Borderless Business: Intra-ASEAN Corridor - Opening doors to diverse opportunities - Standard ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Borderless Business: Intra-ASEAN Corridor Opening doors to diverse opportunities

Contents: Overview of the Intra-ASEAN Corridor: Opening New Doors 3 Our Growth Watchlist: Key Sectors Driving the Future of the Intra-ASEAN Corridor 9 Acting with Impact: Five Focus Areas for ASEAN Companies to Drive Resilient Growth Within the Region 20

Overview of the Intra-ASEAN Corridor: Opening New Doors in ASEAN

Overview of the Intra-ASEAN Corridor

ASEAN’s rising middle class and increasingly been strong over the past 50 years, economic

well-educated workforce, coupled with its progress has not been homogeneous across

supply of natural resources, rapid urbanisation, member countries. Moving forward, however,

and growing infrastructure spend provides a the region cannot rely on the same growth

strong foundation for future growth. Not only drivers to guide its future trajectory. Despite

is ASEAN highly connected through free-trade growth prospects remaining positive, weaker

agreements with major global trading partners economic recovery is expected on the back

such as the US, China and Europe but there is of increasing COVID-19 cases and renewed

also significant focus on intra-ASEAN trade and lockdowns, with IMF having lowered their

investments – opening doors to new growth forecast from 5.2 per cent growth in 2021 to 4.9

opportunities for companies in the region. per cent for five ASEAN countries (Indonesia,

Malaysia, the Philippines, Thailand and

Borderless Business: Intra-ASEAN corridor is Vietnam). ASEAN respondents to our survey

a strategic point-of-view, commissioned by confirm this, with 75 per cent considering the

Standard Chartered and prepared by PwC, COVID-19 pandemic among the top 3 risks for

which explores key sectors of opportunity and their business in the region.

focus areas for ASEAN-based companies to

further their growth within the region. ASEAN ASEAN’s enhanced integration and cooperation

offers a myriad of opportunities for local thus comes at a time where fundamental

and international players in areas such as shifts and disruptions on a global scale have

healthcare and consumer goods, construction, intensified the need to deepen connectivity and

real estate, and renewable energy, given its pursue more sustainable growth.1

favourable demographics, rapid urbanisation

and drive towards sustainability. With Industry Increased intra-regional

4.0 under way, ASEAN’s rapid digitalisation also

provides grounds for growth in manufacturing

cooperation and connectivity

and digital technology. expected to boost regional

This point-of-view elaborates on a number of

growth

key initiatives companies should consider, to With the aim of driving cohesive growth and

ensure that they are well-positioned to seize further regional cooperation within ASEAN,

such opportunities on their path to resilient the bloc established the ASEAN Community

growth. These include diversifying supply agenda in 2015, incorporating blueprints for

chains, digitalising for impact, leveraging regional integration in political, economic and

local partnerships, incorporating sustainability socio-cultural aspects. Under the auspices of

as part of growth targets, and establishing this agenda, the ASEAN Economic Community

adequate governance frameworks to mitigate (AEC) Blueprint 2015 has been successful in

potential risks in a post-COVID-19 world. We facilitating and liberalising trade among

also incorporate insights collated via a survey of ASEAN economies. As a result, economic

senior-level executives from ASEAN companies exchanges among ASEAN members have

that are currently engaged in cross-border grown. Between 2015 and 2019, intra-ASEAN

activities within the region.a total trade in goods increased by 4.3 per cent

CAGR from USD535.4 billion to USD632.6 billion.

ASEAN’s growth trajectory In 2020, due to COVID-19 disruptions, total

remains strong but requires intra-ASEAN trade in goods stood at about

USD565.9 billion (and CAGR for the period 2015

some recalibration to 2020 was 1.4 per cent). The AEC Blueprint

2025 seeks to build on the AEC Blueprint 2015

ASEAN’s remarkable growth in the past

and bring ASEAN economies even closer

decades has brought it on track to becoming

through further reduced tariffs, harmonised

the world’s fourth largest single market by 2030.

capital market regulatory frameworks and

However, while the region’s track record has

platforms, greater labour mobility, improved

a Survey commissioned by Standard Chartered in April 2021 and completed by senior executives from 83 companies based in ASEAN

and focusing on the Intra–ASEAN corridor

Borderless Business: Intra-ASEAN Corridor 4

Overview of the Intra-ASEAN Corridor

consumer and intellectual property (IP) global foreign direct investment (FDI) inflow

rights protection, inclusive development and to ASEAN (~35 per cent increase from USD118

enhanced connectivity. billion in 2015 to USD159 billion in 2019). In

addition, intra-ASEAN FDI is also significant

Moreover, we see ASEAN playing a bigger role with a 13.8 per cent share of total FDI.

in the global production value chain, in view

of its heightened connectivity with five major Figure 2: Intra-ASEAN FDI inflow by source

trading partners – including China, Japan, New country

Zealand, Australia and South Korea – via the

USD billion

Regional Comprehensive Economic Partnership

(RCEP), once it is ratified. RCEP is expected to 30

connect about a third of the world’s population 25.9

25.0 24.2

25

and output; and could potentially add USD209 20.8 22.0

billion to world incomes and USD500 billion to 20

world trade by 2030. According to the ASEAN

Secretariat, RCEP will simplify and streamline 15

the rules and procedures for trade and

investment currently codified in bilateral FTAs, 10

thereby reducing trade inefficiencies. It would

5

also lower trade barriers and improve market

access for companies, enhance transparency 0

in trade and investment, as well as facilitate 2015 2016 2017 2018 2019

Singapore Thailand Malaysia

greater inclusion of ASEAN-based companies Indonesia Vietnam Others

to global and regional supply chains. Notably,

Source: ASEANStats

83 per cent of our survey respondents indicated

that they plan to increase their company’s Within ASEAN, Singapore is a major hub for

investments in ASEAN over the next 3-5 years by investments, being the largest source for

at least 25 per cent, once RCEP is ratified.2 intra-ASEAN FDI and accounting for a majority

share in 2019. In addition, Singapore is a target

market for investments as well and in this

Figure 1: Intra-ASEAN total trade in goods regard, 80 per cent of our survey respondents

USD billion selected Singapore as the country offering the

best expansion opportunities within ASEAN,

700

followed by Thailand at 60 per cent and

: 1.4%

CAGR

Vietnam at 59 per cent. Furthermore, over 85

600

per cent of survey respondents foresee at least

500 a 10 per cent growth in sales or production in

400 ASEAN over the next 12 months.3

644.65 632.60

300 589.12 565.89

535.38 517.95

200

100

0

2015 2016 2017 2018 2019 2020

Source: ASEANStats

Increased intra-regional connectivity through

the flow of capital, integration of production

networks, and vertical or horizontal integration

of supply chains is likely to strengthen ASEAN’s

burgeoning role in global supply chains.

Furthermore, ASEAN’s diverse industrial

landscape also lends itself to be an attractive

location for companies to establish a hub

for the region. This optimism is manifested in

Borderless Business: Intra-ASEAN Corridor 5

Overview of the Intra-ASEAN Corridor

Figure 3: Key drivers for focus on ASEAN and major economies offering expansion

opportunities

Access to the large and growing ASEAN consumer market

Access to a global market (from ASEAN), enabled by a network of FTAs

Presence of a mature and reliable supplier base

Note: Survey questions asked: ‘What are the key drivers for your focus on ASEAN?’ and ‘Which of these major economies within ASEAN

do you think offers the best expansion (sales / production) opportunities for your company?’

For Key Drivers - values indicated refer to the % of survey respondents who included the driver as one of the top 3 ranked choices

Source: Standard Chartered Survey, 2021

Rapid population growth, In addition, with 100 million people region-wide

expected to migrate from the countryside to

urbanisation and digitalisation cities between 2015 and 2030, demand for

expected to give rise to new improved infrastructure will grow significantly.

The Master Plan on ASEAN Connectivity

consumer markets (MPAC) 2025 outlines a roadmap for enhancing

ASEAN’s growing population, coupled the region’s infrastructure, including smart

with rapid urbanisation and digitalisation, city development, physical and institutional

is expected to generate new market connectivity, and people-to-people linkages,

opportunities. The World Economic Forum which are foundational to achieving a fully

anticipates that over the next decade, integrated ASEAN Community.

emerging ASEANb will drive 98 per cent of the

Part of ASEAN’s envisioned integration also

increase in the region’s working population,

involves strengthening the region’s digital

estimated to reach 40 million by 2030. With

connectivity. The gross merchandise value of

this, higher consumption levels are expected

ASEAN’s internet economy was USD100 billion

especially in Indonesia, Vietnam and the

in 2020 and is set to surpass USD300 billion by

Philippines. As per our survey, 69 per cent of

2025. To capitalise on this potential, member

respondents are focusing on ASEAN to gain

states signed the ASEAN Agreement on

access to the large and growing consumer

e-commerce in 2018 in hopes that facilitating

market, and close to 50 per cent cite the

more cross-border e-commerce transactions

availability of an abundant and skilled

would drive further regional growth.4

workforce as a key driver.c

b Indonesia, Malaysia, the Philippines, Thailand and Vietnam

c Value indicated refers to the % of survey respondents who included the driver as one of the top 3 ranked choices

Borderless Business: Intra-ASEAN Corridor 6

Overview of the Intra-ASEAN Corridor

Renewed focus on sustainability Despite such initiatives growing in

prominence, ASEAN has not kept pace with

set to create significant other regions in terms of green economy

opportunities vis-à-vis ASEAN’s initiatives. This suggests that there remain

significant untapped growth opportunities.

infrastructure development Recently, ASEAN has seen a stronger push for

Sustainable financing and infrastructure sustainable products from local governments,

will be key to supporting ASEAN’s growth rising corporate and investor awareness,

moving forward. ASEAN’s transformation and growing consumer preferences. This

towards a greener economy offers economic is reflected in our survey, with over 50 per

opportunities in areas such as energy and cent of respondents indicating that driving

resources, food systems, industries and sustainability and ESG will be a key focus area

logistics, cities, healthcare and education, for their organisations.d

and green financing. Initiatives such as the

Similarly, a recent research report – ‘Carbon

ASEAN Smart Cities Network (ASCN) embody

Dated: The net-zero supply chain revolution’

the bloc’s ambition to build future-ready and

by Standard Chartered – revealed that 78 per

resilient cities across the region. Moreover, it is

cent of multinationals (MNCs) will remove

estimated that every USD1 million invested in

suppliers that endanger their carbon transition

renewable technologies or energy efficiency

plan by 2025. The study also reveals that

could stimulate nearly thrice as much job

MNCs’ focus on tackling supply chain emissions

growth as compared to spending on fossil

could create a USD1.6 trillion opportunity for

fuels. If leveraged fully, USD172 billion worth

the net-zero club: those businesses reducing

of capital expenditure could create 30 million

emissions in line with MNC net-zero plans. This

jobs in ASEAN by 2030.

represents a major opportunity for net-zero-

focused suppliers across the 12 key emerging

and fast-growing markets in the study,

including Singapore, Malaysia and Indonesia.5

d Value indicated refers to the % of survey respondents who included the key focus area as one of the top 3 ranked choices

Borderless Business: Intra-ASEAN Corridor 7

Overview of the Europe-ASEAN Corridor

Intra-ASEAN Corridor

“ASEAN is core to Standard Chartered’s business strategy. As the only international bank with

a full presence in all 10 markets in the region, we believe we play a critical role in enabling our

clients to seamlessly trade and invest across the 10-nation bloc. The findings of this report

clearly validate the trends we are observing among our clients and we continue to invest in our

capabilities to meet their evolving needs.”

Heidi Toribio

Regional Co-Head, Client Coverage, Asia,

Corporate, Commercial and Institutional Banking

Standard Chartered

“ASEAN corporates’ strong appetite to leverage Singapore for expansion within the region

underscores the city-state’s unique position as the gateway to ASEAN. We have seen clients

from countries, such as Indonesia, Malaysia, the Philippines and Thailand, increasingly access

the deep and liquid financial markets in Singapore. Importantly, ASEAN’s growth prospects

remain promising, with the markets offering opportunities from healthcare and consumer

goods to construction and real estate as well as renewable energy. As the go-to bank in

ASEAN, Standard Chartered is committed to provide on-the-ground advisory and innovative

financial solutions to help these businesses succeed in the long term.”

Patrick Lee

Cluster CEO, Singapore and ASEAN Markets

(Malaysia, Vietnam, Thailand & Rep Offices)

Standard Chartered

“The potential for intra-ASEAN trade is enormous. Not only are the 10 member countries

located within close geographical proximity, they are also enjoying rising income levels and

rapid adoption of technology by consumers as well as businesses. In particular, Indonesia offers

abundant opportunities through its young population, growing middle class, and booming

digital economy. The regulatory reforms driven by the Indonesian government are also

expected to stimulate domestic and foreign investment. Similarly, Brunei and the Philippines

have much to offer, and are already actively engaging in intra-ASEAN trade. As the oldest

international bank in Indonesia as well as the Philippines, and a leading global bank in Brunei,

Standard Chartered is well positioned to marry deep local insights with product expertise to

help ASEAN corporates trade, invest, and grow.”

Andrew Chia

Cluster CEO, Indonesia and ASEAN Markets

(Australia, Brunei & the Philippines)

Standard Chartered

Borderless

Borderless

Business:

Business:

Europe-ASEAN

Intra-ASEAN Corridor 8

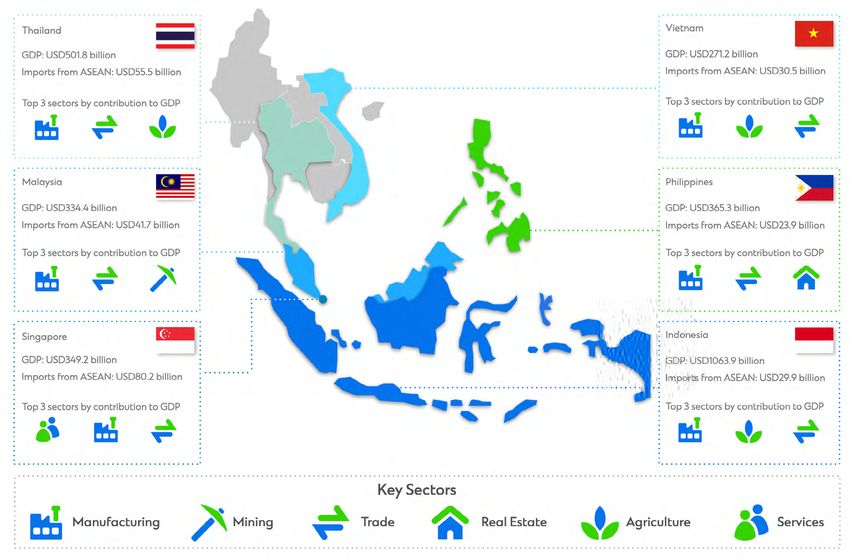

Our Growth Watchlist: Key Sectors Driving the Future of the Intra-ASEAN Corridor

Our Growth Watchlist

ASEAN’s increased physical and digital The region’s expanding middle class, ageing

connectivity through regional initiatives, population, and rising consumption levels

alongside favourable demographics and will bolster growth in the food and beverage

rapid urbanisation, is likely to generate and healthcare sectors. ASEAN’s growing

growth opportunities in several sectors, population density will also give rise to

highlighted below. The region’s maturing infrastructure needs, boosting demand for

manufacturing capabilities offer the potential construction, real estate and more sustainable

for companies to set up regional production sources of energy.

networks, especially in the automotive sector.

Figure 4: Key sectors in ASEAN-6 (by contribution to national GDP), 2020

Note: Trade includes wholesale and retail trade

Source: ASEANStats

1. Growing demand for Going forward, as ASEAN member states

(AMS) focus on expanding universal healthcare

healthcare services post- and dealing with rising health concerns amidst

COVID-19 and increasing focus COVID-19, this trend is forecasted to accelerate

at 8.3 per cent CAGR across the region from

on healthtech to propel growth 2020 to 2025.

in ASEAN

ASEAN’s demographics, accompanied by an

increased government focus on healthcare, has

brought healthcare spending in ASEAN from

USD99.2 billion in 2014 to USD124.3 billion in

2019 at a rate of 4.6 per cent CAGR.

Borderless Business: Intra-ASEAN Corridor 10Our Growth Watchlist

Figure 5: Healthcare spending in ASEAN-6

USD billion CAGR: 8.5% CAGR by Country

Malaysia

200 190.7 7.2%

175.5 21.0

165.0 Vietnam

19.9

150.9 18.7 23.3 7.6%

150 139.0 21.7

17.1

126.6 20.2 26.3 Singapore

15.9

19.1 24.4 8.2%

14.8 17.7 22.6

16.2 20.8 30.8

100 19.5 26.1 28.0

17.7 24.3

22.4 33.8

19.5 28.6 30.8

Thailand

26.1

24.0 8.7%

50 22.3

50.8 55.5

48.9

39.5 43.5 Indonesia

36.0 9.1%

0

2020 2021 2022 2023 2024 2025

Indonesia Thailand Singapore Vietnam Malaysia

Source: Fitch Solutions

ASEAN’s diverse healthcare industry is healthcare industry by facilitating cross-border

home to a number of production hubs – with trade of such products.

pharmaceutical products being the focus

in Singapore, Indonesia and Vietnam; and In addition to the established pharmaceuticals

medical devices in Malaysia and Thailand. and medical devices industry, the healthtech

Additionally, Singapore, Malaysia and Thailand boom has drawn out new segments of growth

are regional market leaders in medical tourism in areas such as telehealth, digital therapeutics,

and are implementing measures to reboot the and remote patient monitoring and analysis.

industry post-COVID-19. Initiatives such as the Local start-ups have received funding from

ASEAN Medical Device Directive, which aims other countries in the region and are looking to

to harmonise the medical device regulatory expand beyond their home markets.6

framework across the region, are expected to

drive even deeper linkages among AMS in the

Government focus on healthcare development and expansion of healthtech to be a vehicle for growth

in key ASEAN markets

Indonesia Thailand Philippines

Indonesia has relaxed restrictions on Thailand has selected healthcare as one The Philippines has plans to establish

foreign investment in the pharmaceutical of its 10 priority industries, as part of its Special Economic Zones (SEZs) for the

sector. Under its New Investment List goal of becoming a regional life sciences pharmaceutical industry to spur medical

(March 2021), foreign companies can centre. It has also granted incentives to research, manufacturing, and tourism

have up to 100 per cent ownership in the pharmaceutical investors and designed in the country. The first SEZ was opened

manufacture and wholesale of finished a regulatory framework to support R&D at the First Bulacan Business Park in

and raw pharmaceutical products. within the country. To access the large Malolos City in February 2021. Singapore’s

Notably, Jakarta-based healthtech healthcare market, Singapore-based Clearbridge Health expanded into

platform, Halodoc, managed to raise telehealth start-up, Doctor Anywhere, the Philippine market in 2018 with the

funding from Singapore firms such as launched a Virtual COVID-19 clinic in acquisition of Marzan Healthcare to

Singtel Innov8, Temasek Holdings, and partnership with Samitivej hospital, True expand its market reach in this high

Openspace Ventures. Digital Group, and AIA Thailand. growth market.

Source: SSEK, Fitch Solutions, Crunchbase, Doctor Anywhere, Philippines News Agency, Clearbridge Health

Borderless Business: Intra-ASEAN Corridor 11Our Growth Watchlist

2. Regional trade ties and when it comes to automotive manufacturing.

For instance, Thailand is known for being an

the emergence of the Electric automotive assembly hub, while Vietnam

Vehicles segment to strengthen contributes to the manufacture of automotive

parts. Strengthened trade linkages across the

the automotive sector in ASEAN region through initiatives such as the ASEAN

post-COVID-19 Economic Community (AEC) and the ASEAN

Free Trade Area (AFTA) can be leveraged

Improving consumer sentiment and economic to create an integrated production cluster

recovery post COVID-19 are expected to boost to boost the region’s ambitions of becoming

demand in ASEAN’s automotive market, with an automotive production and export hub.

vehicle sales projected to grow at a CAGR In addition, automotive manufacturers

of 9 per cent and production at a CAGR of based in ASEAN can capitalise on the added

6.6 per cent from 2020 to 2025. The region’s connectivity RCEP brings to explore export

automotive hubs – Thailand, Indonesia, opportunities with ASEAN’s major trading

Vietnam and Malaysia – have diverse yet partners under the agreement.

complementary comparative advantages

Figure 6: Vehicle production in ASEAN

CAGR: 6.6% CAGR by Country

3.91

4.00

3.72 0.11

3.57

3.39 0.11

0.10 0.32 Vietnam

3.50 3.17 0.09 0.29

0.08 0.22 0.26 7.6%

2.83 0.56

3.00 0.18 0.55

0.07 0.54

0.17 0.53 Malaysia

0.52 8.2%

2.50 1.02

0.49 0.91 0.98

0.86

2.00 0.79 Indonesia

9.5%

0.69

1.50

1.81 1.89 Thailand

1.70 1.76 8.7%

1.00 1.61

1.43

0.50

0.00

2020 2021 2022 2023 2024 2025

Thailand Indonesia Malaysia Vietnam

Source: Fitch Solutions

ASEAN’s growing population has intensified its

energy needs, which, in conjunction with the

rise of global carbon emissions, have spurred

demand for more sustainable transportation in

the form of Electric Vehicles (EVs). Governments

are prioritising this segment to drive the next

phase of growth within the industry with

incentives being provided for manufacturing

and adoption of EVs. Additionally, as countries

in ASEAN target the building of smart cities,

they are looking to develop capabilities in

autonomous driving technology. Singapore

is the regional leader in this aspect and has

already begun tests for driverless vehicles.

Recently, Malaysia and Vietnam are also

making headway in this area.7

Borderless Business: Intra-ASEAN Corridor 12Our Growth Watchlist

EVs a potential focus, with major ASEAN production hubs offering incentives to attract investments

Thailand Indonesia

Growth in Thailand’s established automotive industry is Government policies will encourage the next phase of growth in

expected to be supported by industrial policies and government ASEAN’s largest automotive market through measures, such as

incentive schemes to drive demand, such as trimming of easing vehicle loan requirements, suspension of a luxury vehicle

excise taxes for local EV manufacturing to increase OEM tax and incentives for EV uptake. Growing foreign investment

manufacturing activity. In 2016, Siam Motors set up a joint for production of lithium batteries in Indonesia is expected to

venture with JWD Infologics to provide integrated logistics position the country as a regional hub for battery production for

services for the automotive industry across ASEAN. EVs.

Malaysia Vietnam

Malaysia’s National Automotive Policy 2020 has been designed Vietnam’s government is supporting the fast-growing local

to spur growth in emerging areas such as EVs, Next Generation vehicle production industry through initiatives such as removal

Vehicle (NxGV), and Industry 4.0. There are also efforts to boost of import tariffs for auto parts and accessories to improve the

the domestic industry through the Energy Efficient Vehicles industry’s competitiveness. In 2018, Thailand’s AAPICO Hitech

Programme, which provides support for the local assembly established a JV with Vinfast for production of body-in-white

of hybrid EVs. In 2018, Malaysia signed a JV with Indonesia to parts in Vietnam.

develop the region’s first locally produced car brand.

Source: ASEAN Briefing, Automotive Logistics, Fitch Solutions, Malaysia Ministry of International Trade and Industry, Straits Times, Hanoi

Times, AAPICO

Autonomous Vehicle Test Centre in Singapore minimises risks of driverless

vehicles through rigorous testing

Background Initiative Control Industry adoption

Nanyang Technological The CETRAN AV Test Centre supports In terms of funding,

University (NTU) teamed autonomous vehicle (AV) trials with a testing the government has

up with the Land regime to assess the safety and readiness awarded funding for

Transport Authority of any AVs for Singapore’s public roads. AV trials to a number

(LTA) and Jurong Town Currently, all testing requires a qualified of organisations, such

Corporation (JTC) to onboard safety driver who will be able to take as NuTonomy (for its

opened CETRAN (Centre control of the vehicle in an emergency, hold robo-taxi service in

of Excellence for Testing third-party liability insurance, and share data Singapore), Singapore

& Research of AVs) in from the trials with LTA. This structure gives Technologies and NTU-

Singapore in 2017. assurance to the public relative to safety and Volvo (for the world’s first

provides a structure for the regulator to learn full-size, autonomous

about the technology and build effective electric bus).

long-term regulation.

Source: Economic Development Board

Borderless Business: Intra-ASEAN Corridor 13Our Growth Watchlist

3. Post-COVID-19 economic liberalisation. Moreover, the sector has also

received FDI worth USD56.3 billion between

recovery and easing FDI 2015 and 2019, of which 23.2 per cent was

restrictions expected to boost intra-regional. As ASEAN emerges from the

COVID-19-induced economic slump, the region’s

development of ASEAN’s construction industry is expected to restart

construction and real estate its growth trajectory once economic activities

industry resume. In this regard, the construction industry

(for residential and non-residential buildings)

The real estate sector in ASEAN has witnessed is expected to grow at a CAGR of 11.9 per cent

considerable growth in recent years, from USD105.5 billion in 2020 to USD184.9

supported by growing urbanisation and trade billion in 2025.

Figure 7: Value of residential and non-residential construction industry in ASEAN-6

CAGR: 11.9% CAGR by Country

USD billion

Malaysia

200.0 184.9 9.0%

167.9 11.4

157.2 10.9 12.2 Singapore

8.9%

10.2 11.4 13.8

150.0 139.3

10.6 12.8 21

122.5 9.2

9.8 12 19.1

Thailand

105.5 8.5 17.4

8.9%

9.2 11.1 35.5

7.3 15.9 31.7

100.0 8.3 10.3 28.9 Vietnam

9.6 14.3 8.3%

26.1

12.6 21.9

16.3 91

50.0 78.1 82.1

67.1

58.4

51.4 Indonesia

12.1%

0.0

2020 2021 2022 2023 2024 2025

Indonesia Vietnam Thailand Singapore Malaysia

Source: Fitch Solutions

Demand in the construction sector is Things (IoT) to manage this complexity. BIM

expected to be driven by overall infrastructure was adopted by Singapore in 2010, leading

development, as well as rising income and to increased productivity in the industry; and

consumption levels. Moreover, government it is starting to be adopted by other ASEAN

efforts to attract foreign investment vis-à-vis countries. For example, Vietnam approved a

reforms are expected to further propel growth 2017-2021 roadmap for implementation of BIM

in this sector. As projects in ASEAN grow larger for construction and operation management

in size and increasingly complex, companies will in 2016. Adoption of such innovations to drive

need to look at digital solutions such as Building efficiency and productivity is expected to shape

Information Modelling (BIM) and Internet of the future of ASEAN’s construction industry.8

Investment-friendly policies to drive growth across real estate segments in key markets across ASEAN

Indonesia Philippines Vietnam

The Indonesian government has pushed Although the Philippines has historically In addition to Vietnam’s 2015 Law on

through various reforms, such as the had restrictive regulations on foreign Housing that eases restrictions on

Omnibus bill (passed in 2020) to ease ownership, the recent establishment of foreign ownership on residential housing,

foreign investment and ownership in the REIT market is expected to facilitate Vietnam’s recent Law on Investment

the real estate sector. In 2020, Alpha more real estate investment in the 2020 seeks to attract further foreign

Investment Partners, a subsidiary of country. Singapore-based CapitaLand’s investment by easing restrictions across

Singapore’s Keppel Capital Holdings, business unit, The Ascott Ltd, partnered sectors. In April 2021, Thailand-based

partnered with Indonesia’s Mega with Cebu Landmasters in 2018 with the retail and shopping mall operator,

Manunggal Property and Manulife aim to manage 1600 units by 2022 as Central, announced a USD1.1 billion

Financial Corporation to launch a part of CapitaLand’s effort to expand the investment to expand across 55 cities in

USD200 million logistics property hospitality portfolio of their real estate Vietnam.

venture in Indonesia. business.

Source: Fitch Solutions, Oxford Business Group, Mondaq, Keppel Corporation, The Manila Times, Nikkei Asia, Capitaland, DFDL, Allen &

Gledhill, Vietnam Investment Review

Borderless Business: Intra-ASEAN Corridor 14Our Growth Watchlist

4. Growing urbanisation and a 4.9 per cent CAGR growth from 2014 to

2019 as a result of increasing urbanisation

rising incomes to drive demand and a growing middle class with higher

for Food and Beverage products consumption power. In addition, ASEAN’s

market potential has attracted increased

in ASEAN investments in manufacturing, including from

Household spending on food and beverage international players, buoyed by the region’s

(F&B) in ASEAN is expected to further improving business environment, relatively low

accelerate from 2020 to 2025 with a manufacturing costs, and maturing logistics

projected CAGR of 7.3 per cent, following infrastructure.

Figure 8: Household spending on food and beverage products in ASEAN-6

USD billion CAGR: 7.3% CAGR by Country

800.0 760.1 Singapore

12.4 2.8%

701.2 49.3

700.0 665.1 11.9

11.4 45.2 83.3

608.3 41.5

Vietnam

567.7 10.9 77.5 7.7%

600.0 9.9 38.6

535 10.8 71.5 103.1

35.1 64.3

34 97.2 Malaysia

500.0 57.4 93.3

53.8 88.3 9.1%

84.6 152.1

400.0 82.1 132.7 139.6

126 Thailand

107 119.5 4.7%

300.0

360

200.0 314.6 329.7

261.2 280.1

247.3

100.0 Indonesia

7.8%

0.0

2020 2021 2022 2023 2024 2025

Indonesia Thailand Malaysia Vietnam Singapore

Note: Data includes household spending on food, alcoholic beverages and non-alcoholic beverages

Source: Fitch Solutions

As consumers across ASEAN become more food. There is also an increased demand for

health conscious and proactive about their alternative protein and plant-based products,

physical and mental well-being, there is a as a result of more consumers adopting

growing demand for products in the ‘better flexitarian diets. In Thailand, demand for plant-

for you’ segment. For instance, as per the based meat is forecasted to increase by 200 per

World Economic Forum report titled ‘Future of cent over the next five years. From a distribution

Consumption in Fast Growth Consumer Markets perspective, F&B companies looking to expand

ASEAN 2020’, in Indonesia, 75 per cent of the in ASEAN should pay attention to e-commerce

urban population aims to eat a healthier diet, as a significant channel for sales, as a result

while in Vietnam, 90 per cent of consumers of the increasing digital adoption across the

say they are willing to pay more for healthy region.9

Borderless Business: Intra-ASEAN Corridor 15Our Growth Watchlist

Business-friendly incentives and growing market driving intra-ASEAN expansion in F&B industry

Indonesia Philippines Thailand

Foreign players looking to enter Regulations such as the CREATE Act and Thailand is well-known for its food

Indonesia’s F&B market need to be investment programmes like ‘Make It processing industry and is looking to enter

cognisant of the country’s 2019 Halal Happen in the Philippines’ have been the next phase of growth through its high-

Product law, which requires consumer designed to make the country’s business tech Eastern Economic Corridor (EEC).

products to be halal certified. This law environment friendlier for foreign The country has tried to position itself as a

underpins the country’s goal to be a manufacturers. In 2019, Indonesia-based Food Innovation Hub for future advances

global hub for halal manufacturing, Mayora Indah announced plans to invest in food technology. Jakarta-based, fully-

providing manufacturers setting up USD80 million over 5 years to produce tech enabled coffee chain Flash Coffee,

production here with further growth coffee mixes in the Philippines to expand opened its first Thailand location in 2020

opportunities. In 2017, Singapore-based its market share in the country’s booming and has launched over 25 more outlets in

Delfi partnered with Japan-based Yuraku coffee market. the country since.

Confectionery to produce and market

Delfi’s chocolates in the country.

Source: ASEAN Briefing, Confectionary, Philippine News Agency, Nikkei Asia, Asia Pacific Food Industry, Nestlé, Minime Insights

5. Renewable energy generation consumption, with its electricity consumption

being among the fastest growing in the world

will play a prominent role in at a CAGR of ~6 per cent over the past 20 years.

ASEAN’s quest to meet its In 2020, ASEAN’s electricity consumption was

994 terawatt-hours (TWh) and is projected to

growing energy needs reach 1,287 terawatt-hours by 2025. To meet

Energy is at the forefront of the vision for the these energy needs in a sustainable manner, the

ASEAN Economic Community and has been ASEAN Plan for Energy Cooperation 2016-2025

identified as an integral part of creating an (APAEC), endorsed in 2014, has set a target to

integrated, well-connected, and resilient ASEAN. increase ASEAN’s renewable energy component

The region has seen increased development to 23 per cent of ASEAN’s energy mix by 2025.

in terms of urbanisation and growing

Figure 9: Renewable energy generation in ASEAN

TWh

TWH CAGR: 4.8%

271

262.5

300 254.1

244.1

232

213.9 CAGR by Segment

200

Hydropower

3.8%

204.5

200.2

150 195.6

190

182.2 Geothermal

3.9%

169.7

100

Solar

15.9%

30.2 31.2

50

28.0 29.4

25.7 27.5

Wind

18.4 20.4 23.1

11.1 13.9 16.1 10.4%

7.5

7.59 9.2

.2 10.0 10.7 11.5 12.3

0

2020 2021 2022 2023 2024 2025

Wind Solar Geothermal Hydropower

Source: Fitch Solutions

Borderless Business: Intra-ASEAN Corridor 16Our Growth Watchlist

Energy generated from renewable sources projected CAGR of 15.9 percent and is already

(excluding biomass and waste) was 214 TWh garnering investments from across ASEAN.

in 2020 and is expected to grow to 271 TWh by Thailand is the regional leader for energy

2025 at a CAGR of 4.8 per cent. Looking ahead, generation in the two fastest growing segments

this trend is expected to bring forth a spectrum – solar and wind – with 10.53 TWh generated in

of opportunities for regional cooperation 2020, which is expected to grow to 16.88 TWh

through APAEC Programme Areas such as by 2025. Vietnam is another significant market

‘ASEAN Power Grid’ and ‘Renewable Energy’, expected to see maximum growth in these

requiring new investments to increase installed segments, growing from 2.83 TWh in 2020 to

power capacity in the renewable sector. Within a projected 10.35 TWh in 2025, with a CAGR of

renewables, solar energy is expected to be 29.6 per cent.10

a significant growth segment, growing at a

Borderless Business: Intra-ASEAN Corridor 17Our Growth Watchlist

Solar energy is leading the region’s renewable energy development, supported by key government policies

Thailand Vietnam Philippines

Solar energy is an important growth Solar and wind energy are key growth There is increased focus on solar energy

segment for Thailand as it looks to areas for Vietnam’s renewable energy generation in the Philippines as per the

expand renewable energy generated industry. The government is encouraging country’s ‘Energy Plan 2040’. Additionally,

by the country, incentivised through development in the offshore wind sector geothermal energy (currently accounting

initiatives such as the Energy Ministry’s as a part of Vietnam’s National Energy for 70 per cent of renewable power

Solar Rooftop Scheme. In 2019, Singapore- Development Strategy. In April 2020, generated in the country), which

based Cleantech Solar was commissioned Thailand-based Super Energy Corporation previously did not allow foreign entities to

to install and operate solar rooftop announced an investment of USD457 hold a majority stake, will now allow 100

systems across 19 Tesco Lotus stores in million into four solar plants in Vietnam per cent foreign investment, paving the

Thailand. with a combined capacity of 750 MW. way for further development. Singapore-

based WEnergy Global announced an

investment of USD20 million into four

energy projects in the Philippines.

Source: Fitch Solutions, Cleantech Solar, Super Group, Vietnam Investment Review, WEnergy Global

Several companies, including Singapore’s WEnergy Global, form

partnership to finance renewable energy projects in ASEAN

Background Looking Ahead

Singapore’s WEnergy Global, CleanGrid Partners aims to build and manage a portfolio of

Greenway Grid Global (an invest- electrification projects valued at about USD100 million in the next

ment company with Japan’s TEPCO few years. WEnergy Global has already set the stage by initiating a

PowerGrid Corp as a major share- microgrid project in Palawan, the Philippines. This would be the largest

holder), and IMCG Partners have microgrid solar power plant in the Philippines that will generate 1.3

come together to form a USD60 megawatts of clean renewable energy and reduce the country’s diesel

million Singapore-based investment consumption; as well as provide power to over 600 customers – homes,

entity called CleanGrid Partners, businesses, and hotels.

which will finance and operate

renewable energy projects across Several other projects in the Philippines, Indonesia, and Myanmar are

ASEAN. also in the pipeline.

Source: Company websites

6. High digital adoption driving has had tremendous success in recent years

with regional leaders such as Lazada, Shopee

growth of e-commerce and and Tokopedia emerging across services such

digital platform services as online retail, online travel, online media,

transport and food. This trend was accelerated

Home to over 400 million internet users, last year as a result of COVID-19, leading to

the ASEAN market poses a plethora of a significant gross merchandise value (GMV)

opportunities within the digital ecosystem. The of USD104 billion in 2020 that is forecasted

region’s swift digitalisation has given way for to grow at a CAGR of 24 per cent to USD309

growth of digital services across sectors such as billion by 2025.

e-commerce and cloud services. E-commerce

Borderless Business: Intra-ASEAN Corridor 18Our Growth Watchlist

Figure 10: E-commerce GMV in ASEAN-6

USD billion

Source: Google & Temasek, e-Conomy SEA, 2020

In 2020, ASEAN launched the ‘Go Digital Indonesia also enhancing their capabilities. As

ASEAN’ initiative in partnership with The Asia the ASEAN Digital Master Plan 2025 prioritises

Foundation and Google to support MSMEs development of digital infrastructure in the

(Micro, Small and Medium Enterprises) in the region, expansion across the region is expected

region to take advantage of this looming to become more accessible for companies in

opportunity through upskilling them in digital the digital space.11

tools and technologies and providing grants.

With companies in ASEAN gaining greater

digital maturity in the forthcoming years,

digital platforms and cloud-based services for

enterprises such as data analytics, artificial

intelligence, machine learning and IoT will have

greater expansion opportunities. As a result of

this trend, Southeast Asia is projected to be the

world’s fastest growing region for data centres.

Currently, Singapore is the regional leader

for data centre supply, with Malaysia and

Favourable government policies encouraging investments in e-commerce

Indonesia Thailand Vietnam

To attract technology-related investment, Growth of e-commerce in the country The government’s National E-commerce

the government has established friendly has been driven by the government’s Development Plan 2021-2025, focused

FDI policies and now allows 100 per National E-commerce Strategy (2017- on boosting e-commerce adoption,

cent foreign ownership of e-commerce 2022) and initiatives, such as the envisages that 55 per cent of the

businesses in the country. In 2020, PromptPay E-payment service, making it population will shop online by 2025 with

Singapore-based Grab invested USD100 an attractive destination for investment. average annual online spending per

million in Indonesia-based e-wallet Indonesia-based Gojek launched a new consumer rising to USD600 by 2025,

company LinkAja and inaugurated a Tech app for Thailand in 2020 to gain a greater up from USD202 in 2018. In 2019, Grab

Centre to test tools and technology for the foothold in the market. announced plans to invest USD500

MSMEs market in the country. million over 5 years in Vietnam to spur

development of the country’s digital

economy.

Source: Fintech News Singapore, Nikkei Asia, Grab

Borderless Business: Intra-ASEAN Corridor 19Acting with Impact: Five Focus Areas for ASEAN Companies to Drive Resilient Growth Within the Region

Five Focus Areas

Navigating ASEAN’s fast-evolving and diverse companies are also focused on executing

landscape requires companies to focus on a digital programmes with a view to enhance

few critical areas to achieve success. Figure cyber resilience, and gradually incorporating

11 (below) illustrates the key focus areas that sustainability and ESG principles into

ASEAN-native companies are prioritising to their business practices. Finally, in view of

stay competitive and drive resilient growth. fundamental shifts on the global stage,

These include forging key partnerships with companies are also diversifying their supply

local stakeholders and reinforcing governance chains across ASEAN to guard against

and risk management frameworks. Given anticipated disruptions.

ASEAN’s rapid digitalisation and urbanisation,

Figure 11: Key focus areas to drive resilient growth in ASEAN

Note: Survey question asked: ‘What are the key initiatives / focus areas for your organisation to drive resilient and rebalanced growth in

ASEAN? Please select the relevant options and rank them in order of importance, 1 being the most important.’

Values indicated above refer to the % of survey respondents who included the initiative as one of the top 3 ranked choices

Source: Standard Chartered Survey, 2021

Borderless Business: Intra-ASEAN Corridor 21Five Focus Areas

1. ASEAN offers ideal conditions Diversification needs a holistic approach

for diversified supply chain

Despite advantages brought about by

networks ASEAN’s diverse manufacturing ecosystem,

With the Fourth Industrial Revolution well diversity can also create challenges for

under way, ASEAN’s manufacturing landscape companies looking to operate across the

is experiencing fundamental disruption. Its region. When assessing how to optimise

supplier and production landscape is maturing, production footprints, companies must go

with advancing manufacturing processes beyond basic due diligence or a cost focus

and increasing productivity on the back of and closely evaluate risks – geopolitical,

automation initiatives. ASEAN members with regulatory, business, environmental, etc. –

significant manufacturing capabilities have particular to each market. Even with efforts

potential productivity gains of around USD216 to integrate and streamline standards

to 627 billion. Figure 11 shows that 35 per cent across ASEAN members, each country still

of our survey respondents are keen to build has its own modus operandi, which incom-

production capacity in new locations in ASEAN. ing investors should become familiar with

to avoid any pitfalls when diversifying their

However, digital adoption across ASEAN’s supply chains.

manufacturing landscape is not homogenous.

While more mature manufacturing bases

such as Thailand and Malaysia are focusing

on high-tech manufacturing, middle-income

markets like Vietnam are building capacity in

more labour-intensive production and focusing

on expanding their network of industrial parks

to create manufacturing hubs. Companies

should leverage ASEAN’s manufacturing

diversity to build production networks that are

well-diversified and therefore more resilient in

weathering future disruption.

Borderless Business: Intra-ASEAN Corridor 22Five Focus Areas

operations

build an intra-regional operations network.

Thailand Vietnam

• Manufacturing industry share of • Manufacturing industry share of

GDP (2020): 27.93% GDP (2020): 16.30%

• Strong manufacturing base, well- • Geographical pr

developed infrastructure, and relatively lower labour costs

• Focus on labo

especially for automotives manufacturing in sectors such

as garments and footwear, and

Malaysia automotive clusters

• Manufacturing industry share of • Incr

GDP (2020): 20.45% electronics assembly

• Low

machinery and parts

• Manufacturing industry share of

• Industry 4.0 to drive growth in GDP (2020): 18.45%

sectors such as electrical and • High energy productivity and

electronics, chemicals and

climbing up the value chain slowly.

chemical products, and machinery

However, low-tech manufacturing

and equipment in F&B and textiles continue

to dominate

Singapore

• Growth in high-tech segments

• Manufacturing industry share of such as chemicals and electronics

GDP (2020): 20.25% supported by government

• Robo

manufacturing, advanced

Indonesia

• Manufacturing industry share of

• Strong and diverse manufacturing GDP (2020): 20.67%

• Emerging technology value

for sectors such as aerospace, chains, has the comparative

advantage to advance itself

as a technology hub, especially

in EV manufacturing

Potential high-growth manufacturing sectors

Automotive Chemicals Robotics and AI Food and Electronics

beverage

Textiles and

sciences footwear

News Asia, Insights Solutions Global

With ASEAN members fast evolving in terms At the same time, manufacturers would benefit

from having a presence in other locations

hubs are emerging across the region. For

example, Vietnam is focusing on developing wish to carry out R&D or Sales & Marketing

tech and automotive clusters in the North of

Vietnam or Indonesia; and assemble products

to lure in advanced manufacturers. Targeting in more advanced manufacturing hubs such as

the further development of production hubs

to shorten supply chains, effectively reducing

when responding to demand.

Borderless Business: Intra-ASEAN Corridor 23Five Focus Areas

B. Broadening supply bases by leveraging MPAC 2025 focuses on improving the logistics

ASEAN’s growing connectivity network among ASEAN countries by removing

trade barriers and cross-border obstacles,

To build resilience against uncertainties, ASEAN

allowing for more seamless logistics in moving

manufacturers should focus on addressing

materials and finished products around the

their most pressing vulnerabilities: supply chain

region.

disruptions and materials and component

sourcing. By concentrating manufacturing Companies operating in this corridor can

within at least one or two of ASEAN’s capitalise on initiatives such as the ASEAN

production hubs, manufacturers would be Single Window, single shipping and aviation

able to benefit from tapping into a network of markets, and the ASEAN Database on Trade

regional suppliers, which would allow them to Routes, and Framework for Enhancing Supply

maintain a broad, and therefore more resilient, Chain Efficiency, to realign their footprint in

supply base. However, a notable 66 per cent of ways that can further reduce production costs

respondents currently see building relationships and strengthen supply chain resilience against

with suppliers and adapting supply chain global disruptions. Moreover, the ASEAN

logistics as a significant challenge in the next Customs Transit System (ACTS), implemented

6-12 months.e across six ASEAN countries - Cambodia, Laos,

Malaysia, Singapore, Thailand and Vietnam -

Despite challenges, the increasing maturity of

can help companies reduce the time and cost,

suppliers across the region, as well as ASEAN’s

as well as improve the tracking and movement

growing connectivity via the AEC and AFTA, will

of goods by land, regionally. In the pilot phase,

facilitate the development of regional value

DHL Global Forwarding Singapore successfully

chains and diversified supply chains. This will,

carried out cross-border transit operations from

in turn, allow for a more reliable flow of goods

Singapore to Thailand through Malaysia in

and services and reduce the cost of expanding

October 2020 capitalising on the ACTS.12

into new markets within the region. In addition,

Vinfast works with Thailand’s Aapico Hitech and international

partners to prioritise localisation and build manufacturing

capabilities in Hai Phong

1 2

Background Impact

To achieve its localisation ratio of 60 per The JV between Vinfast and its Thai

cent, Vinfast worked with international partner shows the corporation's

suppliers to set up factories for parts and commitment to increase the localisation

components in its complex in Hai Phong, rate of its products. This JV would also be

Vietnam. the largest project ever undertaken by

Aapico and facilitated the latter’s entry

In June 2018, Vinfast signed a into Vietnam’s automotive market.

Memorandum of Understanding (MoU) for

a joint venture (JV) with Aapico Hitech, one

of Thailand’s leading auto parts manu-

facturers, to build a press shop in Vinfast’s

Supplier Park in Hai Phong to supply Body

in White (BIW) parts for Vinfast products.

“With this partnership, we believe that there will be more domestic and foreign companies

joining the Vietnamese automotive supplier industry. This is an important step in creating a

synchronous ecosystem for the Vietnamese automobile manufacturing industry.”

Nguyen Viet Quang, Vice President and CEO of Vingroup

e Value indicated refers to the % of survey respondents who included the significant challenge as one of the top 3 ranked choices

Borderless Business: Intra-ASEAN Corridor 24Five Focus Areas

2. ASEAN’s focus on digital A. Capitalise on digital business models to

capture new growth opportunities

advancement expected to

Disruptive technologies shift the value pools in

pave the way for companies to existing value chains. As a result, these shifts

strengthen digital capabilities generate new opportunities for both new and

and cyber resilience existing players. However, critical to companies’

continued growth in the region will be their

The digital economy can be a powerful enabler ability to capture these opportunities. To do

to help ASEAN transit into the more dynamic, so, companies must rethink their current ways

networked and innovative region that the AEC of working and drive digital transformation

envisages. Disruptive technologies – particularly across their business. From our survey, 52 per

big data, cloud technology, IoT, the automation cent of respondents indicated that they plan to

of knowledge work and the Social-Mobile- execute digital transformation programmes to

Analytics-Cloud (SMAC) – could unleash some drive resilient growth in the region.f

USD220 to 625 billion in annual economic

impact in ASEAN by 2030. As ASEAN’s growing consumer market demands

faster flows of goods and customer response

The MPAC 2025, acknowledging the potential times, companies should capitalise on Industry

of digital technology, has thus identified digital 4.0 innovations to redesign and improve their

innovation as another pillar for driving further manufacturing processes, reducing their time-

connectivity and inclusive growth in ASEAN. to-market and raising productivity. Notably,

Although communications and trade have HP Singapore had begun adopting digital

been growing exponentially across borders and solutions to increase productivity even before

devices, digital advancement has not been the pandemic hit. The company shifted from

uniform across all communities in the region. a labour-intensive, reactive, and manual work

Therefore, digital innovation could help bridge to highly digitised, automated work. This

this divide. freed up considerable task responsibilities,

offering employees the opportunity and time

ASEAN governments are adopting a series to learn new skills. Through a combination of

of programmes to stimulate companies to university partnerships and targeted training

strengthen their digital capabilities. Although programmes, HP upskilled its operators to

COVID-19 delayed the region-wide 5G rollout, technical specialists, and trained their technical

Thailand is now taking the lead to promote specialists to become engineers. As a result,

5G adoption across ASEAN, and this will likely the company reported a 70 per cent increase in

contribute to companies’ digital advancement productivity and quality, and a 20 per cent drop

across the region. At the national level, in manufacturing costs.

Malaysia has launched its digital economic

roadmap, MyDigital, which identifies cloud Moreover, digital technologies can help

technology, 5G, and cybersecurity as key areas companies gain better visibility of their supply

for Malaysia’s digital development. Similarly, chains across multiple territories and facilitate

Singapore has identified a series of Strategic cross-functional integration; therefore, also

National Projects, which includes streamlining enabling companies to transition from a

online processes for businesses via its national single production site to a series of regionally

project, GoBusiness.13 connected production networks.14

f Value indicated refers to the % of survey respondents who included the initiative as one of the top 3 ranked choices

Borderless Business: Intra-ASEAN Corridor 25Five Focus Areas

Role of financial partners

With on-the-ground knowledge, financial partners can help businesses simplify processes

and navigate regulatory complexities. Financial partners can also offer digital tools to

streamline and aggregate payment methods, with minimal need for technological know-how,

investment or operating requirements, which provides a more seamless experience overall.

Standard Chartered’s digital solutions include online, last mile and in-store, and invoice collections,

multi-channel payment links and instant payments, among others, which are available across multiple

ASEAN countries

Multi-Channel Payment Links Online Collections Last Mile and In-Store Collections

• Due to COVID-19, the Hindu • DHL had to rethink their cash • A leading consumer electronics,

Endowments Board (HEB) in payment ecosystem to minimise IT and furniture retailer wanted

Singapore wanted a “light paper-based processes and to provide an additional payment

touch” online collections facilitate payments in local option – instant payment at

solution without the hassle of currencies across different checkout, in addition to payments

managing a website, app or markets. by credit card or cash.

POS (point-of-sale) terminals.

• Standard Chartered partnered • Standard Chartered collaborated

• With Standard Chartered’s with DHL to co-create an online with the retail client to integrate

payment link feature – collections solution that would their POS terminal with the bank’s

Straight2Bank Pay – HEB could allow DHL’s customers across Asia Straight2Bank Pay platform to

collect payments via e-mail, to make online payments via the generate dynamic instant payment

SMS, digital invoice or social DHL portal using local payments, QR codes.

media (WhatsApp), providing bank transfers, e-Wallets and

operational efficiency and a cards; as well as a QR code • Shoppers can scan the QR code

seamless experience for both generation app to generate using their smart phone and

the client and its devotees. dynamic QR codes for accepting authorise contactless payment via

payments for shipments at DHL’s their mobile banking app.

service points in Singapore.

B. Prepare to address potential risks Figure 13: ASEAN initiatives to bolster

associated with varying data protection regional digital connectivity

regulations ASEAN Framework

on Digital Data Governance

Although digitalisation across ASEAN has not Dec

2018 Aims to engender trust in the collection

been uniform, the region is gradually working of data and its use by businesses, and to

towards that goal through multiple initiatives. encourage the innovation and adoption of

(see Figure 13). The ASEAN ICT Master Plan digital solutions in ASEAN.

2020 (AIM 2020) articulates the bloc’s ambition

ASEAN International

to establish an ICT single market, as part of Mobile Roaming Framework

achieving an integrated ASEAN Community, Nov

Seeks to promote transparent and

and underscores the role of ICT as a ‘horizontal 2017 affordable international mobile data

enabler of all sectors’ in the region. roaming services in ASEAN.

Complementary to ASEAN’s digital integration ASEAN Framework

efforts, the MPAC 2025 also seeks to improve on Personal Data Protection

Nov

open data use and digital data management Aims to strengthen ASEAN cooperation in

2016

in the region by establishing an ASEAN open personal data protection through domestic

laws and regulations, spanning topics

data network and digital data governance such as: consent, notification and purpose;

framework, respectively. Currently, digital accuracy of personal data; security

capabilities and data governance regimes safeguards; transfers to another country or

territory; retention (of data);

differ significantly across ASEAN member and accountability

states. National authorities place different Source: ASEAN Digital Master Plan 2025, ASEAN Framework on

Digital Data Governance

Borderless Business: Intra-ASEAN Corridor 26You can also read