GIANT HEAVY OIL PROJECT IN ARGENTINA - LARGE GAS DEVELOPMENT IN COLOMBIA - CruzSur Energy

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

LARGE GAS DEVELOPMENT GIANT HEAVY OIL PROJECT

IN COLOMBIA IN ARGENTINA

1

DISCLAIMER

This document is a presentation of general background information about PentaNova Energy Corp., (“PentaNova” or the “Company”). The information contained herein has been prepared by the Company solely for information purposes and does not purport to be all-inclusive or to contain all the information

that the recipient may desire or that may be required in order to properly evaluate the business, prospects or value of the Company.

This material has been prepared solely for informational purposes and is not to be construed as a solicitation, an invitation, or an offer to buy or sell any securities and should not be treated as giving investment advice. Neither this material nor anything contained herein shall form the basis of any contract or

commitment whatsoever. It is information in a summary form and does not purport to be complete. This presentation contains statements based on information from third-party sources, which has not been independently verified. It is not intended to be relied upon as advice to investors or potential investors

and does not take into account the investment objectives, financial situation or needs of any particular investor. These should be considered, with or without professional advice, when deciding if an investment is appropriate.

No representation or warranty either express or implied is made as to, and no reliance should be placed on future financial performance, or the fairness, validity, accuracy, or completeness of the information, statements or opinions contained herein including in relation to, statistical data, predictions, estimates

or projections contained in this presentation, which are used for informational purposes only. It should not be regarded by recipients as a substitute for the exercise of their own judgment.

This presentation contains forward-looking information within the meaning of applicable securities laws, including Canadian securities laws and Section 27A of the U.S. Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the U.S. Securities Exchange Act of 1934, as amended. Forward-

looking information may relate to PentaNova’s future outlook and anticipated events or results and may include statements regarding the future financial position, production targets, sales projections, business strategy, budgets, projected costs, financial results and plans and objectives of PentaNova and the

future condition of the oil and natural gas industry and regulatory environment in Colombia and Argentina, as well as other countries in Latin America, in general. In some cases, forward-looking information can be identified by terms such as “may”, “will”, “should”, “expect”, “plan”, “anticipate”, “believe”,

“intend”, “estimate”, “predict”, “potential”, “continue”, “upside” or other similar expressions concerning matters that are not historical facts. Any “financial outlook” or “future oriented financial information” in this presentation, as defined by applicable securities laws, has been approved by management of the

Company. Such financial outlook or future oriented financial information is provided for the purpose of providing information about management’s current expectations and plans relating to the future. Readers are cautioned that reliance on such information may not be appropriate for other circumstances.

Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of PentaNova to be materially different from any future results, performance or achievements expressed or implied by the forward-looking

statements. Although the Company believes that the expectations and assumptions reflected in the forward-looking statements are reasonable based on information currently available to the Company’s management, the Company cannot guarantee future results or events. There can be no assurance that (i)

the Company has correctly measured or identified all of the factors affecting its business or the extent of their likely impact, (ii) the publicly available information with respect to these factors on which the Company’s analysis is based is complete or accurate, (iii) the Company’s analysis is correct or (iv) the

Company’s strategy, which is based in part on this analysis, will be successful.

The forward-looking statements contained herein should not be relied upon as representing PentaNova’s views as of any date subsequent to the date of this Presentation. Except as required by law, PentaNova will not update this information at any particular time and the Company, the placement agents and

their respective affiliates, agents, directors, partners and employees assume no obligation to update or revise forward-looking statements should circumstances or management’s estimates or opinions change and accept no liability whatsoever for any loss or damage of any kind arising out of the use of all or

any part of this presentation or the content contained herein.

All references to “$” herein means the currency of the United States, unless otherwise stated.

Oil and Gas Reserves and Resources Information

Information and statements in this presentation relating to reserves and resources are deemed to be forward-looking statements which are subject to certain risks and uncertainties, as they involve the implied assessment, based on certain estimates and assumptions, that the reserves and resources described

exist in the quantities predicted or estimated, and that the reserves and resources described can be profitably produced in the future.

Certain information in this presentation may constitute “analogous information” as defined in National Instrument 51-101 (“NI 51-101”), including, but not limited to, information relating to areas with similar geological characteristics to the lands held by the Company. Such information is derived from a variety

of publicly available information from government sources, regulatory agencies, public databases or other industry participants (as at the date stated therein) that the Company believes are predominantly independent in nature. The Company believes this information is relevant as it helps to define the

reservoir characteristics in which the Company may hold an interest. The Company is unable to confirm that the analogous information was prepared by a qualified reserves evaluator or auditor and in accordance with the the Canadian Oil and Gas Evaluation (“COGE”) Handbook. Such information is not an

estimate of the reserves or resources attributable to lands held or to be held by the Company and there is no certainty that the reservoir data and economics information for the lands held by the Company will be similar to the information presented therein. The reader is cautioned that the data relied upon by

the Company may be in error and/or may not be analogous to the Company’s land holdings.

The Company has adopted the standard of 6 Mcf:1 bbl when converting natural gas to oil equivalent. Boes may be misleading, particularly if used in isolation. A boe conversion ratio of 6 Mcf:1 bbl is based roughly on an energy equivalency conversion method primarily applicable at the burner tip and does not

represent a value equivalency at the wellhead.

Reserves

The oil and natural gas reserves of the Llancanelo properties in Argentina described herein and the related future net revenue attributable to such reserves were evaluated by Gaffney, Cline & Associates, Patagonia Oil Corp.’s independent reserves evaluator, in accordance with the requirements of NI 51-101 and

the COGE Handbook, effective as of December 31, 2016. The oil and natural gas reserves of the Maria Conchita properties in Colombia described herein and the related future net revenue attributable to such reserves were evaluated by Petrotech, PentaNova’s independent reserves evaluator, in accordance with

the requirements of NI 51-101 and the COGE Handbook, effective as of December 31, 2016.

The determination of oil and gas reserves involves the preparation of estimates that have an inherent degree of associated uncertainty. Categories of proved, probable and possible reserves have been established to reflect the level of these uncertainties and to provide an indication of the probability of

recovery. Possible reserves are those additional reserves that are less certain to be recovered than probable reserves. There is a 10% probability that the quantities actually recovered will equal or exceed the sum of proved plus probable plus possible reserves. The reserves and associated cash flow information

set forth in this presentation are estimates only and there is no guarantee that the estimated reserves will be recovered. Actual crude oil, natural gas and natural gas liquid reserves may be greater than or less than the estimates provided in this presentation. The discounted and undiscounted net present value

of future net revenues attributable to reserves do not represent the fair market value of reserves. The estimates of reserves and future net revenue for individual properties may not reflect the same confidence level as estimates of reserves and future net revenue for all properties, due to the effects of

aggregation.

Resources

This presentation includes certain evaluations of resources for the Llancanelo and Sur Rio Deseado Este properties in Argentina and the SN-9 Block in Colombia prepared by an internal qualified reserves evaluator. These evaluations were not prepared by a person “independent” of the Company as that term is

defined under NI 51-101. These estimates were prepared in accordance with definitions and guidelines in the COGE Handbook and NI 51-101. The product types reasonably expected are shale gas and heavy crude oil resources. Contingent resources are those quantities of petroleum estimated, as of a given

date, to be potentially recoverable from known accumulations using established technology or technology under development, but which are not currently considered to be commercially recoverable due to one or more contingencies. Contingencies affecting the classification as reserves versus resources

relate to the following issues as detailed in the COGE Handbook: ownership considerations, drilling requirements, testing requirements, regulatory considerations, infrastructure and market considerations, timing of production and development, and economic requirements. Contingencies may include factors

such as economic, legal, environmental, political and regulatory matters or a lack of markets. It is also appropriate to classify as contingent resources the estimated discovered recoverable quantities associated with a project in the early evaluation stage. Not all technically feasible development plans will be

commercial. The commercial viability of a development project is dependent on the forecast of fiscal conditions over the life of the project. For contingent resources, the risk component relating to the likelihood that an accumulation will be commercially developed is referred to as the “chance of development.”

For contingent resources the chance of commerciality is equal to the chance of development. Prospective resources are those quantities of petroleum estimated, as of a given date, to be potentially recoverable from undiscovered accumulations by application of future development projects. The economic

status of the resources is undetermined. Not all exploration projects will result in discoveries. The chance that an exploration project will result in the discovery of petroleum is referred to as the “chance of discovery.” Thus, for an undiscovered accumulation the chance of commerciality is the product of two risk

components: the chance of discovery and the chance of development. With respect to discovered resources (including contingent resources), there is uncertainty that it will be commercially viable to produce any portion of the resources. With respect to undiscovered resources (including prospective resources),

there is no certainty that any portion of the resources will be discovered. If discovered, there is no certainty that it will be commercially viable to produce any portion of the resources. The estimates of the resources provided in this presentation are estimates only and there is no guarantee that the estimated

resources will be recovered. Actual shale gas and heavy crude oil resources may be greater or less than the estimates provided in this presentation, and the difference may be material.

2

Introduction

Industry Overview

Asset Overview

Appendix

3

INTRODUCTION

EXECUTIVE MANAGEMENT

Serafino Iacono Luciano Biondi

Executive Chairman CEO

Over 30 years of experience developing oil Over 40 years of experience in South

and mineral resource projects, raising American oil and gas operations from

more than $5Bn in Latin America and exploration through to production

abroad

Warren Levy

Gregg Vernon

President, Argentina Operations

President

Over 20 years of experience in upstream

Professional engineer with over 38 years

and downstream projects from Latin

of experience in the petroleum industry

4 America to Vietnam

managing operations from Colombia to

China

ACHIEVEMENTS

IN THE FIRST SIX MONTHS OF 2017

ü Established operations in Colombia and Argentina

ü We have the have the Right Board and a proven Management Team

ü Llancanelo heavy oil field is a world class development project

ü Gas growth platform in Colombia, drilling in September

ü Closed two financings in six months for a total value of +US$70 million

ü Partnerships with the right players – YPF joint venture in Llancanelo

5

INTRODUCTION

OVERVIEW

Our Company

An Energy company with immediate production and significant upside in Colombia and Argentina

Significant Heavy Oil Gas Development

& Light Oil & Exploration

Acquired four Argentine Heavy and Light Acquired three Colombian gas blocks

oil and gas blocks in July 2017 in January 2017

■ Llancanelo Heavy Oil Block ■ Maria Conchita

■ Km8 Light Oil Property, ■ Sinu 9, and

■ La Mariposa Gas Area, and ■ Tiburon

■ Sur Rio Deseado Heavy Oil Block

■ Development Area

■ Exploration Area

6

INTRODUCTION

COMPANY TIMELINE

Fast Paced Execution, Establishing a First Class Growth Platform

Acquisition of Colombian assets Successfully closed a $35MM

§ Maria Conchita

financing, $12.2MM cash &

§ Sinu 9

$22.8MM equivalent in shares,

§ Tiburon

to acquire the Argentina assets

Completion of RTO process

of PentaNova Resources

December 2016 January 2017 February March April May June July

Agreement to acquire Argentinean

Successfully closed a $34MM capital assets

raise to finance the acquisition of the ü Llancanelo

Colombian assets ü KM8

ü Sur Rio Deseado Este

7

INTRODUCTION

QUALITY BOARD MEMBERS

Blue Chip Board with a Strong Track Record of Overseeing High Growth Companies and Creating Value for Shareholders

■ Involved in the financing and ■ External Relations Director for LNG

Serafino Iacono development of oil, mining and other Susannah Pierce

Canada, a joint venture of Shell,

resource projects in Latin America, PetroChina, Mitsubishi and Korea

Chairman & Executive the United States and Europe raising Gas, which proposes to build BC's

Director more than $5 billion for numerous Director largest LNG export facility

natural resource projects

■ Mr. Keep has extensive business ■ Mr. Scott has decades worth of deep

Gordon Keep experience in investment banking Jeffrey Scott energy related management and

and creating public natural resource operating experience and currently

companies and is currently the CEO serves as the President at Postell

of Fiore Management & Advisory Director Energy, and Executive Chairman at

Director

Corp., a private financial advisory Sulvaris. He is also the founder of

firm. Gran Tierra.

Frank Giustra ■ Canadian businessman and Francisco Sole ■ Currently a member of the board of

philanthropist with an established directors of Mapfre Seguros

track record of building natural Generales de Colombia and the

Director resource companies through access Chairman of the board of Editorial

to capital and creative deal-making Director Planeta Colombiana and the

Chamber of Commerce Hispano-

Colombian

Hernan Martinez ■ Served as Minister of Mines in Jaime Perez ■ Managing Director of Next Ventures

Colombia from July 2006 to August Branger Corp. since 2006 and Executive

2010 and previously a Director of Chairman of PetroMagdalena

Pacific Exploration and Production Energy Corp. from June 2011 to July

Director since 2011 Director 27, 2012

8

INTRODUCTION

PROFESSIONAL MANAGEMENT TEAM

Technical Expertise with Proven Track Record Building Companies and Creating Value

■ Involved in the financing and development of oil, mining and other resource projects in Latin America, the United States and

Serafino Iacono Europe raising more than $5 billion for numerous natural resource projects

■ Currently serving as a director and Executive Co-Chairman of Colombia’s largest gold producer, Gran Colombia Gold (TSX:

Chairman GCM), and as a director of US Oil Sands (TSXV: USO)

30+ Years of Experience ■ Served as Executive Co-Chairman of the Board and co-founder of Pacific E&P (TSX: PEN), and was a director and Co-

Chairman of CGX Energy (TSXV: OYL) and PetroMagdalena Energy (TSXV: PMD)

Luciano Biondi ■ Petroleum Engineer who began his career with Shell de Venezuela, and who has held a number of increasingly senior

managerial positions across various oil and gas companies in South America

■ Served as CEO of PetroMagdalena Energy, a public company with operations in Colombia, and as a member of the board

Chief Executive Officer

and Vice President of Operations for CPVEN, an oil well cementing and services company operating in Venezuela

48+ Years of Experience

■ Professional engineer with vast experience in the petroleum industry across various international operations, reservoir

Gregg Vernon characterization, negotiations, and project management in China, Colombia, Argentina, and Canada

■ Served as the founding president of Petro Andina Resources Inc and as a founder and Chairman of Prospero

President Hydrocarbons, private companies which operated in Argentina and Colombia, as well as serving as interim CEO and COO

38+ Years of Experience of PetroMagdalena Energy

Christopher Reid ■ Chartered Accountant of the institute of Alberta, as well as a CPA, with significant experience in the domestic and

international oil and gas industry

■ Served as the President and CEO of Petrodorado Energy, a petroleum company with operations in Colombia, where he led

CFO & Corporate Secretary the turnaround of the company through a divesture program resulting in a market capitalization increase of approximately

10+ Years of Experience 400% in 2015

Warren Levy ■ Involved in the operations of various upstream and downstream companies from Argentina to Vietnam and Thailand

■ Served as the founder and CEO of Estrella International Energy Services, a public oilfield services company in Argentina, as

President, Argentina well as the founder and CEO of Frontier Hydrocarbons, where he was actively involved in raising over $800 million in capital,

Operations and also held a variety of operational and senior management positions at Schlumberger

20+ Years of Experience

Francisco Bustillos ■ Currently Director and Founder of F&B Consultores Asociados, a Financial and Strategy Consulting Firm, incorporated in

February 2003, that advises on an extensive range of financial and strategic services

VP, Corporate Development ■ Served as Vice President of Administration & Performance for Petrominerales Ltd. from November 2013 until October 2015

and Administration ■ Served at Pacific Stratus Energy as Vice President of Finance from May 2011 until May 2012 and then Vice President of

30+ Years of Experience Administration & Performance from May 2012 until November 2013

9

Introduction

Industry Overview

Asset Overview

Appendix

10INDUSTRY OVERVIEW

EARLY MOVER ADVANTAGE IN ARGENTINA HEAVY OIL AND GAS

Why Argentina? Argentina Is Investment Ready

■ Exceptional opportunities in the oil and gas ■ Focus on Vaca Muerta shale has left the large

sector due to 16 years of underinvestment heavy oil opportunities in the country

■ Constructive pricing framework above unattended and ripe for the taking

international markets ■ In January 2017, President Macri announced

■ Extension of concessions for 10 years companies engaged in Vaca Muerta

available committed to invest ~US$5.0Bn to develop

the play during 2017

■ The new Macri government has shifted toward

market friendly government policies: Over US$8 Bn+ in Vaca Muerta Multiyear Commitments

● Raised US$29Bn in sovereign debt

● Lifted foreign currency restrictions

● Pushing tax and labor reforms

● Tackling union issues

● Clear movement to international price

parity for oil and gas

High quality heavy oil resource position while the industry has focused on light oil development at Vaca Muerta

11INDUSTRY OVERVIEW

ATTRACTIVE HYDROCARBON PRICING – ARGENTINA

Developing Pricing Environment

■ Gas Pricing

● Government plans to eliminate end-user natural gas tariff subsidies by 2019

Ø Strategy will be implemented via gradual increase in end-user tariffs until 2019 which contemplates an increase in gas

prices for upstream producers

● In January 2017, President Macri announced an extension of the Plan Gas program from 2017 to 2020 for companies investing

in E&P projects in the Vaca Muerta, guaranteeing minimum gas prices

● Gas prices have increased to over US$7/MMbtu from US$0.15/MMbtu over the past 10 years

■ Oil Pricing

● The current administration seeks to deregulate prices in an effort to converge to free competition international prices in 2017

Price Dynamics Leading to Argentina’s O&G Industry Normalization

Domestic Gas Price Dynamics (US$/MMbtu) Domestic Oil Price Dynamics (US$/boe)

2017 LNG Import Price: US$6.8/MMbtu 125.0

12%

31% 23% 100.0

45% 38%

50%

81%

6.8 75.0

6.0

4.7 5.3

3.8 4.2

3.4

1.3 50.0 50.8

45.8

Mar-16 Oct-16 Mar-17 Oct-17 Mar-18 Oct-18 Mar-19 Oct-19

25.0

Weighted Average Price for Residential and Commercial Consumers Nov-11 Nov-12 Nov-13 Nov-14 Nov-15 Nov-16

% Government Subsidy

WTI Domestic Average Price

LNG Import Price for 2017

12 ____________________

Source: El Cronista, Wall Street Research and Ministry of Energy and Mining.INDUSTRY OVERVIEW

GAS IN COLOMBIA UNDERPINNED BY ROBUST DEMAND FUNDAMENTALS

Why Colombia? New Gas Production Is Necessary

■ Economic stability with a solid and predictable ■ Gas demand in Colombia is heavily outpacing

business environment supply

● Colombia’s steadfast economic policies have ■ Increasing use of gas in Colombia (e.g. mandate

allowed it to maintain investment grade credit to use gas power in towns with population

ratings (BBB/Baa2/BBB) while other >5,000)

hydrocarbon dependent economies in the ■ Chuchupa, Colombia’s largest gas field, is in

region have faltered decline at a rate that requires more than

● Legal system also guarantees equal rights to 86MMscf to come on stream every year to

national and international investors, as well replace produced molecules

as the free flow of capital ■ Superior natural gas prices to Henry Hub ($5.00 -

■ Continued improvements in security with the $6.00/MMbtu)

execution of the peace accord and

demobilization CHEVRON GUAJIRA GAS PRODUCTION NORTHERN COLOMBIA

600,000

500,000

Gas Production (MSCFPD)

400,000

El Niño

generates 300,000

increased gas Chuchupa has declined at

demand 200,000

86MMcfpd per year for the past

100,000

two years

0

Jan/12 Jan/13 Jan/14 Jan/15 Jan/16 Jan/17

BALLENA CHUCHUPA TOTAL Linear (CHUCHUPA)

13INDUSTRY OVERVIEW

ATTRACTIVE HYDROCARBON PRICING – COLOMBIA

Strong Regional Pricing Dynamics Driven by High Demand and Lack of Infrastructure

■ Gas Pricing

● Northern Colombia gas price will be affected by the gas supply

shortfall and the LNG regasification plant pricing at Cartagena

● Gas price expected to rise from current level of US$5.00/MMbtu

● For each US$1.00 increase in the gas price, the value of gas

reserves in Colombia is expected to increase by ~25%

● Lack of regional pipeline integration results in localized markets

that experience upside potential during surges of high demand

Ø Gas prices reached ~US$15-$18/Mcf during the last La Niña

■ Oil Pricing

● Colombia’s oil price is not subsidized by the government and as

a result, it is affected by global petroleum market movements

Hydrocarbon Prices are Supported by a History of Stable Energy Demand Growth and Use of O&G as the Primary Energy Source

Domestic Oil Price Dynamics (US$/boe)

CAGR

60% 62% 56% 56% 53% 57% 58% 57% 58% 59% 60% 59% (‘04-‘15)

852

852 4.1%

780

780 782

782 819

819

733 7 12.1%

702 702

702 733 7

628 629 653 6 6 203 1.4%

629 3 5 6 203

549

549 553

553 4 216 202

3 3 210 184 220 11.4%

2 3 186 120 141

193 201 103 116

174 178 116 108 87

82 71 91 161 175 170 4.8%

43 27 147 143 158

108 113 120 122 140

102

277 297 297 314 331 3.4%

228 237 237 234 251 232 258

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Oil Gas Coal Hydro Renewables % O&G

14 Note: Canacol reports that it is receiving an average sales price of ~US$5.16/Mcf for 76 MMscf/d production for first 3 months of 2017

____________________

Source: Source: ACP, ANH, Ministry of Mining and Energy and BP Statistical Review 2016.Introduction

Industry Overview

Asset Overview

Appendix

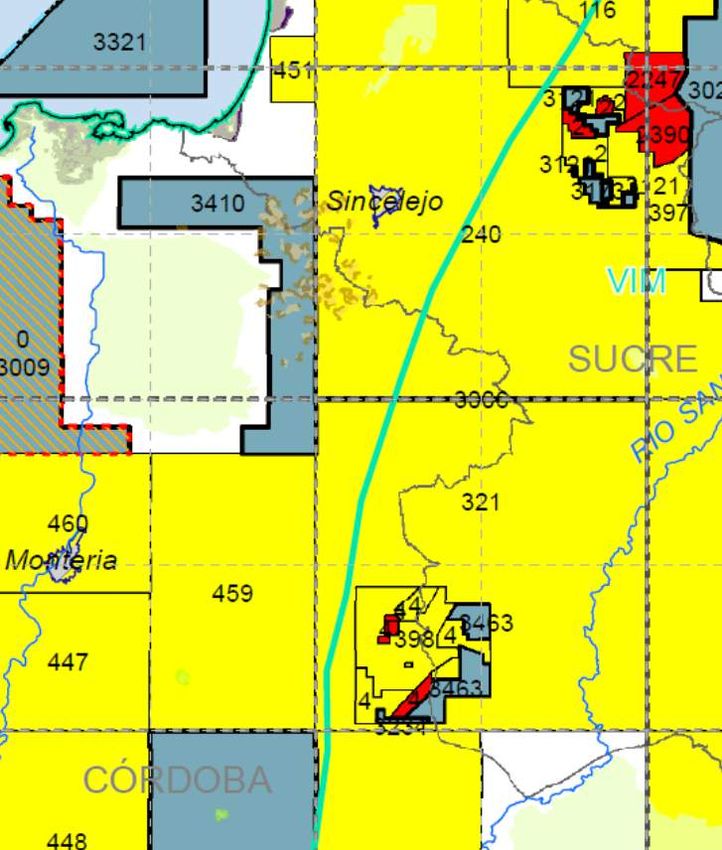

15ASSET OVERVIEW

COLOMBIA PROFILE

Overview Asset Locations

■ PentaNova owns working interests and is the operator of

one development and two exploratory blocks in Northern

Colombia

1

Maria Conchita (24,312 hectares)

Ø Drill ready development block

3

Ø Located next to Chuchupa, Colombia’s largest gas

field with +900 MMboe in reserves accounting for 1

40% of Colombia’s natural gas output

2

2

Sinu 9 (126,925 hectares)

Ø Low-risk exploration play with gas test

Ø Adjacent to Canacol’s Esperanza block, a major

producing asset

3

Tiburon (99,492 hectares)

Ø High impact exploration block

Ø In close proximity to recent multi-TCF discoveries,

Perla and Orca

16ASSET OVERVIEW

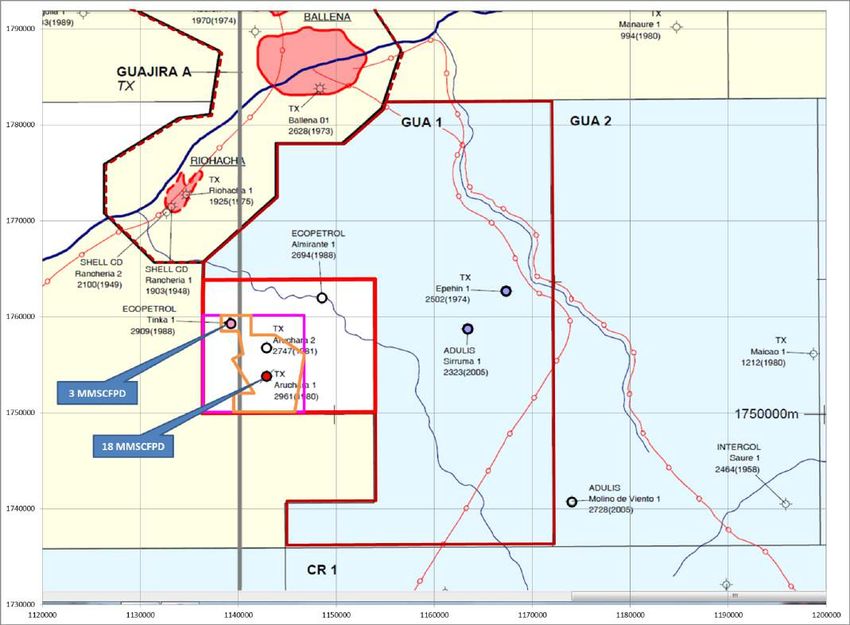

MARIA CONCHITA

Overview 2P Reserves (W.I.) 15.1 MMboe

Operational Highlights

■ Natural gas block (60,076 acres) in the 2P Reserves (W.I.)

Management Target Recovery 15.1 MMboe

44.6

Guajira basin with 3D seismic and a beneficial

Management

Current Target(100%

Production Recovery

) 44.6 MMboe

0 bopd

80% W.I. .

CurrentProduction

2018E Production(WI%

(100%

) ) 0 bopd

1,929 bopd

■ Drill ready with a 24 year production license .

8.0% Oil Royalties

2018E Production (WI% )

Royalty 6.4%1,929 bopd

Gas Royalties

.. 5.4% Overriding Royalties

■ Very attractive prospectivity, given adjacency 8.0% Oil Royalties

Royalty US$5.0M

6.4% Gas Drill & Case

Royalties

Well Cost

US$7.8 Total Capex

to the largest gas field in Colombia ..

5.4% Overriding Royalties

(Chuchupa) Well Cost End Date

Concession

US$5.0M Drill & Case

US$7.82041

Total Capex

..

■ Close proximity (+/- 20 km) to both gas trunk Concession End Date

Operator 2041 - 80.0% W.I.

PentaNova

..

lines Former partners of -

Operator

Partners BochicaPentaNova

Investment - 20.0%

80.0% W.I.

W.I.

. Holdings -

Former partners of -

Partners Bochica Investment 20.0% W.I.

Holdings -

17ASSET OVERVIEW

MARIA CONCHITA

Development Ready Block with 3D Seismic Close to Colombia’s Largest Gas Producing Field and its Infrastructure

Chuchupa

3D Maria

Conchita

Seismic

EIA permit area area

18ASSET OVERVIEW

SINU 9

Overview Operational Highlights

2P Reserves N/A

h .

■ Natural gas block in the Department of Cordoba

2P Reserves Target Recovery

Management 33.9 N/A

MMboe

with a beneficial 80% W.I. in low-risk exploratory h ..

gas block with “in-situ” gas accumulations Management

Current Target(100%

Production Recovery

) 33.9 MMboe

0 boepd

..

(313,638 acres)

Current

2018E Production(W.I.%

Production (100% ) ) 0 boepd

0 boepd

■ Additional upside in mapped structures on trend ..

with gas test 8.0% Oil Royalties

2018E Production (W.I.% ) 0 boepd

6.4% Gas Royalties

Royalty

. 12% x-factor

■ 18,000 acres of structural closure mapped with 4%8.0%

Overriding Royalties

Oil Royalties

.

6.4% Gas Royalties

2D seismic Royalty

12% x-factor

Well Cost $5.0MM

4% Overriding Royalties

■ Hydrocarbon potential on adjacent Canacol ..

Well Cost End Date

Concession $5.0MM

2041

Esperanza Block with 411 BCF of 2P reserves

..

■ Gas trunk lines close (+/- 20 km) to the block with Concession End Date 2041 - 80.0% W.I.

Operator PentaNova

spare capacity ..

Desarrolladora Oleum - 15.0% W.I.

■ Additional oil & gas upside from unconventional Operator

Partners

PentaNova

Clean Energy - 80.0% W.I.

. Resources - 5.0% W.I.

resource potential Desarrolladora Oleum - 15.0% W.I.

Clean Energy

Partners

Resources - 5.0% W.I.

19ASSET OVERVIEW

SINU 9

Exploration on trend with gas discovery, shoot 3D Seismic and drill, adjacent to Canacol gas block and 16 km to gas trunk line

Creciente Gas Field

Sinu 9 Gas

Exploration Block Hechizo-1 Gas Discovery

drilled in 1992

tested 10 MMscfpd

Gas Water Contacts?

Chuchupa

Maria

Conchita

Canacol Gas Block

Sinu 9 structure is over 20 km long with the Hechizo-1

Producing ≈ 80MMscfpd

20 gas discovery on the north endASSET OVERVIEW

TIBURON

Overview 2P Reserves Operational Highlights N/A

h .

■ High-impact exploratory gas block with 2D 2P Reserves

Additional Upside 161.5N/A

MMboe

h .

seismic coverage showing several leads with

Additional

Current Upside (100% )

Production 161.5 MMboe

0 boepd

closure and bright spot gas indicators .

(245,850 acres) with a beneficial 60% W.I. CurrentProduction

2018E Production(W.I.%

(100% )) 0 boepd

.

8.0% Oil Royalties

■ Located between three giant gas fields 2018E Production (W.I.% )

Royalty 0 boepd

6.4% Gas Royalties

. 6.0% Overriding Royalties

collectively holding 28+ TCF: Chuchupa, Perla 8.0% Oil Royalties

Royalty

Well Cost $5.5MM

6.4% Gas Royalties

6.0% Overriding Royalties

and Orca .

Well Cost End Date

Concession $5.5MM

2039

.

Concession End Date

Operator 2039

PentaNova - 60.0% W.I

.

Operator

Partners PentaNova

Colpan - 60.0%

Oil & Gas W.IW.I.

- 40.0%

.

Partners Colpan Oil & Gas - 40.0% W.I.

21ASSET OVERVIEW

ARGENTINA PROFILE

Overview1 Asset Locations

PentaNova has a portfolio of assets in Argentina

comprised of 125,415 gross acres

1

Llancanelo (23,697 acres)

Ø Discovered in 1937, operated by YPF

Ø Average production of 1,366 bopd in June 2017

2 1

KM8 (4,571 acres)

Ø Redevelopment of historic field with +38MMbbl

produced to date

Ø Current production of 88 boepd

3

Estancia La Mariposa (21,780 acres)

Ø Fully carried working interest in a stable producing 2

block that will generate ~US$1.0 – US$1.5 million in

3

free cash flow per annum

4

4

Sur Rio Deseado Este (75,367 acres)

Ø Heavy oil blocks on southern flank of San Jorge

basin

Ø Proven presence of heavy oil (+2.0 Bnbbl OOIP)

22ASSET OVERVIEW

LLANCANELO 2P Reserves (W.I.) 3.3 MMbbl

h .

Overview Management Operational

Target Recovery

2P Reserves (W.I.) (W.I.) Highlights

62.7 MMbbl

3.3 MMbbl

h .

■ Heavy oil exploration & development

Current Production

2P Reserves

Management (W.I.)

Target Recovery (W.I.) 1,736 bopd

3.3 MMbbl

62.7 MMbbl

concession (23,697 gross acres) h

.

Current Production

Management Target(W.I.)

Recovery (W.I.) 868 MMbbl

62.7

1,736

1,366 bopd

bopd

■ Current 39% working interest in this giant .

heavy oil field and will enter into a joint 2018E

CurrentProduction

Production(W.I.)

(W.I.) 1,442

1,736 bopd

868 bopd

683

.

venture with YPF, and hold an option to farm-

CurrentProduction

2018E Production(W.I.)

(W.I.) 868 bopd

1,442

15.45% bopd

Royalty

in to an additional 11% working interest Royalty

. [2.00%] GORR

.

■ Primary cold multilateral well development for 2018E Production (W.I.) 1,442 Royalty

15.45% bopd

Royalty

Well Cost . [2.00%] GORR

$4.1MM

low cost production growth .

15.45% Royalty

Royalty

■ Option for thermal enhanced recovery for Concession

Well Cost End Date [2.00%]

May 28,GORR

$4.1MM2036

.

incremental recovery PentaNova - 50.0% W.I

Well Cost End Date

Concession

Operator May

YPF (Operator $4.1MM

of 28, 2036 - 50.0% W.I.

Record)

■ Close access to underutilized infrastructure . Joint Operations Team

PentaNova - 50.0% W.I

Concession End Date May 28, 2036

(pipelines and refinery) Operator

.

YPF (Operator of Record) - 50.0% W.I.

Joint Operations Team

PentaNova - 50.0% W.I

■ Ability to triple area with proven oil resource Operator YPF (Operator of Record) - 50.0% W.I.

potential from rights in the Llancanelo “R” Joint Operations Team

surrounding acreage

23ASSET OVERVIEW

LLANCANELO

Application of Proven Heavy Oil Development Technology to Unlock the Potential of a Massive Oil Accumulation

Horizontal wells have been drilled and are on production proving the

economic viability of full field cold horizontal well development.

Llancanelo Block

Llancanleo R Block surrounds the Llancanelo Block

24ASSET OVERVIEW

KM8

2P Reserves (W.I.) N/A

h .

Overview Management Operational

Target Recovery

2P Reserves (W.I.) (W.I.) Highlights5.0 MMboe

N/A

h .

■ 100% W.I. in a shallow light oil development 2P Reserves

Current (W.I.)

Production

Management Target Recovery (W.I.) N/A

88 MMboe

5.0 boepd

h .

concession (4,571 acres) with a 100% W.I.

Management

Current Target(W.I.)

Production Recovery (W.I.) 46

88boepd

5.0 MMboe

boepd

■ Shallow, low cost workover and drilling to .

target light oil CurrentProduction

2018E Production(W.I.)

(W.I.) 88boepd

46

1,428boepd

boepd

.

■ Close proximity to operating center for the Current

Royalty Production(W.I.)

2018E Production (W.I.) 88 boepd

9%

1,428Royalty

boepd

.

basin ensures low cost

2018E

Well Production (W.I.)

Cost

Royalty 1,428 boepd

$1.1MM

9% Royalty

■ Additional production potential from the D-129 .

productive formation, which is undrilled to date Royalty

Concession

Well Cost End Date 9% Royalty

In Perpetuity

$1.1MM- No Expiry

.

on the block

Well Cost End Date

Operator

Concession $1.1MM

PentaNova - 100.0%

In Perpetuity W.I

- No Expiry

.

■ Concession exists in perpetuity and comes

Concession

Partners

Operator End Date In Perpetuity

PentaNova - No Expiry

- 100.0%

N/A W.I

with an environmental waiver for prior activity .

■ YPF has proven the ability to redevelop Operator

Partners PentaNovaN/A

- 100.0% W.I

.

shallower formations by drilling wells in 2015-

Partners N/A

2016 within meters of the edge of the block

25ASSET OVERVIEW

KM8

Shallow, Mature Field Reactivation with Additional Development in Formations Producing within Meters of the Block Edge

660

Wells

69

Wells

0

Wells

26ASSET OVERVIEW

SUR RIO DESEADO ESTE

2P Reserves N/A

Overview Operational Highlights

h .

■ Heavy oil asset on the southern flank of the San 2P Reserves

Additional Upside 125.0N/A

MMbbl

h .

Jorge basin with a 54.1% W.I. in Sur Rio Deseado

Additional

Current Upside (100% )

Production 125.0 MMbbl

30 bopd

Este production area and 7.92% W.I. in Sur Rio .

Deseado Este exploration area (75,367 acres) Current Production (100%

(W.I.% ) 30

14 bopd

.

■ Multi billion barrel low sulfur (< 0.5%) heavy oil 12% Royalty

Current Production (W.I.% )

Royalty 14 bopd

[2.00%] GORR

trend on southern flank of San Jorge Basin .

12% Royalty

■ Area has enormous heavy oil potential, every well Royalty

Well Cost $0.6MM

[2.00%] GORR (1)

.

drilled on the block has encountered heavy oil

Well Cost End Date

Concession $0.6MM

March 27, 2021

■ Natural gas available on the block to support .

thermal oil production Concession

Operator End Date/ Expl.)

(Production March

PentaNova 27, 2021

- 58.1% / 52.4% W.I

.

■ Option on open acreage (>1 MM acres) on trend Pluspetrol

Operator

SRDE (Production

Production / Expl.)

Partners PentaNova - 58.1%-/ 52.4%

16.9% W.I

W.I.

San Enrique Petrolera - 24.9% W.I.

under negotiation with the Province of Santa Cruz .

Production Partners Pluspetrol - 44.0%

16.9% W.I.

SRDE Exploration Partners

San Enrique Petrolera - 24.9% W.I.

3.6% W.I.

.

Pluspetrol - 44.0% W.I.

SRDE Exploration Partners

San Enrique Petrolera - 3.6% W.I.

27ASSET OVERVIEW

SUR RIO DESEADO ESTE

Controlling the Southern Flank of the Basin with Heavy Oil Resources

Heavy Oil Province on the Southern

Flank of the San Jorge Basin

• Very large heavy oil accumulation

• Low sulfur heavy oil, less than

0.5%

• Up-hole gas present for thermal

recovery of gas development

140 MILES (≈ 220 KM) • Drilled and testing oil and gas in

the early ’90s

• Infrastructure in place, allowing

oil to be loaded on the water for

Bridas’s Basin Edge Drilling

Program, 1991-1993 sale, gas trunk line goes through

block

SDR: 1,000,000 acres SDRE R: 250,000 acres SDRE: 76,000 acres

28

28Introduction

Industry Overview

Asset Overview

Appendix

29APPENDIX

KM8

Production Type Curves

Concession End Date In Perpetuity - No Expiry ■ IP rate of 157 bopd with a 11.5% monthly decline and

IP Rate (bopd) 157 B=0.6385 and cumulative production of 94,000 bbl

EUR per well (Mbbl) 61

Hydro-carbon Mix 100% Liquids (28-31° API)

Operating Costs Other

Lifting Cost $6.79/bbl Discovery date 1914

Other Opex $2.35/bbl # of wells drilled 729

# of wells on current prod. 11

Capital Expenditures 9% Concession Licence

Royalty rates

Terms

Total Cost Per Well $1.1MM

# Days / Well 30

Well Spacing Variable

# of New Wells to Develop Est.

51

Recoverable Reserves

30APPENDIX

MARIA CONCHITA

Production Infrastructure

Concession End Date 2041 ■ Assumes $11MM to be spent on pipelines and facilities in

2018

IP Rate (Mcfpd) Mid-Miocene 6,500

EUR per well (MMcf) 24.9

Hydro-carbon Mix 100% Gas

Operating Costs Type Curves

Fixed opex of $500,000 plus Mid-Miocene

Lifting Cost

$360,000/well/year Initial Rate (Mcfpd) Decline

Other Opex $0.28/Mcf Aruchara M. Miocene 6,500 0.50%

Offset #1 6,500 0.50%

Capital Expenditures Offset #2 6,500 0.50%

OffSet #3 6,500 0.50%

$5.0MM Drill & Case

Total Cost Per Well Total Production 26,000

$7.8MM Total Capex

# Days / Well 50

Well Spacing 250 acres

Upper Miocene

# of New Wells to Develop 2P 3

Initial Rate (Mcfpd) Decline

Aruchara M. Miocene 4,000 0.50%

Other Offset #2 4,000 0.50%

Offset #3 4,000 0.50%

# of wells drilled 2

# of wells on current prod. 0

8.0% Oil Royalties

Royalty rates 6.4% Gas Royalties

5.4% Overriding Royalties

31INVESTOR RELATIONS

PentaNova Energy Corp.

Phone +1 604 609 6110

HEAD OFFICE

ADDRESS

Suite 3123 – 595 Burrard Street

Vancouver, BC V7X 1J1, Canada

PHONE

+1 604 609 6110

EMAIL

investorrelations@pentanovaenergy.com

32You can also read