hungary and Romania, impacting ~1/3 of the

CAPEX network 30E&P: OVER 40% INCREASE IN YTD CLEAN EBITDA

ON HIGHER OIL PRICES AND FURTHER IMPROVING COST BASE

UPSTREAM EBITDA QoQ (USD mn) COMMENTS

228

219 Lower Brent (-4USD/bbl) and

5 3

9 0

29 shrinking gas prices QoQ...

2

…coupled with lower

production weighted on

120

EBITDA…

…but other items more than

offset (incl. the collection of

109

USD 20mn previously

impaired trade receivables in

Egypt)

EBITDA Prices FX Volumes Exploration Lifting cost Other EBITDA Depreciation EBIT ex‐

ex‐oneoff Expenses ex‐oneoff ex‐oneoff oneoff

Q1 2017 Q2 2017 Q2 2017

UPSTREAM EBITDA YTD (USD mn) COMMENTS

447

Brent rose by 30% from the

13 37 H1 2016 lows

13

8 2

0.5 USD/bbl lifting cost

100

reduction on efficiency

315 235 improvement

Other items driven by the

collection of receivables in

212 Egypt (+USD 20mn vs H1 16)

Lower production and

EBITDA Prices FX Volumes Exploration Lifting cost Other EBITDA Depreciation EBIT ex‐ unfavorable FX moves

ex‐oneoff Expenses ex‐oneoff ex‐oneoff oneoff weighed on EBITDA

H1 2016 H1 2017 H1 2017

31

Notes: consolidated figures, unless otherwise indicatedSLIGHTLY LOWER PRODUCTION IN Q2 2017

PRIMARILY ON REDUCED FLOW RATES AT SCOLTY & CRATHES IN THE UK

QUARTERLY PRODUCTION BY COUNTRY (mboepd) COMMENTS

QoQ:

‐4% ‐2% UK: -2.3 mboepd; constrained

114.4 113.1 Scolty&Crathes production on

112.4 111.2

Estimate 7.5 109.2 109.0 wax build-up in the pipeline

8.0 8.7 ~105

Associated 3.4 8.3 8.8 8.7

2.8 3.3 2.8

companies 4.1 3.0 3.8 2.6 2.4

3.8 3.8 3.9 YoY:

Other 10.2 8.3 7.4 9.0

5.9 6.8

KRI 7.5 Inorganic: -1.5mboepd on MV

7.4 7.4 7.9

UK 1.6 1.5 0.5 8.3 8.4 divestment (Russia)

1.5 0.0 0.0

Pakistan CEE : -2.2 mboepd (o/w -0.8

Russia mboepd off-shore)

Croatia 36.8 36.2 35.2 36.9 Material growth in Pakistan

36.0 35.7

(+0.9 mboepd) and Baitugan

(+0.8 mbeopd)

UK: -1.5 mboepd on Cladhan

July production:

Hungary 44.7 44.2 44.1 44.4 42.7 43.0 Affected by maintenance in

Hungary, Pakistan and the UK

Scolty&Crathes production

issues continued

Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017 July estimate

32This page was left blank intentionally

33DOWNSTREAM STRATEGY

DOWNSTREAM: CEE STRONGHOLD

TRANSFORMATIONAL PROJECTS TO ADD USD 3/BBL BY 2022 TO THE ALREADY

OUTSTANDING MARGIN CAPTURE

MOL 2030 Downstream strategy prepares for peak fossil-fuel

demand

R&M: raising the yield of high-value non-motor fuel product to

at least 50% by 2030

Petchem: debottlenecking existing assets, increasing

feedstock offtake from refining, extending the Downstream

value chain by entering new products and markets

USD 1.9bn transformational capex in petchem in 2017-21 including a

new polyol plant and revamping two steam crackers

Focus on the efficiency and flexibility of the existing high quality,

deeply integrated, land-locked asset base

Maintain outstanding „mid-cycle” cash generation (USD 12+/bbl

margin in 2016, nearly USD 1bn simplified FCF)

Add USD 3/bbl margin through transformational projects by 2022

35DOWNSTREAM WORLD IS UNDER PRESSURE

REGULATORY ENVIRONMENT AND CHANGING CUSTOMER BEHAVIOUR CAN

SERIOUSLY AFFECT CEE REFINERS

LOW-CARBON REVOLUTION

DECLINING DEMAND AND

BACKED BY PROGRESSIVE

ENERGY POLICY1 INCREASING IMPORT IN CEE

FOSSIL FUELS PUSHED ECO-FRIENDLINESS and

OUT FROM SOME OPENNESS TOWARDS

MARKETS1 ALTERNATIVE FUELS

INCREASED IMPORTANCE OF

TRENDS & VALUES

STATE AID & SUBSIDIZATION OF

NEW TECHNOLOGIES 2

PETROCHEMICALS DEMAND TO GROW

REGULATION MARKET & CUSTOMERS

(1) e.g. ECA for Fuel Oil 36

(2) e.g.: effect of EV subsidy – share of EVs in new car sales in 2015: Norway – 20%; Netherlands – 10%; EU average: 1%PREPARING FOR PEAK FUEL DEMAND

FOSSIL FUEL DOMINANCE TO DIMINISH BY 2030, BUT DEMAND STILL SUBSTANTIAL

CHEMICALS

FOSSIL FUEL DEMAND MAY

DECLINE,

AIR TRANSPORT

BUT STILL MATERIAL

OIL-BASED FUEL

CONSUMPTION

ALTERNATIVE FUELS LIKELY TO

TRUCKS

WORLD TRENDS GAIN SIGNIFICANT MARKET

SHARE PASSENGER CARS

INCREASE EXTEND THE MOBILITY &

FLEXIBILITY VALUE CHAIN SERVICES

P RODUCE 50% I NCREASE CHEMICAL E STABLISH A NEW

VALUABLE NON FUELS AND PETROCHEMICAL BUSINESS LINE TO

PRODUCTS PRESENCE RESPOND TO

CUSTOMERS ’ NEEDS IN

MOBILITY

37PRODUCTION: 50% NON-MOTOR FUEL PRODUCTS BY 2030

FROM THE CURRENT LESS THAN 30%

MOTOR FUEL

GROUP REFINERIES YIELD PRODUCTS

2010 2015 2030 • KEEP CURRENT LEADING POSITION

• BUILD ON CURRENT RETAIL NETWORK

VALUABLE NON-MOTOR FUEL PRODUCTS

~60% ~70% • INCREASE PRODUCTION OF PETCHEM

FEEDSTOCK UP TO 3 MTPA

• TAKE ADVANTAGE OF GROWING PROFITABLE

PRODUCTS (JET, BASE OILS, LPG) MARKETS

• INCREASE OTHER CHEMICALS (E.G. AROMATICS)

~50%

50+%

OTHERS

• MINIMIZE THE PRODUCTION OF BLACK

PRODUCTS

38PETCHEM DEBOTTLENECKING TO INCREASE FLEXIBILITY

STEAM CRACKER INVESTMENTS TO INCREASE NAPHTHA INTAKE BY UP TO 800 KT/Y

CAPEX EARLIEST

PROJECT TARGET (USD mn) START-UP

• Energy efficiency and propylene yield

MPC Steam

improvement

Cracker Revamp - ~300 2020-2021

naphtha processing

NEXT FIVE YEARS

• 200kt additional naphtha off-take

400 kt/y additional

Phase 1.

• Additional 60 kt/y propylene and 70 kt/y C4 mix

PRIORITIES

MOL FCC • Increase propylene yield

80-100 2020-2021

Revamp • Additional 65 kt/y propylene

• Lifetime extension and debottlenecking to improve

Slovnaft Steam ethylene and propylene volume

~300 2021 -

Cracker Revamp • Targeted capacity is 280-300 kt/y ethylene

• 200kt additional naphtha off-take

additional naphtha

POTENTIAL

Up to 400 kt/y

processing

FUTURE

MPC Steam

• Intensification of MPC Steam Cracker-2 Too

Cracker

• Targets significant capacity extension and early to 2025

Revamp - Phase

400kt/y additional naphtha off-take define

2.

39PROPYLENE, BUTADIENE & AROMATICS ATTRACTIVE

FOR EUROPEAN NAPHTHA-BASED PRODUCERS

NORTH-AMERICA EUROPE CHINA

Shale gas developments – a Economic slowdown in Asia

Crackers will rely on more expensive naphtha

potential challenge to the turning PE exports towards

feedstock, have to focus on efficiency Europe, yet limited impact on

ethylene leg of the European

petchem industry

improvement and higher value derivatives polypropylene

ETHYLENE PROPYLENE BUTADIENE AROMATICS

Attractive due to supply High price volatility on Short in supply,

Oversupply of ethylene

constraints and do not supply-demand challenging refiners

and its derivatives

suffer from cost balance, profitable in to increase yield/

driven by cheap gas

disadvantage the long-term production

Primary focus Further possibilities being explored

REMAIN

DEFENSIVE

ATTRACTIVE DIRECTIONS TO BE EXPLOITED

40POLYOL – AN ATTRACTIVE PROPYLENE DERIVATIVE

MOL LACKS SUFFICIENT AMOUNT OF OWN FEEDSTOCK TO EXPAND IN PP

FORWARD INTEGRATION OPTIONS ALONG THE

SELECTION CRITERIA

PROPYLENE VALUE CHAIN

Other Propylene Further analysis is in progress

Derivatives Market size 1 WE/CE: 5/0.4 mt/y 2 to recognize other attractive

Others specialties

II. Polyol High degree of vertical

Semi-Commodity

Market size1 WE/CE: 1.2/0.2 mt/y integration

Polymer

Right size in terms of excess

Market growth rate3: ~1%/3%

propylene

High unit margins

I. Polypropylene

Commodity Market size1 WE/CE: 7.4/1.7 An attractive market, but

Polymer insufficient feedstock would

mt/y

not allow for economic

Market growth rate3: plant size

~1%/~2.5% Exposed to very high price

and margin volatility

(1) Market size as of 2014

(2) Propylene consumption other than I+II 41

(3) Market growth rate to 20302030: FIRST MILESTONE OF THE PETCHEM TRANSFORMATION

TEAMING UP WITH WORLD-CLASS PARTNERS FOR 200 KT/PA POLYOL PROJECT

WHAT HAS BEEN REACHED?

Key contracts signed for the purchase of technology licenses and process design packages for HPPO

technology

Fluor Corporation selected as project management consultant (PMC) for FEED, procurement and

construction phases of the project

STEAM CRACKERS POLYOL

AND REFINERY UNITS HPPO UNIT PLANT

WHAT’S NEXT?

Launch FEED (Front End Engineering and Design)

Select licensor for polyether polyol technology

Select location within Hungary

Select contractor for the engineering of utilities and facilities

Timeline (2017-21) and cost estimate (up to USD 1bn) unchanged

42ENTERING THE POLYURETHANES VALUE CHAIN

Petchem feedstock Basic chemicals Intermediates / pre-polymers Polymers

nitro-

benzene MDI/PMDI

benzene

propylene

naphtha propylene polyols polyurethanes

-oxide

nitro-

toluene TDI

toluene

PUR FORMULATORS

„SYSTEM HOUSES”

OLEFIN END-

REFINING PRODUCERS

CHEMICAL COMPANIES (R&D, technical

service, some USERS

production)

MOL GROUP DIVERSIFICATION

SPECIALISATION

current coverage organic development

43WIDESPREAD APPLICATION OF POLYOL

… AS AN ESSENTIAL POLYURETHANE COMPONENT

GLOBAL POLYURETHANE DEMAND BY

DRIVERS

INDUSTRY

% of global demand

Improving access to „essentials of life”,

increasing comfort needs

~30% Improving life expectancy and population

growth

FURNITURE &

INTERIOR

Improving energy efficiency in construction

PU have outstanding insulation

~25% characteristics, 50 – 70% less material is

required to reach same insulation value

CONSTRUCTION

Light-weight vehicles to reduce fuel

consumption

PP / PU represents 50%+ of total plastic used

~15% in car manufacturing

Average plastic content of a midrange car

AUTOMOTIVE grew fivefold since the 1970s (to up to

200kg), including ca. 20-25kg polyol today

44MOL TO BECOME THE SOLE INTEGRATED REGIONAL

POLYOL PRODUCER

POLYOL CONSUMPTION PER CAPITA

CE POLYOL SUPPPLY

(WESTERN EUROPE, 2016 = 100%)

Crude Steam

Polyol

processing cracking

W e s t e r n ‐Europe

110% E a s t e r n‐Europe

100% 90%

65%

Current CE PO

producers

2016 2025

Supply: Demand:

CE producers lack backward-integration… Central European demand is expected to

… and existing CE polyol capacity is grow ~3% vs ~1% in Western Europe…

chlorohydrin based – a declining technology … yet there may still be a substantial per

due to its high cash cost and environmental capita consumption gap by 2025

issues

No ongoing capacity addition project in

Europe

45ATTRACTIVE VALUE CHAIN EXTENSION

WITH 900-1,000 USD/T ADDITIONAL MARGIN CAPTURE OPPORTUNITY

PROPYLENE VS. POLYOL SPREADS1

CE POLYOL MARKET CHARACTERISTICS

(USD/T)

Relative deviation: PP – propylene: 47%

S u p p ly PO – propylene: 13%

Demand ~3% CAGR 1.200

1.000

~80kt

deficit 800

~150

currently

600

400

200

0

Current ~2025 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

source: MOL Group

Polyol (low) ‐Propylene Spread Polypropylene ‐ Propylene spread

Supply–demand balance: Margin exposure:

Central Europe in net import position and Average historical PO–PP spread is 800-1,000

drives European demand growth USD/t

MOL Group is expected to be a front-runner on Polyol is cyclical, but profit generation

the Central European cost curve (margin/spread) is significantly less volatile than

that of polypropylene

(1) Monthly nominal quotations

46~USD 1.9BN EARMARKED FOR PETCHEM UNTIL 2021

PROVIDING ~2 USD/BBL ADDITIONAL EBITDA CAPTURE IN DOWNSTREAM

EARMARKED CAPEX FOR PETROCHEMICAL GROWTH PROJECTS (2017-21, USD MN)

~1,800-2,000

Annual incremental

900-1,000 1,500-1,700 EBITDA1 of USD 250-300mn

from growth projects

• Growth CAPEX shall be

covered from operating

600-700 cash-flow

• Projects to be

committed if meeting

10-15% IRR target

Steam cracker Polyol Other growth Total

intergration & opportunities

others

Potential

CAPEX high

lower

variation

level:

(1) Annual EBITDA contribution calculated based on average historic margin levels 47

(2) EBITDA uplift per barrel calculated over 19 mT p.a. processed volume2030 STRATEGY AND 2030 CULTURE

VISION

VALUES STRATEGY

STANDARDS GOALS

CULTURE

2030 STRATEGY

ENTER

TOMORROW

COMPETENCY ACTIONS

BEHAVIOUR PROCESSES

RESULT

48This page was left blank intentionally

49DOWNSTREAM OVERVIEW

INTEGRATED DOWNSTREAM MODEL IN CEE

12 COUNTRIES

SALES OF 18 mtpa REFINED PRODUCTS

AND 1.25 mtpa PETROCHEMICALS

TO OUR WHOLESALE CUSTOMERS

WORLDWIDE ANNUALY

15,000

SERVICE STATIONS

1,900+

FUEL SOLD

~5.2 bnliters

51DEEP DOWNSTREAM INTEGRATION

HIGH-QUALITY LAND-LOCKED ASSETS WITH OUTSTANDING MARGIN CAPTURE

MARKET SHARE (%)1 DOWNSTREAM INTEGRATION (FUELS)2

~24%

CRUDE INTAKE:

• Russian: ~40%

67%

• Seaborne:

25% ~85%

• Own

Refining ~80%

production: ~36%

8% captive

Retail ~45% market3

own

~15% market

PetchemOVER 12 USD/BBL MARGIN CAPTURE IN 2016

FURTHER ~3 USD/BBL UPLIFT POTENTIAL FROM PETCHEM & CONSUMERS

DOWNSTREAM (W/O INA) CAPTURED EBITDA MARGIN (USD/BBL)

~1

~2

12.3

2.0

Sales

margin

4.6

~5 USD/BBL delivered

through internal

efficiency

Bulk improvement (2012-16)

margin

5.7

R&M gross R&M OPEX R&M Petchem Retail1 2016 First wave Consumer Oil world Further 2022

margin EBITDA of petchem services decline efficiencies EBITDA

investments

(1) Part of Consumer Services 53NXDSP: USD 350MN ASSET&EFFICIENCY IMPROVEMENT

ADDITIONAL USD 150MN TARGETED FROM GROWTH PROJECTS

EFFICIENCY IMPROVEMENT GROWTH PROJECTS’ CONTRIBUTION 2

1

(CUMULATIVE, MN USD) (MN USD)

350 Production

USD ~270MN 1. Availability & USD ~70MN DELIVERED SO FAR

DELIVERED SO FAR maintenance (ONLY USD 10MN IN 2016),

2. Production flexibility BELOW OUR TARGETS

and yield

improvements

A

230 3. Energy management $150MN

Production

4. Hydrocarbon loss Butadiene: 130 ktpa capacity

management Butadiene Extraction Unit

LDPE: 220 ktpa capacity LDPE in

Supply & sales

Slovnaft

1. Develop market access ~55%

110 2. Develop market

B IES

presence

IES refinery conversion completed

3. Logistics

~25%

Retail

C Retail

1. Step change in non‐fuel

2. Solid fuel flow ~20% Over 250 service stations acquired in

3. Portfolio optimisation Czech Republic, Slovakia & Romania

2015 2016 2017

2017 vs

2014

NxDSP delivery figures exclude offsetting items 54OUTSTANDING „MID-CYCLE” FCF GENERATION

WITH CONTINUOUS FOCUS ON EFFICIENCY IMPROVEMENT

CLEAN CCS EBITDA (USD MN)

1,453 1,400-1,500

~150 ~160

~410 400-500

~170

~340 ~1000

874

24

500

350

2011 NDSP Macro* 2014 NxDSP Offsetting Macro 2,3 2016 Macro NxDSP 2017 Normalized Simplified

delivered items 1 CAPEX FCF

(1) Offsetting items were incurred in 2016 and were mostly related to availability issues (unplanned shutdowns) in both petchem and refining

(2) Including offsetting items and the reversal of previous offsetting items 55

(3) Based on normalised downstream margin assumptionsCONSTANTLY IMPROVE EFFICIENCY AND AVAILABILITY

~96,0% 96+%

EXTEND TURNAROUND CYCLES

94.7%

SYSTEMATIC IMPROVEMENT

OF MECHANICAL INTEGRITY

RELIABILITY AWARENESS

MIND-SET AMONG WORKERS

2014 2018 2020

REFINING OPERATIONAL ONE-QUARTILE IMPROVEMENT 50%+ OF NON MOTOR FUELS

AVAILABILITY TO ~96% IN COST EFFICIENCY2 IN REFINERY YIELD

2018 2018+ 2030

CRUDE FLEXIBILITY:

2ND QUARTILE IN ENERGY

INCREASE ASSETS FLEXIBILITY 33% SEA BORNE

INTENSITY INDEX1

50+ QUALITIES

50+ INITIATIVES ALREADY IMPLEMENTED

OPERATIONAL OPTIMIZATION

SELECTED INVESTMENTS

(1) In the Western Europe Group of the Solomon Study, (2) In the Central and Southern Europe Group of the Solomon Study

56~19% SEABORNE CRUDE TO DANUBE REFINERY IN 2016

FIRST SEABORNE CARGO PROCESSED IN BRATISLAVA IN 2016

ADRIATIC PIPELINE ACCESS ESTABLISHED CRUDE DIVERSIFICATION1

Increased

pipeline

capacity:

6Mtpa = SN

REB

97% 75%

Seaborne

Increased 3% 25% 33%

pipeline capacity:

14Mtpa = MOL+SN

2011 2016 2020

ENHANCING FEEDSTOCK FLEXIBILITY

Number of purchased cargos* through

Majority of the crude intake remains Ural, however, the number

Adria pipeline for landlocked refineries

of tested crudes in the complex refineries is on the rise

Targeting further increasing seaborne crude oil supply to 33%

with widening crude basket to reach 50 types by 2020

19-25 Following the successful rehabilitation and expansion of the

15 17 Friendship 1 pipeline, seaborne crude oil delivery to Slovnaft was

8 launched in 2016

3 Opportunistic approach based on continuous optimization -

2012 2013 2014 2015 2016 2017E capturing benefits of fluctuating crude spreads

57

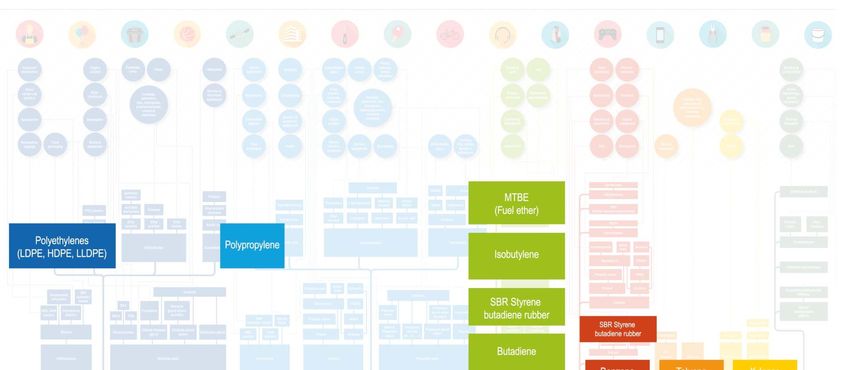

* One cargo is equivalent of 80kt crude; (1) Group level, including INAPETROCHEMICALS IN MOL’S INTEGRATED

DOWNSTREAM VALUE CHAIN

RELEVANT POLYOLEFIN CAPACITY IN

MOL’S PETROCHEMICALS VALUE CHAIN

EUROPE (2015 KTPA)

Capacity

LyondellBasell

Borealis

420 kT HDPE SABIC Europe

INEOS

Total Petrochemicals

285 kT LDPE Repsol

MOL Group 1.200

ExxonMobil

Refining Petchem 535 kT PP Basell Orlen

Kazanorgsintez

Internal feedstock1: Versalis

~1.5 Mt in 2015 350 kT Aromatics2

Chemopetrol

Braskem

Dow

Sibur

130 kT Butadiene 40kT SSBR

LDPE, HDPE, PP capacity source: MOL Group

LDPE4: 220 ktpa unit replaced three old ones in Bratislava in 2016

Butadiene: 130 ktpa unit commissioned in 2016

SSBR: 60 ktpa unit is under construction (49% MOL stake)

(1) Considering steam cracker feedstock (naphtha & LPG) from Danube & Bratislava refineries only

(2) Considering 2015 production 58SEVERAL OPTIONS TO EXPAND ALONG THE VALUE CHAIN Polyethylenes (LDPE, HDPE) source: www.petrochemistry.eu 59

CONSUMER SERVICES

A LEADING REGIONAL NETWORK

USD 307MN EBITDA IN 2016

CZECH R.

MARKET LEADING MARKET POSITION: 2

MARKET SHARE: 20% SLOVAKIA

MARKET POSITION: 1

IN 60% OF THE NETWORK MARKET SHARE: 47%

TOP 3 HUNGARY

MARKET POSITION: 1

IN 90% OF THE NETWORK MARKET SHARE: 44%

SLOVENIA

MARKET POSITION: 3

10 COUNTRIES1 MARKET SHARE: 10% ROMANIA

MARKET POSITION: 3

MARKET SHARE: 20%

7 WELL ESTABLISHED BRANDS

ITALY2

MARKET POSITION: N/A

1,900+ MARKET SHARE: 50% MARKET POSITION: 1

MARKET SHARE: 14%

~1 MN TRANSACTIONS / DAY

CORE 5 COUNTRIES REFINERY

(1) Montenegro (1 station) is not included in the map, (2) Italy is not considered anymore as core market 61

Market share sources: Hu, Ro, Sk, Cz – oil association share (incl. Eni), Slo – retail market share (incl. Eni), Cro, Srb, BiH – own estimationA VALUE GENERATING NETWORK…

…AS EBITDA PER SITE ALMOST DOUBLES

EBITDA (REPORTED, USD MN) NORMALIZED FCF (USD MN1)

0

56

193 200

29

179

307 126

204 221

151

2013 2014 2015 External Internal FX 2016 2013 2014 2015 2016

EBITDA (CONSTANT, USD MN 2) EBITDA PER SITE (USD TH1) COMMENTS

164 Fuel is still the main EBITDA

307 growth contributor:

119 123

221 Fuel margins, strong fuel

87

170 consumption main drivers

120

Recent M&A contributes

Contribution of non-fuel

2013 2014 2015 2016 2013 2014 2015 2016 increasingly on the rise

(1) Based on Reported Figures 62

(2) Constant USD Figures at FX 2016FUEL SALES ON THE RISE

GROWTH MOSTLY DRIVEN BY RISING CEE FUEL CONSUMPTION; M&A CONTRIBUTES

M&A DRIVEN NETWORK EXPANSION FUEL SALES (MN LITERS)

CZECH R. HUNGARY

SLOVAKIA

ROMANIA

SLOVENIA 5,239

BOSNIA

MONTENEGRO

4,837

SLOVENIA CZECH R.

SLOVENIA CZECH R. 4,292 4,323

ITALY CROATIA

BOSNIA

CROATIA

AUSTRIA

1861 1967

1658 1558 1574 1690 1686 1664

999 1076

772

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2013 2014 2015 2016

CEE1 MOTOR FUEL DEMAND FUEL THROUGHPUT PER SITE

COMMENTS

(2008 = 100%) (MN L/SITE)

1.10

2.84 2.94 Rising fuel consumption and

2.76

1.05 2.52 constantly optimized network drive

rise in throughput

1.00

Future M&A an option likely outside

0.95

“domestic” markets (Slovakia,

0.90 Hungary and Croatia), but always

within the supply radius of refineries

0.85

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

2013 2014 2015 2016

YTD

63

(1) Hungary, Slovakia, Croatia, Slovenia, Czech Rep., Romania, Bosnia-H., SerbiaNON-FUEL INCREASINGLY A GROWTH DRIVER

CONCEPTUAL CHANGE, COCO/A OPERATING MODEL SUPPORT GROWTH

NEW CONCEPT AND A COMPLETE REVAMP NON-FUEL SHARE OF TOTAL MARGIN GROWTH (%)

Introducing a non-fuel concept: FRESH CORNER

37

24

4

SKUs heavily reduced and optimized 2

Focus on coffee, fresh food, everyday groceries

2013 2014 2015 2016

Positive customer response

TOTAL NUMBER OF FRESH CORNERS NON-FUEL AS % TOTAL MARGIN

331 24

303 22

248 19 21

167

91

6 22 23 42

Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 2017 2013 2014 2015 2016

642021 STRATEGIC PRIORITIES

EXPLOIT POTENTIAL IN FUEL, ACCELERATE SHIFT TOWARDS NON-FUEL

RETAIL MARGIN DEVELOPMENT 2021 STRATEGY

ACCELERATE SHIFT TOWARDS NON-FUEL

5 DRIVEN AND OMNI-CHANNEL2 OFFERING

3 4

24% 2

1 EXPLOIT FUEL POTENTIAL: IMPROVE

FUEL QUALITY AND BRAND MESSAGING

76%

1 1 2 CONTINUOUSLY IMPROVE OPERATIONS:

CATEGORY MANAGEMENT, LOYALTY,

PURCHASE PRICE MANAGEMENT ETC.

2016 2021

Non‐fuel Fuel 3 OPTIMIZE/CUSTOMIZE STORE FORMAT,

AND IMPROVE OFFERING/SERVICES

EBITDA (CONSTANT, USD MN1)

450

4 ENTER COFFEE SHOPS AND

CONVENIENCE STORES BUSINESS

307

221

170 5 GO ONLINE AND COMPLETE DIGITAL

120 ... TRANSFORMATION

2013 2014 2015 2016 2021

(1) At constant avg. 2016 USD FX.

(2) A multichannel approach to sales that seeks to provide the customer with a seamless shopping experience

65

whether the customer is shopping online from a desktop or mobile device, by telephone or in a store.EXPLORATION AND PRODUCTION STRATEGY

E&P BUSINESS SUCCESSFULLY REBALANCED

CREATING VALUE AT ~50 USD/BBL OIL PRICE

7 USD/boe free cash-flow delivered in

2016 on the back of the successful New

Upstream Program implementation

Production to peak at ~115 mboepd in

2018/19

E&P business shall seek for inorganic

expansion possibilities to replace

reserves

2016-21 post-tax free cash-flow:

shall cover reserve replacement

necessary to maintain today’s

production @ 50 USD/bbl

shall be sufficient for 100% reserve

replacement @ 60 USD/bbl

EXPLORATION PRODUCTION

67TOP 15% IN SUSTAINABILITY

A COMMITMENT TO THE INTEGRATION OF ECONOMIC, ENVIRONMENTAL AND SOCIAL

FACTORS INTO EVERYDAY OPERATIONS

HEALTH & SAFETY WE OPERATE SAFELY OR WE DON’T OPERATE

IMPLEMENTING ACTIONS AIMING AT ZERO

INCIDENTS AND ZERO FATALITIES 1

ENVIRONMENT

REDUCE THE NUMBER OF SPILLS (OVER 1

CUBIC METER) BY 30%

CLIMATE CHANGE

DECREASE GHG EMISSIONS FROM FLARING

BY ~33% 2

HUMAN CAPITAL

INCREASE EMPLOYEE ENGAGEMENT LEVEL +

FURTHER DEVELOP AND UTILIZE

TECHNICAL CAREER LADDER IN UPSTREAM

(1) Lost-time injury frequency, own and on-

site contractors LEVEL B 68

(2) Tons in CO2 equivalentPRODUCTION IN 8 COUNTRIES

RUSSIA

Reserves: 50 MMboe

CEE TOTAL Production: 6.4 mboepd

Croatia, Hungary KAZAKHSTAN

Reserves: 262 MMboe Reserves: 60 MMboe

Production: 78.7 mboepd

PAKISTAN

o/w CEE offshore Reserves: 10 MMboe

Reserves: 10 MMboe Production: 8.3 mboepd

Production: 8.4 mboepd

OTHER

INTERNATIONAL

UK, NORTH SEA Egypt, Angola, Kurdistan

Reserves: 23 MMboe Region of Iraq, Syria

Production: 7.9 mboepd Reserves: 55 MMboe

Production: 6.3 mboepd

PRODUCTION BY COUNTRIES AND RESERVES BREAKDOWN BY COUNTRIES

PRODUCTS (MBOEPD; H1 2017) AND PRODUCTS (MMBOE; 2016 YEAR END)

16% 9% 14% 10%

23%

5%

7% 41% 42% 43%

6% 110 110 459 459

24%

50% 47%

34%

33%

Hungary WEU (North Sea) Oil Hungary WEU (North Sea) Oil Condensate

Croatia MEA & Africa Gas Croatia MEA & Africa Gas

CIS Condensate CIS 69

Note: Group production figures include consolidated assets, JVs (Baitex in Russia, 6.4mboepd) and associates (Pearl in the KRI, 2.4mboepd)7 USD/BOE FREE CASH-FLOW DELIVERED IN 2016

ON THE BACK OF SUCCESSFUL NEW UPSTREAM PROGRAM IMPLEMENTATION

2016 2016

TARGET FACT

Material CEE onshore growth

on Production Optimization

PRODUCTION1

105-110 112 (110) 1 Higher UK volumes, growth in

Mboepd low-cost Russia, Pakistan

YoY production growth fully

liquids-driven

Around USD 90mn opex (incl.

UNIT OPEX

6-7 6.6 (6.3)2 G&A) reduction delivered in 2016

USD/boe

Opex declined across the board

NEW

UPSTREAM

PROGRAM ORGANIC Exploration capex down by

CAPEX C. -15-30% -36% 70%+ in 2016

Achieved at the bottom of

FREE CASH the cycle (USD 44/bbl

FLOW POSITIVE USD 268mn Brent in 2016)

Actively seeking to secure new, attractive and low-cost exploration

acreages

Notes: consolidated figures, unless otherwise indicated; FCF/boe is calculated as (EBITDA-CAPEX)/ Consolidated production

(1) Reported Group production now includes „JVs and associates” including ~2.4 mboepd from Pearl Petroleum, while the

original 2016 target did not include production related to Pearl

(2) Reported Opex now includes only „Consolidated subsidiaries”, while the original target was set including Baitex, FED too 70

(now among „JVs and associates”)PRODUCTION TO STABILIZE AT ~110 MBOEPD UNTIL 2019

~10-15 MBOEPD NEEDED TO SUSTAIN PRODUCTION BEYOND 2020

MID-TERM PRODUCTION PROFILE KEY MESSAGES

(MBOEPD)

120

112 ~110-115 Stable contribution from CEE

~110 ~110 New

104 ~10-15 barrels Impact of successful production

required

100 optimization and EOR

Pursue transfer of undeveloped reserves

and EOR opportunities

80

Capturing value from international projects

60

Continue field development in TAL (PAK)

and Baitugan (RUS)

~95-105

Development and infill projects to

40 contribute to production growth in the UK

New barrels (~10-15 mboepd) will be required

20

to at least sustain today’s level of production

0

2015 2016 2017 2018 2019 2020-2021

Rest CEE Production guidance

71

Note: figures include consolidated assets, JVs and associatesE&P DELIVERS SUBSTANTIAL FCF IN 2016-21

WITH MATERIAL FLEXIBILITY ON THE CAPEX SIDE

EBITDA, CAPEX AND FCF EXPECTATIONS (2016-21, USD MN) KEY MESSAGES

Brent @ 60

USD/bbl Next 5Y post-tax free

+USD

Less than 20% of cash-flow shall cover

~750mn

the total Upstream reserve replacement

EBITDA

CAPEX pool is necessary to maintain

Brent @ 50 committed

between 2017-21

today’s production @ 50

USD/bbl

USD/bbl

Next 5Y post-tax free

2,000-2,200 cash-flow shall be

sufficient for 100% reserve

replacement @ 60

USD/bbl

3,500-3,900

1,500-1,700

~600

900-1,100 268

1,200- 1,400

EBITDA CAPEX Simplified Tax & FCF 2016 FCF Total FCF FCF to FCF to

FCF other

1 (post-tax) delivered 2016 - 21 maintainshareholders

production

2017-21 expected 2016 actual

72THE MINIMUM ASPIRATION TO SUSTAIN PRODUCTION

BUT IT HAS TO MAKE ECONOMIC SENSE

PRO-FORMA 2016-21 2P RESERVES EVOLUTION (MMBOE) KEY MESSAGES

514 514 Sustain at least current

100%

RRR level of production to

maintain the integrated

100‐105

business model of MOL

170‐175 Group

Maintain

production

65‐75 Organically this is not

feasible...

...although Norwegian

exploration portfolio

provides upside potential

in the mid-term

2015 YE 2P Production (2016‐ Reserves needed to Reserves needed Reserves after 100% RR

Booked Reserves 2021), divestment maintain ~110 to reach 100% RR

& organic bookings mboepd production

73EXPLORATION AND PRODUCTION OVERVIEW

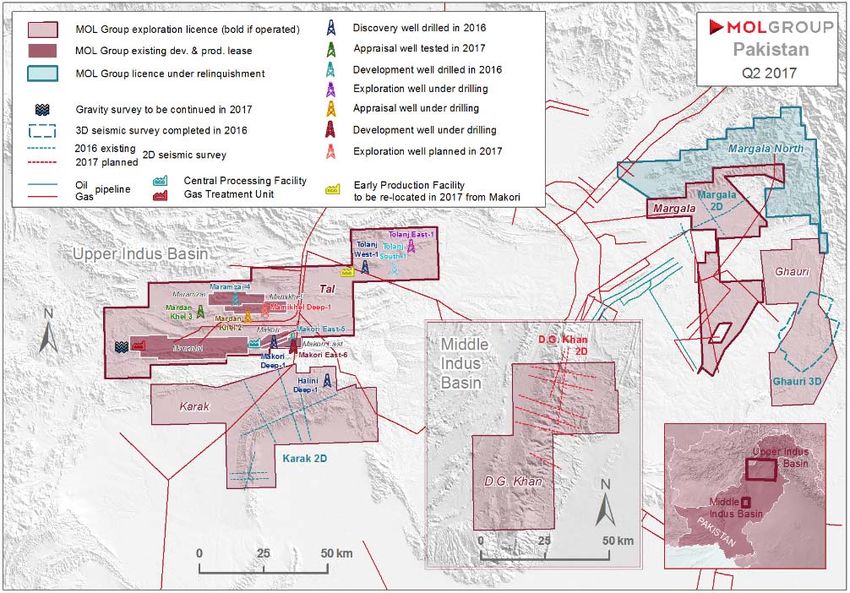

BALANCING THE PORTFOLIO IN THE MID-TERM IS A

CHALLENGE

Time to first oil 1-3 years 4-5 years 5+ years

KEY MESSAGES

Pakistan

Hungary Hungary Norway

Exploration

Croatia Limit ExpEx to nearfield

FED Croatia

exploration in CEE and

Pakistan as well as to high-

impact Norway

Limited development

project pipeline

Croatia

New development projects

FED

are required

Baitex

Croatia Baitex Pakistan

Development

FED Hungary Hungary

Pakistan

Hungary Croatia

UK

FED

2P reserves additions (from exploration projects) &

Developed reserves increase from current undeveloped 2P (development projects)

75STRICT COST DISCIPLINE TO CONTINUE

CAPEX SPENDING IN THE NEXT 5 YEARS

DIRECT UNIT OPEX (USD/BOE)

(USD BN) 1, 2

2.0-2.2

Exploration ~20%

9

2013-14

average

@ 8.0

USD/bbl

8

Development ~55%

7

6

Other ~25%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2013 2014 2015 2016 2017 2018

(1) Incl. a total USD 800mn ABEX, sustain CAPEX and production intensification expenditures

(2) Exploration CAPEX excludes Norway

76

Note: consolidated figuresCEE: STRONG CASH FLOW, HIGHER ONSHORE PRODUCTION

ON THE BACK OF COMPREHENSIVE PRODUCTION OPTIMIZATION PROGRAM

HUNGARY AND CROATIA (105+156 MMBOE) Production

100

Employed a systematic approach to identify improvement

potential in both surface and subsurface 80

CAGR ex

Production optimization through increased number of well

mboepd

offshore

workovers and well interventions 60

Target maximum transfer of undeveloped reserves with 40 1%

scrutiny on breakeven prices

20

Pursue further EOR opportunities

Extension of exploration capacity in Hungary thanks to recently 0

acquired new licences 2014 2015 2016 2017F 2018F 2019F

Continue nearfield exploration looking for new play concepts Hungary CRO onshore CRO offshore

77PAKISTAN: 15+ YEARS OF SUCCESSFUL OPERATION

HIGHLY SUCCESSFUL TAL DEVELOPMENT WITH EXPLORATION IN NEARBY BLOCKS

HIGHLIGHTS AND KEY FOCUS AREAS

(10 MMBOE)

Operator of the TAL block around 80 km from the

border of Afghanistan, where production exceeded 80

mboepd on 100% basis in Q1 2017

13 discoveries (9 operated) since 2000, over 400 MMboe

discovered (@ 100%)

Nr. 1 LPG, Nr. 2 oil and condensate and Nr. 5 natural gas

producer in Pakistan (TAL @ 100%)

Present in 4 blocks (Karak, Ghauri, Margala, DG Khan)

near TAL block in the Upper and Middle Indus area

Production in a growing trend following series of tie-ins

from new discoveries

Stable cash generation

Pursue new licences

OTHER

BLOCK W.I. OPERATOR

PARTNERS

Production Tal 10.53% (expl.) MOL PPL, OGDCL,

8.42% (dev.) POL, GHPL

10

Karak 40% MPCL

8

mboepd

Margala 70% MOL POL (30%)

6

Ghauri 30% MPCL PPL (35%)

4

DG Khan 30% POL

2

0

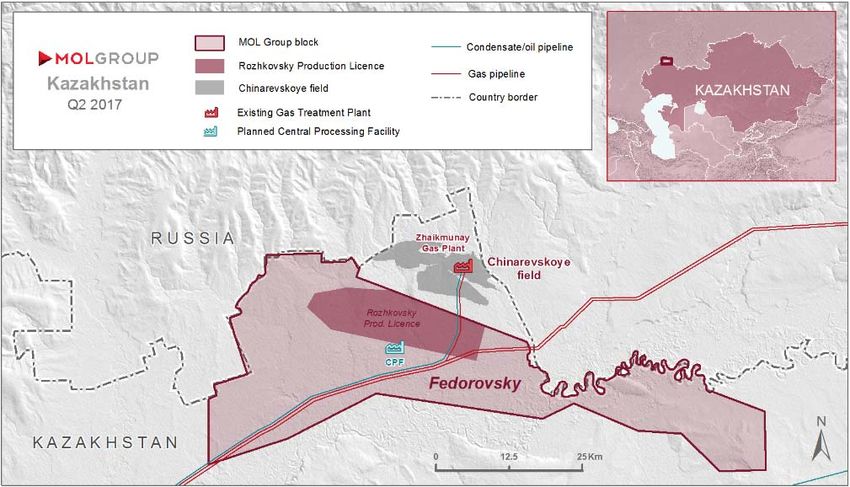

2014 2015 2016 2017F 2018F 2019F 78CIS: FIELD DEVELOPMENT OF LOW-COST BAITUGAN

WITH STABLE CASH FLOW GENERATION EVEN AT CURRENT OIL PRICES

RUSSIA (50 MMBOE) - Baitugan

A shallow, compact field with developed infrastructure ensures low unit

costs thus stable cash-flow generation

Ongoing intensive development program to be pursued in the future on

Baitugan block to maintain production growth (~20% increase in 2016)

Investigating options to improve the ultimate recovery factor

Wide well-workover campaign and infrastructure development program

started in 2016

KAZAKHSTAN (60 MMBOE)

The drilling of the U-25 well was completed

Lower Tournasian layer was tested for gas and

condensate. Upper Tournasian was fracked and

tested gas and condensate.

Surface engineering works will be carried out at

Rozhkovsky gas condensate discovery in the frame

of Trial Production Project (TPP)

79NORTH SEA, UK: VISIBLE CONTRIBUTION IN 2016

WITH AN ONGOING COMPREHENSIVE VALUE OPTIMIZATION PLAN

NORTH SEA, UK (23 MMBOE)

First oil achieved on Scolty and Crathes in November

2016 ahead of schedule and significantly below budget

Scott: infill drilling which commenced in 2016 will

continue throughout 2017

Catcher:

The 2016 drilling programme was successfully

completed with good operational and subsurface

results for all 6 wells

The 2016 subsea programme was successfully

completed with all major subsea equipment now

installed

5 additional wells, the remaining subsea tie-in

scope and completion of construction activities for

the FPSO are planned for 2017

Production

15

10

mboepd

5

0

2014 2015 2016 2017F 2018F 2019F

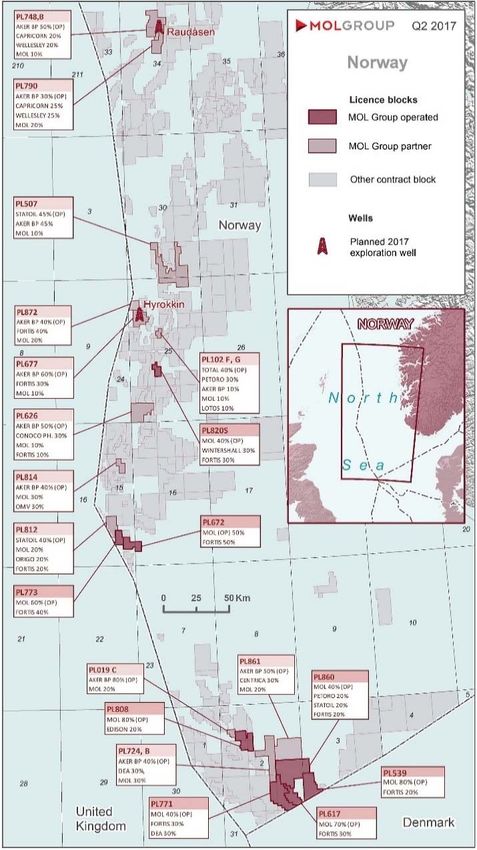

80NORWAY: A NEW EXPLORATION HUB

INCREASING FOOTHOLD IN THE NCS

Entered Norway in 2015, acquiring 100% ownership in

Ithaca Petroleum Norge – a pre-qualified operator

Successfully participated in the 2015 and 2016 APA

licensing rounds and acquired further eight licences

Currently has 20 exploration blocks (8 operated) on

the Norwegian Continental Shelf (NCS)

Key focus to mature prospectivity and high grade the

prospect inventory within core areas of the North Sea

Partnering strategy (sharing risk, financial exposure

and experience with best in class North Sea explorers)

Developing a new offshore exploration hub and centre

of excellence for the Group, building on the

experience of a strong exploration-focused team

3 Core areas are targeted in the North Sea (Central

Graben South, South Viking Graben, Northern North

Sea)

81FINANCIALS, GOVERNANCE, OTHERS

SOURCES AND APPLICATIONS OF CASH

SOURCES AND APPLICATIONS OF CASH, 2012-17 (USD MN)

180

‐549 284

666 521

407

579

459

196 950

205 270

200

202

456 420 302

2 524 370

2 477

2 308 2 300 350

164 2 183 2 153 111

1 689

1 211 1 258

1 034 1 011 1 000

2012 2013 2014 2015 2016 2017E

Clean CCS EBITDA Organic CAPEX Inorganic CAPEX Interests & Taxes Dividend (De)leveraging & Other

EBITDA/CAPEX gap should comfortably cover taxes, cost of funding, rising dividends and

small-size M&A...

...and would also contribute to funding the upcoming transformational projects

83STRONG BALANCE SHEET AND LIQUIDITY

DRAWN VERSUS UNDRAWN FACILITIES

AVAILABLE LIQUIDITY (30.06.2017)

(30.06.2017)

USD 3.5bn

3.5

0.3

3.0 0.1

2.5

2.0

1.5 3.0

1.0

0.5

0.0

Undrawn Marketable Cash Total available

facilities securities liquidity

NET DEBT TO EBITDA GEARING (%)

2.5 40

36

35 33

2.0 1.96 31

1.72 30 28

1.66

25 25 24

1.5 1.44 1.38 25

1.31 21 21

20

20

0.97 16

1.0 0.88 15

0.79 0.74 0.75

10

0.5

5

0

2008 2009 2010 2011 2012 2013 2014 2015 2016 Q1 H1 2008 2009 2010 2011 2012 2013 2014 2015 2016 Q1 H1

2017 2017 2017 2017

84AMPLE FINANCIAL HEADROOM

FROM DIVERSIFIED FUNDING SOURCES

AVERAGE MATURITY OF 3.46 YEARS

1,500 Reported cash & cash equivalents Medium term loan Undrawn facilities

Senior Unsecured Bonds Long term loan (multilaterals)

1,000

575

1,275

500 41

464 702 856

467 500

0 21 112 41 22 22 13

Reported 2017 2018 2019 2020 2021 2022 2023

cash&cash

equivalents

MID- AND LONG-TERM COMMITTED FIXED VS FLOATING INTEREST RATE

FUNDING PORTFOLIO PAYMENT OF TOTAL DEBT AS OF 30.06.2017

Other bilateral loans Floating Fixed

2% Syndicated / club loans drawn 100

Multilateral loans 1%

3% 80 41% 34% 41%

Senior unsecured bonds 60

29% 100%

40

59% 66% 59%

20

0

Syndicated / club loans undrawn HUF & Other EUR USD Total

65%

85DOUBLE INVESTMENT GRADE RATING ACHIEVED

TO MAINTAIN CURRENT IG RATINGS AND AIMING FOR AN UPGRADE AT S&P

HISTORICAL FOREIGN LONG TERM FFO ADJUSTED NET LEVERAGE

RATINGS (3Y AVG. 2014-2016)

MOL Fitch MOL S&P MOL Moody's (BBB‐)

1.7

BBB+ Baa1

(A‐) 2

Baa2

BBB

BBB‐ Baa3 (A‐) 2.2

BB+ Ba1

(BBB‐) 2.2

BB Ba2

3.5

(BBB)

0 0.5 1 1.5 2 2.5 3 3.5

Source: www.fitchratings.com, for ENI Spa avg. 2013-2015

Standard & Poor’s revised outlook to positive from stable on MOL’s credit rating (BB+ LT

corporate credit rating affirmed on 20 July)

New Moody’s Baa3 investment grade rating received on 31 March

BBB- (Stable outlook) by Fitch Ratings

MOL’s strong financials are visible even among better rated peers

Note: S&P has been rating MOL since 2005, Fitch since 2010 and Moody’s since March 2017 86You can also read