Thinking big Doing better - Adani Enterprises Limited Investor Presentation - BankTrack

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Adani Enterprises Limited

Investor Presentation

Thinking big

Doing better July 2018

Legal Disclaimer

Certain statements made in this presentation may not be based on AEL assumes no responsibility to publicly amend, modify or revise any

historical information or facts and may be “forward-looking forward looking statements, on the basis of any subsequent

statements,” including those relating to general business plans and development, information or events, or otherwise. Unless otherwise

strategy of Adani Enterprises Limited (“AEL”), its future outlook and stated in this document, the information contained herein is based on

growth prospects, and future developments in its businesses and management information and estimates. The information contained

competitive and regulatory environment, and statements which herein is subject to change without notice and past performance is

contain words or phrases such as ‘will’, ‘expected to’, etc., or similar not indicative of future results. AEL may alter, modify or otherwise

expressions or variations of such expressions. Actual results may differ change in any manner the content of this presentation, without

materially from these forward-looking statements due to a number of obligation to notify any person of such revision or changes.

factors, including future changes or developments in its business, its No person is authorized to give any information or to make

competitive environment, its ability to implement its strategies and any representation not contained in and not consistent with this

initiatives and respond to technological changes and political, presentation and, if given or made, such information

economic, regulatory and social conditions in India. This presentation or representation must not be relied upon as having been authorized

does not constitute a prospectus, offering circular or offering by or on behalf of AEL. This presentation is strictly confidential.

memorandum or an offer, or a solicitation of any offer, to purchase or This presentation does not constitute an offer or invitation

sell, any shares and should not be considered as a recommendation to purchase or subscribe for any securities in any jurisdiction,

that any investor should subscribe for or purchase any of AEL’s shares. including the United States. No part of its should form the basis of or

Neither this presentation nor any other documentation or information be relied upon in connection with any investment decision or any

(or any part thereof) delivered or supplied under or in relation to the contract or commitment to purchase or subscribe for any securities.

shares shall be deemed to constitute an offer of or an invitation by or None of our securities may be offered or sold in the United States,

on behalf of AEL. without registration under the U.S. Securities Act of 1933, as

AEL, as such, makes no representation or warranty, express or implied, amended, or pursuant to an exemption from registration therefrom.

as to, and does not accept any responsibility or liability with respect to, This presentation is confidential and may not be copied or

the fairness, accuracy, completeness or correctness of any information disseminated, in whole or in part, and in any manner. This presentation

or opinions contained herein. The information contained in this contains translations of certain Rupees amounts into U.S. dollar

presentation, unless otherwise specified is only current as of the date amounts at specified rates solely for the convenience of the reader.

of this presentation.

2

Contents

Adani Group

Company Profile

AEL: Coal Mining & ICM

Adani Gas Ltd

Adani Wilmar Ltd

Mundra Solar PV Ltd

Others

Carmichael Mine, Australia

3

Nation Building - Responding strategically to some of India’s profound challenges

One of the global growth Rising middle class Estimated to be the

engines of the 21st century, places increasing world’s 5th largest Availability of cost

ranking high on many macro- demand on consumer market by effective engineering

economic indicators infrastructure 2025 resources

Rising Energy Needs Growing Infra Requirements Increasing Power Demand Food Safety

• Indian economy to remain • 90% of the volume and 72% • ~70% of electricity is • India has among the highest

heavily reliant on Coal of total value of country’s generated from thermal food losses in the world

international trade is power which will continue

• The key driver of coal through maritime transport over the next two decades • Stagnant oil seed

demand is the power sector production and rising edible

• Shipping Ministry estimates • In 2015, as per IEA, World oil demand is increasing

Indian Ports will need to Energy Outlook, over 240 import dependency

have capacity to handle 2.5 million Indian citizen had no

bn MT cargo by 2025 access to electricity

• Resources: Obtaining coal • Logistics: A large network • Energy: Conventional and • Agri: Agri products &

from mines and trading; in of ports, Special Economic Renewable Power infrastructure

future it will also include oil Zone and multi-modal generation, transmission,

and gas. logistics – rail and ships Solar PV manufacturing and

• Adani’s coal operations will gas distribution

account for ~20% of India’s • Adani Ports will handle ~20% • Adani’s power generation will • Adani will cater to 25% of

projected coal requirements of the total cargo at Indian represent ~5% of India’s India’s edible oil demand by

by 2021 Ports by 2021 projected capacity by 2021 2021

4

The Making of India’s Leading Infrastructure Group

1988 1995 2002 2009 2018

Coal Trading

Started a Commenced Among the largest

(1999) Coal traders in the

Commodity world

Trading ICM

Gautam Adani

Business Awarded India’s

Chairman 1st MDO

(2006)

Acquired Carmichael

Adani Acquired Bunyu coal mine Australia

Coal Mine (2010)

Enterprises listed

Indonesia (2008)

(1994) Mining operations

in India, Indonesia Coal Mining

& Australia

Mundra Port

(MDO)

Commenced

1995 (1995)

50: 50 JV with

Wilmar International Commissioned

(2000) Solar PV plant at Mundra

(2017)

Grain Silo Depot

2002 commissioned at 7

Solar Mfg

locations (2007)

Adani Power

1st CNG Station

Adani listed (2009)

Ahmedabad Awarded Grain Storage

Ports

(2004) business from MP state

listed

(2007)

“Fortune”

Largest Food

2009 Commissioned first 1st transmission FMCG brand in

line India

unit (2009)

commissioned

(2009) Worlds Largest JV with

Single location Indian Oil Agro

Acquired Solar Power Plant Corporation

Presence

Dhamra Port Listed (2015) (648 MW) (2016) (2014)

Acquired 1,200 MW in 13 cities

(2014)

Udupi Thermal Power

plant (2015)

Acquired GMR and

Reliance Transmission Project pipeline To be

Lines (2016) > 2GW listed

(2018)

2018 Operates 10

Bangladesh PPA

ports/terminals

Signed (2017) To be

BSES acquisition (2017)

listed

(2018)

Adani Gas

Adani Ports Adani Power Adani Transmission Adani Green Energy

Adani Green Energy = will be demerged from AEL w.e.f from 1st April 2018 FMCG = Fast-moving consumer goods

All business in green colour in Adani Enterprises Limited 5

Adani Group – At a Glance

Largest private sector ports, thermal power, transmission, renewables and coal trading player in India

180 MMT ~15% of India’s EXIM trade 10,440 MW ~5% of India’s Thermal Generation Capacity

2,500 MW ~4% of India’s Renewable Generation Capacity 11,890 Ckt Km ~3% of India’s Transmission Network

Promoter Promoter Promoter Promoter Promoter Promoter

Group Group Group Group Group Group

74.9% 63.6% 73.1% 74.9% 86.9% 74.9%

Adani Enterprises Adani Ports and SEZ Adani Power Adani Transmission Adani Green Energy Adani Gas

–Integrated coal –India’s largest –India's largest private –India’s largest –Renewables –Leading Private

management commercial ports thermal power private transmission Capacity: 1.9 GW Sector CGD

operations operator and generation Co with Co operational, 1.2 GW Company in India

–Over 50% market integrated logistics installed capacity of –Installed Capacity under pipeline –Focussed Pure Play

share in coal (66 Company 10,440MW 5,000ckt KMs; –Solar: 90%, Wind: Gas Marketing and

MTPA) –Market share of ~15% –A national record: doubling by 2019 10%(3) Distribution

–Leading Coal MDO in India’s cargo Mundra thermal plant –SPA signed in Dec –Geographically company

player in India –10 Ports across West running continuously 2017 to acquire BSES diversified portfolio –Operational in 4

and East Coast for 600 days Electricity cities

–Agro commodities and –Tamil Nadu 648 MW

storage, ‘Fortune’ - –Multi-modal logistics –Signed PPA with Govt distribution (c. 3 mn : World’s largest –IOAGPL – 50:50 JV

India's leading cooking of B’desh in 2017 for consumers) single location solar with Indian Oil

–Mundra SEZ (8481 1.6 GW ultra super-

oil brand ha) –Rated Investment plant Corporation with

critical thermal power Grade by Moody’s, operations in 9 cities

–India’s largest solar –Rated Investment project (COD 2022) –Quality

panel and cell S&P, Fitch Counterparties:

Grade by Moody’s,

manufacturer (1.2 GW S&P, Fitch SECI – 28%,

p.a.)

NTPC - 17%

Revenues EBITDA Revenues EBITDA Revenues EBITDA Revenues EBITDA Revenues EBITDA Revenues EBITDA

₹ 37,984 Cr ₹ 3,002 Cr ₹ 12,334 Cr ₹ 8,073 Cr ₹ 21,093 Cr ₹ 6,174 Cr ₹ 3,239 Cr ₹ 2,937 Cr ₹ 1,078 Cr ₹ 857 Cr ₹ 1309 Cr ₹374 Cr

Total Debt Total Assets Total Debt Total Assets Total Debt Total Assets Total Debt Total Assets Total Debt Total Assets Total Debt Total Assets

₹ 17,915 Cr ₹ 43,615 Cr ₹ 21,433 Cr ₹ 47,375 Cr ₹ 52,835 Cr ₹ 69,523 Cr ₹ 10,009 Cr ₹ 17,265 Cr ₹ 9,280 Cr ₹ 13,280 Cr ₹348 Cr ₹1,311 Cr

Market Cap: ₹ 14,776 Cr Market Cap: ₹ 76,731 Cr Market Cap: ₹ 7,039 Cr Market Cap: ₹ 16,634 Cr Market Cap: 4,337 Cr Listing Oct 2018

Operational

Massive Unmatched

excellence Track record of Experienced management

scale execution

Focus on integrating Expertise in regulatory

Largest in Greenfield assets

productivity, acquisitions environment in India

class in record time

lowest cost

Note 1: All the financials are from respective companies’ Annual Financial Statements dated 31 March 2018

2: Market cap is as of 18th June 2018 3: Mix as of March 31, 2018 6

Adani Group : Financial Snapshot* and Stock Price Movement

Revenue Total Net Worth

EBITDA Total Assets

15% CAGR

16,953 39,904 73,640 75,729 5,546 18,218 21,043 1,75,597 1,91,058 1,151 19,490 38,310 45,106

474 1,06,997

5,534

4% 4% 4% 4%

11% 11% 7% 6% 8% 3%

27% 14% 8% 13%

8% 8%

32% 28% 31% 2%

35% 51% 48%

41%

69% 29% 34% 65%

13% 16% 46% 47%

38% 25%

96%

81% 24% 25% 23%

37% 39%

52% 50% 49% 44% 39%

31% 34% 28% 35% 35%

28% 27%

17% 14%

FY 2007 FY 2012 FY 2017 FY 2018 FY 2007 FY 2012 FY 2017 FY 2018 FY 2007 FY 2012 FY 2017 FY 2018 FY 2007 FY 2012 FY 2017 FY 2018

AEL APSEZ APL ATL AGEL AEL APSEZ APL ATL AGEL AEL APSEZ APL ATL AGEL AEL APSEZ APL ATL AGEL

Stock Price Movement (%)

Adani Enterprises Adani Ports and SEZ Adani Power Adani Transmission

34%

133%

394%

16%

16%

16%

Oct-2016 Mar-2018 Oct-2016 Mar-2018 Oct-2016 Mar-2018 Oct-2016 Mar-2018

Adani Enterprises NIFTY 50 Adani Ports & SEZ NIFTY 50 Adani Power NIFTY 50 S&P BSE POWER Adani Transmission NIFTY 50

•

•

Includes listed Group Companies

Stock Price Movements are until 31-03-2018

7

Adani Enterprises: a Diversified Incubator

8

Thinking Big, Doing Better

Unique Incubator with a distinctive capability in nurturing businesses of national

importance creating value for all stakeholders

Massive Scale - Largest & best in class

Unmatched Execution - Greenfield assets in record time

Experienced Management Team - Expertise in regulatory environment in India

Operational Excellence - Focus on productivity, lowest cost

Delivered stupendous CAGR of 32% for 24 years (since listing)

9

Adani Enterprises : Evolution

2018

• Demerger of Adani Green Energy & Adani Gas

2010

• QIP of $ 850 mn

• Acquired Carmichael Coal Mine

• Won First Coal MDO contract

2007

• APSEZ IPO subscribed 116x

• FCCB Issue of $ 250 mn

2017

• Solar Mfg plant

2001 commissioned

• Adani Gas Started

2015

1996 • Demerger of APSEZ, APL & ATL

• Bonus Issue of 1 : 1

2009

• APL IPO subscribed 21x

• Bonus Issue of 1 : 1

2006

Nov-1994 listed on • Stock Split : Ratio 10 : 1

BSE & NSE @ Rs

150/share

Subscribed 25x 1999

• Signed JV with Wilmar, Singapore

• Bonus Issue of 1 : 1

10AEL: Corporate Structure

Promoters

75%

Adani Enterprises Limited

(AEL)

Coal MDO ICM **

(Division) (Division)

100% 100% 51% 50% 100%

AGL AWL

Adani Global MSPVL

(City Gas (Edible Oil & Others

Mauritius (Solar Mfg)

Distribution) Food)*

100% AALL/AAFL

100% 100%

(Agro Storage)

AGPTE AGFZE

Singapore Dubai 100% Defence

100%

Road, Metro &

100% 100% 100% 100%

Railways

AMPTY PTAG ASPL ABPL

Carmichael Bunyu Coal

Shipping Bunkering 100% Cement

Coal Mine Mine

(Singapore) (India)

(Australia) (Indonesia)

100%

Water

Consolidated Financials FY18 (₹ in Crs)

Parameter Total Coal MDO ICM AGL MSPVL AALL+AAFL Others AWL*

Revenue 37,984 863 29,454 1,309 554 314 5,406 26,435

Op. EBIDTA 3,002 466 1,261 374 328 100 473 1,010

* AWL financials shown are on 100% basis

** ICM – Integrated Coal Management 11Adani Enterprises : Exemplary Value Creation

EBIDTA Mix

AEL delivered CAGR of 32% since listing

1000000 FY2012 Others,

Vs 8%

Nifty CAGR of 9.3% & Sensex CAGR of 9.3% ICM, APSEZ,

28% 38%

100000 APL, 26%

FY2015

10000 Others,

ICM, 12% 6%

APSEZ,

31%

APL, 51%

1000

FY2018

100

ICM

9%

Coal MDO 13%

Solar Mfg 25%

Solar Gen

37%

10 CGD 11%

1995

1997

1998

1994

1996

1999

2002

2001

2007

2003

2005

2008

2014

2000

2004

2006

2009

2016

2010

2011

2012

2013

2015

2017

Others

5%

AEL Nifty Sensex

Note: Chart value in log scale rebased to 100

12Adani Enterprises : Experienced Management Team

Mr Gautam Adani, Chairman & Founder - Adani Group Mr Rajesh Adani, MD – Adani Enterprises Ltd

Mr Adani has more than 33 years of business He has been associated with Adani Group since its

experience. His journey has been marked by his inception. He is in charge of the operations of the

ambitious and entrepreneurial vision, coupled with Group and has been responsible for developing its

great vigour and hard work. This has not only enabled business relationships. His proactive, personalized

the Group to achieve numerous milestones but also approach to the business and competitive spirit has

resulted in creation of a robust business model which is helped towards the growth of the Group and its various

contributing towards building India. businesses.

Mr Pranav Adani, Director

Mr Vinay Prakash, CEO - Mining & ICM

He has been active in the group since 1999. He has

A mechanical engineer with MBA (finance), Mr. Vinay

spearheaded the Joint Venture with the Wilmar Group

Prakash has a rich and diversified experience of over 24

of Singapore and transformed it from a single refinery

years, spanning across the complete coal value chain,

edible oil business into a pan India Food Company. He

from Mining, Trading, Shipping & Logistics to Port &

also leads the Oil & Gas, City Gas Distribution & Agri

Power. He has been instrumental in nurturing our

Infrastructure businesses of the Group. His astute

trading & mining business & achieving multi-fold growth

understanding of the economic environment has helped

subsequently.

the group in scaling up the businesses multi fold.

Mr Rajeev Sharma, CEO – Adani Gas Ltd Mr T K Kannan, CEO – Adani Wilmar Ltd

Mr Sharma has over 38 years of focused experience in Mr Kannan has been active in the group since 1999. He

Oil & Gas industry especially natural gas pipelines and has about 40 years of experience in the Edible Oil

city gas distribution networks. He has been with Adani Sector. Out of which the last 20 years he has been with

since 2003 & responsible for Group’s initiatives in city Adani Wilmar Ltd working in Singapore & India. With his

gas distribution. He was associated with GAIL for 19 rich experience he has been handling the Edible Oil

years in various capacities. Mr Sharma was the business and Co-ordinating, Trading, Marketing &

founding MD of Indraprastha Gas Ltd and has Manufacturing since inception. Prior to joining Adani

implemented the prestigious CNG Program in Delhi. Wilmar, he worked 20 years for Godrej Soaps Ltd.

Mr Ramesh Nair, CEO – MSPVL (Solar Manufacturing) Mr Rajiv Nayar, CFO

Mr Nair has over 27 years of experience in the Mr Nayar joined the Adani Group in April 2016 after a

manufacturing industry. He has worked in Essar Steel 30 years career at Citigroup. At Citi, he had a broad

Limited, Sterlite Industries Limited as COO Sterlite based experience in both developed and emerging

Copper and Director - MALCO and Jindal Stainless markets in India, London and Hong Kong across various

Limited as President & Executive Director. Before disciplines including Corporate Banking, Project

joining Adani Solar, he was the CEO and whole time Finance, Leveraged and Acquisition Finance, Capital

Director of Bharat Aluminium Company Limited (BALCO) Markets as well as Risk and Portfolio Management.

for the last 4 years.

13Adani Enterprises : Consolidated Historical Financials

AEL FY 16 FY 17 FY 18 Value creation

35,131 38,056 37,984 • Demerger of AGEL, renewables vertical

Revenue

• Listed in June 2018

EBITDA 2,789 3,090 3,002

• Demerger of AGL, city gas distribution vertical

PAT 1,009 988 870 • Listing in 2H FY 19

Basic and Diluted EPS (in ₹) 9.19 8.98 6.89

Net Fixed Assets (NFA) 18,135 21,399 16,081

Expansion of existing businesses

Total Assets 41,756 47,689 43,615

• Enhancing nationwide footprint in Agro and

Total Long Term (LT) Debt 8,163 10,166 5,072

Coal MDO through organic route

Total Debt 19,169 20,846 16,990

• Acquisition of Ruchi Soya, one of the largest

Total Net Worth (TNW) 13,463 14,698 15,588 edible oil producers in India, by Adani Wilmar,

EBITDA / Interest 2.1x 2.5x 2.3x

Total LT Debt / EBIDTA 2.9x 3.3x 1.7x Highly successful incubator

Total LT Debt / TNW 0.6x 0.7x 0.3x • Unparalleled track record of transforming

Total Debt / EBITDA 6.9x 6.7x 5.7x businesses from challenging gestation to

1.4x 1.4x 1.1x robust independence

Total Debt / TNW

• Venture into new businesses such as

Note 1: Excludes Adani Wilmar (50% JV) now consolidated as per equity method per IndAS. defence, roads, cement and water

Note 2: FY18 figures exclude AGEL

Note: 1. Per Indian Accounting Standard (IndAS) 2. Note: EBITDA = PBT + Depreciation + Net Finance Costs 3. Debt figures exclude Intra-Group Borrowings

14AEL: India Coal – Coal MDO & ICM

1

5Global Coal: Demand to remain stable, with India contributing significantly towards

imports & Australia towards exports

India net imports, Australia net exports to be the highest

-38

-67

+40

~+95 +69

+21

-67

-3

+130

India thermal coal imports by country

Seaborne Thermal

Coal Market 2017 2035

1062

/ Net exports/ imports in 2035 over 2017 levels

29%

945 44% 42%

51%

5% 29%

2017 2035

Coal Volumes (Mt) Indonesia Australia Others

Source: Wood Mackenzie

16Global Coal Scenario – Stable Outlook

Global coal demand flat lines, with falls in China and OECD offset by increases in India and other Asia

2,500 Million toe Coal Consumption by Region 5.0% Coal Consumption Growth and Regional Contributors

4.0%

2,000 China India OECD Other Asia Other

3.0%

1,500 2.0%

1.0%

1,000

0.0%

500

-1.0%

- -2.0%

2000 2010 2015 2020 2030 2040 2000-2010 2010-2020 2020-2030 2030-2040

China India OECD Other Emerging Asia RoW

Source: BP Statistical Review Source: BP Statistical Review

Decline in exports from Indonesia to be offset by exports from Australia With thermal coal prices projected to remain stable

1,600 Thermal coal price nominal estimate(US$/t)

120

500 96

1,200 100

87 86

457 80 82

76 78

429 80

Rest of World

800

416 Indonesia

60

397

Australia

316

40

400

550 20

399 450

0 0

2015 2025 2040 2017 2018E 2019E 2020E 2021E 2022E 2023E

Source: International Energy Outlook, 2017 Source: Bloomberg, JP Morgan Estimates

17Evolution of Indian Coal Mining & Opportunities

Amendment to Coal Mines Nationalization Act •Allowed private sector participation in coal mining for captive usage

(1973), 1991 •Case to case basis allotment of 218 coal blocks

Auction by Competitive Bidding of Coal Mines •Additional regionally-explored (RE) coal blocks allocated to various PSUs - 14 for Power

Rules, 2012 end use & 3 for commercial mining

•Various complaints were received by the Govt.

CAG Report, 2012 & SC Judgement in 2014

•Arbitrary and non transparent allotment led to cancellation of 204 coal blocks out of 218

•Re-Allocation of the coal blocks; 2- pronged strategy

Coal Mines Special Provisions Act, 2015

•Auction for Private & Allocation for PSUs - either for captive or commercial use

•MoC has opened commercial mining for private sector under Act’ 2015

Way Forward

•Methodology for auction published on Feb 27, 2018 and tender process expected soon

Captive mines portfolio including CIL’s mines for potential MDO business shown below

Category No. of Coal Blocks Category No. of Blocks

Allocation/Auction under Coal Mines Act 204 Allocation & Auction 86

Category No. of Coal ~52 Bn Ton

2015

To Allocate/ Auction Blocks

118

Allocation under CMN Act 1973 14 Pakri Barwadih, Tasra 2

Category No. of Coal ~7 Bn Ton

UMPP Linked Block Blocks12

Sub Total (Coal Blocks) 218

PSUs – Power; allocated 10

Allocation under Mining Rules 2012 ~9 Bn Ton

17

PSUs- Power; cancelled 4

Category No. of Coal

CIL Coal Block for MDO 3 Commercial Mining Blocks 3

~2 Bn Ton

Grand Total 238 Kaniha , Siarmal, Pelma 2

70 Billion Ton

18Demand Drivers for Thermal Coal in India

Share of Thermal Power to go down to 51% in next 5 years, although expected to increase in absolute terms

2016-17 2022-23

Coal

8% Large Hydro

2% 2%6%

4%

Small Hydro 13%

10% & Bio Mass

Wind Power

4% 326 GW 472 GW 51%

Solar Power 13%

59%

13% Nuclear 4%

Gas & Diesel 12%

Coal based thermal power capacity @ 240 GW by FY 2023

240000

220000

200000

Additions Capacity

MW

180000

160000

140000

120000

FY 17 FY 23

Coal based power capacity expected to increase from 204 GW in FY 2018 to 240 GW in FY 2023

Power generation expected to increase at rate of 6 to 7 % for next 5 years

Source: Ministry of Power, Adani Estimates 19Domestic Coal Production

CIL Total Coal Production (Mn Ton) SCCL Total Coal Production (Mn Ton)

800 762 90 84

CAGR: 721 CAGR: 79

750

726 80 75 80

700

Base—4.6%, 683 Base—4.5%, 71 76

694 68 73

Pessimistic-3.6%, 646

664 70 Pessimistic---3.5%, 64 70 76

650 612 634 692 67 74

Optimistic---5.6%, 668 Optimistic---5.5%, 64 71

579 606 69

600 645 60 60 61 66

622 64

579

550 554 579 600 52 53

50

53

538 50

500 493

40

450 452 462

436

400 30

CIL- Base CIL- Pessimistic CIL- Optimistic SCCL - Base SCCL - Pessimistic SCCL - Optimistic

210 Captive & Others Coal Production (Mn Ton) MoC has auctioned/allocated 94 captive coal blocks

191

180 under CMN* Act 1973, CMSP Act 2015, CBR 2012

172

147

150

152 Production started in 13 auctioned/allocated coal blocks

111 132

120

80 100 117 Production forecasted to reach 172 MT by FY23 based on

90

63 59

52 51 53 72 89 possible opening of new mines and ramp up

60 40 44 46

53 64

46

30 46 47

FY-12 FY-13 FY-14 FY-15 FY-16 FY-17 FY-18 FY-19FY-20 FY-21 FY-22 FY-23

Optimistic Base @90% Pessimistic@80%

FY-15 FY-16 FY-17 FY-18 FY-19 FY-20 FY-21 FY-22 FY-23

Peak MTPA 115 53 68 73 106 143 206 256 308

• CMN Act : Coal Mines Nationalization Act, 1973

Source: Ministry of Coal, Market reports, Adani Analysis • CMSP : Coal Mines Special Provisions Act, 2015 20

• CBR 2012 : Competitive Bidding of Coal Mine Rules, 2012Demand Supply of Thermal Coal

MMT Supply Total Demand

1200 1117

1050

988

1000 930

852 886

828 843

783

800 733

647 686

597 625

600

400

200

0

FY-17 FY-18 FY-19 FY-20 FY-21 FY-22 FY-23

Imports over the next 5 years likely to be range bound between 140 to 160 MMT

(MMT) 2016-17 2017-18 2018-19 2019-20 2020-21 2021-22 2022-23 CAGR (18 to 23)

Total Demand 828 852 886 930 988 1050 1117 5.6%

% Increase 3.05% 2.94% 3.99% 4.97% 6.24% 6.28% 6.38%

Total Supply

597 625 647 686 733 783 843 6.2%

(Pessimistic)

% Increase 3.3% 4.6% 3.5% 6.02% 6.8% 7.09% 7.5%

Total Supply (Base) 597 625 659 706 763 825 897 7.5%

% Increase 3.3% 4.7% 6.4% 7.4% 8.54% 8.25% 8.9%

Imports may go beyond the range based on how CIL & captive performs, removal of infrastructure bottlenecks

including railways !!

21Adani India Mining: Introduction

Largest Mine Developer & Operator in India

• Exploration

Parsa East and Kanta Basan,

Peak Capacity 15 MMTPA • Preparation of GR, Mine Plan

• Land Acquisition, R&R

Kente Extension

Peak Capacity – 7 MMTPA • Obtaining Clearance

• Establishment of washery & reject based TPP

Parsa,

Peak Capacity – 5 MMTPA (if applicable)

• Planning, Developing & Operations

Jitpur, • Operation of mine

Peak Capacity – 2.5 MMTPA

• Logistics solution

Talabira II & III

Peak Capacity – 20 MMTPA

Gere Pelma-III

Peak Capacity – 5 MMTPA

• Average Potential mine life: 30 years

• Estimated direct employment to 3200 persons

Operational Under Development

Map Source: http://clipground.com/clipart-maps-of-india.html MMTPA: Million Metric Tons/ Annum 22MDO Business Model & Project Pipeline

Mine Owner Packages wherever applicable basis

Payments to MDO Coal Delivery by MDO

Facilitating in obtaining clearances, DPR / mine plan, Land

Mine Developer acquisition and R&R

and Operator

(MDO) Construction of Infra such as CHP, Washery, rail siding etc.

Bundled

Coal & OB Removal Package

Coal Loading & Transport

MDO to do all Investments as per

Scope of Work of which some O&M of Washery & Disposal of rejects

part are reimbursable

O&M of railway siding

Major risks are transferred to one contractor- Ease in Contract Management

Parsa East & Kente Gare Pelma Talabira II

Parsa Gare Pelma -II Jitpur Total

Kante Basan Extension -III & III

Owner RRVUNL RRVUNL RRVUNL CSPGCL Mahagenco NLC APL 7 Contract

Geological

516 256 200 210 736 589 81 2588

Reserves (MnT)

Mineable

451 184 160 (Est) 134 553 554 66 2102

Reserves (MnT)

Capacity

15 5 7 (Est) 5 23.6 20 4 80

(MTPA)

Status of Producing Start in Start in Start in Start in Start in

Start in 2019

Production since 2013 2021 2018 2021 2019 2020

Adani Role MDO MDO MDO MDO MDO MDO Captive

CMDPA

Contract Status Signed Signed Signed Signed LoA awaited LOA issued

signed

23Why we entered into MDO? - a natural progression from Coal Trading

Successfully developed Power

projects and Ports in India –

Gained experience in LA,

Community engagement, infra

development- critical for Coal

mining as well

Mining in Indonesia since 2007- Our presence in Coal Trading

Built credence to venture in business with PSUs, SEBs –

Indian mining industry after a Built strong relationship with

taste of success in foreign soil PSUs

Adani entered in

Indian Mining

MDO Business in

2008 - with

RVUNL

24PEKB Project - World class infrastructure developed within a record time

Infrastructure consisting Pit top railway siding, silo

Mining Operation Started in Jan 2013

with Rapid Loading system for evacuation of coal

Coal Production commenced in Feb 2013 is under final completion

Mining operations started within record time of 5 Strong EBIDTA Margins & Profitability with stable

cash inflows and robust financial indicator

years from the date of allocation of coal block

In-house expert team of Geologists and Mining

Engineers

8.27 8.33

More than 25 MMT coal produced since the start

6.3

of mine

Peak Mining capacity as per approved plan - 15 3.44

MMTPA

Developed world class coal washery and CHP

FY 15 FY 16 FY 17 FY 18

ROM Production (MMT)

PEKB mine - a model project - it is vertically integrated through private rail corridor (SRCPL) to provide last mile

delivery of coal at TPS

PEKB – Parsa East & Kante Basin 25Competitor Landscape

Turnover (Rs.Cr) Financial Position of Competitors FY16-17 Networth (Rs.Cr)

10000 JSPL* 10000

Jaypee Power

9000 Adani 9000

Turnover Networth Essel

8000 8000

7000 Less 7000

6000 Aggressive 6000

Dilip Buildcon Competitors

5000 Most Aggressive Competitors 5000

Adani

4000 Sadhbhav 4000

Jaypee Power

3000 3000

Monte Carlo BGR Lanco Sadhbhav

2000 Sainik 2000

VPR AMR Dilip Buildcon

1000 Ambey Sical Essel 1000

Southwest Thriveni

Lanco

0 Dhansar 0

Mahalaxmi

Single Mine with Highest Mineral Production in one

Mineral (Mn Year From FY11-FY17 Mineral+OB

35 Ton) (Mn Cum) 70 80

Mineral (LHS)

30 60

25 50 MDO for Coal/Lignite/Iron Ore

20 40

15 30

10 20

5 10

0 0

Dhansar

Sainik

AMR

JSPL

VPR

Essel

Mahalaxmi

Sadhbhav

PT Darma

Southwest

Monte Carlo

Sical

Adani

Ambey

BGR

Jaypee Power

Thriveni

Indonesian

Company

* JSPL : Turnover - Rs. 15494 Cr. ; Networth – Rs. 21675 Cr. Source: Adani Analysis, Company Reports

26Robust operations driving strong financial performance

8.27 8.33

7.31 7.1

6.3

5.5

3.44

2.95

1.2 0.96

FY 14 FY 15 FY 16 FY 17 FY 18 FY 14 FY 15 FY 16 FY 17 FY 18

ROM Production (MMT) Washed Coal Dispatch (MMT)

61%

56%

54%

47%

956 579

863

466

570 23% 322

286

135

77

18

FY 14 FY 15 FY 16 FY 17 FY 18 FY 14 FY 15 FY 16 FY 17 FY 18

Revenue (in ₹ Cr) EBITDA (in ₹ Cr) Margin

27Integrated Coal Management: Our Global Footprint…

Multi-Country Multi modal Customer Account

Financing Management

Procurement Logistics

ICM

Private Adani Power Overseas

PSU

Business Ltd business Yamunagar

Suratgarh Panipat

Hissar Harduaganj

Dadri Tanda Vindyachal

Kota Unchahar Kahalgaon

Badarpur

Parichha Sagardighi

Chhabra Rihand

Dhamra Bakreshwar

Kandla Mejia Bandel

Panki Durgapur

Wanabori

Mundra Kolaghat

Gandhinagar Sipat

Bedi Haldia Tarakan

Navlakhi Korba [Talcher]

Samarinda Tanjung Bara

Dahej Tiroda

Koradi Bontang

Paradip

Hazira Chanderpur

Parli

Ramagundam Vishakhaptnam Muara Satui

TanjungIndonesia

Simhadri

Kondapalli Gangavaram Pemancingan

Kakinada

Richard Bay

Goa

South Africa

Queensland

Ennore

North Chennai Australia

Mettur Tuticorin

Ports

Locations served

Tuticorin

We are a team of 200 + People with operations spread across globe through more than 20 satellite offices & branch

offices, 4 global offices and a HO based out of Gurgaon

28AEL: Integrated Coal Management – Amongst World’s leading & India’s largest

Resilient Business Model with Dominant Market Position Sales Mix

In MMT FY 18

7%

31% 48% 56% 45%

22% SEBs

66 MMT APL

78 81

185 66 Exports

58 164

145 147

63% Private/Others

8%

FY15 FY16 FY17 FY18

AEL Coal Trading Volume India Steam Coal Import

Stable Operating Performance Realizations on an uptrend

in ₹ Crs. In $/ MT

Revenue EBIDTA

27,446 30,232 29,454 66.61

55.71

52.52

967 998 1,261

2.85

1.85 1.84

FY 16 FY 17 FY 18

Revenue / MT EBITDA / MT

FY16 FY17 FY18

29AEL: Adani Gas –

City Gas Distribution

www.adanigas.com

30Natural Gas – A Low Cost, Clean & Efficient Source of Energy

Abundance Availability Affordability

Acceptability

Gas Value Increasing Expanding Price decline,

Less polluting,

Proposition Liquefaction Imports / commoditized,

clean and green

capacity infrastructure fungible

Global Gas export capacity increasing 50% between 2016-20 Infrastructure around natural gas import is accelerating

425 398

400 374 80 73

375

350 328 60 53

325 44

299

300 40 28

265 24

275 245 248

241 16

250 20

225

200 0

13 14 15 16 17e 18e 19e 20e China LNG (MMTPA) India LNG (MMTPA) India Pipeline ('000 KM)

mtpa FY 16 FY 20E

Poor air quality in cities supporting gas adoption Gas is cheaper than oil linked fuel

$/MMBTU

Oil Linked Fuels

Gas Price

Iran 3

Nigeria 11.3 10.8

5

Pakistan 5 8.7

7.6 7.1

B'desh 6 6.3

Saudi Arabia 6 No of Cities 3.7

2.7

China 16

India 31

0 10 20 30 40

World’s 100 cities with worst Air Quality

From a fragmented and regional market, natural gas now a global commodity. Supply is driven by new discoveries and demand

by rapid infrastructure development

31India belatedly catching up on the Natural Gas

Environmental commitments, “Make in India” initiative, need for energy security makes natural gas a priority

Lower Gas Consumption per Capita (Cbm/person) India Contracted and Uncontracted LNG Demand

30,630 21,449

2,367 1,678

253 152

80

UAE Qatar United Thailand Bangladesh China India

States

Gas as % of primary energy consumption declining National Priorities

60 61 • Paris agreement requires 35% reduction in CO2 over 2005 level

51 49 49 50

46

40 42

32

36 37

• Reduce oil import 10% by 2020

28 30

26 26

9 10 10 10 • Balance energy mix- gas 6% to 15%, by 2022

8 7 7 8 8 8 8 8 8 7 7 6 6

2000 2002 2004 2006 2008 2010 2012 2014 2016

• 100% LPG/PNG penetration

Gas as % of Primary energy Prmary Energy Gas Consumption

India has lagged, but given the global glut, this might be a advantage with significant uncontracted demand.

Gas and Renewables together serves the twin purpose of climate and growth

32City Gas Distribution (CGD) infrastructure generates demand

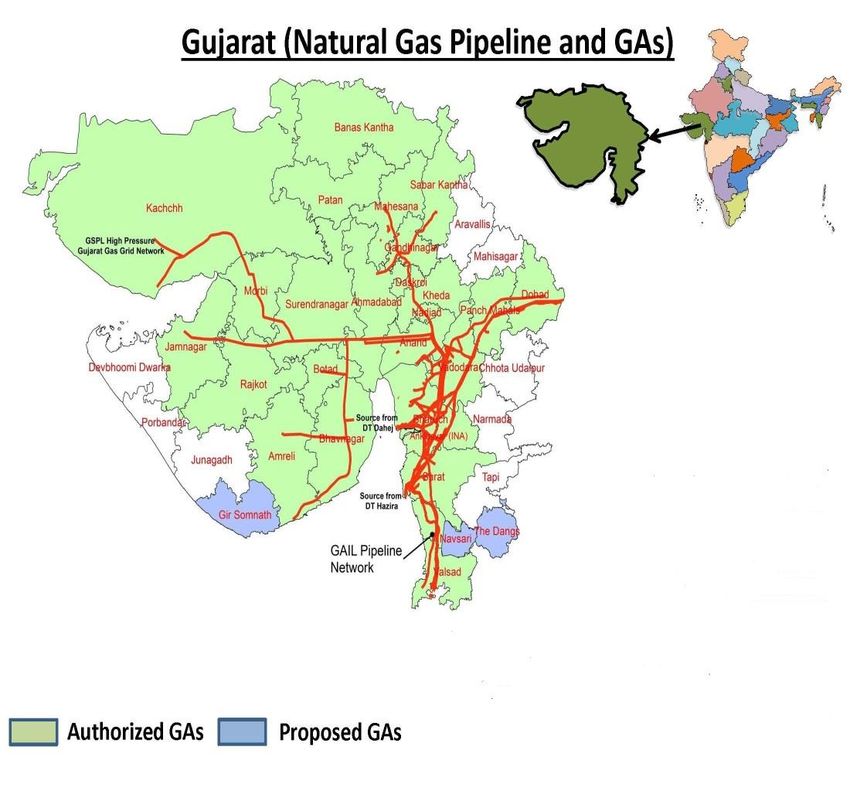

China Gujarat

Gas consumption increased 4 times compare to India Highest CGD penetration and gas has 25% share in energy mix

LNG as transport fuel picked up due to LNG infrastructure compare to national average of 6%

Gas demand India Vs China (In BNSCMD)

India China

188

200 172

151

Gas Consumption

137

150

111

93

84

100 73

59

48

35 41

50 30

71

60 61

51 49 49

36 37 40 42

28 30 32

-

FY 02 FY 04 FY 06 FY 08 FY 10 FY 12 FY 14

China LNG as auto fuel demand rising as fueling station increasing

200 2800 3000

2667

180

Heavy Duty trucks('000)

2230 2500

160

140 1824

2000 LNG Station (Nos)

120

100 1500

175

80

777 137 1000

60 124

40 304 74 500

203

20 101

14 17 22 38

0 0

FY 09 FY 10 FY 11 FY 12 FY 13 FY 14 FY 15 FY 16

Heavy duty Trucks ('000) LNG station (in Nos)

Consensus at political & judicial level to replicate Gujarat model , i.e. to increase gas share to 25%

33Massive Infrastructure Investment in Oil & Gas sector is underway

Carrier first- Commodity latter. Infrastructure will unblock latent demand.

Ongoing Infrastructure Investment

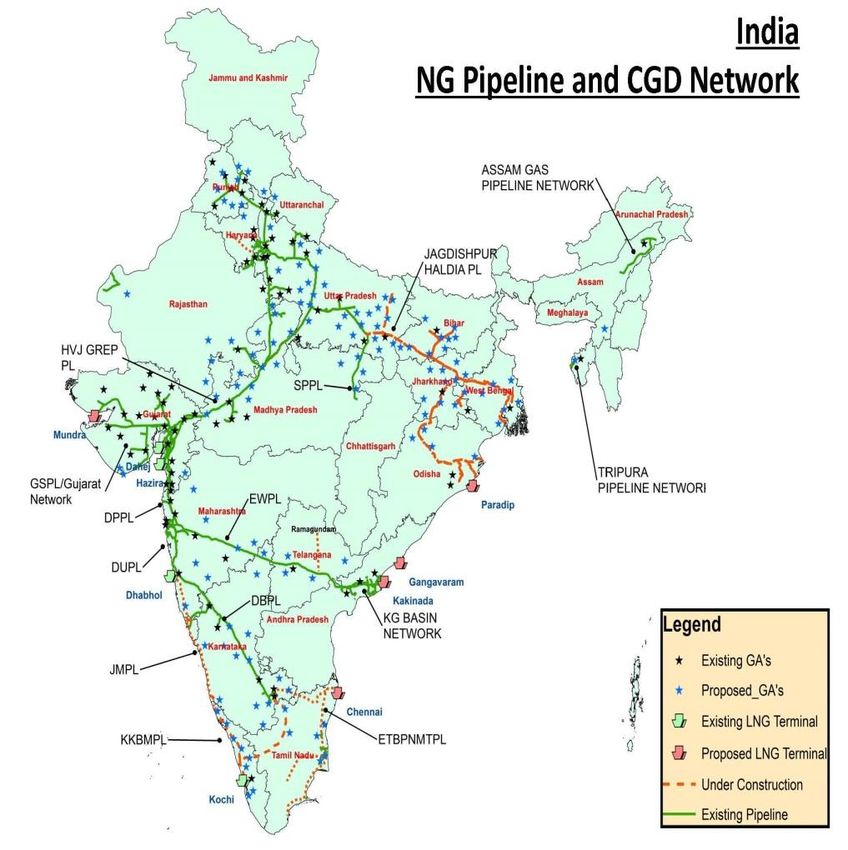

India Gas Pipeline and CGD Network

• LNG terminals from 4 to 11; 6 under construction, 2

terminal from group company

• Pipeline network of 16000 kms extended by

13000kms work is started on most of stretches

• City Gas Distribution from 78 to 250 cities by 2020,

bids for 150 cities are likely by March 2018.

• Incentives to explore and extract gas, 1st round

under OLAP/HELP is going on.

• Small oil field 1st round concluded and second

round by May 2018.

Blue star denotes proposed 146 GA for CGD bidding

About $23bn will be spent in the next 5 years to build oil & natural gas infrastructure.

Approx. $1 bn VGF has been granted to GAIL to build pipeline infrastructure with likely unbundling

34Indian CGD is ready for next growth cycle

CGD to provide base load to Gas Economy. Government is aggressively pushing Compressed Natural Gas and Piped Natural Gas

Growth Drivers

India Gas Demand is Increasing

252

500

219 • 120 districts have high pollution levels

190

400 167

150 • Stringent emission norms. SC suggestion to ban Fuel Oil &

MMSCMD

300 Petcoke on pan India basis

191 206

157 173

200 134

0 131

0 139

0 146

121

0 117

0 • Coverage to increase to 322 cities (total >700 districts)

100

• Favourable regulatory support for CGD

0

FY 12 FY 13 FY 14 FY 15 FY 16 FY 17 FY 18 FY 19 FY 20 FY 21

• Tax arbitrage between liquid fuel and Gas

Normalised Demand Bull Case

• Energy security by balances energy mix

CGD demand adequately covered by domestic production • Industrial automation supports gas as fuel

38%

140 40%

35% • Domestic production of natural gas is rising and expected to

120 35% grow considerably

31%

100 29%

30%

80

26% • Fuel Oil production declining at refineries

21% 25%

60 111

97

17%

19%

100 103 108

20%

• Absolute constrain on LPG production and Import

92 88 87 91

40 infrastructure

14%

20 41 15%

27 31 36

15 16 17 18 22

0 10% • Highway, Inter city traffic, MHV, 2W will drive demand

FY 13 FY 14 FY 15 FY 16 FY 17 FY 18 FY 19 FY 20 FY 21

• Urbanisation and High rise building supports CGD

India CGD Demand Domestic Productiom

CGD as % of Domestic Production

CGD will have wider political patronage due to its wider, small consumption intensity (Household, passenger vehicles, small

enterprises)

35Natural Gas: Clean Fuel for Swachh Bharat (Clean India)

Fuel for urban India, clean India, digital India, GST compliant India

CNG has significant price advantage over Petrol Khurja- Case Study

INR/ ltr energy equalized

80.00 Demonetization, GST roll out and environmental pressure changing the

70.00 fuel landscape.

60.00

33.44 Small town about 100 Km from Delhi is famous for ceramics art work. 150

50.00

units making hand crafted pottery and ceramic work.

40.00 14.83

9.06

30.00 11.78 Unorganized sector, avoided using natural gas which leaves a trail and can

20.00 reveal financial data.

29.22

10.00 22.64

- Used all kinds of fuels – Furnace Oil, PetCoke, Kerosene, Rubber/Tyre Oil,

Petrol CNG as emission monitoring not a deterrent

Brent/ Gas S&D Cost/ Margins Taxes

The tri–combination of Demonetization, GST and SC’s decision to ban

Furnace Oil, PetCoke has proved to be a game changer for fuel mix.

Natural Gas Vehicle Penetration is low and will increase

India 1% November 2016 our total PNG sale in Industrial segment at Khurja was

2000 SCMD.

Thailand 1%

China 2%

December 2017 sales, increased to 16000 SCMD, registering 8 fold growth

Brazil 2%

Egypt 3%

FY 19 will reach 80000 SCMD, growth of 4000% in 2 year expecting 100%

Banglade… 11% units on Natural Gas.

Iran 15%

Pakistan 33% Industry is happy with ease of use with gas: saving space/ easy to handle/

on tap/ pay after use/ safe and reliable. It has improve the product quality.

0% 10% 20% 30% 40%

NGVs as % of total vehicle population

Apart from less polluting and ease of operation, Natural Gas will continue to have significant competitive advantage over

liquid fuel

36Regulatory Framework, Policy Landscape

Regulator Framework Pricing Mechanism Recent Policy Impetus

• No regulatory control on Sales Price

• Allocation of domestic gas for household

Petroleum and Natural Gas Regulatory

Board • Sales price are benchmarked to alternate

and transportation segment

fuel in each segment

• Public Utility status to CGD

Asks for bids for Municipal areas based • Natural Gas will have clean and Green

upon premium over alternative fuel • CGD eligible for funding from infra cess

• Network Tariff-20% • Prices are more stable and less volatile • LNG approved as fuel for highway

• No. of Domestic Connection-50% than liquid fuel

• No. of CNG Outlets-20% transportation

• Inch KM of Pipeline-10% Gas Supply Mechanism

• Natural gas is likely Ito be included in GST

• Government allocates gas for CNG &

• Push for LPG penetration in rural area

domestic use

• Strong entry barriers by regulation-

Awards 25 years concession • Gas for other segments bought from open

market exclusivity

• Awardee to build the urban

network • Sourcing is fair mix of short term and spot • Ban on Fuel Oil in NCR and SC suggestion

o Network exclusivity for 25 yrs

o Marketing exclusivity for 5 yrs contracts

to ban pan India

expected to increase to 8 year

• Term prices are benchmarked to Brent

• Massive infrastructure in oil & Gas

• No regulation around marketing crude

margin

• Main suppliers are GAIL, GSPC, IOCL • Likely unbundling of GAIL

In essence, Utility Business with a market economy flavour - largely unregulated

* Compressed Natural Gas 37Adani Gas Expanding CGD Network

AGL is directly operating in 4 cities and added 9 cities in recent bidding rounds through IOCL JV, All 9 cities to be operational by 2021

Chandigarh AGL along with JV to expand footprint

Udham Singh Nagar Network by FY21 ADANI GAS IOAGPL

Panipat

Bulandshahr Cities 4 9

Faridabad

Khurja Infrastructure

-Steel Pipeline KM 500 750

Ahmedabad -PE Pipeline KM 6,000 5000

Allahabad Customer No.

-Industrial 1,500 750

-Household 4,00,000 2,50,000

Vadodara -Commercial 3,000 1,000

Daman

CNG Outlets No. 100 75

Dharwad

South Goa Gas Volume

MMSCMD 1.75 1.5

Adani Gas

Ernakulum IOAGPL Aspirations to add more cities to portfolio in upcoming

bidding rounds

Largest private sector CGD. Well positioned to expand the network

38The JV with IOCL: Public sector pedigree with private sector expertise

Petronet LNG, IGL with 50% private ownership are success stories in Indian gas sector, IOAGPL to replicate and exceed the

same in CGD JV will have private sector character

Domain Expertise Infrastructure

• Processes Logistics & resources

• Manpower Borrowing Capacity

• Strong commitment of promoters

• Promoters has stake in 5 upcoming LNG terminal

• Economics of scale will allow

• Continued cost leadership

• Competitive sourcing of gas, IOC is importing LNG

• With IOC good support at government/ regulatory levels

• Easy access to ready marketing infra of IOCL, 25000 retail outlets

• Strong credit rating of promoters

• Ability to hire talent

• Easy to scale on technology platform developed by AGL

• Strong safety practices adopted at AGL

IOAGPL is in perfect position to participate in growth driven by new geographies and intensify growth within developed

cities

39Adani Gas – Key growth drivers

Intensifying the growth within same and new geography, increasing PNG penetration in each segment

Replicating the AGL learnings at JV

CNG Household Industrial/Commercial LNG

• Existing User- additional • Building with infrastructure-

mileage • Linked with Economic growth • Long distance fixed route

current penetration < 50%

• Inbound from other GA highway vehicle

• Outbound to other GA • New Industrial clusters

• New Building, under

• New User construction building- 100% • Industries not connected with

• New CNG car buyers • NCR- as much coverage Pipelines

penetration from day-1

• New CNG conversion

• New Segment • Outer Faridabad • CNG for cities closer to LNG

• Pubic building, Defense, PSU

• Commercial MHV colony, Auda terminal not yet authorized

• Cab aggregators

• Existing user of other CGD • Heating application current user

• boarder area base around 30%

Strategy Strategy Strategy Strategy

• Zero waiting at outlet • Customer Ease • On demand connection • Early mover

• Spot Billing

• Targeted marketing and • Prepaid meters • EMI for upfront cost • Pilot type projects

awareness

• Targeted marketing and • Targeted marketing and

• Strategic positioning of new awareness awareness

outlets

• Safety awareness • Safety awareness

CGD is in resurgence mode and ready for next round of growth, likely to have higher growth compared to peers

40Adani Gas customer base is well spread out across segment and cities

Pure play CGD company with 10 year of operational track record

Segment Wise Volume City wise Volume

Comm VAD KHJ

The Differentiators

3% 6% 2%

Dom

7% • Balanced product segment mix

FBD

28% • Wide customer base

Ind CNG

37% 53% AHD

64%

• No single entity greater than 2% of revenue

• Cost leadership – Lowest operating cost in the industry

• Under penetrated market in Gujarat and NCR

Gujarat segment Volume NCR segment wise Volume

Comm

• Management Depth

Comm Dom 1%

Dom 4% 3%

9% • Strong Brand

• Technology driven only CGD company to have SCADA

CNG Ind CNG

53% 44% 52%

Ind

34% based operation

• Evolving SCM integration with new terminals

Well established player, competitive advantage from low operating cost, scale advantage for new cities

41Adani Gas: De-Merger

Adani Gas Limited (AGL) operates the CGD business and is currently 100% subsidiary of AEL

• AGL is operating in 4 cities and its 50: 50 joint venture with Indian Oil Corporation

Largest Private Sector CGD

Limited, has been authorised for 9 cities.

player in India with significant

• CGD is end customer facing business, listing of AGL will provide AGL with brand

growth opportunities

awareness for future growth

• AGL will be a pure play gas marketing and distribution company.

Focused Pure Play Gas

• All the CGD assets will be housed under AGL

Marketing and Distribution

• Focused management team to capture emerging opportunity in Gas as Green Fuel

• Unlocks value of CGD business currently embedded in the value of AEL

Shareholder Value Unlocking • Shareholders to get direct exposure to high growth CGD business of AGL, removing any

holding company discount

Post demerger, AGL is to list on stock exchanges tentatively by end of H1FY19

42Resilient operations resulting into robust financial performance

Strong Operational Matrix

Volume in MMSCMD Gross Margin INR per SCM Gross Margin in % & INR/Crs)

800 50%

25

CAGR 10.1 700 45%

1.50 9.6 9.7

1.3 37% 38%

40%

20 8.5 600

1.1 1.1 33%

1.20 1.1 1.0 35%

500 25%

15 30%

0.63 6.0

0.90 11.09 12.34

0.57 0.51 11.80 400 178 25%

0.52 0.47

11.81 16% 133 20%

10 300 132

0.60 94

7.53 15%

200 93

0.30 0.61 0.68 5 306 10%

0.55 0.56 0.57 7.69 7.73 240 232 261

7.11 100

4.47 4.96 152 5%

- 0 - 0%

FY 14 FY 15 FY 16 FY 17 FY 18 FY 14 FY 15 FY 16 FY 17 FY 18 FY 14 FY 15 FY 16 FY 17 FY 18

CNG PNG PNG CNG CNG

Robust Financial Performance

Operating EBIDTA INR per SCM / Free Cash Flow INR/Crs. ROCE (%)

EBIDTA Margin in %

9 35%

7.6

8 49 21%

6.9 6.9

7 30% 19% 18%

5.8 16%

6 30% 29% 12 33 140

40

25%

5 4.1 26% 125

30 11%

4 0 78

20%

3 18%

50

2 15% 128 96 152

1

11%

79 178

0 10%

FY 14 FY 15 FY 16 FY 17 FY 18 FY 14 FY 15 FY 16 FY 17 FY 18 FY 14 FY 15 FY 16 FY 17 FY 18

EBIDTA (Per SCM) FCF (Post Capex) ROCE

43Key Investment Highlights

Natural gas has become a major source of clean fuel based energy across the world with heavy investment in

production, transportation and distribution infrastructure

Lower cost and cleaner than other fossil fuels

India has lagged; however now serious efforts to catch up: $23bn earmarked

Exponential multiyear growth expected

Adani Gas is the largest private sector player – well positioned to take advantage of this growth

Cost leader, strong balance sheet and superior execution capability should help in building pan India CGD

infrastructure

44AEL: Adani Wilmar – Edible Oil & Food www.farmpik.com

Edible Oil Industry in India

• India consumes almost 21 MMT edible oil every year

• Consumption of edible oil growing @ CAGR of approx. 4%

• India is the third largest consumer of edible oils (12% of global consumption), after China and the EU

• Every increase in income translates to a rise in demand for food products including cooking oil.

• Consumption-driven demand growth has outstripped domestic supply growth, increasing the country's import dependence to nearly 60%.

46Indian Edible Oil Consumption Growth Drivers

One of the lowest per capita oil consumption (in kg) Market Dynamics

70

61.1 63.9 63.9 63.6

59.7 • Exponential increase in consumption driven by rising

60 62.4 62.8 64.2

59.5 60.1 income levels and aspiration.

50

43.8 43.8

40 39.6 39.7 41.2

• Imports which constituted 3% in late nineties of

30 overall consumption now at 70%.

25.1 25.7 26.2 26.4 26.6

20

15.4 15.8 16.7 17.4

14.9

10 • Per capita consumption to rise to about 23kg by 2025

with a growth likely to be around 4%.

0

2011-12 2012-13 2013-14 2014-15 2015-16

EU USA China Brazil India • Indian oilseed production stagnating and not likely to

grow – fueling growth of Imports

Consumption to grow manifold

35

30 • Lowest Per Capita Consumption (Kg) of Edible Oil in

30 26 India – Huge potential to grow.

25 23

20 20

20 17

15 • 50% of consumption still catered by unorganized

10 sector- Huge potential for consumer pack business.

5

0

• Demand not constraint - Supply is abundant.

2015-16 2020-21 2024-25

Per Capita (In Kg) Demand (MMT)

47Adani Wilmar: Strong Growth through Brand across Food segments

Edible Oil and Food Business Dominant Market Share

(as at March-18)

19%

14%

5% 4% 4%

Basket of Brands for Edible Oil & Food Products

• Refineries spread across India to cater the geographies Haldia-

(North East), Mundra-(West) Mangalore, Kakinada&

Krishnapatnam- (South).

• Crushing Units located in the proximity to seed cultivating areas-

Mantralayam –Sunflower Seed, Neemuch, Chindwara, Shujalpur

(M.P.) , Bundi (Rajasthan) & Nagpur (Maharashtra)-Soya Seed,

Alwar & Bundi (Rajasthan)-Mustard Seed.

• Job work units spread across India to cater the local markets.

48Business Model & Strategy

Journey so far….

• Set up first refinery at Mundra with a refining capacity of 600 TPD in the year 1999

• Launch of Fortune Brand in the year 2000

• Grown from 1 refinery in 1999 to 18 refineries in 2018

• Refining capacity increased from 600 TPD in 1999 to 11000 TPD in 2018

• Owns 18 refineries and 10 crushing units at various strategic locations across India.

• One of the leading exporters of Castor Oil, Oleo-Value Added Products and De-oiled Cakes

• Revenue went up from INR 417 Cr to INR 25000 Cr over these years

• Capital investment of INR 2500 Cr as on date

Competitive Advantage Future Plans

• 18 Refineries & 10 Crushing Units • To be considered as FMCG Food Company instead of only

• Refining capacity of over 11,340 tonnes per day

edible oil company

• Seed crushing capacity of 8,950 tonnes per day

• Packaging capacity of 8,360 tonnes per day • Overall Volume Target – 10 MMT by 2021-22

• 5000+ distributors & >1 mn outlets serve 30 mn • Consumer Packed Oil Business – 3LMT/Month as against

households

1.75-1.80 LMT/Month at present

• India’s No.1 edible oil brand “Fortune” having presence all

over India • Plan to Grow in new business segments like Wheat Flour,

• Diversified food products such as Rice, Soya, Pulses, Besan, Rice, Soya Nuggets and Sugar

Castor and Soya & Oleo value added products

49Financial Parameters

Volume MMT Revenue Rs Cr

4.50 4.27 30000

3.92 26435

4.00 CAGR : 11% CAGR : 16%

25000 23215

3.50 3.15

3.00 2.78 2.73 20000 17828

2.50 14836 14861

15000

2.00

1.50 10000

1.00

5000

0.50

0.00 0

FY14 FY15 FY16 FY17 FY18 FY14 FY15 FY16 FY17 FY18

EBIDTA Networth

Rs Cr Rs Cr

1200

1800 1655

1010

1000 1600

CAGR : 24% CAGR : 21%

1400 1280

783

800 1200 1048

961

600 525 1000

502 776

426 800

400 600

200

400

200

0 0

FY14 FY15 FY16 FY17 FY18 FY14 FY15 FY16 FY17 FY18

50Key Investment Highlights

1

Indian food

consumption trend is

a compelling case

for AWL’s business

7 2

Competitive advantages in

Strong parentage, company sourcing, investment in

managed by professionals

capacities and strong

and industry experts business strategy aligned to

shift in consumption pattern

Investment 3

6

Diversified product highlights

Pan India presence and

portfolio and focus on extensive manufacturing,

branding to capture marketing, sales and

incremental market share distribution platform

5 4

Strong financial profile with Prudent business strategy and

revenue growth ~25% CAGR, risk management policies, given

with comfortable cash flows the low margin business coupled

throughout the tenor of the with commodity cycles and

project competition

51AEL: Mundra Solar PV - Solar Manufacturing

52Solar Manufacturing - Demand-Supply Scenario

Global solar PV demand projection (in GW)

China US Japan India EU RoW

119 121

116 116

107 33

99 38

45 42

79 14

48 13

52 3

13 4

34 12 17

51 5 16

10 6

15 7 12 13 14 15

15 12 12

7 11 13

8

12 9 10

5 9 35 40

2 8 7 21 28 31

7

6 9 11

2015 2016 2017E 2018E 2019E 2020E 2021E 2022E

India cumulative solar capacity (MW)

Installed Capacity

Projected Capacity

100000

82500

65000

48000

32000

12288

3745 6760

FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22

To achieve such an ambitious target, India is projected to install on average 18,000 MW of solar capacity annually

Source: GTM Research – PV Pulse, February 2018, MNRE

IEO – International Energy Outlook 53Drivers & Regulatory framework for Growth

• Impending safeguard / CVD duties to open up market demand

India • Increased demand for Indian made cells / modules set to raise ASPs and margins

domestically

• Cells / Modules imported from India exempt from Section 201 tariffs

USA

• Projected market of ~350 MW / year opens up with price premiums

Vietnam • Announced project pipeline is above 8.8 GW

• Energy Strategy Package - 40 GW of PV on top of installed 19.2 GW (EoY 2016),

Italy

translating to 3 GW annual market from 2018 to 2030

• Resurgence of European demand in 2018 will bring 43% annual growth from 2017 levels

Europe

of 6.3 GW

• France, Netherlands and Taiwan round out some of the most attractive markets by 5-

Others

year market size (~ 2 GW/annum) and growth rate (2-3x)

Supportive Regulatory framework

Gujarat Govt. Policy Safeguard Duty Countervailing Duty M-SIPS Policy

o INR 100 Cr CAPEX o Status o Status o Status

subsidy • Recommended • Ongoing • INR 342 Cr. Capex

o INR 10 Cr Interest subsidy assessed

subvention o Expected impact o Expected impact

o Full exemption of • 70% duty on imported • 30-35% on panel o Timeline

electricity duty cells from China / prices • Subsidy disbursement

o INR 1/unit rebate on Malaysia expected shortly

electricity rates

o SEZ benefits on import

duties

Duty impacts are expected to have a cumulative impact on imported PV products; an additional customs duty of

7.5% is also being considered

Source: GTM / BNEF 54Support for Incremental Capex

Proposed Capital Subsidy for new/upgraded capacities

Polysilicon Wafer Cell Module

Est. Capex for

1000 MW ~ $150 Mn ~ $120 Mn ~ $160 Mn ~ $50 Mn

2-3 GW 4 GW 6 GW 6 GW

Upper limit of

CFA* @30%

~ $46 Mn ~ $37 Mn ~ $48 Mn ~ $16 Mn

Manufacturing Support Creation of Local Offtake

• Interest subvention of up to 3% for upgrading/expansion • Restructuring requirements for greater backward

of existing capacity integration

• Exemption from customs duty on import of capital goods • Rooftop DCR to have 40% requirement of domestic

• Lenient allocation and banking of renewable energy for cells in 2018/19

manufacturing • 20% of DCR modules to have domestic made wafers

• Supply of power at APPC + 5% rates from 2019/20

• Land at preferential rates / near ports • 2020/21 to see earmarked DCR component of 20% for

domestic polysilicon

CPSU scheme has been increased to 12 GW from 1 GW;

Creating offtake and price premiums for locally made cells and modules

* CFA – Central Financial Assistance 55Why India needs to build Solar Manufacturing Capacity

• Controlling Forex outflow: In the absence of manufacturing, India will need to import USD 42 bn. of solar equipment by 2030

corresponding to 100 GW of installed capacity1.

• Job Creation: Solar manufacturing can also create direct employment of more than 50,000 in the next 5 years assuming local

manufacturing captures 50% domestic market share and 10% global market. Another at least 125,000 indirect jobs will be created in

the supply chain

• Investment opportunity in the country impacting the GDP

• Achieving self-sufficiency:

a) Major exporters may decide to divert most of their supply for domestic use (as evidenced by increased demand pull in Q3 2017 and

non-availability of imported modules)

b) Sudden jump in prices in the future due to supply shortages (polysilicon supply constraint raised the price due to supply disruptions)

c) Dispute with major suppliers (as evidenced in the case of China’s rare earth supply to Japan or supply of gas by Russia to European

nations)

d) Unless end-to-end value chain capability is created domestically, temporary protectionist measures like ADD/CVD on cells/modules

may attract additional tariffs on imported raw material like wafers/polysilicon

• Protection against fluctuation in pricing: Unless end-to-end value chain capability is created domestically, temporary protectionist

measures like ADD/CVD on cells/modules may attract additional tariffs on imported raw material like wafers/polysilicon

• Quality and warranty assurance

1) India’s energy imports have risen sharply from USD 43 bn. in 2005-06 to USD 167 bn. in 2013-14. In comparison India’s trade deficit

in 2013-14 was USD 139 bn. Solar power is a strategic need for the country as solar power can potentially save USD 20 billion in fossil

fuel imports annually by 2030.

56You can also read