Adding Value to Parcel Delivery - September 29, 2015 - Accenture

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Adding Value to Parcel Delivery September 29, 2015

Research Approach

A comprehensive analysis of CEP (Courier, Express & Parcel) industry

Assesses historic performance, identifies future trends and determines shareholder value drivers

Includes B2B and B2C segments, domestic versus international shipping as well as overnight

and non-day, and time definite products segments under 150 pounds or 70 kilograms

Examines current and new players in this market, including global integrators, postal organizations,

regional players, shared economy and crowdsourcing actors, as well as retailers moving downstream

Sources include: public information, paid and proprietary primary and secondary research, internal

and external subject matter expert interviews and extensive market and financial analysis

Copyright © 2015 Accenture. All Rights Reserved. 2

Market Definition

Definition of CEP (Courier, Express and Parcel)

Time sensitivity: Usually consignments

Same day & delivered by a specified day and even

in-night Air/Road express Air charter

by a specified time

Time certain

Priority Express

Express freight Size of consignment: Maximum weight

Next day usually considered to be about 31.5kg

(70lbs); Few exceptions.

Deferred and

Day certain Other Express Freight Forwarder

Day Groupage

uncertain Postal FTL

LTL Mostly Door to Door

Document Parcel Freight LTL, FTL

Space represented by pure express players

>1kg 31.5kg 1000kg such as UPS, FedEx and TNT Express; as

well as express and parcel arms of postal

Source: TNT, Accenture Research companies such as Geo Post (La Poste)

Scope of Market = Courier, Express and Parcels and Purolator (Canada Post)

Copyright © 2015 Accenture. All Rights Reserved. 3

Parcel Delivery—Key Findings Summary

Power shifting to the consumer

Internet driving growth, transforming the supply chain

B2C outgrowing and cannibalizing B2B

The world is flat: rise of the micro multi-national

Parcel

Delivery Growing demand and increased volatility

Product mix means lower yields per package

Investments to grow capacity, yet declining ROIC

Costs are rising faster than revenue

High fixed cost means less flexibility when it is key

Last mile is where the battle is taking place

Sharing economy set to disrupt the last mile further

New technology will change the game

Home delivery becomes the new premium

Most delivery organization know what to do, but need to do it better, faster, cheaper

Copyright © 2015 Accenture. All Rights Reserved. 4Digitally enabled consumers driving most of the eCommerce demand

see bargaining power shifting toward them

Rise of the digital consumer

Consumers with:

Empowers: So they seek:

Greater choice

Advent of:

Faster reviews

Lower prices

Data

Low switching costs Greater convenience

Seamless experience

Devices

Retailers and Deliverers with: in

More competition Buying Paying

Social networks

Receiving Returning

Easier aggregation of

services

Better visibility in

supply chain

Presents: So they provide:

We have crossed barriers in choice, transparency, and service expectations

Source: Accenture analysis

Copyright © 2015 Accenture. All Rights Reserved. 5The parcel delivery value chain has expanded in scope.

Roles at each stage have evolved toward a stronger service orientation.

Evolution of parcel delivery value chain

Past—Deliver Present—Digital, Transparent, Fast and Flexible Delivery

Pick up

• Less visibility into

demand for services

• Limited influence on

demand

Warehousing

• Low C2C and B2C

• Less transparency

• Easier timelines

• Limited competition

Transportation

• Recipients with low

bargaining power

• Low service

expectations

Delivery

Need to develop new resources and capabilities to deliver on service expectations at each step of the value chain

Source: Accenture analysis

Copyright © 2015 Accenture. All Rights Reserved. 6The last mile, which holds key to the consumer experience, has

witnessed an emergence of multiple delivery models

Last mile delivery models

A) Postal mail-run

Warehouses

B) Courier delivery 2

D) Lifestyle/ Lifestyle/Crowd-shippers’ delivery to homes similar to courier

Crowd-shippers

C) Courier delivery to lockers

Crowd-shippers delivery to lockers

Retail stores Parcel lockers/

Access points

Consumer convenience and cost reduction have been primary objectives guiding the change

Source: Accenture analysis

Copyright © 2015 Accenture. All Rights Reserved. 7The challenge of increasing service needs is exacerbated by the

growing delivery demand calling for scale up of infrastructure

Courier-Express-Parcel (CEP) market size and growth

USD billion, %, 2008-2020F

Routes

Global market size

USD billion Faster growth (~5.4%, 2013-2017) than

International domestic primarily due to growing cross-

border eCommerce

+5% 343.1

Continues to be >75% of overall market

+4%

Domestic with ~5.0% growth (2013-2017)

237.9

194.8 Customer segments

Slower than B2C with close to GDP growth

B2B but significant share and higher margin

contribution

Close to eCommerce growth rates and

2008 2013 2020F B2C growing in significance

Emerging segment from growth in auction

C2C sites and the circular economy

Geographies

Market APAC N. America W. Europe Europe Rest Middle East S. America Africa

2013 share 32% 33% 23% 5.7% 3.5% 2.5% 1.5%

2020 share 38% 30% 19% 5.3% 4.1% 2.5% 1.9%

2013-20 CAGR 15% 9% 5% 8% 7% 5% 10%

Fixed cost heavy model: The growth has significant investment implications to meet demand

Source: Accenture research, Transport Intelligence

Copyright © 2015 Accenture. All Rights Reserved. 8eCommerce is driving growth in domestic and international markets

Courier-Express-Parcel (CEP) market size and growth

USD billion, %, 2010-2013 and 2013-2017F

Domestic vs. international growth—Historical and Future1 Drivers of growth

20%

131.9 70% Of worldwide spending by millennials by 20202

International (2010-2013 & 2014-2017 CAGR)

75.4

346.0

15% 55% Urban population out of total by 20173

10%

237.9

109.4

49% Smartphone penetration in mobile phones by 20174

81.6

77.4

46% Internet penetration in population by 20175

5%

67.4

Europe N. America 27% International eCommerce out of total by 20176

APAC Global

0%

0% 5% 10% 15% 20% 12% Middle class growth rate in APAC 2009-20207

Domestic growth (2010-2013 and 2013-2017 CAGR)

Fixed cost heavy model: The growth has significant investment implications to meet demand

Notes:

Size of the bubble represents market size. Previous point—2013, Leading point—2017F. Total market expected to move from US$ 237.9 billion to US$346.0 billion.

Source: 1 Transport Intelligence, 2 https://badgeville.com, 3 “World Urbanization Prospects” UN Report, 4,5 www.digitalbuzzblog.com, 6 eMarketer, 7 Ernst & Young

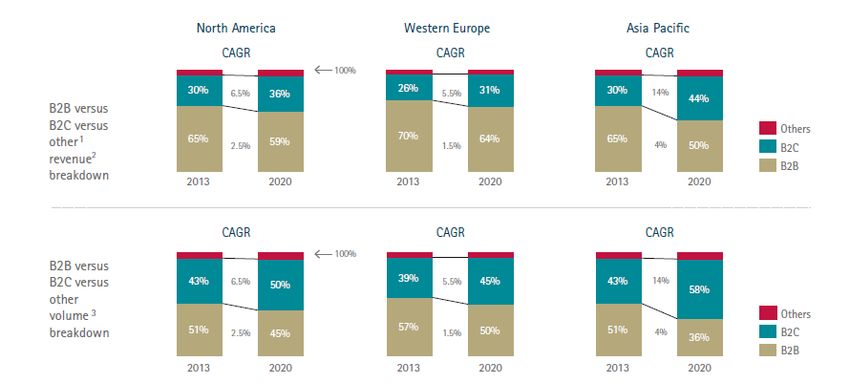

Copyright © 2015 Accenture. All Rights Reserved. 9B2C will continue to grow in significance across geographies,

driving growth and presenting challenges

CEP market size and growth—B2B vs. B2C

USD billion, %, 2013-2020F

B2B vs. B2C growth1 Drivers of growth

15%

Asia Pacific 55% Urban population out of total by 20173

49% Smartphone penetration in mobile phones by 20174

B2Cl (2013-2020 CAGR)

10% Global

46% Internet penetration in population by 20175

North America

5% Western Europe 12% Middle class growth rate in APAC 2009-20207

Challenges:

0% Volatility Last mile Yields Returns

0% 5% 10% 15%

B2B (2013-2020 CAGR)

B2C focused delivery networks call for different focus areas vs. B2B

Notes:

1 Size of the bubble represents total market size in 2020. Total market expected to move from US$237.9 billion to US$343.1 billion.

Source: Accenture research, Transport Intelligence, Accenture analysis

Copyright © 2015 Accenture. All Rights Reserved. 10Although B2C is expected to grow in share, B2B will remain a

sizeable opportunity

CEP market share—B2B vs. B2C

USD billion, %, 2013-2020F

Price Product Scope for

Segment Size Growth Density Profitability

sensitivity dominance differentiation

B2C Lower Higher Lower Higher Deferred Lower High

B2B Higher Lower Higher Lower Express Higher High

Firms need to find optimal balance in portfolios and investment focus in both B2B and B2C

Source: Accenture research, Accenture analysis

Copyright © 2015 Accenture. All Rights Reserved. 11Although B2C is driving growth; it is also exposing delivery

companies to more volatility in demand

B2C implications—Volatility Dec 2013: “UPS admits it was Dec 2014: “UPS slammed by a

unprepared for the late surge different holiday season mess-up

in online holiday shopping”1 …adding too much extra firepower”1

FedEx average and maximum daily shipping UPS average and maximum daily shipping

volume (million)2 volume (million)2

25 35

20 30

15 25

10 20

5 15

0 10

2009 2010 2011 2012 2013 2014 2009 2010 2011 2012 2013 2014

Maximum shipments in a day Average shipments in a day Maximum shipments in a day Average shipments in a day

UK Cyber Monday—20143 China Singles Day—20134

39% More parcels than previous Monday 166 Shipments across China

million

More cross-border shipments than Greater than average daily shipping

86% previous year 10x volume

Agility in value chain would be important to contain costs without compromising service standards

Source: 1 News reports; 2 Financial reports and News reports; 3 Metapack; 4 Financial Times

Copyright © 2015 Accenture. All Rights Reserved. 12Investments are being made by delivery firms and retailers to expand

capacity and modernize network in the parcel delivery business

Capital expenditure on parcels

2014

Major investment stories—Parcel delivery Major investment stories—Retailers

DPD

DPD has invested £10.2 million in six depots to Ali Baba is investing US$1.5 bn

expand its capacity to handle B2C parcels Ali

Baba over three to five years to

expand the logistics network in

China (2014)

DHL investing EUR 750 million to modernize and

DHL expand its parcel network…building Germany’s largest

parcel processing center in Hessen (2013)

Ali Baba’s Institutional investors are co-

co- investing US$3 billion over the

Investors same period along with Ali Baba.

FedEx Ground investing US$1.2 billion this year in 70

Fedex expansion projects in addition to the US$2.5 billion

spent over the past five years to add capacity (2014)

Australia Post doubling capacity at Sydney and

Aus

Post Melbourne parcel facilities as a part of its AUD 2

billion investment in the Australia Post Network

(2012) Amazon has spent US$13.9

Amazon billion since 2010 on

UPS plans to invest US$2 billion over the next five warehousing and fulfilment to

years to develop its international infrastructure in support its business including 13

UPS Europe, Asia and the Americas, (4.5% to 5% of annual parcel depots in the United

revenue) …targeting growth markets and Kingdom.

improvements in the profitability of eCommerce

deliveries. (2014)

Firms are scaling up to meet future demand and becoming more fixed cost heavy

Source: News reports, Accenture analysis.

Copyright © 2015 Accenture. All Rights Reserved. 13Many firms have pursued the inorganic route to build scale and

acquire new capabilities to widen the scope of their business

Mergers and acquisitions Trend is continuing in 2015 with

the FedEx €4.4bn bid for TNT

Number of deals by year1 Number of deals by business (Last five years)

2009-2014 2009-2014

45

42

Logistics and Transportation 89

34 Parcels and Express 38

Marketing and Sales 17

22

20 IT Services and Software 14

14 Financial Services 9

Mail 6

Real Estate 6

2009 2010 2011 2012 2013 2014

Acquisition strategy would be key in acquiring the right assets and maximizing effectiveness and efficiency

Notes:

1 Firms included are DPDHL, Austrian Post, Canadian Post, La Poste, PostNord, SingPost, Australia Post, UPS, Fedex, Bpost, Swiss Post and Itella.

Source: Financial reports, Accenture analysis

Copyright © 2015 Accenture. All Rights Reserved. 14Sharing economy start-ups are witnessing an upsurge in venture

capital interest across industries

Total funding in sharing economy start-ups

958

357

283

60 96 116

2009 2010 2011 2012 2013 2014

Top funded companies Top investors

Stay 800

Airbnb($776.4M), Wimdu($90.0M) Sequioa, TPG Growth

Transport 645 Lyft ($333M), RelayRides($53.2M), Trinity Ventures, Shasta Ventures,

Boatbound($5.3M) Google Ventures, August Capital

Personal Goods 273 Chegg ($252M; IPO at $1.1B).

N/A

Bag Borrow or Steal($20.0M)

Private Spaces 51 LiquidSpace($26.2M), Shasta Ventures, Roth Capital Partners,

PivotDesk($6.7M), Storefront($8.9M) Lucas Venture Group, Spark Capital

Business Equipment 16

Getable($3.2M), Yard Club($1.6M) N/A

Food 11

EatWith ($9.2M), Suppershare GreyLock

Logistics 4

Friendshippr($1.2M), WeDeliver($0.8M) N/A

Storage 0

Roost($160k), StowThat($50k) N/A

Source: Sharing Economy Landscape 2015, Tracxn research

Copyright © 2015 Accenture. All Rights Reserved. 15New entrants are drawn to a growing but underserved industry and

are enabled by technology

List of promising start-ups by business segment

Transportation Systems Crowd Shipping Containers

Futuristic shipping models Flexi-cost last mile shipping Container packing innovation

PiggyBee, Friendshippr, Roadie Staxxon, Holland Container

Matternet, Google drones, Barnacle, Nimber, Zipments For You, Innovations

Amazon drones Bringrs, UberCARGO

Freight Rates Local Delivery 3PL and Other Services

Transparent shipping costs Low-cost urban delivery models Enabling shippers

Swapbox, Boxc, Postmates,

Freightos, Tanspoteca,

DoorDash, Zipments, Deliv, Sidecar, Shipwire, Cloud Fulfillment, Scurri,

iContainers, Freight Filter,

Uber, ParcelBright, Parcel Metapack, 71lbs, Axida

Xeneta, Shippo, ShipHawk,

End-to-end Shipping Storage Trucking

Uber of shipping in C2C space Crowd-sourcing storage space enabling Tracking and management

flexi-delivery

Cargomatic, TruckTrack, KeepTruckin,

Shipster, Shyp, Shipbob, Youtruckme.com, Keychain Logistics,

Lockitron, MakeSpace, Boxbee, Cubbyhole,

Schlep, MinFragt.dk uShip

Parcel Pending, ShareMyStorage, Roost

Last Mile

Creating new challenges and opportunities for legacy companies

Source: www.jonathanwichmann.com

Copyright © 2015 Accenture. All Rights Reserved. 16The new entrants in last mile are mostly asset-light and utilize the

power of crowdsourcing to achieve outcomes at lower costs

Start-ups—Last mile

Storage solutions mostly based

on crowdsourcing spaces. Offer

temporary storage for later Local

Crowd delivery and collection.

Shipping Deliveries

Present opportunities to

manage flexible deliveries while

minimizing travel costs.

Crowdshipping enabling asset- Localized, urban delivery models

light, low fixed-cost models to offering delivery solutions at

solve the last mile delivery. lower prices than legacy

players and enabling offline

Potential partners for parcel retailers to add delivery

delivery companies that do not Storage services.

wish to grow investments in last

mile. They are competitors and

potential partners.

Operationally flexible models generate cost advantage for new entrants but scalability remains to be evaluated

Source: www.jonathanwichmann.com, Accenture analysis

Copyright © 2015 Accenture. All Rights Reserved. 17Parcel Delivery— Conclusions – 9 Value Drivers

Power shifting to consumers

1 To deliver on

To support market

strategies Focus on consumers’ wish-list

Increase the

4 Efficiency 3

Recipients

and

Productivity

Go Beyond

Traditional

Variablize

Costs

Underserved

& Growing Grow

International

Disaggregate

the Value

Chain

Brand and

Segment

Mergers and

6 5

Acquisitions

To build sustainable Deploy To succeed in executing

operating model Strategic market strategies

Pricing

2

Consumers’ Wishlist

Copyright © 2015 Accenture. All Rights Reserved. 18Executive Takeaway

Parcel Value Drivers (1 of 2)

Rationale/Why? Description Benefit/Value Description

• Rise of digital • Relationship • Better customer • UPS MyChoice

consumer w/recipient experience • Australia Post

Focus on • Mobile lifestyle • Two-way • Market share retention • La Poste

the recipient • Competition for last communication • Lower cost to serve

mile • New products/services • Incremental revenue

• Auto-replenishment • Monetize preferences

• Transportation a • Value added services • Additional revenue • UPS SCS

commodity • eLogistics and • Customer stickiness • SingPost

Go beyond • Growth of eCommerce warehousing • Long-term contracts • FedEx/Genco

traditional • Supply chain • Returns management • Diversification of risk

disruption • Delivery options

• Declining yields

• Rise of micro • Cross-border • Revenue growth • FedEx (Brazil, Mexico,

multinational partnerships • Higher yield per TNT)

Grow international • Lower barriers to X- • E2E visibility package • Austrian Post (EEC)

border • Customs integration • Higher margins • Japan Post / Toll

• Access to Internet • Global trade tools • Diversification of risk Priority

• Growing middle class

• Segment growth • Segmentation • Greater market share • UPS SCS

• Rise of delivery • Vertical specialization • Lower price sensitivity • Austrian Post and

Brand and options • Brand positioning • Higher revenue Fiebra brands

segment • Expansion of services • Product portfolio • Higher margin • La Poste

• Blurring of player lines management

• Declining yield per • Subscriptions services • Higher margins • Amazon Prime

package • Analytics • Incremental cost • FedEx and UPS

Deploy strategic • Poor pricing practices • Competitive pricing coverage pricing (residential and

pricing • Costs to revenue • Surge/cost-based • Greater revenue fuel surcharges

increasing pricing • Greater market share • Uber peak pricing

• New products/services • Airline pricing

Copyright © 2015 Accenture. All Rights Reserved. 19Executive Takeaway

Parcel Value Drivers (2 of 2)

Rationale/Why? Description Benefit/Value Description

• The firms need • Big data • Higher margin • Purolator

to build capabilities • Analytics • Greater supply • bPost

Increase efficiency to succeed • Technology chain agility • FedEx Express

and productivity at implementing • Leading practices • Cost avoidance

market strategies • Greater

revenue/share

• Growing peaks • Outsourcing • Lower/avoided • Innovapost

and valleys • Lease vs own CAPEX • Lasership

Variabilize • Declining asset • Labor strategies • Cash generation • Deliv

costs utilization • Asset divestment • Higher margins

• High downside if • Speed to market

revenue declines

• Declining asset • Value creation • Higher ROA • SingPost Books

utilization • Capacity expansion • Faster speed • GXG @ USPS

Disaggregate • Shared economy • Asset utilization to market • Uber Last Mile

the value chain growth • Build ecosystem • Higher revenue

• Last mile competition • Higher margin

• Stagnant B2B growth • Market assessment • Revenue growth • Austrian Post

• Declining package • Target identification • Speed to market • DHL

Mergers and yield • Post-merger • New capabilities • FedEx

acquisitions • Excess capacity integration or geos • Sing Post

• Need for • Synergies realization • Cost synergies

specialization

Copyright © 2015 Accenture. All Rights Reserved. 20Contact Details

For more information, please contact:

Tim Bateman Brody Buhler Andre Pharand

Global Parcel Lead Global Managing Director Global Post & Parcel Management

Post & Parcel Lead Consulting Lead

tim.bateman@accenture.com robert.b.buhler@accenture.com andre.pharand@accenture.com

+44 7774 299 350 +1 703 405 1253 +1 917 755 5551

Copyright © 2015 Accenture. All Rights Reserved. 21Copyright © 2015 Accenture. All Rights Reserved. 22

You can also read