SEA-Salga-SACN City Power Presentation - Presented by: Paul Vermeulen Manager DSM and SSM City Power - Sustainable ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SEA-Salga-SACN

City Power Presentation

Presented by: Paul Vermeulen

Manager DSM and SSM

City Power

Contents 1 Drivers of change 2 Key trends 3 What is in the headlines? 4 What are the key challenges 5 What are the key opportunities 6 What is COJ doing?

Drivers of change 01

Transformational change in P&U is being driven

by numerous factors

Significant investment is required to

update or replace power, gas and

water assets.

Infrastructure

Aging workforce and challenges of Generation mix is shifting to cleaner

investment

the new digital economy require sources, including natural gas and

Changing

effective knowledge transfer and Talent and renewables, and is becoming more

energy mix

fresh thinking. diversity decentralized.

and DG

Customers are being offered choices

New and powerful entrants have

begun to offer customers innovative

New Sector in Empowered to manage their energy use, through

competitors transformation customers both distributed generation (DG) and

home energy management products

energy management solutions.

and services.

Regulatory

frameworks Digitization

Regulatory compact is under Smart meters, “big data” and

pressure to accommodate changing Market and analytics can be used to optimize

customer demands and encourage policy energy delivery, improve energy

innovation. reforms efficiency and enhance customer

experiences.

Federal and state mandates are

driving restructuring, creating

incentives and imposing new rules.

4

Key trends 02

Global demand for electricity is expected to

increase at 2.1% CAGR through 2040 with

most growth coming from emerging markets

Growth in electricity demand by region, 201240 (CAGR) Electricity generation in OECD and non-OECD countries

4.0% 30.0

3.3% 25.0

2.7% 20.0

2.5%

Global average: 2.1%

15.0

1.4%

10.0

0.8%

5.0

0.0

OECD E.Europe Latin Middle East Africa Asia (inc 1990 2012 2020 2025 2030 2035 2040

Eurasia America China,

India) OECD Non-OECD

Source: World Energy Outlook (WEO) 2014 Source: WEO 2014

CAGR: Compound Annual Growth Rate – The year-over-year growth rate of an investment over a specified period of time

OECD: Organisation for Economic Co-operation and Development, an international economic organisation of 34 countries, founded to stimulate economic progress and world trade

► World electricity demand is expected to increase by more than three-fourths over the period 201240, growing at an average rate of

2.1% per year.

► The most dramatic growth in demand will come from Africa (4% CAGR).

► Asia, led by China and India, is also expected to experience dramatic growth in electricity demand of 3.3% CAGR through 2040.

6

Meeting this demand will require enormous

infrastructure investment of more than

US$23t in power and gas alone

Investment in supply infrastructure, 201440 (2013 US$b) Drivers of capex

Total Total Total Total ► Aging power stations

Replacement

power power gas

cycle ► High expenditure on asset replacement

plant T&D T&D*

Europe 2,109 970 303 3,382

E.Europe/Eurasia 835 526 417 1,778 Environmental ► Government-imposed environmental

targets targets imply massive spend

Middle East 479 273 241 993

India 1227 788 70 2,085

Africa 776 848 241 1,865 ► Power demand to grow especially in

Demand growth

emerging markets

Asia-Pacific 4,180 3,536 588 8,304

OECD Americas 1,952 1,215 586 3,753

Non-OECD Americas 593 530 93 1,216

More than US$23.3t globally in power and gas

World 12,151 8,686 2,539 23,375

* Gas T&D values are for the period 2014-35 in 2012 US$b

Sources: IEA, WEO 2014; World Energy Investment Outlook 2014

In addition, the OECD estimates that more than US$1t per annum needs to be invested globally just to replace and maintain water infrastructure.

7

Coal-fired generation is expected to continue to

account for a significant share of global

electricity supply

Global coal-fired electricity generation is expected to grow from 9.2TWh in 2012 to 12.2TWh in 2040,

representing a CAGR of 1.02%.

Coal-fired electricity generation Global electricity generation by source

22,721TWh 40,104TWh

16

14 21%

33%

12 11%

Trillion kWh

10 12%

22%

8

24%

6

4 41%

2 31%

0 5% 1%

2010 2015 2020 2025 2030 2035 2040 2012 2040

United States Rest of World Oil Coal Natural gas Nuclear Renewables

Source: US Energy Information Administration International Energy Outlook 2013 Source: IEA WEO 2014

Reference

► Coal will still be a dominant fuel source for power generation in 2040, accounting for more than 31% of global generation, but there will be a

massive decline from its 40%-plus share today.

► Natural gas-fired generation is expected to maintain its 22%-24% share of global generation, which will still imply a huge expansion in natural

gas absolute volumes.

► The real global growth story of course is renewables, which are expected to overtake coal as the primary source of power generation by 2040.

8

Fossil fuels will hold a dominant position in

global electricity generation for several

decades, with renewables gaining ground …

New capacity additions by region, 201440

25%

43% 40%

49%

63% 13% 60%

69%

1% 5%

6%

34% 43%

14% 4%

2%

46%

5%

28% 32%

30% 19%

17% 19%

3% 9% 3% 6%

3% 5% 1% 1% 2% 0%

Latin America Africa Middle-East Asia, Asia-Pacific E.Europe/Eurasia OECD Americas OECD Europe

* Renewables include hydro-power plants.

Oil Coal Gas Nuclear Renewables*

Source: IEA WEO 2014

► Renewables will represent the lion’s share of new capacity installed over the next couple of decades in every region.

9

… and growth in renewable energy investment

shifting to emerging markets

Non-hydro renewables share of power generation Investment in renewables by region, 2013

by region

8.2% Middle East & Africa

Oceania

US$9b US$9b

5.7% Central & 4%4%

South America 5% Europe

4.9% 24%

US$12b US$57b

3.1%

2.8% 22%

2.0% 1.9% North America &

1.3% Caribbean

0.2% 0.4% US$52b

Asia

41%

Middle East Asia-Pacific North Central & Europe US$98b

& Africa America & South

Caribbean America Total = US$237b

2002 2012 Solar PV has attracted the highest annual investment for the past three

years (US$112b in 2013).

Source: BP Statistical Review of World Energy, 2013 Source: EY analysis of BNEF data

► For most regions, the share of non-hydro renewables in the ► Investment in renewable energy sources across Europe and

generation mix at least doubled between 2002 and 2012. North America peaked in 2011 at $108b and $62b, respectively.

► In Europe, driven by subsidies and government incentives, the ► Investment is shifting to emerging markets, led by China as they

share of non-hydro renewables in total generation quadrupled from pursue clean power sources and reduce dependence on fossil fuel

2% in 2002 to just over 8% in 2012. generation.

10State mandates and the need for energy

efficiency are driving the deployment of

smart meters across the globe …

Expected smart meter penetration (by region, 201222)

“Smart technology has already cut load

growth for utilities by half through energy

conservation. Adding distributed

generation and storage systems would

accelerate that trend.”

– GTM Research

Source: Navigant Research report, 2013

smart meters are expected to be installed CAGR is expected in the smart meter

by 2022, (currently 313m), bringing the revenue in Europe through 2020, making it

1.1b global market for smart meters to US$22b

9.4% the fastest growing region.

by 2020.

penetration to be achieved in US with the of overall shipments of smart meters in

deployment of 65m by 2015. Almost 2012 were attributable to Asia-Pacific and it

45%-50% US$3b has been invested in smart meters

49.2% is expected to remain the largest regional

in the US. market in terms of volume.

11Although recent electrical energy

sales were flat growth is expected

* Excludes Sandton, Soweto; Natural Gas represents piped gas from eGoli gas 14What is in the headlines 03

The latest headlines

Nuclear Energy: a 'secure' option for South Africa BRICS bank a global game changer , says Eskom’s

Load shedding drags down sub-Saharan growth

Although South Africa could procure more energy Molefe: The launch of the Brics New Development

report Gross domestic product (GDP) growth rate in from other African countries to help plug its energy Bank would change global development finance,

sub-Saharan Africa will average 4.2% in 2015, gap, nuclear energy would be a more secure option said Eskom‟s Brian Molefe on Thursday. “They will

according to the latest World Bank report. In its in the long run, says former South African Nuclear talk about global development finance before and

Global Economic Prospects report for June 2015, the Energy Corporation CEO Dr Rob Adam. He told after Ufa,” said Molefe, acting CEO of South Africa‟s

World Bank made a 0.4% downward revision of the attendees at a South African National Energy... Full power utility and head of the nation‟s section of the...

Article Full Article

region's GDP growth rate. The report attributed this

to... Full Article

Solidarity launches plan to help households in Angola says to spend $432m on electricity

unlikely event of electricity blackout: Trade meters: Angola's government plans to spend

union Solidarity, in conjunction with KragDag $432-million to roll out over a million electricity

The National Energy Regulator of South Africa meters by 2017, the State news agency said, in

(Nersa) on Monday rejected Eskom’s application for and Maroela Media, has launched an

a move that could help boost revenues for

a further 2015/16 tariff hike in addition the 12.69% emergency plan to assist households in the power producers. Energy Minister Joao

already granted for the year. Nersa chairperson event of a total power blackout, owing to the Baptista Borges said the meters would be

Jacob Modise announced that, owing to a number of ongoing problems at State-owned electricity linked to a prepaid system, which is... Full

deficiencies in the application, the regulator... Full

provider Eskom. The plan offered practical tips Article

on how households could... Full Article

Article

16What are the key challenges 04

Power and Utilities: Key challenges and risks

Key challenges: The top 10 Global risks:

► Load shedding ► Compliance and regulation

► Theft (copper) and vandalism ► Commodity price volatility and access

► Economic downturn and increasing electricity to competitively priced long-term fuel

costs supplies

► Municipal finances ► Political intervention in power and

► Skills and capacity shortages utilities (P&U) markets

► Service delivery protests ► Uncertainty in climate policy and

► Illegal connections carbon pricing

► State of infrastructure and development ► Significant shifts in the cost and

affordability accessibility of capital

► Industry direction – embedded generation, ► Capital project execution

alternative energy, technology (DG), etc. ► Economic shocks and resulting short-

term energy demand shocks

► War for talent

► Aging generation and network

infrastructure

► Managing planning and public

acceptance

18What are the key opportunities 05

Utilities need to innovate across the value chain

to derive competitive advantage and turn

disruptive threats into opportunities

The top 10 opportunities:

1. Rising emerging markets’ energy demands

(including poverty reduction and access to

power)

2. Acquisitions or alliances to gain new

capabilities (including growing skills base)

3. Growth in energy and ancillary services

markets (including sustainable jobs)

4. Enhancing relationships with external

regulatory and compliance bodies

5. Improving public perceptions (including

customer control)

6. Increased focus on investor relations

programs and communications (including

security of supply to drive investor appetite)

7. Integration of distributed energy resources

(including necessity to innovate)

8. Increased investment in generation capacity

and delivery infrastructure in emerging

markets (including security of supply and

network investment)

9. Rising energy innovation in emerging markets

10.Improving onshore and offshore wind supply

chain efficiency

20In summary

► Global demand for electricity is expected to increase more than two-thirds between now and 2040.

► Meeting electricity demand will require about US$21t of investment in power infrastructure over this period.

► This amount more than doubles when gas pipeline and water infrastructure investment is included.

► Fossil fuel generation is expected to remain a significant part of the global generation mix in coming decades.

► Coal-fired generation is expected to continue to account for a significant share of global electricity supply

► The shift to renewable energy is a global growth trend with investment shifting to emerging markets.

► Utilities can turn disruptive threats into opportunities by:

► Investing in smart metering and grid modernisation for a more intelligent, responsive and reliable network.

► Expanding beyond the meter service offerings such as demand response and home energy management.

► Investing in distributed generation, energy storage and microgrids.

► Optimising the capture, storage and analysis of big data from smart meters and intelligent devices.

► African power and utilities is always a hot topic in the media

► Utilities need to innovate across the value chain to turn disruptive threats into opportunities

Challenges: Opportunities:

► Load shedding ► Rising emerging markets’ energy demands.

► Theft and vandalism ► Growth in energy and ancillary services markets.

► Municipal finances ► Enhancing relationships with external regulatory and

compliance bodies and the customer

► Aged infrastructure

► Increased focus on investor relations programs

► Skills and capacity shortages

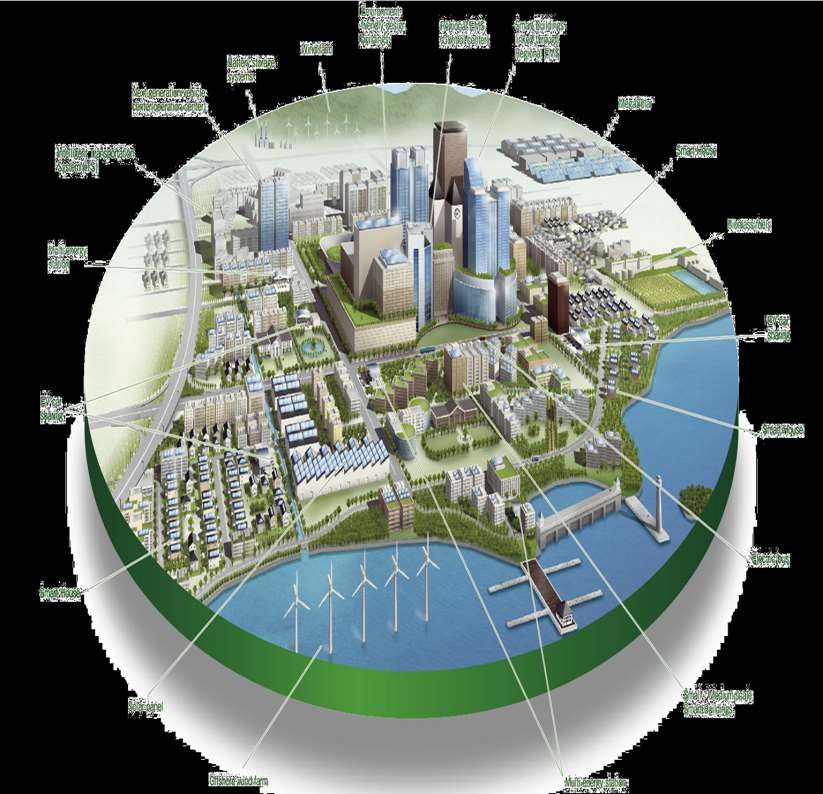

► Rising energy innovation in emerging markets06 City of Johannesburg 22 22

A City of the future…

Interconnected

Integrated

Participatory

Efficient

Sharing

Distributed GX

Energy Diverse

Smart1. Improved quality of life and development-driven resilience for all

2. Provide a resilient, liveable, sustainable urban environment – underpinned by

infrastructure supportive of a low-carbon economy

3. An inclusive, job-intensive, resilient and competitive economy that harnesses

the potential of citizens

4. A high performing metropolitan government that pro-actively contributes to and

builds a sustainable, socially inclusive, locally integrated and globally

competitive Gauteng City Region

- Growth and Development Strategy (GDS) 2040

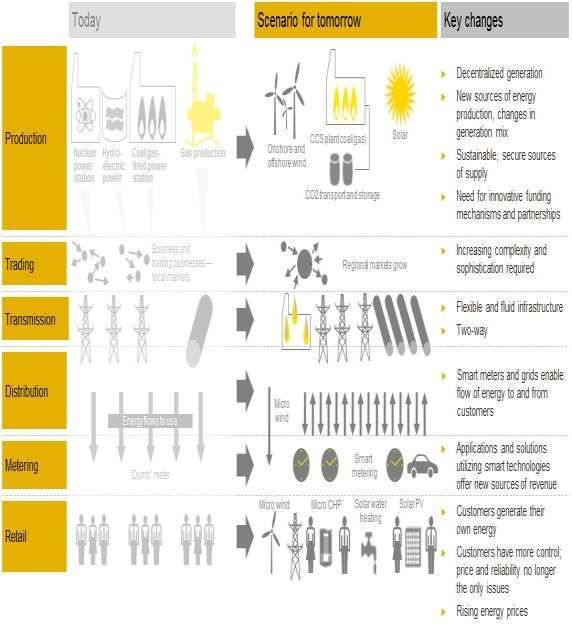

24A future view of energy availability

Electricity Natural Gas Automotive Fuels How do we manage this

Automotive Fuels

• In the short to medium term (without a bankable anchor project) the increase of piped natural gas

resources to the City is unlikely (for power generation purposes) and this won’t add significantly

to the diversification of energy supply and security;

• The current electricity business model has a key asset in terms of the network (wires) but limited

short term options for diversification exists (Eskom, Kelvin);

• The future electricity business model will be based on the utilisation of the network (wires) as

an asset and:

– diversify the input sources of energy (Distributed generation, PV, Batteries Storage) to

become more resilient, cleaner and less dependant on the national grid;

– be able to use the grid in the trading of electricity. This will be dependent on the smart grid

and sufficient telecommunications infrastructure (TELCO) and

– provide value added services to customers to negate anticipated revenue losses

• New electrical technologies innovation makes it a critical point for GHG emissions projects 25Supply and demand options

available to the City

A combination of these sources leads to

Technology options increases diversity in the supply mix and

(with high level consideration of technical, decrease net emissions.

economic and market potential)

National grid Kelvin upgrade Ops. efficiency Demand

+ Ownership options

(besides national grid)

management • Utility owned

Energy Efficiency • Customer owned (own supply)

• Third party / customer owned (grid supply /

wheeling)

• Partnerships (e.g.. PPP)

Demand Fuel switching WTE & landfill gas Cogen and biogas

reponse (gas)

+ Opportunity to be utilised as

an embedded or distributed

solution

(whether likely to be pursued as distributed or

embedded/onsite solutions)

Gas turbines Solar (PV and CSP) RE incl Wind Energy storage

Greener options

Other technology

… innovations including Joburg

Water Hydro conduit Dams

26

NuclearUtilities globally are grappling

with these challenges

Largest generation company in the US RWE is one of Europe’s five leading Germany’s biggest utility distributing

and a vertically integrated utility that electricity and gas companies – i.e. a across Europe – vertically integrated

includes a retail business. generation, trading and distribution (Gx, Tx & Dx).

business.

Move to “carbon-lite” electricity grid;

“Our traditional business model is “spinning off” conventional, centralised

collapsing under us”. Referring to fossil fuel generation assets; focusing

2010 2014 flat demand for electricity instead on distributed generation,

- November 2013, Peter Terium, including solar, storage, and micro-grids

“As part of our continued

CEO of RWE

commitment to consumers, NRG “I think everyone understands at this

has embraced the idea of point that value creation is moving

enabling customers to make their “A significant part of our business downstream, to the customer, from

own energy choices.” - David model is now facing new the commodity side to the solution

Crane, CEO of NRG challenges,” side. So E.on is striving hard in

“Whatever we do in terms of cost Europe to go to those parts of the

“Sustainability is our reality and Capex-cutting won’t fully value chain where we are close to

We're partnering with businesses compensate the profit loss we see our 25 million customers, where we

to build a more sustainable in conventional power generation.” enable them and can share with

future.” RWE CFO, Bernhard Guenther them the advantages of efficiency.

- 5 Dec 2013

Moving from volumetric to value will take courage, but some are taking the first steps

27Shareholder Mandate

Drive Whilst

• Increasing and securing the • Reducing the burden of cost on

supply of energy the consumer

• Acquiring electricity from • Balancing the financial

renewable and alternative sustainability of the business,

sources delivery of services and

Shareholder goals

• Reducing greenhouse gas

emissions • Moving to the “Smart City”

concept via a Smart Grid and

• Strategic use of a mix of integration with other City

technologies and energy initiatives (e.g. transport)

sources to achieve goals

28Time of Use Tariffs Basket of energy options

Load shedding IPP PV Renewable City – Waste to

240

mitigation applications Energy tariff Energy

Embedded GX PPA MTN / Rural Gas/PV City – Landfill

30

3

policy ABSA systems Gas

City –

Demand Solar Water Diesel

60

20

Gravitational feed

Response Heaters Generation GX

Demand Side

200

Electric Vehicles

Kelvin Battery Storage charging

Management

Smart meter / Gas Turbines

112

Independent Power Producers /

80

Load Limiting (OCGT) Embrace Renewable Energies

Own Rooftop

20

Ripple Control Structural Open

6

PV Changes Grid/Trading

Immediate Short term Longer termDISCUSSIONS /

THANK YOU

30You can also read