The Delicate Transition - Investment Outlook February 2021 - Jarden

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

I

nves

tmentOut

look

Febr

uar

y2021

TheDelicat

e

Trans

iti

on

NZEqui

ti

es t

Ausrl

aia t

nEquies

i Gl

oba

lEqui

ti

es

BUYAFT, BUYAppen, BUYAl phabet

,

Hear

tl

and,Mai

nfr

eight Har

money,Rams

ay, BlackRock,Micr

on,

Pushpay,

ZEnergy Wi

set

ech Salesfor

ce,WaltDi

sney

Investment Outlook February 2021

Jarden

Overview

February 2021 A year on, the impact of the Covid-19 pandemic continues to dominate investors

thinking. The big difference between now and then is that mankind currently has

several vaccines available to prevent its spread, with more vaccines in the pipeline.

Consequently, we can now see a time, probably in a years’ time, when the restrictions

which currently impede people’s movements and activities can be lifted and life

without pandemic restrictions returns to the developed world. Developing countries

are likely to lag due to issues which impede achieving the desired levels of

vaccinations in their populations.

However, this positive outlook is not without risks. Close attention will be paid to the

progress of the vaccine’s deployment, particularly as the number of vaccinations

deployed ramps up. There have certainly been some early issues, which have been

put down as the typical teething problems that could be expected when starting such

a massive undertaking.

In response to the impact of measures taken to control Covid-19, central banks and

governments took unprecedented action to support the people and businesses

adversely affected. None more so than in the US where an additional US$0.9 trillion

support package was announced after Christmas and a further US$1.9 trillion support

package is in the process of being approved. Such massive stimulus has caused

investors to start thinking about when the US Federal Reserve (Fed) and other central

banks may start to reduce support. We explore the potential impact on financial

markets.

In this edition of the Investment Outlook, we profile Darrin Grafton, the CEO and co-

founder of travel booking company Serko. While Serko has a fascinating future in front

of it as it expands globally and rolls out new technology designed to improve people’s

travel experience, the adverse impact of Covid-19 on its revenue has been

extraordinary. Under Darrin’s leadership, Serko has met these challenges head on and

continues with its expansion plans.

As noted in our last edition Jarden has made a significant investment in establishing

an Australian business. A key part of the business is the establishment of a research

team under the leadership of the highly respected consumer analyst Ben Gilbert. We

take this opportunity to introduce Ben to you and discuss the new approach to

research that he and the extensive research team will bring to you. With the research

team now largely complete evidence of their work will become increasingly evident in

the coming months as they ramp up research coverage of the Australian equity

market.

John Norling,

Director, Head of Wealth Research

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 2

Investment Outlook February 2021

Contents

The Top Five Issues for 2021 ............................................................................................................................................... 4

Asset Allocation – Caution May Reign Until More Confidence Returns ....................................................... 8

Company CEO – Darrin Grafton, Serko ………………………………........................................................................................ 13

Introducing Ben Gilbert, Head of Australian Research ……………….…………………….................................................. 15

Top Stock Picks - 2021 ……………..………………….………………...…................................................................................................. 17

New Zealand Equity Metrics ............................................................................................................................................... 27

Australian Equity Metrics ...................................................................................................................................................... 28

Global Equity Metrics ............................................................................................................................................................. 29

Interest Rates – Coming to the End of the Road ….…..….……………............................................................................ 30

New Zealand Dollar – Well Supported …....................................................................................................................... 31

To Rebalance or Not to Rebalance? …........................................................................................................................... 33

Reminder – New Regulation on its Way ……................................................................................................................. 34

Importance of Being Independent ….............................................................................................................................. 35

Jarden in the Community – Surfing for Farmers .…………......................................................................................... 36

Calendar ....................................................................................................................................................................................... 37

Your Local Jarden Team ..................................................................................................................................................... 38

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 3

Investment Outlook February 2021

The Top Five Issues

for 2021

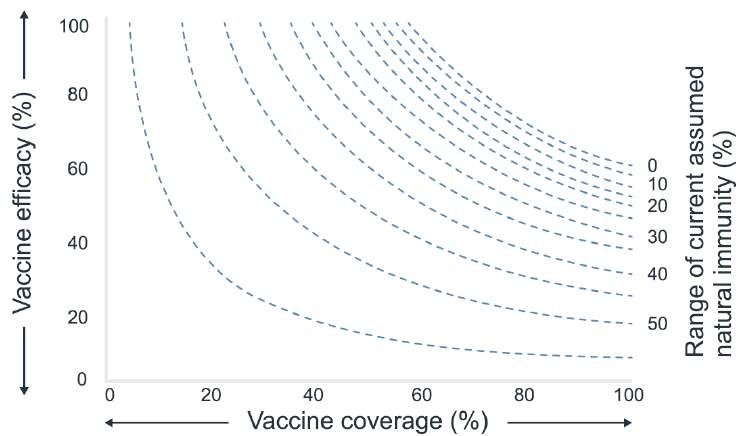

Key Takeaways The Vaccine Game Changer

• Investors expect While the Covid-19 pandemic was the worst thing to come out of 2020, the rapid

vaccines to put an development of effective vaccines was the biggest positive. Vaccines have provided a

end to the Covid-19 much more certain outlook for many companies. However, it will not be until herd immunity

disruption as herd is reached in early 2022 that large scale testing, mask wearing, and tracking will end, and

immunity is travel restrictions will be lifted allowing borders to reopen.

achieved

Herd immunity is achieved when a sufficient proportion of the population is simultaneously

• The risk of higher

immune to prevent sustained virus transmission. The chart below illustrates how different

inflation re-

levels of natural immunity in the population, the vaccine’s efficacy and the proportion of the

emerging is being

closely monitored population vaccinated achieves herd immunity. For example, herd immunity can be

achieved with 90% efficacy,10% natural immunity and 65% vaccine coverage. The one

• A gradual reduction

variable which affects herd immunity not shown below is how infectious the virus is. The

in excess liquidity

more infectious the virus, the greater the proportion of the population that needs to be

should see equity

vaccinated or have natural immunity. This is the concern with the new strains of Covid-19

valuation multiples

ease from the United Kingdom and South Africa. Compounding the problem is that it gets

increasingly difficult to vaccinate additional people as the proportion of the population

• Concerns about

vaccinated increases.

regulation

resurface

• House price growth

is expected to

dwindle as

underlying

fundamentals

soften

Achieving Herd

Immunity

Source: McKinsey

Things to watch which could undermine the achievement of herd immunity:

1. Significant supply chain or manufacturing delays.

2. Unexpected safety issues with the vaccines.

3. Shorter than anticipated duration of immunity after being vaccinated.

4. A slower than expected rollout of the vaccination. To date, where this has been the

A slower than expected

case it has been dismissed as teething issues.

vaccination rollout

5. Problems arising from each vaccines dosing protocol not being followed correctly.

6. Not getting a high enough proportion of the population vaccinated.

7. More infectious strains of the vaccine arising.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 4

Investment Outlook February 2021

Inflation and Employment

Despite recent subdued inflation globally, investors’ expectations of future inflation are

trending up. This has become apparent as investors have raised expectations of future US

government spending in the wake of the Democratic Party winning the US presidency and

gaining a slim majority in Congress. In the short-term, inflation is likely to rise modestly

because prices were so depressed amid pandemic lockdowns last year. Investors appear

to be expecting higher inflation to persist. Is this justified?

2.0

US Market 5-Year

Inflation 1.8

Expectation

Source: Bloomberg 1.6

%

1.4

1.2

1.0

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21

A possible omen of higher inflation is the combination of extremely loose monetary policy

and substantial increases in government spending. Once countries are sufficiently

vaccinated, with all that money sloshing around there is a risk people go on a spending

spree. Supply of goods and services may struggle to keep up, thus stoking higher inflation.

A bit of extra inflation The US Federal Reserve and other central banks have clearly indicated they would be

will keep central banks happy to see inflation moderately above 2% before they even consider tightening monetary

happy policies. They will almost certainly not react as prices rebound from depressed levels a year

ago.

There are counterforces at play, however. Unemployment in major developed economies is

likely to remain significantly higher than pre-pandemic rates and spare capacity will take

But relatively high time to dissipate. This will continue to dampen prices, particularly for services which

unemployment will typically drives inflation. Unemployment may well persist above pre-pandemic rates for a

prevent inflation from considerable period if a spending spree does not eventuate and firms cautiously re-employ

surging… workers. Secular forces such as e-commerce growth, outsourcing production to countries

with cheaper labour, and consumer preferences for experiences over goods keep inflation

low. Finally, future Inflation is influenced by past inflation, so subdued inflation will likely

persist.

… and central banks will There will also be a limit to central bank tolerance for higher inflation. Experience has shown

have a limit to how that once the inflation genie is well out of the bottle it is difficult to put it back in again.

much inflation they will Although central banks have committed to keeping policy interest rates at current low

tolerate levels for an extended period, possibly until 2023, they will start to ease back on asset

purchases much sooner. The Fed will likely start tapering its asset purchases by the end of

2021, with other central banks following in 2022.

Turning off the Liquidity Tap

There is a strong relationship between the expansion and contraction of equity valuation

multiples and the level of excess liquidity in the economy (defined as the difference

Equity valuation between the money supply growth and nominal economic growth). In recent times, the

multiples are affected amount of excess liquidity in the economy has been massive. Consequently, interest rates

by growth in excess have fallen even though governments have significantly increased spending, as the debt

money supply issued has been bought by central banks. These two factors have caused valuation

multiples to expand to very high levels and credit spreads on investment grade debt

securities have contracted to very low levels.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 5Investment Outlook February 2021

Currently there appears little risk of the liquidity tap being turned off now as inflation is low,

unemployment is high (therefore there is spare capacity in the economy) and central banks

There appears little risk have openly stated that they expect to err on the side of too much inflation rather than too

of the liquidity tap being little. This reflects the failure to meet inflation objectives over many years.

turned off now… However, this scenario has recently being called into question following the announcement

of an additional US$1.9 trillion of fiscal stimulus. This has seen 10-year US Treasury bond

interest rates rise 0.2% to 1.1% and some commentators forecast that the Fed will start

… although some tapering its bond buying program by September 2021. Tapering is expected before any

commentators expect change is made to the Fed Funds Rate. As noted above, whether this occurs will depend on

the Fed may start inflation being comfortably above 2% and unemployment falling. We expect that any

tapering its bond change in policy will be very gradual and well telegraphed to financial markets as the Fed

buying program by will not want to spook investors like it did in 2013. This being the case, any resulting

September 2021 valuation multiple contraction is likely to be largely offset by higher earnings growth. The

net result being lower returns being generated by equities, but not losses.

Regulation Emerges From its Den

Regulation has again risen up the list of investors’ concerns. This reflects numerous

concerns around the big technology companies and the election of Joe Biden as US

President combined with the Democrats gaining control of both houses of government.

There is a risk that the huge market shares gained by the big technology companies (for

example Google has 92% share of internet search in the US and 75% of US households

Technology companies’ have an Amazon Prime account) ends up working against them. While large market shares

large market shares are partially due to their popularity with consumers, there are real concerns surrounding

may work against them some of the technology companies’ actions. Some examples include failing to take an

adequate ‘duty of care’ for the content published on their sites and the pre-installation of

their applications on hardware they sell. It should be noted that the concerns do not just

come out of the US with regulatory action recently being taken in regions including the

European Union, United Kingdom and Australia. However, typically the probes which result

in new regulation take time to complete and generally result in incremental change. There

China’s large is greater concern in China where a probe has started into Alibaba’s activities and the

technology companies Peoples Bank of China has issued an order requiring Ant Group to return to its payment

appear to be making the services roots. It appears that the Chinese big tech companies are getting too big, too

Chinese government quickly and are gaining influence over the population, which is making the Chinese

nervous government nervous. While the outcomes are uncertain, history suggests that resulting

actions will be manageable for the companies affected and may slow growth somewhat,

but not stop it.

A Democrat government in the US poses risks for some US companies in the energy,

healthcare, technology, and communication services sectors. However, it is worth

remembering that the Democrats have a very large list of items they want to tackle. Top of

the list is to stop the Covid-19 pandemic followed by the implementation of as much of their

$1.9 trillion fiscal stimulus package as possible. Also high on their agenda is getting the US

back into the Paris Agreement on Climate Change and a focus on green energy. Over time

this will be a headwind for the oil and gas industry. Although to date the only change is to

no longer issue permits for fracking on government owned land. Other key issues include

reversing Donald Trump’s isolationist foreign policy, combating racism and undoing

Trumps’ migration policies. The healthcare sector is expected to see a cap on drug prices

and reduced health insurance premiums as all Americans are given the ability to enrol in a

public health insurance plan. However, there is little time to achieve them with the mid-term

elections due in 2022, where the Democrats tenuous grip on power may be lost, thus

making policy/regulatory change very difficult.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 6Investment Outlook February 2021

Finally, it is worth remembering that regulation can be positive for some companies. The

Regulation can be

expected focus on climate change and clean energy will benefit companies looking at

positive for some

hydrogen as a fuel, wind generation and companies making home insulation products. The

companies

clean energy thematic has already received much attention as evidenced by the dramatic

rise in the iShares Global Clean Energy Fund.

A Cooler Housing Market

The housing market has surged since July, with accelerating sales and price increases. This

Monetary and fiscal

defies earlier predictions that the local housing market would be hampered by Covid-19

stimulus and lack of

lockdowns and closed New Zealand borders. The spark for the housing fire has been the

housing supply have

“go hard and go early” monetary and fiscal policies of the Reserve Bank of New Zealand

boosted house prices

(RBNZ) and the Government. A housing shortage has fanned the fire.

25.0%

20.0%

New Zealand

House Price Index 15.0%

Source: Real Estate New 10.0%

Zealand

5.0%

0.0%

-5.0%

-10.0%

1993 1996 1999 2002 2005 2008 2011 2014 2017 2020

Recognising that the hot housing market presents a growing risk to financial stability, the

Loan-to-value RBNZ recently announced it will reinstate loan-to-value restrictions on bank mortgage

restrictions will start to lending from March. However, the major banks have already instituted the proposed loan-

take heat out of housing to-value limits as they recognise the dangers of liberal mortgage lending in a climate of

market… rapidly rising house prices and uncertain economic prospects. We expect the loan-to-value

limits will start to dampen housing activity from March 2021.

By March, the housing market is likely to be cooling anyway. This reflects New Zealand’s

border being largely closed until early 2022, which will limit the number of migrants and

… at a time the housing overseas students. With the government wage subsidy scheme now ended and unlikely to

market is likely to be be replaced, unemployment is set to rise. In the past, significant rises in unemployment

cooling anyway have tended to dampen house prices as incomes stagnate and people worry about their

jobs and businesses. At the same time, house building has been continuing at pace, which

is steadily increasing the supply of houses and easing the pressure on house prices. Still,

low mortgage interest rates and the prospect of a post-pandemic economic activity will

provide underlying support for house prices. Therefore, annual house price inflation is likely

to ease to around 0-5%.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 7Investment Outlook February 2021

Asset Allocation –

Caution May Reign Until

More Confidence Returns

Key Takeaways A Global Economic Recovery Remains on the Horizon

• Low interest rates The surge in Covid-19 infections and reinstatement of lockdowns of various degrees of

likely to continue stringency in large, developed economies means a weaker prognosis for the global

despite a surging economy in the first quarter of 2021. Unemployment has flatlined at levels above those

post-pandemic prevailing prior to the pandemic and retail activity has been in decline in recent months

economy.

after a strong initial bounce off the first wave of lockdowns.

• Recovering

economies and 7,000

low interest rates

likely to provide 6,000

support for

5,000

equities.

• Uncomfortably 4,000

high inflation is

the biggest risk to 3,000

equity valuations.

2,000

US Initial Jobless 1,000

Claims 0

Source: US Department of Jan-19 Apr-19 Jul-19 Oct-19 Jan-20 Apr-20 Jul-20 Oct-20

Labor, Bloomberg

In the US, much of the recent pull-back in household spending has been due to job losses

and the expiration of previous government income support under the Coronavirus Aid,

Relief, and Economic Security (CARES) Act. However, with the recent passing by the US

Congress of $US900 billion in additional support, and $US1.9 trillion more support

promised by the incoming Biden administration, fiscal policy will substantively compensate

for declining wage income until the US economy normalises. Elsewhere in the world,

governments have indicated that they will similarly stoke spending to compensate for

short-term loss of wage incomes and to ensure households keep spending.

Eventually, vaccinations will reach a point where a high degree of community Covid-19

immunity is achieved. However, it will take a while to vaccinate on a sufficient scale to allow

a full return to normal life in the world’s largest economies, probably towards the start of

Households have built 2022. By this stage, governments are likely to have started pulling back from large-scale

buffers to spend post- fiscal support. Households have significantly increased their savings during the pandemic

pandemic and are in positions to increase spending when the time allows it. However, after an initial

surge in spending, a degree of spending caution may reign for a period as people regain

confidence to mingle in the post-pandemic world. This could delay a return to pre-

pandemic levels of activity until at least early 2022.

Inflation could spike Despite economic light on the horizon, central banks are unlikely to materially reverse their

up in short-term but ultra-accommodative policies in the foreseeable future. Although there could be a

unlikely to be a temporary spike in inflation as prices lift from depressed levels experienced last year,

problem longer-term elevated levels of unemployment and peoples’ entrenched expectations of continuing low

inflation is likely to lead to only moderate inflation in the foreseeable future.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 8Investment Outlook February 2021

In any case, many central banks have made it clear that they will tolerate higher rates of

In any case, central

inflation than their mandated targets of around 2% to make up for persistently low inflation

banks will tolerate

in recent years. This means central banks will keep low interest rates and accommodative

higher inflation

monetary policy settings until there is clear evidence of achieving 2% inflation and, even

then, will be careful about removing stimulus too soon.

Global Equities Supported in the Medium Term

On a short-term basis the risk of an equity market correction is increasing as investors factor

in a solid run of positive news, which has left limited space for disappointment. To a large

degree, the positive outlook hinges on a successful Covid-19 immunisation campaign. It

will be important to monitor progress as the campaign ramps up.

However on a medium-term view, rock bottom interest rates mean that investors seeking

Equities appear regular investment income and/or who seek to protect the inflation-adjusted value of their

attractive compared

investments have been forced to look at riskier investments, like equities. Equity valuations,

to bonds therefore, compared to their traditional investment alternative, debt securities, continue to

look attractive on a medium-term horizon.

On a shorter horizon, US money supply has rocketed up over the past year due to large-

scale US Federal Reserve asset buying, as shown in the chart below. We expect the Fed will

Fed likely to reduce its recognise the need to ease back on its bond buying by the end of the year as the economy

bond buying recovers. However, it will also be wary of sparking a sharp rise in bond interest rates, as

gradually but money happened in the disruptive 2013 “taper tantrum”. Therefore, reductions in Fed asset

supply will increase at purchases are likely to be signalled well in advance and be relatively gradual. Money

a good pace supply growth will likely continue to be strong, which has traditionally been supportive of

equities.

70%

US M1 Money

60%

Supply – Annual

Percent Change 50%

Source: US Federal

40%

Reserve, Bloomberg

30%

20%

10%

0%

2014 2015 2016 2017 2018 2019 2020

There is still a higher degree of anxiety amongst equity investors about the short-term

outlook than existed pre-pandemic. This is reflected by a higher level of the VIX Index,

Still room for equity which is an indicator of US equity investors’ expectations of market volatility over the next

investor nerves to three months. Lower levels of the VIX are often associated with higher equity valuations, so

calm a reversion to calmer market prices as economies recover from the pandemic could see

further support for equity valuations.

A combination of improving economic growth, low interest rates, and surplus financial

Cyclical stocks could market liquidity will favour equities of a more cyclical nature relative to more defensive parts

outperform more of equity markets. These will tend to be the stocks that have largely underperformed the

defensive areas of rest of the equity market in recent years, such as those in the financial, energy, materials,

equity markets and industrial sectors. In contrast, stocks that have substantially outperformed in the period

of low and falling interest rates, Covid lockdowns, and uncertain growth prospects, such as

the large technology companies, may struggle to keep pace with the market overall.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 9Investment Outlook February 2021

A key risk to our constructive outlook on global equities is a sharper rise in inflation than

Uncomfortably high

central banks are comfortable with. Central banks will be quite happy to see inflation lift

inflation is a relatively

moderately above 2% for an extended period. Inflation in the 2-3% range has historically not

low probability but

been detrimental to equity valuations, as the following chart shows. However, when

could have major

inflation has risen above 3% it has tended to coincide with lower equity valuation multiples.

effects on equities if it

This is likely because central banks often must sharply raise interest rates to get inflation

occurs

back under control, which hurts equity prices.

20

Price-to-earnings multiple 18

US Price-to-

Earnings Multiple 16

and Inflation 14

Source: US Bureau of Labor

12

Statistics, Bloomberg

10

8

6

-1 - 0% 0 - 1% 1 - 2% 2 - 3% 3 - 4% 4 - 5% 5 - 6% 6%+

Inflation

Have New Zealand Equities Run Out of Puff

New Zealand equity The New Zealand equity market has outperformed many other developed equity markets

valuation ratios have a in recent years. This is largely due to the outperformance of growth stocks such as Fisher

tight relationship with and Paykel Healthcare and high dividend yield stocks such as the electricity generators.

long-term interest The share prices of companies in the retirement village sector have benefited from rising

rates house prices. Performance in these parts of the market have been driven by low and falling

interest rates, which makes stocks in them more attractive. The chart below shows the

relatively tight past relationship between New Zealand equity valuations, as measured by

price-to-earnings multiples, and the 10-year government bond interest rate.

40

New Zealand

Price-to-earnings multiple

35

Price-to-Earnings current

Multiple 30

Correlates with

25

Long-term

Interest Rates 20

Source: Bloomberg

15

10

0% 1% 2% 3% 4% 5% 6% 7%

Government bond interest rate

Looking ahead, we expect long-term New Zealand interest rates to gradually rise. Based on

Local equities are

past relationships, higher interest rates will be more of a headwind for New Zealand equities

vulnerable to

than for global equities. In addition, the New Zealand equity market is not significantly

underperformance as

leveraged to the global economy due to the largely domestic focus of New Zealand listed

interest rates rise

companies so probably will not benefit to the same degree as more cyclical equity markets

from a revival of global economic activity once the Covid vaccines take effect.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 10Investment Outlook February 2021

Cyclical Exposure to Benefit Australian Equities

In contrast to New Zealand equities, the performance of Australian equities have lagged the

performance of many other developed equity markets over the past year. However, the

Australian equity market is well positioned to take advantage of the global economic upturn

Australian equities brought on by Covid-19 vaccines and moderately rising interest rates. Australian equity

could benefit from a valuation ratios are not generally as high as markets like the US or New Zealand. Because

global upturn and the Australian equity market has a relatively high concentration of listed companies with

higher interest rates positive exposure to commodity prices, like iron ore and copper, that should perform well

as the global economy recovers. In addition, the Australian equity market has a relatively

high proportion of bank stocks, which are expected to perform well as interest rates

gradually rise. Furthermore, the Reserve Bank of Australia has materially lifted the cap on

the level of dividends the banks can pay their shareholders.

Forecasts

Economics As at 28 January 2021

Fiscal Balance % GDP GDP Growth % Inflation % 3 month Libor % 10 Year Government%

2020E 2021F 2022F 2020E 2021F 2022F 2020E 2021F 2022F Spot 3mth 12mth Spot 3mth 12mth

New Zealand -8.5 -7.7 -10.2 -4.7 4.5 3.3 1.4 1.5 2.0 0.3 0.3 0.3 1.1 1.1 1.4

Australia -8.0 -7.2 -7.3 -2.9 3.6 3.0 0.7 1.5 1.8 0.0 0.1 0.1 1.1 1.1 1.3

US -15.6 -16.0 -9.7 -3.5 4.1 3.4 1.2 2.0 2.1 0.2 0.2 0.2 1.0 1.1 1.3

Japan -13.0 -11.9 -7.5 -5.3 2.6 1.9 0.0 0.1 0.5 -0.1 -0.1 -0.1 0.0 0.0 0.0

Europe -9.5 -9.6 -5.0 -7.3 4.3 3.9 0.3 0.9 1.2 -0.5 -0.5 -0.5 -0.5 -0.4 -0.2

United Kingdom -18.7 -13.9 -7.2 -10.8 4.7 5.7 0.9 1.5 1.9 0.0 0.1 0.1 0.3 0.4 0.8

China -6.7 -6.7 -5.9 2.1 8.2 5.5 2.6 1.6 2.3 2.6 3.0 2.9 3.1 3.3 3.3

Source: Jarden, Bloomberg (* actuals)

NZ and Australia fiscal balance is 30 June

NZ is the 90-day bank bill yield

Equities and Commodities Foreign Exchange

Spot 12 mth forecast Past Past

USD NZD

Month Year

Australia – ASX 200 6,770 6,590 - 7,280 1.4% -4.4% Spot 12mth Spot 12mth

Emerging Markets 1,401 1,410 - 1,560 10.5% 22.3% NZD 0.72 0.74 - -

Europe – Stoxx 600 411 410 - 450 3.8% -3.1% AUD 0.78 0.80 0.93 0.92

Japan - Topix 1,850 1,900 - 2,100 3.1% 6.0% EUR 1.22 1.25 0.59 0.59

New Zealand – NZX 50 13,026 12,800 - 14,140 2.7% 10.9% JPY 103.5 102.0 74.7 75.5

UK – FTSE 100 6,740 6,950 - 7,680 3.2% -11.9% GBP 1.37 1.37 0.53 0.54

US – S&P 500 3,852 3,760 - 4,150 3.8% 15.7% CNY 6.46 6.50 4.66 4.81

Oil Brent USD/bbl 56 54 - 60 7.3% -5.4% Source: Jarden, Bloomberg

Gold USD/Oz 1,872 1,900 - 2,100 -0.5% 19.9%

Source: Jarden, Bloomberg

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 11Investment Outlook February 2021

Asset Allocation

February 2021

Based on the Asset Allocation discussion on pages 8-11, we have not made any changes to our Tactical Asset Allocation.

The Strategic Asset Allocation represents the average weighting over the long term (circa ten years or an entire economic

cycle). The Tactical Asset Allocation represents a deviation from the Strategic Asset Allocation to take advantage of

expected changes in asset class returns over the short term (say 6 months plus).

% Strategic Allocation Tactical Deviation %

Income Assets Growth Assets

Conservative

Cash 15 -2 +1

NZ Debt Securities 55 +2

Property 4 -2

NZ Equities 8 -1

Australian Equities 3 +1

Global Equities 12 +2

Alternative Strategies 3

Balanced/Conservative

Cash 11 -2 +1

NZ Debt Securities 44 +2

Property 5 -2

-1

NZ Equities 12

Australian Equities 6 +1

Global Equities 18 +2

Alternative Strategies 4

Balanced

Cash 8 -2 +1

NZ Debt Securities 32 +2

Property 6 -2

NZ Equities 16 -1

Australian Equities 8 +1

+2

Global Equities 25

Alternative Strategies 5

Balanced/Growth

Cash 7 -2 +1

NZ Debt Securities 23 +2

Property 6 -2

NZ Equities 20 -1

Australian Equities 10 +1

Global Equities 29 +2

Alternative Strategies 5

Growth

Cash 5 -2 +1

NZ Debt Securities 15 +2

Property 6 -2

NZ Equities 23 -1

Australian Equities 12 +1

Global Equities 34 +2

Alternative Strategies 5

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 12Investment Outlook February 2021

Darrin Grafton – Serko

CEO & Co-Founder

It is quite conceivable that Darrin could describe his place of residence as “no fixed

abode” given the huge amount of travelling he did prior to the Covid-19 pandemic.

He fully expects this to be the case again once the pandemic is brought under

control and travel restrictions are lifted. He notes that while applications like Zoom

have been a great solution to the immediate problem of travel restrictions, humans

are social beings and thrive on face-to-face connections.

Growing up in Waimauku

Darrin Grafton

Darrin’s life started on the family’s Waimauku dairy farm on the outskirts of

Auckland. Being the eldest son, he helped out on the farm before and after school

Key Takeaways

from a young age. This instilled in him a strong work ethic, tenacity, and problem-

• As a boy, Darrin

solving skills. Darrin recollects that at school he was good at maths, really enjoying

developed acute

solving mathematical problems and looking for patterns in data. While he typically

problem-solving

skills which have

did well in school exams, his school reports had a continual theme – “could do

served him well. better”. Looking back, he thinks he must have been a rather disruptive child to have

in the classroom, due to his constant chatter.

• Darrin loves to set

and achieve Living close to Muriwai Beach it is little surprise that Darrin enjoyed surfing in his

extreme goals. spare time. In addition, from the age of fifteen he took up Kung Fu, training five

• Serko’s goal is to nights a week for eight years.

make business

travel an easy Leaving school in the sixth form Darrin got his first exposure to computers at

stress-free Carrington Polytechnic (now Unitec Institute of Technology). Having had no prior

activity, exposure to computers, he was selected as one of a handful of successful

particularly when applicants based on an aptitude test. Initially he found the course content

unforeseen challenging and was assisted by a teacher who, on his own time, came into the

disruptions occur. polytechnic each weekend to help Darrin’s learning. This resulted in a light bulb

• Darrin is moment when all the concepts being taught fell into place, from which point there

passionate about was no holding Darrin back.

New Zealand Inc

It was at Carrington that Darrin first met his lifelong business partner Bob Shaw.

Darrin and Bob have had and continue to have numerous business ventures

Darrin met his lifelong together including jointly founding Interactive Technologies in 1994 (which

business partner Bob

became Gullivers Travel Group) and Serko in 2007. On completing their studies

Shaw at Carrington

both ended up working for IMaCS creating corporate accounting software using

Polytechnic in 1985

Cobol.

In his spare time Darrin loves boating and fishing. Being on the water is the trigger

for him to switch off and relax. Despite being deeply involved in his work Darrin puts

family first. His family is very important in keeping him grounded, which is important

as he has a habit of setting extreme goals.

Darrin as Serko’s CEO

Darrin has a mantra of executing on what you say you will, and never to hype

Customer loyalty is expectations. He also believes that honesty, helping clients during a crisis, humility,

reflected in Serko’s and trust build loyalty. Customer loyalty is reflected in Serko’s high retention rate.

high retention rate Many loyal customers also become your advocates.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 13Investment Outlook February 2021

Darrin enjoys nothing more than dreaming up solutions to problems. The ultimate

problem, and Serko’s reason for existing, is to make travel an easy stress-free

Solutions are backed activity, particularly when unforeseen events disrupt travel plans. The solutions he

up by rigorous data dreams up are backed by rigorous data analysis and are then brought to life by

analysis Serko’s super talented and diverse staff. Having great staff allows Darrin to

comfortably relinquish different aspects of his responsibilities as Serko grows and

he finds that he is doing too much. To ensure that he is up to the task, Darrin sets

aside time each day for himself and ensures that all emails are answered each day.

In running the business, Serko and Darrin have received numerous awards. Darrin

is most proud of being selected as one of the world’s top 25 most influential

executives by Business Travel News in 2014 and Serko being recognised as the

2020 HiTech Company of the Year, a fitting tribute to the success of the Serko

team.

Covid-19 Travel Restrictions Bite

Covid-19 travel restrictions have dramatically impacted Serko’s revenue and

earnings. In the six months to 30 September 2020 the number of travel bookings

fell 77% and total revenue fell 66% before factoring in any government grants.

Looking to the immediate future it is worth remembering that 93% of Serko’s

revenue is generated by domestic business travel in New Zealand and Australia.

New Zealand travel

New Zealand bookings have quickly recovered, currently nearly 90% of pre-Covid

bookings are now at

levels. Australian bookings have been slower to recover due to successive Covid-

nearly 90% of pre-

19 outbreaks leading to travel restrictions. Eventually, New Zealand’s dramatic

Covid levels

recovery is expected to be mirrored in Australia. While the impact of Covid-19 on

travel, and Serko’s revenue, remains highly uncertain in the short-term, Serko

expects to be able to manage its costs in line with the level of revenue which

eventuates and thus achieve its earnings target.

“Cash is more When it comes to managing a company’s cash position Darrin quips, “cash is more

important than your important than your mother”, as a company without adequate funding has few

mother” options. Consequently, Serko is constantly running scenarios to test that it has

adequate cash, with adequate being at least $16-18 million (following the recent

equity capital raising Serko had over $90 million cash). The business cases for the

different development projects are also regularly tested under various scenarios,

with immediate action taken whenever necessary to get a project back on track.

The issue which keeps Darrin awake at night, is not the pandemic, but the ability to

employ enough staff with the required skills and experience. Since September

2020 Serko has employed over 50 new staff and expects to employ 50-100 more in

2021.

Serko’s medium-term goal is to achieve $100 million revenue. There are several

paths Serko can take to achieve this. They include expansion in Australia, North

America, and Europe, rollout of Zeno and through the expansion of Bookings.com

for Business powered by Zeno. achieving the goal does not require all of these to

Zeno Travel eventuate. Success could come via one or a combination of partial successes.

The Vision for New Zealand Inc

Darrin’s goal is to see Darrin is passionate about New Zealand, which includes keeping Serko listed here.

New Zealand become Through mentoring of tech start-ups, it is Darrin’s goal to see New Zealand become

a global technology a global technology hub. In time as the value of Serko grows Darrin expects to

hub gradually sell down part of his interest in Serko so that he can further assist new

companies establish themselves by providing them with capital.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 14Investment Outlook February 2021

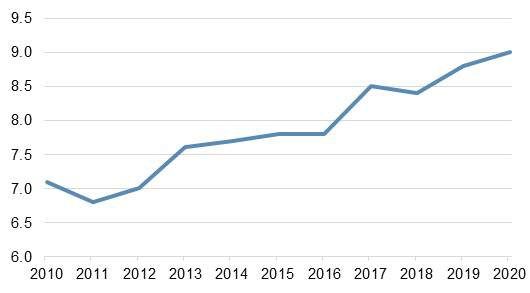

Introducing Ben Gilbert –

Head of Australian Research

Jarden has made a significant investment in Australia. A significant part of this

investment involves the creation of an extensive research capability which will benefit

our New Zealand Wealth Management clients. This process started with the

appointment of Ben Gilbert as Head of Australian Research.

Since starting in September, Ben has initiated coverage on the Australian food sector

and employed a research team of nearly twenty analysts, who all will have commenced

work by early February. The research team will be completed once a couple more

analysts are hired. As shown in the graph on the following page, by the middle of the

year we expect Jarden’s coverage of Australasian listed companies to rank in the top

Ben Gilbert three of all equity research teams in Australasia.

Key Takeaways A Proud South Australian

• During his school Ben was born and bred in Adelaide. He was educated at St Peter’s College, a highly

years Ben proved

regarded boy’s school in Adelaide. There Ben undertook the International Baccalaureate

himself to be multi-

diploma program which involved a broad subject matter – chemistry and economics at

talented both inside

which Ben excelled plus English, maths, art and Chinese. Ten years of studying Chinese

and outside the

culminated in a trip to China which included staying with a family in Shanghai for a

classroom.

period. Outside the classroom Ben enjoyed skiing, qualifying as a state representative. In

• Ben has almost

relating to this achievement, he adds with a wry smile that being in Adelaide the skiing

completed building

was all indoors. Ben also played AFL although switched codes in his final year to qualify

a new Australian

for the first eleven soccer team and go on a trip to New Zealand where his team played

equity research

against five different North Island schools. Despite this temporary change in sports, Ben

team with the future

firmly in sight. remains an avid AFL fan and supporter of the Port Adelaide Power. To ensure that his

five-year-old son shares his passion for the sport he recently signed him up to AFL

Auskick, which teaches kids fundamental motor skills and what it means to play as part

of a team. These days Ben enjoys the occasional ski, running and is very keen to get a

Jarden netball or soccer team going in the Sydney office.

Off the sports field Ben was a successful debater. He always went as the third speaker of

the debating team. Being the third speaker it was his role to attack the substantive

arguments raised by the opposing team, which allowed him to hone his skills of thinking

on his feet. In a similar vein, Ben also enjoyed mooting (an oral presentation of a legal

The loss to the legal issue against an opposing counsel) where he represented his school in state

fraternity is a gain to the competitions. This raises a question as to why he chose a career in investment research

equity research rather than law. For him, the answer reflects the action and dynamic nature of financial

profession markets. Consequently, on leaving school Ben headed for the University of Sydney to

study finance, accounting, and economics rather than staying in Adelaide to study law.

While Ben recounts that he was more focused on having a good time at university than

his studies, he clearly did well, first gaining an internship at KPMG and then an internship

at UBS.

The next fifteen years of his career were spent at UBS, where he was Deputy Head of

Consistently ranked as Research and led the consumer research team. Since 2015, Ben has consistently ranked

Australia’s number one as Australia’s number one consumer analyst in multiple surveys across the retail and

consumer analyst food/beverage sectors. In addition to the dynamism financial markets dish up constantly,

Ben finds significant satisfaction in being able to build a unique helicopter view of the

sectors he analyses. The unique view that equity analysts can develop reflects the wide

range of stakeholders that analysts get to speak to, many of whom do not or will not

speak to each other. For example, in the consumer space Ben speaks to company

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 15Investment Outlook February 2021

management, competitors, suppliers, landlords, consultants, regulators, developers of

new technology, industry bodies, and investors, all of which have a unique picture of the

consumer sector. Furthermore, many of these contacts have overseas connections

which give a perspective of developing trends which are yet to reach Australian shores.

Building a Formidable Research Team

Ben has hired the best Ben is excited to be leading a new research team, which can be constructed properly

people from a diverse with a medium-term view of the future. Building a new team has allowed Ben to hire the

range of backgrounds best people, from a diverse range of backgrounds, who have different perspectives on

the world, a passion for their research, and who have a shared vision of Jarden research.

Ben observes that the nature of research is changing as the sectors and factors that

produce the next generation of returns will invariably be different to those of today.

Jarden’s objective is to lead the change. This will be achieved by:

1. Focusing on collaboration across the research team.

2. Utilising data, with an emphasis on differentiated and proprietary data sets.

3. Having research which is easy to digest.

4. Utilising external partnerships.

5. Having an agile approach to company coverage.

Identifying new themes Consequently, the Jarden Australia research team will spend more time on producing

early and challenging differentiated research and less on maintenance research, which simply extrapolates

current thinking will be a what is currently happening adding limited value. Identifying new themes early will be

hallmark of the team’s critical and challenging current thinking by looking at it from a new perspective will be a

research hallmark of the team’s research.

Coverage Target

Jarden’s Near-term

Target will put it in

the Top 3 by

Australasian

Research Coverage

Source: Jarden

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 16Investment Outlook February 2021

Top Stock Picks – 2021

Key Takeaways New Zealand Equities

• NZ Equities:

AFT Pharmaceuticals (AFT.NZ) Price $5.13 Rating: Outperform

- AFT

- Heartland

Why? We have higher confidence in AFT’s organic growth outlook, in particular the

- Mainfreight

continued momentum across the Maxigesic product suite and steady growth in the

- Pushpay

Australasian product portfolio. The simplified capital structure also helps to underpin

- Z Energy

strong valuation support.

• Australian Equities:

Investment thesis? Management have maintained guidance for FY21 EBIT $14-$18

- Appen

million despite the challenges so far. A more exaggerated skew to 2H21 is expected as

- Harmoney

Covid-19 complications from a disrupted 1H ease. Importantly, the monthly run-rate in

- Ramsay

early 2H was up on the previous year. We also expect the company sales pipeline to build

- Wisetech

with an acceleration in the number of new countries AFT is selling into. Furthermore,

- Worley

Maxigesic IV is now registered in 20 countries (up from 17 in March 2020) but currently

• Global Equities: only sold in 3. This is expected to underpin robust revenue and earnings growth over the

- Alphabet medium term. Another pleasing development is the company intends to start paying

- BlackRock dividends in FY22 after achieving target net debt of $25-$30 million.

- Micron

Catalysts? News flow on outlicencing deals, uptake of Maxigesic IV and new

- Salesforce

developments of platforms NasoSurf and Pascomer, 2021 profit result in May 2021.

- Toyota Motors

- Unilever Key risks? Out-licensing execution, clinical trials, regulatory change and competition.

- UnitedHealth

- Walt Disney

Note: Prices as of 28 January. Heartland Group (HGH.NZ) Price $1.88 Rating: Neutral

Why? The outlook for the bank continues to improve with lower impairments (versus prior

expectations), solid cost control and higher interest income all supporting a strong

recovery in earnings.

Investment thesis? Heartland’s New Zealand business offers continued growth through

Motor, Business and Reverse Mortgages, while further growth in Australia is anticipated on

the back of expansion in Reverse Mortgages (currently 26% market share), Business and

Consumer activities. Digitalisation is expected to underpin the Bank’s offering, having

launched a residential mortgage platform that enables it to offer interest rates at materially

lower levels than the larger, more traditional banks. We expect this strategy to help build

scale and drive net interest margin expansion. Heartland now trades at a price-to-book

value multiple of 1.4x with a forward return on equity of 10.4%. This compares favourably

to the larger banks at 1.3x and 8.4% respectively.

Catalysts? Removal of the RBNZ’s dividend suspension, Australian Reverse Mortgage

growth, NZ credit/deferral progression, 1H21 profit result in February 2021.

Key risks? Resurgence in Covid-19 impairments, RBNZ capital adequacy rules, low

interest rate environment slowing retail deposit growth which pushes Heartland towards

higher cost wholesale funding.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 17Investment Outlook February 2021

Mainfreight (MFT.NZ) Price $68.40 Rating: Outperform

Why? Mainfreight is a high-quality business with solid operating momentum and a

defensive balance sheet. The thematic appeal is Mainfreight’s exposure to the global

economic recovery through increased freight activity.

Investment thesis? Mainfreight has been a major beneficiary of the pressure put on the

freight industry during Covid-19 driven by substantial share gains, greater essential

business mix, better line haul utilisation (especially on Australian regional routes) and

good cost control. As a result, the company reported underlying net profit growth of 23%

in 1H21. We expect ongoing growth for Mainfreight over the near-term, albeit with FY21

profit growth moderating to 11%, reflecting a combination of increasing network intensity

and utilisation, along with freight verticals exposed to better-than-expected underlying

consumer demand. In addition, European margins should benefit from a normalisation in

warehouse utilisation following a period of inventory contraction in this business.

Unsurprisingly, given the disrupted Covid-19 backdrop in the US, this business is likely to

remain the key detractor to overall group performance. We expect these headwinds to

subside in 2021 as progress is made on the vaccine rollout and activity levels recover with

the US election now in the past.

Catalysts? Interim trading updates, 2021 profit result in May 2021.

Key risks? Covid-19 lockdowns, an unsuccessful vaccine roll-out.

Pushpay (PPH.NZ) Price $1.68 Rating: Outperform

Why? We see Pushpay as well positioned for a structural growth opportunity driven by the

increasing share of digital payments in the US faith sector where it has a dominant share

Investment thesis? 2020 was been remarkable for Pushpay with Covid-19 significantly

accelerating the shift to digital giving, effectively compressing 3 years’ worth of growth

into one. As such, the company delivered 1H21 processing volume growth of 45%,

revenue growth of 53% and earnings growth of 178%. The key earnings driver has been

margin expansion which has grown to 31%, from 17% a year ago. This highlights the

significant operating leverage in the business. Given the strong cash generation (forecast

FY21 free cash flow yield of 3.5%) and expected pay down of debt, we forecast Pushpay

will return to a net cash position by 2H21. We are also optimistic on Pushpay’s more

targeted focus on the Catholic church segment where it is underrepresented and consists

of around 17,000- 20,000 churches.

Catalysts? New customer wins over the next 6-12 months and continued traction in

selling its integrated Church Management Software product.

Key risks? Slowing new customer growth, decline in US giving market, processing fee

compression, governance concerns, increased uncertainty surrounding the Huljich family

stake of 15.7% after Peter Huljich resigned from the board.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 18Investment Outlook February 2021

Z Energy (ZEL.NZ) Price $3.06 Rating: Outperform

Why? We are becoming increasingly confident in the new strategy management are

executing which should lead to a turnaround of the business.

Investment thesis? We believe the key reason why Z Energy appears so undervalued is

the low confidence investors have in management’s ability to execute. We are becoming

increasingly confident that management are now executing a strategy that should

reposition the business to return to earnings growth going forward. Recent trading

updates have confirmed our view with volumes tracking well (despite the lack of

international tourist demand), broadly steady margins and cost-out delivering. The

company has reiterated FY21 earnings guidance of $235-$265 million. While it has left the

door open to a possible 2H21 dividend, we believe the company would need to produce

FY21 earnings of $285 million to satisfy its debt covenants, which feels like a stretch.

Hence, the likely resumption will be after its 1H22 result in November. We believe the

prospect of a FY22 dividend of 24 cents per share (resulting in a gross forecast dividend

yield of 10.6%pa) will be the catalyst for the market to re-rate the share price.

Catalysts? Monthly volume data, 2021 profit result in May 2021 and any guidance around

dividend.

Key risks? Competitive pressures from the continued expansion of low-cost operators,

discounting and lower petrol margins. Other risks include Z Energy’s ability to retain cost

savings and NZ Refining’s desire to fast track the conversion to an import terminal.

Australian Equities

Appen (APX.AU) Price A$22.94 Rating: Neutral

Why? Appen collects and labels image, text, speech, audio, and video data used to build

and improve the artificial intelligence (AI) systems of its corporate (Facebook and Google)

and government customers. The big opportunity is more companies deploying AI or

complex machine learning algorithms.

Investment thesis? Appen’s market-leading scale positions the business well to capitalise

on this rapid sector growth. Covid-19 significantly disrupted Appen’s customers,

particularly in California, and new projects commencing. This resulted in an earnings

guidance downgrade in December to A$106-$109 million (from A$125-$130 million).

However, the industry backdrop remains favourable and we expect growth momentum to

bounce back over 2021-22. There remain short-term uncertainties over Appen's sales

pipeline however this appears factored into its lower share price which creates some

buffer. Furthermore, the 32% increase in the number of new and early-stage projects from

key customers is a testament to Appen's market-leading credentials.

Catalysts? FY20 profit result in February.

Key risks? Concern about Appen's lack of earnings visibility compared with domestic tech

peers.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 19Investment Outlook February 2021

Harmoney (HMY.AU) Price A$2.62 Rating: Buy

Why? Harmoney’s innovative marketing strategy through the advanced use of Google

smart bidding allows a targeted approach which yields significantly better returns than

traditional ad placements. This combined with its repeat customer program, sees it well

positioned to capitalise on the ongoing structural shift towards non-bank lenders.

Investment thesis? Harmoney is a leading personal lender in Australasia, providing

unsecured loans directly through digital channels. Harmoney’s share price has

underperformed since listing, potentially reflecting a more modest near-term growth

profile versus peers. The company made a conscious decision in the early Covid-19

period to limit originations in response to economic uncertainty. With originations having

bottomed in July 2020 and Harmoney reporting 2Q21 growth of 47% on the previous

quarter (NZ +44% to $89 million and Australian +69% to $27 million), we believe the

volume recovery is tracking very well. Harmoney has also derisked the funding side

further by securing a second NZ warehouse funding facility, increasing total capacity to

$264 million. Increased wholesale funding at a lower cost should underpin margin

expansion, allowing reinvestment into loan growth through sharper pricing. The

company’s customer acquisition process should continue driving operating leverage with

approximately 60% of originations coming from existing clients with lower acquisition

costs and impairments, therefore accruing significantly higher incremental margins.

Catalysts? Sustained volume recovery in line with peers and 1H21 profit result in February.

Key risks? Covid-19 led economic headwinds impacting volumes and impairments,

reliance on wholesale funding and higher interest rates over the medium term.

Ramsay Health Care (RHC.AU) Price A$63.89 Rating: Neutral

Why? Whilst we expect Covid-19 to continue impacting private health participation in a

negative way over the short term, we are more confident in the inevitable volume recovery

over the medium term and Ramsay’s ability to generate solid earnings growth through

brownfield developments, potential acquisitions, and cost savings.

Investment thesis? We remain confident Ramsay is well positioned to benefit from a

sustained pickup in elective surgery volumes over the next 1-2 years. Furthermore,

elective surgery wait list pressure in the public system could result in increased

outsourcing of work to private providers such as Ramsay, where capacity is not

constrained. The volume recovery in the UK and Europe is likely to be hampered given

the second wave of Covid-19 infections, but we expect government support programs to

be extended into 2021.

Catalysts? Further government support programs, a successful Covid-19 vaccine rollout,

1H21 profit result in February.

Key risks? Execution on brownfield developments, changes to government policy,

structural change of industry growth rates relative to history and unexpected tariff cuts.

Jarden Securities Limited | NZX Firm | www.jarden.co.nz 20You can also read