QUIC RESEARCH REPORT - Queen's University Investment Counsel

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

August 22, 2016

QUIC RESEARCH REPORT

Technology, Media &

Telecom

David Del Balso

Shun Yao

Josh Morris

Adam Klingbaum

Intel Corporation (NASDAQ: INTC)

Leader in Semiconductors Offers Value in New Markets

Introduction

- The QUIC TMT portfolio currently does not have direct exposure to

the semiconductor industry, and we believe Intel would be an

excellent company to add to the portfolio.

- The semiconductor industry has recently been hit by declining

demand from PC end markets, but has a bright outlook in the

automotive, industrial, and communications markets. There will be

continued M&A activity in this industry.

- Intel is the leading designer and manufacturer of microprocessors,

and is therefore able to achieve scale and maintain bargaining

power over customers.

- Intel is uniquely positioned to capitalize on growth ahead in its Data

Center Group segment and in new markets in which it is making

investments.

- Intel trades at a discount to its peers on several valuation multiples.

Based on trading comparables and a DCF, we have established a

price target of $39.30 for INTC, which would generate an all-in

return of 14.14%. QUIC Research Reports focus on

emerging investment themes that

- This report will dive deeper into the semiconductor industry and affect current portfolio companies

Intel as a company and an investment candidate. and companies under coverage.

The information in this document is for EDUCATIONAL and NON-COMMERCIAL use only and is not intended to constitute specific legal, accounting,

financial or tax advice for any individual. In no event will QUIC, its members or directors, or Queen’s University be liable to you or anyone else for any loss

or damages whatsoever (including direct, indirect, special, incidental, consequential, exemplary or punitive damages) resulting from the use of this

document, or reliance on the information or content found within this document. The information may not be reproduced or republished in any part

without the prior written consent of QUIC and Queen’s University.

QUIC is not in the business of advising or holding themselves out as being in the business of advising. Many factors may affect the applicability of any

statement or comment that appear in our documents to an individual's particular circumstances.

© Queen’s University 2016

QUIC Research Repor t August 22, 2016 Intel Corporation Pitch Table of Contents Industry Overview and Outlook 3 Industry Overview and Outlook 6 Investment Thesis I 8 Investment Thesis II 9 Investment Thesis III 10 Catalysts and Risks 11 Discounted Cash Flow Analysis 12 Comparable Companies Analysis and Valuation Summary 13 References 14 August 22, 2016

QUIC Research Repor t

August 22, 2016

Intel Corporation Pitch

Industry Overview and Outlook

Semiconductors 2) Microprocessors: integrated circuits that carry

out all functions of central processing unit in a

A semiconductor is a solid substance that can carry computer; Intel dominates this segment,

a level of conductivity greater than that of an though AMD still remains a player

insulator but less than that of a conductor.

Semiconductors are crucial components of the 3) Commodity Integrated Circuit: standardized

electronic circuits that are used in all sorts of chips that perform basic processing; this

technology because the properties of a segment is occupied predominantly by large

semiconductor allow it to control the state of a producers in Asia

component in a circuit with minimal voltage. Since

the introduction of this technology, semiconductors 4) Complex System on a Chip: integrated circuit

have created a $54.2 billion market in the U.S. chip combining an entire system’s capability;

this segment offers the highest growth

Types of Semiconductors potential for players

Semiconductors can be grouped into four main Major Players

categories:

The two major players in the U.S. semiconductor

1) Memory chips: store temporary data and pass industry are Intel and Samsung, though many other

information; major players are Toshiba, smaller players exist, including Texas Instruments,

Samsung, and NEC. Advanced Micro Devices, Qualcomm, and NVIDIA.

EXHIBIT I EXHIBIT II

Major Player Market Shares – U.S. Industry Revenue and Growth

Intel leads the semiconductor market as a whole. The industry took a hit when PC sales began to drop.

100,000 20.0%

14.7%

80,000 10.0%

11.4% 60,000 0.0%

40,000 (10.0%)

3.5%

20,000 (20.0%)

70.4%

0 (30.0%)

2011 2012 2013 2014 2015 2016E

Intel Samsung T.I. Other Revenue YoY

Source: IBIS World Source: IBIS World

August 22, 2016 3

QUIC Research Repor t

August 22, 2016

Intel Corporation Pitch

Industry Overview and Outlook (Continued)

Industry Characteristics by end-market demand for electronics, including

laptops, tablets, and mobile phones. The decline in

After growing almost non-stop for 40 years, the the demand for personal computers has been a

semiconductor industry has seen signs of revenue significant challenge for industry players, who are

slowing over the last few years with average selling now trying to grow their other revenue sources to

prices to end markets decreasing. The industry can offset the weak personal computer environment.

also be characterized by perpetual technological

innovation, primarily driven by Moore’s law, a Foundry, Fabless, and IDM

phenomenon that states the number of transistors

on a single chip will double every two years. The Companies competing in the semiconductor

optimization and scaling of production processes industry typically take on one of two operating

has allowed this phenomenon to sustain itself. models – foundry or fabless. Foundry companies

Lastly, the industry can also be characterized by the operate solely in the manufacturing of chips. The

intensive capital requirements to maintain growth largest foundry in the U.S. is IBM. Fabless chip

and continue augmenting technological processes. makers take on the design and marketing of chips,

Many semiconductor companies, including Intel, are but outsource the manufacturing of them. Fabless

global leaders in research and development, but semiconductor companies include Advanced Micro

R&D in this industry can often be risky due to the Devices, NVIDIA, and Qualcomm. Intel is known as

amount of time that may exist in between the an Integrated Device Manufacturer (IDM), as it

designing, manufacturing, and actually bring a chip designs, manufactures, and sells its integrated

to the market. Sales in the industry are highly driven circuit products.

EXHIBIT III

Average Selling Price for Semiconductor Devices

Average selling prices are beginning to stabilize, but will likely face a perpetual decrease.

Source: PriceWaterhouseCoopers

August 22, 2016 4

QUIC Research Repor t

August 22, 2016

Intel Corporation Pitch

Industry Overview and Outlook (Continued)

M&A in the Semiconductor Industry players who can achieve scale and pricing power

over suppliers and end market customers.

As revenues in the industry have slightly slowed, Depending on the demand coming from the PC

companies have looked to M&A activity to expand market, winners in the industry will also be able to

into emerging markets with growth opportunities. generate revenue from other end markets.

Given the competition in the industry, companies

have also been using M&A activity to gain market The most promising growth opportunities in the

share and achieve scale, which can gives certain industry lie within the automotive, industrial, and

companies advantages in their design and communications end markets, while the consumer

production life cycles. and computer segments show signs of mature

markets. Companies will continue to engage in

Outlook M&A activity to find growth and profitability in the

promising end market segments.

While average selling prices in the industry are

expected to continue getting squeezed by end Across the three promising market segments –

segments and applications, revenue growth in the automotive, industrial, and communications – there

industry will likely only remain in the low-to-mid also exists an opportunity for semiconductor

single digits, and profitability will be tough to companies to produce chips enabling the Internet

maintain with increasing fab costs, process of Things, which could likely be a big turning point

development costs, and chip design costs. Going for the semiconductor industry.

forward, the industry will be dominated by large

EXHIBIT IV EXHIBIT V

Annual Semiconductor Deal Volume ($MM) Five-Year Growth Rates by Sub-Segment

M&A remains a major component of the industry. Automotive, Industrial, and Communications lead.

11.2%

25,059

7.3% 7.2%

17,380

10,730 0.8% 0.4%

8,102

2011 2012 2013 2014

Source: PriceWaterhouseCoopers Source: PriceWaterhouseCoopers

August 22, 2016 5

QUIC Research Repor t

August 22, 2016

Intel Corporation Pitch

Company Overview

Business Overview and desktop computers, servers, tablets, mobile

phones, and Internet-of-Things-enabled devices.

A designer and manufacturer of advanced Intel’s offerings also span to software and services.

integrated digital technology platforms, Intel is a

leader in the semiconductor industry. Each Intel Moore’s Law

platform consists of a microprocessor and a chipset,

as well as any additional hardware, software, and This company’s strategy revolves around its effort

services that serve to enhance the platform. Intel’s to continue pursuing Moore’s Law. Gordon Moore,

platforms are based upon a lineup of nine the co-founder of Intel, observed in 1965 that the

microprocessors: (1) Intel Quark Processor, (2) Intel number of transistors per square inch on integrated

Atom Processor, (3) Intel Pentium Processor, (4) circuit doubles every two years. Intel continues to

Intel Celeron Processor, (5) Intel Core m Processor, persistently pursue this phenomenon in order to

(6) Intel Core i Processor, (7) Intel Xeon Processor, maintain its leading position in the semiconductor

(8) Intel Xeon Phi Processor, and (9) Intel Itanium manufacturing industry.

Processor.

Top Share Ownership

Intel sells its platforms to original equipment 1. The Vanguard Group, Inc.: 6.33%

manufacturers, original design manufacturers, and 2. BlackRock Institutional Trust Company: 4.16%

industrial equipment manufacturers in computing 3. State Street Global Advisors: 4.00%

and communications markets. Intel’s platforms are 4. Capital World Investors: 3.53%

incorporated in the world’s leading commercial and 5. Capital Research Global Investors: 3.53%

personal technological devices, including notebook

EXHIBIT VI

Intel Stock Price Relative Performance – Last Twelve Months

Intel has outperformed the S&P 100 the last twelve months.

130

120 121.3

110

103.9

100

90

80

1-Aug-15 16-Oct-15 31-Dec-15 16-Mar-16 31-May-16 15-Aug-16

NASDAQGS:INTC S&P 100 Index

Source: Capital IQ

August 22, 2016 6

QUIC Research Repor t

August 22, 2016

Intel Corporation Pitch

Company Overview (Continued)

Operating Segments

Intel’s business activities are grouped into six 4) Non-Volatile Memory Solutions Group

segments: (NSG): All NAND flash memory platforms used

in solid-state drives.

1) Client Computing Group (CCG): All Intel

platforms designed for notebook and desktop 5) Intel Security Group (ISecG): Security software

computer, 2-in-1 devices, tablets, and mobile for computers, mobile devices, and networks.

devices. It also includes wireless and wired

connectivity products and mobile com- 6) Programmable Solutions Group (PSG):

munication components. Programmable semiconductors and related

items designed for a variety of market; formed

2) Data Center Group (DCG): All platforms that in 1Q16 as result of Altera acquisition.

offer leading performance for enterprise, cloud,

communications infrastructure, and technical Acquisition of Altera

computing markets.

In 1Q16, Intel acquired Altera Corporation, a global

3) Internet of Things Group (IOTG): All designer and seller of programmable

platforms engineered for applications in retail, semiconductors and related technology, for total

transportation, industrial, and home and consideration of $14.5 billion. This acquisition will

buildings markets, among others. expand Intel’s reach to new classes of platforms.

EXHIBIT VII EXHIBIT VIII

FY 2015 Revenue Breakdown by Segment Key Intel Professionals

DCG now makes up a larger portion than it ever has. Andy D. Bryant (Executive Chairman):

• Previously EVP of Tech, Manufacturing, and Enterprise

4% 5% • Also worked at Ford and Chrysler

4% • MBA in finance from University of Kansas

Brian M. Krzanich (Chief Executive Officer):

• Previously served as Chief Operating Officer

• Has served various other roles at Intel since 1994

• Bachelor’s in chemistry from San Jose State University

29% Stacy J. Smith (Chief Financial Officer):

58%

• Joined Intel in 1998 and has held positions in finance,

sales & marketing, and information technology

• MBA in finance from University of Texas

Paula Tolliver (Chief Information Officer):

• Joined Intel in August 2016

CCG DCG IOTG SSG Other • Previously CIO at The Dow Chemical Company

• Bachelor`s in Computer Science from Ohio University

Source: Company Report Source: Capital IQ

August 22, 2016 7QUIC Research Repor t

August 22, 2016

Intel Corporation Pitch

Investment Thesis I: Market Leader with Scale Advantage

Intel has defended its leading position in the manufacture chips and platforms at lower costs

semiconductor industry for several decades. As the than competitors. In the declining ASP environment

word’s largest semiconductor IDM, they are the of the semiconductor industry, Intel is able to use

preferred choice of microprocessor for the world’s this advantage to increase its operating margins, as

leading designers and manufacturers of computers, it has done in the past. Their leadership also gives

mobile devices, servers, and now autonomous them bargaining power over buyers, making them

vehicles and Internet-of-Things-enabled devices. less sensitive to the declining average selling prices

in the industry.

Intel’s leading position has been established

through their heavy investments in research and As well, being a leader in the industry, with an

development and their relentless effort to continue industry-leading R&D budget, also means that Intel

to keep up with Moore’s Law. As the exponential can position itself in new markets with high growth

growth suggested by Moore’s Law becomes harder potential than other smaller players in the industry.

to achieve as time goes on, Intel is becoming

recognized more as the one company that can keep As a leader in semiconductors, Intel retains the

pace with this phenomenon. business of the “Super 7”: Google, Amazon,

Facebook, Microsoft, Baidu, Alibaba, and Tencent,

Intel’s leadership in the market gives them points of all for whom Intel makes custom chips with special

attraction for a QUIC investment that other players features. Intel has a dominant position in the

in the industry do not have. Firstly, it gives them a industry, and the above mentioned competitive

scale advantage, which means they can advantages make this position sustainable.

EXHIBIT IX

Some of Intel’s Customers for Whom it Makes Custom Chips

Source: Company websites

August 22, 2016 8QUIC Research Repor t

August 22, 2016

Intel Corporation Pitch

Investment Thesis II: Value in Data Center Segment

Intel’s Data Center Group (DCG) designs and Intel’s management has made clear their dedication

manufactures platforms for enterprise, cloud, to driving growth in DCG on account of: (1) growing

communication infrastructure, and technical Cloud demand, (2) their ability to penetrate the

computing markets. This segment has become a networking market, and (3) their position to

greater portion of Intel’s revenue as the company capitalize on the artificial intelligence market.

has strived in recent years to focus less of their

business on the personal computers market. This With regard to the Cloud, as a market leader with a

segment has realized impressive growth, and grown 99% share in the enterprise server market, Intel is

at 12% compounded annually. well positioned to drive growth from increasing

Cloud demand with the ability to produce units at

The year-over-year growth of the DCG segment in an unparalleled scale. Speaking to networking, his

Intel’s 2Q16 fell short of the company’s target. market is estimated as an $18 billion total

Senses of investor uncertainty and pessimism about addressable market with customers transitioning to

this segment were likely priced into the stock, standardized silicon chips, photonics, and fabrics.

implying the full potential of this segment is valued Intel can capture this market with its new

at a discount. However, management’s generation of Xeon chips and Omni-Path Fabric.

commitment to continue driving growth in this With regard to artificial intelligence, Intel has been

segment could lead to low double-digit year-over- gaining momentum in this emerging market with

year growth for the next few years. The higher efforts in deep learning. Intel is capturing market

margins in the DCG segment will also contribute share with its Xeon Phi chips and its strengthened

directly to Intel’s bottom line. partnership with Baidu’s deep speech initiatives.

EXHIBIT X EXHIBIT XI

Intel DCG Annual Revenue ($MM) Intel’s “Virtuous Cycle of Growth”

Intel has grown their DCG segment 12% annually. These market segments feed each other’s growth.

15,977

14,387

12,163

10,741

10,129

2011 2012 2013 2014 2015

Source: Company Report Source: Company repot

August 22, 2016 9QUIC Research Repor t

August 22, 2016

Intel Corporation Pitch

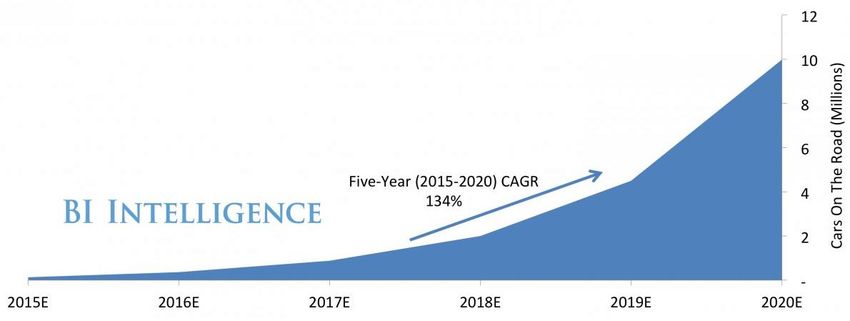

Investment Thesis III: Well Positioned for New Markets

Intel’s leaders have strongly emphasized their goal dominant manufacturer of semiconductors for this

to move beyond personal computers and gain market segment due to its end-to-end approach

share of new markets. The efforts concentrated in that can address the vehicle, network, and cloud

their Data Center Group have been a large components of autonomous driving. Intel’s Xeon

component of this, but the company has extended and Xeon Phi are able to handle the inference and

their efforts to investing in other new markets, training aspects, while their offerings in 5G and

namely autonomous driving and the Internet of optical connectivity can address the networking

Things. The semiconductor industry has been component. Then, Intel’s software is able to mesh

challenged by the declining revenues from the all these systems together. Intel’s unique end-to-

personal computer market, and Intel’s investment in end offerings for autonomous driving give the

these other areas, and their ability to gain more company an excellent position to capitalize on this

share than competitors, will be a contributing factor emerging market.

to Intel offsetting declining PC revenue better than

its competitors, implying reason for Intel to be At the beginning of July 2016, Intel entered a

valued higher than its peers. partnership with BMW Group and Mobileye to

develop solutions for fully automated driving. BMW

Autonomous Driving selecting to partner with Intel is a clear testament to

Intel’s leadership in the semiconductor industry,

The emerging market in autonomous driving yields and the opportunities that lie ahead for Intel in

opportunity for growth in the semiconductor autonomous driving leave much room for valuation

industry. Intel is uniquely positioned to become the expansion and make Intel an attractive investment.

EXHIBIT XII

Estimated Global Installed Base of Cars with Self-Driving Features

Source: Business Insider Intelligence Estimates 2015

August 22, 2016 10QUIC Research Repor t

August 22, 2016

Intel Corporation Pitch

Catalysts and Risks

Catalysts

1) Order from Apple: In June of 2016, a rumour Risks

entered the market that Intel will be supplying

modem chips for the versions of Apple’s next 1) Greater than expected decline in PC: As

iPhone on AT&T’s U.S. network and some other previously mentioned, declining PC demand

networks overseas. Representatives of both has been challenging companies in the

companies decline to comment on the matter, semiconductor industry, including Intel.

but if Apple were to give Intel this order, it Revenue estimates for Intel take into account

would be the first major score for an Intel the weak PC market environment, which is

mobile chip and would take share away from expected to be offset by Intel’s other revenue

Intel’s biggest competitor in the mobile space, sources, including the high-growth Data Center

Qualcomm. Cowen and Company estimates this Group segment and new revenue sources in the

order could generate $1.5 billion of revenue for programmable semiconductors space.

Intel, leading to $850 million of operating However, given that a large portion of Intel’s

profit. This deal could also open up a whole sales is still linked to sales in the PC end market,

new relationship between Apple and Intel and the downside risk remains that PC sales could

possibly open up more opportunity for Intel to decline at a greater than expected rate, which

make share gains in the tablet and smartphone potentially would not be offset by other

end markets. sources of revenue.

2) Acquisition of Altera: At the end of 2015, Intel 2) Deceleration of Data Center segment: As

acquired Altera Corporation, a leading provider Intel concentrates efforts toward moving away

of field-programmable gate array technology. from the PC end market, they are investing

This acquisition was made in an effort for Intel heavily in growing their Data Center Group. If

to compete in the programmable for reasons related to the enterprise cloud and

semiconductors market segment. This deal networking end markets, Intel is not able to

added an entirely new operating segment to generate the growth it is expecting from this

Intel’s business and will drive a whole new segment, it would be tough for Intel to offset

source of revenue for the company. FY 2016 will revenues that it is losing in the tough PC

be the first complete year of Intel reporting environment.

Altera’s operating results, and if these results

might be impressive enough to serve as a 3) Competition: Though Intel has remained a

catalyst for Intel’s stock price. market leader in microprocessors for several

decades, there does exist the risk of Intel losing

3) Launch of 10nm: Intel is expected to launch a market share to competitors like AMD. If Intel is

new set of 10nm chips in 2017. The success of unable to maintain its lead, its existing OEM

this release would show the global and ODM customers may switch suppliers,

semiconductor industry that Intel is capable of causing Intel to lose market share to

keeping on pace with Moore’s Law, claiming competition.

them as the leader of this market. The 10nm

chip could also allow Intel to get more mobile

and tablet wins.

August 22, 2016 11QUIC Research Repor t

August 22, 2016

Intel Corporation Pitch

Discounted Cash Flow Valuation

Discounted Cash Flow Model Historical Fiscal Years Projected Fiscal Years

FY 2013 FY 2014 FY 2015 FY 2016 PF FY 2017E FY 2018E FY 2019E FY 2020E

Total Revenue 52,708 55,870 55,355 57,846 60,738 64,383 66,314 68,303

YoY Change (1.2%) 6.0% (0.9%) 4.5% 5.0% 6.0% 3.0% 3.0%

Cost of Sales (21,187) (20,261) (20,676) (21,317) (22,079) (23,082) (23,443) (23,805)

% of Revenue 40.2% 36.3% 37.4% 36.9% 36.4% 35.9% 35.4% 34.9%

Gross Profit 31,521 35,609 34,679 36,529 38,659 41,300 42,871 44,499

% Margin 59.8% 63.7% 62.6% 63.1% 63.6% 64.1% 64.6% 65.1%

Operating Expenses (19,230) (20,262) (20,677) (21,382) (22,299) (23,476) (24,015) (24,565)

% of Revenue 36.5% 36.3% 37.4% 37.0% 36.7% 36.5% 36.2% 36.0%

Earnings Before Interest and Taxes 12,291 15,347 14,002 15,147 16,360 17,824 18,856 19,934

% Margin 23.3% 27.5% 25.3% 26.2% 26.9% 27.7% 28.4% 29.2%

Income Tax Expense (2,991) (4,097) (2,792) (3,181) (3,435) (3,743) (3,960) (4,186)

Net Operating Profit After Tax 9,300 11,250 11,210 11,966 12,924 14,081 14,896 15,748

YoY Change (13.6%) 21.0% (0.4%) 6.7% 8.0% 9.0% 5.8% 5.7%

Plus: Depreciation and Amortization 8,032 8,549 8,711 8,173 8,278 8,453 8,375 8,167

% of Revenue 15.2% 15.3% 15.7% 14.1% 13.6% 13.1% 12.6% 12.0%

Plus: Share-Based Compensation 1,118 1,148 1,305 1,330 1,387 1,460 1,494 1,528

% of Revenue 2.1% 2.1% 2.4% 2.3% 2.3% 2.3% 2.3% 2.2%

Less: Capital Expenditures (10,711) (10,105) (7,326) (10,045) (10,547) (11,180) (11,515) (11,860)

% of Revenue 20.3% 18.1% 13.2% 17.4% 17.4% 17.4% 17.4% 17.4%

Change in Net Working Capital 3,140 (99) (1,081) 991 212 272 406 470

Unlevered Free Cash Flow 10,879 10,743 12,819 12,415 12,255 13,086 13,656 14,052

YoY Change 33.5% (1.3%) 19.3% (3.2%) (1.3%) 6.8% 4.4% 2.9%

Discount Period 0.5 1.5 2.5 3.5 4.5

Discount Factor 96.4% 89.5% 83.1% 77.1% 71.6%

Present Value of Unlevered Free Cash Flow 11,962 10,963 10,869 10,531 10,061

WACC Calculation Share Price Calculation Terminal Growth Rate

Risk-Free Rate 1.54% PV of UFCF 53,700 $40.65 1.50% 1.75% 2.00% 2.25% 2.50%

Market Risk Premium 7.50% Terminal Growth Rate 2.00% 7.31% 39.85 41.93 44.24 46.79 49.62

WACC

Beta 1.05 Discount Rate 7.71% 7.51% 38.31 40.24 42.38 44.73 47.33

Cost of Equity 9.42% PV of Terminal Value 148,873 7.71% 36.87 38.67 40.65 42.83 45.23

Enterprise Value 202,572 7.91% 35.53 37.21 39.05 41.07 43.29

Pre-Tax Cost of Debt 3.25% 8.11% 34.28 35.85 37.56 39.43 41.49

Effective Tax Rate 21.00% Enterprise Value 202,572

Cost of Debt 2.57% Less: Total Debt 22,748

Plus: Cash & Equivalents 15,308

Capital Structure: Equity Value 195,132

% Equity 75.00%

% Debt 25.00% Shares Outstanding 4,800

WACC 7.71% Implied Share Price $40.65

August 22, 2016 12QUIC Research Repor t

August 22, 2016

Intel Corporation Pitch

Comparable Company Trading Multiples

Company Name Market Enterprise EV / EBITDA Dividend Price / Earnings EV / Sales

Capitalization Value LTM 2016E 2017E Yield 2016E 2017E 2016E 2017E

Intel Corporation $167,288 $178,324 7.9x 8.3x 7.5x 3.0% 14.1x 13.1x 3.1x 3.0x

QUALCOMM Incorporated $92,589 $87,243 11.4x 10.1x 9.4x 3.4% 14.6x 13.2x 3.8x 3.7x

Texas Instruments Inc. $70,225 $71,298 13.3x 13.0x 12.2x 2.2% 21.8x 20.3x 5.5x 5.3x

NVIDIA Corporation $33,386 $29,943 21.9x nmf 17.5x 0.7% nmf 26.7x nmf 4.9x

Advanced Micro Devices, Inc. $6,030 $7,311 nmf 121.1x 65.8x - nmf nmf 1.8x 1.7x

Minimum $6,030 $7,311 7.9x 8.3x 7.5x 0.7% 14.1x 13.1x 1.8x 1.7x

25th Percentile $33,386 $29,943 10.5x 9.7x 9.4x 1.8% 14.4x 13.2x 2.8x 3.0x

Median $70,225 $71,298 12.4x 11.5x 12.2x 2.6% 14.6x 16.8x 3.4x 3.7x

75th Percentile $92,589 $87,243 15.5x 40.0x 17.5x 3.1% 18.2x 21.9x 4.2x 4.9x

Maximum $167,288 $178,324 21.9x 121.1x 65.8x 3.4% 21.8x 26.7x 5.5x 5.3x

Valuation Summary

Target Share Price Calculation

Our target price for Intel is an average of: (1) the implied

DCF Share Price $ 40.65 50%

share price from our discounted cash flow analysis and (2)

Median P/E 2016E $ 36.34 25%

trading multiples that we thing are fair to assign to Intel’s

operating metrics based on its comparable peers. On all

Median EV/Sales 2016E $ 39.55 25%

trading multiples, Intel is trading at a discount to the median

Target Share Price $ 39.30

of its select peers. Given Intel’s potential to grow revenue at a

higher rate than its peers in the new markets it is entering,

and its ability to scale operations and increase operating

Return Calculation

margins in an environment of decreasing average selling

prices, we believe Intel should trade in line with 75th

Share Price (2016-08-22 Close) $ 35.36

percentile forward multiples. Given the slight uncertainty of

12-month Target Price $39.30

the revenue growth Intel’s DCG will generate and the

Dividend Yield 3.00%

uncertainty in the PC market segment, we instead assigned it

All-in Return 14.14%

multiples in line with peer medians.

We arrived at a target share price of $39.30. With Intel’s 3.00% dividend, an investment in

Intel would yield an all-in return of 14.14%.

August 22, 2016 13QUIC Research Repor t August 22, 2016 Intel Corporation Pitch References 1. Bloomberg 2. Business Insider 3. Capital IQ 4. Company Websites, Reports, and Press Releases 5. Deutsche Bank Securities 6. IBIS World 7. Jefferies 8. Morgan Stanley 9. PriceWaterhouseCoopers August 22, 2016 14

You can also read