INDUSTRY OVERVIEW - HKEX :: HKEXnews

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

THIS DOCUMENT IS IN DRAFT FORM. The information contained in it is incomplete and is subject

to change. This Document must be read in conjunction with the section headed ‘‘Warning’’ on the

cover of this Document.

INDUSTRY OVERVIEW

The information that appears in this section has been prepared by Euromonitor and

reflects estimates of market conditions based on publicly available sources and trade opinion

surveys, and is prepared primarily as a market research tool. References to Euromonitor should

not be considered as the opinion of Euromonitor as to the value of any security or the

advisability of investing in the Company. Our Directors believe that the sources of information

contained in this section are appropriate sources for such information and have taken

reasonable care in reproducing such information and we have no reason to believe that such

information is false or misleading or that any material fact has been omitted that would render

such information false or misleading. The information prepared by Euromonitor and set out in

this section has not been independently verified by our Group, the Sole Sponsor, the

[REDACTED], the [REDACTED] or any other party involved in the [REDACTED] and

neither they nor Euromonitor give any representations as to its accuracy and the information

should not be relied upon in making, or refraining from making, any investment decision.

SOURCES OF INFORMATION

We commissioned a report from Euromonitor to conduct an analysis of, and to report on, the

construction industry in Singapore. A total fee of US$110,500 was paid to Euromonitor for the

preparation of the Euromonitor Report. Established in 1972, Euromonitor is the world leader in

strategy research for both consumer and industrial markets. The Euromonitor Report has been

compiled after thorough and diligent research conducted by Euromonitor’s Singapore office. The

market research process was undertaken through a top-down central research and bottom up

intelligence to present a comprehensive and accurate picture of the construction industry in

Singapore. Euromonitor’s detailed primary research involved: (i). secondary research which

involved the review of published sources from government and regulatory statistics and

independent research reports; (ii). primary research which involved interviews with a sample of

leading industry participants and industry experts for latest data and insights on future trends and

to verify and cross check the consistency of data and research estimates; (iii). projected data were

obtained from historical data analysis plotted against macroeconomic data with reference to

specific industry-related drivers; and (iv). review and cross-checks of all sources and independent

analysis to build all final estimates including the size, shape, drivers and future trends of the

Singapore market and prepare the final report.

With both primary and secondary research in place, Euromonitor has utilised both types of

sources to validate all data and information collected, with no reliance on any single source.

Furthermore, a test of each respondent’s information and views against those of others is applied

to ensure reliability and eliminate bias from these sources.

– 76 –

THIS DOCUMENT IS IN DRAFT FORM. The information contained in it is incomplete and is subject

to change. This Document must be read in conjunction with the section headed ‘‘Warning’’ on the

cover of this Document.

INDUSTRY OVERVIEW

FORECASTING BASES AND ASSUMPTIONS

Euromonitor prepared the Euromonitor Report based on the following assumptions: (i). the

Singapore economy is expected to maintain steady growth over the forecast period (2020-2024);

(ii). the Singapore social, economic, and political environment is expected to remain stable in the

forecast period; (iii). there will be no external shock (aside from COVID-19), such as financial

crisis or raw material shortage that affects the demand and supply of construction works in

Singapore during the forecast period; (iv). key market drivers such as the government’s continued

regard towards public infrastructure development, policies in relation to housing, workplace skill

development and measures to increase construction productivity growth are expected to boost the

development of the Singapore construction market; and (v). key drivers including Singapore’s

rising GDP growth and the adoption of more advanced construction technology by contractors are

likely to drive the future growth of the Singapore’s construction market.

The research results may be affected by the accuracy of these assumptions and the choice of

these parameters. The market research was completed in August 2020 and all statistics in the

Euromonitor Report are based on information available at the time of reporting. Euromonitor’s

forecast data comes from analysis of historic development of the market, the economic

environment and underlying market drivers, and is cross-checked against established industry

data and trade interviews with industry experts.

1. MACRO-ECONOMIC ENVIRONMENT IN SINGAPORE

Singapore enters a phase of slower growth due to restructuring of the economy

Singapore’s economy registered a CAGR of 5.0% for nominal GDP over the review

period (2014-2019). Since 2011, the Singapore economy has entered a phase of slower

growth as the economy transitioning from manpower-driven growth to productivity-driven

growth. Real GDP growth slowed in 2015 and 2016, due to the weaker global economy and

a protracted slump in oil prices, which affected the domestic oil and gas industry. However,

the economy showed an improvement in 2017 with real GDP growth reaching 3.9%, riding

on the recovery in the global economy and the increase in trade activities. During 2014-

2019, GDP (as contributed by the construction industry) declined at a CAGR of 1.6% to

account for 3.5% of the total nominal GDP in 2019. The drawn-out trade war between the

US and China has had a negative impact on Singapore’s export-oriented economy since

2019. Real GDP expanded by 0.7% in 2019, which is the country’s slowest growth since

2009.

– 77 –

THIS DOCUMENT IS IN DRAFT FORM. The information contained in it is incomplete and is subject

to change. This Document must be read in conjunction with the section headed ‘‘Warning’’ on the

cover of this Document.

INDUSTRY OVERVIEW

Table 1 Macro-economic environment in Singapore (historical)

2014 2015 2016 2017 2018 2019

GDP (Nominal) S$ billion 396.9 421.0 437.3 464.9 503.4 507.6

GDP (as contributed by

the construction industry) S$ billion 19.3 20.5 19.8 17.0 17.0 17.8

Source: National statistics published by the Department of Statistics of the Government of Singapore and

the Ministry of Trade and Industry of the Government of Singapore

2. OVERVIEW OF THE CONSTRUCTION INDUSTRY IN SINGAPORE

Classification of construction activities in Singapore

Construction activities in Singapore can be divided into general building works and

civil engineering works. General building works include general construction and major

repair works, as well as other construction works to facilitate or support the construction of

all types of buildings. Civil engineering works typically relate to infrastructure projects,

including construction of the MRT network, airports, roads and bridges. Construction

activities can also be classified as public sector or private sector construction projects.

Public sector projects are construction activities undertaken by the government or public-

sector agencies, while private sector projects are construction works commissioned by

private entities.

High level of subcontracting activities behind tenders awarded to main contractors

Subcontracting is a prevalent practice in the construction industry, whereby main

contractors or developers would bid for projects, and then subcontract different parts of the

construction project to several specialised subcontractors. For large projects, multi-layered

subcontracting is common, with subcontractors further contracting out work to smaller

contractors. There are many subcontractors in the industry, which specialise in different

parts of the construction value chain. As a result, the values of tenders won by main

contractors do not give a complete picture of the work subsequently awarded to

subcontractors.

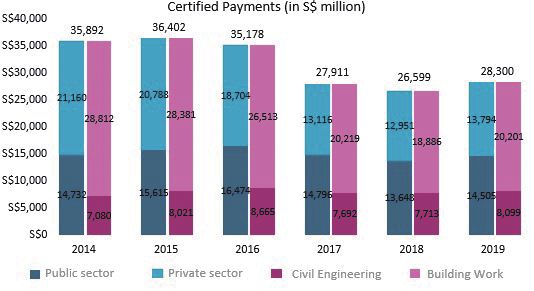

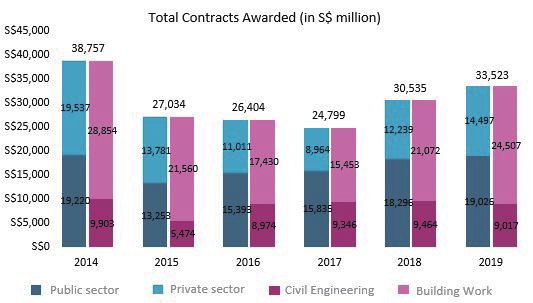

Public sector outperforms private sector in the review period

Demand for public sector construction works rose, mainly from industrial building

works and civil engineering works, and provided support for the overall industry growth.

Therefore, growth in the construction industry was largely driven by public sector projects

over the review period. Total contracts awarded to public sector construction projects

accounted for 56.8% of all construction contracts in 2019, up from 49.6% in 2014.

– 78 –THIS DOCUMENT IS IN DRAFT FORM. The information contained in it is incomplete and is subject

to change. This Document must be read in conjunction with the section headed ‘‘Warning’’ on the

cover of this Document.

INDUSTRY OVERVIEW

Table 2 Performance of construction industry in Singapore, historical

Source: The BCA as of 8 January 2020

– 79 –THIS DOCUMENT IS IN DRAFT FORM. The information contained in it is incomplete and is subject

to change. This Document must be read in conjunction with the section headed ‘‘Warning’’ on the

cover of this Document.

INDUSTRY OVERVIEW

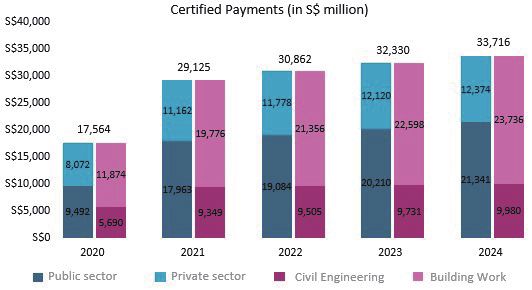

Healthy construction project pipeline for both private and public sector demand in the

future despite COVID-19

The construction industry is expected to resume robust growth from 2021 onwards,

supported by the recovery of domestic demand and a strong pipeline of projects in the

forecast period. According to the Euromonitor Report, construction demand is forecasted to

hold steady in 2020, with an estimated value that falls between S$28 billion and S$33

billion, compared to S$33.4 billion in 2019. Demand is expected to strengthen beyond 2020,

and could increase to between S$27 billion and S$34 billion per year during 2021-2022, and

between S$28 billion and S$35 billion per year during 2023-2024. However, due to COVID-

19, total contracts awarded and certified payments are expected to be delayed in 2020.

Public sector construction demand over the medium-term will be supported by public

residential projects, the redevelopment of older buildings in strategic areas, such as the

Central Business District, and major infrastructure projects, which include developments at

Jurong Lake District and Changi Airport Terminal 5, and MRT projects such as the

Thomson-East Coast Line, Cross Island Line and Jurong Regional Line. Between 2020 to

2024, certified payments for public sector is expected to register a CAGR of 22.5%,

growing from S$9.5 billion in 2020 to S$21.3 billion in 2024.

The private construction sector is also expected to gradually increase in the medium-

term despite the industry contraction in 2020, boosted by further growth in the other

economic sectors. Projects that are expected to contribute to construction demand from 2020

onwards include redevelopment of en-bloc sale sites, recreational developments at Mandai

Park, Changi Airport new taxiway and berth facilities at Jurong Port, the expansion of the

two Integrated Resorts at Marina Bay Sands, Resort World Sentosa and Tanjong Pagar

Terminal. Between 2021 and 2024, private sector construction demand is expected to

recover from the plunge in 2020, in line with the recovery of the general economy. Between

2020 to 2024, certified payments for private sector is expected to register a CAGR of

11.3%, growing from S$8.1 billion in 2020 to S$12.3 billion in 2024.

– 80 –THIS DOCUMENT IS IN DRAFT FORM. The information contained in it is incomplete and is subject

to change. This Document must be read in conjunction with the section headed ‘‘Warning’’ on the

cover of this Document.

INDUSTRY OVERVIEW

Table 3 Performance of construction industry in Singapore, forecast

Source: Forecast estimated based on the construction demand forecast range released by the BCA in January

2020

2.1 Overview of civil engineering industry

Civil engineering industry benefits from Singapore’s infrastructure development

In transport infrastructure, Singapore is well known for its airport, ports, road

and MRT network. Singapore was ranked first globally by the World Economic

Forum’s Global Competitiveness Index for 2019 for the robustness of its transport

infrastructure. The civil engineering industry of Singapore’s construction industry is

instrumental in delivering Singapore’s infrastructure, and has enjoyed strong growth in

the last few decades thanks to an infrastructure development boom. Civil engineering

certified payments registered a CAGR of 2.7% from 2014 to 2019, supported by a

strong pipeline of transport infrastructure projects, including various Thomson-East

Coast MRT Line contracts.

– 81 –THIS DOCUMENT IS IN DRAFT FORM. The information contained in it is incomplete and is subject

to change. This Document must be read in conjunction with the section headed ‘‘Warning’’ on the

cover of this Document.

INDUSTRY OVERVIEW

Civil engineering contracts registered large swings

The value of civil engineering construction contracts awarded experienced large

swings in the review period, as the timing of infrastructure projects tend to fluctuate.

By July 2014, the LTA had awarded 25 major civil engineering contracts for the

Thomson-East Coast MRT Line at a total contract sum of approximately S$9.9 billion.

However, civil engineering contracts awarded in 2015 fell by 44.7% year-on-year to

S$5.5 billion, due to the rescheduling of major public infrastructure projects from the

fourth quarter of 2015 to early 2016. Consequently, civil engineering contracts

awarded surged by 64.0% in 2016, with the award of more major infrastructure

contracts for the Thomson-East Coast MRT Line and the construction of LTA’s 4-in-1

rail and bus depot, known as the East Coast Integrated Depot. Civil engineering

certified payments growth is expected to pick up pace in the forecast period; however,

it is expected to register a sharp decline in 2020 due to disruptions related to COVID-

19. When activities return to normal, it is anticipated that the government will step up

investments in major infrastructure projects to drive Singapore’s economic recovery.

Public sector infrastructure projects are typically carried out over a period of four to

eight years, and they are expected to create sustained demand for civil engineering

works. According to the estimation of Euromonitor, the civil engineering certified

payments is expected to grow by a CAGR of 15.1% from S$5.7 billion in 2020 to

S$10.0 billion in 2024.

2.2 Overview of general building works industry

General building works’ contribution to construction industry declines

General building works forms an important part of the construction industry in

Singapore and contributed to 73.1% of total contracts awarded for the construction

industry in 2019. However, the value share of general building works in the

construction industry, has witnessed a decline in the review period falling from 79.8%

in 2015 to 73.1% in 2019. Between 2014 and 2019, the value of general building

works contracts declined at a CAGR of 3.2% due to the slowdown in the Singapore

economy and the rollout of major infrastructure projects which has boosted the

importance of civil engineering. According to the estimation of Euromonitor, the

certified payments of general building works is expected to grow at a CAGR of 18.9%

from S$11.9 billion in 2020 to S$23.7 billion in 2024. The outlook for the general

building works beyond 2020 is positive, considering a steady pipeline of new public

housing construction, upgrading works for HDB flats, and several upcoming sizeable

condominium projects. Moreover, major commercial office building projects, industrial

projects such as the Integrated Waste Management Facility, and institutional projects

such as healthcare facilities and educational facilities for Institutes of Higher Learning

(IHL) are expected.

– 82 –THIS DOCUMENT IS IN DRAFT FORM. The information contained in it is incomplete and is subject

to change. This Document must be read in conjunction with the section headed ‘‘Warning’’ on the

cover of this Document.

INDUSTRY OVERVIEW

3 DRIVERS AND CONSTRAINTS IN THE CONSTRUCTION INDUSTRY IN

SINGAPORE

Development of transport infrastructure such as MRT drives civil engineering demand

The civil engineering sector has been driven by the Singapore’s government

commitment to developing the public transport system. Major projects awarded in the

review period include the construction of Thomson-East Coast MRT Line, Changi Airport’s

3-runway system (package 2), and improvement works to the Kranji Expressway and Pan-

Island Expressway. Under the government’s plans to extend the coverage of the MRT

network, construction of the Thomson-East Coast Line, Circle Line 6 and North East Line

extension was started in the review period. In addition, the government has begun planning

for two more new rail lines – the Cross-Island Line and the Jurong Region Line.

Notable public sector projects provide support for general building works

One key growth driver for the general building industry is the number of notable

projects in both public and private sectors. Demand for general building works is closely

related to the national economic development. Demand comes from multiple economic

sectors including real estate, healthcare facilities, industrial facilities, commercial space and

office space. Notable projects in the review period include public housing construction and

HDB upgrading works, healthcare facilities and industrial projects such as the National

Cancer Centre at Outram and the fourth Desalination Plant at Marina East.

Productivity enhancement measures help companies become more productive and take

on more complex projects

Under the Construction Industry Transformation Map launched in October 2017, the

BCA aims to more than double the number of personnel trained in technologies and

innovation. It also plans to make jobs in the sector more highly skilled and attractive to

Singaporeans. Through this framework, the BCA targets to train 35,000 skilled workers in

design for manufacturing and assembly (DFMA), 20,000 personnel in integrated digital

delivery (IDD), and 25,000 in green buildings by 2025.

The BCA also encourages the construction industry to adopt automation and

technology. Under a research and development roadmap released in October 2016, BCA

identified 35 technologies, including robotics, DFMA and 3D printing, to help contractors

change the way they construct buildings and sustain productivity improvements in the long

run.

– 83 –THIS DOCUMENT IS IN DRAFT FORM. The information contained in it is incomplete and is subject

to change. This Document must be read in conjunction with the section headed ‘‘Warning’’ on the

cover of this Document.

INDUSTRY OVERVIEW

Competition for projects push down tender prices

Most projects in the civil engineering sector are public sector works. Players bid for

projects via government tenders, and cost competitiveness is one of the key evaluation

criteria. As a result, players compete to put in the lowest bids possible, which have

contributed to the falling profit margin in the industry. The challenge becomes exacerbated

for smaller players by rising labour prices, making projects even less profitable.

The BCA Building Works Tender Price Index (TPI) provides an indication of

historical movement of tender prices in the construction industry. The TPI reflects changes

in material costs, labour costs and the competition in the market, the risk and profit as these

are factored into contractors’ bids. Since 2015, the TPI has been on a downward trend. This

can be attributed to pressure on bid price for contracts due to growing competition among

construction companies, a slowdown in available building works contracts and a reduction

in private sector building demand.

Table 4 Changes in the BCA’s Tender Price Index (TPI)

Base Year = 2010 2014 2015 2016 2017 2018 2019

BCA’s Tender Price Index 106.8 104.8 98.0 96.7 98.6 99.9

Source: The BCA

Rising costs and longer payment period presents cashflow problems for smaller players

Singapore imports almost all its construction materials, consisting predominantly of

ready mixed concrete, steel bars, granite, concreting sand and cement. As a result, industry

players are susceptible to the fluctuations in the price of raw materials, caused by external

factors that determine pricing and supply of the raw materials. With high operating costs

and a highly competitive landscape, construction companies have been faced with the

challenge of falling profit margins. The impact is felt more by smaller players, as they tend

to take up smaller jobs, and hence lack the economy of scale to absorb rising costs.

The problem of tight cash flow for smaller contractors has deteriorated in 2017 due to

payment period getting longer. Singapore Commercial Credit Bureau reported that in 2017

construction is the only sector that registered a year-on-year rise in the number of slow

payments. A major reason for the increase in late payments is due to over supply in

contractors and a lower number of jobs, resulting to lower tender prices in 2017. When a

main contractor accepts low price projects, they tend to prolong their payments to their

subcontractors.

– 84 –THIS DOCUMENT IS IN DRAFT FORM. The information contained in it is incomplete and is subject

to change. This Document must be read in conjunction with the section headed ‘‘Warning’’ on the

cover of this Document.

INDUSTRY OVERVIEW

However, payment behaviours appear to have improved in recent years, along with

improved prospects in the construction industry. According to the Euromonitor Report, the

construction industry saw significant improvements in debt settlement in the second quarter

of 2019 (Q2 2019) compared with the last quarter of 2018 (Q4 2018), due to a healthy

pipeline of activities within the construction industry. Only 16% of construction companies

were more than 90 days delinquent in their debt payments in Q2 2019, versus 35% in Q4

2018. The settlement timeline for construction also decreased to 39 days in Q2 2019, down

20 days from 59 days in Q4 2018.

Despite the rebound in debt settlements, the Singapore Council Credit Bureau has

raised concerns over the slower payment of bills among Singapore companies, which

included the construction industry, largely due to the US-China Trade War tensions. In the

fourth quarter of 2019, these industries and sectors all saw an increase of slower payments

with construction sector increased by 2.5%, from 46.9% in third quarter of 2019 to 49.4% of

construction companies paying less than 50% of the total bills within the agreed terms.

COVID-19 increases operational challenges for companies

Since the circuit breaker measures were lifted on 2 June 2020, construction companies

have adapted their operations to comply with the BCA’s COVID-safe restart requirements.

Examples include contact tracing at work sites, testing of workers for COVID-19 before

heading back to site, installation of artificial intelligence on the lorries, which will trigger an

alarm if workers come too close to one another, staggering the working hours for

employees, segregating workers into different zones at work sites, and ensuring workers

comply with measures such as wearing face masks on work sites. These measures are likely

to incur higher operations costs for contractors, but the costs are alleviated by the funding

support offered through government’s Construction Support Package.

3.1 Value chain & costs

Raw material costs fluctuate with the global economy

The main costs of operating a construction company in Singapore include the

costs of raw materials, machinery and equipment rental, logistics, manpower and safety

costs. While the main cost categories are applicable to both general building works

contractors and civil engineering contractors, the detailed costs may differ among the

two depending on the complexity and requirements of the projects.

As Singapore market depends heavily on imports of these materials, the price

movements of construction materials are driven by global demand and supply which

contractors in Singapore have little influence on. When there is a high level of

construction activities, demand for construction materials would rise and push up

prices.

– 85 –THIS DOCUMENT IS IN DRAFT FORM. The information contained in it is incomplete and is subject

to change. This Document must be read in conjunction with the section headed ‘‘Warning’’ on the

cover of this Document.

INDUSTRY OVERVIEW

Table 5 Changes in Market Prices of Major Construction Materials in Singapore

Unit 2014 2015 2016 2017 2018 2019 CAGR

Cement in bulk S$/Tonne 97.9 93.0 83.0 75.9 78.8 84.6 –2.9%

(Ordinary Portland

Cement)

Steel Bars (16-32 mm S$/Tonne 653.9 501.4 500.5 688.8 751.0 713.9 1.8%

High Tensile)

Granite (20 mm S$/Tonne 22.5 19.7 15.4 16.1 17.4 19.2 –3.1%

Aggregate)

Concreting Sand S$/Tonne 23.3 22.7 18,3 17.1 21.1 28.4 4.0%

Ready Mixed S$/Cubic Metre 111.2 99.5 85.0 81.4 87.1 95.9 –2.9%

Concrete

Source: The BCA

Construction labour costs continues to climb due to tight labour market

Singapore’s construction industry relies on a large foreign workforce. According

to the MOM, Singapore had about 293,300 Work Permit holders in the construction

industry as of December 2019. The construction labour market has tightened in recent

years, as part of the government’s efforts to reshape the sector’s workforce to push for

greater productivity. However, a recent speech by Deputy Prime Minister Heng Swee

Keat in May 2020 suggested that the government recognises that there is a limit to

how far Singapore can go in reducing the need for manual work. It is likely that the

number of foreign construction workers will rise in the forecast period as the

government rolls out large-scale infrastructure projects to boost the economy.

Table 6 Total wage (excluding employer CPF) changes for the construction

industry in Singapore (YOY%)

In % 2014 2015 2016 2017 2018 2019

Total wage (excluding employer CPF)

changes for the construction

industry in Singapore 3.8 3.1 2.1 2.0 2.8 2.6

Source: Survey on Annual Wage Changes, Manpower Research and Statistics Department, MOM

– 86 –THIS DOCUMENT IS IN DRAFT FORM. The information contained in it is incomplete and is subject

to change. This Document must be read in conjunction with the section headed ‘‘Warning’’ on the

cover of this Document.

INDUSTRY OVERVIEW

Cost of leasing or buying construction machinery (one of the major operating

costs of the contractors)

Due to the specialised nature of construction works, special machinery is

sometimes required. The costs of leasing or buying construction machinery is one of

the major costs for construction companies. Contractors commonly lease construction

machinery, as and when required by their projects, as the costs of buying machinery

and maintaining them is typically more expensive than the costs of leasing. Moreover,

smaller contractors are also constrained by the lack of storage space for bulky

machinery. According to the Euromonitor Report, both purchase costs and rental/lease

costs of construction machinery have been on the rise over the years due to inflation

and the increasing complexity of building design requiring more advanced machinery

and equipment. Other contributing factors include projects with tight timelines and

limited construction machinery providers. Due to the costs of storage space, the

number of machinery providers remains relatively stagnant. Coupled with increasing

demand for the machinery, machinery costs are expected to continue rising, creating an

opportunity alternate revenue streams for machinery owners.

Higher construction costs due to COVID-19

During the COVID-19 period, the construction industry has experienced a

shortage of materials and manpower. Import of construction materials from main

supply countries like Malaysia and China was disrupted by movement control and

lockdown measures. Construction companies may have to source raw materials from

suppliers who may charge higher prices due to COVID-19 interruptions. In terms of

manpower costs, the number of foreign workers available for work has reduced as

travel restrictions prevented foreign workers from coming back to Singapore. In

addition, the measures to prevent the spread of COVID-19 transmission in the

construction industry are expected to increase operational costs for contractors.

– 87 –THIS DOCUMENT IS IN DRAFT FORM. The information contained in it is incomplete and is subject

to change. This Document must be read in conjunction with the section headed ‘‘Warning’’ on the

cover of this Document.

INDUSTRY OVERVIEW

3.2 Competitive landscape

Fragmented construction industry saw healthy growth in number of company

formations until 2014

The formation of business entities in construction industry fell steadily every

year between 2014 and 2018, and the number appears to have stabilised in 2019. The

more challenging operating environment since 2015 due to the property market

downturn and delay of MRT projects led to less work being available and as a result it

is less attractive for potential new entrants to enter the industry. At the same time,

there has been an increase in the cessation of business entities in construction industry

in 2015 and 2016. As compared to 2,429 business entities in 2014, only 2,347

business entities ceased operations in the industry in 2019. This corresponds with

improving outlook for the industry and the economy. As of August 2020, 958

companies were registered under the ‘‘Civil Engineering’’ category of BCA’s

Contractor Registration system with less than 10% of which graded A2 or above.

Lack of track record and shortage of local talent are key barriers to entry

In general, there are few hurdles for new players to enter the civil engineering

industry as a subcontractor, as there are no significant capital investment requirements

for subcontractors just starting out. Due to the diverse nature of works in the

construction industry and the widespread practice of subcontracting, subcontractors can

get work from main contractors, even if the subcontractors themselves do not satisfy

the registration criteria for BCA Contractor Registration System. In practice, new

entrants may face barriers in terms of a lack of track record and difficulty in securing

contracts, as the construction industry still relies to a large extent on reputation and

reliability.

– 88 –THIS DOCUMENT IS IN DRAFT FORM. The information contained in it is incomplete and is subject

to change. This Document must be read in conjunction with the section headed ‘‘Warning’’ on the

cover of this Document.

INDUSTRY OVERVIEW

Ranking of leading main contractors for civil engineering works in Singapore

Table 7 Ranking of leading main contractors for civil engineering works in

Singapore based on revenue receipts, 2019

Revenue

Receipts in Market

Rank Company 2019 Share Listed or private Nature of business/enterprise

(S$ million) (%)

1 Company A 177.4 2.2% Private General Building, Civil Engineering, Air-

Conditioning, Refrigeration & Ventilation

Works, Building Automation, Industrial &

Process Control Systems, Communication &

Security Systems, Electrical Engineering,

2 Company B 177.0 2.2% Listed in Korea General Building, Civil Engineering, Curtain

Stock Exchange Walls, Air-Conditioning, Refrigeration &

Ventilation Works, Building Automation,

Industrial & Process Control Systems,

Electrical Engineering, Fire Prevention &

Protection Systems, Mechanical Engineering,

Integrated Building Services

3 Company C 157.6 1.9% Private Civil Engineering, Electrical Engineering

4 Company D 150.2 1.9% Listed in Tokyo General Building, Civil Engineering, Piling

Stock Exchange Works

5 Company E 142.9 1.8% Private Building Automation, Industrial and Process

Control Systems, Solar PV System

Integration, Electrical Engineering,

Mechanical Engineering, Electrical

Equipment, Mechanical Equipment, Plant &

Machinery

Others 7,294.0 90.0%

8,099.2 100%

Source: Euromonitor estimates based on information published by BCA and information gathered

from desk research and trade interviews with leading construction companies in Singapore

Note: audited data if available is usually not industry specific and includes other products/services.

Industry ranking is therefore estimated on publicly available data and the trade opinion survey

(not just the companies themselves). When ranking and shares are being disclosed, the Client’s

entity name and its corresponding market share will be revealed concurrently, for other leading

players, if their market shares are to be revealed, their entity name will then be disclosed on an

anonymous basis.

Based on Euromonitor’s market estimates, the revenue of the Company (including

revenues as either main-contractor or sub-contractor) had market share equivalent to

approximately 1.7% of revenue receipts for civil engineering works in Singapore in

2019.

– 89 –THIS DOCUMENT IS IN DRAFT FORM. The information contained in it is incomplete and is subject

to change. This Document must be read in conjunction with the section headed ‘‘Warning’’ on the

cover of this Document.

INDUSTRY OVERVIEW

3.3 Outlook for infrastructure development in the region

Civil engineering construction companies in Singapore can potentially play a key

role for infrastructure development across Asia. This will be supported by the setting

up of a new Infrastructure Office by the government under the 2018 Budget. The

Infrastructure Office intends to bring together local and international players from

across the entire value chain (including developers, institutional investors, management

and professional services providers) to develop, finance and execute infrastructure

projects. The initiative is expected to provide opportunities and a platform for

Singapore players to play an active role in the region’s infrastructure development.

Future projects in Singapore

The LTA has plans to double the length of the MRT network from 178km in

2013 to 360km in 2030 by building two completely new MRT lines (the Cross Island

Line and Jurong Regional Line) and lengthening existing lines (e.g. Circle Line Stage

6 and the North East Line extension). By 2030, eight in ten Singapore households will

be within a 10-minute walk of a train station. Below are highlights of the future MRT

projects:

• The Cross-Island Line was announced in 2013 and is targeted to be

completed by 2030. It is in planning stages including an engineering

feasibility study and an Environmental Impact Assessment for the alignment

around the Central Catchment Nature Reserve.

• Jurong Region Line is scheduled to be fully completed in 2028, adding 24

stations to the existing rail network. The line is expected to become

available to commuters in three stages from 2026 onwards.

• Circle Line Stage 6 (CCL6) will close the loop for the Circle Line by

connecting Harbour Front Station to Marina Bay Station. As of November

2017, LTA has awarded a total of approximately S$2.3 billion worth of

contracts for the civil construction of Keppel, Cantonment and Prince

Edward Stations, associated tunnels and Kim Chuan Depot extension for

CCL6. CCL6 is expected to be completed in 2025.

• Construction of tunnels to the future Punggol Coast station on the North

East Line extension is awarded in December 2017. Part of the S$ 79 million

contract will involve the construction of a pair of tunnels between Punggol

station and the new Punggol Coast station. Work on the tunnels is expected

to be completed by 2023. With the new station, there will be a total of 17

stops along the North East Line.

– 90 –THIS DOCUMENT IS IN DRAFT FORM. The information contained in it is incomplete and is subject

to change. This Document must be read in conjunction with the section headed ‘‘Warning’’ on the

cover of this Document.

INDUSTRY OVERVIEW

• Between 2015 and 2018, a total of SGD7.2 billion of contracts was

awarded by the LTA for works on the Downtown Line and the Thomson-

East Coast Line. These expansion plans are designed to extend the

Downtown Line from Expo to Sungei Bedok by 2024 and to open Hume

Station by 2025.

• A proposed new line has been revealed in the Land Transport Master Plan

2040. This new line will supplement the transport network in the north and

northeast regions to serve new and growing developments, as well as

existing towns which currently do not enjoy direct access to the rail

network. The corridor served by the new line could include areas such as

Woodlands, Sembawang, Sengkang, Serangoon North, Whampoa, Kallang

and the Greater Southern Waterfront.

Other than MRT-related projects, the other notable upcoming project in

Singapore include:

• Changi Airport Terminal 5, which is scheduled to start in 2020 and to be

completed around 2030. This terminal double Changi Airport size to cover

more than 2,000 hectares and bring an additional capacity of up to 50

million passengers a year – more than twice the size of any of the other

three main terminals. According to Strait Times article published in Oct

2018, the project is Singapore’s most ambitious attempt, since Changi

Airport opened on July 1, 1981, to cement Singapore’s status as a key

aviation hub for regional and global traffic.

• The Tuas Mega Port is a major milestone in Singapore’s next generation

container terminal development. In addition, there are plans to develop Tuas

Terminal into a maritime hub with storage facilities and commercial

amenities. The project includes four phases, targeted for completion in

2040. The mega port will commence its first phase of operations in 2021,

with two berths for ships.

• The Greater Southern Waterfront Plan, announced in 2013, will transform

Singapore’s southern waterfront, which extends from Pasir Panjang to

Marina East, into a new major gateway and location for urban living.

Development will take place in phases, starting with the former Pasir

Panjang Power District, Keppel Club and Mount Faber in the next 5 to 10

years. The plan will also entail moving port terminals to Tuas, with Pasir

Panjang Terminal slated to move by 2040 in order to free up prime land for

redevelopment.

– 91 –THIS DOCUMENT IS IN DRAFT FORM. The information contained in it is incomplete and is subject

to change. This Document must be read in conjunction with the section headed ‘‘Warning’’ on the

cover of this Document.

INDUSTRY OVERVIEW

Among contracts that have been awarded by LTA in 2018 but have yet to start

work, the most notable project is the construction of the North-South Corridor (NSC),

a 21.5km expressway which will connect towns in the north to the city centre and

features dedicated bus and cycling lanes. The full project is targeted to be completed

in 2026. In December 2019, the LTA awarded the final batch of three contracts, worth

a combined S$954.1 million for the NSC.

– 92 –You can also read