CRYPTO PROXIMA AN ANALYSIS OF AUTONOMOUS BITCOIN TRADING SIMON ANDERSSON JAKOB HÄGGSTRÖM URLICH ICIMPAYE HJALMAR LINDSTEDT - DIVA

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MAT-VET-F-21012

Examensarbete 15 hp

Juni 2021

Crypto Proxima

An analysis of autonomous Bitcoin trading

Simon Andersson

Jakob Häggström

Urlich Icimpaye

Hjalmar Lindstedt

Abstract

Crypto Proxima

Simon Andersson, Jakob Häggström, Urlich Icimpaye, Hjalmar Lindstedt

Teknisk- naturvetenskaplig fakultet

UTH-enheten The purpose of this project is to analyze to what extent it is

possible to profit from autonomous bitcoin (BTC) trading. This was

Besöksadress: tested by using three different models in varying complexity and

Ångströmlaboratoriet

Lägerhyddsvägen 1 simulating these using real market data. The tested models were a

Hus 4, Plan 0 Long Short Term Memory (LSTM) neural network, a technical analysis

model based on moving averages (MA), and a random model that

Postadress: generates different buy and sell points. The LSTM model showed

Box 536

751 21 Uppsala indications of possible profitability when trading at higher

frequencies. For certain parameters, the model outperformed the

Telefon: market. The MA model was tested using a combination of different

018 – 471 30 03 parameters for a total of 48 simulations. These had different trade

Telefax: offs based on the combinations, where some were able to predict the

018 – 471 30 00 market to some extent. Regarding the random interval model, the

results showed that the simulations were normally distributed around

Hemsida: approximately half of the market gain or loss. The reason behind this

http://www.teknat.uu.se/student

is likely because the model is invested half of the time, and idle

the other half. It seems that autonomous trading definitely can be

profitable, however choosing the optimal parameters remains as a

subject for further research.

Handledare: Kaj Nyström

Ämnesgranskare: Natalia Ferraz

Examinator: Martin Sjödin

ISSN: 1401-5757, MAT-VET-F-21012

Tryckt av: Uppsala

Populärvetenskaplig sammanfattning

I följande projekt har det undersöks i vilken utsträckning det är

möjligt att dra till nytta av autonom bitcoin-handel (BTC). Detta

testades genom att använda tre olika modeller av varierande kom-

plexitet och simulera dessa med marknadsdata. De modellerna som

prövades var ett neuralt nätverk som kallas ”Long Short Term Mem-

ory” (LSTM), en teknisk analysmodell baserad på glidande medelvärden

(MA) och en slumpmässig modell som slumpmässigt genererar olika

köp- och säljsignaler. LSTM-modellen visade indikationer på möjlig

lönsamhet vid handel på högre frekvenser. För vissa parametrar överträffade

modellen marknaden. MA-modellen testades med en kombination av

olika parametrar för totalt 48 simuleringar. Dessa hade olika avvägningar

baserat på kombinationerna, där vissa kunde förutsäga marknaden i

viss utsträckning. När det gäller den slumpmässiga modellen visade

resultaten att simuleringarna normalt fördelades runt ungefär hälften

av marknadsvinst- eller förlusten. Anledningen till detta beror troli-

gen på att modellen var investerad hälften av tiden och inaktiv den

andra hälften. Autonom handel kan vara lönsam, men att välja de

optimala parametrarna förblir emellertid ett ämne för vidare forskn-

ing.Contents

1 Introduction 1

1.1 Background . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.2 Purpose . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

2 Theory 2

2.1 Long Short Term Memory . . . . . . . . . . . . . . . . . . . . 2

2.2 Moving Average . . . . . . . . . . . . . . . . . . . . . . . . . . 4

2.3 Random Time Intervals . . . . . . . . . . . . . . . . . . . . . . 5

3 Method 6

3.1 Data preprocessing . . . . . . . . . . . . . . . . . . . . . . . . 6

3.1.1 API . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

3.1.2 TimeSeries . . . . . . . . . . . . . . . . . . . . . . . . . 6

3.2 Model Implementation . . . . . . . . . . . . . . . . . . . . . . 7

3.2.1 LSTM . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

3.2.2 Moving Average . . . . . . . . . . . . . . . . . . . . . . 9

3.2.3 Random Intervals . . . . . . . . . . . . . . . . . . . . . 9

3.2.4 Simulation . . . . . . . . . . . . . . . . . . . . . . . . . 9

4 Results 10

4.1 LSTM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

4.2 Moving Average . . . . . . . . . . . . . . . . . . . . . . . . . . 12

4.3 Random Intervals . . . . . . . . . . . . . . . . . . . . . . . . . 14

5 Discussion 16

5.1 LSTM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

5.2 Moving average . . . . . . . . . . . . . . . . . . . . . . . . . . 17

5.3 Random intervals . . . . . . . . . . . . . . . . . . . . . . . . . 18

6 Conclusion 181 Introduction

1.1 Background

Ever since the first stock market opened in Amsterdam 1653 people have

been trying to predict the future prices of goods and assets [1]. Regardless of

various bursted bubbles and financial crises, the stock market has survived.

The recent invention of cryptocurrencies have allowed for a new type of mar-

kets where these cryptocurrencies are traded. These exchanges work in the

same manner as a regular stock exchange, with a few exceptions. The stock

market is only open for a few hours on working days, while the cryptocur-

rency exchanges are open everyday around the clock.

One advantage that cryptocurrencies provide is that they are available to

anyone in the entire world. While you might only be able to buy stocks in

your own country and a few others, these purchases must be done within the

legislation of the laws and bureaucratic systems in that particular country

and stock exchange. This is in direct contrast to cryptocurrencies where any-

one, anywhere, can buy cryptocurrency. Since it is a decentralized currency,

nobody can legislate the terms of conditions. This also allows anyone to send

crypto to anyone else in the world without having any obstacles or having to

use an intermediator[2][3].

Another key difference between stock- and cryptoexchanges is that cryp-

tocurrencies are also a means of payment. However, it is not yet advanta-

geous to use these cryptocurrencies over regular fiat currencies when trading

goods online. This is why BTC is often treated as an asset, or store of

value, instead of an actual currency. Since the value of BTC is significantly

higher (in relation to other fiat currencies) and extremely volatile, it makes

it unreliable and inconvenient to use as a means of payment in practise [3].

1.2 Purpose

In this project the goal is to examine what type of methods is suitable to use

in order to autonomously trade BTC and to maximize the profit. Three dif-

ferent methods were used, and were tested using different hyperparameters.

Based on simulations they were compared on the profit that they made, us-

ing data from the BTC market. The selected models had varying complexity

1in order to see if this had any impact on the profitability. These methods

are not exclusively used to analyze data from BTC, they could be used to

analyze any data from a time series. The main reason for why BTC was

chosen to be analyzed in this project is due to the availability of data.

2 Theory

2.1 Long Short Term Memory

The importance of order and causality is recurrent in various fields. A simple

example is predicting the last word of a sentence. You need the permutation

of the earlier words in order to understand the context of the sentence, which

gives the basis of a valid prediction. Another problem that takes order into

account, is this very project. The aim is to predict future prices, and to

do so you need to take past data in time into account in order to make a

valid prediction. A model that might be a appropriate fit to this problem,

is a Long Short Term Memory network. LSTM (Long Short Term Memory)

networks is a type of recurrent neural network that has the ability to store

important information from the past [4]. It deciphers patterns in a text or

a time series by processing information trough a network of hidden cells, or

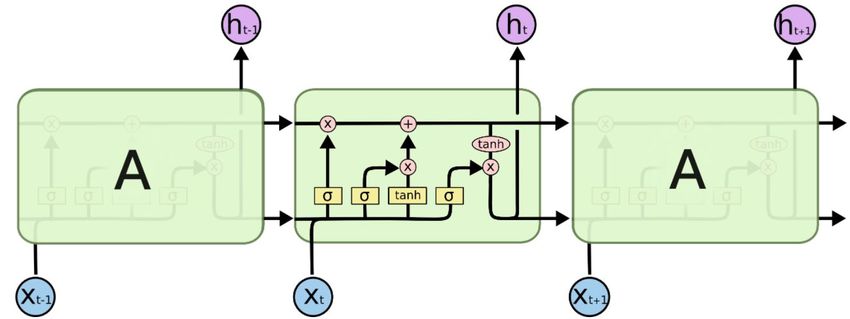

also called hidden units, which has the architecture as shown in figure 1.

Figure 1: The architecture of a LSTM network. Taken from [4]

Each cell that is shown in figure 1 is built in different gates that decides

whether to forget or to remember current and past information by using

sigmoid and hyperbolic tangents as acivation functions. The information is

stored in in a so called cell state Ct , which is the essential building stone in a

2LSTM network. Every hidden unit has its own cell state, but not necessarily

unique, since it is connected with the neighbouring cell of the last timestep.

If the gates decide to keep the cell state of the past and neglect the infor-

mation from the current timestep, then the cell last state flows through the

current hidden unit unchanged.

How does the LSTM network operate? Firstly, the information from the

input xt , which is often a tensor of dimension (number of sequences, length

of each sequence, number of features in each sequence), is concatenated with

output of the last cell ht−1 . Thereafter, the new tensor flows into the first

layer, which is the forget gate. Here it is decided if the output of the last

cell is still relevant in respect to the current input. For example, if you are

to predict the next price of BTC, and the sequence at the earlier timestep

indicates stagnation but the current sequence implies an increase, then it is

not necessary to keep the information from the past. In a LSTM point of

view, the concatenated tensor goes through a sigmoid activation function,

which transforms all values into the range zero to one, where zero means

forget entirely and one remember everything.

After deciding if the information of the past is worth keeping, you also need

to evaluate the relevance of the new information. This is done when the

information tensor enters the input gate layer. The gate has two operations

that work in parallel on the information tensor. Firstly you decide on what

extent you are to remember the new information. This is done in similar

fashion to the forget gate where the tensor flows into a sigmoid function that

decides the relevance of the current information. The input gate layer also

calculates a candidate C̃t for the current cell state by using a hyperbolic tan-

gent function with the input tensor as input. Finally, the current cell state

becomes the sum of the old and new candidate weighted with the output of

the corresponding sigmoid function of its gate. In mathematical terms:

Ct = ff orget ∗ Ct−1 + finput ∗ C̃t (1)

The last part of the cell is the output gate. The output from this gate is

mostly decided by the current cell state, where the gate is simply a hyperbolic

tangent function the cell state as input multiplied with a sigmoid function,

in similar manner to the other gates. In order to interpret the output from

the LSTM network, you need to connect a dense layer to the output layer.

The choice of dense layer depends on the application, for instance, if you are

3to predict the next word in a sentence, then a dense layer with a softmax

function that calculates the next word with a certain probability would be a

appropriate choice [5].

2.2 Moving Average

Another model used in the project was the moving average model, MA. It

utilises three parameters of a time series to make decisions such as buy and

sell.

• LA - The long average,

• SA - The short average

• ∆ - The band width

LA is an arithmetic average of the price calculated over a given time pe-

riod. SA is also an arithmetic average, calculated over a smaller time period

than the long average. The reason why it’s called a moving average is because

these averages are updated along the data set. SA could be calculated for

the latest hour, and when given new price data it’s calculated again. Finally,

∆ is a constant which defines a band region B together with LA. This region

is defined as LA ± ∆.

At every time instance, SA is compared against B, (the sum or difference

of LA and ∆). A sell signal would happen if SA is larger than the sum of

∆ and LA, given that there is an asset to sell. On the other hand, a buy

signal occurs when the short average is smaller than difference between the

long average and the lower boundary. The algorithm is as follows:

1 i f ( ( SA > LA + D e l t a ) and have a s s e t ) :

2 return ’ S e l l ’

3 e l i f ( ( SA < LA − D e l t a ) and not have a s s e t ) :

4 return ’ Buy ’

When the a sell signal occurs all of the asset are sold, while a buy signal only

occurs if there’s no asset in the portfolio. An example of how the algorithm

works can be visualised in figure 2.

4Figure 2: A visualisation of the algorithm behind MA

The short and long average are the green and red lines respectively, while

the blue line is the price and the dashed lines are the border of region B.

The green and red dots in the graph indicate when the trading bot bought

or sold its assets.

The idea behind the algorithm is that SA detects temporary price trends,

while LA represents a more stable, long term trend. When SA crosses the

lower bound of region B the asset might be undervalued, which is a buy-

signal, and vice versa for the upper bound.

2.3 Random Time Intervals

The price of BTC is highly chaotic, and very hard to predict in general.

A random model is an interesting baseline to compare the other models

against.

53 Method

3.1 Data preprocessing

3.1.1 API

Binance is a criptocurrency exchange, where investors can trade crypturren-

cies. Binance also offers an application programming interface (API). That

allows users to connect to Binance’s servers via several programming lan-

guages and pull data. Historical data on BTC was collected with features

such as opening price, high, low, closing price, volume, quote asset volume,

number of trades, taker buy price and taker buy quote asset volume. The

data gathered spanned from 2017 October to 2021 April. The time incre-

ments between each datapoint was one minute.

To achieve the aforementioned data gathering, the API was used in Python

programming language. The function ”get historical klines” was used to re-

trieve the historical data, which returned the data in array format [6]. This

was then converted to a data frame, because of the functionality it offers. The

features were normalized in order to reduce the training time, as followed:

x−µ

(2)

σ

where x is the sample, µ is the mean of the training samples and σ is the

standard deviation of the training samples. This was done using scikit-learn’s

prepossessing package [7] .

3.1.2 TimeSeries

The output from the API was csv-file. The package pandas offers many

features and functionalities when it comes to these files [8]. A new class,

TimeSeries, was defined in order to provide something more niched for our

project.

A TimeSeries class object is initialised with a csv-file or pandas DataFrame

from the API. The class extracts the properties of interest from the data,

and saves it. The class has methods for splitting data easily and for plotting.

The models Moving Average and Random Time Intervals both work with

data from TimeSeries objects.

63.2 Model Implementation

3.2.1 LSTM

The construction of the LSTM based trader was done in two parts, train-

ing a LSTM model to predict future prices and utilize it by implementing a

trading strategy. Since this projects aim is to evaluate different approaches

to autonomous trading, the focus will rather lie on the models performance

while trading rather than its ability to predict future prices and finding the

best possible model to describe the cryptocurrency market.

A LSTM network was implemented by using the LSTM module from open

source machine learning package pytorch. The module constructs a neural

network depending on your desired dimension of input, dimension of output,

number of hidden units and layers, which means how many LSTM networks

you choose to stack on each other. Furthermore, you need to interpret the

output from the LSTM network in a dense layer. The desired output is the

future price, which is a quantity, and therefore you need a regression model

that produces a numerical value from a certain input. In this case a pytorch

function linear was chosen to be used in the dense layer. The function works

as a general linear regression model, which performs a linear transformation

on the input matrix to the desired output dimension.

Machine learning models such as LSTM needs training data to find a fit.

The training data set training data set that was used to fit the model con-

tained the price of BTC in USD every full hour since the Binance market

opened. Since the LSTM model essentially interprets sequences, you had

to transform the dataset into a tensor of several batches of time sequences.

In other words, the original data set is split into slices of time interval of

a chosen length and the slice moves one time step at a time. For example,

one batch might contain the prices of BTC at timestamps 10:00-15:00, and

the next batch includes prices at 11:00-16:00. This results in a tensor of

dimension (number of batches, interval length, number of features), where

number of features always has dimension one since the dataset only includes

one feature. The output becomes the price at timestamp after the last ele-

ment in a sequence. For example, if your input is BTC prices at timestamps

10:00-15:00, then your output is a prediction of the price at 16:00.

7When the data is prepared, then the model is set for training. In order

to make it possible to evaluate the model in a simulation, the whole data set

is split into two sets where 97% is used for training and the last 3% is left for

evaluation and simulation. The model is trained by using ADAM, which is

a optimization algorithm that finds the parameters that minimizes the loss

function, which in this case is chosen to be a mean square loss function since

this is a regression problem. This algorithm is repeated multiple times, be-

cause it is not guaranteed that you find the minimum after one iteration or

in machine learning terms epoch. Therefore you perform the optimization

until the mean square loss is sufficiently small [9].

Fitting a LSTM network is a rather computational expensive process be-

cause the number of parameters in the model grows quickly as you increase

number of hidden units or layers [10]. This makes it difficult to run an

autonomous process that finds the most optimal parameters because of the

long training times or without risking maximizing the RAM. The parameters

in the model were therefore chosen to be relatively low. Furthermore, the

length of the price sequences in the training data set was also varied, and the

combination of sequence length, number of hidden units and layers that had

the least mean square error relative to the validation data set was chosen to

be used in the simulation. The most optimal model that was found in this

project was sequence length of twenty hours, two layers and fifty hidden units.

When the model is finalized, then the next task is to implement a trad-

ing strategy that makes trades based on the prediction of the model. The

strategy that was implemented together with the LSTM model in this project

was an own constructed short term strategy that utilizes the prediction of

the price a hour forward in time. If you know the current price Pt and you

∗

make a prediction for the price a step forward in time Pt+1 then you can

∗

formulate the decision function D(Pt , Pt+1 , r) as:

P ∗ −Pt

Buy

if t+1Pt > r

∗ P ∗ −Pt

D(Pt , Pt+1 , r) = Sell if t+1Pt < −r (3)

Do nothing else

Where r is a user chosen threshold value that sets the decision boundary for

the trader. The decision in equation 3 is made by calculating the predicted

percentual change in the predicted price relative to the current, and if the

8rate is larger or lesser than the chosen threshold, then an action is made. You

can also consider the threshold parameter as a setting of trading frequency,

since it performs a trade depending on percentual rise of the upcoming price.

The lesser the threshold value, the more likely you are to make a trade since

the interval in where you make the decision to do nothing ([−r, r]) decreases.

This was further on implemented in python, where the model was trad-

ing on validation data for different threshold values. It was assumed in the

simulation that you didn´t know the next datapoint, and the prediction was

calculated with the price of the current hour and the 19 earlier ones. This

was iterated through period March to April 2021, and the accumulation of all

the transactions made in the simulation was compared to the price difference

of BTC of the first and the last timestamp.

3.2.2 Moving Average

The algorithm described in the theory section was implemented in Python.

The bot was then simulated on BTC’s Binance data from 2017 to 2021. Sev-

eral combinations of hyperparameter were tested, namely all combinations

of the following:

• SA: [15, 30, 60, 120] minutes

• LA: [3, 6, 12] hours

• ∆: [50, 100, 500, 1000] USD

3.2.3 Random Intervals

The random model was designed as follows: to do that is to generate a

normal distribution of time intervals to select from. Then given an interval

a decision to buy or sell can be made after the interval has run out. For

example given a normal distribution with an expected value of 6 hours and

a standard deviation of 1 hour. A time interval of how long to hold and then

sell can then be drawn randomly. The same was done for buy signals.

3.2.4 Simulation

The simulation of each model was performed under similar circumstances.

Though the time periods and intervals differed, but the basic principle were

9the same. The assumptions made in order to pursue a feasible simulation

were the following:

• The trader can only own one BTC at a time. This means that the

wallet has to be empty in order to purchase a Bitcoin.

• Each transaction only deals with one unit, which leads to that each

transaction contains one BTC back and forth.

• Taxes and commission fees were neglected in order to simplify the sim-

ulations.

4 Results

4.1 LSTM

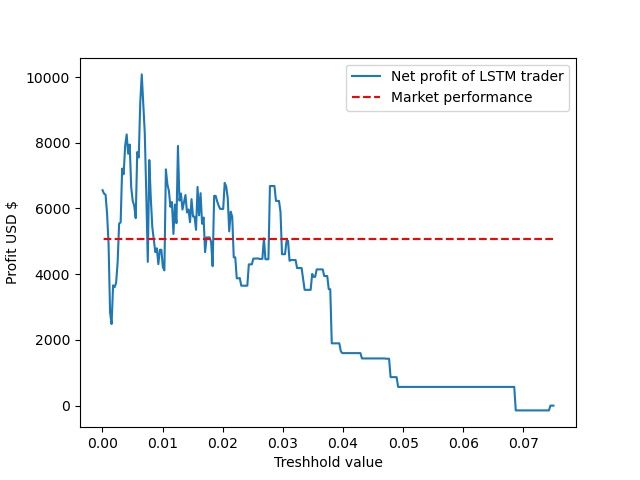

The LSTM model was tested for 300 different threshold values in the inter-

val 0.075-0.00001 using data from the period March-April 2021. The best

performer is thereafter presented in table 1 and the timestamps where the

transactions occured are shown in figure 3.

10Figure 3: The profit versus its corresponding threshold value for 300 simula-

tions. Hold is this case means the difference in price at the first and the last

point in the interval.

Table 1: The best result from the simulations with the LSTM model.

Threshold r Profit Number of trades Hold

0.00653 10079.68$ 156 5065.07$

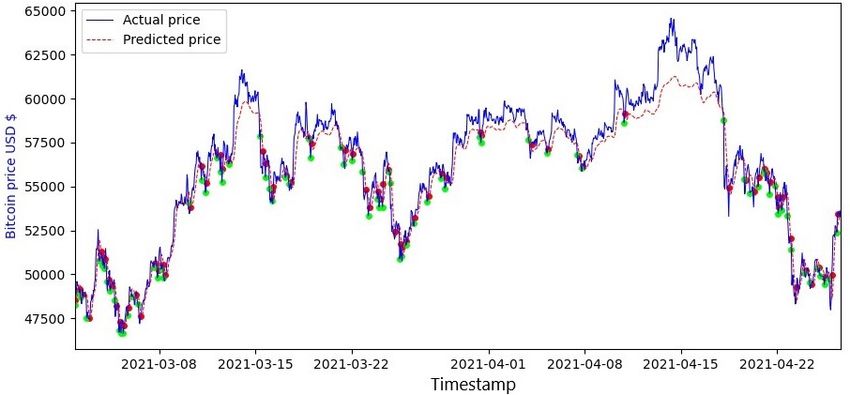

11Figure 4: The real and predicted price from the LSTM model and the best

performing threshold value. Green circle indicates a purchase, and red a sale.

In figure 4 all the trades of the LSTM model using the best threshold

value can be seen. The price of the BTC versus the price of the predicted

price from the LSTM model is also represented in the plot.

4.2 Moving Average

The moving average model ran on the entire data set for all combinations of

hyperparameters presented in the method section. That is, 4 × 3 × 4 = 48

configurations. The most interesting results are presented below. The blue

line in the graphs are the profits over time. The red line is the same for

every run, and represents the BTC price. The titles over the plots show

which hyperparameters that were used. B is ∆, LT is LA and ST is SA.

12(a) (b)

Figure 5: Results for two MA simulations

(a) (b)

Figure 6: Results for two MA simulations

(a) (b)

Figure 7: Results for two MA simulations

134.3 Random Intervals

The random interval bot performed differently every run due to its random

elements. Hence, the profitability varied between the runs. The performances

are presented in histograms, which can be seen below. The yellow dashed

lines are bell curves with the same mean and standard deviations as the

data in the respective histogram. The red lines indicate how the BTC price

changed during the corresponding time period. It shows how much you would

earn or lose by buying a BTC in the beginning of the time period and sell it

at the end of the time period. First, the model ran 1000 times on the entire

data set from 2017. The profitability histogram can be seen in figure 8.

Figure 8: The random interval bot’s profitability for 1 000 runs

The model also ran 5 000 times each on three shorter periods. Histograms

for these months can be seen in figures 9, 10 and 11.

14Figure 9: Profitability histogram for February 2018

Figure 10: Profitability histogram for April 2018

15Figure 11: Profitability histogram for November 2018

The average profitability for every time period as well as the BTC price

change can be seen in table 2

Table 2: Average profitability and BTC price changes

Time Period Average profit [USD] BTC price change [USD]

2017 - 2021 25 915 53 239

February 2018 112 46

April 2018 1 129 2319

November 2018 -1 172 -2 330

5 Discussion

5.1 LSTM

When reviewing the data from the LSTM-model a few conclusions can be

made. At figure 3 the graph shows the profits versus the market performance

for each threshold value. From this graph it appears that when the thresh-

old value is over 0.03 the profits made from the LSTM model are negative,

compared to the market performance. However, when the threshold value

is 0.03 and below, the LSTM model often outperforms the market. Thus

these results seems to imply that when lowering the threshold value, and

16therefore increasing the frequency of the trades, it also increases the chance

of higher profit. As seen in figure 4, the machine learning model predicts the

price relatively well, with a few exceptions, compared to the market. This

indicates that the model predicts the market behaviour relatively well and

has the potential to capitalize on these predictions.

There are a few things that could be tested in order to further improve the

model. One way would be to test using assymetrical values on the thresh-

olds. This would mean that it would require different values for buy and sell

decisions in equation 3. For a more advanced improvement the system could

adapitvely choose a threshold value based on the volatility of the market. For

example, if the market is in a steady state, it would make little sense to trade

in a high frequency. However, if the market is more volatile then it is pre-

sumably advantageous to trade in a higher frequency. Another improvement

would be to include social signals as input in the LSTM model. This could

be done in a number of different ways. One way would be to measure the

search count for different cryptocurrencies, and in that way draw conclusions

on the current popularity of the currency. These signals could offer another

type of data which interprets the market sentiment and could indicate an

upcoming rise or decline.

5.2 Moving average

When reviewing the simulations from the moving average model, a few graphs

were selected to display the key differences. When tweaking the hyperparam-

eters in the model, we see that it is resulting in different outcomes over the

same time period. When using a more narrow bandwidth ∆ the model is

more active, and benefits from the relatively small market fluctuations be-

tween 2018 and the end of 2020. However, this comes with the trade off, larger

market movements are often bypassed - The model sells too early. This can

be seen in figure 5a where the model outperforms the market at first, but

misses out on the large upswing at the end of 2020. At the other end of the

spectrum we have the models that use a broader bandwidth. These models

are unable to operate effectively when the market is more stable, but handle

larger market movements better. This can be seen in figure 7b and 6a. The

model with the most all-round parameters are displayed in figure 7a. This

set of hyperparameters was profitable at the beginning of the data set, but

also manages to hang on when the market rushed upwards in the end of 2020.

17An improvement to the model could be to use an adaptive bandwidth based

on the volatility of the market. This would enable the model to predict both

small and large market movements. This could be done by measuring the

standard deviation in the data, compared to the market volatility. This is a

method commonly used in technical analysis.

5.3 Random intervals

The results from the random interval model seems to imply that it’s most

likely to make a profit even though the the timestamps where to buy and

sell is chosen at random. This is because the overall direction of BTC was

upward between 2017 and 2021. Another observation from figure 8, is that

the market delta was 53239 USD, while the expected value of the wallet delta

was around 22000 USD. This is probably due to that the model was idle for

approximately half of the simulation time and invested for the other half.

Therefore it is most likely that the gain or loss from the model is half of the

market performance.

6 Conclusion

This project has analyzed and investigated the profitability of autonomous

trading in BTC. The conclusion that can be drawn from the various results

is that autonomous trading has potential to be profitable. Though, there

are still difficulties with adapting the models to a real market. Choosing the

appropriate parameters depending on the market behaviour is of the utmost

importance, but remains a challenging task. This task is yet to be fulfilled,

and remains a topic of further research.

18References

[1] James Chen. Amsterdam Stock Exchange (AEX) .AS Definition. 2019.

url: https://www.investopedia.com/terms/a/aex.asp.

[2] Satoshi Nakamoto. Bitcoin: A Peer-to-Peer Electronic Cash System.

2008. url: https://bitcoin.org/bitcoin.pdf.

[3] Ludvig Öberg. Interview with Ludvig Öberg, Co-founder of Safello and

an expert within cryptocurrencies. 2021-04-16.

[4] Christopher Olah. Understanding LSTM Networks. 2015. url: https:

//colah.github.io/posts/2015-08-Understanding-LSTMs.

[5] Jason Brownlee. The 5 Step Life-Cycle for Long Short-Term Memory

Models in Keras. 2017. url: https://machinelearningmastery.com/

5-step-life-cycle-long-short-term-memory-models-keras/.

[6] Binance. Kline/Candlestick Data. url: https : / / binance - docs .

github.io/apidocs/delivery/en/#kline-candlestick-data.

[7] Preprocessing data. url: https : / / scikit - learn . org / stable /

modules/preprocessing.html.

[8] Time series / date functionality. url: https://pandas.pydata.org/

pandas-docs/stable/user_guide/timeseries.html.

[9] Jason Brownlee. Gentle Introduction to the Adam Optimization Algo-

rithm for Deep Learning. 2021. url: https://machinelearningmastery.

com/adam-optimization-algorithm-for-deep-learning/.

[10] Murat Karakaya. LSTM: Understanding the Number of Parameters.

2020. url: https : / / medium . com / deep - learning - with - keras /

lstm-understanding-the-number-of-parameters-c4e087575756.

19You can also read