REBUTTAL TESTIMONY OF MARK A. ISRAEL - April 9, 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

BEFORE THE PUBLIC UTILITIES COMMISSION

OF THE STATE OF CALIFORNIA

___________________________________________

│

In the Matter of the Joint Application │

of TracFone Wireless, Inc. (U4321C), │

América Móvil, S.A.B. de C.V. and │

Verizon Communications, Inc. for │ Application 20-11-001

Approval of Transfer of Control over │

Tracfone Wireless, Inc. │

___________________________________________|

REBUTTAL TESTIMONY OF MARK A. ISRAEL

April 9, 2021CONTENTS

I. INTRODUCTION..............................................................................................................1

A. ASSIGNMENT ............................................................................................................1

B. SUMMARY OF CONCLUSIONS .....................................................................................1

II. THE TRANSACTION WILL NOT MATERIALLY REDUCE

COMPETITION. ...............................................................................................................4

A. DR. SELWYN HAS PREVIOUSLY RECOGNIZED THE COMPETITIVE

DISADVANTAGES THAT MVNOS FACE, WHICH LIMIT THEIR ABILITY TO

COMPETE WITH MNOS..............................................................................................5

B. HHIS CANNOT PROVE HARM FROM THE TRANSACTION.............................................6

C. DR. SELWYN’S TREATMENT OF MVNOS IN HIS HHI CALCULATIONS IS

FLAWED AND CONTRADICTS HIS PRIOR TESTIMONY...................................................8

D. THE MERGER WILL NOT HARM WHOLESALE COMPETITION. ....................................11

III. THE TRANSACTION WILL RESULT IN SUBSTANTIAL

EFFICIENCIES THAT WILL BENEFIT CONSUMERS..........................................13

A. QUANTIFICATION OF EFFICIENCIES .........................................................................15

B. EFFICIENCIES FROM THE TRANSACTION WILL BE PASSED THROUGH TO THE

BENEFIT OF CONSUMERS..........................................................................................18

1. Pass-through of efficiencies and upward pricing pressure are

symmetrical. ...............................................................................................18

2. Dr. Selwyn’s claims about elasticity and pass-through are

incorrect as a matter of economics and marketplace realities. .................19

3. Empirical economic evidence demonstrates substantial pass-

through as the expected outcome...............................................................22

4. Verizon’s documents support pass-through to the benefit of

consumers. .................................................................................................24

5. The fact that TracFone has a high share among MVNOs and

flanker brands does not mean that Verizon would have no incentive

to pass through merger cost savings..........................................................35

IV. DR. SELWYN’S PROPOSED REGULATORY REMEDY WOULD NOT

REPLICATE MERGER EFFICIENCIES....................................................................36

iV. APPENDIX: ESTIMATING VERIZON’S MARGINAL NETWORK

COSTS ..............................................................................................................................37

iiI. INTRODUCTION

A. ASSIGNMENT

1. On November 5, 2020, TracFone Wireless, Inc. (TracFone), América Móvil, S.A.B. de

C.V. (América Móvil), and Verizon Communications, Inc. (Verizon), filed a joint application

seeking approval to transfer control of TracFone from América Móvil to Verizon (Transaction).

On March 12, 2021, I submitted Opening Testimony explaining the basis for my conclusions

that: (a) the Transaction will result in substantial efficiencies that will benefit consumers in the

United States overall and in California specifically; (b) the Transaction will not materially reduce

retail wireless competition in the United States or in California; and (c) the Transaction will not

materially reduce wholesale wireless competition in the United States or in California. 1 On

April 2, 2021, Dr. Lee L. Selwyn submitted testimony on behalf of the Public Advocates Office

of the California Public Utilities Commission addressing certain points in my testimony and

advancing other analysis related to the Transaction. 2

2. I have been asked by counsel for TracFone to assess and respond to certain arguments

that Dr. Selwyn makes and to determine whether the conclusions from my Opening Testimony

still stand.

B. SUMMARY OF CONCLUSIONS

3. Based on my review of materials, and my training and experience as an economist, my

main conclusion remains that there is significant wireless competition today, and the Transaction

1

Opening Testimony of Mark A. Israel, March 12, 2021 (hereinafter Israel Testimony).

2

Direct Testimony of Lee L. Selwyn, April 2, 2021 (hereinafter Selwyn Testimony).

1will make the market even more competitive and increase consumer welfare. 3 This main

conclusion is supported by the following specific conclusions:

• The Transaction will not materially reduce competition. Dr. Selwyn has previously

recognized the competitive disadvantages that MVNOs face, which limit their ability

to compete with MNOs. Dr. Selwyn’s treatment of MVNOs in his HHI calculations

is flawed and contradicts his prior testimony. In fact, the substantial differentiation

between Verizon and TracFone—distant competitors in the wireless space, each of

which competes more closely with multiple brands at other wireless carriers than with

each other—together with the weak competitive position of MVNOs means that HHIs

(particularly those that treat MVNOs as fully independent) cannot be used to predict

harm to competition in this case.

• The Transaction will result in substantial efficiencies that will benefit consumers.

TracFone currently purchases wholesale network access and the Transaction

would allow it to instead realize costs associated with “owner’s economics.” That

is, while today the incremental costs to TracFone from adding a customer with

associated usage reflect the marked-up charges from an MNO, post-merger

TracFone will internalize Verizon’s lower actual incremental cost of serving that

additional load. Because the costs associated with the latter are substantially

3

Although I do not respond to every argument that Dr. Selwyn raises, nothing in his testimony

causes me to change the conclusions that I described in my Opening Testimony.

2lower than those associated with the former, the Transaction will substantially

reduce TracFone’s marginal costs.

And as a matter of fundamental economics, this reduction in marginal costs

means that every TracFone customer that Verizon can add is cheaper to serve—

and every upgraded service offering Verizon can sell is cheaper to provide—and

thus more profitable for Verizon at any price point compared to TracFone as an

MVNO. This gives Verizon a strong incentive to compete more vigorously to

attract more customers (and to sell those customers improved products) via lower

prices and/or improved quality—and thus lower quality-adjusted prices—for the

TracFone offering. By sharing the benefits of lower costs with customers in this

way, Verizon will be able to compete more effectively for those customers—who

become more attractive to serve due to the cost savings from the Transaction—

thus simultaneously benefiting consumers and Verizon’s bottom line. This is the

power of variable cost efficiencies: By making TracFone more efficient, they

permit simultaneous improvement in profitability and consumer welfare. And

economics shows that to do anything other than share the benefits in this way—

that is to do anything but pass the benefits through to consumers, at least in part—

would be irrational, because it would not be profit-maximizing for Verizon.

Moreover, contrary to Dr. Selwyn’s assertions and consistent with the economic

incentive to pass through variable cost savings, the Verizon documents to which

he cites show that prices will be lower and customer growth will be higher with

the Transaction than without.

3• Dr. Selwyn’s proposed regulatory remedy would not achieve the same efficiencies as

the merger. Although DISH obtained favorable wholesale rates for a limited period

of time as part of the remedy in Sprint/T-Mobile, even on its own terms, this

approach would not replicate the large efficiencies that would be achieved in this

Transaction as it would not give TracFone owner’s economics or eliminate double

marginalization. Moreover, this approach does not solve the coordination problems

that arise in an arm’s-length MVNO relationship.

4. The remainder of this Testimony explains these conclusions in greater depth and provides

details of the facts and analyses that led me to reach them.

II. THE TRANSACTION WILL NOT MATERIALLY REDUCE COMPETITION.

5. In my Opening Testimony, I concluded that the Transaction would not materially reduce

retail competition 4 or wholesale competition. 5 In contrast, Dr. Selwyn argues that (a) the

Transaction will “diminish competition for prepaid wireless services;” 6 and (b) the Transaction

would affect the wholesale market. 7 I address his claims below and show that they are not

grounded in sound economics, do not reflect the realities of the wireless marketplace, do not

properly capture the benefits and lack of competitive harm from the Transaction, and thus do not

survive scrutiny. Dr. Selwyn’s flawed analyses cause him to miss that the Transaction is one that

4

Israel Testimony, § III.

5

Israel Testimony, § IV.

6

Selwyn Testimony, § VI.

7

Selwyn Testimony, § V.

4unlocks substantial efficiencies with very little scope for any competitive issues and thus is

clearly procompetitive on balance.

A. DR. SELWYN HAS PREVIOUSLY RECOGNIZED THE COMPETITIVE DISADVANTAGES

THAT MVNOS FACE, WHICH LIMIT THEIR ABILITY TO COMPETE WITH MNOS.

6. In his Opening Testimony, Dr. Selwyn dismisses the competitive limitations that result

from TracFone’s status as an MVNO and thus reliance on MNOs, asserting that: 8

If TracFone is to be believed, one is compelled to conclude that competition from

MVNOs not affiliated with a facilities-based MNO is simply not viable, that such

MVNOs cannot be relied upon to competitively constrain pricing and other

actions of the three remaining facilities-based wireless carriers.

He treats this statement as incorrect and suggests that MVNOs can be a powerful

competitive constraint, as would be required to find material harm to competition from

the Transaction.

7. Dr. Selwyn’s views in this case thus stand in sharp contrast to those he has testified to

very recently. In testimony before the CPUC in the Sprint/T-Mobile transaction, Dr. Selwyn

recognized the very same limitations that TracFone has described in this proceeding and noted

that these limitations can make MVNOs non-viable competitors. In that proceeding, Dr. Selwyn

explained that “[a]n MVNO exists as a successful business venture at the sufferance of the host

facilities-based carrier” 9 and noted that this dependence on MNOs leaves MVNOs vulnerable to

8

Selwyn Testimony, ¶ 53.

9

In the Matter of the Joint Application of Sprint Communications Company L.P. (U-5112) and T-

Mobile USA, Inc., a Delaware Corporation, For Approval of Transfer of Control of Sprint

Communications Company L.P. Pursuant to California Public Utilities Code Section 854(a),

Application 18-07-011, On Behalf of the Public Advocates Office, Direct Testimony of Lee L.

Selwyn, January 7, 2019 (hereinafter Selwyn T-Mobile/Sprint Testimony), ¶ 88.

5margin squeezes by MNOs. He quoted a McKinsey report in which “[t]he authors warn MVNOs

about the potential for the host carrier to engage in price squeeze tactics by collapsing – or even

eliminating – the spread between its own retail prices and the wholesale prices it offers to

MVNOs.” 10 And Dr. Selwyn quoted comments from cable MVNO Charter that: 11

Charter faces certain limitations in its ability to compete in the mobile market on

the same terms as Verizon or other facilities-based carriers. There are significant

limitations to its MVNO agreement, which are confidential but limit Charter’s

ability to fully manage the mobile network and sell the product, thereby hindering

the competitiveness of Charter’s mobile service.

Providing mobile service through Charter's MVNO resale arrangement is

materially different than providing mobile service as a facilities-based nationwide

or even regional mobile carrier . . . Charter believes that under the existing

MVNO agreement, Spectrum Mobile is not and cannot reasonably be viewed as

having the ability to counteract price increases or other anticompetitive effects, if

any, arising from a merged T-Mobile/Sprint.

8. Notably, these previous statements from Dr. Selwyn not only recognize the

marketplace reality that MVNOs are of limited competitive significance—meaning the

Transaction has little scope for competitive harm—but also recognize that integration

with an MNO, thus making TracFone into a facilities-based carrier, greatly increases its

ability to compete.

B. HHIS CANNOT PROVE HARM FROM THE TRANSACTION.

9. Despite acknowledging that “[s]everal recent telecommunications mergers have been

approved despite HHI increases that were significantly greater than” those that he calculates

here, Dr. Selwyn nevertheless asserts that “the potential diminution of competition should be

10

Selwyn T-Mobile/Sprint Testimony, ¶ 88.

11

Selwyn T-Mobile/Sprint Testimony, ¶ 112.

6more than sufficient to warrant rejection.” 12 In fact, HHIs are, at best, a starting point for the

analysis of a merger. 13 Most fundamentally, HHIs do not account for efficiencies arising from a

merger, as Dr. Selwyn acknowledges. 14 They also do not account for product differentiation. 15

For this reason, when evaluating the competitive effects of mergers, antitrust agencies typically

use HHIs merely as a screening mechanism to determine whether further analysis is required. 16

10. As I demonstrated in my Opening Testimony and further demonstrate below, the

Transaction will result in substantial efficiencies that will benefit consumers. And as I have

demonstrated, the substantial differentiation between Verizon and TracFone—distant

competitors in the wireless space, each of which competes more closely with multiple brands at

other wireless carriers than with each other—together with the weak competitive position of

MVNOs means that HHIs (particularly those that treat MVNOs as fully independent) cannot be

used to predict harm to competition in this case.

12

Selwyn Testimony, ¶ 76.

13

U.S. Department of Justice and the Federal Trade Commission, Horizontal Merger Guidelines,

August 19, 2010 (hereinafter Horizontal Merger Guidelines), § 5.3 (“Market shares may not fully

reflect the competitive significance of firms in the market or the impact of a merger. They are

used in conjunction with other evidence of competitive effects.”).

14

Selwyn Testimony, ¶ 76.

For a discussion of efficiencies, see Israel Testimony, § II and Section III below.

15

For a discussion of how TracFone’s products are substantially differentiated from those of

Verizon, see Israel Testimony, § III.C.

16

Horizontal Merger Guidelines, § 5.3 (“The purpose of these thresholds is not to provide a rigid

screen to separate competitively benign mergers from anticompetitive ones, although high levels

of concentration do raise concerns. Rather, they provide one way to identify some mergers

unlikely to raise competitive concerns and some others for which it is particularly important to

examine whether other competitive factors confirm, reinforce, or counteract the potentially

harmful effects of increased concentration.”).

7C. DR. SELWYN’S TREATMENT OF MVNOS IN HIS HHI CALCULATIONS IS FLAWED

AND CONTRADICTS HIS PRIOR TESTIMONY.

11. In calculating HHIs among prepaid providers, Dr. Selwyn treats TracFone and Boost

Mobile, both of which provide service as MVNOs, as independent competitors and assigns them

independent market shares. 17 As explained in my Opening Testimony, this treatment fails to

reflect the complex competitive dynamics between MNOs and MVNOs. 18 MNOs control the

price at which they provide wholesale network access to MVNOs and can accordingly influence

MVNOs’ ability to compete. Because MVNOs depend on wholesale access to MNOs, they are

not fully independent competitors. As noted above, Dr. Selwyn has previously testified to the

competitive limitations that MVNOs face because they are not independent competitors.

12. Dr. Selwyn’s treatment of MVNOs as independent competitors in calculating market

shares and HHIs contradicts his approach in the Sprint/T-Mobile transaction. In Sprint/T-

Mobile, Dr. Selwyn presented market shares and HHIs among prepaid providers in which he

only included “Branded Prepaid Subs” of MNOs Verizon, AT&T, T-Mobile, and Sprint. 19 By

not including MVNOs in his HHI calculations, Dr. Selwyn treated MVNOs as if they were not

competitors at all and exerted no competitive impact—that is, he treated them as irrelevant to his

assessment of competition among MNOs. Yet, he now claims that an MVNO is so

competitively relevant that the acquisition of one by Verizon will substantially harm

competition. Figure 1 below shows that the prepaid market shares and HHIs that Dr. Selwyn

17

Selwyn Testimony, Tables 10-11.

18

Israel Testimony, ¶¶ 39-40, 44.

19

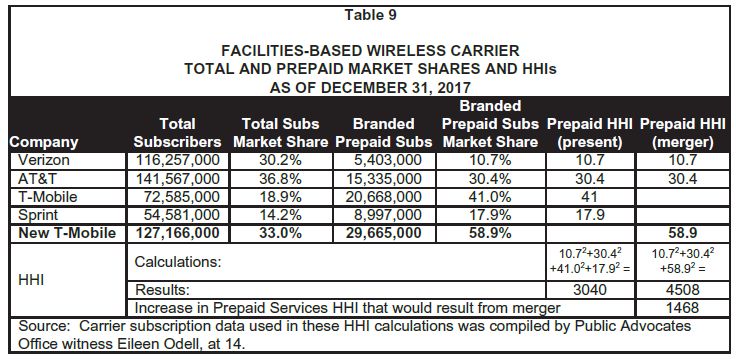

Selwyn T-Mobile/Sprint Testimony, Table 9.

8presented in Table 9 of his direct testimony in Sprint/T-Mobile omit TracFone and other

MVNOs.

Figure 1: Dr. Selwyn’s Treatment of MVNOs in Sprint/T-Mobile

13. In calculating the prepaid HHIs shown above in Sprint/T-Mobile, Dr. Selwyn cited and

relied on carrier subscription data compiled by California Public Advocates Office witness

Eileen Odell. Like Dr. Selwyn, Ms. Odell excluded MVNO subscribers in her calculations of

market shares among prepaid providers and only provided “Branded Prepaid Subscribers” of

Verizon, AT&T, T-Mobile and Sprint. 20 Ms. Odell explained that “[t]he FCC generally excludes

non facilities-based providers from its analysis of market concentration.” 21 My view has been

20

In the Matter of the Joint Application of Sprint Communications Company L.P. (U-5112) and T-

Mobile USA, Inc., a Delaware Corporation, For Approval of Transfer of Control of Sprint

Communications Company L.P. Pursuant to California Public Utilities Code Section 854(a),

Application 18-07-011, Direct Testimony of Eileen Odell, January 7, 2019 (hereinafter Odell T-

Mobile/Sprint Testimony), p. 14.

21

Odell T-Mobile/Sprint Testimony, p. 15.

9and remains that MVNOs should not be ignored, but rather that any analysis of them should

incorporate the limitations and higher cost of the MVNO structure, which is precisely the reason

I conclude that the Transaction—by making TracFone a lower-cost, stronger competitor—is

procompetitive.

14. In Sprint/T-Mobile, Dr. Selwyn also presented additional HHIs using an alternative

methodology that similarly excluded MVNOs. Dr. Selwyn presented county-level HHIs of

MNOs in California using spectrum bandwidth allocation shares. 22 Because TracFone and other

MVNOs generally lack spectrum, they were excluded from Dr. Selwyn’s spectrum-based HHI

calculations. Following the announcement of the divestiture of Boost Mobile to DISH in the

Sprint/T-Mobile transaction, Dr. Selwyn presented additional spectrum-based HHI calculations

that accounted for DISH’s entry into the mobile wireless services market as a facilities-based

competitor. 23 Once again, Dr. Selwyn presented HHIs that excluded non-facilities-based

MVNOs, including TracFone. If the MNOs and MVNOs are competitors in the manner he

suggests in this proceeding, all of those prior calculations were incorrect.

22

Selwyn T-Mobile/Sprint Testimony, ¶¶ 42-43 (describing the methodology for calculating county-

level HHIs and explaining that “[p]re-merger HHIs were calculated using the spectrum bandwidth

allocation shares of each of the four largest carriers in each census block” and “[p]ost-merger

HHIs were calculated by combining the Sprint and T-Mobile availability-adjusted bandwidth

shares. . . .”); see also In the Matter of the Joint Application of Sprint Communications Company

L.P. (U-5112) and T-Mobile USA, Inc., a Delaware Corporation, For Approval of Transfer of

Control of Sprint Communications Company L.P. Pursuant to California Public Utilities Code

Section 854(a), Application 18-07-011, On Behalf of the Public Advocates Office, Reply

Testimony of Lee L. Selwyn, November 22, 2019 (hereinafter Selwyn T-Mobile/Sprint Reply

Testimony), ¶ 10 (“The county level HHIs that I presented in my January 7 testimony were based

upon spectrum shares. . . .”).

23

Selwyn T-Mobile/Sprint Reply Testimony, ¶ 51 (describing the methodology for calculating

spectrum-based HHIs that include DISH).

1015. Dr. Selwyn’s treatment of MVNOs as full-fledged, independent competitors in this

proceeding also runs counter to the District Court’s conclusion in Sprint/T-Mobile. In that case,

the District Court concluded that “MVNOs should not be considered independent competitors in

the [retail mobile wireless telecommunications services market],” and it adopted the State of

California and other Plaintiff States’ position in holding that “MVNO shares should thus be

attributed to the MNOs from which the MVNOs lease network access.” 24

16. As noted in my Opening Testimony, if one follows the District Court’s approach and

attributes their share to the corresponding MNOs, the Transaction would actually reduce

concentration among prepaid plans and MVNOs. 25 And among postpaid, prepaid, and MVNO

providers, the HHI would increase by just 20 to 27 points, far below the “safe harbor” levels in

the Horizontal Merger Guidelines. 26

D. THE MERGER WILL NOT HARM WHOLESALE COMPETITION.

17. Dr. Selwyn asserts that MVNOs would exit the marketplace or at least “become

substantially diminished” as a result of this Transaction. 27

18. As an initial matter, I stress again that the effect on MVNOs per se is not the relevant

question. Instead, the relevant question is whether the Transaction is procompetitive, meaning

whether it benefits wireless consumers. As I explained in my Opening Testimony: 28

24

New York v. Deutsche Telekom AG, 439 F. Supp. 3d 179, 200 (S.D.N.Y. 2020).

25

Israel Testimony, ¶ 42.

26

Israel Testimony, ¶ 43.

27

Selwyn Testimony, ¶¶ 54, 74, 76.

28

Israel Testimony, ¶ 51.

11From an economic perspective, the correct standard for assessing the effects of

the transaction is the effect on consumers, not the effect on, for example, a

specific competitor or set of competitors. This standard focuses on consumers and

naturally incorporates the effects of efficiencies, including the reduction in

marginal costs from the elimination of double marginalization, as well as all other

competitive effects to reach a bottom-line conclusion about the transaction’s

competitive effects. Conversely, a focus on harm to MVNOs in the wholesale

market, for example, distinct from the effects on consumers in the downstream

market, would not constitute an appropriate standard for evaluating the effects of

the merger because any such “harm” to MVNOs can reflect stronger competition

from the merged firm. In particular, a TracFone that realizes substantially lower

marginal costs would be a much more formidable competitor to other MVNOs,

which would benefit consumers even if it reduces the margins of rival MVNOs,

meaning the effects on MVNOs of the transaction is the wrong standard, as

procompetitive, pro-consumer changes can harm rival MVNOs by increasing the

competition they face.

19. In any event, Verizon will continue to have an incentive to sell wholesale network access

to competitively relevant MVNOs—which are the only MVNOs that can matter for an

assessment of the Transaction’s effect on competition and consumers—including cable

companies and other MVNOs with distinct business cases to serve particular sets of consumers

(such as those who want to buy wireless services as part of a bundle from their cable provider). 29

Verizon will continue to have this incentive because those MVNOs offer unique value

propositions (e.g., cable companies can bundle mobile service with wireline services) and selling

wholesale network access to them allows Verizon to share in the value that those MVNOs create.

Those MVNOs will also retain the ability to purchase wholesale network access from AT&T and

T-Mobile (and, potentially, DISH), which continue to sell such access despite also owning

flanker brands. Indeed, to the extent that AT&T and T-Mobile find it beneficial to replace

29

Israel Testimony, § IV.B.

12TracFone subscribers that shift to the Verizon network, that would give them an additional

incentive to serve other MVNOs.

III. THE TRANSACTION WILL RESULT IN SUBSTANTIAL EFFICIENCIES

THAT WILL BENEFIT CONSUMERS.

20. In my Opening Testimony, I explained that the Transaction would lower costs and benefit

consumers through several mechanisms. Principal among these was a reduction in TracFone’s

network costs, from the wholesale prices that it currently pays, down to just the much lower

incremental network costs that Verizon incurs to serve TracFone subscribers. 30 I also explained

that the Transaction would solve a coordination problem and lead to faster product roll-outs, 31

and that it would result in economies of scale and scope. 32 Finally, I explained that Verizon

would have an economic incentive to pass through cost savings to consumers. 33

21. Dr. Selwyn advances two main arguments against efficiencies: (a) they have not been

quantified; 34 and (b) they would not be passed through to consumers. 35 I address each of these

criticisms below. In summary:

• As I described in my Opening Testimony, TracFone currently purchases wholesale

network access and the Transaction would allow it to instead realize costs associated

30

Israel Testimony, § II.A.

31

Israel Testimony, § II.B.

32

Israel Testimony, § II.C.

33

Israel Testimony, § II.D.

34

Selwyn Testimony, ¶ 15.

35

Selwyn Testimony, § III.

13with “owner’s economics.” 36 That is, while today the incremental costs to TracFone

from adding a customer with associated usage reflect the marked-up charges from an

MNO, post-merger TracFone will internalize Verizon’s lower actual incremental cost

of serving that additional load. Because the costs associated with the latter are

substantially lower than those associated with the former, the Transaction will

substantially reduce TracFone’s marginal costs. Below, in response to Dr. Selwyn’s

criticism, I provide a quantification of the size of these cost savings.

• And as a matter of fundamental economics, this reduction in marginal costs means

that every TracFone customer that Verizon can add is cheaper to serve—and every

upgraded service offering Verizon can sell is cheaper to provide—and thus more

profitable for Verizon at any price point compared to TracFone as an MVNO. This

gives Verizon a strong incentive to compete more vigorously to attract more

customers and sell them higher quality products, via lower quality-adjusted prices.

By sharing the benefits of lower costs with customers in this way, Verizon will be

able to compete more effectively for those customers—who become more attractive

to serve due to the cost savings from the Transaction—thus simultaneously benefiting

consumers and Verizon’s bottom line. This is the power of variable cost efficiencies:

By making TracFone more efficient they permit simultaneous improvement in

profitability and consumer welfare. And economics shows that to do anything other

than share the benefits in this way—that is to do anything but pass the benefits

36

Israel Testimony, ¶ 15.

14through to consumers, at least in part—would be irrational, because it would not be

profit-maximizing for Verizon. Moreover, contrary to Dr. Selwyn’s assertions and

consistent with the economic incentive to pass through variable cost savings, the

Verizon documents to which he cites show that prices will be lower and customer

growth will be higher with the Transaction relative to the Standalone case.

A. QUANTIFICATION OF EFFICIENCIES

22. To quantify the marginal cost efficiencies, described above, I calculate the marginal

network cost savings as the difference between the wholesale costs that TracFone would pay on

a standalone basis and the on-network costs that Verizon incurs on the same traffic. As I

described in my Opening Testimony, these savings accrue on both TracFone subscribers

currently on the Verizon network (due to the elimination of double marginalization) and

TracFone subscribers currently on non-Verizon networks (due to the reduction in wholesale costs

paid to those MNOs). 37

23. As I describe in more detail in the Appendix (Section V below), I use information

provided by Verizon to calculate the incremental network costs associated with accommodating

incremental network traffic. These costs range from [BEGIN VERIZON CONFIDENTIAL

LAWYERS ONLY] [END VERIZON CONFIDENTIAL LAWYERS

ONLY]. 38

37

Israel Testimony, §§ II.A-B.

38

See Table 4 below.

1524. Table 1 summarizes the marginal network cost savings separately for TracFone

subscribers on the AT&T, T-Mobile, and Verizon networks. Because the amount of usage and

the wholesale prices vary for each group, the resulting marginal cost savings also vary.

• For AT&T TracFone subscribers, marginal costs savings expressed on a per-GB basis

vary from [BEGIN CONFIDENTIAL LAWYERS ONLY]

[END CONFIDENTIAL LAWYERS ONLY] and expressed on a per-

subscriber/month basis vary from [BEGIN CONFIDENTIAL LAWYERS ONLY]

[END CONFIDENTIAL LAWYERS ONLY]

• For T-Mobile TracFone subscribers, marginal costs savings expressed on a per-GB

basis vary from [BEGIN CONFIDENTIAL LAWYERS ONLY]

[END CONFIDENTIAL LAWYERS ONLY] and expressed on a per-

subscriber/month basis vary from [BEGIN CONFIDENTIAL LAWYERS ONLY]

[END CONFIDENTIAL LAWYERS ONLY]

• For Verizon TracFone subscribers, marginal costs savings expressed on a per-GB

basis vary from [BEGIN CONFIDENTIAL LAWYERS ONLY]

[END CONFIDENTIAL LAWYERS ONLY] and expressed on a per-

subscriber/month basis vary from [BEGIN CONFIDENTIAL LAWYERS ONLY]

[END CONFIDENTIAL LAWYERS ONLY]

16[BEGIN CONFIDENTIAL LAWYERS ONLY]

[END CONFIDENTIAL LAWYERS ONLY]

25. Expressed as a percentage of TracFone’s ARPU, which is approximately $28, these

marginal cost efficiencies are approximately [BEGIN TRACFONE CONFIDENTIAL

LAWYERS ONLY] [END TRACFONE CONFIDENTIAL LAWYERS ONLY]

percent of revenues. Marginal cost efficiencies of this magnitude, even before accounting for the

other benefits of the Transaction that I described in my Opening Testimony, would make post-

merger TracFone a much more potent competitor, and they are clearly the dominant effect of the

Transaction. In particular, given the extremely limited scope for any harms to competition—

because of TracFone’s status as an MVNO and its differentiation from Verizon—marginal cost

17savings of this size surely swamp any possible harms to competition, which implies that the

Transaction is procompetitive and consumer-welfare enhancing.

B. EFFICIENCIES FROM THE TRANSACTION WILL BE PASSED THROUGH TO THE

BENEFIT OF CONSUMERS.

26. As I explained in my Opening Testimony, “[p]rofit-maximizing firms have an incentive

to pass through marginal cost savings because doing so is profitable.” 39 In an argument that runs

counter to the most fundamental teachings of microeconomics, Dr. Selwyn argues that “Verizon

will have no incentive to flow any cost savings resulting from its acquisition of TracFone

through to TracFone customers.” 40 He also argues that Verizon’s documents demonstrate that it

would not pass cost savings on to consumers. 41 Both arguments are simply incorrect as a matter

of economics and of facts. I address each of these arguments below and explain why, in fact,

fundamental economics shows that Verizon will pass through cost savings (in lower prices

and/or higher quality than absent the Transaction), and Verizon’s documents are consistent with

this conclusion.

1. Pass-through of efficiencies and upward pricing pressure are

symmetrical.

27. The economic literature has demonstrated that upward pricing pressure arising from a

merger of horizontal competitors is economically equivalent to a marginal cost increase. 42 This

39

Israel Testimony, ¶ 37.

40

Selwyn Testimony, ¶¶ 15-20.

41

Selwyn Testimony, ¶¶ 21-32.

42

Robert Willig (2011), “Unilateral Competitive Effects of Mergers: Upward Pricing Pressure,

Product Quality, and Other Extensions,” Review of Industrial Organization, 39(1-2): 19-38

(hereinafter Willig (2011)). See also Luke Froeb, Steven Tschantz, and Gregory Werden (2005),

18equivalence means that the same pass-through rate that applies to merger efficiencies also

applies to upward pricing pressure. For this reason, mergers are often evaluated by considering

the “first-order effects”—i.e., by balancing upward pricing pressure against marginal cost

efficiencies without considering pass-through. 43 Indeed, if Dr. Selwyn were correct that the

pass-through rate is zero, then his testimony would also imply that the merger will result in no

harm to consumers. So, while I correct Dr. Selwyn’s errors with regard to pass-through below,

in an important sense, the question is irrelevant: If the marginal cost savings from the

Transaction outweigh the scope for competitive harm—as they clearly do—the Transaction is

procompetitive and thus consumer-welfare enhancing.

2. Dr. Selwyn’s claims about elasticity and pass-through are incorrect as

a matter of economics and marketplace realities.

28. Dr. Selwyn asserts that pass-through of marginal cost savings would be profitable to

Verizon “only if the demand for the TracFone service is sufficiently price-elastic,” 44 and he

claims that the demand that post-acquisition TracFone will face will be “highly price-inelastic,”

such that there will be no pass-through. 45 That is, he claims that pass-through only occurs in

situations where consumers are price-sensitive, and he argues that TracFone subscribers are not

price-sensitive, and thus he claims there will not be significant pass-through in this case.

“Pass-Through Rates and the Price Effects of Mergers,” International Journal of Industrial

Organization, 23: 703-715.

43

Horizontal Merger Guidelines, § 6.1; Willig (2011); Joseph Farrell and Carl Shapiro (2010),

“Upward Pricing Pressure in Horizontal Merger Analysis: Reply to Epstein and Rubinfeld,” The

B.E. Journal of Theoretical Economics, 10(1), Article 41.

44

Selwyn Testimony, ¶ 16.

45

Selwyn Testimony, ¶ 17.

1929. Dr. Selwyn is incorrect on both counts: The claim that there will only be pass-through

when consumers are price-sensitive is wrong as a matter of economics, and the claim that

TracFone subscribers are price-inelastic is wrong both as a matter of economics and marketplace

realities. While lower price elasticity leads to higher optimal price levels for any given costs, as

long as consumers react at all to prices (meaning demand is not perfectly inelastic), economic

theory and data show that there will be pass-through, and it is generally substantial. And

TracFone subscribers are certainly price-sensitive, given both TracFone’s position in the

marketplace and what economics tells us about what price elasticities must be.

30. With regard to elasticities, there would be no pass-through incentive only if demand were

perfectly inelastic, meaning that consumers would not react at all to a change in price, such that

a change in price would result in no change in quantity whatsoever. 46 However, if this were the

case, TracFone would have an incentive to price much higher today (effectively, to set an infinite

price) than it does because raising prices would cause it to lose no volume. Assuming TracFone

is seeking to maximize profits, demand cannot be inelastic (that is, the demand elasticity faced

by Tracfone cannot be less than one in absolute value) in a well-defined economic equilibrium. 47

Moreover, as an empirical matter, demand is likely to be quite elastic, especially for the price-

conscious prepaid and MVNO customers who are the focus of Dr. Selwyn’s analysis. 48

46

In this case, there would also be no merger harm.

47

Dennis W. Carlton and Jeffrey M. Perloff (2005), Modern Industrial Organization, 4th Edition,

Pearson, p. 94.

48

Selwyn Testimony, ¶ 39 (“In a competitive market, customers – and particularly prepaid

customers who do not have a fixed term contract – are free to move to a different provider if they

are dissatisfied with their current service. In fact, the high churn rates – the frequency with which

2031. As long as demand is not perfectly inelastic, which it cannot be as a matter of logic and

sound economics, pass-through rates are determined not by the level of the elasticity at a

particular point on the demand curve, but by the relative change in elasticity as quality-adjusted

prices change (i.e., the extent to which consumers become less sensitive to quality-adjusted

prices as they decline). 49 In the present case, the price sensitivity faced by TracFone may not fall

much as prices fall: If by cutting prices or increasing quality, TracFone is able to capture even

more value-conscious customers—as is consistent with Verizon’s plans post-merger—then the

price elasticity it faces would not be expected to fall rapidly as its quality-adjusted prices fall,

meaning pass-through would be substantial. In simpler terms, in some situations (unlike this

one), the incentive to pass through cost reductions gets “choked off” because, as a firm cuts

quality-adjusted prices, consumers react less and less to those price cuts, so they become a

customers switch services – associated with prepaid services confirms that this is already

happening on a regular basis.”).

49

This result—that pass-through depends on the curvature of the demand curve, not just the level of

elasticity—holds quite generally in models other than perfect competition. For example, Weyl

and Fabinger (2013) show the pass-through rate under monopoly is a function of not only the

elasticities of demand and supply, but the curvature of the logarithm of demand as well. This

same result—that pass-through depends on the curvature of the demand curve, not just the level

of elasticity—holds for Bertrand competition among firms selling differentiated products (the

standard economic model applies to the wireless industry), using the residual demand curve faced

by each firm holding all other firms’ qualities and prices fixed. Verboven and van Dijk (2009)

derive the industry-level pass-through rate under Cournot competition and show that it is a

function of the number of firms in the industry and the curvature of the inverse demand function.

A convex inverse demand function exhibits declining price sensitivity of demand as price rises

and corresponds to ρ > 0, thus shrinking the denominator and in turn increasing the pass-through

rate. On the other hand, a concave inverse demand function exhibits an increasing price

sensitivity of demand as price rises and corresponds to ρ < 0, which increases the denominator

and thereby decreases the pass-through rate. (E. Glen Weyl and Michal Fabinger (2013), “Pass-

Through as an Economic Tool: Principles of Incidence under Imperfect Competition,” Journal of

Political Economy, 121(3): 528-583, pp. 534 and 539; Frank Verboven and Theon van Dijk

(2009), “Cartel Damages Claims and the Passing-On Defense,” Journal of Industrial Economics,

57(3): 457-91, pp. 475-76.)

21weaker tool to attract customers. Here, if cutting quality-adjusted prices brings in more value-

conscious subscribers, the tool will not weaken as quality-adjusted prices fall, so pass-through

would be expected to be substantial.

3. Empirical economic evidence demonstrates substantial pass-through

as the expected outcome.

32. There is substantial empirical evidence that firms pass through cost savings both in

general and in the wireless industry. Below, I briefly review the economic literature on pass-

through.

(a) Empirical literature on pass-through.

33. The economic literature finds empirical evidence of substantial pass-through in a broad

variety of industries. Pass-through rates of approximately 100 percent or more have been

estimated from energy cost changes to cement prices 50 as well as the prices of boxes and

plywood, 51 from wholesale to retail coffee prices, 52 from price changes of sugar to the price of

French soft drinks, 53 from imposition of an air ticket levy to European airline fares, 54 and from

50

Nathan H. Miller, Matthew Osborne, and Gloria Sheu (2017), “Pass-Through in a Concentrated

Industry: Empirical Evidence and Regulatory Implications,” RAND Journal of Economics, 48(1):

69-93, pp. 84-86; Sharat Ganapati, Joseph S. Shapiro, and Reed Walker (2020), “Energy Cost

Pass-Through in US Manufacturing: Estimates and Implications for Carbon Taxes,” American

Economic Journal: Applied Economics, 12(2): 303-42, p. 333.

51

Ganapati, id.

52

Emi Nakamura and Dawit Zerom (2010), “Accounting for Incomplete Pass-Through,” Review of

Economic Studies, 77(3): 1192-1230, p. 1201.

53

Céline Bonnet and Vincent Réquillart (2013), “Impact of Cost Shocks on Consumer Prices in

Vertically-Related Markets: The Case of the French Soft Drink Market,” American Journal of

Agricultural Economics, 95(5): 1088-1108, p. 1102.

54

Marc Ivaldi and Tuba Toru-Delibaşi (2018), “Competitive Impact of the Air Ticket Levy on the

European Airline Market,” Transport Policy, 70: 46-52, p. 49.

22changes in excise taxes on the prices of alcohol, 55 cigarettes, 56 e-cigarettes, 57 and motor fuel 58 (at

least in some states). The cost of the tobacco industry’s Master Settlement Agreement was

passed through to cigarette prices at roughly 100 percent. 59 Emission costs are passed through to

Spanish electricity prices at more than 80 percent. 60 A study of retail pass-through at

Dominick’s Finer Foods, a supermarket chain in Chicago, found pass-through rates of 60 percent

or more in 9 of 11 product categories. 61 A study of automobile promotions found that 70-90

percent of “customer cash” promotions were passed on to buyers, as were 30-40 percent of

55

Vinish Shrestha and Sara Markowitz (2016), “The Pass-Through of Beer Taxes to Prices:

Evidence from State and Federal Tax Changes,” Economic Inquiry, 54(4): 1946-62, pp. 1955-59;

Mark Stehr (2007), “The Effect of Sunday Sales Bans and Excise Taxes on Drinking and Cross-

Border Shopping for Alcoholic Beverages,” National Tax Journal, 60(1): 85-105, p. 90.

56

Andrew Hanson and Ryan Sullivan (2009), “The Incidence of Tobacco Taxation: Evidence from

Geographic Micro-Level Data,” National Tax Journal, 62(4): 677-98, p. 686.

57

Henry Saffer, Daniel Dench, Michael Grossman, and Dhaval Dave (2020), “E-Cigarettes and

Adult Smoking: Evidence from Minnesota,” Journal of Risk and Uncertainty, 60(3): 207-28, p.

213.

58

Robert K. Kaufmann (2019), “Pass-Through of Motor Gasoline Taxes: Efficiency and Efficacy of

Environmental Taxes,” Energy Policy, 125: 207-15, p. 212.

59

Dean R. Lillard and Andrew Sfekas (2013), “Just Passing Through: The Effect of the Master

Settlement Agreement on Estimated Cigarette Tax Price Pass-Through,” Applied Economics

Letters, 20(4): 353-57, p. 355.

60

Natalia Fabra and Mar Reguant (2014), “Pass-Through of Emissions Costs in Electricity

Markets,” American Economic Review, 104(9): 2872-99, p. 2882.

61

David Besanko, Jean-Pierre Dubé, and Sachin Gupta (2005), “Own-Brand and Cross-Brand

Retail Pass-Through,” Marketing Science, 24(1): 123-37, p. 131.

23“dealer cash” promotions. 62 Pass-through rates of roughly 50 percent have been estimated from

changes in Medicare Advantage benchmarks to plan bids. 63

(b) Evidence from TracFone indicates that pass-through is likely to be

substantial.

34. There is also evidence of pass-through in the wireless industry and, in particular, that

given the competitive situation it faces, which is the one Verizon will inherit from the

Transaction, TracFone itself finds it optimal to pass through cost savings. For example, Eduardo

Diaz Corona, Chief Executive Officer at TracFone Wireless, Inc., testifies that “TracFone always

uses cost savings and improved offerings negotiated with MNOs to provide better offers to

consumers and to better compete with vertically-integrated prepaid brands.” 64 Mr. Diaz Corona

presents several examples in which TracFone lowered its price or offered improved quality in

response to negotiating more favorable wholesale network access terms. 65

4. Verizon’s documents support pass-through to the benefit of

consumers.

35. Dr. Selwyn argues that Verizon’s documents indicate that:

62

Meghan Busse, Jorge Silva-Risso, and Florian Zettelmeyer (2006), “$1,000 Cash Back: The Pass-

Through of Auto Manufacturer Promotions,” American Economic Review, 96(4): 1253-70, p.

1253.

63

Marika Cabral, Michael Geruso, and Neale Mahoney (2018), “Do Larger Health Insurance

Subsidies Benefit Patients or Producers? Evidence from Medicare Advantage,” American

Economic Review, 108(8): 2048-87, pp. 2063-64; Zirui Song, Mary Beth Landrum, and Michael

E. Chernew (2013), “Competitive Bidding in Medicare Advantage: Effect of Benchmark Changes

on Plan Bids,” Journal of Health Economics, 32(6): 1301-12, p. 1308.

64

Rebuttal Testimony of Eduardo Diaz Corona, Chief Executive Officer at TracFone Wireless, Inc.,

April 9, 2021 (hereinafter Diaz Corona Rebuttal Testimony), p. 2.

65

Diaz Corona Rebuttal Testimony, pp. 3-5.

24• Average revenue per user (ARPU) would be higher with the Transaction than without; 66

• TracFone would have [BEGIN VERIZON CONFIDENTIAL-LAWYERS ONLY]

[END VERIZON CONFIDENTIAL-LAWYERS ONLY] customers with the

Transaction than without; 67

• TracFone’s total revenue would be [BEGIN VERIZON CONFIDENTIAL-

LAWYERS ONLY] [END VERIZON CONFIDENTIAL-LAWYERS ONLY]

with the Transaction than without; 68

• Non-network costs are projected to be [BEGIN VERIZON CONFIDENTIAL-

LAWYERS ONLY] [END VERIZON CONFIDENTIAL-LAWYERS ONLY]

with the Transaction than without; 69 and

• Verizon’s EBITDA gains are greater than the projected cost savings. 70

I address each of these points below. I show that none supports a conclusion that the merger is

anticompetitive or that Verizon would not pass through merger cost savings to consumers. In

fact, they support the opposite view—that TracFone customers will get better options making

TracFone a stronger competitor, which benefits both Verizon and customers, and that TracFone

prices will fall more over time with the Transaction than without.

66

Selwyn Testimony, ¶ 22.

67

Selwyn Testimony, ¶ 23.

68

Selwyn Testimony, ¶ 25.

69

Selwyn Testimony, ¶ 26.

70

Selwyn Testimony, ¶¶ 27-31.

2536. ARPU: ARPU, as the name indicates, is not a price. Instead, it reflects average revenue

per user across multiple users purchasing multiple products at differing price points. ARPU can

increase even if the underlying product prices do not change at all or even if prices decrease if

customers migrate to higher-quality, higher-price plans over time, or otherwise change their

product choices.

37. In the present case, any projected increases in ARPU arise from the fact that Verizon

anticipates that consumers will choose to switch to higher-quality products that become available

as a result of the merger, meaning they are consumer-welfare enhancing. Dr. Selwyn himself

cites a Verizon data response stating that Verizon: 71

[BEGIN VERIZON CONFIDENTIAL-LAWYERS ONLY]

[END VERIZON

CONFIDENTIAL-LAWYERS ONLY]

That same response indicates that [BEGIN VERIZON CONFIDENTIAL-LAWYERS

ONLY]

72

[END VERIZON CONFIDENTIAL-LAWYERS

ONLY] If the merger makes alternative products more attractive such that TracFone customers

71

Selwyn Testimony, ¶ 22 (citing Attachment A-12: Verizon Response to Cal Advocates DR V-7-

10).

72

Selwyn Testimony, ¶ 22 (citing Attachment A-12: Verizon Response to Cal Advocates DR V-7-

10).

26would choose to migrate to higher-quality products, that reflects a benefit of the merger, not a

harm.

38. In fact, Dr. Selwyn’s claim that prices will be higher in the Acquisition case is

incorrect. 73 To use ARPU to compare prices between cases (Standalone and Acquisition) and to

look at trends in prices—while taking out the effect of changes in the mix of plans chosen by

customers between cases (Standalone and Acquisition) and over time—one should use a

weighted-average ARPU, applying weights to each brand that do not change between the two

cases (Standalone and Acquisition) or over time. That is, in order to use ARPU to compare

prices—taking out the effect of different product choices made by consumers over time—one

must look at a fixed basket of products, similar to how measures like the consumer price index

(CPI) are computed. 74 I have done so—weighting each brand in each year by the average of its

projected number of subscribers in 2020 and 2025 in the Standalone and Acquisition cases,

according to the Verizon documents cited by Dr. Selwyn, thus weighting each brand by its

average popularity over the relevant time period. The results are presented in Table 2, below. As

seen there, [BEGIN VERIZON CONFIDENTIAL-LAWYERS ONLY]

[END VERIZON

73

Verizon’s documents use the term “Acquisition case” to refer to the scenario with the Transaction

and the term “Standalone case” to refer to the scenario without the Transaction.

74

For a description of the CPI, see U.S. Bureau of Labor Statistics, “Consumer Price Index

Frequently Asked Questions,” available at https://www.bls.gov/cpi/questions-and-answers.htm,

site accessed April 7, 2021.

27CONFIDENTIAL-LAWYERS ONLY]. 75 Thus, contrary to Dr. Selwyn’s claim, once one

uses fixed weights, in order to isolate price changes from the effects of plan choice made by

customers, Verizon’s documents [BEGIN VERIZON CONFIDENTIAL-LAWYERS ONLY]

[END VERIZON

CONFIDENTIAL-LAWYERS ONLY]

[BEGIN VERIZON CONFIDENTIAL-LAWYERS ONLY]

[END VERIZON CONFIDENTIAL-LAWYERS ONLY]

39. One may ask whether the discontinuation of certain brands represents an attempt to

“force” customers to more expensive brands, and thus invalidates the comparison in Table 2

above. First, this point does not change the fact that consumers choose between the remaining

brands, and thus any comparison of ARPUs that does not use a “fixed basket” of products across

cases and over time—such as the comparison Dr. Selwyn makes—is not a valid comparison of

75

I obtain similar results to those presented in Table 2 when I use 2020 Standalone subscribers as

weights.

28prices. And second, the fact that Verizon may [BEGIN VERIZON CONFIDENTIAL-

76

LAWYERS ONLY] [END VERIZON CONFIDENTIAL-

LAWYERS ONLY] does not invalidate the comparison or suggest that Verizon is attempting to

“force” consumers to higher-price plans. As Dr. Selwyn’s Table 3 reveals, [BEGIN VERIZON

CONFIDENTIAL-LAWYERS ONLY]

77

78

40.

76

Selwyn Testimony, ¶ 23.

77

Selwyn Testimony, Table 3 (citing Attachment A-11: Verizon Response to Cal Advocates DR V-

3-1, HSR Attachment 4(c)6, VZW_000877, VZW_000880).

78

TracFone will [BEGIN VERIZON CONFIDENTIAL-LAWYERS ONLY]

[BEGIN VERIZON CONFIDENTIAL-LAWYERS ONLY] In addition, TracFone has

[BEGIN TRACFONE CONFIDENTIAL-LAWYERS ONLY]

[END TRACFONE

CONFIDENTIAL-LAWYERS ONLY] (Diaz Corona Rebuttal Testimony, § III.C.)

29[END VERIZON CONFIDENTIAL-

LAWYERS ONLY]

41. Moreover, ARPU reflects only the monthly recurring fees associated with subscribing to

a mobile wireless plan. It does not capture other elements of the price that consumers pay or the

changes to the all-in price as a result of the merger. Verizon documents indicate that [BEGIN

VERIZON CONFIDENTIAL-LAWYERS ONLY]

79

[END VERIZON

CONFIDENTIAL-LAWYERS ONLY]

42. In addition, prices cannot be compared without accounting for the amount of data that

customers are consuming; to do so would be akin to comparing the prices of two bags of M&Ms

without accounting for the fact that one bag has twice as many M&Ms. On this point, Verizon

documents also indicate [BEGIN VERIZON CONFIDENTIAL-LAWYERS ONLY]

80

[END VERIZON CONFIDENTIAL-LAWYERS

ONLY]

79

HSR Attachment 4(c)5, pp. VZW_000861 (showing the Standalone case) and VZW_000864

(showing the Acquisition case).

80

Data provided by Verizon.

3043. Customer Counts: As Dr. Selwyn’s Table 2 demonstrates, Verizon projects that

[BEGIN VERIZON CONFIDENTIAL-LAWYERS ONLY]

81

82

[END VERIZON

CONFIDENTIAL-LAWYERS ONLY]

44. Notably, [BEGIN VERIZON CONFIDENTIAL-LAWYERS ONLY]

83

84

[END VERIZON CONFIDENTIAL-LAWYERS

81

Selwyn Testimony, Table 2 (citing Attachment A-11: Verizon Response to Cal Advocates DR V-

3-1, HSR Attachment 4(c)6, VZW_000877, VZW_000880).

82

Selwyn Testimony, Table 2 (citing Attachment A-11: Verizon Response to Cal Advocates DR V-

3-1, HSR Attachment 4(c)6, VZW_000877, VZW_000880).

83

Selwyn Testimony, Table 1 (citing Attachment A-11: Verizon Response to Cal Advocates DR V-

3-1, HSR Attachment 4(c)6, VZW_000877, VZW_000880).

84

[BEGIN VERIZON CONFIDENTIAL-LAWYERS ONLY]

[END VERIZON CONFIDENTIAL-

LAWYERS ONLY]

31ONLY] In particular, some TracFone customers currently ride on non-Verizon networks—

effectively buying access to those networks via TracFone—and it is to be expected that some

number of them will choose to remain with those other networks post-Transaction. 85 Consistent

with this, Verizon’s modeling assumes that [BEGIN VERIZON CONFIDENTIAL-

LAWYERS ONLY]

[END VERIZON CONFIDENTIAL-LAWYERS ONLY]. 86 But this

also means that Verizon’s projection that [BEGIN VERIZON CONFIDENTIAL-LAWYERS

ONLY]

[END

VERIZON CONFIDENTIAL-LAWYERS ONLY] Put simply, Verizon’s TracFone brand will

be a more powerful competitor for AT&T and T-Mobile, including their prepaid brands, than it

is today. Bottom line, [BEGIN VERIZON CONFIDENTIAL-LAWYERS ONLY]

[END VERIZON

CONFIDENTIAL-LAWYERS ONLY] reflects increased competitive strength as a result of

85

Indeed, this is consistent with the practice of attributing some or all of the MVNO share to the

MNO on which the traffic is carried.

86

[BEGIN VERIZON CONFIDENTIAL-LAWYERS ONLY]

[END

VERIZON CONFIDENTIAL-LAWYERS ONLY]

32the very large merger efficiencies, documented above, which gives Verizon strong incentive to

compete for subscribers.

45. Revenues: Revenues are the product of prices and quantity. Higher revenues, on their

own, do not indicate whether the merger is good or bad. Instead, one needs to look at, among

other factors, prices and subscriber counts, which I address above, showing that: [BEGIN

VERIZON CONFIDENTIAL-LAWYERS ONLY]

[END VERIZON CONFIDENTIAL-LAWYERS ONLY]

46. Costs: Dr. Selwyn argues that [BEGIN VERIZON CONFIDENTIAL-LAWYERS

ONLY]

87

88

[END VERIZON CONFIDENTIAL-LAWYERS ONLY] These investments are

procompetitive and benefit consumers. In addition, starting in the second year after the

acquisition, [BEGIN VERIZON CONFIDENTIAL-LAWYERS ONLY]

87

Selwyn Testimony, ¶ 26 (“In other words, with the exception of the savings attributable to

“owner’s economics” and the elimination of double marginalization, the remainder of TracFone’s

operations will actually become less efficient following its acquisition by Verizon than if it were

to continue on a standalone basis.”).

88

[BEGIN VERIZON CONFIDENTIAL-LAWYERS ONLY]

[END VERIZON CONFIDENTIAL-LAWYERS

ONLY] VZW_000861 (showing financials for the Standalone case), and VZW_000864-65

(showing financials for the Acquisition case).

33You can also read