QUARTERLY PROPERTY MARKET & ECONOMIC UPDATE - NEW ZEALAND QUARTER 1, 2019 - CORELOGIC

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Quarterly Property Market & Economic Update New Zealand Quarter 1, 2019

Contents

About CoreLogic 3

CoreLogic Data and Analytics .................................................................................................................................................................... 3

Legal Disclaimer ............................................................................................................................................................................................... 3

Executive Summary ........................................................................................................................................................................................ 4

Macro Economic and Demographic Indicators 5

New Zealand Asset Classes ......................................................................................................................................................................... 6

NZ and Australia GDP Growth .................................................................................................................................................................... 7

New Zealand Population ............................................................................................................................................................................... 8

Migration ............................................................................................................................................................................................................. 9

Regional Building Consents ......................................................................................................................................................................... 10

Consumer Confidence ................................................................................................................................................................................... 10

Employment ....................................................................................................................................................................................................... 11

Interest Rates .................................................................................................................................................................................................... 12

Housing Overview 13

Lending Conditions ......................................................................................................................................................................................... 14

Sales Volumes ................................................................................................................................................................................................... 15

Listings ................................................................................................................................................................................................................. 16

Nationwide Values ........................................................................................................................................................................................... 18

House Price Index ............................................................................................................................................................................................ 19

Rent ....................................................................................................................................................................................................................... 22

Buyer Classification ......................................................................................................................................................................................... 23

Main Cities Housing Market Indicators 24

Auckland Market Activity ............................................................................................................................................................................. 26

Auckland Values ............................................................................................................................................................................................... 27

Auckland Suburb Value Change ................................................................................................................................................................ 28

Current Auckland Suburb Values .............................................................................................................................................................. 30

Hamilton Market Activity .............................................................................................................................................................................. 32

Hamilton Values ................................................................................................................................................................................................ 33

Tauranga Market Activity .............................................................................................................................................................................. 34

Tauranga Values ............................................................................................................................................................................................... 35

Wellington Market Activity ........................................................................................................................................................................... 36

Wellington Values ............................................................................................................................................................................................ 37

Christchurch Market Activity ....................................................................................................................................................................... 38

Christchurch Values ........................................................................................................................................................................................ 39

Dunedin Market Activity ................................................................................................................................................................................ 40

Dunedin Values ................................................................................................................................................................................................. 41

2 | CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.

About CoreLogic

CoreLogic is a leading property information, analytics and services provider in the United States, Australia and

New Zealand. CoreLogic helps clients identify and manage growth opportunities, improve performance and

mitigate risk, by providing clients with innovative, technology-based services and access to rich data

and analytics.

Whilst all reasonable effort is made to ensure the information in this publication is current, CoreLogic does

not warrant the accuracy, currency or completeness of the data and commentary contained in this publication

and to the full extent not prohibited by law excludes all loss or damage arising in connection with the data and

commentary contained in this publication.

Contact

Call us 0800 355 355

Wellington office

Level 2, 275 Cuba Street

PO Box 4072

Wellington 6140

Auckland office

Level 5

41 Shortland Street

Auckland 1010

Email: reports@corelogic.co.nz

www.corelogic.co.nz

CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 3

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.

Executive Summary The first three months of 2019 delivered pretty much the same property market performance as for most of 2018 - sluggish sales activity and consistent (yet controlled) value growth – with the notable exception of Auckland. It wouldn’t be any surprise to see more of the same for the rest of 2019. First, the macroeconomic environment remains supportive. Yes, GDP growth has slowed and will probably ease down a bit further. But at 2-2.5% both this year and next, growth will still be respectable (and probably higher than Australia’s figures of perhaps 1.5-2%). The labour market is another strong foundation for property sales and prices in NZ, with unemployment low. Limited wage growth isn’t however doing much to help improve housing affordability. Second, the lending environment is favourable for borrowers – provided of course that they can meet the deposit, income/expense, and debt serviceability tests. For a start, the next move in the OCR now looks likely to be a short term cut (in May or August) rather than a longer-term rise. That will at least help to keep mortgage rates low, even if they don’t fall much further. The intense competition in the banking sector to either win new borrowers or capture market share at refinancing time from other lenders is also leading to some really attractive deals for borrowers, e.g. sub 4% two year and three year fixed rates. The recent rise in lending volumes (by value) has been driven largely by first home buyers (FHBs), with greater than 80% LVRs drawing down larger average loans (rather than more loans). The sector is however still operating well below the mandated speed limit, which determines that no more than 20% of owner occupier loans can be at >80% LVR. It therefore seems unlikely that the Reserve Bank will be especially concerned just yet. In fact, there would still seem to be some impetus for overall lending volumes yet to come from the higher LVR segment. Within the relatively quiet overall market nationally, it’s FHBs and mortgaged investors that are of most interest according to our Buyer Classification series. Their shares of purchases were 24% apiece in Q1 - putting FHBs well above normal levels, and investors making a return to form, even if still below past levels. Anecdotally, some investors are reported to be exiting the sector and selling to FHBs. But there’ll also be other investors simply snapping up sales to boost their own portfolios, so it’s hard to envisage that the stock of available rental property is about to change much anytime soon. Looking specifically at Auckland, it’s not hard to see why values have dipped by 1.5% over the past year and why further modest falls could occur. Affordability is still low (FHBs are still managing to buy using their KiwiSaver funds and/or compromising on location/property type), listings are high and buyers aren’t in any rush. A key theme to watch relates to policy intervention in the housing market from both the Government and Reserve Bank. The prospect of a broad-based capital gains tax in 2021 has been ruled out, but the effects of last October’s Foreign Buyer Ban seem to be playing out in softer sales activity, while the tax ring-fence for rental property losses is currently going through the parliamentary process. Although not yet law, when it does pass, it will apply to the current tax year (starting from April 1st) – so investors will need to be factoring this into their sums right now. Then out on the horizon we have the potential requirement for banks to hold more capital on their balance sheets, and hence have less money to lend out. We also need to keep an eye on KiwiBuild and how that might impact supply. Overall, although the NZ property market is on a relatively solid footing, sales volumes are likely to remain subdued in 2019. National average prices may edge up by about 3% from their current level of $686,523. Auckland however looks set for further weakness. As always, we keep a running monitor on the property market every week via our NZ Property Market Pulse articles, so be sure to check these out on our website http://www.corelogic.co.nz/news-research/all-news/ 4 | CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 © Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.

Macro Economic and

Demographic Indicators

CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 5

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.

New Zealand Asset Classes

RESIDENTIAL REAL ESTATE

$1.1 trillion

$264 Billion in home loans

COMMERCIAL/INDUSTRIAL REAL ESTATE

$212 billion

NZ LISTED STOCKS

$146 billion

NZ SUPER & KIWISAVER

$94 billion

The value of residential property remains above one trillion dollars, with mortgages secured against 24% of

this value. In other words, 76% of the value of the property market is household equity.

The commercial & industrial property sector ($212bn) is much smaller than residential, as is the value of the

share market and the country’s superannuation savings.

Sources: CoreLogic NZ, Reserve Bank of NZ, NZX, NZ Super Fund, Financial Markets Authority

6 | CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.

NZ and Australia GDP growth

Annual Average GDP Growth (%)

8

NZ

7

Australia

6

5

4

3

2

1

0

-1

-2

Capital Economics forecast

-3

1990 1994 1998 2002 2006 2010 2014 2018

New Zealand’s economy expanded by 0.6% in the final quarter of 2018, double the figure in Q3 (0.3%). This result was driven

by the services sector - which includes retail, business services, and tourism. By contrast, goods-producing activities lagged

a little behind in the fourth quarter.

During the 2018 calendar year, the economy expanded by 2.8%: slower than 3.1% in 2017 but hardly a disaster. That said,

growth is anticipated to cool again in 2019 (perhaps to about 2%), as migration eases and the construction impetus from

previous events such as the Christchurch and Kaikoura earthquakes fades further. However, NZ may remain slightly ahead

of Australia in both 2019 and 2020 in terms of GDP growth.

Source: Reserve Bank of New Zealand, Capital Economics

CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 7

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.

New Zealand Population

Quarterly Change in National Population (persons per quarter)

35,000

Population growth slowed again in the fourth

Quarterly population change quarter of 2018, from about 1.9% annually to

30 ,000 4 quarter moving average 1.7%. This was the slowest growth rate in four

years, and acts as a natural handbrake on the

25,000 housing market.

20,000 Once again it was net migration that pulled

the overall growth rate down. In 2017, net

15,000

migration added 70,000 people to our

population, whereas that figure dropped

to less than 56,000 in 2018.

10,000

At 26,000, natural population growth (births

5,000 minus deaths) in 2018 was barely changed from

2017, and still in the 25,000-30,000 range that

0 it’s been in for several years now.

1991 1994 1997 2000 2003 20 06 20 09 2012 2015 2018

Population Change Composition (persons per quarter)

25,000

Natural increase

20,000

Net migration

15,000

10,000

5,000

0

-5 ,0 00

-10,000

1996 1999 2002 2005 2008 2011 2014 2017

Annual Change in Population (persons)

New Zealand 91600

Auckland 38700

Hamilton City 3900

Tauranga City 3500

Wellington Cit y 3600

Christchurch City 7000

Dunedin City 1900

Source: Statistics New Zealand

8 | CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.

Migration

Long term migration (12-month rolling totals)

180,000

Net

Unfortunately the net migration statistics are

160,000 Arrivals

not as useful at present as they have been

Departures

140,000 in the past, due to a change in the collection

methodology and the tendency for big revisions

120,000

to be made each month. Previously, migration

100,000 was estimated on an ‘intentions method’ (what

people said they planned to do). It’s now

80,000

calculated on an ‘outcomes method’ (what

60 ,0 00 people actually did). Because actual outcomes

are not known for at least a year after a migrant

40 ,0 00 arrives or departs, recent patterns must be

20 ,0 00 statistically estimated/modelled, and that

gives rise to uncertainty and revisions.

0

-2 0, 00 0 The trans-Tasman balance is also no longer

available, because of a conscious choice by

-4 0, 00 0 Statistics NZ to no longer track migration

20 02 20 06 2010 2014 2018 by residency (although they still track it by

citizenship). District-level migration flows will

Comparison of old and new net migration series still be available on the new method, but just

(12-month rolling totals) not yet.

80,000 The bottom line is that the net migration figures

need to be treated with caution at present.

70,000 However, taking them at face value (with the

60,000 caveats firmly still in mind), NZ has had a net

migration inflow of almost 61,600 people over

50,000

the past 12 months, an increase of about 10,000

40,000 from a year ago – driven by more arrivals and

flat departures. This rise in net migration would

30,000

have resulted in higher property demand and

20,000 prices than otherwise would have been the case.

10,000

0

-10,000

- 20,000

- 30,000

2002 2006 2010 2014 2018

Net Gain Last Year % Change

TOTAL ALL AREAS 62,733 -11.6%

Auckland Region 31,417 -13.7%

Hamilton City 1,887 -2.0%

Tauranga City 735 -24.1%

Wellington 2,917 -16.7%

Christchurch City 4,722 -13.5%

Dunedin City 899 -15.2%

Main Urban Area (Other) 4,719 -14.3%

Rural Centres 3,713 -23.0%

Not applicable/Not stated 11,724 3.4%

Source: Statistics New Zealand

*Note that these figures relate to Q3 2018. The next publication date for these figures from Statistics NZ is yet to be advised.

CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 9

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.

Regional Building Consents

New dwelling consents trend (consents per month) The boom in residential building consents

has continued over the past three months,

with Statistics NZ’s trend measure (which

1,200 smooths out seasonal and other fluctuations)

showing that in the year to February 2019 more

than 34,100 new dwellings were approved to

1,000 be built. That was 8.8% higher than a year ago,

itself already a high figure (31,375). This is the

first time that consents have broken above

800 34,000 annually on this measure.

Auckland remains the key growth area,

600 although the Waikato and Wellington regions

have also been contributing. By property type,

it’s been smaller dwellings (e.g. apartments,

400 flats) driving the growth, particularly in

Auckland. Indeed, more than half of the recent

consents in Auckland have been small dwellings,

200 with these properties in our biggest city now

making up more than 20% of all consents across

New Zealand. This is a good thing from the

0 point of view of housing a growing population.

1995 1999 2003 2007 2011 2015 2019

It’s important to note however that as many

Source: Statistics New Zealand as half of the recent consents in Auckland have

simply been replacing demolished properties,

so we’re cautious of the emerging view that

the city’s shortfall is starting to be eroded

more significantly. Very few of the new-builds

in Auckland are going into lower value segments

either, so there’s still a clear case for some kind

of intervention (e.g. KiwiBuild).

Consumer Confidence

ANZ-Roy Morgan Consumer Confidence (index, monthly)

160 After a lull in the middle of last year, consumer

confidence on the ANZ-Roy Morgan measure

140 has edged higher over the past few months,

reaching 121.8 in March. That’s a couple of points

120 above the long-term average, albeit below

where confidence was a year ago (128.0

this time last year).

100

It can sometimes be a little tricky to

80 disentangle all of the various influences

on consumer confidence, but given that

60 unemployment is still low and mortgage rates

are very favourable it’s not too hard to explain

slightly above-average levels of sentiment at

40 present. At the margin, this should support

activity in the housing market.

20

0

2004 2007 2010 2013 2016 2019

Source: ANZ NZ, Roy Morgan

10 | CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Employment

Annual change in employment, The slowdown in employment growth continued

in the fourth quarter of 2018, with the year-on-

full time and part time

year figure falling from 2.9% in Q3 to just 2.4%.

10% That was the slowest rate since the first quarter

of 2016. Full-time employment growth slowed

8% from 3.6% year-on-year to 3.1%, while part-time

employment actually fell by 0.4% in the year to

6% Q4 2018. A drop in that figure hadn’t occurred

since Q3 2013.

4%

That said, we need to bear in mind that

2% employment growth has been strong for

an extended period and as the number of

0% people employed rises (and fewer people are

unemployed), it’s simply not possible to keep

-2 %

employment growing at the same rates as

before. Indeed, the labour force participation

-4 %

rate - the share of the working age population

-6 %

that are either employed or looking for work -

continues to hover at about 71%, a record high.

-8 % The unemployment rate remains below 4.5%,

1987 1990 1994 1998 2001 20 05 20 09 2012 2016 on a par with previous record lows.

In other words, the labour market is still robust

Labour force participation rate (%) and actually, there are shortages of labour in

72 certain industries (such as construction). This

provides a solid base for the property market,

both in terms of sales volumes and property

70 values. With most people in work, the risks

of repayment problems and mortgagee

68 sales are low.

66

64

62

60

58

1986 1989 1993 1997 2000 20 04 20 08 2011 2015

Unemployment Rate

12

10

8

6

4

2

0

1986 1989 1993 1997 2000 2004 20 08 2011 2015 Source: Statistics New Zealand

CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 11

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Interest Rates

Mortgage Interest Rates (%) The latest OCR review from the Reserve Bank

surprised most analysts by flagging that a near

25

term rate cut (rather than a longer term rate

Floating mortgage interest rates rise) is more likely to be the next move.

2 year fixed rate

The timing of that potential cut remains

20

uncertain, but could be as soon as May,

or failing that, August.

The Reserve Bank’s OCR projections shown in

15

the charts here pre-date that announcement,

but even though they don’t contain a rate cut

in the future path shown, the key message is the

10

same: official interest rates will be low for some

time to come, and this bodes well for borrowers.

It’s an even more favourable environment for

5

borrowers when you also consider the intense

competition between banks at present (witness

the re-emergence of mortgage rate wars).

0

In turn, this will underpin a decent level of

1965 1971 1977 1983 1989 1995 2001 2007 2013 2019

property sales and support house prices.

Official Cash Rate and Mortgage Rates (%) However, there are some upside risks to

12 mortgage rates over a 3-5 year horizon. Most

importantly, the Reserve Bank is likely to impose

10

extra capital requirements on banks and it’s

been estimated that this need to for them

to hold more money on their balance sheets

8 could force up mortgage rates by about one

percentage point.

6

Of course, many recent borrowers will be well

prepared for that anyway, given that they’ve

4 already had to pass tougher serviceability

tests to get their loan in the first place (such as

satisfying the bank that they could still service

2 the mortgage at a theoretical interest rate of

7-8% not just the current 4-5%).

0

20 00 20 03 20 06 20 09 2012 2015 2018 2021

Average Two Year Fixed Rates (%)

5.20 %

5.10 %

5.00 %

4.90 %

4.80 %

4.70 %

4.60 %

4.50 %

Sources: Reserve Bank of New Zealand and interest.co.nz

12 | CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Housing Overview

CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 13

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Lending conditions

Annual Change in Gross New Lending Flows Gross new lending has continued to rise

over the past three months, with February’s

($m per month)

mortgage lending figure ($4.8bn) up by about

$130m from a year earlier. That extended the

1,500

run of increases to 11 months (and the 13th in

1,000

the past 14 months), with larger average loans

rather than a rise in the number of loans being

50 0 the key driver.

0 By borrower type, the overall increases in

mortgage lending continue to be driven by

-500

owner-occupiers, with investors still showing

-1 ,000

broadly flat volumes year-on-year. In February,

for example, the flow of lending to owner-

Investor occupiers was $3.9bn, about $280m higher than

-1,500

Owner-occupier a year ago. By loan type, the share of lending on

-2 ,0 00 interest-only terms remains far lower (28%) than

it was at the peak in May 2016 (41%).

-2 ,500

2016 2017 2018 2019

Much of the growth in lending lately has been

High LVR Lending to Owners and Investors driven by first home buyers (FHBs) with less

than a 20% deposit. However, we doubt that

(% of new lending) the Reserve Bank will be overly concerned

about this just yet. First, given the banks’

25%

current strict lending criteria (e.g. income and

expense testing, debt servicing ability), those

20 %

FHBs getting loans will tend to only be the

‘best’ borrowers anyway – and they’re more

likely to keep servicing the debt in the (unlikely)

15% event of a major economic/property downturn.

Second, the LVR speed limits remain some way

10% off in the distance. The current speed limit for

high LVR owner-occupier borrowing is 20% –

but the actual figure for February was down at

5% just 12%. (Note that the figures for investors at

the new speed limit, i.e. a 5% cap for borrowers

with less than a 30% deposit, or 70% LVR, are

0% not available until July. The lending flows at the

Oc t 16 Feb 17 Jun 17 Oct 17 Feb 18 Jun 18 Oct 18 old 65% LVR mark have been discontinued.)

Refinancing Profile for Mortgages (% of stock) Looking ahead, the rise in mortgage lending

looks set to roll on, giving support to sales

volumes and property values. Competition

40 %

amongst the banks will stay pretty intense

35 % and this will lead to more attractive deals for

borrowers. With more than 80% of mortgage

30 % debt in NZ on a fixed interest rate, household

finances also look relatively resilient.

25%

20 %

15%

10%

5%

0%

Source: Reserve Bank of New Zealand

14 | CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Sales Volumes

Nationwide Sales Volumes (monthly total) There were 7,973 property sales across NZ

in March, down by 12% from a year earlier and

the lowest number for the month of March since

2011. Auckland was even weaker, with sales

down by 16% from a year ago. In other words,

it’s still a pretty soft property market in terms

of volumes, both nationally and in Auckland.

However, to an extent there are different reasons

for this. Around most of NZ, the stock of listings

available on the market is relatively low, so sales

activity is being restrained more by a lack of

choice for buyers rather than an absence of

demand. In that environment, it’s not surprising

that values are rising.

In Auckland, however, listings are high,

so the lack of sales can be attributed to

soft demand. Indeed, the choice available to

buyers in Auckland means that they don’t need

to rush – and equally, with unemployment and

interest rates low, vendors generally aren’t

Nationwide Annual Change in Sales Volumes (%) desperate either. So days to sell is rising and

sales themselves have dropped. For vendors

that do need to sell, prices are dipping a little.

The Foreign Buyer Ban is probably also

playing a role in reducing turnover, but at the

same time this will also have at least opened

up some opportunities for would-be domestic

buyers to return to the market.

Regional Sales Volumes (year-on-year % change)

CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 15

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Listings

New listings (three-week rolling total)

As per normal, new listings rose in January

and February as the market resumed after the

holiday period. However, they’ve peaked for this

season now and will tail off further as winter

sets in. Compared to a year ago, the still-tight

markets in Wellington and Otago have at least

started to see more of a response from would-

be vendors, with new listings rising in response

to the growth in prices.

New Listings Average last 3 weeks 1 month change 1 year change

New Zealand 2,295 -7% 8%

Auckland 671 -11% -8%

Waikato 237 -15% 5%

Bay of Plenty 171 -14% 4%

Wellington 216 0% 27%

Canterbury 331 -12% 10%

Otago 127 -6% 48%

16 | CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Listings

Total listings

Total listings across NZ as a whole are 7% higher

than they were a year ago, driven by Otago,

Auckland, and to a lesser extent Waikato and

Wellington. In Auckland, listings were already

high, so this is just an added headwind for

values (which have already drifted a little

lower in the past few months).

But in Otago and Wellington, listings were

starting from a low base, and so the recent rises

probably won’t be enough to take the steam

out of property value growth just yet. The stock

of property on the market (i.e. listings) is pretty

much unchanged from a year ago in Canterbury.

New Listings Average last 3 weeks 1 month change 1 year change

New Zealand 32,372 2% 7%

Auckland 11,121 2% 14%

Waikato 3,551 5% 9%

Bay of Plenty 2,290 3% 6%

Wellington 1,697 6% 8%

Canterbury 4,965 -2% 1%

Otago 1,327 3% 18%

CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 17

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Nationwide Values

Average Value of Housing Stock - New Zealand ($) National average property values increased

by 2.6% in the year to March 2019, a slowdown

from the figure of 3.0% recorded in February.

That dip in growth may have been small, but

it took the figure down to its slowest pace

since December 2011 (2.3%), when the market

was finally accelerating and permanently

emerging from the GFC-induced lull.

Of course, although they’ve slowed, values are

still growing – boosted by a rising population

(albeit also slowing), the undersupply of

properties, and low unemployment and

mortgage rates. Indeed, at more than $686,500

in March, the average property in NZ hasn’t

become any more affordable in recent months.

A year ago, the average property was about

$17,400 cheaper (at around $669,100).

Annual and Quarterly Change in Value (%)

18 | CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.House Price Index

Average Dwelling Value ($) Dunedin is still easily the strongest of the

main centres in terms of property value growth,

with an increase of 13.3% in the year to March.

Wellington is also rising steadily, with average

values up by 8.4% over the past 12 months.

Robust demand and a tight supply of listings

on the market are boosting values in both

places. Meanwhile, Tauranga and Hamilton

are still seeing rising prices, just slower than

Wellington and Dunedin.

By contrast, Christchurch remains a flat

market, with value growth hovering around

zero (0.6%y/y in March), as it has done for about

two years now. In Auckland, property values

have weakened over the past few months, and

were down by 1.5% in the year to March – that’s

the biggest annual fall for a decade, with values

being held back by low affordability, lots of

listings and no rush from buyers.

March 2019

Current Value 3 months 12 months Since 2007 peak

New Zealand $686,523 0.5% 2.6% 66%

Auckland $1,039,917 -0.8% -1.5% 91%

Hamilton $580,285 1.6% 4.5% 61%

Tauranga $733,102 1.7% 3.7% 52%

Wellington $702,896 2.2% 8.4% 54%

Christchurch $497,298 0.1% 0.6% 31%

Dunedin $451,199 3.7% 13.3% 58%

Source: CoreLogic NZ QV Monthly House Price Index

CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 19

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.House Price Index Annual Value Change (%) Over the past 12 months, the sluggish markets in Canterbury and Auckland (as well as the West Coast of the South Island) can be clearly seen on a map view. By contrast, the stronger markets have tended to be in the central and eastern parts of the North Island, and to a lesser extent in Otago and Southland. *Size of bubble represents the number of properties in the Territorial Authority 20 | CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 © Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.

Three Month Value Change (%)

The emerging weakness in Auckland is the clearest feature of the timelier three

month changes in values, with several parts of the wider city/region showing blue

(modest price falls). Most other parts of the country look stronger, other than again

Canterbury and parts of the upper South Island.

*Size of bubble represents the number of properties in the Territorial Authority

CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 21

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Rent

National Annual Change in Value and Rent (%)

25% National rents averaged $433 per week in

the three months to March 2019, up by 6.0%

from $408 a year earlier. Rental growth has

20 %

ticked up a few notches in the past few months,

as landlords perhaps try to recoup the extra

15% costs imposed on them from new government

measures such as insulation requirements.

10%

However, a 6.0% annual rise in rents isn’t

completely out of sync with past norms.

5% Ultimately, any rent increases that landlords

can successfully push through tend to be

0% anchored simply by how much tenants can

afford to pay – itself determined by wage

growth. So with wage growth relatively limited

-5 % at present, we wouldn’t envisage rental growth

accelerating much further.

-10%

Several of the main centres are seeing sizeable

rises in rents at present – at least 7% annually in

-15% Wellington, Dunedin, Tauranga, and Hamilton. In

1998 20 01 20 04 20 07 2010 2013 2016 2019 Wellington and Dunedin in particular, rents will

be rising for the same reason as property prices

Gross Rental Yield – National (%) – shortages of property and robust demand.

6% From an investors’ perspective, it will be

heartening to see gross rental yields now

rising, after a long period where they’ve

5% dropped. Of course, from the troughs of 3.1%

nationally in 2017, the current average yield of

3.3% isn’t exactly a huge amount higher – but

given the slowdown of capital gains, at least it’s

4% moving in the right direction for landlords.

3%

2%

1%

0%

1998 20 01 20 04 20 07 2010 2013 2016 2019

Median Weekly Rent Annual Change in Rent Gross Yield

Auckland $526 2.7% 2.2%

Hamilton $389 7.2% 3.5%

Tauranga $466 8.0% 3.3%

Wellington $525 8.9% 3.3%

Christchurch $372 3.5% 3.9%

Dunedin $352 8.5% 4.1%

Sources: CoreLogic NZ and MBIE

22 | CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Buyer Classification

Buyer Classification – New Zealand (% of sales)

Many of the same patterns that we saw for

30% buyer classification in 2018 have remained

30% 27% in place in the first three months of 2019.

26% Movers (i.e. existing owner occupiers who are

24% relocating) remain slightly less of a presence

than normal in terms of their percentage share

21% 24% of purchases, with the key areas of interest

20% Mover being activity from first home buyers (FHBs)

First Home Buyer and multiple property owners (MPOs) with

Multiple Property Owner Mortgage

Multiple Property Owner Cash a mortgage.

New to Market

ReEntry 13% Across NZ, FHBs accounted for 24% of

Other purchases in Q1 2019, basically unchanged

10% 10% from the final two quarters of 2018. However,

putting that into a longer-term context, FHBs

6% have a larger market share than at any time

5%

since 2007 – and are certainly playing a more

4% 5%

important role than when they only made 18% of

4% 2%

purchases back in Q1 2014. Access to KiwiSaver

0% for the deposit and a willingness to compromise

2006 2008 2010 2012 2014 2016 2018 on location and/or property type (and hence

access lower value housing) are factors allowing

FHBs to continue in the market.

NZ Property Transfers by Non-Citizens or no Resident Visa

(% of total transfers) Mortgaged MPOs have arrested the slide that

they experienced in the aftermath of LVR III

3.5%

in October 2016 (which required them to have

a 40% deposit).After hitting a trough of 22%

3.0% in Q4 2017, they now account for 24% of

purchases. That’s the same as FHBs, whereas

historically mortgaged MPOs have tended

2.5% to enjoy a clear buffer over FHBs in terms of

market share. One difference now is that with

gross rental yields generally low, it’s harder for

2.0%

some would-be investors to make the sums

stack up – especially since costs are rising too

1.5% (e.g. extra insulation requirements, the tax ring-

fence for rental property losses).

1.0% As noted, movers are just ticking along. Their

share of purchases in Q1 2019 was 27%, down a

touch from 28% a year ago and not really much

0. 5%

different from historical norms. With the costs

involved to move and also many with already-

0. 0% large mortgages, staying in the current property

2016 Q4 2017 Q2 2017 Q4 2018 Q2 2018 Q4 and perhaps renovating (rather than relocating)

is a choice many people are making currently.

Source: Statistics New Zealand

CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 23

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Main Cities Housing

Market Indicators

CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 24

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 25

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Auckland Market Activity

Buyer Demand – Auckland (volume index)

Buyer demand as measured by valuations

activity is still subdued in Auckland, which isn’t

surprising given low affordability and no real

need to rush to make a purchase (because

listings/choice are high).

The fascinating aspect of buyer classification in

Auckland is that FHBs are the biggest individual

buyer group (27% of purchases), even though

the average property in the city costs more

than $1m. FHBs haven’t been this important to

Auckland’s demand since back in 2006-07, and

the latest figures surely reflect the willingness

of FHBs to move further out from the CBD or

to buy a smaller dwelling.

In terms of their share of purchases,

Auckland’s movers and mortgaged multiple

property owners (MPOs) are less active than

normal. It’s likely that many movers with

already-large debts are just preferring to

sit tight for now, while the low gross yields

(sometimes less than 2%) on offer in Auckland

Buyer Classification – Auckland (% of sales) are probably keeping a lid on the new demand

for property from investors.

There are reasonably clear signs in these figures

that the Foreign Buyer Ban is having an effect

in Auckland. The market share of ‘cash MPO’

(which will cover domestic cash investors,

30%

28% but also some overseas buyers) has reduced

27% recently, as has the ‘new to market’ category.

27% People from Australia and Singapore are exempt

27% 25%

from the ban, and foreign buyers can still invest

24% and hold apartments in large developments –

20% Mover but even so, there are signs in the latest buyer

Multiple Property Owner Mortgage classification stats that the ban has taken a

Multiple Property Owner Cash reasonable chunk of foreign buyers out of

First Home Buyer the market.

New to Market

Other

10% ReEntry 12%

7% 6%

4% 4%

0% 2%

2006 2008 2010 2012 2014 2016 2018

26 | CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Auckland Values

Average value of housing stock Auckland ($)

The falls in Auckland property values in recent

months (which, to be clear, are only modest so

far) have been relatively widespread across the

area. Only Rodney has escaped price falls on

both a three-month and twelve-month horizon,

with the weakest market over the past year

being North Shore (down by 3.1%).

The drops in the past 12 months have been

1-2% in Papakura, Waitakere, Auckland City and

Manukau, and only a minor 0.5% in Franklin.

Annual and quarterly value change Auckland (%)

March 2019

Current Value 3 months 12 months Since 2007 peak

Rodney $953,096 0.2% 0.3% 62%

North Shore $1,197,945 -1.2% -3.1% 86%

Waitakere $814,078 -1.1% -1.3% 92%

Auckland City $1,230,817 -0.2% -1.1% 98%

Manukau $892,867 -1.5% -1.1% 95%

Papakura $691,235 -1.4% -1.7% 92%

Franklin $671,797 -0.3% -0.5% 70%

CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 27

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Auckland Suburb Value Change Annual value change (%) 28 | CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 © Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.

Even in a flat to slightly falling market, there’ll always

be variation. Currently, the weakness of values is centred

around the North and East of Auckland, with parts of the

West and South faring a little better. One key reason for

this will be that property is still a bit more affordable in

the West and South, so buyer demand is slightly stronger.

*Size of bubble represents

the number of properties in the suburb.

Based on CoreLogic Median E-valuer

CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 29

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

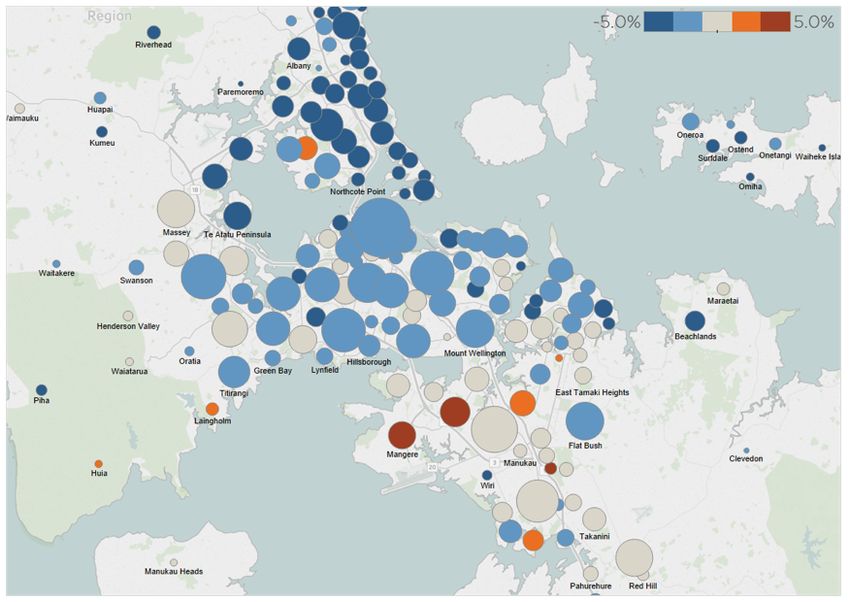

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Current Auckland Suburb Values Auckland suburb values 2018 ($) Over the past five years, almost all parts of the country have seen large rises in property values. CoreLogic’s interactive ‘Mapping the Market’ product (www.corelogic.co.nz\mapping-market) shows these changes across the country, it’s freely available and updated quarterly. The heatmaps in ‘Mapping the Market’ are point-in-time snapshots from 2014 and 2019. Auckland is illustrated in the heatmap here. There are no longer any suburbs with a median property value below $500,000 in Auckland. Five years ago, about 20% of all suburbs were below that $500k threshold. At the end of February 2014, 13.8% of suburbs had a median value of at least $1m. Now that figure has risen to 48.0%. *Based on CoreLogic Median E-valuer 30 | CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 © Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.

CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 31

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Hamilton Market Activity

Buyer Demand – Hamilton (volume index)

Similar to the story in Auckland,

mortgaged MPOs are just stepping back

a bit in Hamilton, and first home buyers

have come in and now account for a

record high share of purchases (29%) –

as well as that, they’re actually the

largest individual buyer group.

Mortgaged MPOs (investors) accounted

for 27% of Hamilton property purchases

in Q1 2019, the lowest for more than a

decade. Admittedly, at 11%, there is a little

more activity from cash MPOs in Hamilton

than typically tends to be the case.

Movers are also relatively inactive in

Hamilton (22%), so it’s become a key first

home buyer market. At 29%, FHBs’ share

of purchases in Q1 2019 was the largest of

any individual group, and well above their

previous best of 27% back in late 2006.

Buyer Classification – Hamilton (% of sales)

40%

31%

30% 29%

27%

27%

25%

22%

20% First Home Buyer

Mover

Multiple Property Owner Cash

Multiple Property Owner Mortgage

New to Market

ReEntry 11%

10% Other

7% 7%

4% 4%

0% 3% 1%

2006 2008 2010 2012 2014 2016 2018

32 | CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Hamilton Values

Average value of housing stock – Hamilton ($)

Hamilton’s average property value rose by 1.6%

in the first three months of 2019, with the rise

over the full 12-month period to March coming

in at 4.5%.

Hamilton South East has shown the largest gain

in average property values since March last year

(7.0%), also recording a figure of 2.0% in the first

three months of 2019 alone. The smallest gain

in property values over the past 12 months has

been in Hamilton North East (at 3.0%), where

average values are already the highest (at more

than $722,000).

Annual and quarterly change in value – Hamilton (%)

March 2019

Current value 3 months 12 months Since Peak

Hamilton Central & North West $535,166 1.3% 4.0% 50%

Hamilton North East $722,263 1.3% 3.0% 61%

Hamilton South East $535,462 2.0% 7.0% 53%

Hamilton South West $519,467 1.8% 4.0% 52%

CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 33

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Tauranga Market Activity

Buyer Demand – Tauranga (volume index)

In terms of the main centres of NZ, Tauranga’s

buyer classification make-up is different to the

others. First home buyers are generally less of

a presence in Tauranga, partly because house

prices are high in relation to local incomes.

By contrast, movers from both within the city

and from elsewhere – who have more wealth

and equity behind them – tend to be the key

purchasing group.

Indeed, in Q1 2019, movers accounted for 35%

of property purchases in Tauranga – that’s not

far off previous cyclical peaks. By contrast, FHBs

made just 17% of purchases, while the general

drop-off in market share for mortgaged MPOs

that’s been in progress since early 2016 hasn’t

really turned around yet either. They accounted

for 22% of purchases in Q1 2019.

Buyer Classification – Tauranga (% of sales)

First Home Buyer

Multiple Property Owner Mortgage

40% Multiple Property Owner Cash

Mover

New to Market

33% ReEntry

35%

Other

30%

22%

23%

20%

16%

17%

15%

10% 12%

6% 6%

6%

4%

3% 2%

0%

2006 2008 2010 2012 2014 2016 2018

34 | CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Tauranga Values

Average value of housing stock – Tauranga ($)

Average property values in Tauranga were up by

1.7% in the first three months of 2019, taking the

gain over the last 12 months as a whole to 3.7%.

The level in Tauranga is now $733,102, about

$26,000 higher than a year ago and $57,000

above two years ago.

Annual and quarterly change in value – Tauranga (%)

CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 35

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Wellington Market Activity

Buyer Demand – Wellington (volume index)

Overall activity levels in Wellington are perhaps

not as high as might be thought, given that the

steady growth in values that’s occurring would

normally be associated with a busy market.

However, it needs to be noted that listings are

low – so activity is likely to have been restrained

simply because of a limited supply of stock on

the market actually available to buy.

The purchases that are being made are often

going to first home buyers – in fact, they’re

accounting for as high a share (33%) as ever

before, and they’re the largest individual

buyer group.

The next largest buyer group, which is

mortgaged investors, are quite a long way

back, with a 27% market share. Although that’s

lower than normal, investors have at least made

a comeback in the past few quarters, from a

trough of 23% in Q4 2017. Rising rents and yields

in Wellington may have helped entice some

new investors into the market.

The recent comeback of mortgaged investors

Buyer Classification – Wellington (% of sales) has come at the expense of movers, who have

dropped down to just 20% of purchases. That’s

lower than ever before.

33%

30%

28% 27%

27%

27%

20% First Home Buyer

Mover 20%

Multiple Property Owner Cash

Multiple Property Owner Mortgage

New to Market

ReEntry

Other

10%

8% 9%

4% 5%

3% 4%

3% 2%

0%

2006 2008 2010 2012 2014 2016 2018

36 | CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.Wellington Values

Average value of housing stock – Wellington ($)

The growth in property values around

Wellington region remains pretty strong across

the board. The largest gains are being seen in

Upper Hutt and Masterton (both 12.3% in the

year to March), followed by Carterton (11.6%).

The other parts of the region are all seeing

values rise by about the 7-9% range, with

Porirua towards the top, and Kapiti Coast and

South Wairarapa a little further back.

Annual and quarterly change in value – Wellington (%)

March 2019

Current value 3 months 12 months Since Peak

Porirua $597,865 1.1% 8.9% 57%

Upper Hutt $542,220 2.9% 12.3% 54%

Lower Hutt $576,086 3.0% 8.2% 47%

Wellington City $828,645 1.9% 7.9% 56%

Carterton $425,136 1.8% 11.6% 53%

Kapiti Coast $586,842 1.7% 6.8% 53%

Masterton $377,865 1.2% 12.3% 32%

South Wairarapa $514,326 2.3% 6.7% 52%

CoreLogic Quarterly Property Market & Economic Update New Zealand Q1 2019 | 37

© Copyright 2019. CoreLogic and its licensors are the sole and exclusive owners of all rights, title and interest

(including intellectual property rights) the CoreLogic Data contained in this publication. All rights reserved.You can also read