Quarterly Market Outlook - 1Q2021 Global Markets January 2021 - Hong Leong Bank

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Quarterly Market Outlook

1Q2021

Global Markets

January 2021

Content

Macro Landscape

FX Outlook

Fixed Income Outlook

2

Global Growth Outlook

Real GDP

Latest 2 Quarters Actual Forecast Forecast (official)

(% YOY)

2Q20 3Q20 2019 2020 2021 2020 2021

World - - 2.9 -4.4(-3.9) 5.2 (5.2) -4.4(-4.9) 5.2 (5.4)

DM/ G10 -23.1 15.3 1.7 -5.2 (-5.8) 4.0 (4.2) - -

US -9.0 -2.8 2.3 -3.5 (-4.3) 3.9 (3.7) -2.4 (-3.7) 4.2 (4.0)

Eurozone -14.7 -4.3 1.2 -7.4 (-8.0) 4.6 (5.5) -7.3 (-8.0) 3.9 (5.0)

UK -20.8 -8.6 1.4 -11.3 (-10.0) 5.3 (6.3) -11.0 (-9.5) 7.3 (9.0)

Japan -10.3 -5.7 0.7 -5.3 (-5.7) 2.7 (2.5) -5.5 (-4.7) 3.6 (3.3)

BRICs -2.6 1.9 5.2 0.9 (0.6) 5.4 (4.9) - -

China 3.2 4.9 6.1 2.0 (2.1) 8.3 (8.0) - -

India* -23.9 -7.5 6.1 -8.5(-8.0) 9.2 (8.1) - -

Asia ex-Japan -2.4 1.7 5.3 0.8 (0.8) 5.5 (5.1) - -

EMEA -9.5 -2.0 2.5 -3.8(-4.5) 3.6 (3.8) - -

Source: Bloomberg, official sources

Figures in ( ) are previous forecasts

*FY ending Mar-21 and Mar-22 respectively

3Global Central Banks Policy Outlook

Current 1Q21 2Q21 3Q21 4Q21 Remarks

United States

Federal Reserve 0-0.25 0-0.25 0-0.25 0-0.25 0-0.25 No change in 2021

Fed Funds Rate

Eurozone

European Central Bank -0.50 -0.50 -0.50 -0.50 -0.50 No change in 2021

Deposit Rate

United Kingdom

Bank of England 0.10 0.10 0.10 0.10 0.10 No change in 2021

Bank Rate

Japan

Bank of Japan -0.10 -0.10 -0.10 -0.10 -0.10 No change in 2021

Policy Balance Rate

Australia

Reserve Bank of Australia 0.10 0.25 0.25 0.25 0.25 No change in 2021

Cash Rate

New Zealand

Reserve Bank of New Zealand 0.25 0.25 0.25 0.25 0.25 No change in 2021

Official Cash Rate

Malaysia

Potential cut/

Bank Negara Malaysia 1.75 1.75 1.75 1.75 1.75

Easing bias

Overnight Policy Rate

Thailand

Potential cut/

The Bank of Thailand 0.50 0.50 0.50 0.50 0.50

Easing bias

1-Day Repurchase Rate

Indonesia

Bank Indonesia 4.00 3.75 3.75 3.75 3.75 Plenty of room to cut

7-day Reverse Repo Rate

Singapore

Monetary Authority of Singapore - - On hold - On hold No change in 2021

SGD NEER

Source: Bloomberg, HLBB Global Markets Research 4US - Mixed recovery as job growth slowed; hope on more stimulus

8 'mil 'mil 30 • Slower labour market revival; surging coronavirus

7 Initial Jobless Claims -LHS cases pose downside risk to economic recovery.

25

6

Continuous claims (Lagged one

20

5 week), RHS • Consumer spending outlook is uncertain after

4 15 coming off the steep recovery; effect of first stimulus

3

10 checks had tapered off.

2

5

1

• A Democrats-controlled Congress alongside the

0 0

Biden Administration to offer more meaningful fiscal

15-Feb

07-Mar

28-Mar

03-Oct

24-Oct

14-Nov

05-Dec

26-Dec

18-Apr

30-May

09-May

11-Jul

01-Aug

22-Aug

12-Sep

04-Jan

25-Jan

20-Jun

expansion, instantly brightening spending prospect.

20

• Manufacturing expansion is expected to continue

15

Personal Spending, MOM % but weighed down by Covid-19 related supply

10 Retail Sales, MOM % constraint/disruption.

5

0 • The bright spot remains on the housing sector as

Mar-19

Mar-20

May-19

May-20

Apr-19

Jul-19

Apr-20

Jul-20

Feb-19

Oct-19

Feb-20

Oct-20

Aug-19

Sep-19

Nov-19

Dec-19

Aug-20

Sep-20

Nov-20

Jan-19

Jun-19

Jan-20

Jun-20

-5 low borrowing rates, change in working culture (ability

-10 to work from home) spurred suburban shifts.

-15 Downside remains the lack of (housing) supply.

-20

Source: Bloomberg, HLBB Global Markets Research

5Eurozone – Lockdowns to delay bloc’s recovery

15

10 Germany IPI, MOM %

• Extended and stricter lockdowns to delay

EU IPI, MOM % economic recovery. New Covid-19 strain poses

5

downside risk to economy despite vaccine

0

rollout.

Dec-19

Dec-18

Apr-18

Apr-19

Apr-20

Feb-18

Oct-18

Feb-19

Oct-19

Feb-20

Oct-20

Jun-18

Aug-18

Jun-19

Aug-19

Jun-20

Aug-20

-5

-10 • Pandemic related supply constraint to drag on

-15

overall manufacturing sector. Germany is

expected to remain a growth driver.

-20

8.8 • Unemployment rate has fallen from peak.

8.6 Sustained growth in manufacturing would

8.4

Unemployment Rate, %

recreate more employments but extended

8.2

lockdowns threatened services job.

8.0

7.8

7.6

7.4

7.2

7.0

Feb-18

Feb-19

Feb-20

Apr-18

Apr-19

Apr-20

Oct-18

Oct-19

Oct-20

Dec-18

Dec-19

Jun-18

Aug-18

Jun-19

Aug-19

Jun-20

Aug-20

Source: Bloomberg, HLBB Global Markets Research

6UK – Near term prospects falter amid raging pandemic

1200 5.1

• Near-to-medium term economic recovery

1000 4.9

prospect dampens considerably after third

UK Jobless Claims Change ('000), 4.7

800

LHS

lockdown was ordered.

4.5

600 Unemployment Rate, %, RHS

4.3 • Less generous job retention scheme

400

4.1 alongside stricter restrictions are negatives

200

3.9 for job market and retail sector - higher jobless

0 3.7 rate and jobless claims.

Feb-18

Apr-18

Oct-18

Feb-19

Apr-19

Feb-20

Apr-20

Oct-19

Oct-20

Dec-18

Dec-19

Jun-18

Aug-18

Jun-19

Aug-19

Jun-20

Aug-20

-200 3.5

• Post-Brexit adjustment/hiccup an added risk

20 potentially derailing recovery efforts

15

10 Retail Sales, MOM %

5

0

-5

-10

-15

-20

Apr-20

Feb-18

Apr-18

Feb-19

Apr-19

Feb-20

Oct-18

Oct-19

Oct-20

Dec-18

Dec-19

Aug-20

Jun-18

Aug-18

Jun-19

Aug-19

Jun-20

Source: Bloomberg, HLBB Global Markets Research

7Australia – Heightened dispute with China a new risk

300 8

200 7

100

• Gradual economic recovery after recent

6

0 emergence from hard lockdown in the Victoria

-100 5

state.

-200 4

-300 3

-400 Employment Change('000), LHS • Firms expected to raise employments as

2

-500 Unemployment Rate (%), RHS labour force also expanded.

-600 1

-700 0

• Growth in services sector - retail sales seen

Feb-18

Feb-19

Feb-20

Apr-18

Apr-19

Oct-19

Apr-20

Oct-18

Oct-20

Dec-18

Dec-19

Jun-18

Aug-18

Jun-19

Aug-19

Jun-20

Aug-20

improving post lockdown.

20

15 • Downside risk from trade dispute with China,

10 its biggest trading partner.

5

0

-5

-10 Retail Sales, MOM %

-15

-20

Apr-18

Apr-19

Apr-20

Feb-18

Oct-18

Feb-19

Oct-19

Feb-20

Oct-20

Dec-18

Dec-19

Jun-18

Aug-18

Jun-19

Aug-19

Jun-20

Aug-20

Source: Bloomberg, HLBB Global Markets Research

8Japan – Third virus wave dragging on already weak economy

3.5 15

3.0 10 • Manufacturing and international trade to benefit

2.5 5 from rebound in global demand. PMIs are pointing to

2.0 0 stabilisation at factories.

1.5 -5

1.0 -10 • Third virus wave an immediate threat to recovery

Household Spending, YOY % (RHS)

0.5 Japan Jobless Rate, % (LHS) -15 and could once again lead to rescheduling of the

0.0 -20 Tokyo Olympics resulting in economic losses.

Dec-18

Dec-19

Feb-19

Apr-20

Apr-18

Apr-19

Feb-18

Oct-18

Oct-19

Feb-20

Oct-20

Jun-18

Aug-18

Jun-19

Aug-19

Jun-20

Aug-20

• Consumer spending remains cautious as job

15 10

market weakened. Inflation is expected to remain

10 weak.

5 5

0

-5 0

-10

-15 -5

-20

Japan Export, YOY % (LHS)

-25 -10

Japan IPI, YOY % (RHS)

-30

-35 -15

Feb-19

Apr-20

Apr-18

Apr-19

Feb-18

Oct-18

Oct-19

Feb-20

Oct-20

Aug-18

Dec-18

Aug-19

Dec-19

Aug-20

Jun-18

Jun-19

Jun-20

Source: Bloomberg, HLBB Global Markets Research

9China – Positioning for pre-eminence

20 China’s key metrics continue their rebound (% YOY) • We forecast elevated 8% GDP growth in 2021,

15

10 supported by base effects. Growth is likely

5 consumer-led as Covid-19 vaccination spreads,

0

-5

confidence returns and labor market improves.

-10

-15 • Export growth (>9% YOY Aug-Nov 2020) has

-20

-25 also been strong and should persist. The

Jul-18 Jan-19 Jul-19 Jan-20 Jul-20 recent RCEP deal is positive for intra-Asia trade.

Industrial production Retail sales Exports

• Inflation (particularly core) may start to

Forecasts 2020 2021

rebound from muted levels from mid-2021.

GDP (%) 1.7 8.0 We expect food inflation to taper off in contrast.

Inflation (%, Avg) 3.0 2.7 • We expect the People’s Bank of China to

maintain a neutral stance for now. PBOC

5Y LPR (%) 4.65 4.65 should allow modest CNY strengthening, while

injecting liquidity if needed. We do not expect

USD/CNY 6.53 6.25 many interest rate moves.

Source: Bloomberg, HLBB Global Markets Research

10Hong Kong – Piggybacking on China’s recovery

Total Exports: to China

HK$, bn

450

Total Exports to Others

Exports to China, %

%

40.0

• Economy showing more signs of

400 Total Exports YOY, %

30.0

stabilisation, although still in downturn.

350

20.0

300

• Prospect for recovery brightened alongside

250 10.0

200

firmer rebound in China. Hong Kong still

0.0

150 exports more than 50% of its goods to China and

-10.0

100 strong demand from Mainland set the course for

50 -20.0

its trade sector.

0 -30.0

2018 2019 2020

• Domestic demand is improving. Retail sales

40

30

narrowed its decline to single-digit recently,

20 Retail Sales, YOY % driven by purchases of durable household items.

10 Sales may improve further this month ahead of

0

Lunar New Year.

-10

-20

-30

-40

-50

May-18

May-19

May-20

Feb-18

Mar-18

Apr-18

Jul-18

Feb-19

Mar-19

Apr-19

Jul-19

Feb-20

Mar-20

Apr-20

Jul-20

Oct-18

Oct-19

Oct-20

Nov-18

Dec-18

Nov-19

Dec-19

Nov-20

Jun-18

Aug-18

Sep-18

Jan-19

Jun-19

Aug-19

Sep-19

Jan-20

Jun-20

Aug-20

Sep-20

Source: Bloomberg, HLBB Global Markets Research 11Singapore – Some bottlenecks against swift recovery

80

Divergent performance among export components (% YOY)

60

40 • A rebound in services sector activities is

20

0

likely to underpin GDP growth in 2021.

-20 Vaccination program will take place mostly in 1H-

-40 2021. Domestic sectors (services and

-60

construction) are likely benefit from improved

-80

-100 activity levels.

Jan-13 Jul-14 Jan-16 Jul-17 Jan-19 Jul-20

Oil exports Non-oil domestic exports Non-oil re-exports

• Export growth (particularly electronics)

should benefit from advance rebound in Asia

Forecasts 2020 2021

trade. Still, oil-related products are still in a

GDP (%) -5.8 6.3 slump and may persist for 1H-2021 (see chart).

Inflation (%, Avg) -0.2 0.5 • We expect Monetary Authority of Singapore

to maintain policy settings in April 2021.

3m SIBOR (%) 0.40 0.40 Inflation may still stay benign while financial

conditions stay fragile.

USD/SGD 1.32 1.285

Source: Bloomberg, HLBB Global Markets Research

12Vietnam – Outperforming ASEAN neighbours

9

8

GDP Growth YOY, % • Economy managed to stave off recession

7 thanks to low virus cases but global pandemic

6 sent annual growth level to the lowest in more

5 than 30 years.

4

3

2

• Manufacturing and trade sectors benefited

1 from US-China trade dispute and is set to

0 continue driving growth in 2021.

Jun-13

Mar-17

Mar-14

Jun-14

Mar-15

Jun-15

Mar-16

Jun-16

Jun-17

Mar-18

Jun-18

Mar-19

Jun-19

Mar-20

Jun-20

Dec-13

Sep-14

Dec-14

Dec-15

Dec-16

Dec-17

Dec-18

Dec-19

Dec-20

Sep-13

Sep-15

Sep-16

Sep-17

Sep-18

Sep-19

Sep-20

• Government set ambitious growth target of

40 6.5% for 2021 (pre-pandemic 2020 target: 6.0%)

30

Vietnam IPI, YOY % anticipating further economic revival.

Exports, YOY %

20

10

0

Feb-19

Feb-18

Apr-18

Apr-19

Feb-20

Apr-20

Oct-18

Oct-19

Oct-20

Dec-18

Dec-19

Dec-20

Aug-20

Jun-18

Aug-18

Jun-19

Aug-19

Jun-20

-10

-20

Source: Bloomberg, HLBB Global Markets Research

13Malaysia – Cautious recovery in 2021

• Broad-based recovery expected from both

domestic and external front – aided by global

recovery, policy measures and low base effect

from last year’s slump

• Private consumption (~60% of GDP) expected

to turn around but remained subdued and below

long-run average, constrained by to softer job

market and consumer sentiments; but stimulus

measures will provide some support

Forecasts 2020 2021 • Overall investment to remain weak and see

narrower declines amid bleak business outlook

GDP (%) -6.0 5.4

• Net exports will remain a main growth pillar in

Inflation (%, Avg) -1.0 1.3

2021 as gains in exports outweigh imports

OPR (%) 1.75 1.75

• No change to OPR - BNM to maintain OPR at

USD/MYR 4.02 3.88 current accommodative level of 1.75%, barring

substantial shift in downside risk.

Source: Department of Statistics Malaysia, HLBB Global Markets Research

14FX Outlook

Q4-20A Q1-21 Q2-21 Q3-21 Q4-21 • We expect another year of dollar weakness. Without

significant fiscal impulse, the US Federal Reserve will likely

DXY 89.94 88.50 89.00 88.50 87.50 keep monetary policy at current accommodativeness.

Negative real US interest rates, a global recovery and

USD/CAD 1.273 1.255 1.260 1.240 1.230 market appetite for risky assets are usually dollar negative.

EUR/USD 1.222 1.245 1.240 1.245 1.255

• We expect some gains in EUR and GBP. Fundamentals

GBP/USD 1.367 1.385 1.375 1.385 1.400 are soft, even as a Brexit deal provides some relief to the

pound. However, the Eurozone and the UK should recover

USD/CHF 0.885 0.870 0.875 0.870 0.865 from a raging pandemic, as immunization rates rise.

AUD/USD 0.769 0.780 0.770 0.780 0.795 • Potential for commodity price recovery positive for

AUD, NZD, CAD, MYR. These G10 and other Asia

NZD/USD 0.718 0.730 0.725 0.735 0.745 currencies benefit from risk-on mood. Downside risk is that

the respective central banks resist from moving to negative

USD/JPY 103.25 102.5 103.5 103.0 101.0 interest rate policies.

USD/MYR 4.020 3.900 3.950 3.900 3.880 • A strong CNY may support other Asian currencies

(such as MYR and SGD). We are positive on intra-Asia

USD/SGD 1.322 1.305 1.310 1.300 1.285

trade leading the global recovery.

USD/CNY 6.503 6.350 6.400 6.350 6.250

Source: Bloomberg, HLBB Global Markets Research

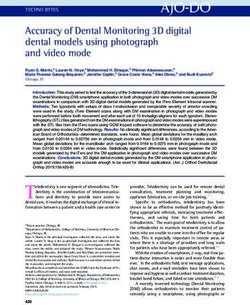

15US Fixed Income – Upward pressure on yields amid recovery expectations

UST

- Upward pressure on UST yields were seen extending out from 5Y onwards with overall

benchmark yields settled between 0-23bps higher QOQ. The UST 2Y however

maintained at 0.12% whilst the much-watched UST 10Y spiked the most by 23bps at

0.91% as at end-4Q2020. The curve has steepened to its widest levels in four years.

- Expect the Republican-led govt to exert their influence and this could potentially lead to

Chart 1 upward pressure on both interest rates and inflation; as well as higher taxes to pay for

additional fiscal stimulus.

- With the recent additional $900b fiscal bill, expect no change in the monetary policy

side as the Fed Dot Plot projection show rates staying pat throughout 2021 and

extends up to 2023. The Fed may embark on yield-curve control and enhancing its

forward guidance. Potential tapering of the Fed’s bond-buying may ensue.

- Expect 10Y UST to range between 0.95-1.15% for 1Q2021 but we are generally

underweight nominal UST’s but akin to favor inflation-linked bonds .

Corporates

– On average about one third of IG Corporates which have an OAS spread of 100bps

have negative outlook or review from S&P; including 35% of all BBB’s; whilst Moody’s

is more sanguine at 20%. Issuances are expected to drop by 25% to $300b in 1Q2021

Chart 2 (2021: $1.3 trillion).

- Average HY issuances are expected at ~$70b for 1Q2021; the lowest among all

quarters; compared to the average of $108b per quarter last year (2020 total ~ $432b).

- We are still mildly positive on IG issuances that include energy and essential

services such as water, sewerage and power that are expected to maintain credit

standing.

Source: Bloomberg, HLBB Global Markets Research 16Malaysia Fixed Income – Re-rating and supply concerns may weigh on

bond yields

Government Bonds

- MYR government bonds saw the opposite of UST performance with the

curve bull-steepening QOQ; pivoted along the 10Y. Overall benchmark

yields ended between -15 to +3bps with the longer-ends slightly

pressured.

- Expect some upward pressure on yields based on our projected front-end

Include the govvies IYC curve just like you did for UST loading of supplies whilst taking cognizance of EPF’s restrained appetite for

1H2021.

- Following Fitch’s earlier downgrade, expect some nervousness ahead of

further potential rating announcements. FTSE Russell’s potential re-

classification of Malaysia bond weightage in the WGBI end-March is another

pivotal event.

- Our 10Y MGS yield target is 2.65-85% levels.

Corporate Bonds/Sukuk

- The consistent supply of GG-bonds due to the roll-out of mega

infrastructure projects should be monitored for signs of widening

yield-risk. However, decent demand metrics by the relatively wide base on

the buy-side should augur well on yield-carry requirements.

Chart 2 - We favour conglomerates, toll, utilities and also energy-related issuers

in the AAA (credit spreads ~43-70bps) and AA-space (credit spreads for

AA2 ~75-100bps) as economic recovery takes shape in 1Q2021.

- For yield-carry requirements, unrated bonds are an option. However many of

these issuances are from the property sector that may be highly leveraged.

Source: Bloomberg, BNM, HLBB Global Markets Research

17Malaysia Fixed Income – 2021 Auction Calendar

MGS/GII issuance pipeline in 2021

No Stock Tenure Tender Quarter Projecte Private

(yrs) Month d Placeme - Government bond tenders in 2020 ended the year on a weaker

Issuance nt X

Size average BTC ratio of 2.22x as opposed to the 2.54x in 2019.

(RM mil)

1 7-yr reopening of MGS (Mat on 06/28) 7 Jan Q1 3,500

2 15.5-yr new Issuance of GII (Mat on 7/36) 15 Jan Q1 3,000 1,500

3 10-yr Reopening of MGS (Mat on 04/31) 10 Jan Q1 4,000

- Total maturities in 2021 continue to be sizeable at ~RM73.7b.

4 5-yr Reopening of GII (Mat on 03/26) 5 Feb Q1 4,500 Gross MGS/GII supply is expected to rise to circa RM152.5b (net

5 20-yr Reopening of MGS (Mat on 05/40) 20 Feb Q1 2,000 2,500

6 7-yr Reopening of GII (Mat on 09/27) 7 Feb Q1 3,500 of projected RM6.0b SPK bond switch). On a net MGS/GII supply

7 30-yr Reopening of MGS (Mat on 06/50) 30 Mar Q1 2,000 2,000

8 10-yr Reopening of GII (Mat on 10/30) 10 Mar Q1 4,000 perspective, the estimated net supply of circa RM72.8b is more

9 5-yr Reopening of MGS (Mat on 09/25) 5 Mar Q1 4,500

10 20.5-yr New Issue of GII (Mat on 09/41) 20 Mar Q1 2,000 2,500

than 2020 and remains elevated compared to previous years.

11 7-yr Reopening of MGS (Mat on 06/28) 7 Apr Q2 4,000

12 15-yr Reopening of GII (Mat on 7/36) 15 Apr Q2 3,000 1,000

13 3-yr Reopening of MGS (Mat on 06/24) 3 Apr Q2 4,000 - Issuance supply for 2021 is slightly skewed towards the shorter

14 30-yr Reopening of GII (Mat on 11/49) 30 May Q2 2,000 2,000

15 15-yr Reopening of MGS (Mat on 05/35) 15 May Q2 3,000 1,500 tenures i.e. belly and also some long tenures i.e. 20Y with main

16 5-yr Reopening of GII (Mat on 03/26) 5 May Q2 4,000

17 10-yr Reopening of MGS (Mat on 04/31) 10 Jun Q2 3,500 1,000

targeted tenures still being within 3-15Y space.

18 3-yr Reopening of GII (Mat on 10/24) 3 Jun Q2 4,500

19 20-yr Reopening MGS (Mat on 05/40) 20 Jun Q2 2,000 2,000

20 15-yr Reopening of GII (Mat on 07/36) 15 Jul Q3 3,000 1,500 - Federal Government’s funding requirements are projected to be

21 5-yr Reopening of MGS (Mat on 11/26) 5 Jul Q3 4,000

22 10-yr Reopening of GII (Mat on 10/30) 10 Jul Q3 2,500 1,500 primarily funded onshore via issuances of MGS/GII save for the

23 30-yr Reopening of MGS (Mat on 06/50) 30 Aug Q3 2,000 2,500 scheduled USD800m foreign currency-denominated debt maturity

24 7-yr Reopening of GII (Mat on 08/28) 7 Aug Q3 4,500

25 3-yr Reopening of MGS (Mat on 06/24) 3 Aug Q3 4,000 by the Government of Malaysia (GOM) in July which is expected to

26 20-yr Reopening of GII (Mat on 09/41) 20 Sep Q3 3,000 1,500

27 10-yr Reopening of MGS (Mat on 04/31) 10 Sep Q3 3,500 1,000 be rolled over.

28 5-yr Reopening of GII (Mat on 03/26) 5 Sep Q3 4,000

29 7-yr Reopening of MGS (Mat on 06/28) 7 Oct Q4 4,000

30 30-yr Reopening of GII (Mat on 11/49) 30 Oct Q4 2,000 2,000 - Continued presence of foreign institutional investor appetite in view

31 5-yr Reopening of MGS (Mat on 11/26) 5 Oct Q4 4,000

32 10-yr Reopening of GII (Mat on 10/30) 10 Oct Q4 2,000 2,000 of the deluge of negative-yielding global debt and also relatively

33 15-yr Reopening of MGS (Mat on 05/35) 15 Nov Q4 3,000 1,500

34 3-yr Reopening of GII (Mat on 10/24) 3 Nov Q4 4,000 liquid and diversified local institutional base may help provide

35 20-yr Reopening of MGS (Mat on 05/40) 20 Nov Q4 2,000 2,000

36 7-yr Reopening of GII (Mat on 08/28) 7 Dec Q4 3,500

support; barring shocks from further sovereign rating changes and

37 3-yr Reopening of MGS (Mat on 06/24) 3 Dec Q4 3,000 FTSE Russell WGBI weightage changes.

Gross MGS/GII supply in 2021 152,500

Source: BNM, HLBB Global Markets Research 18Singapore Fixed Income – corporate supply-maturity mismatch may see

retail demand spike

SGS

% Benchmark SGS Yields SGS 2Y

3.50 – The SGS curve flattened overall as benchmark yields were pressured on

SGS 5Y

3.00 SGS 10Y the front-ends; closing mixed between -3 to +3bps QOQ. SGS bonds

SGS 20Y returned 8% for 2020; a feat unlikely to be repeated this year as MAS may

2.50

not continuously embark on using exchange rate as the main policy tool.

2.00 - The ultra-long debt may continue to outperform some of its peers as the

1.50 government taps on its large pool of fiscal reserves rather than borrowings to

1.00 finance various stimulus packages to combat the economic impact of the

0.50

virus pandemic.

- Generally we are neutral for 1Q2021 as gains may be capped despite the

0.00

flush global liquidity and limited supply relative to other markets.

06/16

03/20

12/15

03/16

09/16

12/16

03/17

06/17

09/17

12/17

03/18

06/18

09/18

12/18

03/19

06/19

09/19

12/19

06/20

09/20

12/20

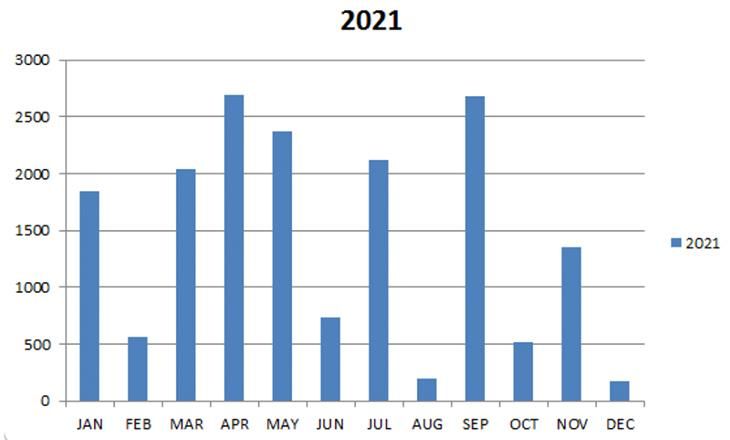

Corporate

Corporate Bond maturities – With a relatively high savings rate, individual demand for corporate bonds

are likely to be sustained for yield-carry purposes; offsetting banks

proprietary appetite as loan books are expected to be on an uptrend on

expectations of an economic recovery as removal of movement restriction

and vaccine rollouts take place.

Chart 2 - Nevertheless, expect supply in 2021 to be outstripped by demand amid

bond maturities of SGD17.0b in 2021 (1Q2021: SGD4.5b); thus creating

demand mainly from retailers. The chart on the left reveals corporate bond

maturities in SGD for 2021.

- We like medium-duration in sectors that encompass financials,

conglomerates and state-owned entities.

Source: Bloomberg, HLBB Global Markets Research 19DISCLAIMER

This report is f or inf ormation purpos es onl y and does not take int o account t he i nvest ment obj ecti ves, financial situation or particul ar needs of any particul ar

recipient. The information c ont ained her ein does not constitut e the pr ovision of inves tment advice and is not intended as an of fer or solicitati on wit h res pec t t o t he

purchase or sale of any of the financial instruments mentioned in this report and will not form the basis or a part of any contract or commitment whatsoever.

The information c ont ained in this publication is deri ved from dat a obt ained fr om sources believed by Hong Leong Bank Ber had (“HLBB”) to be reliable and in good

faith, but no warranti es or guarantees, representations are made by HLBB wit h regard to the accurac y, compl eteness or s ui tabilit y of the dat a. Any opi nions

expressed r eflect the c urrent judgment of t he authors of t he report and do not necess arily represent the opinion of H LBB or a ny of t he c ompanies wit hin the Hong

Leong Bank Group (“HLB Group”). The opini ons reflected herei n may c hange wit hout notice and the opinions do not necess arily corres pond t o the opinions of

HLBB. HLBB does not have an obligation to amend, modif y or update t his report or to ot her wise notif y a reader or recipient th ereof in the event that any matt er

stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or subsequently becomes inaccurate.

HLB Gr oup, t heir directors, employees and represent ati ves do not have any res ponsibilit y or liabilit y to any person or reci pi ent ( whether by reason of negligence,

negligent misstat ement or ot herwis e) arising from any s tat ement, opini on or inf ormation, express ed or implied, arising out of , contai ned in or derived from or

omission from t he reports or matter. H LBB may, t o the extent per mitt ed by law, buy, sell or hold significantl y long or short positi ons; act as inves tment and/ or

commercial bankers; be repres ented on t he board of the issuers; and/or engage i n ‘mar ket making’ of sec urities mentioned here in. The past perf ormance of

financi al instruments is not indicati ve of future results. Whilst every ef fort is made t o ensure that s tat ements of f acts made in t his report are accurat e, all esti mates,

projections, f orecas ts, expressions of opini on and other s ubj ecti ve j udgments contained in t his report ar e based on assumpti ons c onsi dered to be reasonabl e as of

the dat e of t he doc ument in which t hey are c ont ained and must not be construed as a repres entation t hat the mat ters ref erred to t herei n will occur. Any projec tions

or forec asts mentioned in this report may not be achi eved due to multiple ris k f actors i ncludi ng wit hout limit ation mar ket volatility, sect or vol atility, corporat e ac tions ,

the unavailabilit y of complete and accurate inf ormation. No ass uranc e can be given that any opinion des cribed herei n woul d yi eld f avorable inves tment results.

Recipients who are not mar ket professional or ins titutional inves tor c ustomer of HLBB s hould s eek the advic e of their i ndepen dent financi al advisor prior to t aking

any investment decision based on the recommendations in this report.

HLBB may provide hyperlinks to websit es of entities mentioned i n t his report, however the incl usion of a link does not i mpl y that HLBB endors es, rec ommends or

approves any mat erial on the linked page or acc essible from it. Such linked websites ar e access ed entirely at your own risk. HLBB does not acc ept res ponsi bility

whatsoever for any such material, nor for consequences of its use.

This report is not direct ed t o, or intended for distribution t o or use by, any person or entit y who is a citizen or resident of or loc ated in any st ate, c ountr y or other

jurisdiction where s uch distribution, publication, availabilit y or us e would be contrary t o law or regulation. This report is for t he us e of t he address ees onl y and may

not be redistributed, reproduc ed or passed on t o any ot her pers on or published, in part or in whole, for any purpose, wit hout the pr ior, writt en consent of HLBB.

The manner of distributing this report may be restrict ed by law or regulati on in cert ain c ountries. Persons int o whose poss ession this report may c ome ar e required

to inform themselves about and to observe such restrictions. By accepting this report, a recipient hereof agrees to be bound by the foregoing limitations.

20You can also read