Global Investment Weekly 2019.04.01 - CTBC Private Banking

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Global Investment Weekly

2019.04.01

Market Calendar, 2019/4

W1(4/1-4/5) W2(4/8-4/12) W3(4/15-4/19) W4(4/22-4/26) W5(4/29-5/3)

Composite ECB Meeting(10) U. Of Michigan IFO Outlook(24) Euro Zone Q1

PMIs(1) Confidence(12) BOC Meeting(24) GDP(30)

DM BOJ Tankan(1) Germany ZEW(16) US Durables

RBA Meeting(2) Fed Beige Book(18) Orders(25)

US Nonfarm(5) US Retail Sales(18) BOJ Meeting(25)

US Q1 GDP(26)

Composite

EM China Social China Q1 GDP(17) CBR Meeting(26) China NBS PMI(30)

PMIs(1)

Financing(10~15)

Financials Results Growth Sector Results

Healthcare, Cons. Energy Results

S ector Staple Results Commodities

Results

Utilities, Telecom Iranian

Results Sanction

Waiver Expiry

S ur pr i se

E vent

M ar ket India Election Indonesia Election

Topic

Source: Compiled by CTBC Bank, 2019/3/29

1

Investment Strategy Summary

Inversion≠Recession, Investment Strategy Is Key

Brexit: May Sent Deal In Batches For Voting, Parliament Consensus

Past Hard To Reach

EU: Weak Mfg But Confidence And Leading Indicator Improved

Topics

FX: ECB/FED Both Dovish, DXY and EUR To Consolidate

AUD: Rate Cut Expectation Rose, Long-term Negative On AUD

Central

Russia: Inflation Stable, CBR To Hold For The Year

Banks Commodity: Real Demand To Recover Moderately, Positive On 2Q19

US Macro: Inversion Had Causes, Apr Data Gives The Key Direction

Key Topic US Equity: Moderate Monetary Policy Fuels Expansion, Room To Rally

In 2Q19

Yield

Financials: Index Went Against Fundamentals, Cautious On Shocks

Inversion

EM Bonds: Negative Yield And Yield Inversion Favor EM Bonds

Source: Compiled by CTBC Bank, 2019/3/29

2

Agenda

Part I Macro and Market Review

Part II Short-Term Focus and Strategy

3

Macro Review

Economic Data Release Review(3/22-3/28)

Macro Data: Overall Euro Zone Manufacturing PMI slid for the 8 consecutive months. New orders also hit the lowest

since end of 2012 while services PMI pulled it back slightly to above 50 in the expansion zone. IFO business climate

recovered from 98.7 in Feb to 99.6. The most exciting part was the expectation rebounded to 95.6, indicating corporate

outlook and sector certainty both improved. US Conference Board Consumer Confidence fell from 131.4 to 124.1 in Mar.

Current situation reached one year low while expectation weakened slightly to 99.8. It reflected that recent slowing

employment and high oil price squeezed disposable income, affecting consumer confidence. US 4Q18 GDP QOQ

reached 2.2% with household consumption sliding to 2.5% and government expenditure and corporate investment both

slowed slightly. Overall 2018 growth rate reached 2.9%, the highest in 3 years with Trump’s tax cut and corporate

investment incentives.

Release Date Country Economic Data Period Consensus Actual Prior

03/22/2019 16:30 GE Markit/BME Germany Manufacturing PMI Mar 48 44.7 47.6

03/22/2019 17:00 EC Markit Eurozone Manufacturing PMI Mar 49.5 47.6 49.3

03/22/2019 17:00 EC Markit Eurozone Composite PMI Mar 52 51.3 51.9

03/22/2019 18:30 RU Key Rate Mar 22 7.75% 7.75% 7.75%

03/25/2019 17:00 GE IFO Business Climate Mar 98.5 99.6 98.5

03/25/2019 20:30 US Chicago Fed Nat. Activity Index Feb -0.38 -0.29 -0.43

03/25/2019 22:30 US Dallas Fed Manf. Activity Mar 8.9 8.3 13.1

03/26/2019 22:00 US Richmond Fed Manfact. Index Mar 10 10 16

03/26/2019 22:00 US Conf. Board Consumer Confidence Mar 132.5 124.1 131.4

03/26/2019 16:30 GE Gfk Consumer Confidence Apr 10.8 10.4 10.7

03/28/2019 20:30 US GDP Annualized (QOQ) 4Q T 2.3% 2.2% 2.6%

Source: Bloomberg, Compiled by CTBC Bank, 2019/3/28

4

Market Review

Global Equities Pulled Back, Financials The Weakest

Country: Overall market has pulled back in the past week without signs of risk-off. The main reason for the fall was

because the YTD rally was too fast and too much. Before corporate earnings momentum turns upward, market stays on

hold. Furthermore, US treasury yield inversion topic resurfaced, providing another reason for profit taking.

Sector: Yield inversion caused pressure in outlook of the global 11 sectors. The most sensitive financials sector fell the

most in both the past week and past month, in response to the outlook concern. Tech sector volatility also intensified.

The relatively strong real estate sector in the past month also has the rally shrunken in the past week.

Global Equity Index Change Global Sector Index Change

Source: Bloomberg, past month is for 2018/2/28~2019/3/28, past week is for 2019/3/21~2019/3/28.

Sector indices based on Morgan Stanley Capital International (MSCI) global 11 sectors. 5

Market Review

Outlook Concern Depressed EM FI/FX, DXY And US Treasury Stronger

FI: Fed was cautious on outlook with its dovish policy stand depressing treasury yield curve so dollar denominated

IGBs performed relatively well. EM central banks stayed neutral to dovish but geopolitical and FX disturbance dragged

the performance of local currency bonds. The longer duration and better quality Asian local currency bonds still rallied.

FX: Turkey turmoil continued. EM currencies volatility increased, weakening together. South Africa nonfarm

employment data were stronger than consensus but it still waited for Moody’s to confirm its sovereign rating. RBNZ

turned dovish, depressing the commodity currencies. Capital flew to safe haven dollar and yen.

Global Bond Index Change Global FX Change (Against USD)

Source: Bloomberg, past month is for 2018/2/28~2019/3/28, past week is for 2019/3/21~2019/3/28

Note: Bonds take BAML Bond Index price change in the period. FX is against USD. 6

Brexit Progress

May Sent Deal In Batches For Voting, Parliament Consensus Hard To Reach

May Sent The Deal In Batches: On 3/28, May planned to sent

Path After Batch Votes

the deal to vote in 2 stages with parliament debating and voting

the withdrawal agreement on 3/29. Indicative votes on 3/27

showed no consensus so May announced to resign in exchange

for MPs supporting the deal. This could have some Conservative

MPs turned to support her deal but DUP still objected it. It was

hard to reach consensus in parliament, extension of deadlock

continues. We maintain our base case as circled in red.

May would resign if Brexit deal was passed to

empower some Leave Camp MPs in the next

Deal round of negotiation with EU. To avoid soft Brexit

Brexit or no Brexit after extension, they might choose

to support May’s deal. UK/EU equity could

rebound in this case.

May’s resignation was because she could not

unite the whole Conservatives with the Remain

Extend Camp refusing to allow the Leave Camp

Stay In dominating the negotiation. Alliance DUP’s

objection showed consensus was still hard to

EU

reach. Indicative votes did not yield any

consensus with a divided parliament, extension

of deadlock continues. Rebound of UK/EU

equities might retrace amid uncertainty.

No Deal Brexit extension did not rule out no deal Brexit. If

Brexit this surprise came true, UK/EU equity could

plunge though this is the least likely scenario.

Source: BBC, Compiled by CTBC Bank, 2019/3/29

7

Europe Macro

EU Data Mixed But Confidence And Leading Indicator Improved

EU Manufacturing Worst Hit: Eurozone Mfg PMI slid

for 8 consecutive months. Services pulled up slightly to Euro Zone Mar PMI Dragged By Germany/France

defend the above 50 expansion level. Germany Mfg fell

below 50 for the 2nd month, reflecting EU/China/US

trade conflicts. Others (excl. GE/FR) were stable.

Confidence Boosted Outlook: IFO confidence rose

from Feb 98.7 to 99.6 with the most exciting

expectation rebounding from prior low. It showed

corporate outlook and sector certainty both have

improved. Among that, service, trade and construction

also improved. Domestic demand indicators boosted

outlook.

ZEW Expectation Rose IFO Stopped Falling

Source: (Top Right)JPM, 2019/3/22, (Bottom Left)Bloomberg, 2007/1~2019/3, (Bottom Right)Bloomberg, 2007/1~2019/3

8European Currencies Strategy

ECB Meeting Expected To Be Dovish, EUR/USD To Consolidate At Low

Euro Zone Economic Data Still Weak: Fed slashed rate outlook, reducing dollar momentum. But Euro Zone economies

were still weak so EUR was hard to perform. Euro Zone Mar Mfg PMI released last week continued to slide. 47.6 was the

69-month low. As the most influential country of Euro Zone, Germany Mfg PMI was only 44.7. Luckily Germany IFO

confidence rebounded from 98.7 of prior month to 99.6, 1st rise in 7 months. Market still holds expectation on Euro Zone

monetary and fiscal stimulus could boost the economy.

FX Outlook: Global yield slid swiftly. US 10-yr treasury yield fell to the low of early 2018, making the short-/long-term yield

inverted and causing market concern over future outlook. Germany 10-yr treasury yield was again in the negative region.

With dovish ECB meeting expectation, short-term yield would be maintained at low. Historically, EUR was hard to perform

under such set-up. We expect it to maintain consolidation at the low so that DXY’s consolidation trend at the high would be

hard to change in the short-term.

EUR/USD To Consolidate At Low Germany Yield Turned Negative Again

EUR/USD Daily Chart US 10-yr Treasury Yield

Germany 10-yr Treasury Yield

200DMA

Source: Bloomberg, 2019/3/28

9Agenda

Part I Macro and Market Review

Part II Short-Term Focus and Strategy

10RBA

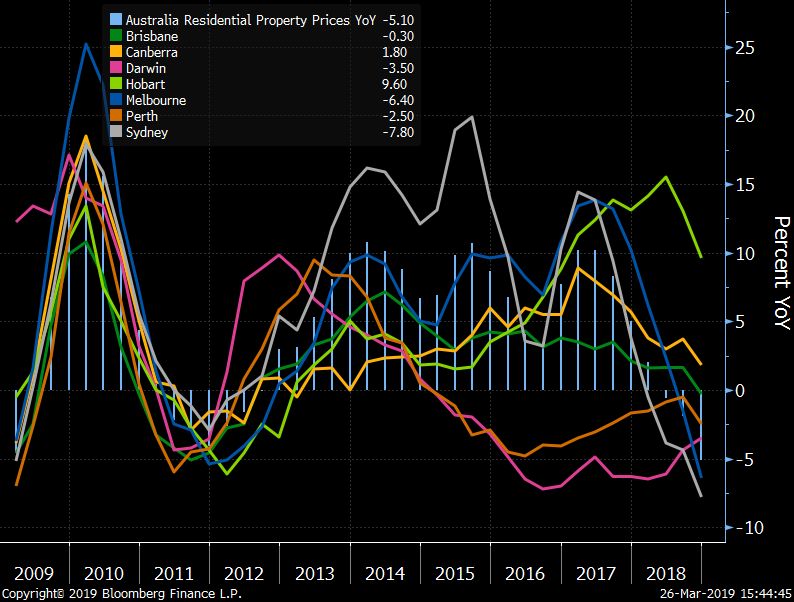

RBA Would Continue The Easing Signal

Australia Outlook Continued To Be Weak: Australia Q4 GDP rose 0.2% SA QOQ and 2.3% YOY, slowest since 2017 and

far below market and RBA forecast. Recent economic data were weak. Retail sales did not exhibit peak season momentum

in Dec while negative wealth effect from falling housing price emerged. We think RBA is likely to downgrade 2019 outlook.

Market Largely Expects RBA To Act On Q3: Australia largest trading partner – China is still having its outlook bottoming.

Australian domestic outlook faced negative wealth effect from falling housing prices so we are conservative on Australia

outlook. As inflation stayed low, though we expect RBA to hold this time, it could cut rate to 1.25% latest in Q3. Major

countries central banks all turned dovish, the probability of RBA bringing rate cut forward to Q2 is increasing. We would

keep a close eye on the housing market, consumption and employment changes.

RBA Continued To Downgrade Outlook Aussie Yield Curve Fell Amid Weakness

Source: (L)UBS, 2012~2020(F), (R)Bloomberg, 2019/1~2019/3

11AUD Strategy

RBA Turned Dovish, Maintain Long-term Negative On AUD

Australia Faced Both Internal/ External Risks: RBA has held its rate for 27 months. External trade tension

channeled to domestic uncertainty. Though global outlook is still within reasonable range, downside risk rises. Internally

low rate has supported the economy with gradually improving unemployment rate and inflation. But main uncertainties

came from household consumption and falling housing prices. RBA forecasted housing investment to be negative to

growth and its fall ‘might tail off sooner and faster than earlier projected’ with profound slowing risk in the next 1 to 2

years. Vice governor also noted that Sydney housing supply surge would affect the housing price and financial stability.

Maintain Negative On AUD: Market expects higher chance of RBA rate cut now. On the other hand, Australia

household debt ratio surged while housing prices fell, making RBA more likely to hold. Sino-US trade talk and Brexit

continue as risk factors so we maintain our negative view on AUD.

Australia Property Price Fell YOY Australia OIS Implied Rate Cut Chance Rose

Multi-tenor OIS

Source: Bloomberg, 2019/3/26

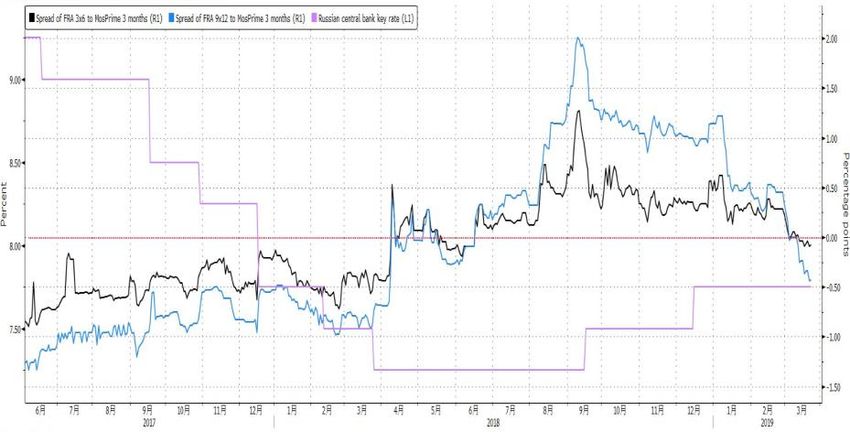

12Russia Monetary Policy

CBR Also Turned So We Downgraded Rate Target

CBR Downgraded Inflation Forecast: Mar meeting

CBR Policy Rate held rate unchanged and downgraded year end inflation

Upward Downward 2Q19 7.75% to 4.7%~5.2% from 5%~5.5%, stressing VAT impact

Deviation Realized Quant Voluntary has largely reflected in price while stronger RUB

lowered inflation threat.

Reason: Russia hiked VAT but the effect on inflation

was lower than forecasted so CBR turned from hawkish Two Hikes Enough To Depress Inflation Expectation,

to dovish. As future inflationary pressure was mild and CBR Has Room For Cuts: Governor stressed two

global major countries have turned their monetary hikes in 18 were enough. Weak domestic demand

policy dovish YTD. Though CBR might not cut rate now,

depressed inflation. Statement also brought the rate cut

rate hike was virtually impossible so we downgraded

2Q19 and 3Q19 benchmark rate target to 7.75%. from 2020 to 2019 but governor did not state exact

timing. FRA reflected the dovish tone immediately.

CBR Preventive Rate Hike Slowed Inflation FRA Fell Into Negative, Rate Cut More Likely

CBR Hiked Twice In

2018

CPI YOY

Source: (L)Bloomberg, 2019/3/22, (R)Bloomberg, 2019/3/22

13Commodity Strategy

2Q19 Commodity Demand To Grow Moderately

Iron Ore Undersupply, Copper Demand To Rebound In Mfg PMIs Weakened, US/CN New Order Higher

2Q19: Vale Brucutu iron ore restart progress was interfered by

the court sanction, delaying it to 2H19. Iron ore price would

consolidate at high in 2Q19 and fell in 2H19. US/CN mfg new

order rebound and China tax cut would boost copper in 2Q19.

Chemicals To Bottom Out In 2Q19: US Chemical Activity

Barometer monthly change bottomed out last Dec, indicating

chemical production to rebound after 2Q19 though slower YOY.

US chemicals would rebound despite its weak EU counterparts.

Slowing Demand Affect Commodity 1Q19 Results: Prices

front run Sino-US trade optimism. MSCI Commodity would

retrace due to weak 1Q19 results but still positive in 2Q19.

CAB Predicts Bottom Out In 2Q19, But Slow Growth Price Forecast: Oil Flat, Cu Up, Fe Down

Forecast

(Normalized)

Source: (Top Right, Bottom Right)Bloomberg, 2019/3/27, (Bottom Left)American Chemistry Council, 2019/3/26, Compiled by CTBC

Bank, 2019/3/27 14Macro Trend Analysis - America

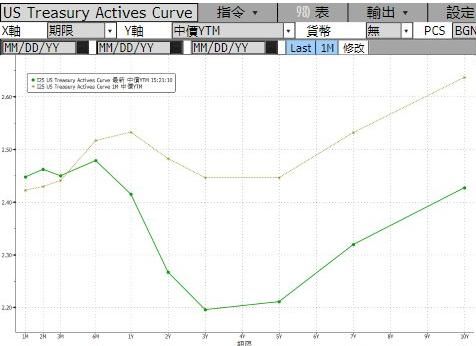

Fed Monitors 1st 3M-10Y Yield Inversion, Apr Data Provide Key Direction

Curve Analysis: Fed quarterly meeting downgrades of outlook and rate were higher than consensus with announcement

to stop QT soon. Officials expected to hold rate this year with only one hike in 2020. Interest rate future-implied rate cut

probability surged to 70%. NY Fed focused on the 1st 3M10Y yield inversion in current cycle. Historically, it occurred when

growth reversed after peaking as FI investors confidence faded. Current yield slide is different from that in 4Q18. 4Q18

slide was due to trade war and risk aversion from oil and equity prices plunge while 1Q19 one was due to government

shutdown and US storm affecting economic activities with delayed data while external dwarfing global trades deteriorated.

Conclusion: Fed held rate unchanged and global QE liquidity maintained short-term yield. In long-term yield, 1Q19

temporary factors (storms & shutdown) would be removed in 2Q19. Recent data have improved with stable initial jobless

claim, better housing and 2Q consumption boost from tax refund. We maintain 2Q19 US outlook recovery. Overbought of

long-term yield would reverse in 2Q19 with Apr nonfarm and global mfg as key signals. Inflation would bottom out in 4Q

after 3Q transportation base effect faded. 10-yr treasury yield 2Q19=2.7%, 3Q19=2.7%, 4Q19=2.9%.

Long Duration Treasury Yield Fell For A Month Fed Closely Monitor 3M-10Y Yield Inversion

US Treasury Yield Curve

2.6 2019/2/25 Vs. 2019/3/25

2.5 2/25

-20.9

-11.8

2.4

2.3 -25 -23.5 3/25

2.2

1M 3M 1Y 3Y 5Y 10Y

Source: (L)Bloomberg, 2019/2/25 and 2019/3/25, (R)Bloomberg, 1962-2019/3/25

15Investment Strategy – US Equity

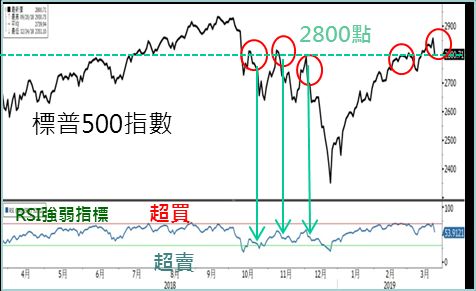

US Yield Inversion To Equity Plunge?

3M10Y Yield Inversion Impact Over Magnified In Equity:

Equity Reflected Fed Dove & Sino-US Optimism

US 3M10Y inversion continues, reflecting market concern

over global growth. In the past 50 years, outlook fell into Factors Market Reaction

recession average 16 months after 3M10Y yield inversion. In

Fed Turned Dovish Upward

terms of US equity return, results were mixed without reliable

references. However, the probability of positive return is high. Sino-US Trade Optimism Upward

US Equity Consolidated Around 2800, Upward Breach Corporate Earnings On Hold

Depends On Several Factors: We think a more moderate Confidence

Fed represents room for further US economic expansion. US Economy Bottom Out On Hold

Corporate earnings might bottom out in 1Q19. Investors long

position is currently low. Overall climate awaits 2Q19 rally. Liquidity Negative

Cumulative Return After 3M10Y Inversion In 50 Yrs S&P500 Consolidated Around 2800

%

Source: (Bottom Left)CS, 2019/3/25, (Bottom Right)Bloomberg, 2019/3/25, (Top Right)Compiled by CTBC Bank

16Investment Strategy- Financials

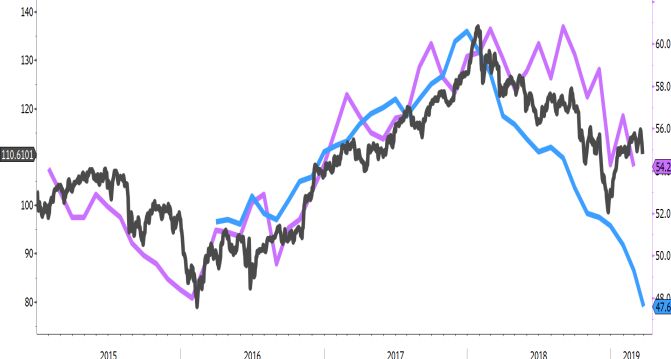

MSCI Financials Against Fundamentals, Cautious On Future Shocks

Financials Went Against Fundamentals, Cautious On

US Banking Cut Costs In Conservative Operation

Future Shocks: Recent yield inversion caused market

concern over pessimistic outlook. The highly sensitive Interest Income Growth(YOY%)

financial sector fell the most. We think MSCI Financials might Non-Interest Income Growth(YOY%)

Expenditure Growth(YOY%)

continue to retrace because its rally YTD was against

fundamentals. Till 4Q18, Financials have stable earning

growth in interest income but slowing growth in non-interest

income while banks continue to slash costs. Last time banks

slashed costs was during outlook downturn in 2015. With

current US/EU outlook in the downward trend in contrast to

the rally of financial sector equity. Analysts were not more

optimistic about 2Q19 earnings growth in MSCI Financials so

we believe probability of MSCI Financials to retrace is high.

Financials Went Against US/EU Outlook Trend Fund Managers Unwilling To Add Banking

US ISM Manufacturing

Euro Zone Manufacturing PMI

MSCI Financials

50 Threshold

Source: (Top Right, Bottom Left)Bloomberg, 2019/3/26, (Bottom Right)BofA, 2019/3/19, Compiled by CTBC Bank, 2019/3/27

17Investment Strategy – EM Bonds

Negative Yield And Yield Inversion, Investors Might Favor EM Bonds

EM Bonds Largely Rallied During Last Inversion: Fed paused monetary tightening would benefit EM assets while

global negative yield bond size rose to 2017/9 high, attracting more funds into EM bonds. In last(2006) yield inversion,

major EM bonds returned average 8% for the year, especially major currency sovereign bonds. But in terms of yield

spread, concern of outlook and growth rises in the late stage of Fed rate hike cycle, yield spread had little room for

narrowing. Returns were mainly from coupons.

Dollar Consolidated At High Increased FX Volatility Risk: Current setup is still different from 2006. Europe was

recovering at that time while global economy is slowing now with US momentum stronger than Europe. DXY might

still consolidate at thigh while EM currencies volatility would be enlarged. We prefer EM major currency sovereign

bonds with attractive yields.

All EM Bonds Rallied In Previous Yield Inversion Inversion As Double-edge Sword For EM Sovereign

Local IGB Corporate HYB Major Currency

Currency Bond Sovereign Bonds

Source: ICE Data Indices, Bloomberg, 2019/3/27, Compiled by CTBC Bank

18Target Price

Target Price – Rates/FI

第二層 第三層 2019/3/28 2019Q2 2019Q3

美國聯邦基準利率(上緣) 2.50 2.50 2.50

美 美國10Y 2.39 2.70 2.70

巴西利率 6.50 6.75 6.75

歐洲央行再融資利率 0.00 0.00 0.00

德國10Y -0.07 0.35 0.35

英國央行利率 0.75 0.75 0.75

歐 英國10Y 1.00 1.35 1.30

南非政策利率 6.75 6.75 6.75

南非2Y 6.99 7.20 7.35

俄羅斯政策利率 7.75 7.75 7.75

日本央行利率 -0.10 (0.10) (0.10)

日本10Y -0.09 (0.10) (0.12)

中國存準率 13.50 12.5 12.0

亞 中國2Y 2.68 2.50 2.45

台灣央行利率 1.38 1.38 1.38

澳洲目標利率 1.50 1.50 1.25

澳洲10Y 1.73 1.85 1.80

第二層 第三層 2019/3/28 2019Q2 2019Q3

全球投資級債 2.84 3.30 3.14

成熟市場投資級債指數 美國投資級債 3.64 3.99 3.99

歐洲投資級債 0.83 1.20 1.08

全球高收益債 6.03 6.92 6.86

成熟市場高收益債指數 美國高收益債 6.34 6.96 7.13

歐洲高收益債 3.47 4.46 4.14

新興主要貨幣主權債指數 新興主要貨幣主權債 5.77 6.30 6.05

新興主要貨幣企業債 5.74 6.50 6.28

新興主要貨幣企業債指數 新興投資級債 4.02 4.70 4.55

新興高收益債 7.11 8.00 7.70

新興當地貨幣債 6.32 6.65 6.50

新興當地貨幣債指數 人民幣債 3.60 4.05 4.20

亞洲當地貨幣債 4.77 5.30 5.20

Source: Compiled by CTBC Bank, 2019/3/29 : TP Adjustment

19Target Price

Target Price - Equity

第二層 第三層 2019/3/28 2019Q2 2019Q3

成熟市場股 2095.2 2150 2000

美國 2815.4 2900 2600

美

拉丁美洲 2686.4 2800 3000

巴西 94388.9 97000 103000

歐洲 3101.1 2960 3100

英國 3951.4 3800 3920

歐 德國 11428.2 11200 11900

新興歐洲 315.3 292 312

俄羅斯 1207.3 1100 1190

泛太平洋 158.6 160 165

澳洲 6256.5 6200 6500

日本 21033.8 23000 23000

新興市場股 1045.2 1020 1080

新興亞洲 532.4 520 560

中國A 2994.9 2800 3100

亞

中國H 11294.8 11000 12000

香港 28775.2 27500 30000

台灣 10536.3 10500 10650

韓國 2128.1 2300 2350

印度 38545.7 39550 39550

東協 790.5 820 820

科技 251.4 250 260

成長型產業 非核心消費 247.9 253 260

工業 248.2 255 259

金融 110.6 104 107

利率型產業

地產 222.9 205 210

能源 207.3 203 207

天然資源產業

原物料 250.2 248 245

公用事業 137.3 132 130

核心消費 231.7 230 230

防禦型產業

健護 245.0 238 260

電信 68.4 65 69

Source: Compiled by CTBC Bank, 2019/3/29

20Target Price

Target Price – FX/Commodity

第二層 第三層 2019/3/28 2019Q2 2019Q3

美元指數 97.202 96 94

美元兌日圓 110.63 112 110

成熟國家 歐元兌美元 1.1221 1.14 1.17

美元兌瑞郎 0.9956 0.99 0.96

英鎊兌美元 1.3044 1.34 1.32

澳幣兌美元 0.7074 0.69 0.69

商品貨幣 紐幣兌美元 0.6777 0.66 0.65

美元兌加幣 1.3438 1.34 1.35

美元兌台幣 30.856 30.8 30.6

美元兌星幣 1.3565 1.35 1.34

新興貨幣

美元兌人民幣 6.7391 6.85 6.75

美元兌南非幣 14.6077 13.8 13.5

布蘭特原油 67.16 66 70

鐵礦砂 84.75 78 80

黃金 1290.42 1330 1350

Source: Compiled by CTBC Bank, 2019/3/29

21GENERAL DISCLAIMERS:

1. This document and the investments and/or products referred to herein are for information only and do not have regard to your specific investment objectives, financial situation or particular needs.

2. This document and the investments and/or products referred to herein should not be construed as any recommendation for you to enter into the investment briefly described above and this document must

be read with CTBC’s General Terms and Conditions including without limitation Risks Disclosure Statements, Supplemental Terms and Conditions and such terms and conditions specified by CTBC from time to

time.

3. You are advised to exercise caution in relation to this document. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice from a licensed or

exempt financial adviser before making your commitment to invest in the investments and/or products referred to herein.

4. If you choose not to seek advice from a licensed or exempt financial adviser or such other independent professional, you should carefully consider whether investment in the investments and/or products

referred to herein is suitable and appropriate for you taking into consideration the risks and associated risks.

5. The final terms and conditions of the proposed investment in the investments and/or products referred to herein will have to be set out in full in the definitive trade confirmation between CTBC and you.

6. CTBC does not guarantee the accuracy or completeness of any information contained herein or otherwise provided by CTBC at any time. All of the information here may change at any time without notice.

7. CTBC is not responsible for any loss or damage suffered arising from this document.

8. CTBC may act as principal or agent in similar transactions or in transactions with respect to the instruments underlying the transaction.

9. Until such time you appoint CTBC, CTBC is not acting in the capacity of your financial adviser or fiduciary.

10. Investments involve risks. Past performance figures, predictions or projections are not necessarily indicative of future or likely performance. Actual performance may differ from the projections in this

document.

11. Any references to a company, financial product etc is used for illustrative purpose and does not represent our recommendation in any way.

12. Any scenario analysis is provided for illustrative purpose only and is no indication as to future performance and it does not reflect a complete analysis of all possible scenarios that may arise under an actual

transaction. All opinions and estimates given in the scenarios are illustrative and do not represent actual transactions.

13. The information in this document must not be reproduced or shared without our written agreement.

14. This document does not identify all the risks or material considerations that may be associated with you entering into of the transaction and the transaction period you wish to consider.

15. This document does not and is not intended to predict actual results and no assurances whatsoever are given with respect thereto. It does not present all possible outcomes or takes into consideration all

factors that may affect or influence the transaction.

16. This document is based on CTBC’s understanding that you have inter alia sufficient knowledge, experience and access to professional advice to make your own evaluation and choices of the merits and risks

of such investments and you are not relying on the CTBC nor any of our representatives or affiliates for information, advice or recommendations of any sort whatsoever.

17. You should have determined without relying on CTBC or any of our representatives or affiliates for information, advice or recommendations of any sort whatsoever, the economic risks and merits as well as

the legal tax and accounting aspects and consequences of the transaction and that you are able to fully assume such risks.

18. CTBC accepts no responsibility or liability whatsoever for any loss of whatsoever nature suffered by you arising from the use of this document or reliance on the information contained herein.

19. CTBC may have alliances with product providers for which CTBC may receive a fee and product providers may also receive fees from your investments.

20. The following exemptions under the Financial Advisers Regulations apply to the CTBC and its representatives:

(1) Regulation 33(1) – Exemption from complying with section 25 of the Financial Advisers Act (“FAA”) when making a recommendation in respect of (a) any designated investment product (within

the meaning of section 25(6) of the FAA) to an accredited investor; (b) any designated investment product (within the meaning of section 25(6) of the FAA) that is a capital market product, to an

expert investor;

(2) Regulation 34(1) – Exemption from complying with section 27 of the FAA when making a recommendation in respect of (a) any investment product to an accredited investor; (b) any capital

markets product to an expert investor or (c) any Government securities;

(3) Regulations 36(1) and (2) – Exemption from complying with sections 25, 26, 27, 28, 29, 32, 34 and 36 of the FAA when providing any financial advisory service to any person outside of Singapore

who is (a) an individual and (i) not a citizen of Singapore; (ii) not a permanent resident of Singapore; and (iii) not wholly or partly dependant on a citizen or permanent resident of Singapore; or (b)

in any other case , a person with no commercial or physical presence in Singapore.

22You can also read