Market report German residential market - Growth in the shadow of the major cities - Savills

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Savills World Research

Germany

Market report

German residential

market March 2018

Growth in the shadow of the major cities

savills.de/research 01

savills.de/research

Market report | Residential market Germany March 2018

Growth in the shadow of the major cities

Conditions in the German residential market remain excellent for owners and investors. The population

continues to grow, average household incomes rose at the fastest rate for ten years in 2017 and the

unemployment rate is at its lowest level since German reunification. Furthermore, it is highly unlikely that

this environment will significantly deteriorate in the foreseeable future. Residential investors are, therefore,

expected to enjoy continued outstanding conditions over the coming years. However, this also entails

certain challenges. Already, there are no longer any genuine hidden gems for investors to discover in

the major cities and competition among bidders is correspondingly strong everywhere. That being

said, outside of the traditional ABCD city categories, there remain some interesting locations where few

investors have been active to date.

Text: Matti Schenk

GRAPH 1

only risen for thirteen years. New-build

Half of all districts will activity has also risen consistently Population will decline, number of

continue to grow since 2010. In 2016, a total of around households will increase by a majority

Population growth is not only benefiting 278,000 apartments were completed growing stagnating shrinking

350

the major cities. Between 2012 and in Germany, approximately 115,000 of

2016, the population increased in which were in apartment buildings. This 300

some two thirds of the 401 rural represents an increase in completions

districts (Landkreis) and urban districts of almost 39% compared with five 250

(kreisfreie Stadt). In further 81 districts, years earlier. The number of new-build

number of districts

the population remained relatively apartments completed in apartment 200

stable (+/- 1%). Only 45 districts buildings even rose by 62% (Graph 2).

150

recorded a decline of 1% or more in However, this still fell significantly short

the number of inhabitants, with 32 of of the current annual requirement of 100

these situated in the federal states 400,000 new-build apartments. In

created from the former East Germany. addition, the trend for the number of 50

Going forward, however, population building permits is showing signs of

figures will decline in an increasing reversal. According to the Federal 0

2012-2016 2017-2030* 2012-2016 2017-2030*

number of districts. According to Statistical Office, around 313,700

population households

projections from Bulwiengesa based apartments were approved between

Source: Bulwiengesa, BBSR / * forecast

on the 13th coordinated population January and November 2017, which

projection of the Federal Statistical reflects an 8% decrease year on year.

Office, only 95 rural and urban districts While there may be a large backlog

GRAPH. 2

will witness growth between 2017 and in terms of building permits, the

2030. In 237 rural and urban districts, indications of an end to the boom in More is being built, but still too little

the population is expected to decline apartment construction are increasing.

(Graph 1). Growth in the number This is substantiated by research from completions permits

of households is significantly more the German Institute for Economic completions: proportion of apartments permits: proportion of apartments

450,000 90%

positive. This is expected to increase Research, which cites a lack of

in 198 rural and urban districts, i.e. half tradespeople, shortage of sites and 400,000 Demand of new buildings per year 80%

share apartments in apartment buildings

of all districts, by 2030. These regions rising construction costs as reasons. 350,000 70%

account for 62% of all households. The effects of measures to promote

300,000 60%

housebuilding agreed between the

apartments

SPD and CDU/CSU during coalition 250,000 50%

No relaxation at the negotiations remain to be seen. 200,000 40%

rental apartment However, there is little evidence to

markets indicate any noticeable relief in the 150,000 30%

Owing to the high demand, rents on strain in the housing markets on the 100,000 20%

existing and new-build apartments rose horizon. Consequently, landlords will

50,000 10%

once again last year, increasing by an remain in a strong position in many

average of 6% year on year in the 127 locations. 0 0%

2010 2011 2012 2013 2014 2015 2016

largest property markets. Rents did not

fall in a single city. Indeed, they have Source: Federal Statistical Office

savills.de/research 02Market report | Residential market Germany March 2018

even these cities have witnessed GRAPH 3

Investment market appreciable yield compression since Largest investment dynamics in some

remains highly 2015. Yields in Oberhausen, for

cities in the Ruhr region

competitive instance, hardened by 167 basis points

transaction volume 2017

In view of the favourable general between 2015 and 2017 while those transaction volume compared to the 5-year average

conditions combined with modest in Mülheim hardened by 144 basis 28 700

growth in supply, demand for points. This represents significantly 24 600

2017 vs. Ø previous 5 years

22

apartments also remains high in greater yield compression than in the

20 500

the investment market. Moreover, A-cities, where yields hardened by an

a multitude of recently launched average of just 90 basis points. The 16 400

€m

15

residential funds will now start to same applies to other cities. Of the 22 12 300

11

build their portfolios, which will cities that recorded yield compression

8 200

further intensify competition among of more than 150 basis points, 18 7

116

333

630

89

bidders. Average prices of apartments have negative population growth 5

89

245

4 4 4 100

3 3 3 3 3 2 2 2

Oberhausen 124

transacted have already risen projections. These include Salzgitter,

Mainz 190

76

Remscheid 50

Ingolstadt 81

Kaiserslautern 68

Hanau 65

Fürth 55

Neuss 60

0 0

significantly over the last three years. Brandenburg (Havel), Recklinghausen

Mülheim (Ruhr)

Düsseldorf

Bochum

Chemnitz

Duisburg

Schönefeld

Essen

In 2017 alone, average prices rose and Siegen (see Graph 4). Oberhausen

by 28%. In the seven A-cities, the and Mülheim will also witness

corresponding increase was 33%. population declines of 5% by

While this may be explained by other 2030 according to the projections. Source: Savills / * only transactions from 50 units; locations from €50m

factors, such as a higher proportion of Although population projections are

development acquisitions, it is likely to just one indicator among many for

be at least partially attributable to the evaluating opportunities and risks, GRAPH 4

more intensive competition among this observation can be regarded as

bidders. an indication of stronger appetite for Strong yield compression even in

risk on the part of investors. While shrinking cities

stable rental income can doubtlessly 300

Majority of investors be achieved on residential properties Salzgitter

remain focused on

yield compression in basic points 2015-2017

in good locations in Oberhausen, 250

established markets

Brandenburg (Havel)

Chemnitz and Mülheim, the

Recklinghausen

Competition among bidders remains significantly greater risks of the macro- 200

Chemnitz Bremerhaven

Zwickau

strong, particularly in the A-cities, location cannot be ignored. Villingen-Schwenningen

Erfurt

which is attributable both to the

150

positive growth prospects and the

high liquidity of these markets. The Under-valued cities are

seven A-cities accounted for around now scarce 100

50% of the transaction volume last That some investors are now venturing

50

year (5-year average: 46%). A further into cities with unfavourable population

19% of the volume was attributable to projections could also be explained by

the 14 B-cities (5-year average: 16%). the fact that there are now scarcely any 0

-20% -15% -10% -5% 0% 5% 10%

To put this into context, these 21 cities with favourable fundamental data population forecast 2017-2030

cities are home to around 20% of the that do not attract significant demand

Source: Bulwiengesa

German population. Hence, investors from investors. If we compare average

are narrowing their focus on a small gross initial yields and population

number of major cities, driving local projections in the 127 largest property

GRAPH 5

prices even higher. markets (Graph 5), there are only six

growing cities in Bergisch Gladbach, Yield-risk-matrix: Hardly any

Brunswick, Bremerhaven, Flensburg, under-valued growth location

Some investors are Greifswald and Halberstadt where tendential overrated tendential balanced tendential underrated

relaxing their attitude to yields appear relatively high. Two years 10%

risk ago, there were eleven such cities. This

9%

However, other cities also attracted also demonstrates that investors have

8%

gross initial yield 2017

significantly greater interest from widened their search radius.

investors last year. Transaction 7%

volumes in cities such as Oberhausen 6%

and Mülheim an der Ruhr, for Beyond the city limits – 5%

example, totalled more than ten times are surrounding regions

the hidden champions?

4%

the average figure over the last five

3%

years. Other cities in the Ruhr region, While some investors are seeking

such as Duisburg and Bochum, also investment opportunities in the 2%

witnessed significant growth (see demographically less favourable 1%

Graph 3). Many of these locations C-cities and D-cities, the population is 0%

are gaining in popularity due to increasingly migrating to other regions. -20% -15% -10% -5% 0% 5% 10%

population forecast 2017-2030

relatively attractive gross initial yields The surrounding regions of A-cities

of significantly above 6%. However, in particular are registering increasing Source: Bulwiengesa

savills.de/research 03Market report | Residential market Germany March 2018

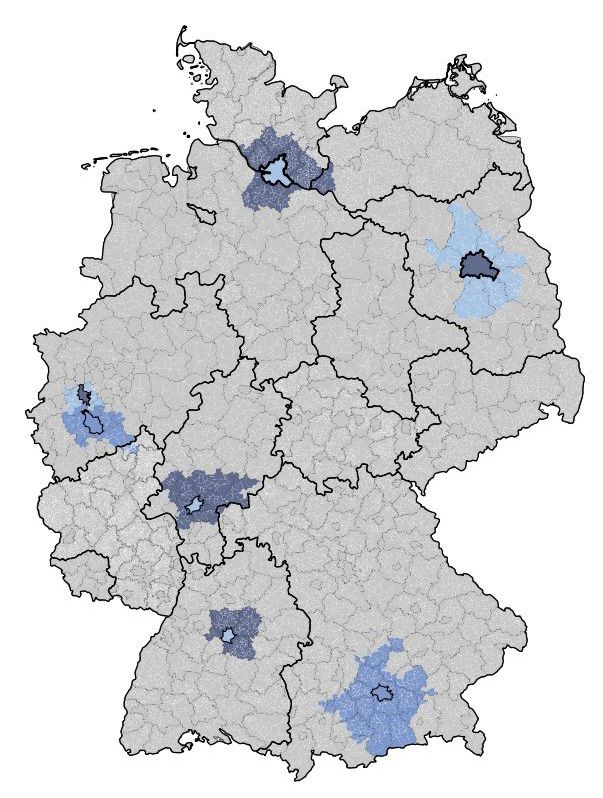

GRAPH 6

„In the surrounding areas of A-citites Population growth in the surrounding

strong fundamentals are meeting areas is gaining momentum

comparably low demand from investors.

core cities: 2011-2015 surroundings: 2011-2015

core cities: 2014-2015 surroundings: 2014-2015

9%

Therefore, checking these locations could 8%

be worthwhile.” Matti Schenk, Savills Research 7%

growth of population

6%

population growth. While such regions increased migration to surrounding 5%

have received little attention as areas. As shown by BBSR analysis,

4%

investment locations to date, there is Berlin and Munich for instance have

much to suggest that this neglect is consistently lost inhabitants to their 3%

unwarranted. surrounding areas since 2005. Even

2%

during the boom in the major cities

of recent years, there has been 1%

Metropolitan regions are continuous suburbanisation and 0%

likely to be even more there are indications that migration Berlin Frankfurt Hamburg Munich Düsseldorf Cologne Stuttgart

attractive going forward to surrounding areas has been on Source: BBSR, Federal Statistical Office

It is safe to assume that the major the increase. Migration from Berlin

metropolitan regions will continue to Brandenburg, for instance, was

to grow. As centres of academia higher in 2015 than at any time in the GRAPH 7

and business, they will continue to last 15 years. Migration from Munich

attract young and well-educated to Bavaria has also risen significantly. Asking rents are rising partly faster

people from elsewhere in Germany Both cities have been growing for than in core cities

and abroad. Besides the core cities, many years, primarily due to positive rent core city rent surrounding area

core city: rental growth 2014-2017 surrounding area: rental growth 2014-2017

this is also likely to benefit the external migration. As shown by BBSR

20 20%

surrounding areas as illustrated by research, the immediate surroundings

average asking rents in € per s qm

18 18%

the small-scale population projection of commuter intersection areas are

from the German Federal Institute particularly likely to benefit from 16 16%

rental increase 2014-2017

for Research on Building, Urban increasing migration from cities to 14 14%

Affairs and Spatial Development surrounding regions 12 12%

(BBSR). In contrast, the prospects

10 10%

in small and medium-sized cities in

structurally weak areas in particular Some surrounding 8 8%

are overwhelmingly unfavourable. In regions are already 6 6%

his column in the New York Times, growing faster than their 4 4%

Nobel Prize winner Paul Krugman core cities 2 2%

recently wrote about the decline of For the purpose of defining the

0 0%

America’s small and medium-sized surrounding regions, we will use the Berlin Düsseldorf Frankfurt Hamburg Cologne Munich Stuttgart

cities. Although the situation in the urban-rural regions (Stadt-Land-

Source: empirica Systeme Marktdatenbank

USA cannot be compared directly Region)1devised by the BBSR. Based

with that in Germany, industrial cities upon these regions, more than 9.9

and rural locations in Germany are million people live in the surrounding

GRAPH 8

also expected to predominantly regions of the A-cities. This is higher

lose inhabitants over the long term. than the populations of the cities Transaction volume remains behind

Conversely, in an increasingly themselves, which total approximately core cities

digitised knowledge-based economy, 9.8 million people. While population transaction volume surrounding areas of A-cities*

academia, research and high-quality figures in the A-cities grew faster than transaction volume compared to A-cities

900 18%

services will continue to expand. This in the surrounding regions between

transaction volume in % of the A-city-volume

suggests that the metropolitan regions 2011 and 2015, this trend is slowly 800 16%

could be even more attractive going reversing. In 2015, four in seven

transaction volume in €m

700 14%

forward. Another consequence of surrounding regions witnessed faster 600 12%

this is that demand for housing will growth than their core cities, as shown

500 10%

increase further in future in Graph 6. This was particularly the

case in Berlin and Munich. While 400 8%

no more recent population growth 300 6%

Are we at the start data is available from the individual

of a new wave of municipalities, it can be assumed that

200 4%

suburbanisation? this trend has continued and there is 100 2%

However, the core cities in the much to suggest that the growth will 0 0%

metropolitan regions already continue for the long term. 2009 2010 2011 2012 2013 2014 2015 2016 2017

appear to be reaching their growth

limits. This could potentially lead to Source: Savills / * only transaction from 50 units; locations from €50m

1

The demarcation of these regions respects municipality (Gemeinde) boundaries and is primarily

based around commuter intersections and accessibility. savills.de/research 04Market report | Residential market Germany March 2018

Some surrounding GRAPH 9

regions are overtaking The seven urban-rural regions of A-cities with development of

core cities in terms of asking rents since 2014

rental growth

Not only are the surrounding regions

benefiting from relatively favourable

demographic growth, the situation

in the rental apartment market is

also attractive to investors. This

is substantiated by an analysis of

average asking rents (Graph 7).

Between 2014 and 2017, these

showed higher growth in the

surrounding regions of Frankfurt,

Hamburg and Stuttgart than in the core

cities. In Cologne and Munich, asking

rents rose at the same pace in the

surrounding regions and core cities.

Only in Berlin (-5 percentage points)

and Düsseldorf (-1 percentage point)

did rents increase more slowly in the

surrounding regions (see also Graph 9).

Building a portfolio in

the surrounding regions

could be worthwhile

In addition, from an investor's

perspective, the investment markets

in surrounding regions are significantly

less competitive than in the core cities.

Although the surrounding regions of

the A-cities have more inhabitants than

the A-cities themselves, residential

properties in the surrounding regions

changed hands for a total of just

€812m last year (Graph 8). This

compares with a transaction volume

of more than €6.7bn in the A-cities

themselves. A total of approximately

5,400 apartments were sold in the

surrounding regions at an average

price 20% lower than in the core

cities. While the number of existing

apartments in apartment buildings

is lower in the surrounding regions

than in the A-cities, surrounding

districts account for approximately

44% of all apartments in apartment

buildings. Consequently, investment Legend: rental growth of core city and surrounding area in comparison

opportunities for institutional investors stronger rent increase

are available. Therefore, it may be weaker rent increase

a promising strategy to extend

same rent increase

investment searches beyond the

boundaries of the A-cities. Source: Savills / map source: BKG

savills.de/research 05Market report | Residential market Germany March 2018

Savills Germany

Savills is present in Germany with HH

around 200 employees with seven

offices in the most important estate

sites Berlin, Dusseldorf, Frankfurt,

B

Hamburg, Cologne, Munich and

Stuttgart. Today Savills provides

expertise and market transparency

to its clients in the following areas

D

of activity

Unsere Dienstleistungen C

»» Investment

»» Agency F

»» Portfolio Investment

»» Debt Advisory

»» Valuation

S

M

www.savills.de

Savills Germany

Please contact us for further information

Marcus Lemli Karsten Nemecek Draženko Grahovac Matti Schenk

CEO Germany Corp. Finance - Valuation Corp. Finance - Valuation Research Germany

+49 (0) 69 273 000 12 +49 (0) 30 726 165 138 +49 (0) 30 726 165 140 +49 (0) 30 726 165 128

mlemli@savills.de knemecek@savills.de dgrahovac@savills.de mschenk@savills.de

Savills is a leading global real estate service provider listed on the London Stock Exchange. The company, established in 1855, has a rich heritage with unrivalled growth. It is a company

that leads rather than follows and now has over 600 offices and associates throughout the Americas, Europe, Asia Pacific, Africa and the Middle East with more than 35,000 employees

worldwide. Savills is present in Germany with around 200 employees with seven offices in the most important estate sites Berlin, Dusseldorf, Frankfurt, Hamburg, Cologne, Munich and

Stuttgart.

his bulletin is for general informative purposes only. Whilst every effort has been made to ensure its accuracy, Savills accepts no liability whatsoever for any direct or consequential loss

arising from its use. The bulletin is strictly copyright and reproduction of the whole or part of it in any form is prohibited without written permission from Savills Research.

© Savills March 2018

savills.de/research 06You can also read