New Zealand Government Debt Market Outlook - January 2019 - New Zealand Debt Management

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

New Zealand Government Debt Market Outlook January 2019

Overview

New Zealand Economic Outlook

New Zealand Government: Fiscal Outlook

Debt Management: Funding Strategy and Announcements

2

Economic Outlook

Summary of forecasts

Executive summary table

2018 2019 2020 2021 2022 2023

Year ended 30 June

Actual Forecast Forecast Forecast Forecast Forecast

Economic

Real GDP (production basis, annual average % change) 2.7 2.9 3.1 2.7 2.5 2.3

Real GDP per capita (production basis, annual average % change) 0.7 1.1 1.5 1.4 1.2 1.2

Unemployment rate (annual average, %) 4.5 4.1 4.0 4.0 4.0 4.1

CPI inflation (annual average % change) 1.5 2.0 1.8 2.0 2.0 2.0

Current account balance (% of GDP) -3.4 -3.5 -3.6 -3.6 -3.6 -3.7

Fiscal (% of GDP)

Core Crown tax revenue 27.9 28.1 28.2 28.5 28.8 28.9

Core Crown expenses 28.0 29.5 28.7 28.8 28.4 28.3

Total Crown Operating balance before gains and losses 1.9 0.6 1.3 1.5 2.2 2.3

Core Crown residual cash 0.5 -1.7 -0.8 -0.3 0.3 0.8

Net core Crown debt 20.0 20.9 20.7 20.1 19.0 17.4

Net worth attributable to the Crown 45.1 44.5 44.5 45.0 46.3 48.0

Source: The Treasury, HYEFU 2018

4

Growth remains solid

Real GDP growth

%

5.0

Forecast

2.5

0.0

-2.5

Jun-05 Jun-08 Jun-11 Jun-14 Jun-17 Jun-20 Jun-23

Quarterly

Quarterly % change (RHS) Annual average % change

Source: The Treasury, HYEFU 2018

5

Terms of trade supportive

Index (2009/10=1000)

1300

Forecast

1200

1100

1000

900

Jun-05 Jun-08 Jun-11 Jun-14 Jun-17 Jun-20 Jun-23

Quarterly

Source: The Treasury, HYEFU 2018

6

House prices and net migration

Annual average % change Number (000)

20 80

Thousands

Forecast

15 60

10 40

5 20

0 0

-5 -20

-10 -40

Jun-05 Jun-08 Jun-11 Jun-14 Jun-17 Jun-20 Jun-23

Quarterly

House prices Net migration (RHS)

Source: The Treasury, HYEFU 2018

7

Business confidence a risk

Net % Index

60 140

40 130

120

20

110

0

100

-20

90

-40

80

-60 70

-80 60

Dec-04 Dec-06 Dec-08 Dec-10 Dec-12 Dec-14 Dec-16 Dec-18

General business outlook Own activity outlook Consumer confidence

Source: The Treasury, HYEFU 2018 8

A positive output gap

% of labour force % of potential GDP

8 4

Forecast

6 2

4 0

2 -2

0 -4

Jun-05 Jun-08 Jun-11 Jun-14 Jun-17 Jun-20 Jun-23

Quarterly

Unemployment rate Output gap (RHS)

Source: The Treasury, HYEFU 2018

9

No urgency to raise OCR

Annual % Change %

6 9

8

5

Forecast 7

4 6

5

3

4

2 3

2

1

1

0 0

Jun-02 Jun-05 Jun-08 Jun-11 Jun-14 Jun-17 Jun-20 Jun-23

CPI inflation 90-day interest rate (RHS)

Source: The Treasury, HYEFU 2018

10Fiscal Outlook

Budget Responsibility Rules

Current Government is committed to prudent fiscal strategy with 5 Budget

Responsibility Rules:

• Deliver a sustainable operating surplus across an economic cycle.

• Reduce the level of net core Crown debt to 20 per cent of GDP within five years of taking office.

• Prioritise investments to address the long-term financial and sustainability challenges facing

New Zealand.

• Take a prudent approach to ensure expenditure is phased, controlled and directed to maximise its benefits. The Government

will maintain its expenditure to within the recent historical range of spending to GDP ratio.

• Ensure a progressive taxation system that is fair, balanced and promotes the long-term sustainability and productivity of the

economy.

Source: Budget Policy Statement, HYEFU 2018

12Operating surpluses sustained

$billions

15

Forecast

10

5

0

-5

-10

-15

-20

-25

2009 2011 2013 2015 2017 2019 2021 2023

Year ending 30 June

OBEGAL (after inter-segment eliminations)

Source: The Treasury, HYEFU 2018

13Capital spending impacts residual cash

$billions

15

10

5

0

-5

-10

2018 2019 2020 2021 2022 2023

Year ending 30 June

Operating Capital Residual cash

Source: The Treasury, HYEFU 2018

14Net core Crown debt contained

$billions % of GDP

80 32

Forecast

70 28

60 24

50 20

40 16

30 12

20 8

10 4

0 0

2009 2011 2013 2015 2017 2019 2021 2023

Year ending 30 June

Net core Crown debt % of nominal GDP (RHS)

Source: The Treasury, HYEFU 2018

15Funding Strategy and Announcements

Announcements at HYEFU

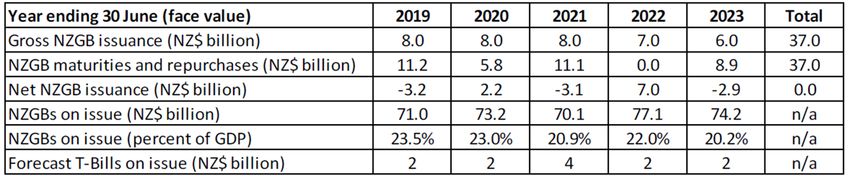

Forecasts – New Zealand Government Bonds and Treasury Bills

• Inflation-indexed bond issuance is expected to be around NZ$1 billion of the NZ$8 billion

2018/19 bond programme.

• There are plans to commence a repurchase programme of the 15 April 2020 nominal bond

before the 30 June 2019. Repurchase activities will be dependent on portfolio requirements

and market conditions.

• Forecast NZGBs on issue are consistent with the Government’s commitment to maintain

levels of NZGBs on issue at not less than 20 percent of GDP over time. This commitment

was taken into consideration when setting the forecast annual bond programme for the

2022/23 year.

Source: The Treasury

17NZGBs – not less than 20% of GDP

NZ$b

25 30%

25%

20

20%

15

15%

10

10%

5

5%

0 0%

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

Annual bond issuance NZGBs as % GDP (rhs)

Source: The Treasury

18IIBs remain important part of funding portfolio

NZ$b NZ$b

70 18

Forecast

16

60

14

50

12

40 10

30 8

6

20

4

10

2

0 0

2013 2014 2015 2016 2017 2018 2019

Nominal Bonds Inflation-Indexed Bonds (RH) T-Bills (RH)

Source: The Treasury

19A strategic approach to IIB issuance

% NZ$b

3.5 3.0

3.0 2.5

2.5

2.0

2.0

1.5

1.5

1.0

1.0

0.5 0.5

0.0 0.0

2012 2013 2014 2015 2016 2017 2018

Inflation-Indexed Bonds Issuance (RH)

Inflation Breakeven for IIB 20 Sep 2025

Source: The Treasury

20Syndication preferred for new bonds

NZ$b

5.0

4.5

4.0

3.5 IIB

Sep

3.0 2030

IIB

Sep NZGB

2035

2.5 Apr

2037

2.0

1.5 IIB

Sep NZGB NZGB NZGB NZGB

2025

1.0 Apr Apr Apr NZGB IIB Apr

2020 2027 2033 Apr Sep 2029

2025 2040

0.5

0.0

2012 2013 2014 2015 2016 2017 2018

Syndication volumes (calendar years)

Nominal Bonds Inflation-Indexed Bonds

Source: The Treasury

21Funding strategy priorities

The debt funding strategy aims to minimise the Crown’s borrowing costs over the

long-term, while keeping risk at an appropriate level.

Implemented in a transparent, even-handed and consistent manner.

Source: The Treasury

22Changing funding needs

NZ$b NZ$b

20 90

Forecast

18 80

16 70

14

60

12

50

10

40

8

30

6

4 20

2 10

0 0

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

Annual bond issuance - year ended June

Total Market Bonds on Issue (RHS)

Source: The Treasury

23Structure of NZGB portfolio

NZ$b

12.0

10.0

8.0

6.0

4.0

2.0

0.0

Mar Apr May Apr Apr Sep Apr Apr Sep Apr Sep Apr Sep

19 20 21 23 25 25 27 29 30 33 35 37 40

Source: The Treasury

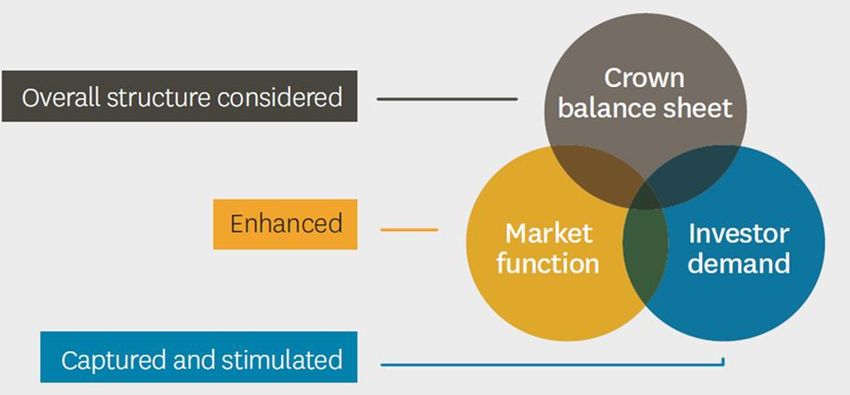

24Evolution of portfolio structure

Source: The Treasury

25Maintaining diverse investor base

NZ$b %

80 90

70 80

60 70

60

50

50

40

40

30

30

20 20

10 10

0 0

Dec 94 Dec 97 Dec 00 Dec 03 Dec 06 Dec 09 Dec 12 Dec 15 Dec 18

Resident holdings of NZGBs (NZ$b)

Non-resident holdings of NZGBs (NZ$b)

Non-resident holdings of NZGBs (%) (RH)

Source: Bloomberg, RBNZ

26Increase in proportion of resident holdings

Non-resident proportional holdings of NZGS

% %

50 75

48

46 70

44

42 65

40

38 60

36

34 55

32

30 50

Jul 2015 Jan 2016 Jul 2016 Jan 2017 Jul 2017 Jan 2018 Jul 2018

Inflation-Indexed Bonds Total (incl. T-Bills) (RH) Nominal Bonds (RH)

Source: RBNZ

27Current snapshot: Holdings of NZGBs

Holdings of New Zealand Government Bonds

NZ$b

December 2018

12.0

10.0

8.0

6.0

4.0

2.0

0.0

2019 2020 2021 2023 2025 2025 2027 2029 2030 2033 2035 2037 2040

NB NB NB NB NB IIB NB NB IIB NB IIB NB IIB

Source: RBNZ

28Disclaimer

This presentation has been prepared by the Treasury on behalf of the New Zealand Government and is for general

information purposes only. By listening to the presentation, or reading the presentation materials, you acknowledge and

agree to the contents of this disclaimer.

To the maximum extent permitted by law, neither the Treasury nor the New Zealand Government makes any representation,

recommendation or warranty, express or implied as to the accuracy, completeness or currency of any of the information in

this presentation and accept no responsibility or liability therefore. Data are indicative and approximate only, and all

information is subject to change. This presentation is intended as a snapshot view of New Zealand only, and the Treasury and

the New Zealand Government have no obligation, and do not undertake or accept any responsibility or obligation, to update,

expand or correct anything in this presentation or inform you of any matter arising or coming to their notice, after the date of

this presentation, which may affect any matter referred to in this presentation.

This presentation contains forward-looking statements including information regarding the Treasury’s future bond issuances

and the New Zealand Government’s forecast fiscal and economic performance based on current information, estimates and

forecasts. Those statements are subject to risks, uncertainties, and assumptions which are hard to predict or anticipate, and

therefore actual outcomes and performance may differ materially from the statements. Any opinions expressed in this

presentation reflect the judgement of the Treasury as the date hereof, and do not bind the Treasury nor the New Zealand

Government.

This presentation is not a product disclosure statement, disclosure document or other offer document under New Zealand law

or any other law. This presentation is not, and does not constitute financial advice. All reasonable care has been taken in

relation to the preparation and collation of this presentation. Except for statutory liability which may not be excluded, no

person, including the Treasury or any person mentioned in this presentation accepts responsibility for any loss or damage

howsoever occurring resulting from the use or reliance on this presentation by any person. Past performance is not indicative

of future performance and no guarantee or future rights are implied or given.

Nothing in this presentation is an offer to sell, or solicitation of an offer to purchase, any securities. This presentation must

not be relied upon by any person for making any investment decision and will not form part of any investment contract. The

information provided in this presentation is not investment advice and does not take into account the investment objectives,

financial situation or particular needs (including financial and taxation issues) of any particular investor. Any person

considering in investing in New Zealand Government securities must refer to any relevant offer documents and disclosures

provided expressly in connection with those securities and should take their own independent financial and legal advice on

their proposed investment. New Zealand Government securities have not been and will not be registered under the United

States Securities Act of 1933 (U.S Securities Act) or the securities laws of any state or other jurisdiction of the United States.

New Zealand Government securities may not be offered or sold, directly or indirectly, in the United States or to, or for the

account or benefit of, any person in the United States except in transactions exempt from, or not subject to, the registration

requirements of the U.S. Securities Act and any other applicable U.S. state securities laws.

This presentation may not be copied, distributed, disclosed or used without the Treasury’s express written consent.

29You can also read