Seeking Zen: A Post-Pandemic 3PL Market - Latest Third-Party Logistics Market Results and Predictions for 2021 Including Estimates for 190 ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Seeking Zen:

A Post-Pandemic 3PL Market

Latest Third-Party Logistics Market

Results and Predictions for 2021

Including Estimates for 190 Countries

August 2021

Phone: +1-800-525-3915

Website: www.3PLogistics.com

Email: Armstrong@3PLogistics.com

ABOUT ARMSTRONG & ASSOCIATES, INC.

Armstrong & Associates, Inc. (A&A) was established in 1980 to meet the needs of a newly deregulated domestic

transportation market. Since then, through its leading Third-Party Logistics (3PL) market research and history of

helping companies outsource logistics functions, A&A has become an internationally recognized key resource

for 3PL market information and consulting.

A&A’s mission is to have leading proprietary supply chain knowledge and market research not available

anywhere else. As proof of our continued work in supporting our mission, A&A’s 3PL market research is

frequently cited in media articles, publications, and securities filings by publicly traded 3PLs. In addition, A&A’s

email newsletter currently has over 88,000 subscribers globally.

A&A’s market research complements its consulting activities by providing continually updated data for analysis.

Based upon its unsurpassed knowledge of the 3PL market and the operations of leading 3PLs, A&A has

provided strategic planning consulting services to over 30 3PLs, supported 24 closed investment transactions,

and provided advice to numerous companies looking to benchmark existing 3PL operations or outsource

logistics functions.

All Rights Reserved.

No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form by

any means, electronic, mechanical, photocopied, recorded or otherwise, without the prior permission of the

publisher, Armstrong & Associates, Inc.

The facts of this report are believed to be correct at the time of publication but cannot be guaranteed. Please

note that the findings, conclusions and recommendations that Armstrong & Associates delivers will be based

on information gathered in good faith from both primary and secondary sources, whose accuracy we are not

always in a position to guarantee. As such, Armstrong & Associates can accept no liability whatsoever for

actions taken based on any information that may subsequently prove to be incorrect.

©2021 Armstrong & Associates, Inc.

U.S. 3PL MARKET

COVID, Volatility and the Reopening

The volatile 2020 U.S. COVID-driven Third-Party Logistics (3PL) Market created growth opportunities

for Third-Party Logistics Providers (3PLs) with strong carrier management, e-commerce, and air freight

forwarding capabilities, while other 3PLs did not fare as well. After having a lackluster 2019 when we saw

a year-over-year decline in transportation activity as import tariffs took hold, we awoke to a pandemic

nightmare in March of 2020 with vast economic shutdowns. In May things began bouncing back as

shutdowns were dialed back and the V-shaped recovery took hold. Even with its local and regional

economic “spits and spurts”, inventories needed to be replenished, and PPE (Personal Protective

Equipment) drove strong air freight demand. There was no time like the present for logistics expertise,

and 3PL prevailed as an essential industry.

Overall, strong domestic and international transportation demand has continued into 2021 further driving

up domestic and international transportation rates. With inventories increasing and COVID case counts

waning, demand for 3PL services seems to be becoming more stable and manageable. As we get closer

to herd immunity in the COVID battle, and barring any shut downs from variants, we should continue to

see increasingly strong demand as more consumers continue to leave quarantine and boost spending.

2021 might be the true start of our generations’ roaring 20’s.

Armstrong & Associates’ (A&A’s) current estimates show U.S. 3PL Market gross revenues grew 8.8%,

bringing the total U.S. 3PL Market to $231.5 billion. Most of the growth came from international and

domestic transportation management which responded to COVID-related demands for PPE and to

restock inventories upon economic reopenings. Overall, 2020 was a better year for 3PLs than 2019,

which registered the Market’s first decline since 2009, but segment growth was uneven.

Figure 1. U.S. 3PL Market 2010 - 2021E (US$ Billions)

©2021 Armstrong & Associates, Inc. 3

U.S. 3PL MARKET

Total 3PL segment net revenues (gross revenues less purchased transportation) grew 2.1% to $93.5

billion reflecting gross margin compression due to a volatile carrier sourcing market and transportation

management 3PLs spending more to secure hard-to-find carrier capacity. The overall gross margin for

all segments declined from 44% to 41%.

Table 1. U.S. 3PL Market Growth by Segment

Gross Revenue 2020 vs. 2019 1995-2020

Net Revenue

3PL Segment (Turnover) Net Revenue Net Revenue

(US$ Billions)

(US$ Billions) YOY % CAGR

DTM 91.2 13.2 -1.8% 10.5%

ITM 70.0 24.6 11.4% 10.8%

DCC 20.0 20.0 0.3% 7.3%

VAWD 46.7 35.7 -1.1% 10.2%

Total* 227.9 93.5 2.1% 9.6%

*Total 2020 gross revenue (turnover) for the 3PL market in the U.S. is estimated at $231.5 billion. $3.6 billion is included for the

contract logistics software segment.

International Transportation Management (ITM)

Leading all 3PL segments for revenue growth in 2020 was International Transportation Management

(ITM) which consists of air and ocean freight forwarding, customs brokerage, and complementary value-

added services. Air freight revenues swelled in 2020 with the pandemic and extraordinary demand for

PPE. With commercial passenger aircraft making up approximately 40% of total air cargo capacity, the

pandemic upended air freight forwarding, and rates surged albeit on lower overall volumes. While air

freight volumes are now above pre-pandemic levels, even with ongoing additions to increase air carrier

capacity, it is still under pre-pandemic levels.

With the economic reopenings in May of 2020, ocean freight demand came on strong as shippers

worked on replenishing inventories. The ongoing results have been port congestion, tight container

drayage capacity, and increased rates. “Blank Sailings” where a scheduled ship is cancelled from a route,

and stronger ocean carrier alliances, have also reduced ocean capacity and buoyed rates.

Overall, ITM realized a 19.2% gross revenue gain in 2020 expanding to $70 billion. While having a lower

growth rate than overall gross revenue, due to a tight carrier capacity market, net revenue increased a

healthy 11.4% to $24.6 billion.

As of July 2021, the good news is that overall capacity is trending up in most ocean and air markets, as

we dig out of the critical situation earlier this year, and port conditions in the U.S. are improving.

For North Asia to the U.S., ocean capacity is still very tight and spot rates are continuing to rise. The air

freight situation is improving, and spot-rate pressure is declining.

The South Asian market is still very strained as COVID has gripped the area. Ocean capacity is declining,

and spot rates are on the rise. Shippers are having to book 2-4 weeks in advance to get capacity. Air

©2021 Armstrong & Associates, Inc. 4

U.S. 3PL MARKET

freight capacity is starting to improve, and spot rates are moderating.

Europe to U.S. ocean capacity is improving, but equipment shortages in Europe are affecting port

operations. This is forcing some shippers to utilize air freight. Air freight capacity is improving and should

improve as more passenger aircraft come online. The main challenge now is flight cancellations.

We expect an improving but tight carrier capacity situation going into 2022 which will keep an upward

pressure on rates. Air capacity will continue to grow with increased passenger belly capacity availability.

A&A’s Top 25 Global Freight Forwarders list for 2020 is provided below. This list is compiled using a

combined overall average ranking which is based on each provider’s individual rankings for gross

logistics revenue, ocean freight 20-foot equivalent units/containers (TEUs), and air freight metric tons

handled in 2020. Averages for this year’s Top 25 Global Freight Forwarders show that although year-

over-year gross logistics revenue growth was up 8.2%, ocean and air freight volumes both fell 3.2% over

2019.

Table 2. Top 25 Global Freight Forwarders*

Gross Revenue Air Metric

Rank Provider Headquarters Ocean TEUs

(US$ M) Tons

1 DHL Supply Chain & Global Forwarding Germany 28,453 2,862,000 1,667,000

1 Kuehne + Nagel Switzerland 25,787 4,529,000 1,433,000

2 DB Schenker Germany 20,761 2,052,000 1,094,000

2 DSV Panalpina Denmark 18,269 2,204,902 1,272,405

3 Sinotrans China 12,174 3,750,000 532,300

4 Expeditors United States 10,116 1,091,380 926,730

5 Nippon Express Japan 19,347 660,152 720,115

6 CEVA Logistics France 7,416 **1,081,100 363,300

7 C.H. Robinson United States 15,490 1,200,000 225,000

7 UPS Supply Chain Solutions United States 11,048 620,000 988,880

8 Kerry Logistics Hong Kong 6,867 1,019,924 493,903

9 GEODIS France 9,135 866,631 290,506

10 Bolloré Logistics France 5,265 761,000 574,000

11 Hellmann Worldwide Logistics Germany 2,740 905,100 552,640

12 Kintetsu World Express Japan 5,750 640,063 556,875

13 Agility Kuwait 4,018 771,000 372,000

14 Yusen Logistics Japan 4,248 764,000 337,000

15 CTS International Logistics China 2,160 1,021,007 398,175

16 DACHSER Germany 6,591 **492,440 310,860

17 Toll Group Australia 7,260 523,300 117,400

18 Hitachi Transport System Japan 6,346 462,000 221,000

19 Maersk Logistics Netherlands 6,963 401,369 138,086

20 Apex Logistics International Hong Kong 2,274 190,000 750,000

21 Logwin Luxembourg 1,292 698,000 167,000

22 Mainfreight New Zealand 2,467 347,638 114,736

*Revenues and volumes are company reported or Armstrong & Associates, Inc. estimates. Revenues have been converted to

US$ using the average annual exchange rate in order to make non-currency related growth comparisons. Freight forwarders are

ranked using a combined overall average based on their individual rankings for gross revenue, ocean TEUs and air metric tons.

**Includes LCL shipments.

In the following table we provide a comparison of 12 of the largest global freight forwarders broken out

by region. For Asia, Apex Logistics International was the clear winner. In Europe, the combined DSV

Panalpina took the cake, and in the United States, C.H. Robinson came out on top.

©2021 Armstrong & Associates, Inc. 5

U.S. 3PL MARKET

Table 3. Top Global Freight Forwarders 2020 vs. 2019 Select Providers Comparison

Gross Revenue Ocean TEUs Air Metric Tons

Provider Headquarters

YOY % YOY % YOY %

Sinotrans China 8.7% -0.5% 6.0%

Apex Logistics International Hong Kong 51.6% 137.5% 44.2%

Kerry Logistics Hong Kong 30.2% -18.4% 20.6%

Kintetsu World Express Japan 13.5% -0.7% -1.8%

Nippon Express Japan -3.0% -6.1% -4.4%

CEVA Logistics France 4.1% 3.0% -12.7%

DHL Supply Chain & Global Forwarding Germany 4.2% -10.8% -18.7%

DB Schenker Germany 7.3% -10.5% -7.8%

DSV Panalpina Denmark 27.3% 15.6% 18.8%

Kuehne + Nagel Switzerland -0.3% -6.8% -12.8%

C.H. Robinson United States 5.9% 20.0% 7.1%

Expeditors United States 23.7% -3.0% -3.0%

While headquartered in Hong Kong, Apex Logistics International has significant operations in the U.S.

and is one of the largest China/U.S. air freight forwarders. Its air freight metric tons grew 44% from

520,000 in 2019 to 750,000 in 2020 driving a 52% increase in gross revenue to $2.3 billion. Apex Logistics

managed multiple weekly air charters of PPE from China to the U.S. and has burgeoning e-commerce

business. It also more than doubled its ocean freight forwarding business which ended 2020 with

190,000 TEUs.

In May 2021, Kuehne + Nagel completed its purchase of Apex Logistics for approximately $1.5 billion. The

combination makes Kuehne + Nagel the largest global air freight forwarder with over 2.1 million metric

air tons surpassing DHL Supply Chain & Global Forwarding. It also significantly expands Kuehne +

Nagel’s Asian 3PL operating network.

2020 marked the first full year of the combined DSV Panalpina, since the August 2019 merger of DSV

and Panalpina, and the combination is working out nicely with double-digit growth in global 3PL

revenues and freight forwarding volumes. The Americas division of Denmark headquartered DSV

Panalpina also grew its top-line ITM gross revenue 38.6% to $3.2 billion and net revenue by 29.5% to

$731.8 million with increases in both air and ocean volumes. Volume-wise, it is the third largest air freight

forwarder globally and fourth largest ocean freight forwarder.

C.H. Robinson, the largest Domestic Transportation Manager, saw a 6% increase in overall 3PL revenues

in 2020. Its Global Forwarding division grew 33.2% to $3.1 billion and net revenue increased 17.8% to

$629 million. It has been expanding rapidly in ITM via a mix of acquisitions and organic growth. In 2011,

it had net revenue of $100 million. To add significant capabilities and operational scale, it acquired $807

million ITM provider Phoenix International in 2012. From there, it added $251 million Aussie provider APC

Logistics in 2016, $124 million Canadian ITM Milgram in 2017, and $84 million Madrid, Spain based Space

Cargo in 2019.

Expeditors International, the largest of the U.S. based freight forwarders, had a better than average

2020 with gross revenue increasing 23.7% to $10.1 billion and net revenue increasing 11% to $2.9 billion.

Growth primarily came from air freight where gross revenue grew a whopping 63% to $4.8 billion from

$2.9 billion in 2019. Ocean gross revenue was up 6% to $2.4 billion. Net revenues grew at a lesser rate

due to increased costs of purchased transportation decreasing operating profit margins in both air and

©2021 Armstrong & Associates, Inc. 6U.S. 3PL MARKET ocean. Dedicated Contract Carriage (DCC) The asset-heavy Dedicated Contract Carriage (DCC) 3PL segment had the second highest net revenue growth of the four 3PL segments with just 0.3% to $20 billion. Gross revenue declined 2%. The negative effect of COVID made 2020 a volatile and lower-volume year versus 2019 when DCC net revenues grew 12.1%. Traditional DCC contracts have one- to three-year terms with specific trucking assets being dedicated to customers. This makes DCC contracts much “stickier” than standard shipper/carrier trucking contracts. A&A’s market research shows dry van trailers being used for 70% of DCC truckloads, reefers 16%, flatbeds 6%, and tankers and others 8%. Three‐fourths of major DCC providers have dry vans and reefers. Half of major DCC providers have flatbeds. Customer trailers/containers are often used especially for retail operations like Walmart. Other types of equipment include bulk tankers, curtain sides, roller beds, end dumps, drop decks, and dry vans with lift gates. The DCC segment leader J.B. Hunt Dedicated Contract Services (DCS) with 9,911 power units in dedicated, posted above average net revenue growth of 3.2% to $2.2 billion making its DCC market share 11% on a net revenue basis. It has over 160 customers and A&A estimates that about half of J.B. Hunt’s dedicated tractors are tandem axle sleepers. About as many are day cabs used in regional operations. A significant part of Hunt’s DCS operations involve direct store delivery. It has also developed a large last-mile delivery network which has significant home delivery capabilities. Penske Logistics, helped by its 2020 acquisition of Black Horse Carriers and 2018 acquisition of EPES Transport System, has grown into the second largest dedicated fleet with 8,436 power units. Combined DCC revenues are estimated at over $1 billion. Werner Dedicated also generated above average growth of 2.2%, expanding net revenue to $1.1 billion. It now ranks fifth with 4,945 power units in DCC. It manages over 120 individual customer fleets ranging from one to over 100 tractors. About 70% of the fleets are managed on-site at customer locations and approximately 30% of its smaller customer fleets are managed from Werner Enterprises’ operations center in Omaha, Nebraska. We expect moderate DCC demand and growth for 2021 as the economy further rebounds. A lot will hinge upon continued strength in contract truckload rates. Domestic Transportation Management (DTM) Non-asset based Domestic Transportation Management (DTM) includes Freight Brokerage which is 83% of segment revenues and Managed Transportation which accounts for 17%. In 2020, 3PLs scrambled to find carrier capacity to meet shipper demand. Gross revenue increased 9.9% to $91.2 billion, but net revenue decreased 1.8% to $13.2 billion as volatility in motor carrier capacity quickly increased spot market rates compressing segment gross margins by 1.7%. The ongoing digitalization of transactional truckload DTM/Freight Brokerage continues at a rapid pace as more large shippers have built integrations to 3PL’s transportation management systems (TMS) for ©2021 Armstrong & Associates, Inc. 7

U.S. 3PL Market API (Application Program Interface) truckload spot-market rate quoting and automated load tendering and booking. In turn, about 20 3PLs have built TMS interfaces which provide these shippers instant rate quotes and the ability to complete load tendering and booking through the system APIs. This process automates traditional spot-market freight brokerage sales functions and is increasing shippers’ use of more spot versus contract pricing. Sales automation for spot-market truckload automation is happening in conjunction with the automation of carrier sales (procurement) functions within freight brokers using intelligent capacity management systems to digitally match shippers’ loads to carriers based upon historical and real-time carrier capacity data analyzed via machine learning/artificial intelligence algorithms. This Digital Freight Matching (DFM) capability has become a competitive differentiator within the DTM segment as DTM 3PLs look to increase the number of loads/shipments they manage per person per day. Ultimately, this automation will put further pressure on freight brokerage gross margins, while it should improve overall profitability. Top DTM/Freight brokers, C.H. Robinson, TQL, XPO Logistics, Hub Group and Echo Global Logistics, are some of the 3PLs driving industry automation along with the newer tech-first Digital Freight Brokers and DTM Market entrants Convoy, Transfix, and Uber Freight. At this point, most of the top freight brokers are strategically looking at ways to digitalize operations while adding value through improved carrier management, and customer and carrier experiences. The DTM “watch list” again includes rapidly growing Nolan Transportation Group (NTG) which had year-over-year net revenue growth of 33.7% to $167 million and 2020 gross revenue of $1.2 billion. Gryphon Investors bought a majority stake in NTG through its portfolio company Transportation Insight in December 2018. Nolan too is leading the digitalization charge. The combined entity now ranks third on our Top DTM/Freight Brokers list. LTL-centric Priority1 also saw rapid growth with increasing net revenue 31.7% to $79 million on gross revenue of $425 million. Also of mention is PepsiCo’s DTM operation, Pepsi Logistics, which grew net revenue 14.6% to $40 million on $469 million in gross revenue. Value-Added Warehousing and Distribution (VAWD) Rapid growth in e-commerce fulfillment could not offset the loss of business-to-business related activity as overall revenues for the Value-Added Warehousing and Distribution (VAWD) 3PL segment sagged in 2020 versus its 9% growth 2019. VAWD net revenues declined 1.1% to $35.7 billion. VAWD 3PLs continue to benefit from growth in retail e-commerce business, which continues to be the fastest growing domestic 3PL segment with a compound annual growth rate of 28% since 2017. Many VAWD 3PLs are supporting retail brands’ strategies to manage their own order fulfillment channels and avoid being captive to large e-retailer platforms such as Amazon. Operationally, the growth in in e-commerce business has meant an expansion in multi-client warehousing/fulfillment operations; many having footprints of under 100,000 square feet. An ongoing headwind for VAWD 3PLs has been the “Amazon Effect”. 3PLs are continuing to see increased competition from Fulfillment by Amazon (FBA) which controls 60% of the U.S. E-commence 3PL Market. It has dramatically impacted warehouse employee wages and lease rates in key distribution areas such as Plainfield, Indiana, and California’s Inland Empire. In turn, it is driving significant interest ©2021 Armstrong & Associates, Inc. 8

U.S. 3PL Market

from VAWD 3PLs to automate warehouses with autonomous robotic solutions. With some autonomous

robots costing less than $500 per month to operate, the cost/benefit and positive return on investment

are increasing 3PLs’ interest in warehouse robots to support activities such as picking, putaway, and

cycle counting.

In terms of North American warehousing square footage, when Amazon and its over 185 million square

feet of estimated 3PL warehousing space is excluded, DHL Supply Chain leads the pack with 140 million

square feet, GXO Logistics (formerly XPO Logistics) is second with 101 million, Ryder SCS is third with 64

million, NFI is fourth with 53 million and Geodis rounds out the top five with 52.2 million square feet of

warehousing space within North America.

Walton, Kentucky based Verst Logistics was one of the growth leaders in 2020 with net revenue growing

14.6% to $240 million. As a mid-market 3PL, it manages large contract packaging operations for

customers in consumer goods, and food and beverage industries. Verst also manages a 396,000 square

foot multi-client e-commerce fulfillment center in Hebron, Kentucky.

RLS Logistics, a mid-market 3PL based in Newfield, New Jersey focusing on refrigerated and frozen

food, also had a good year with 18% revenue growth to $123 million. RLS has 20 million cubic feet of

refrigerated warehousing space in the U.S. Its service offering includes frozen pick/pack e-commerce

fulfilment operations and refrigerated and frozen less-than-truckload consolidation. In September 2020,

RLS expanded its presence in northeast Pennsylvania with the acquisition of third-generation, family-

owned cold storage provider Gress Refrigerated Services & Logistics.

In terms of U.S. segment net revenue compound annual growth rates, ITM has surpassed DTM with a

CAGR of 10.8% since 1995. The most mature segment, DCC, has grown only 7.3% versus its double-digit

contenders and is seeing growing competition from Dedicated Truckload Capacity (DTC) providers.

Figure 2. U.S. 3PL Market Segment Net Revenues (US$ Millions) and CAGRs*

$41,000

$39,000

$37,000

$35,000 10.2%

$33,000

$31,000

$29,000

$27,000

$25,000 10.8%

$23,000

$21,000

$19,000 7.3%

$17,000

$15,000

$13,000

$11,000 10.5%

$9,000

$7,000

$5,000

$3,000

$1,000

Value-Added Warehousing & Distribution (VAWD) - Asset Based

Dedicated Contract Carriage (DCC) - Asset Based

International Transportation Management (ITM) - Non-Asset Based

Domestic Transportation Management (DTM) - Non-Asset Based

*CAGRs are from 1995-2020.

©2021 Armstrong & Associates, Inc. 9U.S. 3PL MARKET

In Dedicated Truckload Capacity, a provider agrees to provide ongoing trucking capacity to a customer

account in specific lanes or routes, and equipment can be shared between customers versus traditional

DCC. In a recent study conducted by A&A, it was found that DTC is growing at over five times the rate of

traditional DCC.

Going into 2021, ITM and DTM remain the strongest segments with year-over-year gross revenue growth

expected at an astounding 42.5% and 22.3%, respectively, over 2020. Segment net revenues should see

double-digit growth as well.

Overall, the U.S. 3PL Market is expected to grow 24% to $287 billion.

Table 4. U.S. 3PL Segment Growth Predictions for 2021

2021E

2021E vs. 2020 2021E 2021E vs. 2020

Gross Revenue

3PL Segment Gross Revenue Net Revenue Net Revenue

(Turnover)

(YOY %) (US$ Billions) (YOY %)

(US$ Billions)

DTM 111.5 22.3% 15.8 20.3%

ITM 99.8 42.5% 30.6 24.2%

DCC 21.0 4.8% 21.0 4.8%

VAWD 50.9 8.9% 38.6 8.2%

Total* 283.2 23.9% 106.0 13.4%

*Total 2021 gross revenue (turnover) for the 3PL market in the U.S. is estimated at $286.9 billion. $3.7 billion is included for the

contract logistics software segment.

Top U.S. 3PLs

On this year’s Top 50 list, after mainstays C.H. Robinson, XPO Logistics and UPS Supply Chain Solutions,

the largest U.S. freight forwarder Expeditors passed J.B. Hunt for fourth place; although Hunt remains a

Top 5 player for the foreseeable future.

Transportation Insight and Total Quality Logistics hit Top 10 status this year pushing out Ryder Supply

Chain Solutions and Hub Group. Total Quality Logistics, also the fourth largest DTM, achieved this via

organic growth. Whereas 4PL, Transportation Insight, was helped by acquisitions. The most notable

being, Nolan Transportation Group, making the combined entity the third largest DTM.

New to this year’s list are the Americas operations of Netherlands based Maersk Logistics (Primarily

the former Damco. The brand was discontinued in October 2020), and Hong Kong’s Kerry Logistics as

well as U.S. based 3PLs AIT Worldwide Logistics, Ascent Global Logistics, Capstone Logistics and Uber

Freight.

AIT was helped by recent purchases of UK based next-day delivery specialist, Panther Logistics,

in November 2020 and Germany’s Fiege Group’s international freight forwarding division, Fiege

Forwarding, a month later. In March, AIT was taken over by private equity firm The Jordan Company in

what is expected to mark the start of another period of growth.

©2021 Armstrong & Associates, Inc. 10U.S. 3PL MARKET

U.S. Express and Cardinal Logistics Management just missed the list at 51st and 52nd, respectively.

Radiant Logistics, Nippon Express (Americas), Neovia Logistics, and SEKO fell a few notches.

Table 5. Top 50 U.S. 3PLs by Gross Logistics Revenue

2020 Gross Revenue

Rank Provider

(US$ Millions)*

1 C.H. Robinson 15,490

2 XPO Logistics 12,107

3 UPS Supply Chain Solutions 11,048

4 Expeditors 10,116

5 J.B. Hunt 9,198

6 Kuehne + Nagel (Americas) 6,789

7 DHL Supply Chain (North America) 4,415

8 Coyote Logistics 4,280

9 Transportation Insight/Nolan Transportation Group 4,270

10 Total Quality Logistics 4,138

11 Burris Logistics 4,100

12 DSV Panalpina (Americas) 4,020

13 Ryder Supply Chain Solutions 3,774

14 Hub Group 3,646

15 Transplace 3,400

16 Penske Logistics 3,200

17 Schneider 2,814

18 NFI 2,631

19 DB Schenker (North America) 2,627

20 GEODIS (North America) 2,543

21 Echo Global Logistics 2,512

22 Ingram Micro Commerce & Lifecycle Services 2,300

23 Landstar 2,196

24 FedEx Logistics 2,100

24 MODE Transportation 2,100

25 CEVA Logistics (Americas) 2,000

26 Americold 1,983

27 GlobalTranz Enterprises 1,651

28 Worldwide Express/Unishippers 1,650

29 Lineage Logistics 1,645

30 BDP International 1,552

31 Werner Logistics 1,527

32 Knight-Swift Transportation 1,430

33 Maersk Logistics (Americas) 1,300

33 TransGroup Global Logistics 1,300

34 Ruan 1,223

35 AIT Worldwide Logistics 1,220

36 syncreon 1,203

37 Radial 1,200

38 Universal Logistics Holdings 1,190

39 Nolan Transportation Group 1,172

40 Kerry Logistics (Americas) 1,115

41 Capstone Logistics 1,040

42 Odyssey Logistics & Technology 1,018

43 Uber Freight 1,011

44 Ascent Global Logistics 974

45 Crane Worldwide Logistics 916

46 OIA Global 876

47 Pilot Freight Services 874

48 APL Logistics (Americas) 867

**Revenues cover all four 3PL Segments (DTM, ITM, DCC and VAWD), are company reported or A&A estimates, and have been

converted to US$ using the annual average exchange rate.

©2021 Armstrong & Associates, Inc. 11GLOBAL COSTS AND REVENUE

Global Logistics Market and Third-Party Logistics

Revenues

Global Third-Party Logistics (3PL) Market revenues reached $962 billion in 2020 resulting in a meager

0.1% increase over 2019 versus the U.S. 3PL Market which saw 8.8% year-over-year growth. As with the

U.S., the ITM segment led the way due to COVID-19 response.

For 2021, we expect a rise of over 15% in 3PL revenues globally as the market continues to evolve

unevenly with some countries still being significantly impacted by COVID-19 versus those with higher

vaccination rates.

Over the next three years, through 2023, we estimate the global 3PL market will see a CAGR near 10%.

Developed countries with longstanding transportation and warehouse contracting practices have

the largest 3PL revenues. Developing countries are growing at faster rates, but have lower total 3PL

revenues. The numbers reflect the greater outsourcing of functions to 3PLs in developed and more

economically sophisticated countries.

Table 6. 2020-2021E Global Logistics Market and 3PL Segment Revenues by Country/Region (US$ Billions)

2020 3PL 2020 ITM 2020 VAWD 2020 TM 2021E Logistics 2021E 3PL 2021E ITM 2021E VAWD 2021E TM

Country/Region 2020 Logistics Cost

Revenue Revenue Revenue Revenue Cost Revenue Revenue Revenue Revenue

Algeria 23.8 1.9 0.6 0.5 0.8 25.0 2.0 0.7 0.5 0.8

Egypt 30.0 2.6 0.8 0.7 1.1 30.0 2.6 0.9 0.7 1.0

Morocco 17.0 1.4 0.4 0.4 0.6 18.6 1.6 0.6 0.4 0.6

Nigeria 69.1 5.1 1.6 1.3 2.2 82.8 6.2 2.2 1.6 2.4

South Africa 32.9 3.4 1.1 0.9 1.5 35.9 3.8 1.3 1.0 1.5

Sudan 6.0 0.5 0.1 0.1 0.2 6.3 0.5 0.2 0.1 0.2

Africa-Others 165.3 12.9 4.0 3.3 5.6 180.0 14.3 5.0 3.6 5.5

Africa Total 344.2 27.9 8.5 7.0 12.0 378.6 30.9 10.9 7.8 12.0

Australia 116.9 12.4 3.8 3.1 5.4 139.1 14.9 5.3 3.8 5.8

Bangladesh 51.3 4.3 1.3 1.1 1.8 55.1 4.6 1.6 1.2 1.8

Brunei Darussalam 1.8 0.2 0.0 0.0 0.1 2.3 0.2 0.1 0.0 0.1

Cambodia 4.3 0.3 0.1 0.1 0.1 4.5 0.4 0.1 0.1 0.1

China 2,134.8 227.4 69.7 57.5 98.2 2,413.1 259.4 91.5 65.6 100.3

Hong Kong 29.7 3.4 1.0 0.9 1.5 31.3 3.6 1.3 0.9 1.4

India 351.8 26.0 8.0 6.6 11.2 396.1 29.7 10.5 7.5 11.5

Indonesia 233.1 18.0 5.5 4.5 7.8 254.9 19.9 7.0 5.0 7.7

Japan 429.1 46.8 14.3 11.8 20.2 457.1 50.3 17.7 12.7 19.4

Lao P.D.R. 3.4 0.3 0.1 0.1 0.1 3.6 0.3 0.1 0.1 0.1

Macao SAR 2.4 0.3 0.1 0.1 0.1 3.9 0.4 0.1 0.1 0.2

Malaysia 44.0 3.3 1.0 0.8 1.4 50.3 3.8 1.3 1.0 1.5

Myanmar (Burma) 14.0 1.1 0.3 0.3 0.5 13.1 1.0 0.4 0.3 0.4

New Zealand 23.4 2.3 0.7 0.6 1.0 27.3 2.7 1.0 0.7 1.1

Philippines 47.1 3.5 1.1 0.9 1.5 52.3 3.9 1.4 1.0 1.5

Singapore 28.9 3.5 1.1 0.9 1.5 31.8 3.9 1.4 1.0 1.5

South Korea 146.7 16.9 5.2 4.3 7.3 162.5 18.8 6.6 4.8 7.3

Sri Lanka 15.1 1.1 0.3 0.3 0.5 15.8 1.1 0.4 0.3 0.4

Taiwan 60.4 6.8 2.1 1.7 2.9 68.5 7.8 2.8 2.0 3.0

Thailand 75.3 5.8 1.8 1.5 2.5 80.8 6.3 2.2 1.6 2.4

Vietnam 68.2 5.4 1.7 1.4 2.3 71.0 5.7 2.0 1.4 2.2

Asia Pacific-Others 15.3 1.2 0.4 0.3 0.5 16.1 1.3 0.4 0.3 0.5

Asia Pacific Total 3,896.9 389.9 119.6 98.7 168.5 4,350.6 440.0 155.2 111.3 170.2

Kazakhstan 24.9 2.1 0.6 0.5 0.9 28.4 2.4 0.9 0.6 0.9

Russia 237.2 19.2 5.9 4.9 8.3 256.2 20.9 6.9 5.3 8.5

Ukraine 24.1 2.0 0.6 0.5 0.9 26.2 2.2 0.8 0.5 0.8

CIS-Others 42.8 3.4 1.0 0.9 1.5 46.0 3.7 1.3 0.9 1.4

CIS Total 329.1 26.7 8.2 6.8 11.6 356.7 29.2 9.9 7.4 11.7

©2021 Armstrong & Associates, Inc. 12TOP GLOBAL 3PLS

2020 Logistics 2020 3PL 2020 ITM 2020 VAWD 2020 TM 2021E 2021E 3PL 2021E ITM 2021E VAWD 2021E TM

Country/Region

Cost Revenue Revenue Revenue Revenue Logistics Cost Revenue Revenue Revenue Revenue

Austria 35.9 3.9 1.2 1.0 1.7 40.3 4.3 1.5 1.1 1.7

Belgium 41.1 4.4 1.3 1.1 1.9 46.4 5.0 1.8 1.3 1.9

Czech Republic 21.5 2.4 0.7 0.6 1.0 24.6 2.7 1.0 0.7 1.1

Denmark 30.8 3.2 1.0 0.8 1.4 34.4 3.6 1.3 0.9 1.4

Finland 22.8 2.4 0.7 0.6 1.1 25.3 2.7 1.0 0.7 1.0

France 228.2 23.8 7.0 4.8 11.8 258.0 27.0 9.1 4.8 12.8

Germany 308.5 32.4 9.8 6.5 15.8 350.3 36.9 12.8 6.5 17.2

Greece 23.4 2.1 0.7 0.5 0.9 25.9 2.4 0.8 0.6 0.9

Hungary 15.5 1.7 0.5 0.4 0.7 17.7 2.0 0.7 0.5 0.8

Ireland 32.4 3.8 1.2 1.0 1.7 36.9 4.4 1.5 1.1 1.7

Italy 169.4 17.4 5.1 3.5 8.6 189.2 19.5 6.6 3.5 9.3

Netherlands 67.5 9.9 2.9 2.0 4.9 75.2 11.0 3.7 2.0 5.2

Norway 32.4 3.3 1.0 0.8 1.4 39.7 4.1 1.4 1.0 1.6

Poland 60.3 6.1 1.9 1.6 2.7 65.2 6.6 2.3 1.7 2.6

Portugal 24.4 2.5 0.8 0.6 1.1 27.1 2.7 1.0 0.7 1.1

Romania 28.6 2.9 0.9 0.7 1.2 33.4 3.4 1.2 0.9 1.3

Spain 105.0 10.7 3.1 2.2 5.3 120.0 12.3 4.1 2.2 5.8

Sweden 42.2 4.4 1.3 1.1 1.9 49.1 5.1 1.8 1.3 2.0

Switzerland 62.1 6.6 2.0 1.7 2.8 68.6 7.2 2.6 1.8 2.8

United Kingdom 230.2 22.6 6.6 4.6 11.2 265.3 26.1 8.8 4.6 12.4

Europe-Others 71.8 7.2 2.2 1.8 3.1 81.2 8.1 2.9 2.1 3.1

Europe Total 1,653.7 173.8 52.0 38.0 82.2 1,873.8 197.1 67.9 39.9 87.7

Iran 103.0 8.3 2.6 2.1 3.6 110.6 9.1 3.2 2.3 3.5

Israel 45.5 4.5 1.4 1.1 1.9 50.5 5.0 1.8 1.3 2.0

Pakistan 41.0 3.4 1.0 0.9 1.5 41.0 3.4 1.2 0.9 1.3

Saudi Arabia 91.2 8.4 2.6 2.1 3.6 104.6 9.7 3.4 2.5 3.8

Turkey 89.2 8.5 2.6 2.1 3.7 98.5 9.5 3.3 2.4 3.7

United Arab Emirates 35.4 3.6 1.1 0.9 1.6 40.2 4.2 1.5 1.1 1.6

Middle East-Others 93.6 7.8 2.4 2.0 3.4 105.3 8.9 3.1 2.3 3.5

Middle East Total 498.9 44.6 13.7 11.3 19.3 550.7 49.8 17.6 12.6 19.3

Canada 147.9 15.7 4.8 4.0 6.8 169.5 18.1 6.3 4.6 7.1

Mexico 129.1 13.9 4.2 3.5 6.1 143.1 15.6 5.4 3.9 6.1

United States 1,674.6 231.5 70.0 46.7 111.2 1,814.0 286.9 99.8 50.9 132.5

North America-Others 73.8 6.3 1.9 1.6 2.7 79.2 6.8 2.4 1.7 2.6

North America Total 2,025.5 267.4 80.9 55.8 126.8 2,205.8 327.5 114.0 61.2 148.3

Argentina 46.6 4.3 1.3 1.1 1.9 50.2 4.7 1.7 1.2 1.8

Brazil 166.4 15.6 4.8 4.0 6.8 173.0 16.4 5.8 4.2 6.4

Chile 29.1 2.8 0.9 0.7 1.2 35.4 3.5 1.2 0.9 1.4

Colombia 33.9 2.9 0.9 0.7 1.3 37.0 3.2 1.1 0.8 1.2

Peru 25.5 2.2 0.7 0.6 1.0 28.2 2.5 0.9 0.6 1.0

Venezuela 5.6 0.4 0.1 0.1 0.2 5.1 0.4 0.1 0.1 0.1

South America-Others 36.8 3.0 0.9 0.8 1.3 38.5 3.2 1.1 0.8 1.2

South America Total 343.8 31.4 9.6 8.0 13.6 367.4 34.0 12.0 8.6 13.1

Grand Total 9,092.1 961.8 292.5 225.5 433.9 10,083.7 1,108.6 387.4 248.8 462.3

Sources: International Monetary Fund WEO April 2021, Nominal GDP forecast, Armstrong & Associates, Inc.

Top Global 3PLs

The Top 10 3PLs on this year’s list are fairly the same compared to 2019 except DB Schenker replaced

Nippon for 3rd, Sinotrans and XPO swapped places for 7th and 8th and Expeditors rounded out the Top

10 replacing J.B. Hunt.

Providers’ that have scaled this year’s list include GEODIS, NFI and Ingram Micro Commerce & Lifecycle

Services.

GEODIS’s revenues were reevaluated and now include its European last-mile delivery operations driving

its rank from 16th to 12th place.

©2021 Armstrong & Associates, Inc. 13TOP GLOBAL 3PLS

NFI grew its revenues 23.5% and its rank from 42nd to 36th. With acquisitions including Long Beach,

California based port logistics provider CalCartage and Canadian 3PL Dominion Warehousing &

Distribution, NFI’s distribution footprint is now 53 million square feet and consists of warehousing,

e-commerce, automated, cross-dock, transloading, and customs examination facilities. Its August 2020

acquisition of CAI Logistics, the non-asset logistics division of CAI International, Inc., marks NFI’s 20th

acquisition since 2000.

For Ingram Micro Commerce & Lifecycle Services, it’s all in the name. E-commerce is its game and it’s

playing well. Ingram Micro Commerce & Lifecycle Services is one of the largest B2C and B2B operations

in the country. It made its first debut on our Global list last year coming in at 46th place (from 53rd) and

this year it lands at 41st.

New to this year’s list are two Asia based companies. Hong Kong headquartered Apex Logistics

International and its 52% year-over-year increase in revenues landed it at 42nd place. China based, CTS

International Logistics, has freight forwarding as its core. The segment accounted for 70% of its business

in 2020. Other services CTS provides include cross-border e-commerce logistics, project logistics,

warehousing, and aviation supplies logistics.

APL Logistics and Worldwide Express/Unishippers, both at the bottom of the list last year, fell off this

year. However, with Worldwide Express’ recent merger with GlobalTranz and the combined company

generating $3.3 billion revenues in 2020, we expect it will place nicely on the list in 2021.

Table 7. Top 50 Global 3PLs by Gross Logistics Revenue

2020 Gross Revenue

Rank Provider

(US$ Millions)*

1 DHL Supply Chain & Global Forwarding 28,453

2 Kuehne + Nagel 25,787

3 DB Schenker 20,761

4 Nippon Express 19,347

5 DSV Panalpina 18,269

6 C.H. Robinson 15,490

7 Sinotrans 12,174

8 XPO Logistics 12,107

9 UPS Supply Chain Solutions 11,048

10 Expeditors 10,116

11 J.B. Hunt 9,198

12 GEODIS 9,135

13 CEVA Logistics 7,416

14 Toll Group 7,260

15 CJ Logistics 7,174

16 Maersk Logistics 6,963

17 Kerry Logistics 6,867

18 DACHSER 6,591

19 Hitachi Transport System 6,346

20 Kintetsu World Express 5,750

21 Bolloré Logistics 5,265

22 GEFCO 4,464

23 Coyote Logistics 4,280

24 Transportation Insight/Nolan Transportation Group 4,270

25 Yusen Logistics 4,248

26 Total Quality Logistics 4,138

27 Burris Logistics 4,100

28 Agility 4,018

29 Ryder Supply Chain Solutions 3,774

30 Hub Group 3,646

©2021 Armstrong & Associates, Inc. 14TOP GLOBAL 3PLS

2020 Gross Revenue

Rank Provider

(US$ Millions)*

31 Transplace 3,400

32 SAIC Anji Logistics** 3,202

33 Penske Logistics 3,200

34 Schneider 2,814

35 Hellmann Worldwide Logistics 2,740

36 NFI 2,631

37 Echo Global Logistics 2,512

38 Sankyu 2,491

39 Mainfreight 2,467

40 Imperial Logistics 2,334

41 Ingram Micro Commerce & Lifecycle Services 2,300

42 Apex Logistics International 2,274

43 Landstar 2,196

44 CTS International Logistics 2,160

45 FedEx Logistics 2,100

45 MODE Transportation 2,100

46 Groupe CAT 1,990

47 Americold 1,983

48 ID Logistics Group 1,930

49 Fiege Logistik 1,925

*Revenues cover all four 3PL Segments (DTM, ITM, DCC and VAWD), are company reported or A&A estimates, and have been

converted to US$ using the annual average exchange rate.

**In-house logistics revenues were capped at 50% for fairness.

In this year’s global Top 50, the number of U.S. based 3PLs that made the list fell from 22 to 21. Due to

CEVA Logistics’ headquarters move from Switzerland to France, Switzerland fell from 2 to 1 and France

gained another Top 50 Global 3PL. China’s CTS International Logistics and Hong Kong based Apex

Logistics International made the list growing China’s Global 3PL count from 3 to 4 and Hong Kong’s

from 1 to 2. Singapore based APL Logistics fell off the list bringing Singapore’s Global 3PL count to zero;

however, parent Japan headquartered Kintetsu World Express moved up two notched becoming a Top

20 Global 3PL.

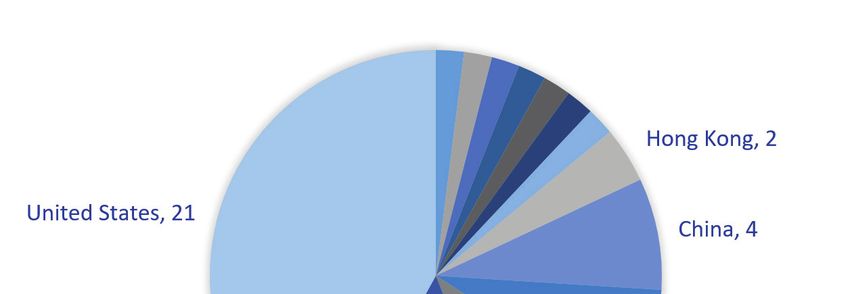

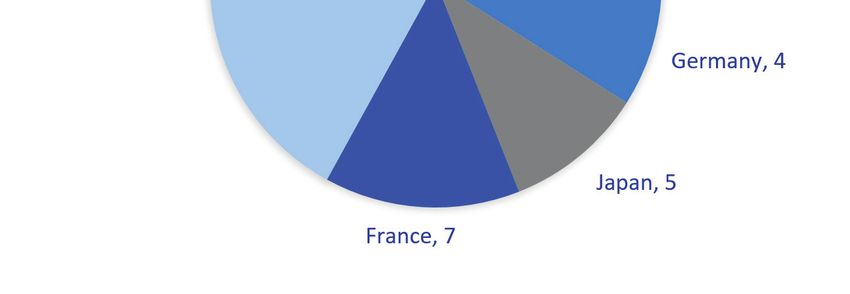

Figure 3. Top 50 Global 3PLs by Country

Australia, Denmark, Kuwait,

Netherlands, New Zealand,

South Africa, Switzerland, 1 each

©2021 Armstrong & Associates, Inc. 15MERGERS & ACQUISITIONS

Merger and Acquisition Activity

Where COVID is still raging, M&A activity is still muted. In countries where vaccines have stemmed the

spread, M&A activity is on the rise.

2020 saw eight large 3PL M&A deals with purchase prices over $100 million including one billion-dollar

deal slipping in at the end of 2020. Although the number of large deals is down from 2019’s level, 2021

has already experienced 11 large deals in just the first seven months with several $1B+ deals starting

to flourish in July. With the 3PL market as strong as it is, there are a lot of 3PL sellers eyeing up big

valuations.

Figure 4. 3PL Acquisitions over $100 Million 1999-July 2021

20

18 18

16

14

12 12

11 11 11

10

9 9

8 8

6 6

5 5 5 5 5

4 4 4

3 3 3

2 2

1 1

0 0

Americold snagged 2020’s largest deal with its purchase of the world’s fourth-largest temperature-

controlled operator, Agro Merchants Group, for $1.74 billion. Based in the Netherlands, Agro’s facilities

cover 236 million cubic feet across 10 countries in Europe, North America, South America and Australia.

After closing, Americold’s warehousing footprint comprised 229 owned and managed facilities and 1.35

billion refrigerated cubic feet of space.

Americold also made two additional purchases over $100 million in 2020. In January 2020, Americold

acquired Canada’s Nova Cold Logistics, and its 19 million cubic feet of temperature-controlled storage

space in Canada, from Brookfield Business Partners for $260.5 million. In its second largest deal of

2020, Americold bought New Jersey based, regional warehousing 3PL Hall’s Warehouse Corp. for $480

million. The deal added 1.6 million square feet of frozen, refrigerated, and dry warehousing space in

eight locations throughout New Jersey to Americold’s warehousing footprint. Americold also snatched

up two of the three $1 billion plus deals that were made in 2019.

Americold’s closest competitor, Lineage Logistics, also made the “purchases over $100 million” club

in 2020 with its acquisition of Emergent Cold for $900 million in June 2020. Just before the purchase,

Emergent Cold had acquired Polarcold, New Orleans Cold Storage, and Oxford Cold Storage

expanding Lineage’s footprint of facilities in the Asia Pacific region.

©2021 Armstrong & Associates, Inc. 16MERGERS & ACQUISITIONS In April 2020, Netherlands based Maersk acquired U.S. cross dock and international deconsolidation and distribution specialist Performance Team for $545 million including lease liabilities of around $225 million. With its footprint of facilities on both coasts (Los Angeles and New York/New Jersey), Dallas, and the Southeastern U.S. region and similar industry focus on consumer electronics, home goods, apparel/ footwear and retail, Performance Team should fit nicely in Maersk’s North American logistics portfolio. In March 2020, C.H. Robinson finalized its $225 million acquisition of Prime Distribution Services (PDS) from Roadrunner Transportation. PDS is a provider of retail consolidation and value-added warehousing and distribution services in North America. The addition expands C.H. Robinson’s retail consolidation business and adds some company-owned warehousing capability to its domestic service offering. In another $225 million dollar deal, Canada’s TFI International acquired DLS Worldwide in November 2020. Previously a business unit of R.R. Donnelley & Sons Company, Bolingbrook, Illinois based DLS Worldwide provides its logistics services through a network of internal sales personnel, commissioned sales agents and agent-stations. The acquired business will continue to operate as a standalone within TFI International’s Logistics segment under its new name “TForce Worldwide, Inc.” As for major 2021 deals, in February, it was announced that SF Holdings and Kerry Logistics were merging. SF, which has most of its operations within the PRC, will benefit from Kerry’s international expansion since its 2013 IPO and growing operations in Southeast Asia and Europe. Kerry Logistics’ business portfolio encompasses contract logistics, international freight forwarding, warehousing, transportation, distribution, trading, merchandising and a wide variety of value-added services and is now managing 52 million square feet of warehouse space, logistics centers and port facilities globally. Its International Freight Forwarding division accounts for 60% of revenues, and its Integrated Logistics division, mainly value-added warehousing and distribution, accounts for the rest. The Greater China region generates about half of gross revenues. Kerry Logistics has acquired several freight forwarders allowing it to expand internationally in countries such as Spain, Italy, Germany, Africa, and the U.S. Its joint venture with Dubai based freight forwarder, Globalink Logistics DWC LLC, expands Kerry Logistics’ coverage in Central Asia and the CIS region. Other recent joint ventures include expansion in e-commerce and food/cold chain logistics. In August 2019, the group acquired a majority interest in Turkey’s ASAV Logistics Services Inc. to further the expansion of its global network. On March 31, 2020, the group completed the acquisition of the remaining 49% in U.S. based Apex Maritime, the third largest NVOCC in terms of volume from Asia to the U.S. in 2019, at a consideration of approximately $176 million. The acquisition of Apex Logistics International, and its rapidly growing air freight forwarding and air charter operations, by Kuehne + Nagel for $1.2 billion was finalized in May. Apex has significant charter operations from China to the U.S. and has been developing significant air freight capacity out of Southeast Asia including Vietnam. Apex Logistics has grown quickly serving e-commerce, high-tech, and healthcare customers. Closer to home, in June 2021, Worldwide Express and GlobalTranz Enterprises announced their merger creating the 7th largest Domestic Transportation Manager/Freight Broker in the U.S. with combined 2020 gross revenue of $3.3 billion and the 32nd largest global 3PL. It combines Worldwide Express’ small parcel network and SMB customer focus with GlobalTranz’s LTL, TL freight brokerage and ©2021 Armstrong & Associates, Inc. 17

MERGERS & ACQUISITIONS managed transportation capabilities allowing for significant cross-selling opportunities. Worldwide Express will also be able to benefit from GlobalTranz’s proprietary technology platform which is above average among leading freight brokers. We would also be amiss if we didn’t mention Uber Freight’s recent $2.25 billion acquisition of Transplace. It combines Uber’s growing transactional Digital Freight Brokerage operations with Transplace’s leading managed transportation operations, which should avail itself to good cross-selling opportunities. Both have similar continuous improvement cultures and aren’t afraid to invest in leading tech. ©2021 Armstrong & Associates, Inc. 18

Market Research

New Releases from Armstrong & Associates, Inc.

Expert Information Service (E.I.S.)

Our premium market research and analysis offering includes

access to our most popular 3PL market research reports and a

subscription to our leading 3PL guide, Who’s Who in Logistics

Online. Discounted phone consulting is available.

INCREASINGLY

TRENDS INSTRATEGIC:

TRENDS IN 3PL / CUSTOMER

3PL / CUSTOMER

RELATIONSHIPS

RELATIONSHIPS

May 2020

November 2016

Phone: +1-800-525-3915

Website: www.3plogistics.com

Email: Armstrong@3plogistics.com

Digitization – The Convergence Increasingly Strategic – Rising Tide –

of Modern Freight Brokerage, Digital Trends in 3PL / Customer The Rapid Growth of

Freight Matching, and Automation Relationships E-Commerce Logistics, 3PL

in Domestic Transportation Solutions, Last-Mile Delivery,

Management and the Dominance of Amazon

Since our first report on Digital Freight This definitive analysis is an expanded This comprehensive report covers the

Matching (DFM) in 2016 where we dubbed update of Armstrong & Associates’ best- growth of e‐commerce logistics in the

the term “Digital Freight Matching”, there selling report. From its analysis of over U.S., e-commerce fulfillment and last-mile

has been increasing focus on these 7,700 current 3PL customer relationships delivery, third-party logistics provider

companies which have been seen by in 44 countries, totaling nearly 21,000 alternatives to Amazon, Amazon’s leading

investors as market disruptors. This report services, the report identifies and market position, and an “apples-to-apples”

details the convergence of DFM, modern details key trends in outsourced third- cost comparison between Fulfillment by

Domestic Transportation Managers, party logistics provider (3PL) customer Amazon (FBA) and 3PL solutions using

and Digital Freight Brokers. It provides relationships. Armstrong & Associates our proprietary e-commerce fulfillment

insights into what systems drive a 3PL’s has been tracking and analyzing 3PL/ pricing benchmarks from 21 3PLs

classification as a DFB and what systems Customer relationships for over a decade representing over 1,000 customers.

can be deployed to augment a TMS with ever-increasing detail.

and digitalize a DTM/Freight Brokerage

operation.

Reports are available for purchase at http://www.3plogistics.comYou can also read