Taking a Deep Dive Investment Outlook

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Investment Outlook

August 2019

Taking a Deep Dive

NZ Equities Australian Equities Global Equities

BUY Kathmandu BUY Aristocrat BUY Amazon,

Mainfreight, Metlifecare, Lend Lease, QBE Insurance, Mastercard, Unitedhealth

Z Energy South32 Group, Walmart

- Page 21 -Page 24 -Page 27

Investment Outlook August 2019

Jarden

Overview

August 2019 Interest rates have dived to extremely low depths as economic growth indicators

turned down due to trade concerns and tensions between Iran and the US and its

allies. Globally central banks have reacted to this by taking a more stimulative stance,

including lowering interest rates. The interest rate falls have caused investors to flock

to dividend yield equities, resulting in significant share price appreciation. This has

been particularly apparent in New Zealand, which has a high proportion of dividend

yield stocks. With dividend yield equities doing so well we have provided readers with

an overview of the New Zealand electricity sector, which has a very high proportion of

dividend yield equities and some interesting longer term dynamics.

Looking forward, we see early signs that economic growth is starting to improve

which suggests that interest rates are likely to bottom out before rising modestly.

Probably the most significant risk to these “green shoots” is a deterioration in trade

negotiations between China and the US. As we go to press, President Donald Trump

has surprised us yet again by imposing a 10% tariff on the US$300 billion of goods

from China that are currently tariff free. The market reaction has been swift with the oil

price down nearly 8%, the gold price up US$32/ounce (reflecting the growing interest

in gold assets we review the outlook for gold and associated investment options), a

modest rise in the Japanese yen, and the US Treasury 10-year interest rate falling

under 1.7%. While this has clearly dented investor and business confidence and

makes it more likely that central banks will continue to reduce policy interest rates, we

retain our view that a broadly positive resolution will emerge from the current trade

negotiations. This reflects our expectation President Trump wants to be re-elected in

the November 2020 presidential election, in which case he will want to be able to

trumpet some success in the trade negotiations and avoid putting the US economy

into recession. Historically, no sitting US president has been re-elected when the US

economy is in recession.

We acknowledge that the current economic cycle is mature and the economy is

probably closer to a recession than it has been for many years. However, at this time

there is no definitive evidence of an economic recession in the foreseeable future.

Finally, we welcome two new advisers to the Jarden Wealth Management team, Greg

Main in Wellington and Anna Boland in Queenstown.

John Norling,

Director, Head of Wealth Research

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 2

Investment Outlook August 2019

Contents

Taking a Deep Dive .............................................................................................................................................................. 4

Asset Allocation ........................................................................................................................................................................ 8

Infratil CEO - Marko Bogoievski ................................................................................................................................... 11

Introducing Ted Tsui – Global Equity Strategist ............................................................................................... 13

Global Direct Equity Portfolio ........................................................................................................................................ 14

New Zealand Electricity Sector 101 .......................................................................................................................... 15

New Zealand Equities ........................................................................................................................................................ 21

Australian Equities ............................................................................................................................................................... 24

Global Equities ....................................................................................................................................................................... 27

New Zealand Debt Securities ...................................................................................................................................... 31

The Future of E-Payments .............................................................................................................................................. 32

Gold Rising .............................................................................................................................................................................. 34

Jarden in the Community - Cystic Fibrosis NZ .................................................................................................. 35

Compass by Jarden .......................................................................................................................................................... 36

Calendar ................................................................................................................................................................................... 37

Your Local Jarden Team ................................................................................................................................................. 38

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 3

Investment Outlook August 2019

Taking a

Deep Dive

Key Takeaways Bad News is Good News

Equity markets

Equity markets have continued to power ahead, particularly in high dividend yield

bounce hard on a

markets such as New Zealand and, to some degree, Australia. Over the past 6-9 months

rosier outlook

Purchasing Manager Indices (timely indicators of economic growth) have declined

Economic activity is globally suggesting economic growth has recently softened. This is a reflection of

likely to accelerate

increased uncertainty from the US-China trade dispute, numerous threats by the US to

after a lack lustre

impose tariffs, growing tensions in the Middle East involving Iran, and lesser issues such

March quarter

as Brexit and Italian budget and debt problems. From the US perspective, over three

The net result of a years of Federal Reserve (Fed) interest rate rises have probably also taken a toll. The

more positive

increased uncertainty has seen gains in safe-haven assets, such as gold (discussed on

outlook is higher

page 34), US government bonds and, to a modest degree, the Japanese yen. No doubt

interest rates

the dive in 10-year US government bond yields from 3.2% to 1.7% also reflects muted

The RBNZ’s bank inflation pressures and an expectation by bond investors that the Fed needs to lower its

capital review is

Funds Rate from its current 2.0-2.25% band. Other central banks, such as the Reserve

likely to result in

Bank of New Zealand (RBNZ) and the Reserve Bank of Australia (RBA), also face softer

higher lending rates

economic growth and subdued inflation, and have either cut interest rates or indicated

over time

an intention to do so. A common thread amongst central banks appears to be the desire

to avoid having their currencies appreciate. Hence, there is a domino effect when large

central banks, such as the Fed, cut interest rates.

While central bank actions to stimulate economic growth in the face of subdued inflation

appears logical, it shouldn’t be overlooked that extremely low interest rates limit the

responses available when a recession arrives and can produce unintended

consequences. These include the adverse impact on savers income resulting in

pressure to save more to achieve the same level of future income, pressure on investors

to take on more risk to maintain the same level of investment income, and downward

pressure on bank earnings as net interest margins compress. Bank profitability is

important in order to have a sound banking system.

18

16

Very Low Interest 14

Rates Drive Up the 12

Savings Rate 10

Source: Bloomberg

8

6

4

2

0

1962 1972 1982 1992 2001 2011

US 10 Year Interest Rate US Savings Rate

Historically, it has taken around a 5% interest rate reduction to resuscitate economic

growth from recession. With central bank official rates in developed economies being at

most 2.5%, or in most cases much less, the scope for this sort of stimulus is limited. The

next weapon in the arsenal is quantitative easing (QE), a policy which arguably has had

only moderate success in stimulating economic growth in the face of structural

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 4

Investment Outlook August 2019

challenges. However, it has successfully inflated asset prices. The lack of success is

exemplified by the Bank of Japan, which as a result of QE owns over US$5 trillion of

assets (mainly bonds, but also 4% of the Japanese equity market). Despite this, inflation

is only 0.7% and economic growth a poultry 1.1%. With monetary policy struggling to

have an impact, the next recession will almost certainly require Government’s to increase

spending to bring it to an end.

“There Is No Alternative”

When considering how much investors should allocate to equities numerous

commentators have concluded that “There Is No Alternative” (TINA). To date, apart from

bouts of short-lived equity price volatility, investors have enjoyed the benefits of taking

on greater risk in their investment portfolios. Investment income has been maintained or

increased and there have been capital gains to boot.

What happens if interest rates rise? Examining history, we observe that interest rate

moves tend to impact the prices of dividend yield equities (dividend yield equities are

those that pay a reliable and generally above average dividend yield).

10.5 5.0

Dividend Yield

4.5

Equity Prices 9.5

4.0

Benefit From Lower

8.5 3.5

Interest Rates, But

the Converse is Also 7.5

3.0

Percent %

Percent %

True 2.5

Source: Bloomberg 6.5

2.0

5.5 1.5

1.0

4.5

0.5

3.5 0.0

May 15 Nov 15 May 16 Nov 16 May 17 Nov 17 May 18 Nov 18

Spark Vector Contact Energy

Genesis Energy Mercury Energy Meridian Energy

Kiwi Property Precinct Property Goodman Property

Auckland Airport (RHS) 10 Yr Interest rate (RHS)

While lower interest rates result in falling dividend yields and higher equity prices, the

converse is also true.

So are interest rates likely to rise or fall over the next twelve months? The RBNZ has

reduced the Official Cash Rate to 1.0%. Current pricing in the overnight indexed swap

(OIS) market suggests that the RBNZ’s Official Cash Rate (OCR) will fall another 0.25%

over the next year and the US Fed Funds Rate will fall a further 0.75%. Following the

recent interest rate cuts, we think further larger falls are unlikely to materialise. We expect

that the risk of higher future inflation, caused by a tight labour market and importantly an

improving economy will see the large decline in US interest rates implied by the OIS

market unwind. Consequently, the balance of probability favours a moderate increase in

interest rates on longer term bonds, unless US/China trade relations deteriorate further.

As shown on the following page, indications of an improvement in economic growth

include a bottoming of composite Purchasing Manager Indices globally.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 5

Investment Outlook August 2019

Composite 59

Purchasing 58

Manager Indices 57

Indicate Green 56

55

Shoots

Source: Bloomberg 54

53

52

51

50

49

Jul 16 Jan 17 Jul 17 Jan 18 Jul 18 Jan 19 Jul 19

US UK Europe NZ Australia

With the New Zealand 10-year government bond interest rate at a historically large 0.5%

below the US 10-year government bond interest rate, we expect any rise in US interest

rates to push local interest rates up. Should this come to pass, some of the recent capital

gains experienced by dividend yield stocks are likely to be lost.

When Bad News is Bad News

In recent times, bad news has been received by equity investors as good news because

it increases the chances that the Fed will lower interest rates. However, if a recession was

to occur, then this bad news would in fact be bad news for equity markets. In this case,

the fall in interest rates would be associated with falling company profits and a decline in

equity valuation multiples as investors demand higher investment returns from risky

assets. Even companies with highly certain profits may suffer from reductions in earnings

and dividends during a recession.

140

120

Dividend Variability 100

Post Global

Financial Crisis 80

Source: Bloomberg

60

40

20

2007 2008 2009 2010 2011 2012

Spark Auckland Airport Vector Contact Kiwi Property Precinct Property Goodman Property

The good news is that while the probability of a recession has increased (based on the

difference between interest rates on long and short maturity bonds, the Federal Reserve

Bank of New York calculates the probability of a US recession as 33%) the three

indicators of a recession that we use are not flashing recession in unison (all three

indicators are needed to avoid the risk of a false reading). However, we concede that

they are all much closer to that point now. Looking at each indicator in turn:

1. The US 10-year interest rate is now below the 3-month interest rate, which is the

only indicator to suggest a recession is imminent.

2. The Fed Funds Rate is 2.1% which is slightly below the current neutral interest

rate estimate of 2.3%, which uses the mid-point of the Federal Reserve Bank of

New York’s range of the estimated neutral rate plus inflation as measured by the

Personal Consumption Expenditures Price Index.

3. The Conference Board US leading economic indicator is still up 1.6%.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 6

Investment Outlook August 2019

Key Questions for 2019 - Progress Report

In the February Investment Outlook, we posed a number of questions that were likely

to be important for the direction of markets in the medium-term. We give a progress

report below.

Can the oil price recover to US$70/barrel? In the June quarter the Brent oil price rose

to over US$74/barrel as supply reductions played out. It is now hovering around

US$66/barrel with extra US supply weighing on the price. However, should tensions

with Iran in the Strait of Houmas erupt, it could spike higher.

Will a recession occur in 2019? Despite softer economic growth so far in 2019, the

year is well advanced and no recession is in sight.

Could the New Zealand dollar fall below US$0.60? Despite the RBNZ reducing the

OCR, the New Zealand dollar continues to trade in a range of US$0.64-0.69.

Will the US/China trade dispute be resolved? Short term yes, long term uncertain.

Will financial markets experience the same elevated levels of uncertainty as in 2018?

To date, financial market uncertainty has been relatively subdued due to dovish

central banks and an easing of trade tensions between the US and China.

Will President Trump be impeached? Unlikely, although the Democrats continue to

search for an angle for impeachment.

Can inflation finally exceed 2%? Inflation remains subdued with New Zealand headline

inflation for the year to 30 June 2019 being 1.7%.

Will New Zealand house prices fall in value? Housing fundamentals remain soft, but

not enough to cause nationwide house prices to fall. The demise of the capital gains

tax proposal, robust inward migration and lower interest rates are expected to support

the housing market.

Will equity prices rise or fall? The 20%+ New Zealand equity market rise since 1

February has trounced our expectation of a modest rise. We did not expect interest

rates to fall and, therefore, didn’t anticipate the sharp appreciation of dividend yield

equities.

Forecasts

Economics As at 1 August 2019

Fiscal Balance % GDP GDP Growth % Inflation % 3 month Libor % 10 Year Government %

2018A 2019F 2020F 2018A 2019F 2020F 2018A 2019F 2020F Spot 3mth 12mth Spot 3mth 12mth

New Zealand 1.1 0.7 0.5 2.8 2.5 2.6 1.6 1.6 1.9 1.5 1.3 1.3 1.4 1.6 1.8

Australia -0.5 -0.2 0.3 3.0 2.0 2.5 1.9 1.6 2.0 1.0 0.8 0.8 1.2 1.3 1.5

US -4.1 -4.4 -4.7 2.9 2.5 1.9 2.4 1.8 2.1 2.3 2.1 2.3 1.9 2.2 2.4

Japan -3.8 -3.5 -3.0 0.7 0.7 0.6 1.0 0.7 1.0 -0.1 0.0 0.0 -0.1 -0.1 0.0

Europe -0.7 -1.0 -1.0 1.8 1.2 1.4 1.7 1.3 1.4 -0.4 -0.4 -0.4 -0.5 -0.3 0.0

United Kingdom -1.5 -1.5 -1.7 1.4 1.2 1.3 2.5 1.9 2.0 0.8 0.8 0.9 0.6 1.0 1.2

China -4.1 -4.4 -4.3 6.6 6.2 6.0 2.1 2.4 2.3 2.6 2.6 2.5 3.2 3.0 2.8

Source: Jarden, Bloomberg

NZ and Australia fiscal balance is 30 June

NZ is the 90-day bank bill yield

Equities and Commodities Foreign Exchange

Spot 12 mth forecast Past Month Past Year USD NZD

Australia – ASX 200 6,789 6,500 - 7,200 2.1% 8.2% Spot 12mth Spot 12mth

Emerging Markets 1,025 1,060 - 1,180 -3.7% -5.7% NZD 0.66 0.68 - -

Europe – Stoxx 600 388 390 - 430 0.0% -0.6% AUD 0.68 0.72 0.96 0.95

Japan - Topix 1,567 1,540 - 1,700 0.9% -11.4% EUR 1.11 1.15 0.59 0.59

New Zealand – NZX 10,861 10,500 - 11,600 4.1% 22.6% JPY 107.4 107.0 70.4 72.8

UK – FTSE 100 7,585 7,400 - 8,100 1.2% -0.9% GBP 1.21 1.28 0.54 0.53

US – S&P 500 2,954 2,970 - 3,280 -0.4% 5.0% CNY 6.90 6.95 4.52 4.73

Oil Brent USD/bbl 61 60 - 66 -7.0% -16.4% Source: Jarden, Bloomberg, IRESS

Gold USD/Oz 1,445 1,340 - 1,490 4.4% 18.9%

Source: Jarden, Bloomberg

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 7

Investment Outlook August 2019

Asset

Allocation

Key Takeaways Global Equities

Given risks and Over the next twelve months or so, we see reasonable support for global equities. We

the late stage of expect company earnings to improve somewhat in the near-term as global economic

the investment growth tentatively rises toward the end of 2019. Short-term interest rates probably have a

cycle, we are little further to decline before stabilising. Gradually rising longer-term interest rates are

circumspect on unlikely to be much of a headwind for equities if earnings are increasing.

equities.

Low interest Global equity valuation ratios, such as the price-to-earnings (PE) ratio, have risen this year

provide some and are now slightly above their longer-term historical average. However, they are not

support for NZ extreme and don’t give too much guidance on the near-term direction of equity markets.

equity prices. Low interest rates, improvements in earnings and easing economic uncertainties are likely

Flatter yields to be more influential on the direction of equity prices in the near-term.

reduce our

appetite for NZ

debt securities. 26

24

22

Global Price-to- Long-term average PE ratio

PE Ratio x

20

Earnings Ratio 18

Source: Bloomberg, Jarden

16

14

12

10

8

2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Balancing the positive near-term signs we see for global equities, we are more cautious on

Slight caution on a longer horizon. This investment cycle has been a long one and vulnerabilities, such as

equities as reward-to- elevated debt levels, are building. We are aware that we are closer to the end of the

risk trade-off investment cycle than the beginning. For this reason, the reward-to-risk trade-off has

diminished somewhat diminished somewhat.

New Zealand Equities

New Zealand equities have been star performers in recent times. New Zealand dividend

yield equities have benefited from the global search for yield in a low and falling interest

rate environment. As a result, valuations have been driven up to very high levels, both

compared to history and relative to the rest of the world. As the following chart suggests,

higher New Zealand valuations are potentially justified given where interest rates have

tracked so far. While low interest rates are supportive we observe the limited number of

observations at current low interest rates (refer to graph on following page), which leaves

us less convinced regarding what the data is currently showing. Regardless of this, the

New Zealand dividend current high valuation ratios are most likely only sustainable if interest rates do not rise

yield equities will be much from current levels. Given how far and fast valuations have risen, it’s possible that

sensitive to even New Zealand’s dividend yield equities will be sensitive to even modest lifts in 10-year

modest lifts in 10-year interest rates. This will be a headwind for their total returns, even accounting for the

interest rates dividend income that is derived from them.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 8

Investment Outlook August 2019

28.0

26.0

Price-to-earnings ratio

Low Interest Rates 24.0

Support High NZ 22.0

20.0

Equity PE Ratios

18.0

Source: Bloomberg, Jarden

16.0 As at 31 Jul

14.0

12.0

10.0

8.0

1.0 2.0 3.0 4.0 5.0 6.0 7.0

10-Year Bond Yield

New Zealand Property

Another area that has benefited from low interest rates to a significant degree is New

Zealand listed property, which like a good proportion of New Zealand equities, provides

sustainably high dividends. Consequently, valuations in the sector have also risen

significantly above historical averages as capitalisation rates have followed interest rates

down.

New Zealand property valuations are likely pricing in the expectation that the interest rate

Higher interest rates on a 10-year government bond will remain at its current low level for a considerable period

may cause New into the future. If, as we expect, longer-term interest rates gradually rise as the year

Zealand listed progresses, then listed property equity prices will likely stutter. High income yields on

property to stutter property equities may not be enough to prevent sector underperformance compared to

the rest of the market.

New Zealand Cash and Fixed Interest

The chart below illustrates how far interest rates have declined over the past three months

to the end of July, particularly for the longer terms to maturity and lower credit quality debt

securities (BBB and BB rated securities). In combination with our expectation that longer

term interest rates will likely come up for air into the end of the year, the investment return

from cash (short-term securities) appears relatively more attractive. We acknowledge that

should investor confidence be dented, by events such as a deterioration in US/China trade

negotiations or an increase in tensions between the US and Iran, then both long and short

term interest rates could dive further in the interim.

5.0%

A Precipitous Fall

4.5%

in Longer Term

Interest Rates 4.0%

-1.0%

Source: Bloomberg, Jarden

3.5%

3.0%

-0.6%

2.5%

2.0%

1.5%

0.3 1.0 2.0 3.0 4.0 5.0 6.0

BBB 3 Months Ago BBB Now BB 3 Months Ago BB Now

As a result of lower interest rates and the outlook, we modestly reduce the allocation to

New Zealand debt securities, and modestly increase the allocation to cash.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 9

Investment Outlook August 2019

Asset Allocation

August 2019

Based on the Asset Allocation discussion on pages 8-9, we have reduced the exposure to NZ Debt Securities by 1% and

increased Cash by 1%. The Strategic Asset Allocation represents the average weighting over the long term (circa ten

years or an entire economic cycle). The Tactical Asset Allocation represents a deviation from the Strategic Asset

Allocation to take advantage of expected changes in asset class returns over the short term (say 6 months plus). We have

retained the overweight exposure to Global Equities and underweight exposure to NZ Equities and Property.

% Strategic Allocation Tactical Deviation %

Income Assets Growth Assets

Conservative

Cash 15 +1

NZ Debt Securities 55 +1

Property 4 -2

NZ Equities 8 -3

Australian Equities 3

Global Equities 12 +3

Alternative Strategies 3

Balanced/Conservative

Cash 11 +1

NZ Debt Securities 44 +1

Property 5 -2

-3

NZ Equities 12

Australian Equities 6

+3

Global Equities 18

Alternative Strategies 4

Balanced

Cash 8 +1

NZ Debt Securities 32 +1

Property 6 -2

-3

NZ Equities 16

Australian Equities 8

+3

Global Equities 25

Alternative Strategies 5

Balanced/Aggressive

Cash 7 +1

NZ Debt Securities 23 +1

Property 6 -2

NZ Equities 20 -3

Australian Equities 10

Global Equities 29 +3

Alternative Strategies 5

Aggressive

Cash 5 +1

NZ Debt Securities 15 +1

Property 6 -2

NZ Equities 23 -3

Australian Equities 12

Global Equities 34 +3

Alternative Strategies 5

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 10Investment Outlook August 2019

Infratil CEO

Marko Bogoievski

Marko wears many hats, one of which is as the Chief Executive Officer (CEO) of Infratil. His

other key role is as CEO of H.R.L Morrison & Co, the manager of Infratil. Before taking up

these roles Marko had a significant breadth of business experience.

The Early Years

As a boy Marko grew up in the Hutt Valley suburb of Petone, attending local schools,

playing football, and supporting the Petone Rugby Club. Somewhat unusually Marko

skipped his last year of secondary school, instead opting to attend Victoria University

where he graduated with a BCA in accounting and economics. Fresh out of university he

joined the Price Waterhouse audit team. Back then, the “Big-8” offered employees

attractive options to gain experience offshore. This saw him hit the streets of New York at

Marko Bogoievski 23, joining Price Waterhouse’s Transaction Services team, which involved the

comprehensive appraisal of businesses on behalf of prospective buyers. The experience

of living in New York had a significant impact on Marko, and in his words, caused him to

Key Takeaways “harden up”. Gaining experience in new areas appear to be a hallmark of Marko’s career.

Life in New York Consequently, after a couple of years at Price Waterhouse he took up a role as financial

and a Harvard MBA controller with one of their clients, Elders IXL subsidiary, Elders Finance US. There he learnt

were key factors first-hand about trading and merchant banking. Problems at Elders IXL saw this job come

shaping a young to an end and what followed was two years at the Harvard Graduate School of Business

man from Petone, where he earned an MBA. The highly competitive environment of Harvard and the need to

New Zealand work fast (three real-world business case studies to prepare each night for the following

Marko has overseen day) and be thorough while reaching robust conclusions (the key person associated with

a period of the case study was often in attendance at the class discussion) has been a great asset.

significant growth

and investment Attracted by the leadership development program offered by Lion Nathan, Marko returned

performance at to New Zealand in 1994 with his American wife and two boys to take up a role as sales

Infratil and Morrison director in the NZ Wines and Spirits business. A few years later, Marko was back in the US

& Co working for Dispatch Management Services Corp, a start-up company, which ultimately

Within Infratil’s listed on the NASDAQ stock exchange. The aim of the company was to provide a same-

portfolio, Marko day delivery service through the amalgamation of a large number of courier companies.

believes Longroad Unfortunately to make this concept work required computer and communications

and Canberra Data technology, which wasn’t cheap or reliable back then. Over 20 years later, Fedex, Amazon

Centres offer near- and Wal-Mart are still working on how to provide consistent same day delivery services to

term valuation their customers.

upside

H.R.L. Morrison & Co and Infratil

What followed was eight years as Chief Financial Officer of Telecom Corporation of NZ,

which subsequently became Spark. Marko thoroughly enjoyed the people, the diversity of

the role and working through the significant strategic issues faced by Telecom at that time.

At the end of his tenure, Marko was approached by the late Lloyd Morrison to join H.R.L

Morrison & Co, the manager of Infratil. At that time Morrison & Co had less than twenty staff

and their main client was Infratil. Rolling forward twelve years Morrison & Co has 130 staff,

approximately $15 billion of funds under management (of which IFT is around one third)

across a number of clients and offices in five countries including New Zealand. The

advantage for Infratil of Morrison’ & Co’s growth relates to the greater number of

investment professionals that can be used to identify opportunities for new investment.

This increases the reach of the organisation across the globe, sectors and investment

themes that Morrison & Co specialises in. The management style engendered by Marko is

a collaborative environment, where employees are given a lot of autonomy and

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 11Investment Outlook August 2019

encouraged to allow investment ideas to be developed in a fluid way rather than by

following a rigid process.

As with many successful people, Marko works hard to achieve a balance between the time

dedicated to his work and his family, which includes his wife, two sons and parents who

continue to live in the family home in Petone.

Invest in ideas that Morrison & Co’s mantra is to “Invest in Ideas that Matter”, a concept that has been applied

matter to Infratil. Recently, this has seen Infratil reset its investment portfolio to be focused on

renewable energy, data, and communications infrastructure. This has seen divestment

activity around NZ Bus, ANU student accommodation, and Perth Energy, and the

acquisition of 49.9% of Vodafone New Zealand for $1.029 billion (representing around

20% of Infratil’s assets) and Canberra Data Centres’ (CDC) acquisition of the Eastern Creek

data centre campus for around A$100 million. In Marko’s eyes IFT is an “absolute return”

fund, which provides steady returns over time while paying a regular distribution to

investors. Over the years it has been one of the best performers in the NZ equity market

producing a compound total shareholder return of approximately 17%pa over the past 20

years.

So which of Infratil’s assets is Marko most excited about? Time will tell with Vodafone; in

the near term CDC and the dark horse in the stable, Longroad, are likely to offer the

biggest performance gains.

Canberra Data Centre (CDC)

Inside a Data A data centre is a large group of networked computer servers typically used by

Centre organisations for the remote storage, processing or distribution of large amounts of

electronic data. Key attributes of a data centre are:

1. Data integrity – Systems should exist to ensure that data is stored and retrieved

exactly as it was received from customers.

2. Availability – The data needs to be available when it is required, so absolute

reliability is key. Therefore electricity supply, communication connections and air

conditioning must be fool proof.

3. Security – Measures need to be put in place to prevent unauthorised access to and

alteration of information held on the data centre’s computer servers.

Source: Infratil 4. Scalability – Data centres need to be able to scale up to meet the changing needs

of customers, without interrupting their current business operations.

5. Capacity – Data centres need to be able to efficiently store and process large and

rapidly growing data volumes. Data centre capacity is measured in megawatts

(MW).

CDC (IFT ownership 48%) currently has 60MW at two sites in Canberra with another

25MW to be completed by the end of the year. At Eastern Creek in Sydney there is 7MW

with the potential to grow up to 120MW. While the contracts at Canberra are generally for

3-4 years with options to extend, the Sydney contracts are for 15 years with revenue

locked in at the rate of inflation.

Longroad Wind Longroad

Turbines Longroad (IFT ownership 40%) is a developer of utility-scale wind and solar electricity

generation projects in North America, which it then on-sells to long term investors such as

pension and insurance funds. Longroad is developing multiple projects of which it has

sold two projects totalling 553MW. In 2019, Longroad is developing four projects totalling

over 800MW. Many investors will also get Longroad to provide long-term management

services for the assets after a sale. Longroad currently services 1,732 MW of electricity

capacity. It is estimated that north America requires 100,000MW of new renewable

Source: Infratil electricity generation capacity by 2030.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 12Investment Outlook August 2019

Introducing Ted Tsui -

Global Equity Strategist

Joining Jarden in early 2018 Ted brings with him a wealth of experience from his time

in Asia working in a range of equity and fixed income research and investment

management positions.

Although Ted was born in Shanghai, he spent most of his youth in Singapore and

completed his tertiary education in Hong Kong. Singapore, in particular, has shaped

his careful and disciplined way of researching and analysing companies. Singapore

maintains an army of 1.2 million soldiers, with all male Singaporean citizens being

required to serve a period of compulsory military service. Consequently, Ted served

Ted Tsui

two and a half years on a full-time basis in the Singapore Armed Forces, where he

learned the importance of paying attention to details in addition to a standard set of

basic military and survival skills. He was discharged with a unit best soldier award in a

Key Takeaways

coastal defence brigade in 2002.

Robotics engineer turned

investment analyst with a On leaving the military, Ted returned to Hong Kong and commenced university.

CFA designation Spurred on by an interest in robotics and artificial intelligence, Ted completed a

A prudent, bottom-up, rigorous bachelor degree with honours in automation and computer-aided

fundamental and engineering. Right before the 2007 global financial crisis, Ted embarked on a

methodological significant career change focusing his attention on the investment industry. This shift

investment specialist came with a decision to undertake a further three years of part-time study, which saw

A youthful look belies him achieve the globally recognised Chartered Financial Analyst (CFA) designation.

years of extensive Ted’s early years in the investment industry saw him undertake a number of roles, in

knowledge and equity and credit research, at various firms in Hong Kong. His professional experience

experience includes working for a Geneva-based family office, Sumitomo Mitsui Banking

Corporation and the Asian arm of a European asset management firm, La Francaise

Group. He found his niche as a fundamental-driven and bottom-up investment

analyst in managing more than USD 500 million of institutional and high-net-worth

client assets. His years of prudent investment experience were built with interviewing

top company officials, visiting factories, attending investment conferences, cross-

checking ground information with industry experts, scrutinising company disclosures

and building complex financial models to draw up various company business

scenarios. Analysing companies fascinates Ted, giving him knowledge of what

particular companies do, which in turn generates a better insight into how the world

operates behind the scenes. Ted, a self-described “infomaniac”, enjoys researching

anything from global macroeconomic data to prices at the Albany Pak’nSave. This

allows him to form a longer-term and deeper understanding of the country and the

industry in question.

At Jarden, Ted continues to use the bottom-up and analytical approach he honed in

Asia. There is no doubt that Ted’s youthful looks belie his years of experience and

extensive knowledge. The evidence of this can be seen in the impressive

performance of the Jarden Global Direct Equity model portfolio, which relies heavily

on Ted’s expertise and is explained by Ted on the following page.

Away from the office Ted enjoys do-it-yourself (DIY) projects at his North Shore home,

cycling and exploring the New Zealand countryside with his wife.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 13Investment Outlook August 2019

Global Direct Equity

Portfolio

Key Takeaways The Global Direct Equity Portfolio commenced on 30 June 2018, with the aim of

providing investors with a model portfolio of enduring international businesses. On

Direct ownership of

average, the portfolio targets outperformance of the MSCI All-Country World Index

enduring

(ACWI) by 2% per annum. In its first year, the portfolio generated a total return of 9.4%

international

businesses in New Zealand dollars (NZD), which was 2.1% more than a passive ACWI portfolio.

A concentrated but The success of the portfolio, in a highly volatile equity market environment, was largely

well diversified due to the favorable results of our bottom-up stock selection process. When selecting

portfolio of 14-16 a company for the portfolio, detailed analysis of comparable companies is conducted

companies in order to identify those that offer superior business performance. A heavy emphasis

Strict risk is placed on the company’s track record to generate a sustainable level of free cash

management flow over past economic cycles to ensure that it can indeed create economic value for

controls with investors. At the same time, a discounted cash flow valuation is conducted to estimate

Investment a reasonable value range for the business.

Committee

oversight In addition, it would be impossible to deliver good investment performance without

observing various risk management rules. The portfolio is highly concentrated,

comprising 14 to 16 companies (domiciled outside Australasia) from various sectors

and geographic regions. To manage portfolio risk, each company represents between

4% and 10% of the portfolio. At the same time, the aggregate exposure to each sector

Disney’s Key Businesses

and geographic region is allowed to vary from the proportions in the ACWI by no more

than 14%. The portfolio is constantly monitored and reviewed monthly by an

investment committee, which consists of Jarden investment professionals across a

range of disciplines with many decades of experience. This also ensures that the

portfolio’s objectives and risk management restrictions are strictly observed. In line

with the portfolio’s aim to adopt a longer-term investment view and keep transaction

costs down, a 12-month rolling turnover budget of 50% is observed.

Walt Disney (DIS)

Walt Disney (Disney) is one of the better-performing stocks in the portfolio (annual

NZD return of 36.6%) and serves as a good illustration of the characteristics we look for

when selecting a company for the portfolio.

Although investors may perceive Disney as a company focused only on cartoons and

theme parks, it has evolved tremendously in recent years to become one of the three

largest media companies in the world. In addition to the traditional cartoon and theme

park businesses, Disney has expanded horizontally and vertically into television, film

and video-on-demand businesses (i.e. Hulu and Disney+). Through owning a

diversified media distribution network and a portfolio of high-quality content beyond

cartoons, Disney’s ability to raise prices and generate a growing stream of free cash

flow over the past economic cycle has been nothing less than spectacular.

When we added Disney to the portfolio, we were anticipating the creation of an even

larger high-quality content portfolio after the acquisition of 21st Century Fox. With the

ultimate launch of its own video streaming services in November this year, Disney will

further monetise their enlarged content portfolio in multiple ways and deliver

unparalleled synergies that are nearly impossible to replicate by its competitors.

Disney has executed its strategy well and is on its way to becoming the largest and

most competitive media company in the world. We believe Disney’s competitive

advantage will continue to stand the test of time and deliver superior returns to

investors.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 14Investment Outlook August 2019

New Zealand Electricity

Sector 101

Key Takeaways In New Zealand, a large number of sectors are represented by a single listed company.

Instantaneous However, there are seven sectors comprising three or more companies. Over the

electricity coming quarters we plan to provide an overview of each of these sectors and the

production and common factors that affect the companies within each sector. We decided to start with

consumption the largest sector being the electricity sector which accounts for 19% of the New

creates interesting Zealand equity market’s total market capitalisation. Adding to the sectors intrigue is the

dynamics recent strong investment returns from long-term interest rates collapsing and changing

Construction and dynamics brought by climate change resulting in a push to reduce carbon dioxide

operating costs, emissions.

asset life, and

capacity utilisation Market Forecast FY20 Dividend Reported

vary materially Investment Return Carbon

Company Ticker Capitalisation Yield

between generation Emissions

($ billion) (CO2e t)

types Net Gross 1 Year 5 Year (pa)

Electricity is Contact Energy CEN 5.7 4.9% 6.2% 45.5% 17.1% 1,186,122

expected to Genesis Energy GNE 3.5 5.1% 6.5% 45.6% 24.7% 1,480,180

increasingly Meridian Energy MEL 12.4 4.1% 5.0% 60.3% 48.1% 3,588

displace fossil fuels. Mercury NZ MCY 6.5 3.3% 4.0% 44.4% 23.5% 346,698

The sector could be TILT Renewables TLT 1.2 0.4% 0.4% 34.6% n/a n/a

upset by the smelter Trustpower TPW 2.4 4.5% 6.2% 46.3% 19.0% n/a

closure or lower Vector VCT 3.8 4.3% 6.0% 23.6% 15.7% 399,015

electricity prices Source: Bloomberg, Jarden, company reports

Electricity is an interesting commodity in that it is consumed immediately after it is

generated. This creates a dynamic where electricity generators have to produce

electricity to meet demand, which fluctuates significantly during the day (with heavy

demand in the early morning and evenings, and limited demand overnight) and at

different times of the year (higher demand in the winter than in the summer). As it is

undesirable for the lights to go out, different forms of generation have to be brought in

and out of production at relatively short notice to meet demand.

The electricity price is determined on a half-hourly basis by electricity generators

submitting offers into the market and large electricity consumers and retailers

(purchasers) submitting bids to buy electricity. The electricity market is operated by the

Electricity Authority.

The electricity sector can be broken down into five distinct parts, which fit together as

shown in the diagram below.

New Zealand’s

Electricity System

Source: Electricity Authority

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 15Investment Outlook August 2019

1. Electricity Generation

Electricity is generated from four energy sources – hydro, wind, geothermal, and

thermal (by burning gas or coal). As can be seen from the charts below, hydro

generation dominates the New Zealand electricity market with production coming

predominantly from four generators.

Hydro Meridian

5% 3% 11%

New Zealand’s Contact

Geothermal 8% 31%

Electricity Sector 16%

Genesis

Broken Down by Thermal 13%

59%

Generation Type and 17%

Mercury

Generator Wind

16% 21% Trustpower

Source: Electricity Authority

Other Other

Hydro

Hydro electricity is generated from water flowing through a penstock and turning a

turbine. While there is some potential to store water behind a dam for future use, water

storage in New Zealand is relatively limited. The maximum storage in any year equates

to 10% of total electricity production. Consequently, most hydro generation is “run of

river”, which means that the electricity is generated as the water naturally flows down

the river. This forms base load generation, while water stored behind dams can be

used to meet peaks in demand. Unfortunately, during dry years there is less water

Construction Cost: high

flowing down rivers to generate electricity and, therefore, less hydro-electricity

Life: 100 years + generation. The capital cost of building hydro electricity generation is very high as

Capacity utilisation: 65% dams are very expensive, although the key factor preventing further hydro

development is the difficulty in getting resource consent as much as construction

costs. Once built, hydro generation lasts a very long time (100 years plus) and the cost

of generating electricity is low as water costs nothing. Consequently, when there is a lot

of water available wholesale electricity prices are low. However, when there is a lack of

water, electricity prices rise reflecting the cost of having to generate electricity from

more expensive energy sources.

Wind

Wind generation is relatively expensive to build (around $2 million per megawatt), but

not as expensive as building a dam. Once built, the cost of generating electricity is low

as wind doesn’t cost anything. However, the maintenance costs on wind turbines are

higher as the variability of wind speeds and direction is tough on the turbines. This also

means that they don’t last as long as hydro dams, with a typical life of 25-30 years.

Based on the current costs of constructing and operating wind generation, it is the

most economic form of new electricity generation and thus sets the long-run cost of

Construction cost: $2 electricity in New Zealand used to value electricity generation assets. A key issue

million/ megawatt associated with wind farms is that they only generate electricity when the wind is

Life: 25-30 years blowing. Hence, wind farms have to be located in areas that have reliably consistent

Capacity Utilisation: 40% wind conditions. Due to the day-to-day variability of wind in New Zealand, wind farms

typically operate at 40% capacity utilisation.

Geothermal

Geothermal electricity uses geothermal steam as a heat source to turn a turbine.

Building a geothermal generation plant is relatively expensive, involving the drilling of a

number of geothermal wells and connecting them up to a generation plant. While the

geothermal steam is free, it is hard on the plant, which means maintenance cost are

high. Geothermal generation has the advantage that the steam comes out of the

ground consistently and is unaffected by weather conditions. It thus represents

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 16Investment Outlook August 2019

Construction cost: $4 baseload generation. It is worth noting that geothermal generation results in

million/ megawatt greenhouse gas emissions that are released as the geothermal fluid is extracted from

Life: 30 years the reservoir.

Capacity Utilisation: 98%

Thermal

Finally, there is thermal generation, which is typically fuelled through burning gas or

coal. The construction costs of a thermal generation plant are relatively low. However,

the cost of fuel, gas or coal, is high. The advantage of a thermal plant is that fuel

sources can be stored and used as required. Consequently, thermal electricity

generation is often used to meet peaks in electricity demand or when other types of

generation are not producing electricity. Burning coal and gas creates a significant

amount of carbon dioxide. Hence, as the cost of producing carbon dioxide rises so

Construction cost: $1-1.5 does the cost of producing electricity from thermal generation. Currently the carbon

million/ megawatt

cost is capped at $25/t. However, it could easily rise to $50/t or much higher based on

Life: 30 years various academic studies.

Capacity Utilisation: 90%

Solar

Apart from a modest number of solar panels on roofs the amount of solar generation in

New Zealand is very small. The largest solar electricity plant is currently being built by

New Zealand Refining in Whangarei (capacity 26MW, covering 31 hectares). This

development is expected to have a very low capacity utilisation of only 15%.

2. Electricity Transmission

Once the electricity is generated it has to be transported from the point of generation to

the point of consumption. The first part of this transportation process is undertaken by

The high voltage the high voltage network, otherwise known as the National Grid (Grid), which is owned

network (National Grid) and operated by Transpower (100% government owned). The Grid is capable of

is owned and operated transporting electricity from one end of New Zealand to the other. As the Grid is a

by Transpower monopoly the amount that it can earn from transporting electricity is regulated. The

regulation is overseen by the Commerce Commission and pricing is reset every five

years. The flow of electricity through the Grid is managed by the Independent System

Operator which is owned by Transpower, but operates independently.

3. Electricity Distribution

Once the electricity exits the Grid it is transported to its final destination for

Low voltage networks consumption via low voltage networks. The low voltage networks are owned by lines

are owned by lines companies of which there are 30 in New Zealand. As the lines companies have

companies of which monopolies in the areas serviced by their networks, the amount they can earn is

there are 30 regulated. As with Transpower, the regulation is overseen by the Commerce

Commission and pricing is reset every five years. The largest lines company is Vector

(VCT), which serves Auckland. VCT also owns an electricity metering business.

Metering is not a monopoly, which means that VCT can set its own prices for providing

metering services.

4. Electricity Retailers

Electricity consumers buy electricity off electricity retailers who buy the electricity off

electricity generators. In New Zealand, it is common for companies to both generate

and sell retail electricity. However, there are an increasing number of niche retail

electricity companies which purchase electricity off the generators to supply their

customers. The electricity price is extremely volatile, often rising or falling by 20% or

more on a weekly basis.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 17Investment Outlook August 2019

100

Weekly Electricity Price Change (%)

Electricity – The 80

Most Volatile

60

Commodity Known

to Man 40

Source: Bloomberg

20

0

-20

-40

-60

Jul 18 Sep 18 Nov 18 Jan 19 Mar 19 May 19 Jul 19

Typically, electricity retailers sell electricity to households based on a fixed tariff, which

includes the electricity generation, transmission and distribution costs, plus a profit

margin. The electricity retailer, therefore, absorbs the electricity price fluctuations.

When electricity prices are low they make large profits and when electricity prices are

high they make losses, which averages out over time. Furthermore, as most retailers are

also generators, during times of high prices the generation division does well at the

expense of the retailing division, and the opposite occurs when electricity prices are

low. Many of the smaller electricity companies provide electricity at prices that reflect

the volatile wholesale price. In the long term, their customers should make savings.

However, their electricity bills will fluctuate significantly from month-to-month, not only

due to the amount of electricity used, but also due to price of electricity.

5. Consumers

Electricity consumers range from households, small-to-medium sized industrial and

commercial users, through to large users such as the Kawerau pulp and paper mill,

NZAS consumes 13% of Glenbrook steel mill and New Zealand’s Aluminium Smelter (NZAS - which consumes

the country’s electricity 13% of the country’s electricity production annually). For some time now, growth in

annually electricity demand has been around 0.5%pa. Domestic demand is driven by the

growth in the number of households. However, while there are more households, the

use of more efficient appliances (e.g. heat pumps and LED light bulbs) results in a

gradual fall in electricity usage per household. Growth in industrial and commercial

demand is influenced by similar factors.

Being a key commodity in today’s modern world the electricity price is always a

potential target for politicians if prices rise too quickly. This has seen the recent

publication of the 2018-2019 Electricity Price Review.

The Energy of the Future

Looking forward there is a major drive towards reducing carbon emissions in an effort

to keep the level of global warming to no more than 1.5-2.0°C above pre-industrial

Electricity demand levels by 2050. As a result, renewable electricity demand growth is likely to increase

growth is expected to from the current 0.5%pa to around 2.0%pa over the coming decades. It is expected that

increase from the electricity generated by renewable sources (wind and geothermal) will displace fossil

current 0.5%pa to fuels both in industrial processes (e.g. milk powder driers) and transport (vehicles). The

around 2.0%pa extent of the extra generation capacity needed in New Zealand will be partially

impacted by whether NZAS continues to operate its smelter at Bluff. At this stage, there

is no imminent sign that they may close down the smelter having just re-energised their

fourth pot line. Its current supply contract with Meridian Energy expires in 2024. At this

time they may decide not to renew their contract and shut the smelter down. We

expect negotiations on a potential new contract to commence in 2022-2023.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 18Investment Outlook August 2019

While the majority of the new generation is expected to be from renewable sources,

there is always likely to be a small amount needed from thermal electricity generation

in New Zealand to ensure continuity of supply in extreme climatic conditions

Electricity Sector Outlook

The electricity sector faces a dynamic outlook driven by a step up in electricity demand

and the construction of new generation following an extended period of no new

development. In addition, there are two events that could have a material impact on the

electricity price and, thus, the value of electricity generation assets. They are the

potential closure of the NZAS’s Tiwai Point smelter and potential change in the

economics of wind generation should cheap capital become freely available. The

availability of cheap capital is a real possibility on the back of low interest rates and the

low returns needed to satisfy foreign investors (e.g. sovereign wealth funds) looking to

invest in long-term stable assets such as electricity generation assets. Under this

scenario the real electricity price could reduce from our expected $80/MWh to

$60/MWh in the mid-2020s. While a lower electricity price would be negative for

electricity generation asset valuations, this would be offset to varying degrees through

the use of a lower capital cost.

Valuation Under Valuation Under

Company Target Company Ticker Share Price Target Price *

Scenario 1 ** Scenario 2 ***

Prices and Potential

Valuations Contact Energy CEN $7.92 $7.01 $6.02 $7.80

Source: Jarden Genesis Energy GNE $3.42 $2.17 $1.85 $1.92

Meridian Energy MEL $4.83 $3.22 $3.23 $4.32

Mercury NZ MCY $4.79 $3.47 $3.11 $3.92

TILT Renewables TLT $2.65 $2.34 n/a n/a

Trustpower TPW $7.59 $5.39 $4.72 $6.98

Vector VCT $3.86 $3.27 n/a n/a

* Base Case: 8.05% cost of capital, $80/MWh electricity price

** Scenario 1: Tiwai closes in January 2021, $80/MWh electricity price by 2027

*** Scenario 2: Low cost of capital (6.0%), $60/MWh electricity price by 2023

Sector Preferences

Contact Energy (CEN) We regard CEN as well positioned to be relatively safe from regulatory and electricity

supply/demand disruptions through its adoption of a cost-light, fast-follower retail

strategy. In addition, CEN has strong opportunities to participate in renewable

electricity growth and industrial electrification.

Mercury NZ (MCY) MCY has a fairly stable earnings path, the most natural competitive advantages, fewest

moving parts, and least negative exposures within the sector. Its predominately upper

North Island portfolio offers a degree of insulation from a potential NZAS exit in the

future. MCY is a 100% renewable generator, trading effectively in the wholesale market

and continues to be an excellent retail operator, despite the high level of competition.

TILT Renewables (TLT) TLT develops, owns and operates wind farms in Australia and New Zealand. It currently

has two sizeable projects (Dundonnell and Waverley) being developed. It also has

development options totalling around 2,700MW (with approvals) positioned for

eventual development. Furthermore, TLT has significant upside potential from the sell-

down of existing windfarms to third parties which are prepared to pay high prices and

accept low investment returns.

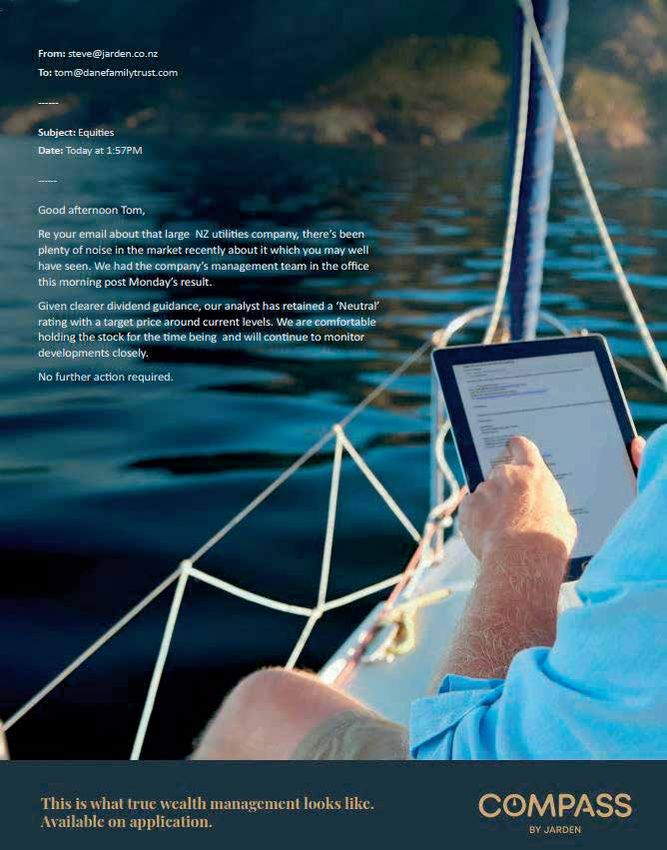

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 19From: steve@jarden.co.nz To: tom@danefamilytrust.com ------ Subject: Date: Today at 1:57PM ------ plenty of noise in the market recently about it which you may well this morning post Monday’s result. Given clearer dividend guidance, our analyst has retained a ‘Neutral’ developments closely. This is what true wealth management looks like. Available on application.

You can also read