Space Launch Market Analysis - HIE- Due Diligence Support February 2021 www.spacetec.partners - Highlands and Islands ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Space Launch Market Analysis

HIE- Due Diligence Support

February 2021

www.spacetec.partners

CONFIDENTIAL

HIE commissioned a market analysis to identify the UK's global positioning

and opportunities in the space launch sector

§ The UK aims to increase its share of the global space economy to 10% by 2030 and has embraced an ambitions

commercial spaceflight initiative

§ In this context, Highlands and Islands Enterprise (HIE) has commissioned RSM UK Consulting and its subcontractor

SpaceTec Partners (STP) to conduct an independent assessment of the current near Space launch market opportunities

§ STP is an independent management consulting firm specialised in the space sector and its application domains, with a

track record of contracts with both institutional and commercial stakeholders across Europe and abroad

§ STP has conducted an extensive market analysis of the space launch sector, which has shown that opportunities exist

for the UK to be at the forefront of the global and European small satellite launch market

– The UK is likely to launch a small orbital launcher in Europe by 2022-2025

– The total addressable market for small rockets (payload

STP is an independent management consulting firm specialised in the

space sector and its application domains

100% independent, Offices in Munich and Brussels,

privately owned hubs in London and Vienna

SpaceTec’s Sweetspot - “Where space meets business”

Market_Analysis_Executive_Summary 2

The performed market analysis followed a five-step approach

The analysis provides a comprehensive overview of the market for small commercial and

institutional satellites, as well as rockets used for launching them, thus identifying the UK Total

Addressable Market (TAM) and competitive positioning on a global scale

Small Satellites Market

and Launches

Demand Analysis

Global space sector UK Target UK Competitive

overview and key Addressable Positioning

trends Market and SWOT

Launch Vehicles and

Spaceports Market

Analysis (Competitive

Landscape)

Market_Analysis_Executive_Summary 3

SpaceTec satellite launch demand forecast scenarios, are based on a detailed bottom-up analysis with focus on small sats (

While the space economy is driven by the downstream revenues, the

upstream segment, including launch services, is the backbone of the sector

Global Space Market Revenues 2018 ($ Billion) and CAGR (%)

UPSTREAM MIDSTREAM DOWNSTREAM

Ground

Launch Segment Satellite User Support

Space System Satellite Satellite Data

Operations and (Equipment, service equipment activities

Manufacturing Operations Sales

Services Test and provisioning manufacturing (e.g. insurance)

Services)

Revenues $20.8B $6.4B $4.6B $14B $276B

Past 10y

4.4% 1.2% 6.0% 1.0% 11.0%

CAGR

Next 10y

3.0% 2.0% 3.0% 6.0% 5.0%

CAGR

Source: Euroconsult Report 2019, SpaceTec Partners Analysis

Market_Analysis_Executive_Summary 5

The launch industry is considered by investors as being high risk

Market failure/additionality – previous research

Source: SpaceTec Partners- European Commission/ European Investment Bank report:

“The Future of the European Space Sector”, 2019

Market_Analysis_Executive_Summary 6

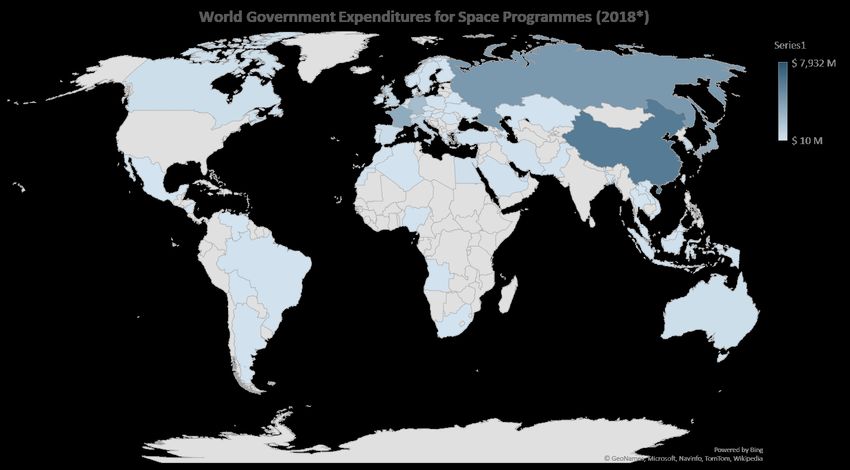

The space sector relies on large institutional investments

World Government Expenditures for Space Programmes (2018*) • Public investments represent the

cornerstone of the funding in space

activities, consisting of ca. $71 B in 2018*,

and growing at 3% CAGR as compared to $52

B in 2008

• Government space activities include military

applications for imagery and

communications and civil activities including

weather forecasting, science, and human

exploration

• In addition, governments, particularly those

of the United States and Europe, also

procure commercial space services,

especially launch, satellite imagery and

Legend:

communications, to meet mission

$ 40,996 M

requirements

• Governments also seek to stimulate

economic growth through space activities.

• Around 90 nations have government space

budgets, at least 9 of them over $1 B, and

nearly 20 close to $100 M

(*) according to Eurospace data, and $80-85B according to Bryce and Space Foundation

Only countries with budgets > USD 10 M are represented

Sources: Euroconsult, OECD, 2019, Bryce Space, SpaceTec analysis

Market_Analysis_Executive_Summary 7

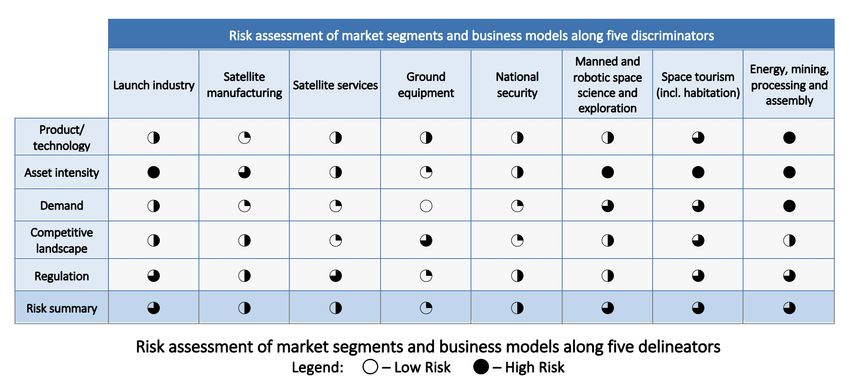

NewSpace is gradually evolving into new commercial fields beyond the

traditional space sector (e.g. constellations of small sats, smaller rockets)…

Traditional Space New Space

Institutional Commercial New Business Services

Space Space with Commercialisation Potential

LEO/MEO/GEO Services: IoT,

GNSS GeoInformation,

Launcher Media and

Data and Services

Internet for All Debris Mitigation

& Removal

Components

Military MSS/ FSS SmallSat

and Subsystems

Space Activities COM Satellites Systems

for SmallSats

On Orbit

Servicing (OOS)

Space Science LEO COM Satellites

Manufacturing in

SmallSat

Evolved PNT Microgravity Energy from Space

Constellations

and Space

Traditional EO

Satellites New and smaller Space Resource

Launch Systems Mining

Human Space

Exploration Space Humans

ISS Servicing Space Tourism

Habitats to Mars

Established Emerging

Source: SpaceTec Partners Analysis

Market_Analysis_Executive_Summary 8

… and new business models not only thriving on technological advancement,

but also on shorter cycles, and bold trade-off of risk, cost, and time to market

National Security

Space Situational Awareness -

Primary B2B Debris Mitigation and Removal

Business Models Short implementation

Satellite LEO Com Satellites

Manufacturing Satellite timespan

MSS/FSS Com Satellites Services

Components and Subsystems for SmallSats

Satellite Servicing

SmallSat Systems

Manufacturing in

SmallSat Constellations (e.g. EO)

Microgravity and Space

Geoinformation, Data and Services

New Launch Systems

Energy from Space Positioning, Navigation and Timing

LEO/MEO/GEO Ground

Space Resource Mining Launcher IoT, Media and Internet for All Equipment

Launch

Energy, Mining, Industry

Processing and Space Tourism

Assembly Space Habitats

Humans to Mars Space Tourism (incl.

Habitation) Primary B2C

Manned and robotic

Long Space Science and Business Models

implementation Exploration

timespan

Market_Analysis_Executive_Summary 9As satellites become cheaper and smaller, more and more satellites have been

launched in recent years, leading to ca. 3000 operational satellites in 2020

Operational satellites in orbit from 2009 to August 2020 Split of the operational satellites by

mass category

3000

Large satellites

2500 Small 2787 (> 500 kg)

satellites operational 39%

(≤ 500 satellites in

kg) August 2020

9.9% 61%

Operational satellites

2000

1500

2787

Split of the operational satellites by customer

type (as % of total in each category)

1000 2218 1700 1087 Total

1886

100%

1738

1419

80%

1305

1235

1071

60%

986

500 Military

40% Civil institutional

20% Commercial

0 0%

2009 … 2013 2014 2015 2016 2017 2018 2019 2020 Small satellites Large satellites

(≤ 500 kg) (> 500 kg)

Source: UCS, SpaceTec Partners Analysis

Market_Analysis_Executive_Summary 10Over time, 95 countries have grown satellite capabilities, but few currently

have launch capacity. Gaining access to space capability will position UK

among leading space fairing countries

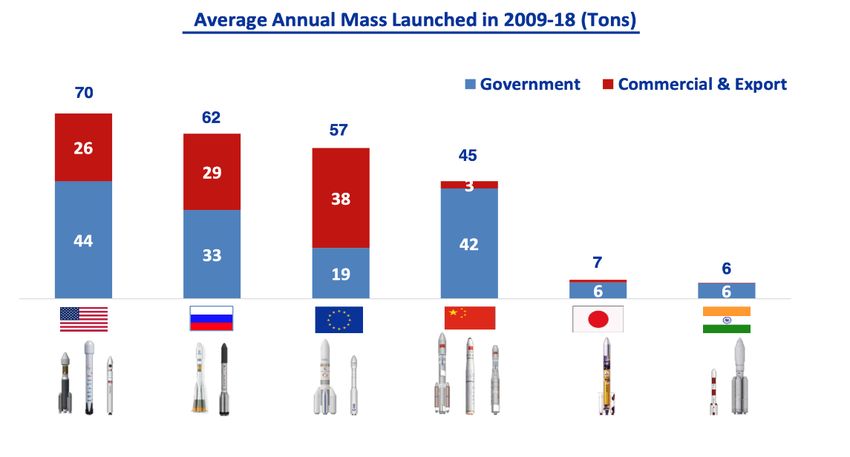

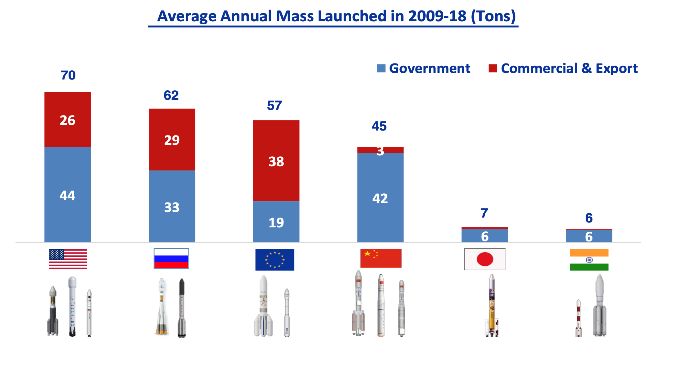

Number of countries operating and launching satellites Key insights

90 95 • Out of 195 worldwide, 95 countries operate satellites

• 6 countries launched more than 95% of the total

80 mass of satellites in 2009-2018. USA, Russia, EU and

China are the most active countries in the launch

70 sector

• Most countries rely on these 6 actors to deploy both

Countries operating their commercial and institutional satellites

60

Number of countries

satellites • Gaining access to space capability as a strategic

50 impact

Countries launching Average Annual Mass Launched in 2009-2018

40 most of the satellites (Tonnes)

70 Commercial &

Widening gap: export

26 Government

30 Opportunity to 50 29

address RoW 3

38

20 demand 30

44 42

33

10 10 19 1 0

6 6 6

0 -10 USA Russia Europe China Japan India

1950 1960 1970 1980 1990 2000 2010 2020

Countries most active in the

satellite launch industry

Source: Avio, SpaceTec Analysis

Market_Analysis_Executive_Summary 11Several micro-lift rockets are emerging to offer flexible launch capabilities to

global commercial smallsat constellation operators

Rocket classification by payload capacity to LEO

Heavy-lift Medium-lift Light-lift Micro-lift

Emerging market, with

around 100 projects

under development

Payload to LEO Payload to LEO Payload to LEO Payload to LEO

> 10,000 kg 4,000 – 10,000 kg 500 – 4,000 kgCa. 100 projects globally announced to be developing a launcher to

address the SmallSat launch demand, >80% micro- and mainly vertical

Breakdown of the Breakdown of the projects by

projects by country maximum payload capacity to LEO

100% Australia Breakdown of the

South Light-lift

Light-lift micro-launchers under

America (1501-4000 kg)

(501-1500 kg) development by launch type

Europe

Other

75% Other Asian 2%

Sea

countries

5%

Micro-lift Balloon

China 7%

(100-500 kg)

50%

≤500 kg Plane

payload 9%

capacity

25% North

America Micro-lift Land

(< 100 kg) 77%

0%

Total= about 100 new projects developing light-lift

(501-4000 kg payload capacity) and micro-lift rockets (≤500 kg payload capacity)

Market_Analysis_Executive_Summary 13Among the existing/ planned small rockets, Orbex, followed by Isar, seem

at a more advanced development stage than their European counterparts

Projected competitiveness of European small satellites launchers

Based on public info to date and benchmark against relevant main international launchers

Heritage & reliability Technology readiness

Projected competitiveness

High

Agreements with spaceports Partnerships

Funding Launch cost

Medium

Low

Country

Max payload to

. 225 300 500 1250 1000 1200 200 1000 315 1000 600 400 300 200

LEO (kg)

Date of the first Late Late 2023-

2017 2018 2021 Q3 2021 Q1 2021 2022 2022 2023 2022* 2025 2024+

flight with payload 2022 2022* 2024*

t

ity

ce

ce

g

.

l se

e

vio

b

ra

e

ce

ly

Co

bi

ac

ur

La

ac

ro

ef

pa

pa

pa

iv

Or

pu

-A

sb

Sp

Sp

&

t

at

Fir

ky

LS

xS

os

ke

m

ug

in

o

el

ht

-S

ex

LD

-E

er

oc

a-

yI

m

i rg

AB

-R

yA

Li g

rb

-P

-H

rA

m

XL

-R

1A

ph

-V

1-

-O

an

or

Na

ga

sa

5

ra

Al

1

ou

on

RS

ct

e

rr

SL

ra

Ve

-I

ro

e

On

r-

zh

Fa

tr

Te

im

iu

y

m

sta

ec

Sk

er

ai

M

et

Pr

tru

El

Ku

ch

rth

ck

ec

un

Ro

No

Sp

La

Unsuccessful maiden e-

Avio is also developing

L/

One launch

On

launch in May 2020

VO

SpaceRider (0.8t) * Stated but unlikely

failure in 2020

EN

Market_Analysis_Executive_Summary 14Meanwhile, new spaceports are emerging worldwide to address the demand

of NewSpace players (e.g. small satellites operators and launchers)

Global spaceport operating or planning to launch commercial satellites Mass launched in 2009-2018 Mass launched in 2009-2018

70 t

Spaceports supporting mainly large launchers only

40 t

Spaceports supporting small rockets

10 t Spaceports to launch small rockets by 2025

Other announced spaceports for small rockets

Zoom on the spaceport landscape in Europe

Andøya Launch Centre

Spaceport Sweden

Esrange Space Center

Shetland Space Centre

Space Hub Sutherland

Spaceport 1

• The most active spaceports are in the US, Europe (French Prestwick Airport German Sea Platform

Guiana), Russia and China. Machrihanish Air Base

• New spaceports for small rocket launches are emerging all over Snowdonia Spaceport

the world, and especially in Europe Spaceport Cornwall

• 7 sites in the UK alone are applying for launch licences, and plan

to cover most types of space launch (vertical and horizontal S3 Croatia

launch) Azores Satellite

Launch Base

• Andøya, Esrange spaceports and a few UK spaceports (TBD) are

expected to start operating small rockets by 2025, with the

Guiana Space Taranto-Grottaglie

Nordics and 3 UK spaceports ahead of the race Centre (Kourou) Airport

El Arenosillo Launch Base

Source: SpaceTec Analysis El Hierro Launch Centre

Market_Analysis_Executive_Summary 15Of the 8 benchmarks analysed, only 1 is fully owned by the private sector

Of the 8 benchmarks analysed, only

1 is fully owned by the private

sector, which is based outside of the

EU.

The other 7 spaceports are all fully

state-owned, with the exception of

Andoya Space Center (however, is

still 90% state-owned)

Source: SpaceTec Analysis

Market_Analysis_Executive_Summary 16Out of the emerging European spaceports the Nordic ones appear to be

ahead of the race, with potential to launch by 2022

Overall Launch Potential anchor Funding

Spaceport Country Target market Regulation Potential first flight

Readiness Type customer sources

2022 (feasible as

construction to start

Sounding Agreements with RFA; and Draft Bill by 2Q21;

Andøya in 2021, public

Norway High Vertical rockets / small potentially Nammo, but Mainly public launch under

Spaceport funding secured,

launchers not mature yet existing reg. risky

additional private

TBD)

N/A.

No customer confirmed

but identifies almost all

European operators as New reg. Delayed; 2022 (feasible as

Sounding

Esrange Space potential customers. might launch under funding secured and

Sweden Medium/ High Vertical rockets / small Public

Centre Interest in US operators existing reg. But planning ready to

launchers

but no TSA yet. unclear how start)

Signed contracts for

engine and stage testing

with ISAR and RFA

Ongoing concession bid >2023 (date hard to

expected to conclude by Public so far, predict until

Azores Sounding Primary legislation in

2020 but no update expected to be concession is

Satellite Portugal Medium Vertical rockets / small place but details to

available. Several Mixed after bid granted and

Launch Base launchers be finalised

European launch concession regulatory hurdles

operators involved. are solved)

Sounding

PLD Space and Deimos

El Arenosillo rockets /

Spain Low Vertical active but none with firm Public No info available >2023/24 (guessed)

Launch Base micro-

plans for domestic launch

launchers

Market_Analysis_Executive_Summary 17Several spaceports with different characteristics are emerging in the UK,

with SHS, Shetland and Cornwall in a more advanced stage than others

Type of orbital launch facility SHS SHETL CORNW SP1 PREST MACC Preliminary

Vertical Horizontal

500 kg payload to LEO

200 kg payload to

Orbital launch LEO

1st launch in

1st launch 1st launch 1st launch in 1st launch 1st launch

4Q 2023 or

in 2022 in Q1 2022 3Q 2022 in 2023 in >2024

2024

Up to 130 km

high

Up to 10 km

Suborbital launch high

1st launch 1st launch 1st launch 1st launch

in 2021 in 2021 in 2021 in 2021

TBC

Range control as a service

Engine and propulsion testing

Aerospace hub / cluster

Market_Analysis_Executive_Summary 18To assess the Total Addressable Market (TAM) for satellite launches from

the UK a step-by-step filtering approach has been applied

Filter by operator Filter by orbit Filter by need*

Satellites of Spaceports in the Of the smaller

countries with UK are ideal for satellites, about

closed domestic targeting polar/SSO half need the

markets (e.g. China, orbits. At the same flexible and Total addressable

Global small

Russia), as well as time, satellites dedicated, but market for ≤500kg

satellite (≤500kg)

those belonging to heading for lower more expensive satellite launches

demand forecast in

shareholders with inclination orbits (0- launch services from UK with MLVs

2020-2031

own rockets 50deg) are likely to offered by micro- in 2020-2031

(Amazon/Blue be launched closer launchers. The rest

Origin, to the equator. will rely on

3 forecast scenarios Starlink/SpaceX) are ridesharing or 3 forecast scenarios

not expected to fly piggy-backing

on European/UK launch services.

rockets

Filter by mass

Most MLVs can Total addressable

mainly launch the market for satellite

* Interviews with space stakeholders and some news articles report that the majority of satellite operators (around 50-70%) smaller satellites launches from UK

would still currently prefer to launch on larger rocket than micro-launchers, mainly due to the lower launch costs, higher

reliability, and current lack of offer. With potential higher confidence built into the micro-launcher solutions, it is expected

(≤200 kg). Heavier with MLVs in 2020-

that by 2031 the share of micro-launchers on the total launch demand of small satellites will range between 30% and 70%, satellites will rely 2031

where 70% represents the case in which certain micro-launchers achieve launch prices comparable to those of larger rockets on bigger rockets

and build a robust launch track record. To address this wide variability of results, three forecasting scenarios have been e.g. light lift,

developed, i.e. scenarios where 30%, 50% and 70% of the satellite operators would opt for a micro-launcher over a larger

rocket launch by 2031 whenever there is the choice between the two services. Once again, the medium forecast scenario is

medium lift and 3 forecast scenarios

considered the most likely to take place. heavy lift rockets

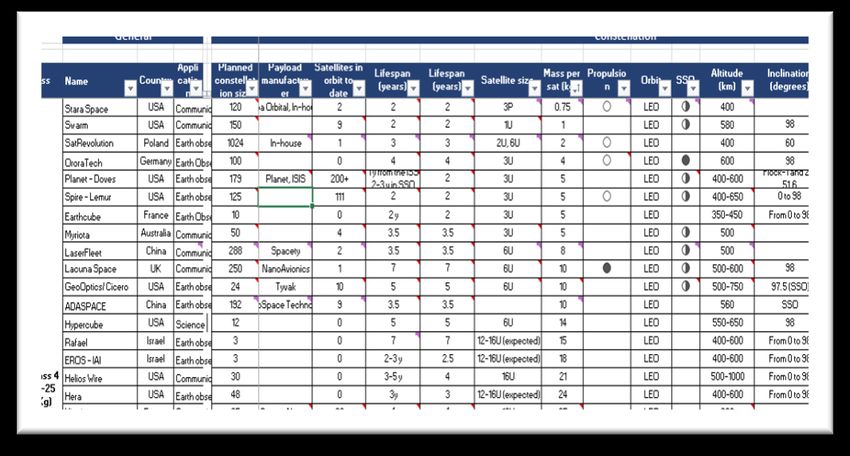

Market_Analysis_Executive_Summary 19Smallsat constellations are the icons of NewSpace, with ca. 150

commercial constellations announced so far, out of which 65 are relevant

ESA’s satellite classes

Other constellations

Class 4 Fleet Space Orbital Micro Systems Earthcube Raphael Astro Digital (Landmapper)

1-25 kg SatRevolution (REC) Sateliot Myriota EROS - IAI NASA Cubesat Initiative

Planet (Flock / Dove) Fleet Space LaserFleet ADASPACE Aistech (DANU, HYDRA)

OroraTech ZeroG Lab (Lingque, Magpie) Lacuna Space HyperCubes Astrocast

PlanetIQ Theia GeoOptics (CICERO) Kineis Kepler Communications

Class 3

26-60 kg

Class 2 Other constellations

61-200 kg Iceye Maxar (WorldView Legion) NorStar GSV-U Zhuhai Orbita (Zhuhai-1)

Xingyun Synspective (StriX) MicroCarb GSV-V Synspective (StriX)

Canon Boeing satellite Earth-i (Vivid-i) CAS100 DigitalGlobe

Class 1

201-500 kg Other constellations

XpressSAR Galaxy Space (Yinhe) UrTheCast Hongyan & Hongyun (CASC)

GW-A59 GW-2

Market_Analysis_Executive_Summary 20The estimated commercial small satellites Total Addressable Market (TAM)

for micro-launchers launched from the UK is ca. 95 metric tonnes in 2020-31

Forecasted cumulative number of commercial SmallSats addressable to Key figures on the UK’s TAM of

be launched from a UK spaceport in 2020-2031 (medium scenario) commercial SmallSats (≤ 500 kg)

25000

3082 SmallSats (95 t)

Cumulative number of satellites expected

Most of them below 200 kg

20000

(3077 satellites, total mass of 92 t)

to be launched in 2020-2031

Excluding mainly

Starlink and Chinese

Addressable by

constellations

light- to heavy-

15000 lift rockets 631 cumulative launches

(53 annual average)

Excluding

22244 non-polar Excluding satellites

10000 orbits flying on a ride-share

on a bigger rocket $3.8 B cumulative revenues

for micro-launchers

5000 95 t 92 t ($316 M annual average)

3082 3077

$320 M cumulative

0

launch service revenues for spaceports

ial ) le ot on r ble )

c a b s n K g a ble ) ($27 M annual average)

er kg s

s e t its U in e s g a

ss kg

m

m 00 dre ock orb the t fly unch dres 00k re 200

5 d r o a d 5 d

co ≤ a K to m n ll a (≤ d

l a et (≤

tal ts ( not n/U ats fro sats mal tal ket ta

To llSa ats ea S e

all abl all a s To ar To ark

a lS op m s m m m

Sm mal Eur S es

r

S

S by d

ad

Market_Analysis_Executive_Summary 21TAM scenarios reflecting variations in the success rate of completion and

replenishment of planned constellations

Forecasted cumulative number of launches addressable from a UK spaceport in 2020-2031

(Total commercial ≤ 500 kg satellites to polar orbit)

1500 1323

≤ 200 kg 200-500 kg Total 1220

1000

TAM Scenarios 613 631

500 345 355

103

10 18

0

Low Medium High

Several commercial constellations Some commercial constellations will

Most of the planned constellations

will not be completed or not be completed or replenished.

Scenario description will be completed and replenished

replenished. Most satellite launches Some satellite launches will deviate

according to plan

will deviate from planning. from planning.

TAM of number of UK Cumulative (2020-31) 355 631 1323

micro-launches (up to 500

kg) Average per year 30 53 101

$2.1 B $7.8 B

TAM for a micro-launcher Cumulative (2020-31) $3.8 B

launching from UK (above (-45% vs medium case) (+105% vs medium case)

in revenues)

Average per year $175 M $316 M $650 M

TAM launch services Cumulative (2020-31) $177 M $319 M $662 M

revenues for a UK

spaceport addressing Average per year $15 M $27 M $55 M

micro-launchers

Market_Analysis_Executive_Summary 22The TAM for institutional SmallSats (military and civil sats) that could be

launched by micro-launchers from UK amounts to 51t in 2020-2031

Forecasted cumulative number of military and civil institutional Key figures on the UK’s TAM of

satellites addressable to be launched from a UK spaceport in 2020-2031 institutional SmallSats (≤ 500 kg)

(medium scenario)

4000

732 SmallSats (51 t)

Cumulative number of satellites expected

3500 Most of them civil (45t civil, 6t military)

Excluding Chinese and Of these, 661 satellites (25t) with a

Russian satellites

mass of less than 200 kg

to be launched in 2020-2031

3000

Excluding

non-polar

2500 orbits 342 cumulative launches

In the medium conservative (28 annual average)

2000 scenario, 80% US institutional of which 170 for ≤200kg sats

satellites not expected to be

(14 annual average)

3397 launched from outside the US.

1500

$2 B cumulative revenues

for micro-launchers

1000 51 t

25 t ($170 M annual average)

UK Skynet and other of which £1 B for ≤200kg sats

500 sats addressable by

medium/high-lift 732 ($85 M annual average)

661

rockets

0 $171 M cumulative

t

ill te

s ble s s no K of

s

ite S ble ) le launch service revenues for spaceports,

e ssa

et it U es g ell U ssa

kg sab g) of which $85 M for the ones addressing

at re ck rb e lit t

k a m re 0 e 0k s

als a dd K ro to o m th atel 500 al s fro add (≤50 ddr ≤20 ≤200kg sats

tio

n

n ot n/U ats fro ge s ss > tion hed tal ket tal a et (

stit

u

a ts pea allS able Lar ma stitu unc To ar To ark

m

S m s a m

al in all Euro S res S in l

t m

S by d U

To ad

Market_Analysis_Executive_Summary 23TAM scenarios for institutional markets, differing levels of UK capability in

capturing US and the rest of the world demand

Forecasted cumulative number of launches addressable from a UK spaceport in 2020-2031

(Total institutional ≤ 500 kg satellites to polar orbit)

600

≤ 200 kg 200-500 kg Total

425

400 342

TAM Scenarios

172 211 213

200 169 170

86 83

0

Low Medium High

Including 20% of US market and rest Including 50% of US market and 50%

Including US market and rest of the

Military of the world (China and Russia rest of the world (China and Russia

world (China and Russia excluded)

Scenario definition excluded) * excluded)

TAM incl. 5% of US, 50% of RoW, TAM incl. only 20% of US and excl. Global TAM excluding Chinese and

Civil

excl. Chinese and Russian sats Chinese and Russian sats* Russian sats

TAM of number of UK Cumulative (2020-31) 169 342 425

micro-launches (up to 500 30 53 101

kg) Average per year

TAM for a micro-launcher $1 B $2.5 B

Cumulative (2020-31) $2.0 B

launching from UK (above (-50% vs medium case) (+25% vs medium case)

in revenues)

Average per year $84 M $170 M $208 M

TAM launch services Cumulative (2020-31) $84 M $171 M $212 M

revenues for a UK

spaceport addressing Average per year $7 M $14M $18 M

micro-launchers

(*): Considering that not all RoW countries have launch capabilities, they will look to launch from elsewhere. In regard to the US market in particular, considering the

privileged relationship between UK and US, We consider reasonable. Also see the interest of US launchers and emerging players to UK favourable ecosystem. Also note

that there are limited available info about military missions. So military market is likely under estimated.

Market_Analysis_Executive_Summary 24The estimated TAM for a UK spaceport results in 146t smallsat mass to be

25

launched to polar orbits, equivalent to over 970 launches of small rockets

Forecasted cumulative satellite metric tonnes addressable to be

launched from a UK spaceport in 2020-2031 Key figures on the UK’s TAM of small

(Bringing to a total TAM for micro-launches from the the UK between 50

and over 200 in 10 years (81 annual average in the medium scenario)

Projected number of micro-launches of commercial and institutional small satellites

that can be addressed by a UK spaceport Medium Scenario

250

Low

973 cumulative launches

Medium

200

High

$5.8 B cumulative revenues

150 for micro-launchers

Number of launches

(ca. $480 M annual average)

100

Ca. $490 M cumulative

launch service revenues for

spaceports

50 ($40 M annual average)

0

2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031

Source: SpaceTec Partners Analysis

Market_Analysis_Executive_Summary 26Interviews revealed the need for flexible and cost-effective launch

solutions, and the current lack of supply for such services

Rocket Lab is more expensive, but it We' re considering small rockets for their launch flexibility, e.g. if we have a big gap in

launches on time. Price is not the only launch cadence. However, at the moment micro-launchers don't really offer such

point we take into consideration. frequent launches and flexible scheduling. [...] Players like us would use micro-launchers

if they were really responsive, if you could sign a contract and throw within two weeks.

CEO of a NewSpace constellation

CEO of a NewSpace constellation

The price of small rockets is a big issue. We would

only use a micro-launcher if there is a customer I need an injection in the right orbit at a schedule that fits my business at a

who has time priority and is therefore willing to pay cost that I can afford. Not all rockets can inject your satellite batch in the right

the premium, and we would piggy-back. [...] We orbit. The envelope that wrap this all is reliability. A start-up cannot afford a

would like to launch in batches of 6-8 satellites. failure on the launch pad.

CEO of a NewSpace constellation CEO of a NewSpace constellation

When you launch a lot of satellites, everything is well Our plan is to launch all the constellation in nine months. It's possible

regulated. With large rockets, the issue of regulation that we cannot do this with just one company. […] We need rockets

becomes a nightmare. We plan to use dedicated launches. that can bring the satellites 5 by 5. […] We were interested to launch

the constellation for around €30 million in 5 launches.

CEO of a NewSpace constellation

Director of Innovation of a NewSpace constellation

Satellite operators and manufacturers Rocket manufacturers and spaceport operators

Surrey Satellite Technology Iceye Kepler Communications Fleet Rocket Factory Augsburg CNES

Interviewed ISIS Space Inmarsat Axelspace OneWeb Hyimpulse Andoya Space Centre

stakeholders Satellogic - Aleph Kleo Connect NorthStar Space Data Kinéis Ariane Group Southern Launch

Market_Analysis_Executive_Summary 27This analysis is rather conservative for different reasons

§ The commercial demand forecast is based on a selection of the currently announced small satellite

constellations (e.g. ca. 70 out of the 150 announced, including for example just one mega constellation

instead of 4 anticipated) and assumed likelihood of success/ delay (driving the low, medium and high

forecast), in any case not speculating on potential upcoming/ unknown new ones e.g. stimulated by

more and more affordable satellite manufacturing and launch costs

§ It focuses on small rockets (launchers with a maximum payload capacity lower than 500 kg) and not on

larger rockets who could address the ride-share part of the addressable market or lift heavier payloads

§ It does not consider the longer-term launch demand for hypersonic flights and/or space tourism

§ The analysis of the military demand is based on a projection of the of the existing “known”

international assets , thus does not include the launch of classified satellites

§ In regard to the UK captive institutional demand of launches the current analysis does not include a

detailed analysis of the UK government planning (e.g. associated to the 20th November 2020

government announcement of UK defence space budgets rise, or associated to the UK increased

investment in ESA)

Market_Analysis_Executive_Summary 28The importance of UK first mover advantage: geopolitical/ strategic vs

market opportunity

Geopolitical/ strategic Market

Performing a first launch from UK before In relation to the market opportunity:

other European countries (i.e. by 2022)

would: § Institutional market: 1st mover advantage is not

critical as the space base choice is driven by national

§ Provide independent access to space (a strategic level agreements (e.g. UK launching US government

asset in the space value chain) missions)

§ Demonstrate the UK’s capability within the space § Spaceports with committed anchor customers: 1st

sector and in doing so: mover advantage is not critical as the customers

– Elevate the UK’s positioning among other choice of spaceport is driven by strategic and business

traditional space fairing countries model drivers and the spaceport’s competitiveness/

viability is determined by the location, number of

– Demonstrate progress in achieving the UK launches secured and its income/cost model

Government’s stated strategy for the sector

– Attract media attention and therefore wider § Excluding the above, 1st mover advantage would be

awareness of UK launch (and wider space) sector critical to secure initial customers (new space

capabilities and potential investment launchers) not yet affiliated/ bonded with other

opportunities spaceports, who are ready to launch by 2022 (based

on our analysis this likely equates to only one or two)

Market_Analysis_Executive_Summary 29UK is well positioned to be at the forefront of the global small satellite

launch market

Strengths Weaknesses

• Ambitious targets and strategy to increase UK space sector market share by • UK is located on an Island, adding logistical challenges for firms based in

2030. UK became the f4th contributors to ESA after France, Germany and Italy continental Europe (nevertheless this is the case also for other emerging sites

• Solid national space capabilities especially in the small satellite sector and in in Europe)

NewSpace • Lack of EU funding for UK spaceports means that a spaceport is a riskier

• Positive VC environment dedicated to space (e.g. UK based Seraphim Capital) venture, as the burden is solely on a national level

• The UK can adapt its regulations to meet the clients needs quicker as it does • Uncertainty around future EU-UK space sector relationship due to Brexit

not require approval of 26 other countries.

• Only personal jurisdiction is applicable in the UK, lowering the barrier to enter

the market, simplifying the landscape

• The UK and US concluded the TSA to smoothen US participation in space

launches from the UK

Opportunities

UK SWOT Threats

• No EU spaceport consistently launches small satellites, this means UK/ • There is a risk of the EU implementing protectionary measures such as making

Scotland would benefit from the first-mover advantage EU companies must use EU sites

• As a third-party country, the UK is not subject to EU laws and regulations, • Several countries pushing for their own spaceports, meaning there is heavy

meaning that is an attractive option for companies who want to minimise red competition in the market

tape • If all UK spaceports are beat to the race of first to market by European

• Upside potential from an upcoming demand of UK national institutional spaceports, and the EU develops Europe wide regulations, many launch

missions (not specified in the present forecast to date) companies will not see a major benefit in re-registering in the UK

• Opportunity to be the preferred European continent country from American • Nevertheless, realistically (non-UK) new launch companies that would be

players (both institutional and commercial) thanks to the historical link ready to launch by 2022 would probably limit to maximum one or two

between UK and USA government

• Also opportunity to play a pivotal role among the Commonwealth states

Market_Analysis_Executive_Summary 30In order to capture a relevant market share of the TAM several actions should be undertaken § Establishment, as soon as possible, of a flexible regulatory framework to allow emerging launch service providers to obtain a UK license - this would help retain gained Launch Service Provider to keep launching from the UK instead of seeking licensing elsewhere (note recent intelligence advises that other European countries are behind UK on this); § Assuring a high level of political and strategic intent to create a national captive market (e.g. buying launching capacity to support academic and research satellite programmes, as well as institutional remote sensing and technology demonstration missions); § Ensuring supportive trade and security agreements with key partners (e.g. USA, key EU Member States, for example Germany and Italy, five allies, NATO partners for military capability); § Balancing technical and market risks across a diversified, yet complementary, project portfolio; § Securing agreements with anchor customers to deliver a robust order pipeline; § Creating a robust innovation eco-system to support the national space sector e.g. strengthen centres of excellence and cluster support, support R&D across the space sector value chain; and, § Attracting and incentivising foreign direct investment within different aspects of the UK sectors value chain § Market_Analysis_Executive_Summary 31

You can also read